Sample Category Title

Sunset Market Commentary

Markets

Two of Wednesday’s dissenters at the Fed hit the wires today. Goolsbee and Schmid both favoured to keep the rate steady but it appears both had a different angle to do so. Schmid wants to keep monetary policy slightly restrictive, citing a balanced labour market but too high inflation and an economy that’s showing momentum. Goolsbee on the other hand was simply concerned on frontloading cuts too much. He wanted to wait till Q1 after some “concerning” inflation data prior to the shutdown. He went on to say he’s projecting more cuts than the median and thinks rates can come down “a significant amount” next year. Neither policymaker had a material impact on (short-term) US rates though. We do see some (natural?) bear steepening of global curves in an otherwise quiet trading session. Long-end yields rise up to 5 bps in the US and around 4 bps in Europe and the UK. European stocks inch higher with the EuroStoxx50 now just a sigh away from its November record high. Tech on WS underperforms following Broadcom’s (lofty) sales outlook miss but declines for the likes of the Nasdaq are limited to 0.3%. The dollar recovers some ground after a two-day beating. EUR/USD trades near 1.173, DXY grinds higher to 98.48. Sterling extends yesterday’s losses after a poor set of economic data this morning in which the surprising monthly GDP drop stood out. EUR/GBP recovers the previously lost support area at 0.8769.

Today’s poor economic calendar puts the spotlight on the one of the coming week. The US publishes November payrolls on Tuesday along with October retail sales and December PMIs that day. November inflation figures are scheduled on Thursday. They carry big value coming after a Fed that cut rates for a third time this week but basically moved in the dark due to the lack of economic input. They’ll certainly shape market expectations for the Fed in early 2026. We consider a weak(er than expected) batch to have the bigger moving potential (ie. lower US rates and dollar) by markets upping the ante for January. The Bank of Japan’s Q4 Tankan on Monday should convince the remaining (if any) doubters on upcoming rate hike at Friday’s policy meeting. Inflation figures are published the same day and will be an above 2% target reading for the umpteenth month running. The UK central bank meets and likely lowers rates to 3.75%. The BoE has to move cautiously though with November inflation - released on Wednesday - expected to be trending north of 3% still. UK PMI business confidence and the October labour market report is on tap Tuesday. The ECB by Thursday will also have a new set of PMIs at its disposal. President Lagarde already hinted earlier this week at another upgrade to the growth forecasts, cementing the case for a 2% deposit rate for longer. She might get grilled on the impact of the carbon tax being postponed on the inflation outlook in 2027. It could push inflation below target but we expect the central bank look through it since it is out of monetary reach. Additionally, having the tax postponed could also be considered as a positive demand shock that at least partially replaces the cost push shock.

News & Views

The Bank of England published its quarterly Inflation Attitudes Survey, conducted by Ipsos. The perception of the UK inflation rate amongst surveyed residents stood at 4.7%, slightly less than the 4.8% in August. Inflation expectations for the next 12 months, the 12 months thereafter and the long-term (5-yr) were all 0.1 ppt lower as well at respectively 3.5%, 3.3% and 3.7%. When asked about the future path of interest rates, 38% of respondents expected rates to rise over the next 12 months, up from 33%. 24% said they expected rates to stay about the same over the next twelve months (from 26%) and 25% said they expected rates to decline over the next twelve months (from 29%). Respondents were also asked to assess the way the Bank of England is ‘doing its job to set interest rates to control inflation’. The net satisfaction balance, the proportion satisfied minus the proportion dissatisfied, was -1%, down from 2% in August.

SEB research’s quarterly investor survey, targeting large Swedish institutional fixed income investors, showed all respondents expected an unchanged Riksbank policy rate at 1.75% in December and January. For December 2026, policy rate expectations shift to the upside. 40% of the respondents predict at least one rate hike, while the share expecting a rate cut have increased only slightly to 28% (from 24% in June). For December 2027, expectations for rate hikes dominate even more. A broad majority (72%) expect the policy rate to be above the current level (1.75%), while the share predicting a policy rate below declines to 12%. The median expectation for the policy rate is 2.25%.

