Sample Category Title

China data disappoints as consumption and investment weaken further

China’s November activity data delivered a broadly weaker-than-expected picture. Industrial production rose 4.8% yoy, missing expectations for 5.0% growth and marking the weakest pace since August 2024.

The sharper disappointment came from consumption. Retail sales rose just 1.3% yoy, far below expectations of 2.9% and slowing markedly from October’s 2.9% pace. It was also the weakest reading since December 2022.

Investment conditions also deteriorated. Year-to-date fixed asset investment fell -2.6%, deeper than expected -2.3% and the sharpest contraction since the pandemic in 2020. The drag from property intensified, with real estate investment down -15.9% in the first eleven months of the year, extending the slump seen earlier and reinforcing the view that the property sector remains a central constraint on China’s recovery.

Japan Tankan: Manufacturing sentiment improves as firms absorb tariff impact

Japan’s Q4 Tankan survey delivered a broadly supportive signal for the economy, reinforcing expectations that the BoJ will proceed with rate normalization. The large manufacturing index rose from 14 to 15, in line with expectations, marking a third consecutive quarterly improvement and the strongest reading since December 2021. The result suggests manufacturers have so far weathered the impact from higher U.S. tariffs better than feared.

Sentiment among non-manufacturers was less impressive, with the index unchanged at 34, falling short of expectations for a modest uptick. Even so, the divergence does not point to a meaningful deterioration in overall conditions, as services confidence remains elevated relative to historical norms.

Capital spending intentions added to the constructive tone. Large firms now plan to increase investment by 12.6% in the current fiscal year ending March 2026, slightly above market expectations of 12.0%.

The survey also indicated firms expect inflation to average 2.4% across one-, three-, and five-year horizons, suggesting expectations are stabilizing around the BoJ’s 2% target.

With tariff uncertainty easing and manufacturing sentiment holding firm, the survey supports the dominant market view that BoJ is positioned to raise rates in December, even as the pace of tightening beyond that remains gradual.

RBNZ’s Breman sees OCR holding at 2.25% if outlook unfolds as expected

RBNZ Governor Anna Breman signaled in media interviews today that the bar for further near-term easing remains high. While the forward path published in the November Monetary Policy Statement allows for a small probability of another rate cut, Breman stressed "if economic conditions evolve as expected the OCR is likely to remain at its current level of 2.25 per cent for some time."

Looking ahead to the next OCR decision in February, Breman said the central bank will continue to assess incoming data, financial conditions, and global developments, with a particular focus on implications for New Zealand’s economic outlook and its medium-term inflation objective.

Breman also reiterated that monetary policy is not on a preset course, highlighting the MPC’s regular meeting schedule as a reflection of that flexibility.

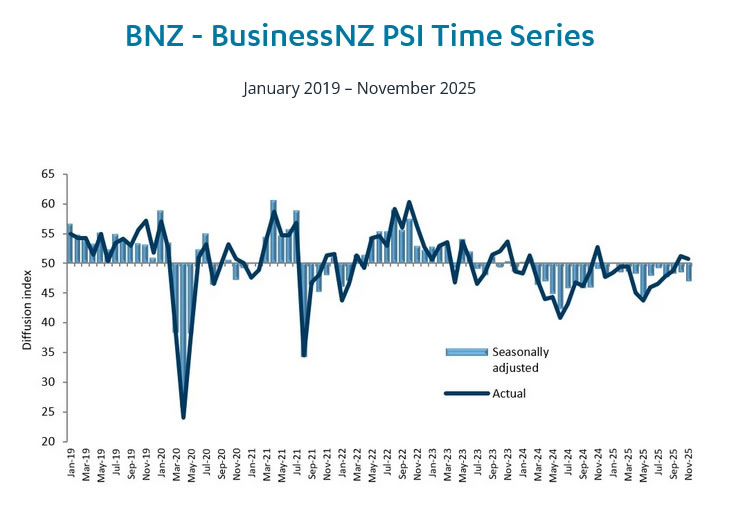

NZ BNZ service falls to 46.9, recovery hopes dented

New Zealand’s services sector slipped deeper into contraction in November, reinforcing signs that domestic demand remains fragile. BusinessNZ Performance of Services Index fell from 48.4 to 46.9, marking the lowest level of activity since May and sitting well below the survey’s long-run average of 52.8. All five sub-indices remained in contraction territory, underlining the broad-based nature of the slowdown.

