Sample Category Title

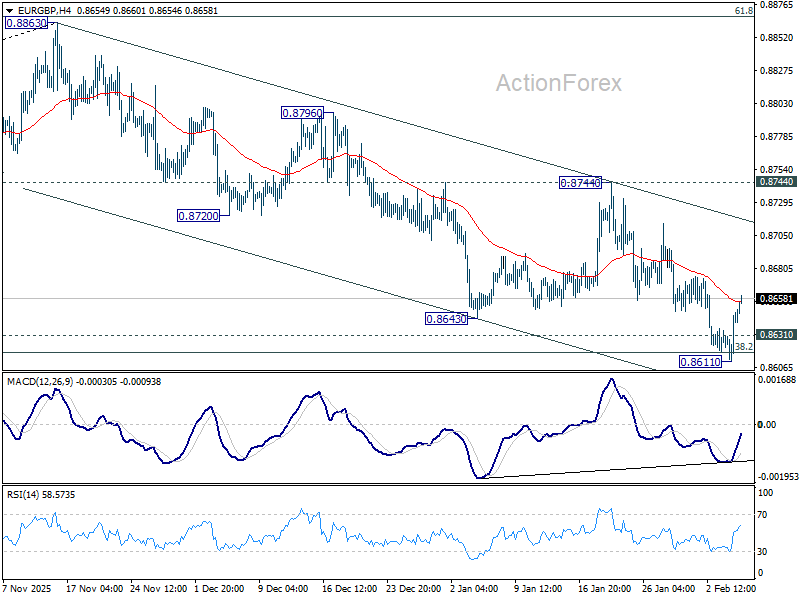

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8623; (P) 0.8636; (R1) 0.8660; More…

Intraday bias in EUR/GBP is turned neutral first with current recovery. On the downside, decisive break of 0.8631 cluster support (38.2% retracement of 0.8221 to 0.8663 at 0.8618) will carry larger bearish implications. Next target is 61.8% retracement at 0.8466. On the upside, however, break of 0.8744 resistance will suggest that fall from 0.8863 has completed as a corrective move.

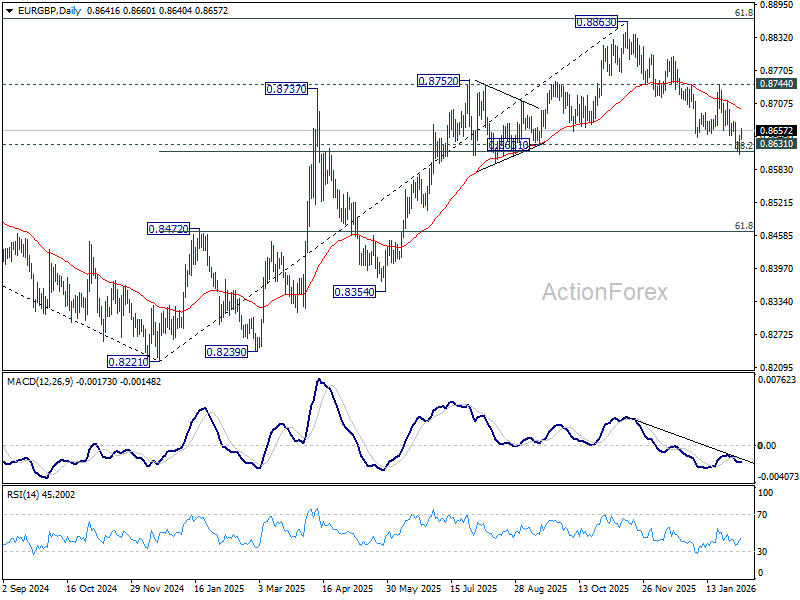

In the bigger picture, rise from 0.8221 medium term bottom (2024 low) is seen as a corrective move. Upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Sustained trading below 55 W EMA (now at 0.8625) should confirm that this corrective bounce has completed. In this case, deeper fall would be seen back to 0.8201/21 key support zone. However, decisive break of 0.8867 will suggest that EUR/GBP is already reversing whole decline from 0.9267 (2022 high). That should pave the way back to 0.9267.

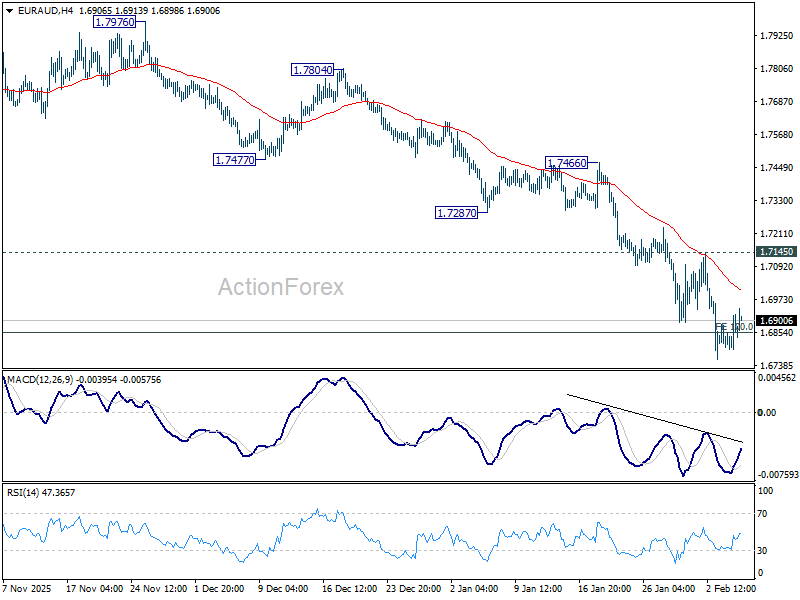

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6804; (P) 1.6863; (R1) 1.6928; More...