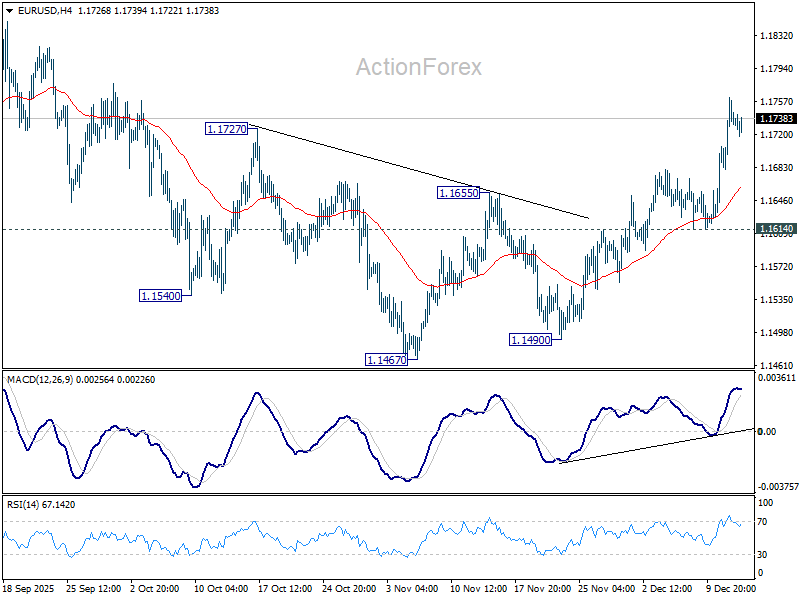

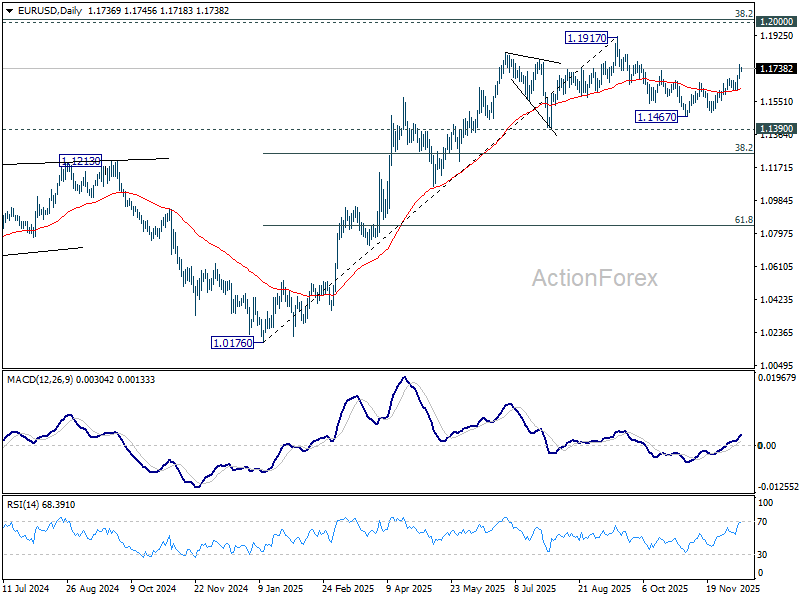

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1692; (P) 1.1727; (R1) 1.1773; More….

Intraday bias in EUR/USD remains on the upside as rise from 1.1467 is in progress. Current development suggests that fall from 1.1917 has completed as a correction to 1.1467. Further rally should be seen to retest 1.1917 high. For now, risk will stay on the upside as long as 1.1614 support holds, in case of retreat.

In the bigger picture, as long as 55 W EMA (now at 1.1346) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will carry larger bullish implication. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