Activity and sales saw the sharpest deterioration, dropping from 48.4 to 45.8, while employment also weakened from 48.6 to 46.4. New orders edged marginally higher from 49.2 to 49.3, offering little evidence of an imminent turnaround in demand.

BusinessNZ Chief Executive Katherine Rich said the November reading "put to bed" any immediate hope that the sector was moving toward expansion. While the proportion of negative comments eased slightly from recent months, businesses continued to cite a weak economic backdrop, low consumer confidence, high living costs, inflation, interest rates, and reduced spending as the dominant constraints on activity.

EUR/USD Reclaims Positive Ground—Is This More Than a Bounce?

Key Highlights

- EUR/USD started a steady increase above 1.1650 and 1.1700.

- It could struggle to clear the 1.1800 resistance on the 4-hour chart.

- GBP/USD climbed toward 1.3450 before it saw a minor pullback.

- Gold started a fresh surge above $4,250 and $4,300.

EUR/USD Technical Analysis

The Euro formed a base above 1.1620 and started a fresh increase against the US Dollar. EUR/USD surpassed 1.1680 to enter a positive zone.

Looking at the 4-hour chart, the pair cleared many hurdles near 1.1700. It settled above the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour). A new multi-week high was formed at 1.1762 before the pair started a consolidation phase.

There was a minor decline to the 23.6% Fib retracement level of the upward move from the 1.1615 swing low to the 1.1762 high. On the downside, there is key support at 1.1705.

The first major support is near the 50% Fib retracement level at 1.1688. The next support could be 1.1670, below which the bears might aim for a move toward the 100 simple moving average (red, 4-hour) at 1.1615.

Immediate resistance sits near 1.1765. The first key hurdle is seen near 1.1800. A close above 1.1800 could open the doors for a move toward 1.1850. Any more gains could set the pace for a steady increase toward 1.1880.

Looking at GBP/USD, the pair gained pace for a strong increase and was able to clear the 1.3400 resistance zone.

Upcoming Key Economic Events:

- NY Empire State Manufacturing Index for Dec 2025 – Forecast 10.6, versus 18.7 previous.

- Fed's Miran speech.

- Fed's Williams speech.

Key U.S. Data and Central Banks Drive the Last Full Trading Week of the Year

The focus of the week was the FOMC meeting. The U.S. Federal Reserve cut interest rates for the third meeting in a row, lowering the policy rate to 3.50%–3.75%. After the decision, Fed Chair Powell sounded more open to further rate cuts than markets expected. This supported U.S. stocks and gold and led to continued selling of the U.S. dollar.

In Japan, GDP data came in weaker than expected, highlighting slowing growth. However, comments from Bank of Japan Governor Ueda shifted market expectations. He said inflation is moving closer to the BOJ’s target, increasing expectations of an interest rate hike at this week’s BOJ meeting. At the same time, the 10-year Japanese government bond yield rose to around 1.95%, an important level for markets.

Toward the end of the week, technology stocks came under pressure, as concerns returned about high valuations in AI-related companies. While overall market sentiment remains positive, these worries could continue to create volatility in the tech sector.

Markets This Week

U.S. Stocks

The Dow dipped early in the week but rebounded strongly after the FOMC statement signaled a more accommodative stance toward further interest rate cuts in 2026. This pushed the index to new record highs. While technology stocks remain under pressure, the Dow continues to show strength, with the 10-day moving average trending higher and acting as support. As long as this uptrend remains intact, buying pullbacks remains the preferred strategy. Resistance is seen at 48,500 and 49,000, while support is located at 48,000, 47,500, 47,000, 46,500, and 46,000.

Japanese Stocks

The Nikkei 225 traded sideways last week as weak domestic economic data and rising expectations for an interest rate hike offset the positive impact of higher U.S. stock prices. The upcoming rate hike is largely priced in and is unlikely to trigger a sharp sell-off as seen in the past. However, with domestic growth under pressure and long-term Japanese interest rates continuing to rise, the risk of a move lower appears higher in the near term. Resistance is at 51,000円, 51,500円, and 52,000円, while support is at 49,000円, 48,000円, and 47,000円.

