Sample Category Title

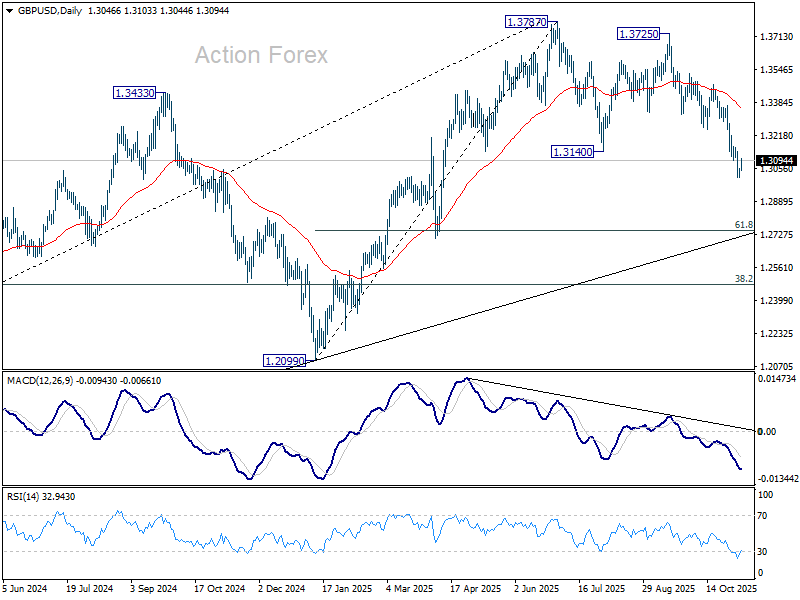

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3023; (P) 1.3038; (R1) 1.3067; More...

GBP/USD's recovery from 1.3008 temporary extends higher, but stays well below 1.3247 support turned resistance. Intraday bias remains neutral and further decline is expected. On the downside, break of 1.3008 will resume the fall from 1.3787 and target 61.8% retracement of 1.2099 to 1.3787 at 1.2744. Sustained break there will pave the way to 1.2099 support next.

In the bigger picture, the break of 55 W EMA (now at 1.3185) is taken as the first sign that corrective rise from 1.0351 (2022 low) has completed. Decisive break of trend line support (now at 1.2780) will solidify this case and target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 next. Meanwhile, in case of another rise, strong resistance should emerge below 1.4248 (2021 high) to cap upside to preserve the long term down trend.

Sterling Slightly Firmer After Tight BoE Hold; Dollar Eases Broadly

Sterling traded mildly higher following the BoE’s decision to keep interest rates unchanged at 4.00% in a tight 5–4 vote. Overall market reaction was modest as the Pound gained slightly against the Dollar but lacked strong momentum, as traders viewed the decision and accompanying remarks as broadly balanced.

At the post-meeting press conference, Governor Andrew Bailey emphasized that future policy adjustments would hinge on two key factors: the persistence of inflation and the degree of slack in the economy. He noted that inflation remains “well above the Bank’s 2% target” and warned that price expectations could stay elevated, keeping inflation higher for longer. At the same time, he acknowledged that economic activity is running below potential, with falling vacancies and stalling employment growth signaling softer demand.

Bailey added that the Bank will have access to more data on inflation and cost pressures before the next MPC meeting in December. Importantly, policymakers will also be able to assess how the upcoming Budget — expected to deliver a contractionary fiscal impulse — will affect the economic outlook and inflation path.

Elsewhere, Dollar weakened broadly, retracing part of this week’s advance. There was no single catalyst for the decline, though traders appeared to be unwinding long Dollar positions after a string of U.S. data releases, including ISM surveys and ADP employment, failed to provide a clear directional signal.

Fed funds futures continue to price a roughly 67% chance of a December rate cut, keeping monetary expectations anchored for now. U.S. equity futures point to a flat Wall Street open, reflecting a cautious tone too.

In weekly performance terms, Japanese Yen remains the strongest currency, followed by Dollar and Euro. Kiwi is at the bottom, trailed by Loonie and Aussie. Swiss Franc and Sterling sit in the middle of the pack.

In Europe, at the time of writing, FTSE is down -0.17%. DAX is down -0.18%. CAC is down -0.54%. UK 10-year yield is down -0.016 at 4.449. Germany 10-year yield is down -0.002 at 2.675. Earlier in Asia, Nikkei rose 1.34%. Hong Kong HSI rose 2.12%. China Shanghai SSE rose 0.7%. Singapore Strait Times rose 1.54%. Japan 10-year JGB yield rose 0.017 to 1.684.

BoE holds at 4.00% in 5–4 vote, inflation peaked, risk more balanced

The BoE held its Bank Rate steady at 4.00% today, as expected, but the 5–4 vote split revealed persistent pressure within the Monetary Policy Committee to continue easing. Governor Andrew Bailey and four others — Megan Greene, Clare Lombardelli, Catherine Mann, and Huw Pill — voted to maintain the current rate. Sarah Breeden, Swati Dhingra, Dave Ramsden, and Alan Taylor backed a 25bps cut. The close decision underscores a deeply divided committee as policymakers weigh the trade-off between disinflation progress and weakening demand.

In its accompanying statement, the BoE acknowledged that headline CPI inflation has peaked, while “progress on underlying disinflation continues.” The Bank noted that the risk of persistent inflation has diminished, while the threat from weaker demand has become more evident — marking a clear shift toward a more balanced risk assessment.

Updated projections painted a mixed picture. The BoE now expects GDP growth of 1.4% in Q4 2025 (down slightly from 1.5%) and the same pace in 2026, before picking up modestly to 1.7% in 2027 and 1.8% in 2028. .

On inflation, the outlook remains largely unchanged: CPI is projected at 3.5% in Q4 2025, easing to 2.5% in 2026 and 2.0% by 2027, with a slight uptick to 2.1% in 2028. The forecasts imply the BoE expects inflation to remain anchored near target in the medium term, providing scope for gradual easing once confidence in disinflation deepens.

Market-implied rates show investors expect the Bank Rate to drift lower toward 3.9% by the end of the year, 3.5% through 2026–27, and 3.6% by 2028.