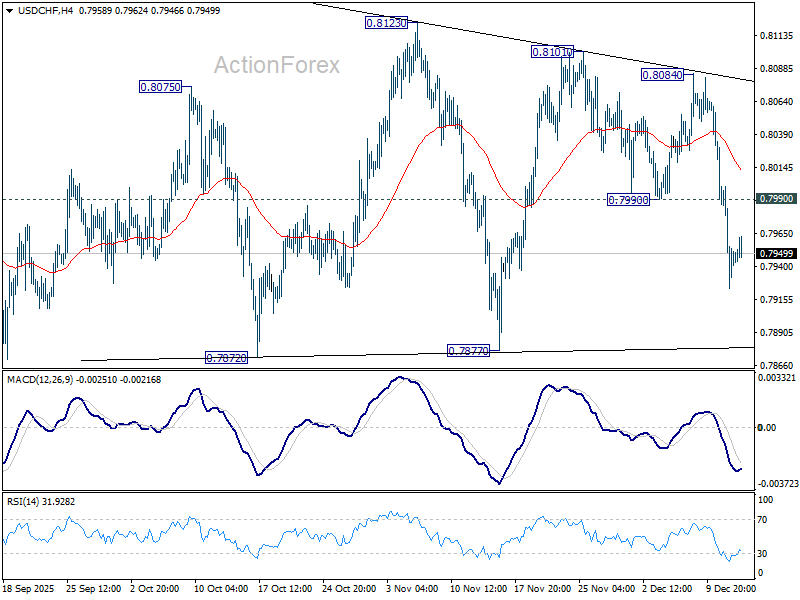

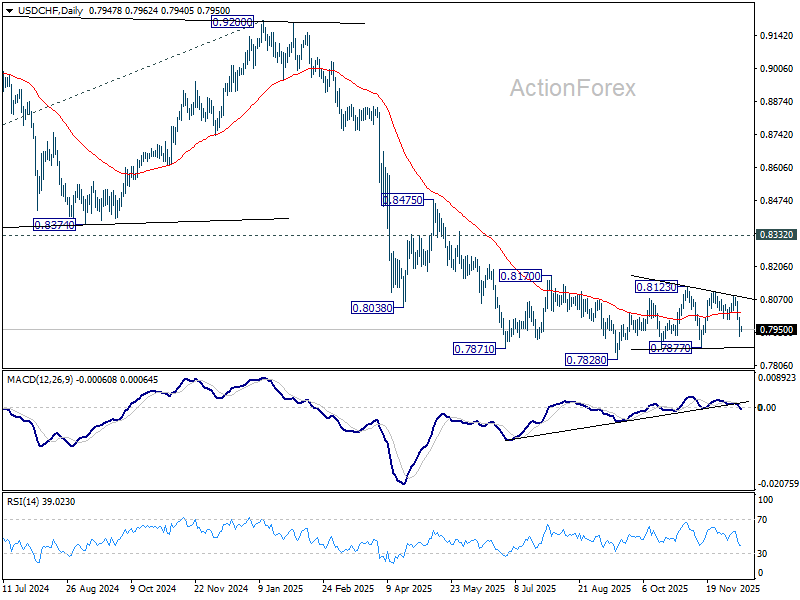

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7917; (P) 0.7961; (R1) 0.7998; More…

Intraday bias in USD/CHF stays on the downside for 0.7877 support. Firm break there will argue that large down trend is ready to resume through 0.7828 low. ON the upside, though above 0.7990 support turned resistance will turn intraday bias neutral again first. Overall, price actions from 0.7828 are seen as a corrective pattern that might still extend further.

In the bigger picture, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low). Long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382.

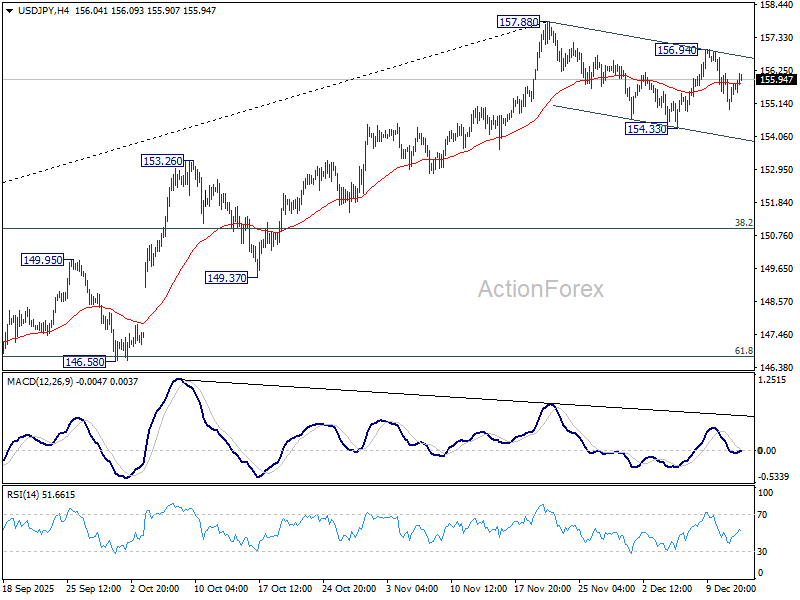

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 154.95; (P) 155.56; (R1) 156.17; More...

Intraday bias in USD/JPY remains neutral as consolidations from 157.88 continues. On the downside, break of 154.33 will target 55 D EMA (now at 153.58) and possibly below. On the upside, above 156.94 will bring retest of 157.88. Firm break there will resume whole rally from 139.87 to 158.85 key structural resistance.

In the bigger picture, corrective pattern from 161.94 (2024 high) could have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. Decisive break of 158.85 structural resistance will solidify this bullish case and target 161.94 for confirmation. On the downside, break of 150.90 resistance turned support will dampen this bullish view and extend the corrective range pattern with another falling leg.

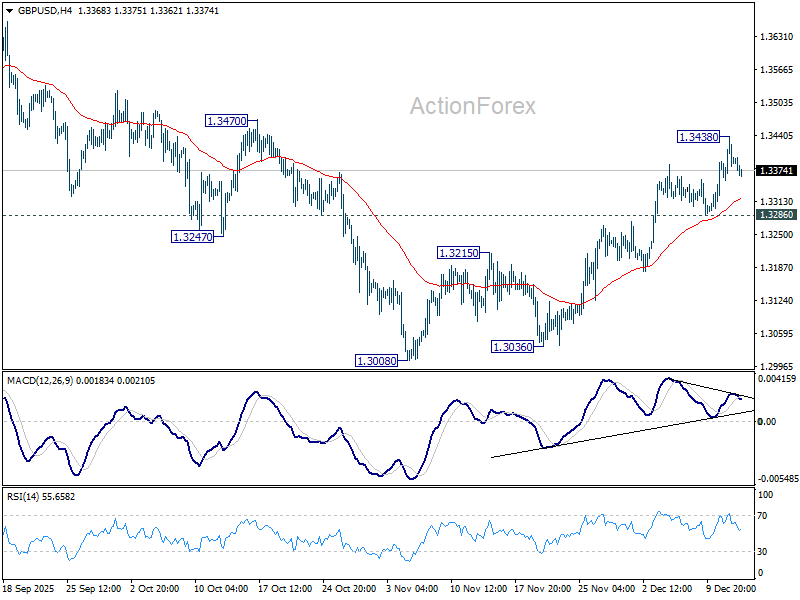

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3349; (P) 1.3393; (R1) 1.3432; More...

