Sample Category Title

Eco Data 1/27/26

| GMT | Ccy | Events | Act | Cons | Prev | Rev |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Corporate Service Price Index Y/Y Dec | 2.60% | 2.50% | 2.70% | |

| 00:30 | AUD | NAB Business Conditions Dec | 9 | 7 | ||

| 00:30 | AUD | NAB Business Confidence Dec | 3 | 1 | 2 | |

| 14:00 | USD | S&P/CS Composite-20 HPI Y/Y Nov | 1.40% | 1.20% | 1.30% | |

| 14:00 | USD | Housing Price Index M/M Nov | 0.60% | 0.30% | 0.40% | |

| 15:00 | USD | Consumer Confidence Jan | 84.5 | 90.1 | 89.1 | 94.2 |

| 23:50 | JPY |

| Corporate Service Price Index Y/Y Dec | |

| Actual | 2.60% |

| Consensus | 2.50% |

| Previous | 2.70% |

| 00:30 | AUD |

| NAB Business Conditions Dec | |

| Actual | 9 |

| Consensus | |

| Previous | 7 |

| 00:30 | AUD |

| NAB Business Confidence Dec | |

| Actual | 3 |

| Consensus | |

| Previous | 1 |

| Revised | 2 |

| 14:00 | USD |

| S&P/CS Composite-20 HPI Y/Y Nov | |

| Actual | 1.40% |

| Consensus | 1.20% |

| Previous | 1.30% |

| 14:00 | USD |

| Housing Price Index M/M Nov | |

| Actual | 0.60% |

| Consensus | 0.30% |

| Previous | 0.40% |

| 15:00 | USD |

| Consumer Confidence Jan | |

| Actual | 84.5 |

| Consensus | 90.1 |

| Previous | 89.1 |

| Revised | 94.2 |

US Government Shutdown Watch: Shutdown Odds Rising

Summary

- The odds of a government shutdown starting on January 31 have risen sharply. The deal that was struck in November to end the record 43-day shutdown resulted in a continuing resolution extending government funding for most federal agencies (accounting for ~90% of annual discretionary spending) through January 30. That bill provided full-year appropriations for three of the 12 annual appropriation bills (Agriculture, Military Construction and Veteran Affairs and the Legislative branch) accounting for the remaining ~10% of the annual discretionary budget.

- Over the past few weeks, the House of Representatives passed the nine remaining fiscal year (FY) 2026 appropriations bills on a bipartisan basis, and the Senate was widely expected to package them into one bill and pass it into law before the January 31 deadline. If enacted, this bill would keep federal discretionary spending roughly flat compared to FY 2025, and it would take another shutdown off the table until October 1 at the earliest.

- As recently as Friday, a shutdown seemed quite unlikely. Prediction markets such as Polymarket pegged the odds of a shutdown at roughly 10% as of Friday evening.

- The shooting by federal agents that occurred in Minneapolis on Saturday has changed the outlook. Importantly, one of the nine annual appropriations bills passed by the House is Homeland Security, which houses Customs and Border Protection (CBP) and Immigration and Customs Enforcement (ICE). In the wake of the incident, some Senate Democrats who were widely expected to support the budget bill have pulled their support until there have been some policy and process reforms to CBP/ICE.

- Even if all 53 Republicans vote for the bill, it would take at least seven Democrats to clear the de facto 60 vote threshold in the Senate, leaving the process at a stalemate. As of this writing, Polymarket traders priced the odds of a shutdown starting Saturday at roughly 80%, which strikes us as reasonable based on what we know now.

- The situation is still highly fluid, and anything can happen, but the deadline for action is imminent. It will be difficult to get a new bill through both chambers in less than a week as the House is scheduled to be on recess this week and the Senate is just coming back into town on Monday/Tuesday. Bad weather throughout much of the country further compounds the time crunch.

- If a short shutdown occurs, this would delay but not cancel the BLS/BEA produced economic data that are slated to be released in the coming weeks, such as the January employment report (scheduled for Feb. 6) and the January CPI report (Feb. 11). That said, if the shutdown was much longer, like the one that occurred last fall, there once again could be severe disruptions that result in lower quality and/or missing data.

- As was the case last fall, a shutdown starting Saturday would not impact the debt ceiling. The U.S. Treasury's borrowing capacity would not be exhausted, and Treasury security auction and interest payments would continue as scheduled.

- Should another extended shutdown occur, it would leave the FOMC in a tricky spot. The lack of visibility that arises from receiving limited economic data could thrust an already divided FOMC into a period of stasis. Fed officials lamented the lack of clarity on inflation during the last shutdown. We expect they would again use this argument to delay additional cuts. We have maintained that the window is closing for the Fed to cut rates again under Chair Powell, and another extended shutdown would not help.