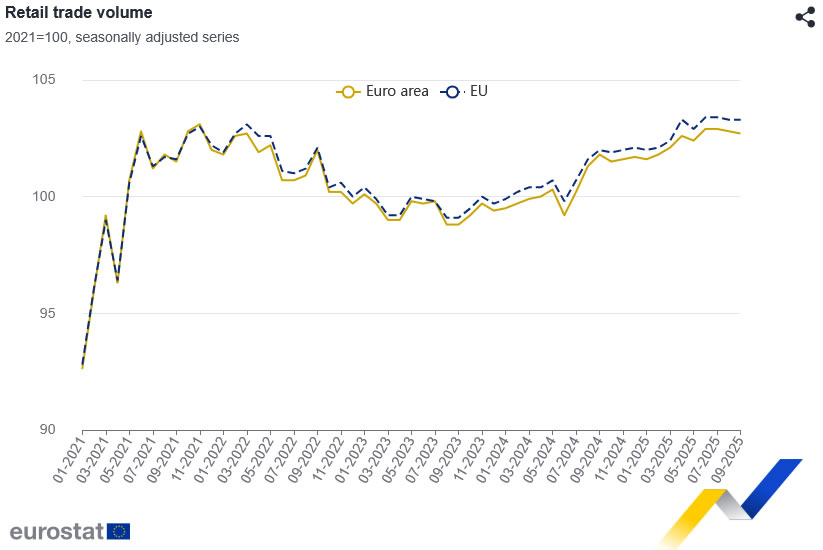

Eurozone retail sales slip -0.1% mom as non-food demand softens

Eurozone retail sales disappointed in September, falling -0.1% mom, missing expectations of a 0.2% gain. The decline was driven mainly by weaker spending on non-food items, which slipped -0.2%, and a sharp -1.0% drop in automotive fuel sales. Meanwhile, sales of food, drinks, and tobacco were unchanged.

Across the broader EU, retail sales managed a modest 0.1% monthly rise, masking divergent trends among member states. The steepest declines were seen in Lithuania (-1.1%), Latvia and Slovenia (-0.7%), and Italy (-0.6%), while Luxembourg and Malta (+1.7%), along with Estonia (+1.5%) and Slovakia (+1.4%), posted strong rebounds.

Japan wage growth at 1.9%, but real income falls for ninth month

Japan’s real wages declined for a ninth consecutive month in September as inflation-adjusted earnings fell -1.4% yoy, following a revised -1.7% drop in August, extending a contraction streak that began in January.

Nominal wages rose 1.9% yoy, slightly below expectations of 2.0% and well short of the 3.4% increase in consumer prices, which accelerated for the first time since April.

While regular pay rose 1.9% yoy, matching August’s pace, and overtime pay ticked up to 0.6% yoy, these gains were insufficient to offset higher living costs. Special payments, largely seasonal bonuses, rose 4.5% after a -7.8% fall in August, offering some temporary relief.

Japan’s PMI composite finalized at 51.5, price risks intensify

Japan’s PMI Services was finalized at 53.1 in October, slightly below September’s 53.3. PMI Composite edged up to 51.5 from 51.3 as strength in services offset continued weakness in manufacturing.

According to Annabel Fiddes, Economics Associate Director at S&P Global Market Intelligence, the survey signaled “further solid expansion” in services output, though other indicators were “not quite as upbeat.”

New business growth slowed sharply, expanding at its weakest pace in 16 months, and foreign demand remained in contraction. At the same time, inflationary pressures intensified, with both input and output prices rising faster, largely due to higher labor costs. Confidence also softened as firms expressed concern about labor shortages and subdued customer demand.

The main risk now lies in intensifying price pressures in both manufacturing and services, which "will be important to monitor in the coming months".

RBNZ’s Hawkesby: Slowdown within expectations, not out of the worst yet

RBNZ Governor Christian Hawkesby said the recent deterioration in the country’s labour market was within expectations. Speaking before a parliamentary committee, Hawkesby noted that the rise in unemployment to its highest level since 2016 reflects where the economy stands in the current cycle. “It is hard out there,” he said, adding that the RBNZ expected this period of softness as part of the adjustment following its recent easing moves.

Despite the alignment with forecasts, Hawkesby warned that risks remain elevated, citing a long list of concerns led by global trade fragmentation and intensifying trade wars. He remarked that “we don’t think we’re out of the worst yet,” pointing to persistent global uncertainty that continues to cloud the medium-term outlook.

The Governor also described New Zealand as a multi-speed economy, with regions and industries responding differently to the current slowdown. While some sectors continue to show resilience, others are struggling under higher costs and weaker demand.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3023; (P) 1.3038; (R1) 1.3067; More...

GBP/USD's recovery from 1.3008 temporary extends higher, but stays well below 1.3247 support turned resistance. Intraday bias remains neutral and further decline is expected. On the downside, break of 1.3008 will resume the fall from 1.3787 and target 61.8% retracement of 1.2099 to 1.3787 at 1.2744. Sustained break there will pave the way to 1.2099 support next.

In the bigger picture, the break of 55 W EMA (now at 1.3185) is taken as the first sign that corrective rise from 1.0351 (2022 low) has completed. Decisive break of trend line support (now at 1.2780) will solidify this case and target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 next. Meanwhile, in case of another rise, strong resistance should emerge below 1.4248 (2021 high) to cap upside to preserve the long term down trend.

BoE holds at 4.00% in 5–4 vote, inflation peaked, risk more balanced

The BoE held its Bank Rate steady at 4.00% today, as expected, but the 5–4 vote split revealed persistent pressure within the Monetary Policy Committee to continue easing. Governor Andrew Bailey and four others — Megan Greene, Clare Lombardelli, Catherine Mann, and Huw Pill — voted to maintain the current rate. Sarah Breeden, Swati Dhingra, Dave Ramsden, and Alan Taylor backed a 25bps cut. The close decision underscores a deeply divided committee as policymakers weigh the trade-off between disinflation progress and weakening demand.

In its accompanying statement, the BoE acknowledged that headline CPI inflation has peaked, while “progress on underlying disinflation continues.” The Bank noted that the risk of persistent inflation has diminished, while the threat from weaker demand has become more evident — marking a clear shift toward a more balanced risk assessment.

Updated projections painted a mixed picture. The BoE now expects GDP growth of 1.4% in Q4 2025 (down slightly from 1.5%) and the same pace in 2026, before picking up modestly to 1.7% in 2027 and 1.8% in 2028. .

On inflation, the outlook remains largely unchanged: CPI is projected at 3.5% in Q4 2025, easing to 2.5% in 2026 and 2.0% by 2027, with a slight uptick to 2.1% in 2028. The forecasts imply the BoE expects inflation to remain anchored near target in the medium term, providing scope for gradual easing once confidence in disinflation deepens.

Market-implied rates show investors expect the Bank Rate to drift lower toward 3.9% by the end of the year, 3.5% through 2026–27, and 3.6% by 2028.