Further decline is expected in EUR/AUD as long as 1.7145 resistance holds. Sustained trading below 100% projection of 1.8554 to 1.7245 from 1.8160 at 1.6851 will pave the way to 138.2% projection at 1.6351 next. However, break of 1.7145 will confirm short term bottoming, and turn bias back to the upside for stronger rebound.

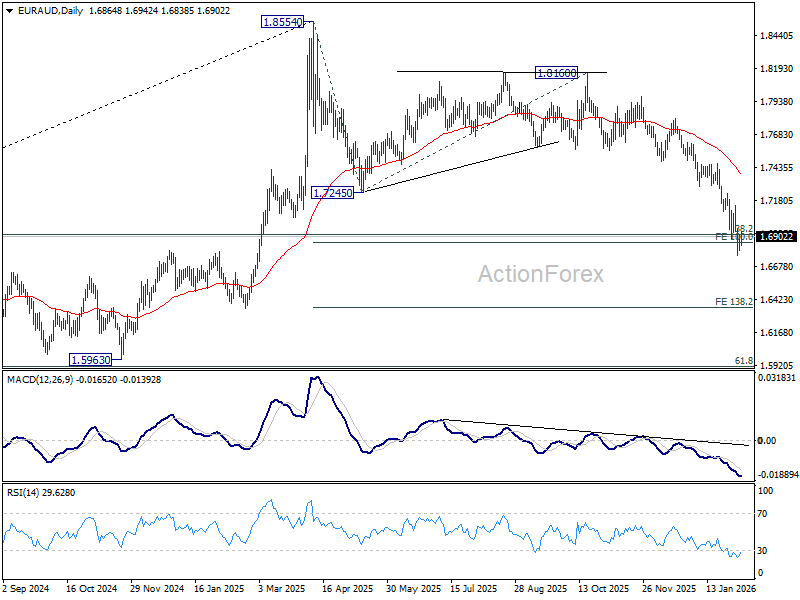

In the bigger picture, fall from 1.8554 medium term top is still in progress. Sustained break of 38.2% retracement of 1.4281 to 1.8554 at 1.6922 will argue that it's already reversing whole up trend from 1.4281 (2022 low). Deeper fall would be seen to 61.8% retracement at 1.5913. For now, risk will stay on the downside as long as 55 D EMA (now at 1.7396) holds even in case of strong rebound.

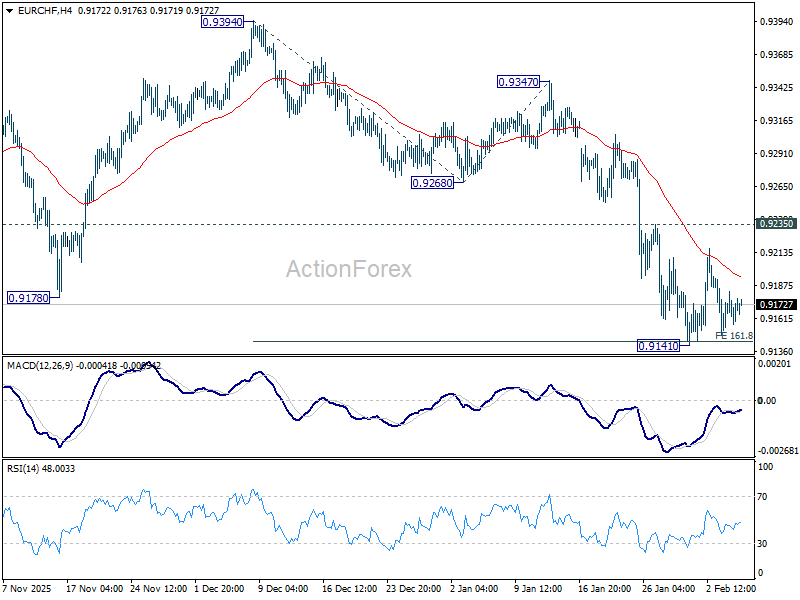

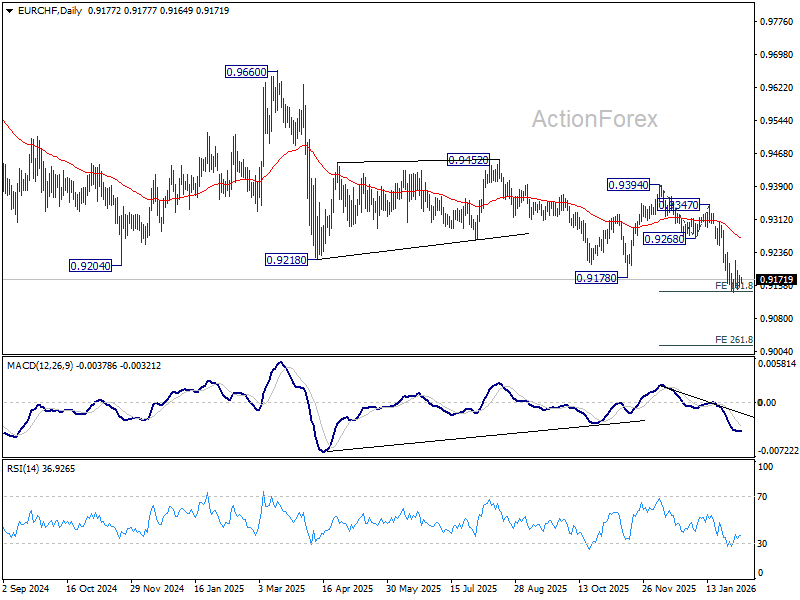

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9163; (P) 0.9173; (R1) 0.9189; More....