Intraday bias in GBP/USD is turned neutral with current retreat, and some consolidations would be seen below 1.3438 temporary top. But further rally is expected with 1.3286 support intact. As noted before, fall from 1.3787 should have completed as a three-wave correction to 1.3008. Above 1.3438 will target 1.3470 resistance. Firm break there will pave the way to retest 1.3787 high.

In the bigger picture, current development suggests that fall from 1.3787 is merely a corrective move, and larger rise from 1.0351 (2022 low) is still in progress. Firm break of 1.3787 will target 1.4248 (2021 high) key structural resistance. This will remain the favored case as long as target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 holds, in case of another fall.

Dollar Attempts Late-Week Recovery, Fed Dissent Fails to Shift Outlook

Dollar edged modestly higher into the final US session of the week, though follow-through remains limited. The rebound looks more like position adjustment than conviction, with markets reluctant to chase the greenback ahead of next week’s key data.

Attention briefly turned to fresh remarks from two Fed officials who dissented against this week’s 25bps rate cut. Chicago Fed President Austan Goolsbee struck a relatively measured tone, stressing a preference to wait for more inflation data before easing further rather than opposing cuts outright. By contrast, Kansas City Fed President Jeffrey Schmid reiterated a firmer stance, arguing policy before the cut was already appropriate and not overly restrictive.

Despite the hawkish pushback, market reaction was muted. Investors appear comfortable with the Fed’s current trajectory, seeing the dissent as part of an ongoing internal debate rather than a signal of an imminent policy shift. A January pause remains the base case, while pricing for a March cut still sits close to a coin toss.

In weekly FX performance, Yen remains pinned to the bottom, followed by Dollar. Sterling slipped to third weakest after today’s UK GDP disappointment. Swiss Franc leads after the SNB signaled earlier in the week no urgency to return to negative rates, with Euro second-best and Kiwi following. Loonie and Aussie remain stuck in the middle.

That distribution reflects a mixed but balanced risk backdrop. Traditional US stocks continue to draw support from expectations of extended Fed easing into next year, while tech shares remain capped by lingering AI valuation concerns, keeping overall sentiment from tilting decisively in either direction.

In Europe, at the time of writing, FTSE is down -0.06%. DAX is up 0.24%. CAC is up 0.62%. UK 10-year yield is up 0.002 at 4.514. Germany 10-year yield is up 0.021 at 2.868. Earlier in Asia, Nikkei rose 1.37%. Hong Kong HSI rose 1.75%. China Shanghai SSE rose 0.41%. Singapore Strait Times rose 1.45%. Japan 10-year JGB yield rose 0.024 to 1.955.

Fed's Schmid: Policy not overly restrictive before rate cut

Kansas City Fed President Jeffrey Schmid explained his dissent at this week’s FOMC meeting, where he voted to keep rates unchanged. He said in a statement his assessment of the economy has not shifted meaningfully since October, citing "continued momentum" in activity and inflation that remains above comfort levels.

Schmid described inflation as “too high” and the labor market as cooling but still “largely in balance.” In that context, his preference is to maintain monetary policy in a "modestly restrictive" setting rather than ease prematurely.

Addressing debate around policy restrictiveness, Schmid downplayed reliance on theoretical estimates of the neutral rate, calling r* an academic concept without a real-world equivalent. Instead, he said policy should be judged by "how the economy actually evolves". From both incoming data and business contacts, he sees an economy that is "showing momentum and inflation that is too hot", suggesting that policy is "not overly restrictive".

Fed's Goolsbee: Waiting for more data the “wiser choice”

Chicago Fed President Austan Goolsbee explained his dissent at this week’s FOMC meeting, where he voted to hold rates rather than support the 25bps cut. He said policymakers should have waited for more incoming data, particularly on inflation, arguing that delaying the decision into the new year "would not have entailed much additional risk" and would have allowed the Fed to assess a more complete set of economic readings.

In a statement, Goolsbee noted that feedback from businesses and consumers in his district consistently points to prices as "a main concern". At the same time, he described the broader economy as showing stable growth, with a labor market that is “only moderately cooling”. He characterized the current environment as one of “low hiring, low firing,” suggesting firms are responding to uncertainty rather than a traditional cyclical slowdown.