FOMC Meeting Preview: Fed To Keep Rates on Hold, Implications for DXY and Gold

The meeting of the Federal Open Market Committee (FOMC) on January 28, 2026 will be an intriguing one.

The current economic data is showing a strange pattern that doesn't follow the usual rules: the US economy is growing very fast with estimates suggesting a massive 5.4% growth rate for Q4 but at the same time, the job market is slowing down.

Meanwhile, inflation is stuck at 3.0%, which is higher than what the central bank wants to see.

Usually, fast growth leads to higher inflation and a hot job market, but that isn't happening right now. This split could mean that businesses are becoming much more efficient and productive.

However, it could also be a warning sign that the economy is starting to "overheat" (growing too fast to be sustainable), even if it doesn't look like it yet due to temporary factors.

Heading into the meeting and market participants are pricing in around a 97% probability of a rate hold at Wednesdays meeting.

Source: LSEG

The Political Economy of 2026

The January 2026 meeting cannot be analyzed in a vacuum of economic data. It occurs within a "storm" of political pressure that threatens the institutional integrity of the Federal Reserve.

The "Eye of the Storm"

The Rabobank report characterizes the current environment as "In the Eye of the Storm". This metaphor is apt. The "storm" is the friction between President Trump’s administration and the Federal Reserve.

- Executive Pressure: President Trump has increasingly tightened his "grip" on the Fed. His administration explicitly favors lower interest rates to boost growth and reduce the cost of servicing the national debt.

- The "Quartermaster": The report mentions a "quartermaster" named Miran—likely a key economic aide or shadow advisor—who advocated for a 50 basis point cut in December. This reveals the delta between the Fed’s action (25 bps) and the Administration’s desire (50 bps). The pressure is for more easing, faster.

The Powell Subpoena and Exit

Chair Jerome Powell is under siege. He faces a subpoena and a Department of Justice investigation.

- Unprecedented Legal Pressure: Never in modern history has a sitting Fed Chair been subject to such overt legal pressure from the executive branch. This is designed to weaken his standing and force compliance with the low-rate agenda.

- Powell's Response: Powell is expected to be defiant in the press conference, likely stating he has "said all he has to say". However, the psychological toll and the distraction are undeniable.

- The May Transition: Powell’s term as Chair ends on May 15, 2026. This date is the event horizon for monetary policy.

- Scenario A: Powell leaves quietly. Trump appoints a loyalist.

- Scenario B: Powell fights to stay on the Board of Governors (his term as Governor lasts until 2028). Trump has warned that Powell’s life "won't be very happy" if he does this. If Powell stays, he denies Trump a vacancy on the Board, preventing the appointment of a crucial swing vote.

The June Pivot

The forecast for a rate cut in June 2026 is heavily predicated on this political transition. Rabobank explicitly states they have "higher confidence" in a June cut because "this will be the first meeting led by the new Fed Chair".

Implication: The market is pricing in a political reaction function. The expectation is that the new Chair will be appointed with a mandate to cut rates, regardless of whether inflation is 3.0% or GDP is 5.4%. This expectation of a "politicized pivot" is a key driver of the Gold rally and Dollar weakness.

Market Implications for FX

The relationship between US politics and money is changing how the world views different currencies. Right now, the US dollar is on a downward trend for a few key reasons:

Why the Dollar is Weakening

The "Bearish" Case: The U.S. Dollar Index (an indicator of the dollar's strength) has dropped to around 97.00.

Falling Interest Rates: Even though the Federal Reserve (the US central bank) has paused some moves, investors know that interest rates are likely headed lower, potentially down to around 3.0%–3.25% by the end of the year. When interest rates in the US fall while other countries stay steady, the dollar becomes less attractive to market participants..

The "Governance Discount": Market participants are becoming worried about political friction in Washington. Specifically, public disagreements between the White House and the Federal Reserve make people feel the central bank might lose its independence. This makes the dollar seem like a riskier place to keep money.

How Other Currencies Are Reacting

The Euro (EUR/USD): The Euro has climbed to around $1.19. Experts believe it will continue to rise throughout 2026 because European interest rates are becoming more competitive compared to US rates.

The British Pound (GBP/USD): The Pound has reached its highest level in four months, hitting nearly $1.37. This is happening because the global economy seems to be heading for a "soft landing" (slowing down without a major crash), which usually helps the Pound.

The Future of the Dollar

The outlook for the dollar is shaky. If the Federal Reserve appoints a new leader who prefers lower interest rates, the dollar index could fall even further. Currently, the dollar's only real "lifelines" would be a sudden spike in US inflation (which would force rates back up) or a major global crisis that makes people run back to the dollar for safety.