Intraday bias in EUR/CHF remains neutral for more consolidations above 0.9141. Upside should be limited by 0.9235 to bring another fall. Decisive break of 0.9141 will extend larger down trend to 261.8% projection of 0.9394 to 0.9268 from 0.9347 at 0.9143. However, firm break of 0.9235 resistance will suggest short term bottoming and bring stronger rebound to 55 D EMA (now at 0.9267).

In the bigger picture, another rejection by 55 W EMA (now at 0.9350) keeps outlook bearish. Downtrend from 1.2004 (2018 high) is still in progress. Firm break of 0.9178 will target 61.8% projection of 1.1149 to 0.9407 from 0.9928 0.8851. Outlook will stay bearish as long as 0.9394 resistance holds, in case of recovery.

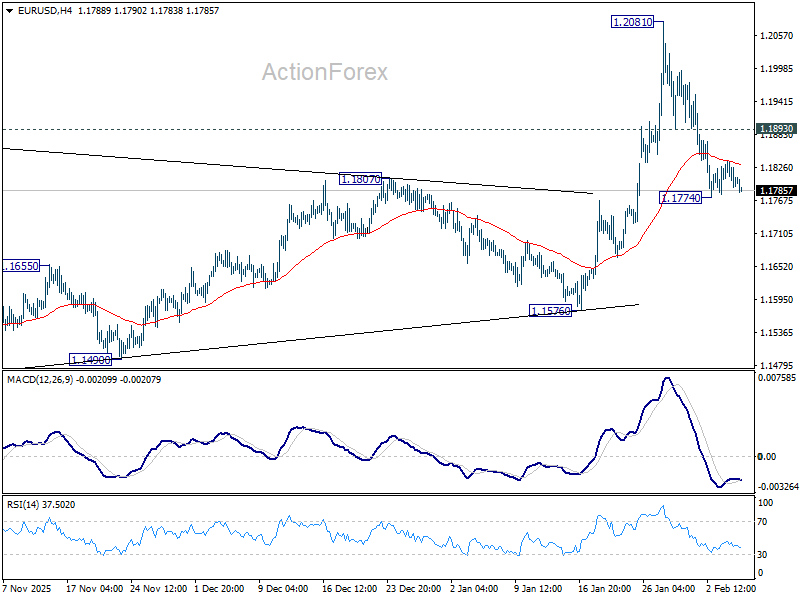

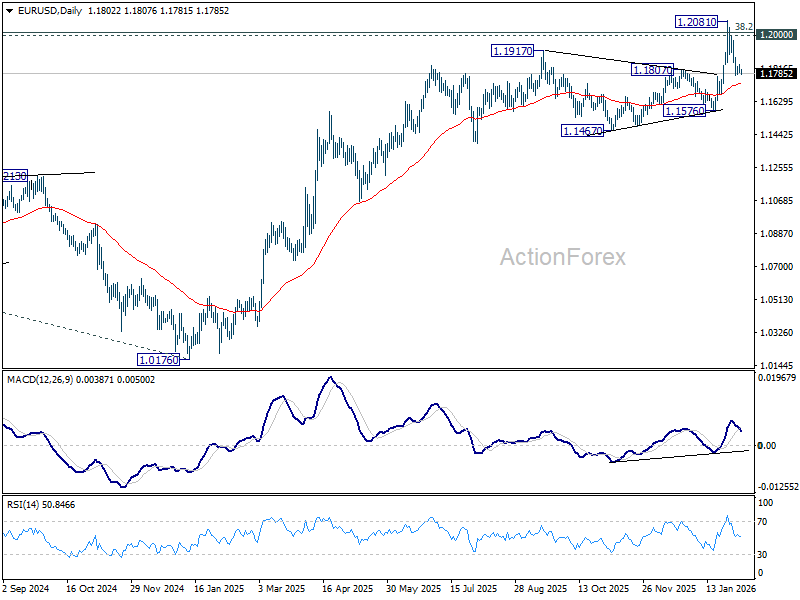

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1786; (P) 1.1812; (R1) 1.1833; More….

Intraday bias in EUR/USD remains neutral for the moment. On the downside, below 1.1774 will extend the fall from 1.2081 short term top to 55 D EMA (now at 1.1724). Firm break there will raise the chance of reversal on rejection by 1.2 psychological level, and target 1.1576 support. On the upside, above 1.1893 minor resistance will bring stronger rebound to retest 1.2081. Decisive break above 1.2 will carry larger bullish implications.