While acknowledging that recent inflation pressures may be linked largely to tariffs and could ultimately prove "transitory", Goolsbee cautioned against assuming that outcome too quickly. He reiterated optimism that interest rates can fall meaningfully over the coming year, but stressed discomfort with heavily front-loading cuts.

UK GDP contracts -0.1% mom in October as services drag deepens

UK GDP contracted by -0.1% mom in October, undershooting expectations for a 0.1% gain and marking a third consecutive month of stagnation or contraction. The economy had already shrunk by -0.1% in September after flat growth in August, reinforcing concerns that momentum is fading as the year draws to a close.

The monthly breakdown was weak across key domestic sectors. Services output fell -0.3% mom and construction declined -0.6%, offsetting a 1.1% rise in production. The continued softness in services is particularly concerning given its dominant share of UK economic activity.

On a three-month basis, GDP fell -0.1% in the period to October compared with the previous three months. Services recorded no growth, extending the recent trend of slowing activity, while production output dropped -0.5% due largely to weaker motor vehicle manufacturing. Construction also declined by -0.3%.

New Zealand BNZ manufacturing improves to 51.1, but momentum still modest

New Zealand’s BNZ Performance of Manufacturing Index edged up from 51.2 to 51.4 in November, remaining in expansionary territory but still below the long-run average of 52.4.

Production strengthened from 52.0 to 52.8, while employment rebounded sharply from contractionary 48.3 to 52.4, suggesting manufacturers are becoming more confident about staffing needs. That said, new orders softened notably, slipping from 54.5 to 51.9, highlighting lingering caution about the sustainability of demand beyond the seasonal boost.

Survey commentary was more encouraging. The share of negative comments fell to 45.6% from 54.1% in October and 60.2% in September. Respondents cited stronger Christmas-related demand, improving economic conditions, rising customer confidence, and a pickup in both domestic and overseas orders, alongside firmer construction activity and new product launches.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3349; (P) 1.3393; (R1) 1.3432; More...

Intraday bias in GBP/USD is turned neutral with current retreat, and some consolidations would be seen below 1.3438 temporary top. But further rally is expected with 1.3286 support intact. As noted before, fall from 1.3787 should have completed as a three-wave correction to 1.3008. Above 1.3438 will target 1.3470 resistance. Firm break there will pave the way to retest 1.3787 high.

In the bigger picture, current development suggests that fall from 1.3787 is merely a corrective move, and larger rise from 1.0351 (2022 low) is still in progress. Firm break of 1.3787 will target 1.4248 (2021 high) key structural resistance. This will remain the favored case as long as target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 holds, in case of another fall.

Fed’s Schmid: Policy not overly restrictive before rate cut

Kansas City Fed President Jeffrey Schmid explained his dissent at this week’s FOMC meeting, where he voted to keep rates unchanged. He said in a statement his assessment of the economy has not shifted meaningfully since October, citing "continued momentum" in activity and inflation that remains above comfort levels.

Schmid described inflation as “too high” and the labor market as cooling but still “largely in balance.” In that context, his preference is to maintain monetary policy in a "modestly restrictive" setting rather than ease prematurely.

Addressing debate around policy restrictiveness, Schmid downplayed reliance on theoretical estimates of the neutral rate, calling r* an academic concept without a real-world equivalent. Instead, he said policy should be judged by "how the economy actually evolves". From both incoming data and business contacts, he sees an economy that is "showing momentum and inflation that is too hot", suggesting that policy is "not overly restrictive".

Fed’s Goolsbee: Waiting for more data the “wiser choice”

Chicago Fed President Austan Goolsbee explained his dissent at this week’s FOMC meeting, where he voted to hold rates rather than support the 25bps cut. He said policymakers should have waited for more incoming data, particularly on inflation, arguing that delaying the decision into the new year "would not have entailed much additional risk" and would have allowed the Fed to assess a more complete set of economic readings.

In a statement, Goolsbee noted that feedback from businesses and consumers in his district consistently points to prices as "a main concern". At the same time, he described the broader economy as showing stable growth, with a labor market that is “only moderately cooling”. He characterized the current environment as one of “low hiring, low firing,” suggesting firms are responding to uncertainty rather than a traditional cyclical slowdown.

While acknowledging that recent inflation pressures may be linked largely to tariffs and could ultimately prove "transitory", Goolsbee cautioned against assuming that outcome too quickly. He reiterated optimism that interest rates can fall meaningfully over the coming year, but stressed discomfort with heavily front-loading cuts.