(BOE) Bank Rate maintained at 4%

Monetary Policy Summary, November 2025

At its meeting ending on 5 November 2025, the Monetary Policy Committee voted by a majority of 5–4 to maintain Bank Rate at 4%. Four members voted to reduce Bank Rate by 0.25 percentage points, to 3.75%.

CPI inflation is judged to have peaked. Progress on underlying disinflation continues, supported by the still restrictive stance of monetary policy. This is reflected in an easing of pay growth and services price inflation. Underlying disinflation is being underpinned by subdued economic growth and building slack in the labour market.

Monetary policy is being set to balance the risks around meeting the 2% inflation target sustainably. The risk from greater inflation persistence has become less pronounced recently, and the risk to medium-term inflation from weaker demand more apparent, such that overall the risks are now more balanced. But more evidence is needed on both.

The restrictiveness of monetary policy has fallen as Bank Rate has been reduced. The extent of further reductions will therefore depend on the evolution of the outlook for inflation. If progress on disinflation continues, Bank Rate is likely to continue on a gradual downward path.

Minutes of the Monetary Policy Committee meeting ending on 5 November 2025

1: Before turning to its immediate policy decision, the Monetary Policy Committee (MPC) discussed key economic developments and its judgements around them, as well as its views on monetary policy strategy. The latest data and analysis underpinning these topics were set out in the accompanying November 2025 Monetary Policy Report.

The Committee’s discussions

2: The Committee’s policy discussions covered: the extent to which disinflation was continuing; the degree of slack emerging in the economy and the extent to which this slack was sufficient to counteract any remaining persistence in underlying inflation; and the extent to which these developments reflected the restrictive stance of monetary policy, both currently and prospectively.

3: Progress on underlying disinflation had continued. Services consumer price inflation had eased. Continued moderation in wage growth was likely to feed through to lower services price inflation, although members continued to take different views on the degree of this pass-through.

4: CPI inflation was judged to have peaked. The increase in headline inflation over the course of this year had been accounted for by base effects in energy prices, as well as one-off factors such as supply disruptions in specific food components and increases in administered prices. In the central projection, this increase in headline inflation did not lead to additional second-round effects on domestic inflationary pressures. However, the Committee was mindful of recent increases in household inflation expectations, and some members continued to place weight on the possibility that structural shifts in wage and price-setting would exacerbate the persistence of underlying inflation.

5: In one scenario set out in Section 3 of the November Monetary Policy Report, inflation was more persistent than assumed in the central projection, as past inflation outturns continued to influence domestic price and wage-setting over the medium term. Among those members who placed weight on upside risks from inflation persistence more generally, there were different views on the most likely mechanism.

6: Looking ahead, contemporaneous indicators of slack, labour costs and services inflation, together with indications of prospective pay settlements and the likely pricing power of firms, would provide important information on the evolution of risks associated with returning CPI inflation to the 2% target sustainably. The Committee would evaluate the accumulation of evidence over time, alongside key upcoming data releases. The Budget would be announced on 26 November.

7: For most members, global developments had not played a large role in their policy deliberations at this meeting, but these would continue to be assessed closely.

8: Underlying disinflation was being underpinned by subdued economic growth and building slack in the labour market. Members had a range of views around the margin of spare capacity that had already emerged and was likely to emerge over time. The labour market was continuing to loosen gradually. For some members, weak growth in consumption and employment indicated the emergence of additional spare capacity. For other members, structural changes in the labour market implied that the margin of spare capacity, its likely evolution, and its implications for nominal dynamics, might prove insufficient to return inflation to target sustainably.

9: In a second scenario set out in the November Report, domestic inflationary pressure faded more quickly than was assumed in the central projection, reflecting more pronounced weakness in household consumption. Most members placed some weight on this scenario.

10: Reflecting the usual lags associated with monetary policy, past restrictiveness was assessed to be weighing on the current level of aggregate demand. This policy restraint was contributing to ongoing disinflation. For those members placing greater weight on downside risks to activity, the combined degree of past and current restrictiveness evident in the latest data risked an inflation undershoot in the medium term. For those members who were more concerned about the persistence of underlying inflationary pressures, there was less evidence that the cumulative restrictiveness imparted by policy to date would generate additional slack in the real economy. All members concurred that the stance of monetary policy had become less restrictive as the level of Bank Rate had been reduced.

11: In considering its approach to the potential removal of remaining policy restrictiveness, the Committee was weighing various considerations. These included the costs associated with loosening policy too quickly or too slowly, and the value in waiting for additional evidence before reducing Bank Rate further. Those considerations reflected different views on the restrictiveness of current monetary policy and on the extent to which incremental news would help resolve uncertainty about the persistence of inflation.

12: Different members placed different weights on how precisely an equilibrium, or neutral, level of Bank Rate could be identified. For some members, the evolution of inflation and other conjunctural data, including what these could reveal about slack, could offer guidance on the restrictiveness of monetary policy. Other members put more weight on quantitative estimates of equilibrium interest rates. There was broad agreement, however, that as Bank Rate approached neutral, the contribution of monetary policy to underlying disinflation would become harder to discern, making the case for further policy easing more finely balanced.

13: Taken together, the recent data suggested that the risk from greater inflation persistence had become less pronounced, and the risk to medium-term inflation from weaker demand more apparent, such that overall the risks were now more balanced. But more evidence was needed on both, and different members placed different weights on these risks.

The immediate policy decision

14: The MPC sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment. The MPC adopts a medium-term and forward-looking approach to determine the monetary stance required to achieve the inflation target sustainably.

15: Five members (Andrew Bailey, Megan Greene, Clare Lombardelli, Catherine L Mann and Huw Pill) preferred to maintain Bank Rate at 4% at this meeting. Four members in this group (Megan Greene, Clare Lombardelli, Catherine L Mann and Huw Pill) placed greater weight on risks of persistence in inflation, requiring more prolonged monetary policy restriction. While there had been some progress in underlying disinflation, these members were concerned that this could stall, as they placed particular weight on the risk of higher inflation expectations or structural shifts leading to inflation persistence. One member in this group (Andrew Bailey) judged that the overall risks to medium-term inflation had moved down to become more balanced recently. But there was value in waiting for further evidence.

16: Four members (Sarah Breeden, Swati Dhingra, Dave Ramsden and Alan Taylor) preferred a 0.25 percentage point reduction in Bank Rate at this meeting. Disinflation had become better established, and current and prospective slack should allow underlying inflation to return to target-consistent rates. These members attached a greater weight to downside risks, given that these would reflect a continuation of current trends, with particular concerns that household saving would remain elevated and weigh on consumption. For two members in this group (Swati Dhingra and Alan Taylor), policy was already significantly over-restrictive, which could unduly damage activity and possibly lead to an undershoot in inflation in the medium term.