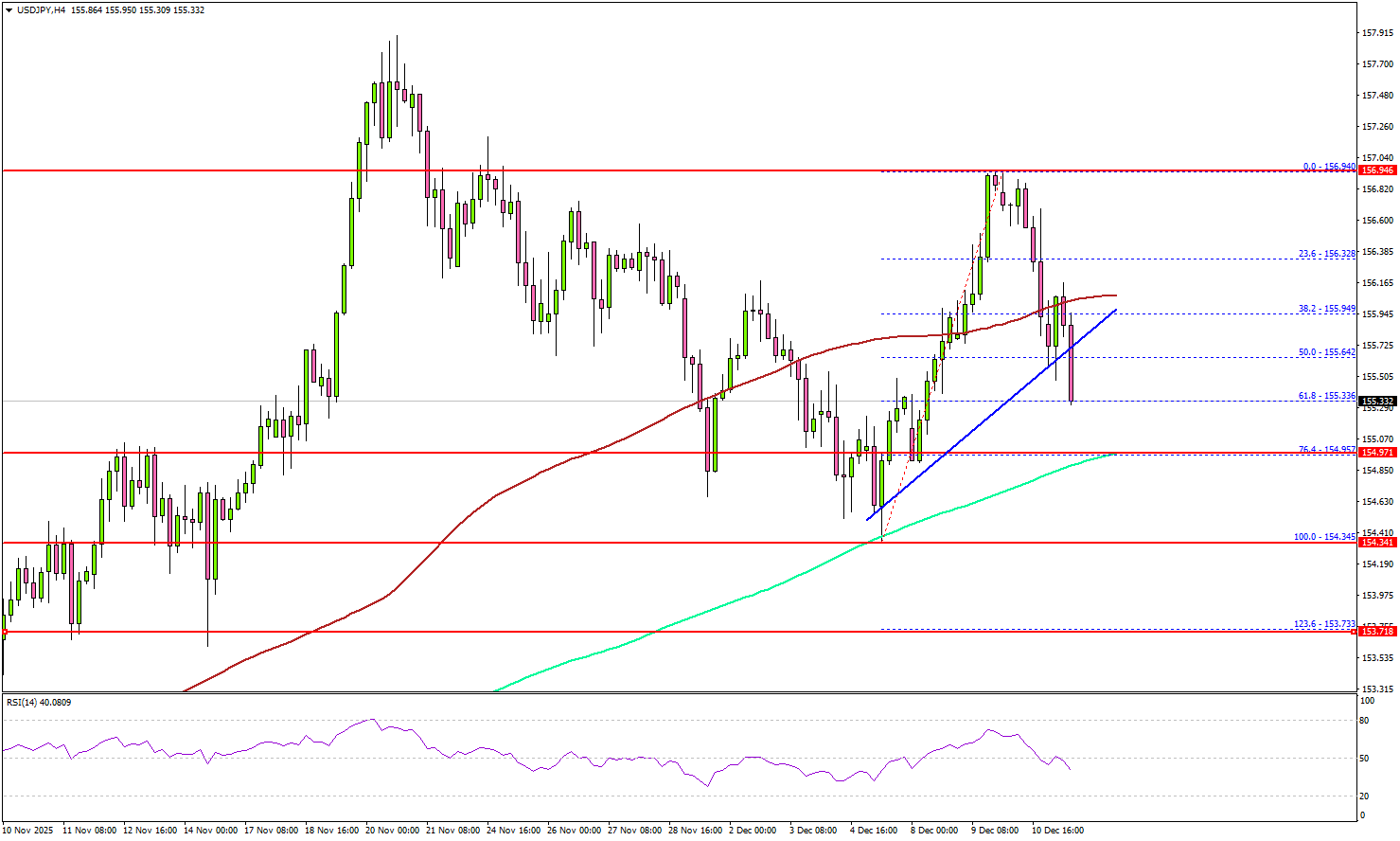

USD/JPY

USD/JPY briefly moved higher on weak Japanese economic data ahead of the FOMC meeting, but finished the week close to unchanged. Fed Chair Powell’s comments increased expectations for further interest rate cuts, putting pressure on the U.S. dollar. Range trading is likely ahead of the BOJ meeting, which is the main focus of the week, offering near-term trading opportunities. Resistance is at 156, 157, and 158, while support is at 154, 153, and 152.

Gold

Gold remained well supported after Fed Chair Powell’s statement weakened the U.S. dollar and reinforced expectations for further U.S. interest rate cuts. Prices paused just below record highs from October as the market became slightly overbought in the short term. Despite this, the broader uptrend remains strong, and buying pullbacks toward the 10-day moving average continues to be the preferred strategy as gold targets new highs. Resistance is at $4,300, $4,350, $4,380, and $4,400, while support is seen at $4,200, $4,150, and $4,100.