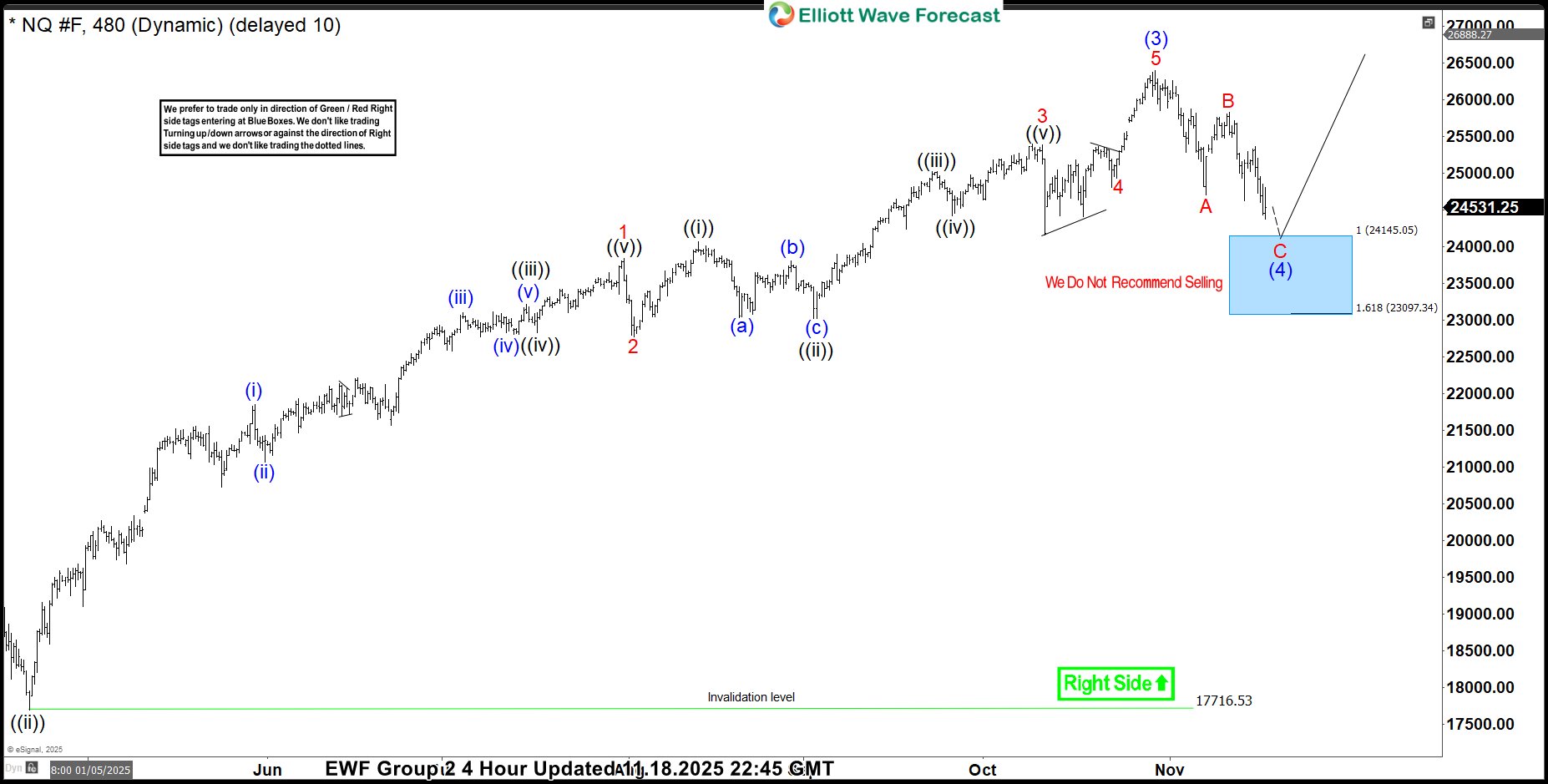

NASDAQ (NQ_F) Elliott Wave: Buying the Dips in a Blue Box

Hello traders. As our members know we have had many profitable trading setups recently. In this technical article, we are going to talk about another Elliott Wave trading setup we got in E-mini Nasdaq-100 Futures. Recently NQ_F made a clear three-wave correction. The pull back completed as Elliott Wave Double Three pattern and made a decent rally. In this discussion, we’ll break down the Elliott Wave pattern and present targets. Let’s start by explaining the pattern.

NQ_F Elliott Wave 4 Hour Chart 11.18.2025

The Futures is forming a 3-wave pullback in wave (4) blue. At the moment, we can see incomplete sequences from the main peak, labeled as wave (3) blue. Our members know that we constantly emphasize the importance of incomplete sequences, as these determine the market’s path.

The structure suggests more weakness toward the Equal Legs area at 24145–23097, where we are looking to re-enter as buyers. We expect at least a three-wave bounce from the Blue Box area.

NQ_F Elliott Wave 4 Hour Chart 12.11.2025

E-mini Nasdaq-100 Futures found buyers as expected at the Blue Box area, making decent bounce. While above the last low 23905 low we count (4) blue correction completed. Wave (5 ) can be in progress toward new highs, targeting 26989 area.