17: The Committee judged that the restrictiveness of monetary policy had fallen as Bank Rate had been reduced. The extent of further reductions would therefore depend on the evolution of the outlook for inflation. If progress on disinflation continued, Bank Rate was likely to continue on a gradual downward path.

18: The Chair invited the Committee to vote on the proposition that:

- Bank Rate should be maintained at 4%.

19: Five members (Andrew Bailey, Megan Greene, Clare Lombardelli, Catherine L Mann and Huw Pill) voted in favour of the proposition. Four members (Sarah Breeden, Swati Dhingra, Dave Ramsden and Alan Taylor) voted against this proposition, preferring to reduce Bank Rate by 0.25 percentage points, to 3.75%.

MPC members’ views

20: Members set out the rationale underpinning their individual votes on Bank Rate.

Members are listed alphabetically under each vote grouping. References in parentheses relate to boxes and sections of the November 2025 Monetary Policy Report. References to scenarios relate to those set out in Section 3 of the November Report.

Votes to maintain Bank Rate at 4%

Andrew Bailey: Upside risks to inflation have become less pressing since August, and I see further policy easing to come if disinflation becomes more clearly established in the period ahead. Recent evidence points to building slack in the economy, and the latest CPI data were promising. But this is just one month of data. Labour costs remain elevated and wage growth, while on a downward path of late, may plateau. In assessing the outlook, I find the mechanisms underlying upside risks less convincing than those underlying the downside. Previous negative labour supply shocks could be less important for the trajectory of inflation today (Box F). Firms’ margin rebuilding may be mitigated by weak demand (Box A), and elevated household inflation expectations may have more limited impact (Box B). The downside scenario seems more likely. It could help explain the elevated saving rate, and Agents’ intelligence on uncertainty. Rather than cutting Bank Rate now, I would prefer to wait and see if the durability in disinflation is confirmed in upcoming economic developments this year. Current market pricing is close to the path suggested by a forward-looking Taylor rule (Annex 1), which is a fair description of my position at present.

Megan Greene: I continue to believe inflation risks are to the upside and worry that the disinflationary process has slowed. Household inflation expectations remain elevated and inflation has been above a threshold increasing the risk of second-round effects for six months (Box C). Despite labour market easing, Decision Maker Panel and Agents’ steers suggest wage growth will remain high next year, indicating that the wage-setting process may have changed. Firms’ cost pressures have increased, potentially slowing the disinflationary process further (Box A). There is a risk of weaker consumption but, if motivated by scarring from recent inflationary episodes, this is best addressed by bringing inflation back to target. All but one of the policy simulations across the central projection and both scenarios argue for a prolonged pause in Bank Rate to lean against inflation (Annex 1). I am not convinced the monetary policy stance is meaningfully restrictive. There is huge uncertainty around the neutral rate, but as we approach it the risk of cutting too far or too fast rises and it becomes more difficult to discern whether inflation is driven by the monetary policy stance or underlying dynamics. I believe it is prudent to hold policy steady to ensure disinflation remains on track.

Clare Lombardelli: While I expect headline inflation to continue to fall, I worry there may be more underlying inflationary pressure in the economy than embodied in the central projection. Despite recent softer-than-expected data, forward-looking indicators of inflation have been less benign, particularly around pay settlements next year. Structural changes in the labour market (Box F) may mean there is less slack in the economy, leading to more persistent inflationary pressures. Higher inflation expectations and associated threshold effects (Box B and Box C) may have changed wage and price-setting behaviour. In such a scenario, we would need a longer period of restrictive monetary policy to bring inflation sustainably back to target. And it is uncertain how restrictive policy is currently. While I find the ongoing weaker consumption scenario compelling (Box D), we have plenty of policy space to lower Bank Rate should it be necessary, while a policy reversal would be costly for the MPC’s credibility.

Catherine L Mann: The inflation persistence scenario is my central case. Price dynamics are unlikely to follow the rapid deceleration shown in the central projection. Administered prices could jump again, elevated household inflation expectations risk further second-round effects (Box B), and wage inflation is expected to remain above target-consistent levels next year. Core goods inflation remains high, with little sign so far of downward pressure from geopolitical factors, global economic developments, or the exchange rate. Monetary policy needs to rein in both inflation and expectations drift so as to reinforce commitment to our 2% target. I place some weight on the lower demand scenario. However, activity and labour market indicators are easing only slowly. Weaker market-sector output and greater slack in the private labour market have been offset by growth in government spending and employment. Policy restrictiveness is past its peak and continues to moderate, particularly through the lens of recent credit indicators. Because the high saving ratio reflects inflation’s erosion of real wealth, and buffers against purchasing-power uncertainty, holding a firm stance against inflation is needed. Therefore, both scenarios support a vote to hold.

Huw Pill: I continue to prefer a slower pace for the withdrawal of monetary policy restriction than delivered over the past 18 months, reflecting my longstanding concern that structural changes in price and wage-setting behaviour have generated stronger intrinsic inflation persistence in the UK, resulting in more sustained above-target underlying inflation. In general, I place more weight on lower-frequency trends in inflation, and less weight on short-term innovations in headline inflation. The former are influenced by a monetary policy that transmits with long lags, whereas that is less the case for the latter. As a result, my concerns follow less from the risks captured in the upside scenario and more from the upside risks stemming from structural changes. Concerns about structural change are motivated by continued strength in services and wage inflation despite the apparent emergence of slack, and are supported by micro-level evidence on participation (Box F). Given that a policy based on erroneous real-time estimates of the economy’s resting place can require costly correction, my concerns on this dimension argue for a cautious approach to further policy easing.

Votes to reduce Bank Rate by 0.25 percentage points, to 3.75%

Sarah Breeden: Data since August have provided me with greater confidence that the disinflation process remains on track and that upside risks to inflation are not materialising. I judge that a degree of slack has and will continue to open up in the labour market, which should continue to dampen pay growth. Bank staff analysis and Agency intelligence on profit margins have given me further confidence that the slowdown in firms’ wage costs will be passed through to prices (Box A). While the upside risks to inflation have diminished somewhat since the August Report, downside risks from the outlook for demand have become more prominent. I think it plausible that a structural change in household behaviour means that the saving rate stays elevated (Box D). Combined with my view that policy remains restrictive and slack continues to build, this gives me enough confidence to cut now. We will need a higher accumulation of evidence on disinflation as we feel our way towards neutral next year, where I see benefits in retaining some insurance against potential structural changes in the labour market (Box F). But in the absence of conclusive evidence that this is happening, I support a gradual policy reduction now.