In the bigger picture, as long as 55 W EMA (now at 1.1458) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will add to the case of long term bullish trend reversal. Next medium term target will be 138.2% projection of 0.9534 to 1.1274 from 1.0176 at 1.2581. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

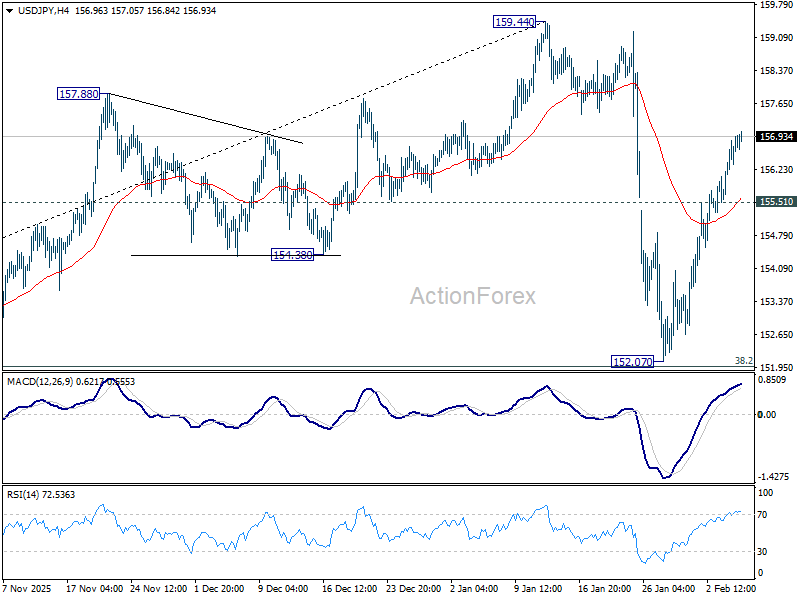

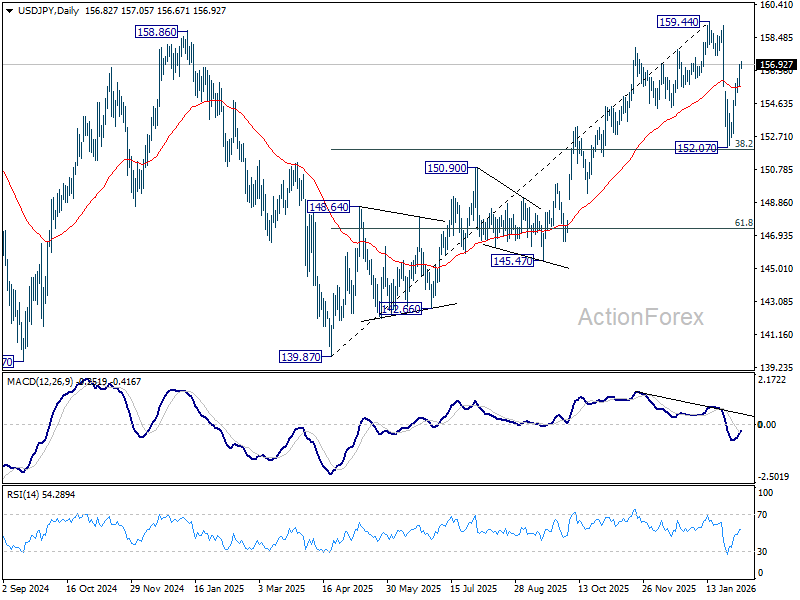

USD/JPY Daily Outlook

Daily Pivots: (S1) 156.03; (P) 156.49; (R1) 157.34; More...

Intraday bias in USD/JPY remains on the upside at this point. Rise from 152.07 is seen as the second leg of the corrective pattern from 159.44. Further rebound should be seen to retest 159.44 next. On the downside, below 155.51 minor support will turn intraday bias neutral first. But overall outlook will stay bullish as long as 38.2% retracement of 139.87 to 159.44 at 151.96, in case of another dip.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 151.59) holds. However, sustained break of 55 W EMA will argue that the pattern from 161.94 is extending with another falling leg.