Crude Oil

WTI struggled to hold above $60 last week as concerns over U.S. demand and rising inventories encouraged selling, despite the Federal Reserve’s interest rate cut. With these supply-demand pressures still in place, the market is likely to remain under pressure into 2025, and a retest of the yearly lows appears increasingly likely. Resistance is seen at $60, $65, $66.50, $70, and $75, while support remains at $55 and $50.

Bitcoin

Bitcoin tested resistance near $95,000, supported by expectations of lower U.S. interest rates. However, selling in technology stocks late in the week put pressure on prices, leaving Bitcoin to close near the middle of its recent range. With buyers cautious, range trading between $85,000 and $95,000 remains the preferred short-term strategy. Resistance is at $95,000 and $100,000, while support is at $85,000, $80,000, and $75,000.

This Weeks Focus Image

This Week’s Focus

- Monday: Japan Tanaka Index, China Industrial Production, E.U. Industrial Production, NY Empire State Manufacturing Index

- Tuesday: Japan au Jibun Bank Services PMI, U.K. Unemployment Rate, E.U. HCOB Eurozone Manufacturing PMI, U.K. S&P Global Manufacturing PMI, U.S. Non Farm Payroll, Retail Sales and S&P Global Manufacturing PMI

- Wednesday: Japan Trade Balance, U.K. CPI, E.U. CPI

- Thursday: U.K. BoE Interest Rate Decision, E.U. ECB Interest Rate Decision, U.S. CPI and Philadelphia Fed Manufacturing Index

- Friday: Japan National CPI and BoJ Interest Rate Decision, U.K. Retail Sales, U.S. Existing Home Sales and Michigan Consumer Sentiment

The final full trading week before the holiday season is set to be busy, with several major central bank meetings. The European Central Bank is expected to leave interest rates unchanged, while the Bank of England is expected to cut rates, and the Bank of Japan is widely expected to raise rates. In the U.S., delayed employment data will be released midweek, alongside retail sales and inflation data, which could influence near-term market sentiment. Inflation data from Europe and the UK will also be closely watched, as markets look for signals on interest rate expectations into 2026.

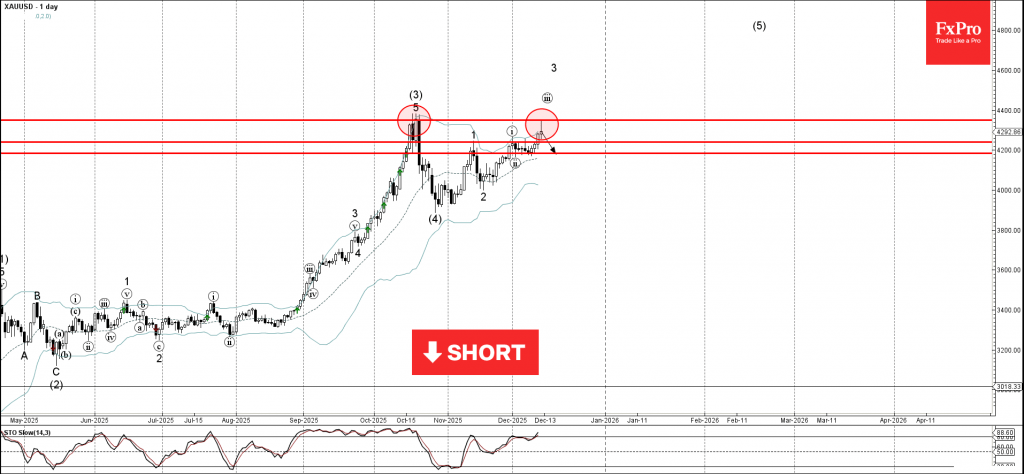

Gold Wave Analysis

Gold: ⬇️ Sell

- Gold reversed from strong resistance level 4350.00

- Likely to fall to support level 4200.00

Gold recently reversed from the resistance area between the strong resistance level 4350.00 (which stopped sharp wave (3) in October) and the upper daily Bollinger Band.

The downward reversal from this resistance area stopped the previous impulse waves iii and 3 of the intermediate impulse wave (5).

Given the strength of the resistance level 4350.00 and the overbought daily Stochastic, Gold can be expected to fall to the next support level 4200.00.