However, with Gold reaching record highs above $5,100, it appears that many investors are now choosing "hard assets" like gold instead of the US dollar when they want to play it safe.

Monetary Policy Outlook

The path for the rest of 2026 is the subject of intense debate among market participants.

The consensus among analysts and market participants (2-3 cuts) is more dovish than the Fed (1 cut). This discrepancy is the source of market volatility. If the Fed sticks to its guns (1 cut), yields will rise, and equities/gold could correct.

If the Fed capitulates (3 cuts), the "melt-up" continues.

There is also the possibility that the Fed may stick to its guns of 1 cut while market participants hold their expectations steady at 2-3 cuts. In such a scenario, the immediate market reaction may be rather muted.

US Dollar Index (DXY) Chart, January 26, 2026

Source: TradingView.Com (click image to enlarge).

Key Levels to Focus On

Support:

- 96.37

- 95.00

- 94.50

Resistance:

- 97.70

- 98.67

- 100.00

XAG/USD: Silver Accelerates Higher After Friday’s Break of Psychological $100 Level

Silver extends gains above psychological $100 level that was broken on Friday (market closed at $103.23) and hit new all-time high well above $111 on Monday.

Silver was strongly boosted by sharply rising demand for precious metals, strong industrial demand, which faces growing disbalance between demand and supply and weakening dollar, in which the price of metal is expressed.

Silver continues to track gold but has strongly outperformed the yellow metal with its 145% advance in 2025, compared to gold’s 66% gain.

The gold – silver ratio which indicates how many ounces of silver is needed to buy one ounce of gold, currently stands at around 46 (the lowest since Sep 2011) and signals that possession of silver should be converted to gold, although many say that the ratio is not relevant in today’s markets.

Silver made an impressive rally in January by advancing 53% until today (record rise), which adds to firmly bullish structure, but also warns of potential correction, due to overstretched studies on all larger timeframes, but also to the fact that the metal stays in steep and uninterrupted rally for nine consecutive months, which continued to accelerate and showed better performance each month compared to the previous month.

Strong bullish structure eyes sustained break above $110 to remain in play for acceleration towards targets at $115 (round-figure) and $116 (Fibo 138.2% expansion) guarding psychological $120 barrier.

Immediate support lays at $110, followed by 108.40 (hourly higher base), 105.40 (daily Kijun-sen) and 103.09 (daily low) and $100 (broken psychological resistance reverted to strong support, which should contain potential deeper dips and keep larger bulls in play for further gains.

Res: 112.00; 115.00; 116.00; 120.00.

Sup: 110.00; 108.40; 105.40; 103.09.

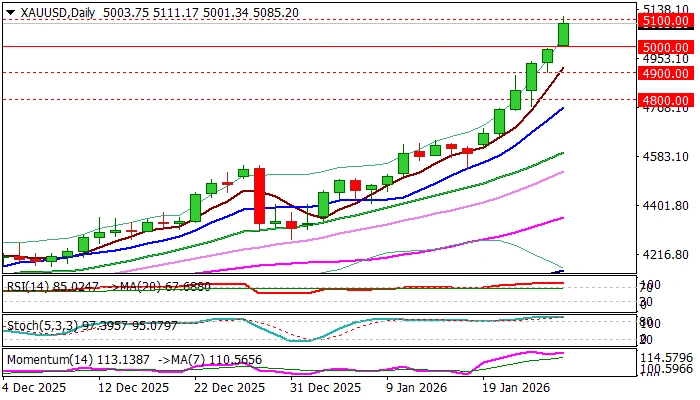

XAU/USD: Gold Surges Through Key $5,000 Barrier and Cracks $5,100

Gold took out $5000 barrier in one single step on Monday, in a widely expected post-weekend action, but made a small surprise to traders by extension to $5100, which happened in just few hours of early Monday’s trading.

The yellow metal started trading with a gap higher and opened slightly above $5K following news over the weekend that added to strong bullish stance.

Growing signals about potential US attack on Iran contributed to strong migration into safety, also fueled by overall geopolitical situation being close to boiling point, weakening economic outlook with signs of deeper crisis on horizon, growing political and economic tensions between the US and EU (Greenland, tariffs) deteriorating situation in Ukraine (no big hopes from current peace talks), fragile situation in the Middle East region and strong demand for gold from investors and central banks.

This leaves very little space for any significant correction despite strongly overbought studies (daily / weekly / monthly) as traders do not dare to take profits on rallying market.