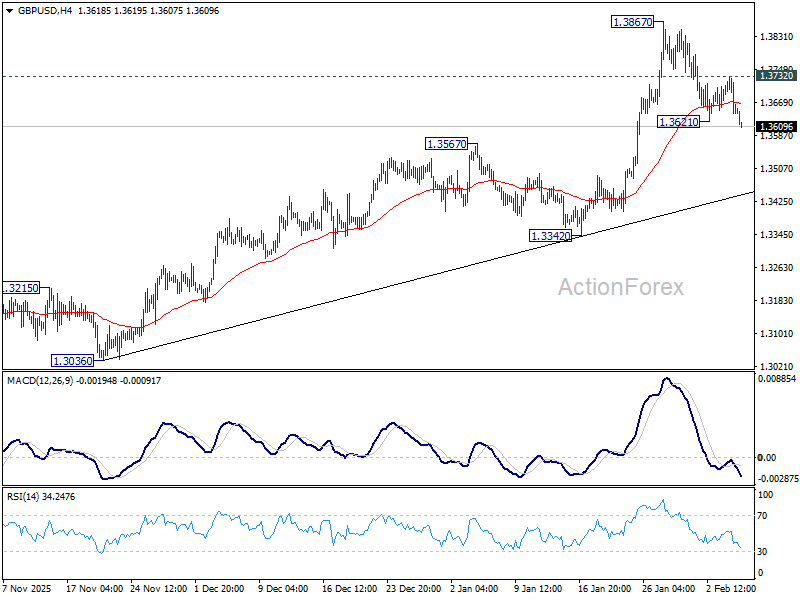

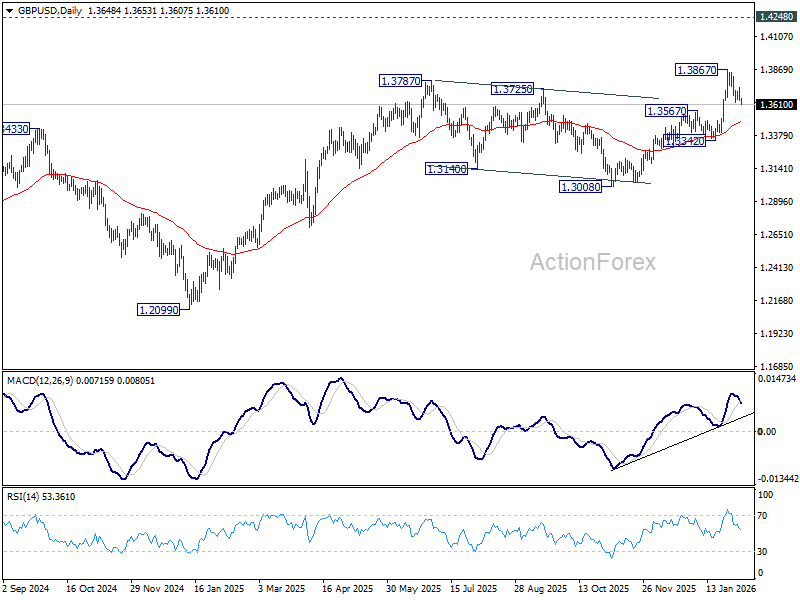

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3622; (P) 1.3677; (R1) 1.3712; More...

Intraday bias is back on the downside as pullback from 1.3867 short term top resumes. Deeper decline would be seen to 55 D EMA (now at 1.3482). On the upside, above 1.3732 minor resistance will bring retest of 1.3867. Firm break there will resume larger up trend towards 1.4284 key resistance.

In the bigger picture, rise from 1.0351 (2022 low) is resuming by breaking through 1.3787 high. Further rally should be seen to 1.4284 key resistance (2021 high). Decisive break there will add to the case of long term bullish trend reversal. For now, outlook will stay bullish as long as 1.3008 support holds, even in case of deep pullback.

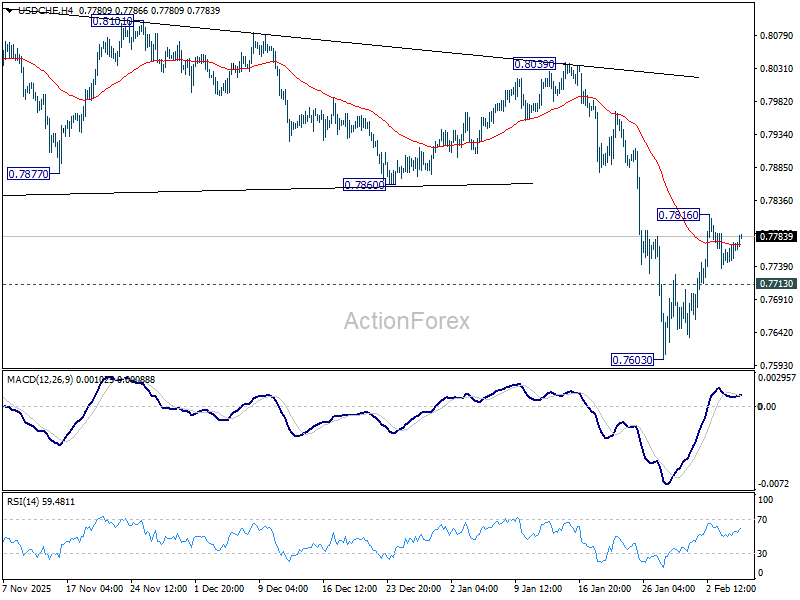

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7754; (P) 0.7765; (R1) 0.7785; More….

Intraday bias in USD/CHF remains neutral for the moment. On the upside, above 0.7816 will resume the rebound from 0.7603 short term bottom to 55 D EMA (now at 0.7905). On the downside, below 0.7713 minor support will bring retest of 0.7603. Firm break there will resume larger down trend to 0.7382 projection level next.

In the bigger picture, larger down trend from 1.0342 (2017 high) is still in progress and resuming. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8166) holds.