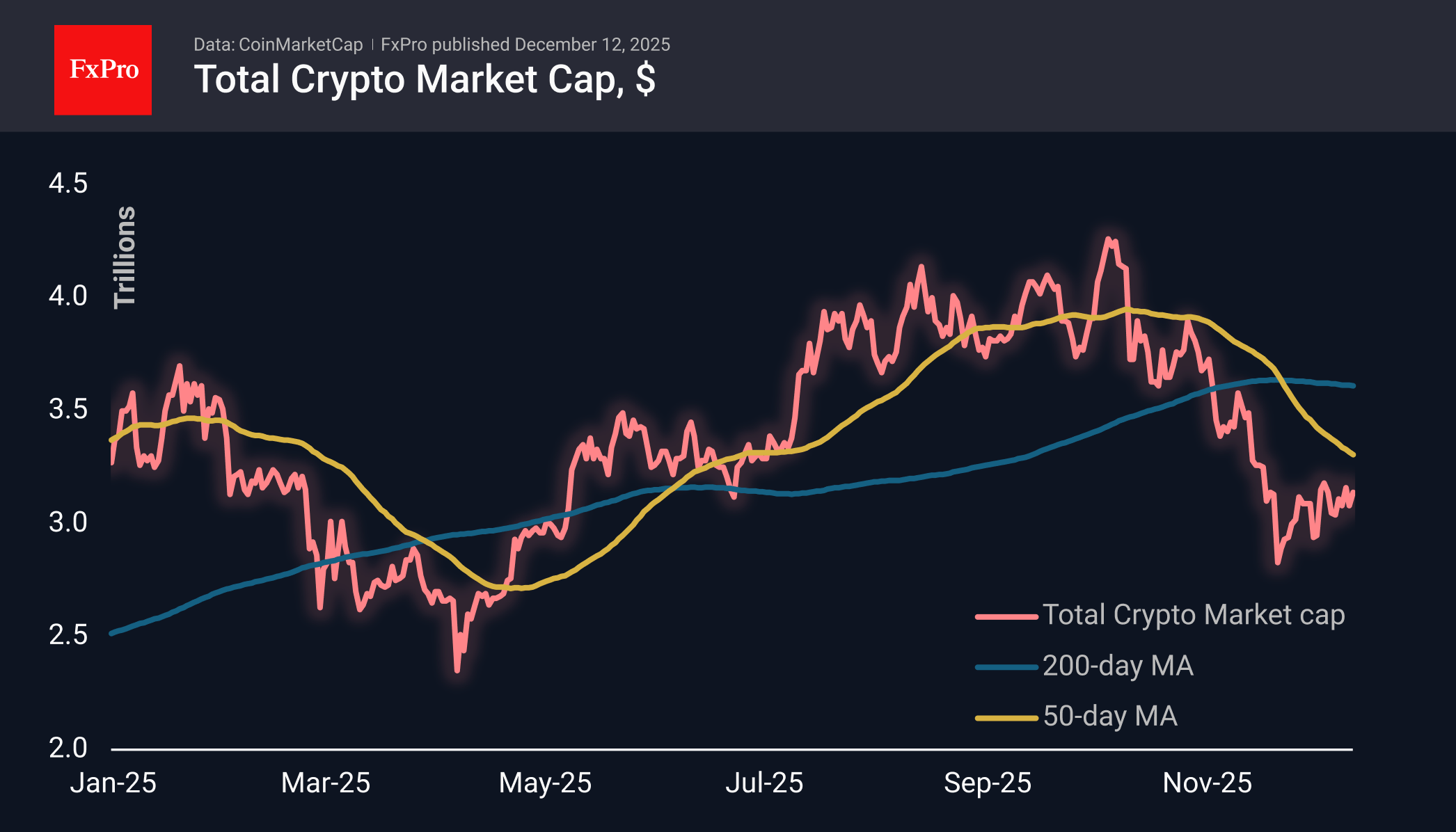

Crypto: Slight Rebound Within a Bear Market

Market Overview

The crypto market capitalisation gained about 2%, returning to the $3.14T level. The good news is that the latest local low fits into the upward trend of higher lows since the end of November. The bad news is that resistance near $3.20T has remained in place all this time. The spring is compressing, promising an end to the relative calm in the next few days. The market will need to decide on a direction for the coming weeks.

The cryptocurrency sentiment index has been stuck at 29 for the last two days, its highest level since early November. The exit from the zone of extreme fear and the prolonged period of calm are working in favour of the bulls, significantly increasing the chances of a bullish rally soon. At the same time, we continue to believe that cryptocurrencies have already entered a bear market, and a price recovery will attract more sellers.