Overall picture remains firmly bullish from both technical and fundamental aspects, though fundamentals remain key driver, suggesting that the price could rise much more if current conditions deteriorate or at least stay unchanged.

Today’s close above $5000 is a minimum requirement to keep bulls intact for further advance, with clear break of $5100 to confirm bullish continuation.

The price is riding on an extended third wave of five-wave cycle from $3997 (Nov 18 higher low), with cracked round figure $5100 and session high / new all-time high at $5111, marking immediate resistances, followed by $5172 (Fibo 161.8% expansion), $5200 (round-figure) and $5253 (Fibo 176.4% expansion).

Minor support lays at $5050 (intraday low) followed by $5039 (20HMA) and the most significant psychological $5000 level (broken key resistance, reverted to strong support, also daily low) where extended dips should find firm ground.

Current structure favors very limited profit taking, with limited dips to mark consolidation and positioning for further upside.

Res: 5111; 5172; 5200; 5253.

Sup: 5040; 5000; 4965; 4937.

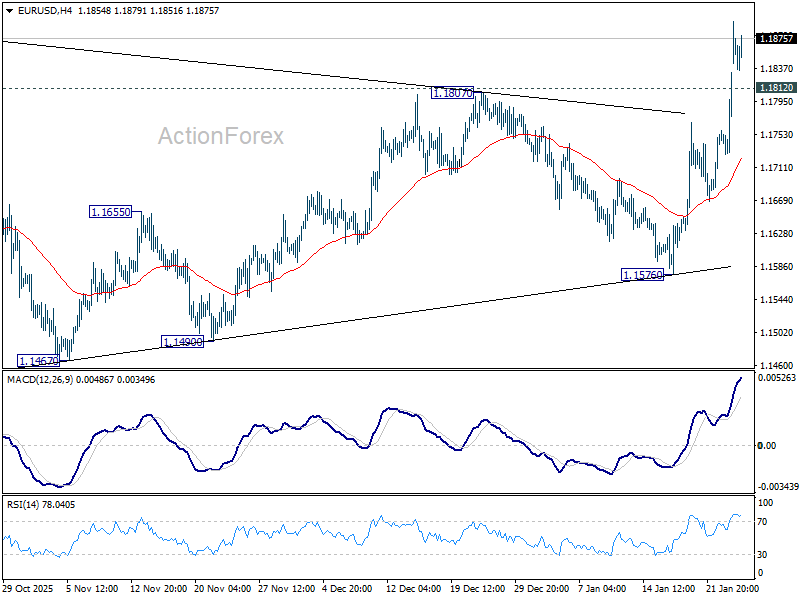

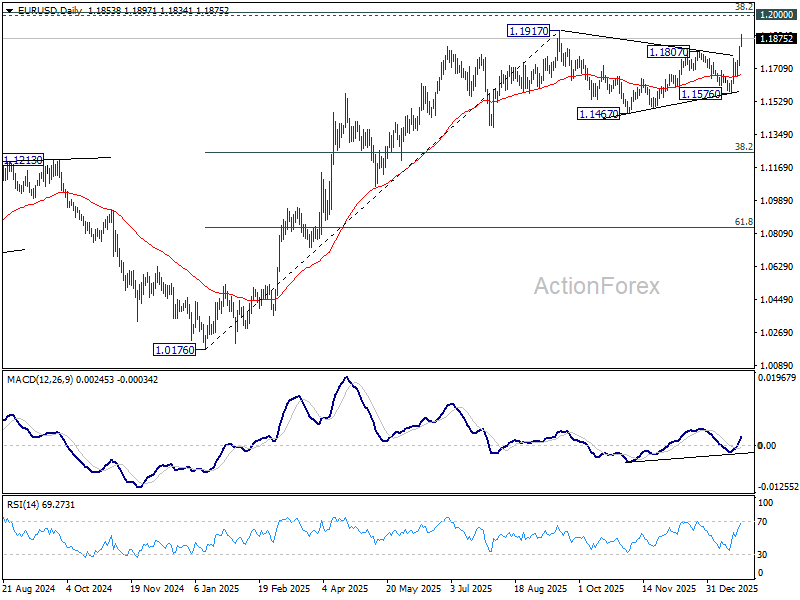

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1760; (P) 1.1797; (R1) 1.1866; More….

EUR/USD's rally continues today and intraday bias stays on the upside for 1.1917 key resistance. Firm break there will resume larger up trend. On the downside, below 1.1812 minor support will mix up the outlook and turn intraday bias neutral again.