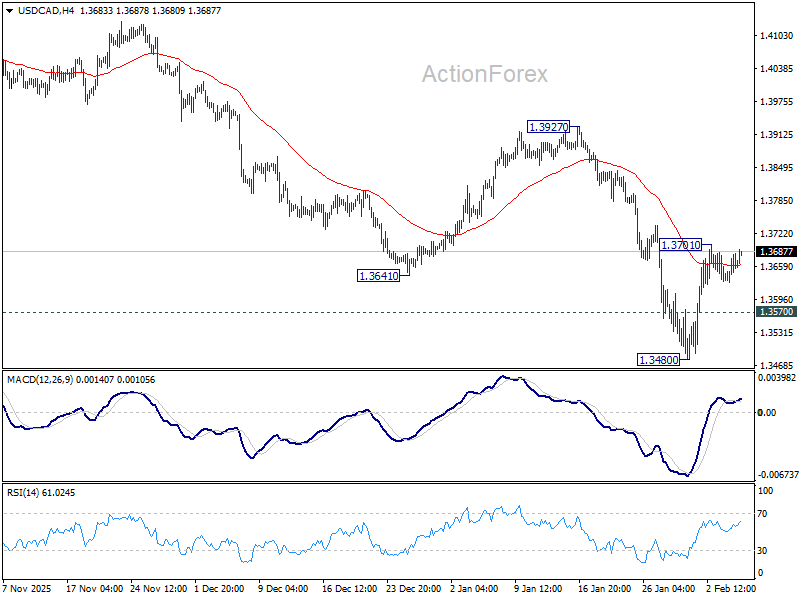

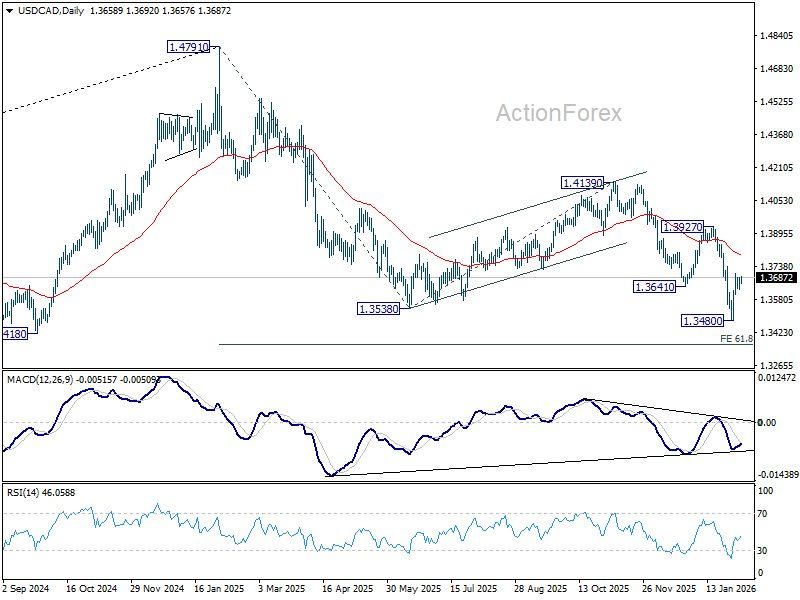

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3634; (P) 1.3659; (R1) 1.3689; More...

Intraday bias USD/CAD remains neutral at this point. On the upside, above 1.3701 will resume the rebound from 1.3480 short term bottom to 55 D EMA (now at 1.3793). On the downside, below 1.3570 minor support will bring retest of 1.3480 low. Firm break there will resume larger fall to 61.8% projection of 1.4791 to 1.3538 from 1.4139 at 1.3365.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen as the pattern extends, and break of 1.3538 will target 61.8% retracement of 1.2005 to 1.4791 at 1.3069. For now, medium term outlook will be neutral at best, until there are signs that the correction has completed, or that a bearish trend reversal is confirmed.