Swati Dhingra: Disinflation remains clearly on track, with balanced risks to inflation and downside risks to activity. Food price inflation, while concerning, may have limited scope to generate second-round effects (Box B) and acting pre-emptively to counteract a mechanism little influenced by UK monetary policy risks potential policy errors. Labour market slack should lean against potential upside risks from inflation expectations. Vacancies have fallen further, while slack may be larger than estimated given high net desired hours and a mechanical overstatement of the NAIRU. The strength of past wage growth is more likely to reflect post-pandemic churn rather than structural shifts. Weak demand should continue to constrain firms’ ability to raise prices (Box A). Bank Rate reductions may have limited countervailing effects on the consumption outlook, due to a continuing drag from the mortgage cash-flow channel and a rise in precautionary savings (Box D). Compared to the downside scenario, I am more concerned about the mix of demand and supply reflected in activity. My view remains that Bank Rate should have been lower already to account for lags in its transmission to the real economy. Policy is overly restrictive and could exacerbate risks from weak demand and reduced supply.

Dave Ramsden: I place weight on our central projection and see risks around it as broadly balanced, although the downside risks are now more prominent for me relative to August, particularly as previous uncertainties around the disinflation process have reduced. Activity is subdued, the labour market is loosening materially and the inflation hump has played out largely as expected. Bank staff analysis on firms’ costs and margins suggest that, as labour cost pressures dissipate, prices will follow suit (Box A). I find the mechanisms in the downside scenario plausible (Box D). Households’ worries about the outlook may continue to keep the saving ratio elevated. And weaker SME cash flow positions should be kept in mind (Box E), particularly given the rising unemployment projection in the forecast. When assessing upside risks, analysis on the salience of different components for inflation expectations has persuaded me that the impact on the current wage-setting process will be modest (Box B). A more compelling potential upside risk comes from the supply side, though there is currently little supporting evidence (Box F). I judge that our policy stance continues to be restrictive and, based on my outlook, expect that a gradual removal of policy restraint will remain appropriate.

Alan Taylor: I disagree with the central projection and my own outlook is weaker. I judge that the current level of slack is larger, and the terminal rate is lower, implying that the current stance is more restrictive than intended. I place more weight on downside risks to inflation, which would materialise if current trends continue, rather than upside risks, which would require new developments to emerge. Data indicate weakening demand and low confidence. The saving rate is more likely to remain elevated (Box D). Inflation has undershot expectations and should fall from here as temporary factors fade, while the labour market continues to soften. Peak unemployment is yet to come, may endure for some time, and our projections for it have drifted higher over successive forecasts. The evidence suggests limited second-round effects from food prices (Box B). Instead, I place weight on our other models that suggest inflation may not stop falling in the second half of next year and could undershoot. I favour reducing restrictiveness now, with more easing likely to come, as insurance against depressed activity amid such an inflation undershoot. This still leaves scope to pause later as needed, or to respond if upside risks materialise.

Operational considerations

21: On 5 November, the stock of UK government bonds held for monetary policy purposes was £555 billion.

22: The following members of the Committee were present:

- Andrew Bailey, Chair

- Sarah Breeden

- Swati Dhingra

- Megan Greene

- Clare Lombardelli

- Catherine L Mann

- Huw Pill

- Dave Ramsden

- Alan Taylor

Sam Beckett was present as the Treasury representative.

Jonathan Bewes was present on 27 October, as an observer for the purpose of exercising oversight functions in his role as a member of the Bank’s Court of Directors.

Gold Price Surges Above $4,000

As the chart shows, XAU/USD climbed above the $4,000 mark today, a move likely driven by:

→ Weakness in the US dollar index – or a pullback from the resistance level discussed in yesterday’s DXY analysis.

→ Concerns over the ongoing US government shutdown – according to media reports, one consequence has been that American airlines began limiting ticket sales in November.

Technical Analysis of XAU/USD

On 28 October, our analysis of gold price movements showed the following:

→ We constructed an ascending channel (marked in blue), illustrating the metal’s remarkable rally from its August low.

→ We suggested that the developing pullback might target the QL line, reinforced by the round-number support at $3,900.

This support zone successfully held, forming a local bottom at point B, after which the price entered a period of consolidation, resembling a symmetrical triangle pattern.

Notably, gold has today broken upward through this triangle (outlined in black). In the broader context, this breakout represents a strong signal from the bulls, suggesting a possible resumption of the 2025 uptrend.

If buying momentum continues, their strength may be tested by:

→ Resistance at $4,045;

→ Resistance near $4,150, which aligns with the 50% retracement of the A→B decline and has previously acted as a reversal zone for XAU/USD.