In the bigger picture, as long as 55 W EMA (now at 1.1443) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will carry larger bullish implication. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

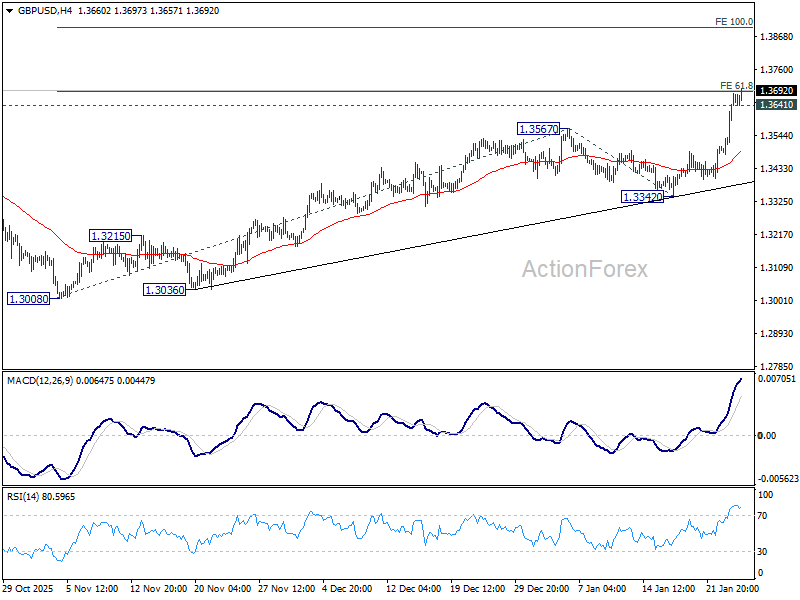

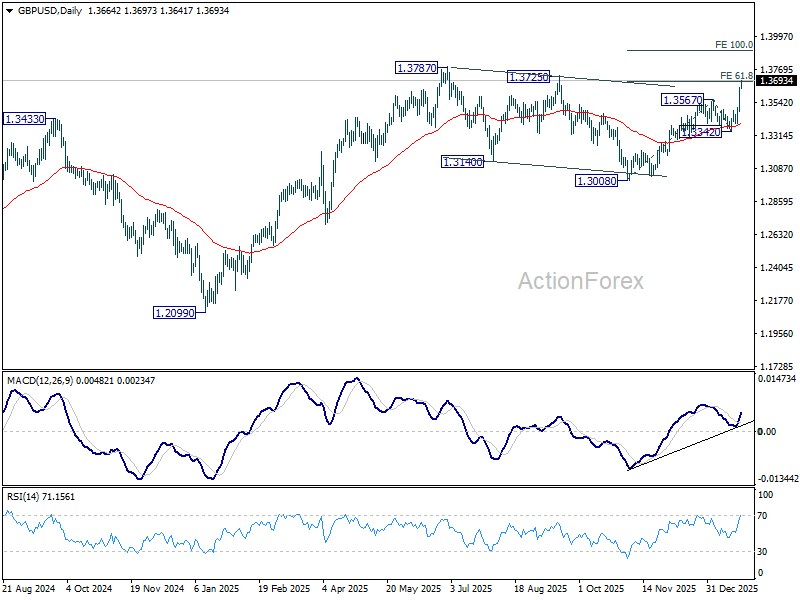

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3534; (P) 1.3590; (R1) 1.3698; More...

Intraday bias in GBP/USD remains on the upside for the moment. Sustained trading above 61.8% projection of 1.3008 to 1.3567 from 1.3342 at 1.3687 should prompt upside acceleration through 1.3787 high to 100% projection at 1.3901. On the downside, below 1.3641 minor support will turn intraday bias neutral. But retreat should be contained well above 1.3342 support to bring another rally.

In the bigger picture, price actions from 1.3787 (2025 high) are seen as a correction to the larger up trend from 1.3051 (2022 low). That might have completed at 1.3008 already. Firm break of 1.3787 will confirm up trend resumption. Next target is 1.4284 key resistance (2021 high). This will remain the favored case as long as 1.3008 support holds.