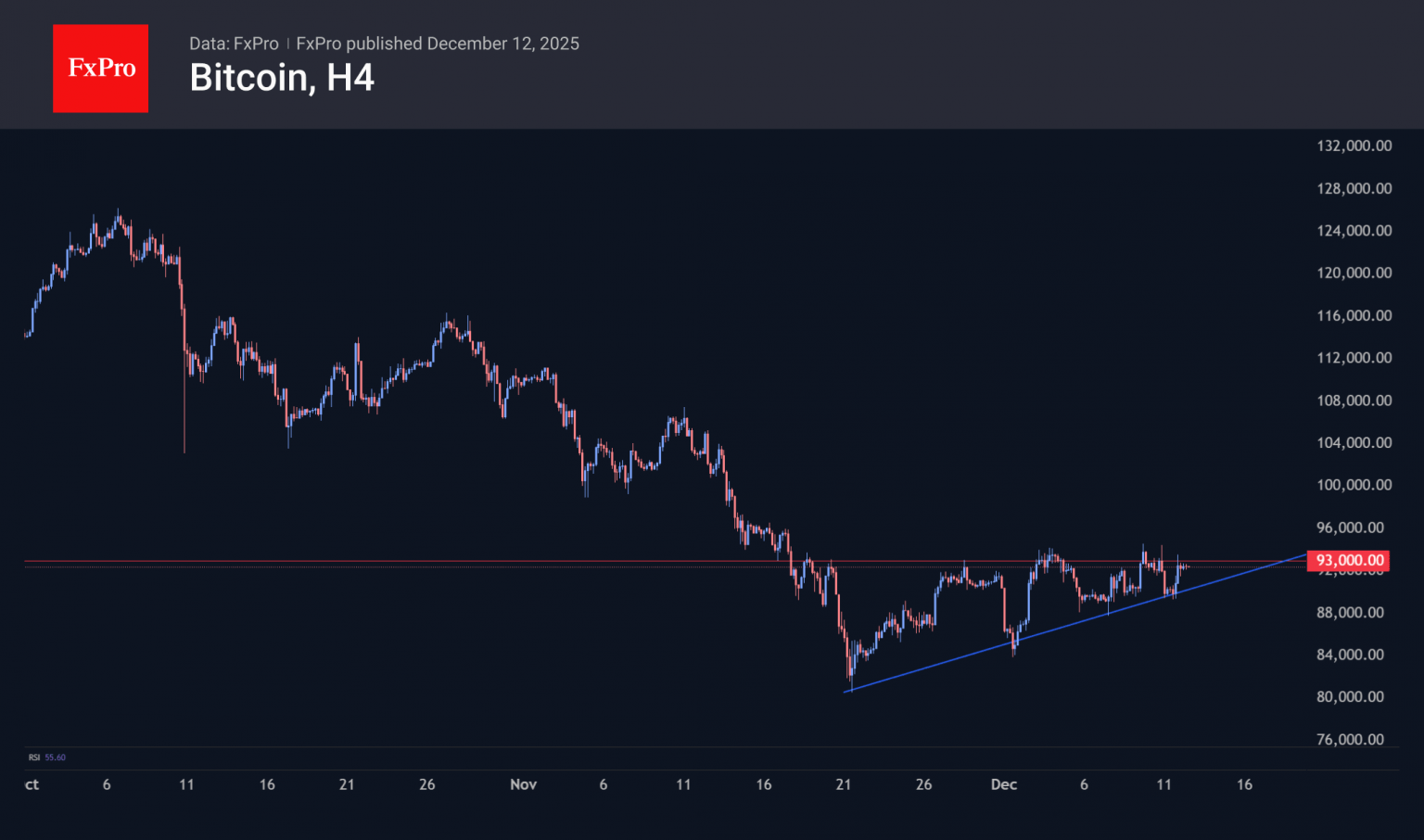

Bitcoin continues to find support on dips, but, like the rest of the market, is facing horizontal resistance. This dynamic suggests that since the end of November, a rebound in the bear market has occurred, and a new downward momentum will likely follow soon.

News Background

The crypto market is showing signs of cautious optimism but has yet to fully recover from the effects of the October 10 crash, according to Block Scholes.

Bitcoin needs to consolidate above $95,000 to break out of the bearish trend, according to Glassnode. Without this, the asset will remain overly vulnerable to macroeconomic events.

The Fed’s key rate cut was insufficient to stimulate growth in the cryptocurrency market. The situation adds uncertainty and dashes hopes for the traditional ‘Santa Claus rally,’ Coin Bureau notes.

The main driver of growth for the first cryptocurrency is a decline in seller activity. The daily inflow of coins to exchanges has decreased fourfold since November 21, to 21,000 BTC. Bitcoin could rise to $112,000 in the next one to three months, but for this to happen, the Fed must ease its monetary policy, according to CryptoQuant.

The entry of institutional investors into the crypto market has buried the chances of an alt season. Risk-prone retail traders have shifted to the stock market, where they trade shares of high-volatility companies, Gemini notes.

According to Arkham, Tom Lee’s BitMine company bought 33,504 ETH for a total of $112 million. The deal took place against the backdrop of the Fed’s decision to cut its key rate for the third consecutive time.

In 2025, 117 new companies added Bitcoin to their reserves; however, the overall trend towards adopting the first cryptocurrency is losing momentum, according to CryptoQuant.