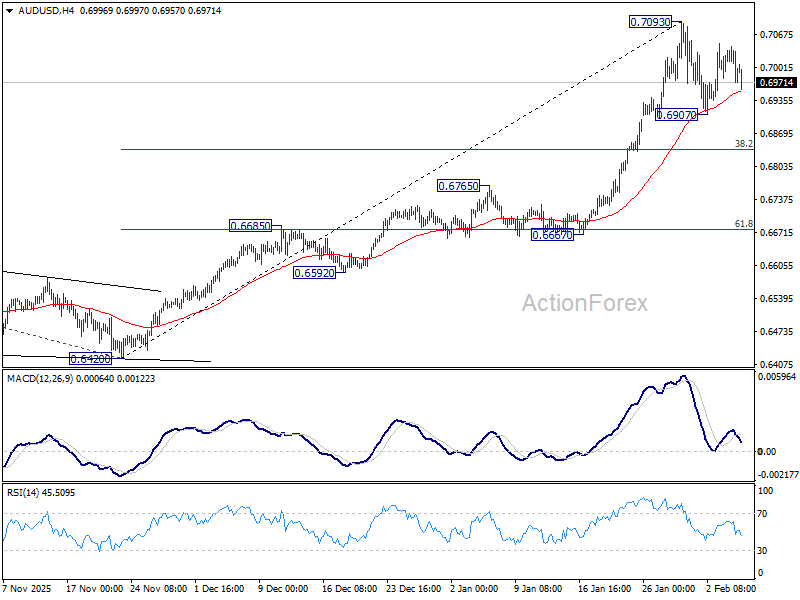

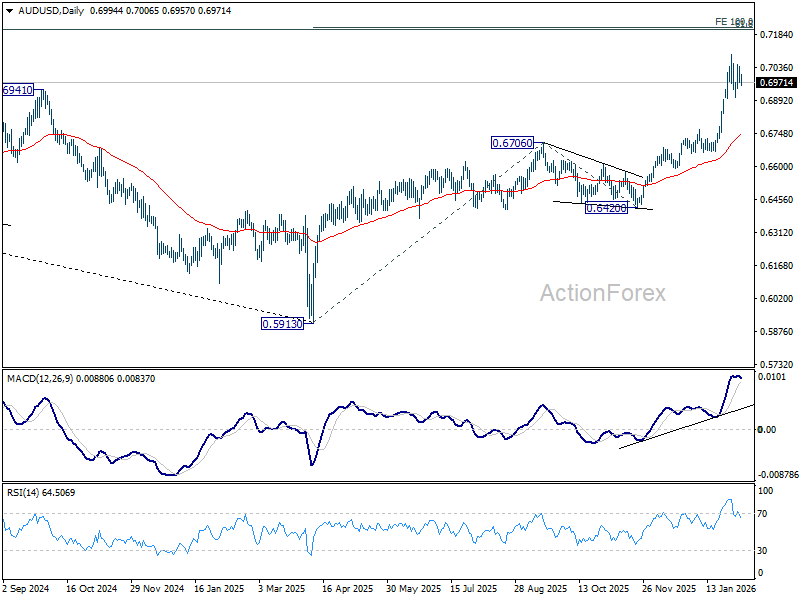

AUD/USD Daily Report

Daily Pivots: (S1) 0.6966; (P) 0.7004; (R1) 0.7037; More...

AUD/USD dips mildly today as range trading continues and intraday bias stays neutral. Further rise is still in favor. On the upside, break of 0.7093 will extend larger up trend to 100% projection of 0.5913 to 0.6706 from 0.6420 at 0.7213 next. However, break of 0.6907 will bring lengthier consolidations before rally resumption. Deeper pullback would then be seen to 38.2% retracement of 0.6420 to 0.7093 at 0.6836.

In the bigger picture, current development argues that rise from 0.5913 (2024 low) is reversing whole down trend from 0.8006 (2021 high). Further rally should be seen to 61.8% retracement of 0.8006 to 0.5913 at 0.7206. This will remain the favored case as long as 0.6706 resistance turned support holds, even in case of deep pullback.

Deepening AI Anxiety Hits Sentiment; ECB and BoE in Focus

Risk-off sentiment intensified in US tech sector overnight, with another down day in the NASDAQ. The move reflected growing unease rather than a single catalyst, as investors continue to reassess the implications of artificial intelligence for earnings, valuations, and capital discipline. That weakness carried into Asia, where Japanese and Korean equities saw steep declines.

So far, traditional and non-tech stocks have shown greater resilience. That divergence supports the narrative that markets are undergoing sector rotation rather than a full-blown risk-off episode. However, whether that insulation can hold if tech pressure persists remains an open question.

Several overlapping themes are driving the current reassessment. The first is growing concern that AI represents a competitive threat to software companies rather than a pure growth catalyst. Software firms long valued for sticky subscriptions and predictable renewals are now under scrutiny. Investors are questioning whether AI-driven automation could compress pricing, reduce switching costs, and lower barriers to entry for new competitors.

A second theme is the rapidly escalating cost of AI investment. Alphabet reported solid results, but its projected capital expenditure of USD 175–185 billion for this year came in well above expectations and rattled investors. The concern is not isolated. Alphabet and its Big Tech peers are expected to collectively spend more than USD 500 billion on AI this year. The scale of spending is forcing investors to question near-term returns. With monetization timelines uncertain, aggressive outlays are increasingly seen as a drag on free cash flow rather than a guarantee of future dominance.

A third pressure point came from the semiconductor space. AMD suffered its worst single-day decline since 2017 after delivering a lackluster forecast. Expectations had been high for a stronger outlook driven by AI demand and data center expansion. The reaction highlighted that even the chip subsector is not immune to broader market sensitivity. AI exposure alone is no longer sufficient to insulate companies from disappointment if guidance falls short.

In FX markets, the shift in sentiment has favored defensive currencies. Both Dollar and Yen found support in Asian session, while Aussie and kiwi softened. Euro and Sterling were mixed as markets awaited policy decisions from the ECB and the BOE.

Despite the daily moves, weekly performance still shows a different ranking. Aussie remains the strongest currency so far this week, followed by Dollar and Sterling. Yen continues to lag at the bottom, trailed by Swiss Franc and Kiwi, while Euro and Loonie sit in the middle.

In Asia, at the time of writing, Nikkei is down -0.86%. Hong Kong HSI is down -0.95%. China Shanghai SSE is down -0.83%. Singapore Strait Times is down -0.27%. Japan 10-year JGB yield is down -0.012 at 2.239. Overnight, DOW rose 0.53%. S&P 500 fell -0.51%. NASDAQ fell -1.51%. 10-year yield rose 0.001 to 2.750.