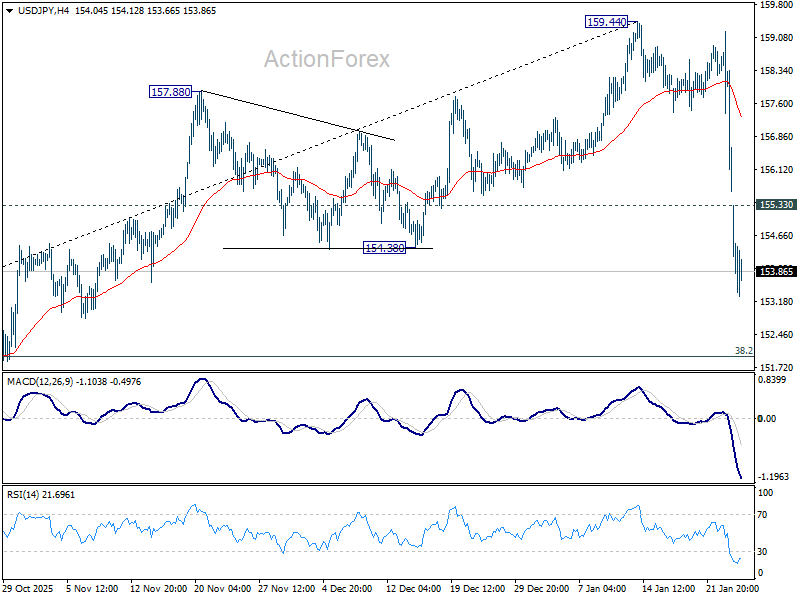

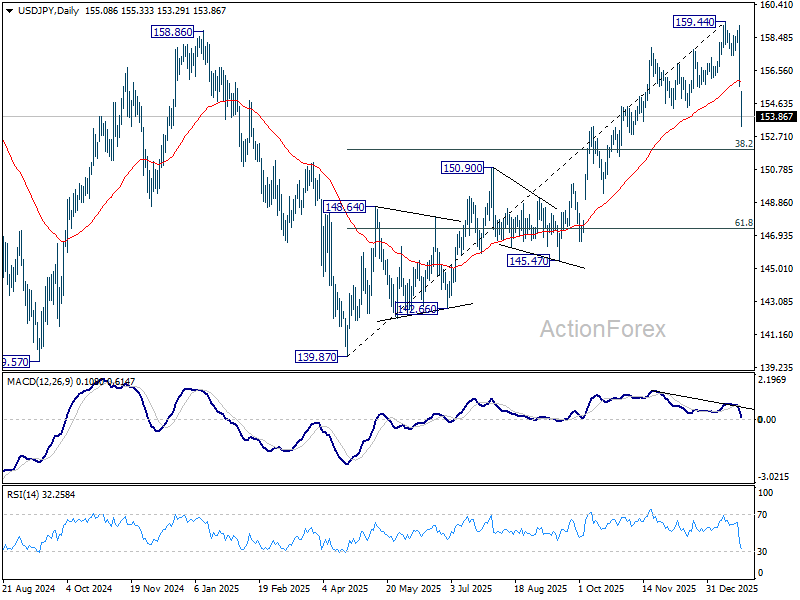

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 154.48; (P) 156.86; (R1) 158.09; More...

Intraday bias in USD/JPY remains on the downside for the moment. Fall from 159.44 is seen as correcting the rise from 139.87. Deeper fall should be seen to 38.2% retracement of 139.87 to 159.44 at 151.96. Strong support should be seen there to bring rebound, at least on first attempt. On the upside above 155.33 minor resistance will turn intraday bias neutral and bring consolidations first. However, decisive break of 151.96 will argue that it is reversing whole rise from 139.87. Deeper decline would then be seen to 61.8% retracement at 147.34.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 151.35) holds. However, sustained break of 55 W EMA will argue that the pattern from 161.94 is extending with another falling leg.