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

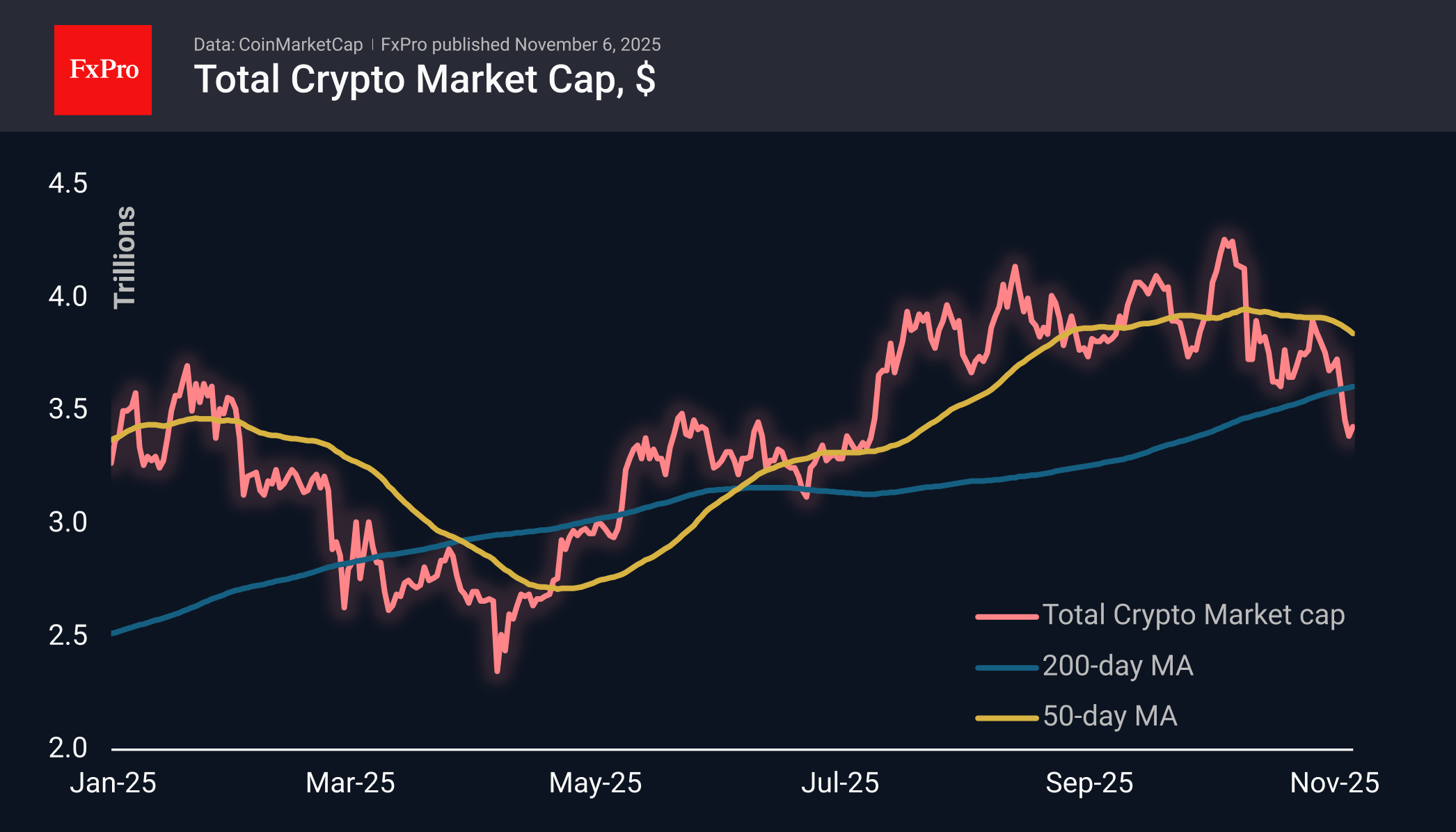

Crypto Bulls Fail to Maintain Momentum

Market Overview

The crypto market has gained 1% over the past 24 hours, the first increase after four days of decline. The market is stabilising at levels just above $3.4 trillion, close to May’s local highs. The situation currently resembles a pause in the decline rather than a serious reversal, due to somewhat cautious sentiment in the stock markets and the strengthening of the dollar since the second half of September. Ironically, this reversal coincides with the resumption of the easing cycle of monetary policy.

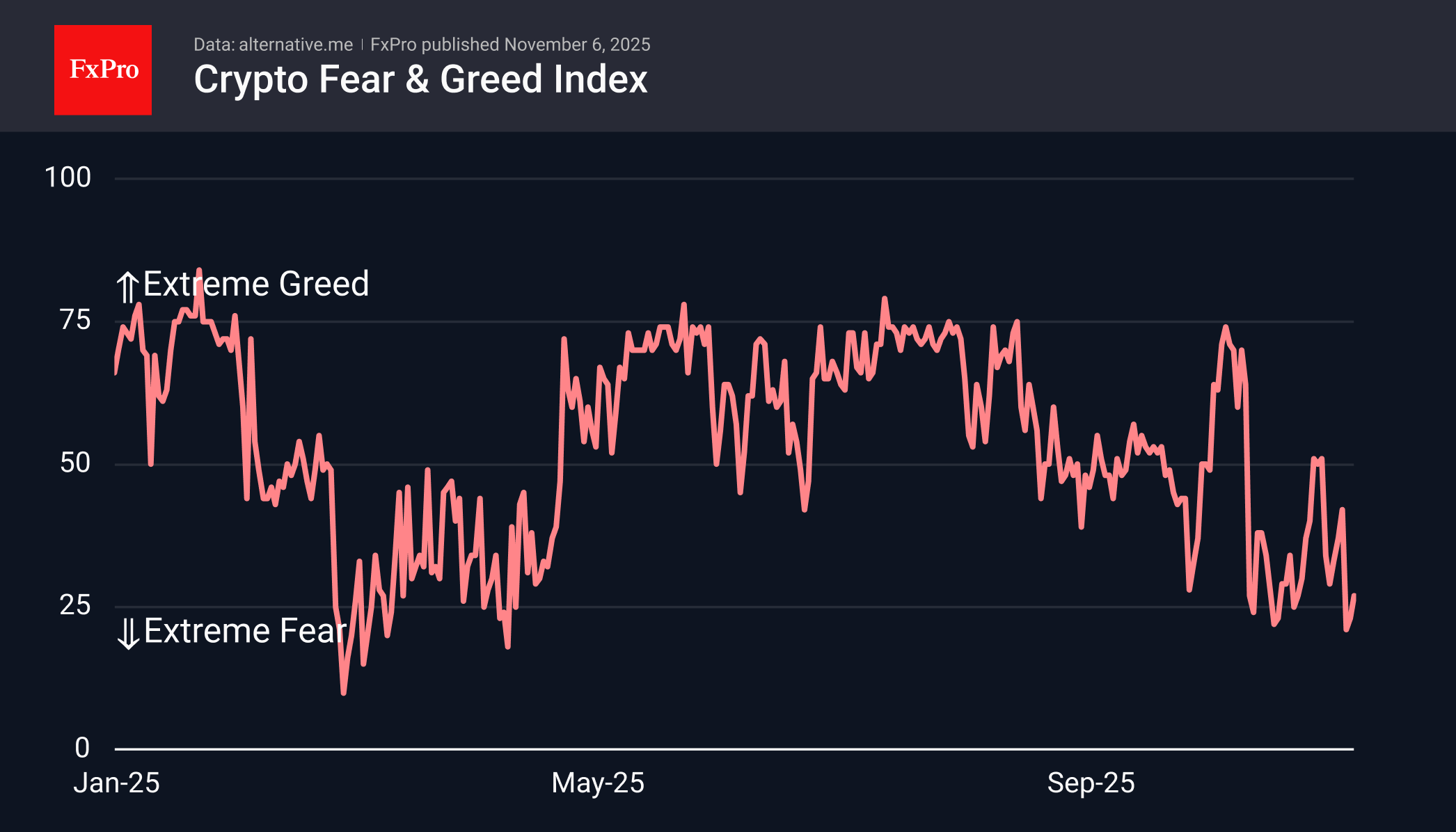

The sentiment index has emerged from the zone of extreme fear, which also coincided with a market rebound. According to the creators of such an index, now is the right time for bulls. Still, traders should be cautious with such an interpretation, as the previous rebound from extreme fear was not long-lasting, and the market is now 5% below the local low of 17 October, when sentiment last recovered from extreme anxiety.