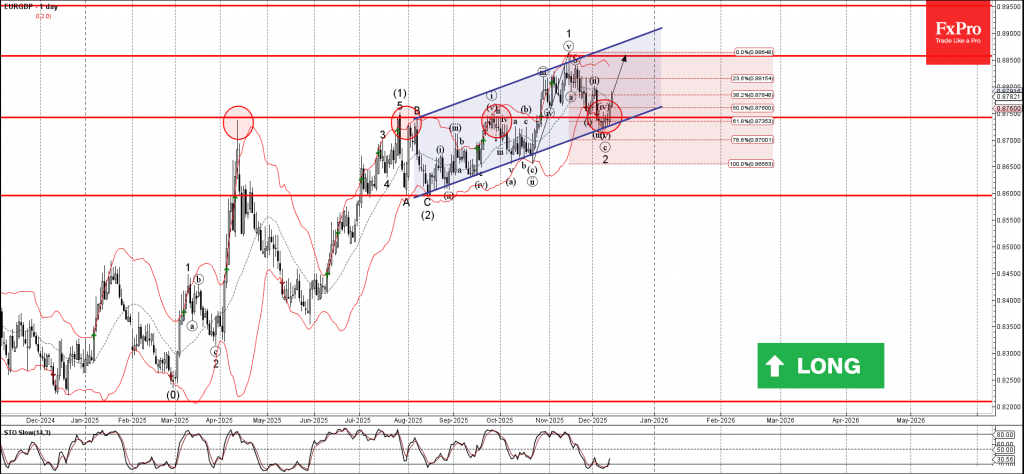

EURGBP Wave Analysis

EURGBP: ⬆️ Buy

- EURGBP reversed from support zone

- Likely to rise to resistance level 0.8850

EURGBP currency pair recently reversed up from the support zone between the strong support level 0.8745 (former resistance from April, July and October) and the lower daily Bollinger Band.

This support zone was strengthened by the support trendline of the daily up channel from July and by the 61.8% Fibonacci correction of the upward impulse from October.

Given the strong daily uptrend, EURGBP currency pair can be expected to rise to the next resistance level 0.8850 (which stopped earlier impulse wave 1).

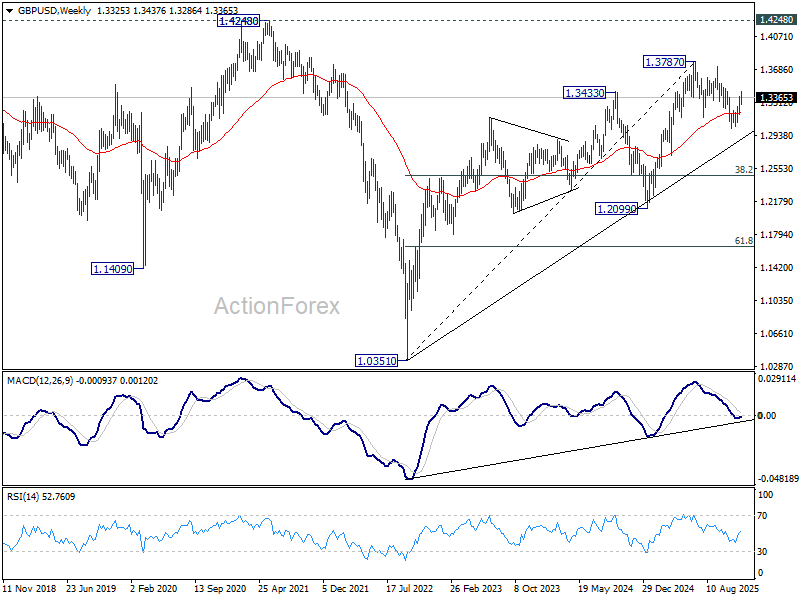

GBP/USD Weekly Outlook

GBP/USD's rally from 1.3008 extended to 1.3438 last week but retreated from there. Initial bias remains neutral this week first. Further rally is expected as long as 1.3286 support holds. As noted before, fall from 1.3787 should have completed as a three-wave correction to 1.3008. Above 1.3428 and firm break of 1.3470 resistance will pave the way back to retest 1.3787 high. However, sustained break of 1.3286 support will mix up the near term outlook.

In the bigger picture, current development suggests that fall from 1.3787 is merely a corrective move, and larger rise from 1.0351 (2022 low) is still in progress. Firm break of 1.3787 will target 1.4248 (2021 high) key structural resistance. This will remain the favored case as long as target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 holds, in case of another fall.

In the long term picture, as long as 1.4248/4480 resistance zone holds (38.2% retracement of 2.1161 to 1.0351 at 1.4480), the long term outlook will remain bearish. That is, price actions from 1.3051 are seen as a corrective pattern to down trend from 2.1161 (2007 high) only. Nevertheless, decisive break of 1.4248/4480 will be a strong sign of long term bullish reversal.