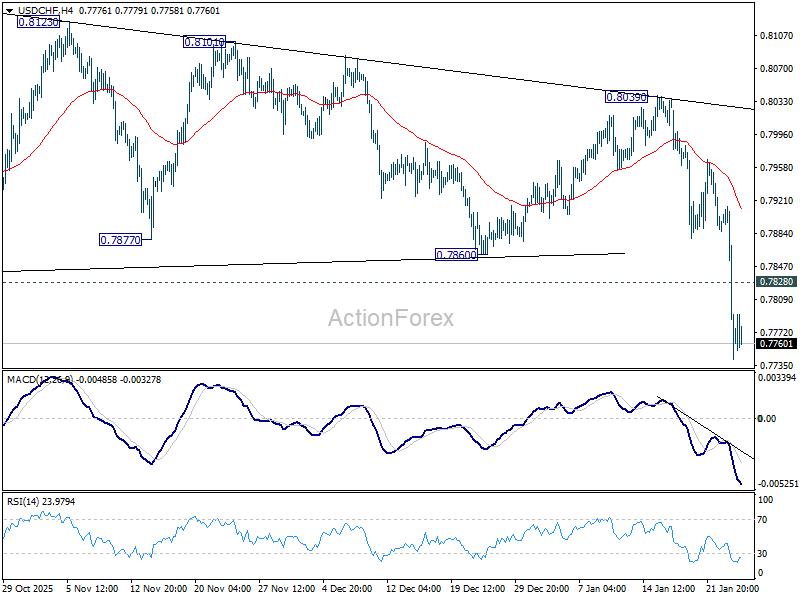

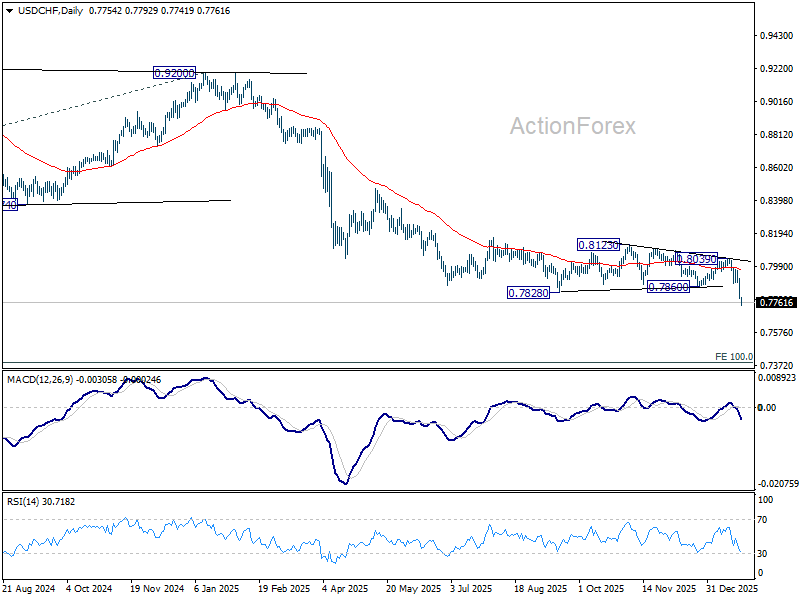

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7754; (P) 0.7836; (R1) 0.7884; More….

Intraday bias in USD/CHF remains on the downside for the moment. Current fall is part of the larger down trend and should target 0.7382 projection level. On the upside, above 0.7828 minor resistance will turn intraday bias neutral first. But recovery should be limited well below 0.8039 resistance to bring another fall.

In the bigger picture, larger down trend from 1.0342 (2017 high) is still in progress and resuming. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8184) holds.

Dollar Stays on the Defensive as Shutdown Risk Returns to the Fore

Dollar remains generally weak as markets move into the early US session, even though outright selling pressure has eased slightly. The slowdown, however, looks more like consolidation than recovery, with the greenback still exposed to fresh political and policy risks. That vulnerability follows an already bruising period marked by renewed transatlantic trade tensions and the latest tariff spat involving Canada. Markets are increasingly uneasy that US trade policy is becoming more erratic rather than more predictable.

A new source of concern has now emerged in Washington, where the risk of another US government shutdown is rising rapidly. Over the weekend, Senate Democrats vowed to oppose a funding package that includes financing for the Department of Homeland Security, following the fatal shooting of Alex Pretti by U.S. Immigration and Customs Enforcement agents in Minnesota. Democrats warned they would not support the USD 1.2 trillion funding bill for federal government operations, citing concerns over how immigration enforcement is being carried out. The stance sharply raises the stakes ahead of a looming funding deadline.

Until recently, markets viewed another shutdown as a manageable risk. Probabilities had hovered around 30% for much of January. That situation has shifted abruptly. On Polymarket, traders now price near 80% probability of a federal government shutdown by January 31, this coming Saturday. The threat is not new, but its immediacy has increased. Funding for a wide range of federal agencies is set to expire at the end of January, and failure to agree on a new package would trigger another partial shutdown, following a similar standoff late last year.

Against this backdrop, markets are struggling to find reasons to buy Dollar. Political dysfunction adds to an already fragile confidence backdrop shaped by trade frictions and capital flow concerns.

Elsewhere on the trade front, developments in other regions offered a contrasting signal. Reports suggest India is preparing to slash tariffs on EU car imports to 40% from as high as 110%, as New Delhi and Brussels close in on a free trade agreement that could be announced as early as Tuesday. Under the plan, Prime Minister Narendra Modi’s government would immediately lower duties on a limited number of high-end vehicles priced above EUR 15,000, with rates eventually falling to 10%. The move would ease access for European automakers.

In currency markets, Yen remains the strongest performer, underpinned by direct and blunt intervention warnings from Prime Minister Sanae Takaichi over the weekend. Aussie and Kiwi follow as the next strongest. Dollar sits at the bottom alongside its neighbor Loonie, with Sterling also lagging. Euro and Swiss Franc are holding middle ground.