Bitcoin is trading near $ 103,000, pausing its rebound but remaining far from its recent lows. The bulls managed to bring the coin back above the 50-week moving average, but there is still a lot of time left until the end of the week, and for now, time is on the bears’ side. On intraday charts, it looks as if the rebound has run out of steam and sellers are ready to seize the initiative again.

News Background

Cryptocurrencies are under pressure from general risk aversion in global markets. Among the factors are concerns about the Fed’s interest rate and the situation in the credit sector, according to Hashdex. Wintermute attributes the worst performance of cryptocurrencies among all other asset classes to the redistribution of cash flows to other markets.

Short-term Bitcoin holders continue to sell cryptocurrencies at a loss, using any rebound as an opportunity to sell, notes analyst Darkfost. However, accumulator addresses — wallets that only buy and never sell — have acquired a record 375,000 BTC over the past month.

Amid the asset’s decline, French company Sequans Communications, which accumulates Bitcoin, was forced to sell 970 BTC to partially repay its convertible debt. The company’s reserves fell from 3,234 to 2,264 BTC.

Japanese company Metaplanet, on the other hand, is raising funds to purchase bitcoins. On 31 October, the company received a $100 million loan secured by its reserves.

Ripple announced that it had raised $500 million in strategic investments (with a valuation of $40 billion) from major institutional players.

Zcash (ZEC) could become an alternative to Bitcoin among those who fear the centralisation of BTC due to Wall Street and are concerned about the tracking of on-chain transactions, according to Galaxy Digital. Supporters of the private coin refer to it as ‘encrypted Bitcoin’ and a return to the principles of the cypherpunks.

Eurozone retail sales slip -0.1% mom as non-food demand softens

Eurozone retail sales disappointed in September, falling -0.1% mom, missing expectations of a 0.2% gain. The decline was driven mainly by weaker spending on non-food items, which slipped -0.2%, and a sharp -1.0% drop in automotive fuel sales. Meanwhile, sales of food, drinks, and tobacco were unchanged.

Across the broader EU, retail sales managed a modest 0.1% monthly rise, masking divergent trends among member states. The steepest declines were seen in Lithuania (-1.1%), Latvia and Slovenia (-0.7%), and Italy (-0.6%), while Luxembourg and Malta (+1.7%), along with Estonia (+1.5%) and Slovakia (+1.4%), posted strong rebounds.

GBP/USD Hovers Near Lows as Bank of England Decision Looms

The GBP/USD pair is attempting to find support around 1.3062 on Thursday, with investors cautiously positioning themselves ahead of today's pivotal Bank of England (BoE) monetary policy meeting. The British currency remains under pressure, trading near a seven-month low against the US dollar and at its weakest level in over two years against the euro.

Market pricing currently implies roughly a one-in-three chance of a 25-basis-point rate cut from the BoE. This uncertainty creates significant asymmetric risk, meaning the pound is poised for a sharp move in either direction once the decision and accompanying statement are released.

The pound's weakness was compounded by the recent release of softer-than-expected UK inflation data, which bolstered expectations for an imminent shift towards policy easing. A simultaneous global sell-off in equity markets, particularly in the tech sector, has further dampened sentiment by reducing appetite for risk-sensitive assets such as sterling.

Adding to the headwinds, investor focus is shifting to the UK budget, due for approval later this month. Chancellor Rachel Reeves has signalled the potential for tax rises, a measure that could stifle economic growth and potentially prompt the BoE to adopt a more dovish stance – another factor weighing on the currency.

Technical Analysis: GBP/USD

H4 Chart:

On the H4 chart, GBP/USD broke downwards from a consolidation range around 1.3140, completing a bearish wave to 1.3010. We now anticipate a technical correction towards 1.3090. Following this pullback, the primary downtrend is expected to resume, with the next key targets at 1.2910 and, ultimately, 1.2811. The MACD indicator supports this bearish outlook. While its signal line is at deeply oversold levels and has diverged from its histogram, suggesting the potential for a short-term corrective rise, the overall structure remains negative.

H1 Chart:

On the H1 chart, the pair similarly broke down from a range around 1.3157, reaching the 1.3010 target. A corrective retracement to test 1.3100 from below is now expected. Once this correction is complete, the downtrend is likely to extend towards at least 1.2950. The Stochastic oscillator aligns with this view. Its signal line is in overbought territory above 80 and appears poised to turn down towards 20, indicating that any near-term strength is likely corrective before selling pressure reasserts itself.

Conclusion

GBP/USD is stabilising at multi-month lows ahead of a high-stakes BoE meeting. The combination of dovish inflation data, a risk-off market mood, and looming fiscal uncertainty has created a profoundly negative backdrop for sterling. Technically, the path of least resistance remains downward. While a short-covering bounce back towards 1.3100 is possible post-decision, the broader trend suggests further losses, with key targets at 1.2910 and 1.2811.

Bank of England Has a Reputation of Daring to Surprise

Markets

The Bank of England has a reputation of daring to surprise. It’s nickname – unreliable boyfriend – is testament to that. Today we might see one of those upsets with UK money markets discounting a 25% probability to a 25 bps rate cut, but the decision probably being a much closer call than that. Much will depend on BoE governor Bailey’s own views and/or his skills to build consensus around the decision. Over the past months, split vote after split vote highlighted the extreme division in the 9-headed MPC. Hawks including BoE chief economist Pill or Greene assess the still lingering inflation threat as key and don’t want to err on the side of loosening the central bank’s grip too early with the risk of igniting more price pressures with a less restrictive monetary policy. Their main arguments lost strength though over the past month with official September CPI inflation peaking at a lower level than feared and underlying dynamics showing a weakening impact from food inflation (also in preliminary October data). The latter has an outsized impact in shaping inflation expectations. Also arguing in favour of a steady outcome today is uncertainty related to the November 26 Budget presentation by Chancellor Reeves. The doves inside the BoE are more concerned about a rapidly deteriorating UK labour market, witnessed both by the official data and in the less formal business circuit often mentioned by BoE Bailey. Implementing the Fed’s “risk management” strategy argues in favour of lower the policy rate today, especially if backed by a more benign inflation dynamic in the new quarterly Monetary Policy Report. The (negative) economic impact of the tax-lifting budget might also in the end be bigger than the (if any) inflationary effects. From a market point of view, we think that sterling is vulnerable both to a dovish pause and especially to an effective rate cut (our preferred scenario). UK money markets only fully discount another 25 bps move lower by the February 2026 meeting and only 50 bps of cumulative decreases over the next 12 months. EUR/GBP broke 0.8768/69 resistance last week with follow-up action levels above 0.88. The 2023-top at EUR/GBP 0.8979 is the next big reference.