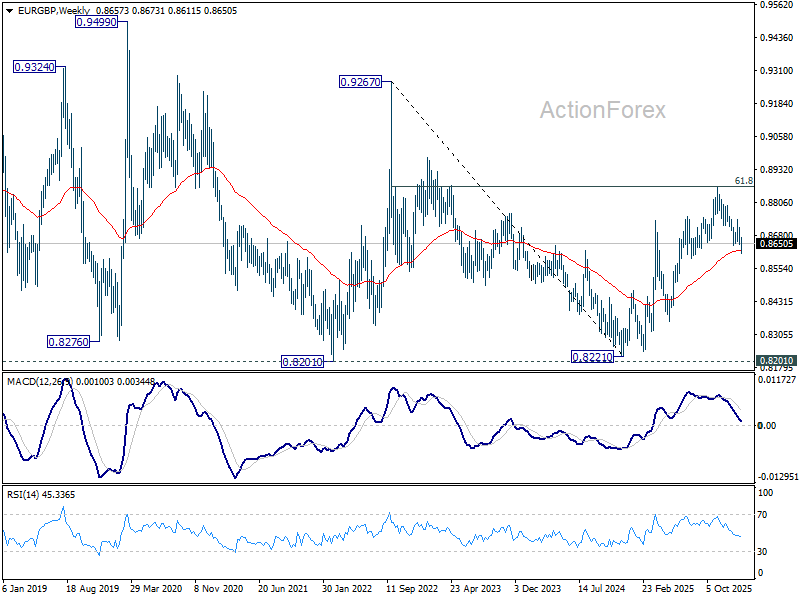

EUR/GBP sits at 0.86 key support, awaits ECB and BoE guidance

EUR/GBP is sitting at a key technical and macro junction around 0.86 level as markets head into rate decisions from the ECB and the BoE. While neither meeting is expected to deliver an immediate policy shift, both carry important signals that could shape expectations and positioning in the cross.

Both central banks are widely expected to stand pat. The ECB is set to keep the deposit rate unchanged at 2.00%, while the BoE is expected to leave Bank Rate steady at 3.75%. With these results fully priced in, the focus is firmly on guidance rather than the decisions themselves.

For the ECB, President Christine Lagarde is likely to repeat that policy is in a “good place.” There is little appetite within the Governing Council to debate changes to borrowing costs in the near term, reinforcing expectations of an extended pause.

Near-term inflation has softened, slipping to just 1.7% in January and potentially easing further in coming months. However, that downside surprise has not meaningfully altered the ECB’s broader inflation outlook. One reason is energy. The recent rebound in oil prices, if sustained, would offset much of the disinflationary impact from Euro strength. That reduces any urgency for the ECB to respond to near-term CPI weakness.

Inflation expectations also remain a concern. The ECB’s latest Consumer Expectations Survey showed five-year inflation expectations rising to 2.4% in December, the highest since the survey began. Shorter- and medium-term expectations also edged higher, supporting the ECB’s view that inflation could reaccelerate.

As a result, the ECB appears comfortable with a prolonged pause, with the next move still more likely to be a hike than a cut. One key focus today will be whether Lagarde references recent Dollar weakness and the EUR/USD exchange rate, particularly around the recently tested 1.20 level.

In the UK, the policy picture is more fractured. The BoE's December rate cut passed by a narrow 5–4 vote, underscoring deep divisions within the Monetary Policy Committee. UK inflation remains elevated, with December’s 3.4% reading the highest among G7 economies. While inflation is expected to move back toward the 2% target, some policymakers remain concerned that underlying pressures are still too strong.

Market pricing reflects that caution. Investors largely expect no move until at least April, and possibly not until July, a much slower pace of easing than seen in 2025. As usual, the MPC vote split will be closely watched for clues on the balance between hawks and doves.

Technically, EUR/GBP is testing a critical support cluster near 0.86. The favored view is that the rebound from the 0.8221 (2024 low was corrective) and may have completed at 0.8863 after failing near 61.8% retracement of 0.9267 (2022 high) to 0.8221 (2024 low) at 0.8867. Decisive break below the 0.8631 support zone (38.2% retracement of 0.8221 to 0.8663 at 0.8618, and 55 W EMA at 0.8625) would confirm bearish reversal.

However, downside confirmation is still lacking. If EUR/GBP finds firm support around current levels and stages a convincing rebound, a break above 0.8744 resistance would suggest that the fall from 0.8863 was merely a corrective pullback. In that scenario, the rise from 0.8221 would likely be resuming, with scope to extend toward through 0.8863 towards 0.9267 in the medium term.

Fed's Cook says inflation risks skewed higher, tariffs key wildcard

Fed Governor Lisa Cook said risks are currently “tilted toward higher inflation,” explaining why she supported the FOMC’s decision to hold interest rates steady at last week’s meeting.

Cook noted in a speech that understanding why inflation leveled off in 2025 requires looking beneath the headline. Disinflation has continued in housing services, while non-housing services inflation has also eased, consistent with a labor market that is no longer as tight as before.

The area of concern, however, lies in "core good prices". Cook highlighted a notable pickup in goods inflation, largely driven by last year’s tariff increases on a wide range of imported products.

While anchored inflation expectations suggest tariff effects should amount to a "one-time rise" in the price level, Cook stressed that uncertainty remains high. The "future direction of tariff policy is unclear", and it is uncertain how quickly price increases will fully pass through or whether they risk influencing expectations.

Until clearer evidence emerges that inflation is moving sustainably back toward target, Cook said inflation is "where my focus will be", barring unexpected changes in the labor market.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6966; (P) 0.7004; (R1) 0.7037; More...

AUD/USD dips mildly today as range trading continues and intraday bias stays neutral. Further rise is still in favor. On the upside, break of 0.7093 will extend larger up trend to 100% projection of 0.5913 to 0.6706 from 0.6420 at 0.7213 next. However, break of 0.6907 will bring lengthier consolidations before rally resumption. Deeper pullback would then be seen to 38.2% retracement of 0.6420 to 0.7093 at 0.6836.

In the bigger picture, current development argues that rise from 0.5913 (2024 low) is reversing whole down trend from 0.8006 (2021 high). Further rally should be seen to 61.8% retracement of 0.8006 to 0.5913 at 0.7206. This will remain the favored case as long as 0.6706 resistance turned support holds, even in case of deep pullback.