In Europe, at the time of writing, FTSE is up 0.30%. DAX is up 0.25%. CAC is up 0.16%. UK 10-year yield is down -0.031 at 4.498. Germany 10-year yield is down -0.037 at 2.872. Earlier in Asia, Nikkei fell -1.79%. Hong Kong HSI rose 0.06%. China Shanghai SSE fell -0.09%. Singapore Strait Times fell -0.62%. Japan 10-year JGB yield fell -0.016 to 2.248.

US durable goods orders surge 5.3% mom in November, led by transport strength

US durable goods orders posted a strong upside surprise in November, rising 5.3% mom to USD 323.8B, well above expectations for a 3.1% increase.

Excluding transportation, orders rose a solid 0.5% mom to USD 204.4B, also beating forecasts of a 0.3% increase. Ex-defense orders jumped an even stronger 6.6% mom to USD 286.9B.

Transportation equipment was the clear driver, surging 17.9% mom to USD 119.3B. While volatility in this category is common, the underlying gains in core orders suggest business investment remained resilient.

German Ifo stalls at 87.6, as weak momentum carries into new year

Germany’s Ifo Institute Business Climate Index was unchanged at 87.6 in January, undershooting expectations for a modest improvement to 88.3. The stagnant headline reading reinforces the view that Germany’s economy is entering the new year without meaningful traction.

Beneath the surface, the details were mixed. Current Assessment Index edged slightly higher from 85.6 to 85.7, suggesting conditions have stabilized but remain weak. In contrast, Expectations Index slipped from 89.7 to 89.5, indicating that confidence about the months ahead has softened rather than improved.

Sector performance highlighted the uneven picture. Manufacturing showed a notable improvement, rising from -14.6 to -12.2, while trade and construction also edged higher to -21.1 and -14.2 respectively. Services, however, deteriorated from -2.1 to -2.6. Ifo summed up the survey bluntly, saying the German economy is "starting the new year with little momentum".

Yuan hits 32-month high against Dollar, but dives against Euro

Chinese Yuan edged higher against Dollar today, pushing to a fresh 32-month high and drawing renewed attention to Beijing’s currency stance. The move comes amid growing speculation that Chinese authorities may be quietly signaling greater tolerance for a firmer Yuan.

However, a broader look at currency markets suggests Yuan’s gains are far more a function of broad-based Dollar weakness than a deliberate shift in Chinese policy. The greenback has been under sustained pressure globally, and USD/CNH has largely followed that trend rather than leading it. Indeed, when compared with other major currencies, Yuan’s appreciation has been notably measured and controlled. This relative restraint argues against the idea that Beijing is prepared to allow a free or rapid strengthening.

Still, markets have taken note of subtle policy signals. Late last week, the People’s Bank of China set Yuan’s daily fixing at 6.9929 per Dollar, the first time the midpoint has been set stronger than the closely watched 7.00 level since May 2023. It also marked the largest one-day strengthening since August. China went a step further today. Before markets opened, the PBOC fixed the midpoint at 6.9843 per dollar, the strongest level since May 17, 2023. The move reinforced the perception that authorities are comfortable with some near-term Yuan strength, particularly against a weakening dollar.

That said, analysts remain wary of extrapolating too much. Expectations are building that authorities could push back if appreciation pressures intensify, using policy tools to smooth gains and preserve competitiveness. The prevailing view remains that any Yuan strength will be tightly managed rather than left to market forces.

Technically, cross-rates echo that narrative. In EUR/CNH, the strong rally over the past two days and a clear break above the 55 Day EMA at 8.2025 suggest the corrective pullback from 8.4638 has completed at 8.0654, 38.2% retracement of 7.4886 (2025 low) to 8.4638 (2025 high) at 8.0913. Near-term focus is now on 8.3004, with a firm break there opening the door for a retest of 8.4638 high.

Meanwhile, USD/CNH continues to drift lower, but downside momentum is clearly waning. Daily MACD shows fading bearish pressure, while the pair has struggled to extend beyond the falling channel floor and 100% projection of 7.4287 to 7.1608 from 7.2224 at 6.9545.. A rebound from current levels, followed by break above 6.9956, would confirm short-term bottoming and reinforce the view that Yuan strength remains controlled rather than open-ended.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7754; (P) 0.7836; (R1) 0.7884; More….

Intraday bias in USD/CHF remains on the downside for the moment. Current fall is part of the larger down trend and should target 0.7382 projection level. On the upside, above 0.7828 minor resistance will turn intraday bias neutral first. But recovery should be limited well below 0.8039 resistance to bring another fall.

In the bigger picture, larger down trend from 1.0342 (2017 high) is still in progress and resuming. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8184) holds.