News & Views

The Brazilian central bank left its policy rate unchanged at 15% for a third consecutive meeting. Vigilance remains warranted, but the tone of the communiqué shows some more comfort that ‘maintaining the interest rate at its current level for a very prolonged period will be enough to ensure the convergence of inflation to the target’. In September, the central bank still formulated this assessment in a more conditional way. With respect to the domestic economy, the BCDB sees economic growth moderating but the labor market is still showing strength. Headline inflation and measures of underlying inflation have shown some improvement but like inflation expectations for 2025 (4.5%) and 2026 (4.2%) remain above the 3% inflation target. Inflation projections show a declining path from 4.8% for this year and 3.6% for next to 3.3% at the end of the policy horizon (Q2 2027; from 3.4% in September). The real (USD/BRL 5.357) is holding strong after already a good rally against the dollar earlier this year (YTD + 13.5%)

The National Bank of Poland (NBP) yesterday further reduced its policy rate by 25 bps to 4.25%. The NBP says that taking into account a decline in inflation and an improved inflation outlook for the coming quarters, in the Council’s assessment, it became justified to adjust the level of the NBP interest rates. October CPI inflation declined to 2.8% Y/Y (from 2.9% in September 2025), largely due to lower annual growth of food prices, but the NBP estimates that inflation net of food and energy prices also decreased, even as services price growth remains elevated. In its new forecast, the NBP sees the 2025 inflation target range at 3.6-3.7% (from 3.5%-4.4%). For 2026 the range is set at 1.9%-4% (from 1.7%-4.5%) and for 2027 at 1.1%-4.1% (from 0.9%-4.3%). The NBP has an inflation target of 2.5% (+/- 1%). Further decisions of the Council will depend on incoming information regarding prospects for inflation and economic activity. Fiscal policy, recovery of demand in the economy and elevated wage growth remain risk factors for low inflation. Uncertainty stems also from the level of energy prices and inflation developments abroad. The zloty yesterday gained modestly after the decision closing near EUR/PLN 4.256.

Tariffs on Trial, Yields on the Rise, Bulls on Pause

Selloff across major US indices slowed yesterday as pressures eased and dip-buyers came in to amass their favourite stocks at slightly lower levels than the recent all-time highs, while attention shifted toward rare economic data and messy politics.

First, the Supreme Court hearing yesterday revived discussions about the legality of Trump’s tariffs. Half of the six members of the GOP-appointed supermajority on the Court expressed skepticism toward arguments defending Trump’s wide-ranging and steep tariff rates imposed on the rest of the world. Yesterday’s hearing therefore suggested that Trump’s tariffs could be rolled back. Prediction markets slashed the probability of these tariffs surviving from the 40–50% range to around 25–30%.

Is it good news? Paradoxically, not really — because it brings uncertainty, renewed volatility, potentially more than $100 billion in refunds the US government may owe to other countries according to Bloomberg, and a deeper fiscal deficit. That’s concerning, especially considering that US debt has now surpassed the $38 trillion mark and is marching toward the $40 trillion psychological level — with nothing in sight to stop the climb. That certainly helped explain why the US 10-, 20-, and 30-year yields pushed higher yesterday.

A better-than-expected ADP print also supported a rise in shorter maturity yields. This week marks the first of a new month — and if the US government were open, we’d be getting the latest official jobs report. But since it remains shut, investors only have private data to rely on. The ADP report showed 42K new private-sector jobs last month, better than the 29K losses in the prior month and the 32K expected. Still, it’s a weak number, and a series of sub-50K prints would point toward recession. But for now, the slightly stronger-than-expected data further weakened the Federal Reserve (Fed) doves’ case. The US 2-year yield — a good gauge of Fed expectations — jumped past 2.60%, while the probability of a December rate cut fell to around 62.5%.

So I’m a little surprised the early-week selloff didn’t extend into a third day. This morning, we see a slightly improved tone in Asia. The tech-heavy Hang Seng returned above its 50-day moving average as local chipmaker SMIC jumped 5% and Alibaba rebounded 3% after the Chinese government banned state-funded data centers from using foreign chips. MSCI is also reshuffling its index to include more Chinese names, helping Chinese equities attract fresh inflows from global investors. Earlier this week, the People’ Bank of China (PBoC) bought bonds to shore up liquidity. As such, Chinese stocks remain in the race and continue to offer diversification versus US tech, as Jensen Huang said China “will win” the AI race with the US.

You know who might not win the race? Tesla. The company has been overtaken by BYD in UK vehicle registrations and is narrowing the gap in Germany. And in October, Tesla sold just 133 cars in Sweden. When I say Tesla doesn’t deserve this hype — and that the P/E ratio of 332 shows the gap between its stock price and reality — I mean it. There could also be some drama if Elon Musk fails to get his trillion-dollar pay package approved, with several large investors reportedly opposed to it.

Elsewhere, European carmakers could feel the pressure of renewed tensions over Nexperia, after reports that the company again halted supply as its Chinese unit refused to pay.

US futures are flat. On one hand, the rebound in Treasury yields and concerns over Big Tech valuations weigh on sentiment; on the other, earnings keep coming in strong and dipbuyers are impatient to join in. Yesterday after the bell, Qualcomm joined its peers with better-than-expected revenue, earnings and guidance — alas, the stock still slipped 2.6% in after-hours trading.

Conclusion: The weather remains cloudy, bulls are hesitant, but the dip-buyers are never far away. I’m not even sure we can get a meaningful dip when retail investors are so eager to jump back in — we’ll see.

In precious metals, gold rebounded yesterday alongside higher US yields — a very unusual move, which I attribute to the latest meme-like rally that temporarily undermined its safe-haven status. There should be a deeper pullback and consolidation before gold can reclaim that role. The longer-term outlook, however, remains unchanged: when in doubt, just look at the debt levels in developed markets.

In currencies, the US dollar’s recent rally hit a speed bump at its 200-day moving average yesterday, and the greenback is broadly sold against most majors this morning. The EURUSD is back above 1.15 after defending a minor Fibonacci support — which may improve appetite in the short term, though resistance sits near 1.1580–1.16.

Across the Channel, Cable managed to hold at the 1.30 psychological mark. The Bank of England (BoE) will likely leave rates unchanged at today’s policy meeting. Even the dovish members may prefer waiting for the Autumn Budget details. Rachel Reeves hinted on Tuesday at what might be coming — perhaps to test market reaction — and potential tax hikes were surprisingly well received by the gilt market. The 10-year gilt yield stayed mostly contained, which could give the BoE room to cut rates at its next meeting. That’s bearish for sterling.