Sample Category Title

Central Bank Meetings on the Menu

In focus today

In Sweden, the preliminary inflation figures for October are released at 08:00 CET. We expect core inflation at 2.65% (cons: 2.6%, prior: 2.7%) and headline CPIF at 2.95% (cons: 2.9%, prior: 3.09%). Our forecasts are one and three tenths above the Riksbank's, respectively. The data should underpin the Riksbank's view that inflation is heading lower, supporting their view that the elevated inflation is temporary. Erik Thedéen and Per Jansson will comment on monetary policy in separate speeches today, at 14:00 and 16:00 CET, respectively - we expect nothing new.

In Norway, we expect Norges Bank to keep the policy rate unchanged at 4.00% at today's MPC-meeting, with signals likely pointing to an unchanged rate in December as well. This is an interim meeting without new forecasts, only a press release and a press conference.

In the UK, the Bank of England meeting is scheduled, and we expect a non-consensus 25bp Bank rate cut to 3.75%. See more in Bank of England Preview - Softer inflation opens door for more easing, 31 October.

In the US, the Challenger Report for US layoff and hiring announcements is due for release for October. While not usually a tier-1 data point, we will keep an eye on the report amid the delays to official data.

In the euro area, data on retail sales for September are released. Retail sales have been stagnant for the past five months following increases early this year likely due to the weak consumer confidence.

In Germany, focus turns to industrial production. Industrial production showed a large and unexpected decline in August to levels seen only during the Covid pandemic and following the financial crisis.

Overnight, China releases trade data for October, which we expect to continue to show robust growth in exports. The numbers are quite volatile, though, so we could see some set-back after a decent rebound last month to 8.4% y/y.

Economic and market news

What happened overnight

In Japan, labour cash earnings rose 1.9% y/y in September, while real wages fell 1.4% y/y, marking the ninth consecutive decline as inflation outpaced wage growth. August's real wage drop was revised to 1.7% (prior: 1.6%). Wage growth remains crucial to the BoJ's rate hike timing, with the widening wage-price gap complicating the monetary policy outlook.

What happened yesterday

In the US, the Supreme Court heard arguments on the Trump administration's use of the International Emergency Economic Powers Act (IEEPA) to justify imposing emergency tariffs. A majority of justices across ideological lines appeared sceptical of the president's authority to implement such measures. Reflecting this scepticism, prediction markets dropped from 45% before the arguments to 25% this morning on the likelihood of a full administration victory. However, the arguments were not entirely one-sided, as several conservative justices acknowledged the president's broad powers in foreign affairs.

Also in the US, the ADP National Employment Report showed private sector jobs increased by 42k in October, stronger than the early estimate of +14k and consensus of +28k, and the previous month revised up by 3k. Growth was driven by education and healthcare, trade, transportation, and utilities, while job losses persisted in professional business services, information, and leisure and hospitality. Larger firms accounted for most of the net hiring.

ISM Services index for October rose to 52.4 (cons: 50.8, prior: 50), marking the strongest expansion since February, and with all subcomponents stronger than expected.

In Sweden, the Riksbank decided to maintain the policy rate at 1.75%, as widely expected. The central bank reiterated its September Monetary Policy Report, stating that: "The policy rate is expected to remain at this level for some time to come, in line with the forecast in September." On the SEK, the Riksbank also repeated its September outlook, saying the krona is expected to strengthen "somewhat" instead of "significantly" going forward. " Read more in Riksbank review - November 2025: On hold at 1.75% as expected - repeating September message, 5 November.

In the euro area, the final services PMI was revised up to 53.0 from 52.6 in the flash release. The flash release was already higher than consensus expectations of 51.2, so we got a significant, positive surprise in October. As the manufacturing PMI confirmed the flash release the composite PMI was revised up to 52.5. The euro area economy has thus entered the final quarter of the year with a solid momentum according to the PMIs, which should strengthen the case for unchanged policy rates in the ECB.

In the EU, member states agreed to a 2040 climate goal, including a delay to the start of the emission trading system for homes and road transport (ETS2), which is dovish for the ECB. Without ETS2, 2027 inflation is likely to undershoot, with ECB estimates suggesting a 0.0-0.4pp impact on headline inflation. While the law awaits European Parliament approval, its shift towards less ambitious climate policies makes approval likely. This move offsets some hawkish growth surprises in the ECB outlook.

In Poland, the National Bank of Poland lowered its main rate by 25bp to 4.25% at its November meeting, marking the fourth consecutive cut and aligning with market expectations.

Equities: Equities bounced back after Tuesday's mysterious pullback. Top performers were the stocks that had sold off in the previous session - primarily semiconductors and AI-capex-related names, with Intel, Qualcomm, and Caterpillar all up 3-4%. Overall, the S&P 500 rose 0.4% for the day (after slipping into the close), while the Stoxx 600 gained 0.2%. Whether the immediate rebound was driven by retail buying is open to speculation. However, as we discussed yesterday, the selloff was not rooted in macro concerns or any negative AI catalyst. This was evident in unchanged bond yields and a VIX that remained comfortably below 20. The recovery is continuing in Asia this morning, while US and European futures are flat, meaning the full decline from Tuesday has yet to be recouped.

FI and FX: The Riksbank held rates unchanged as expected and the meeting turned out to be a non-event for the market with EUR/SEK holding steady. EUR/USD consolidated below 1.15 yesterday after a stronger than expected ADP jobs report pushed US rates higher. The 10Y US Treasury yield rose after the US Treasury hinted it is considering increasing coupon issuance.

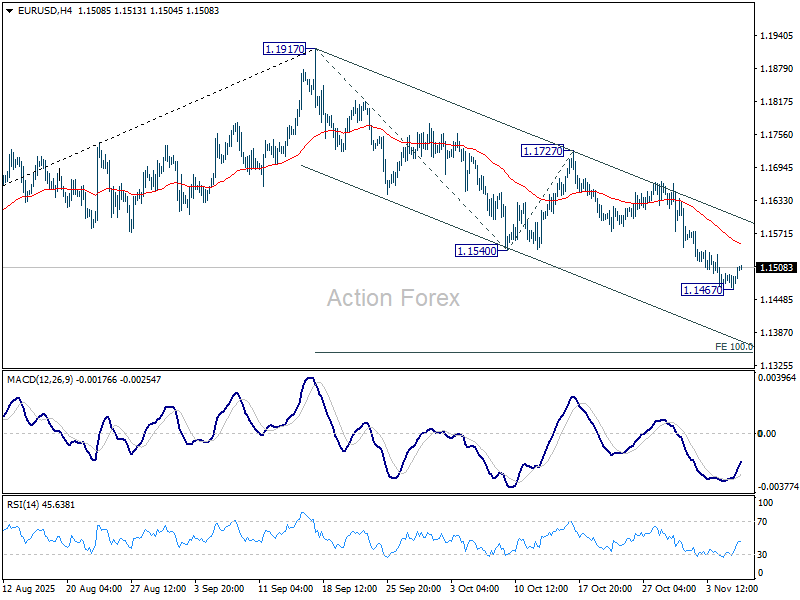

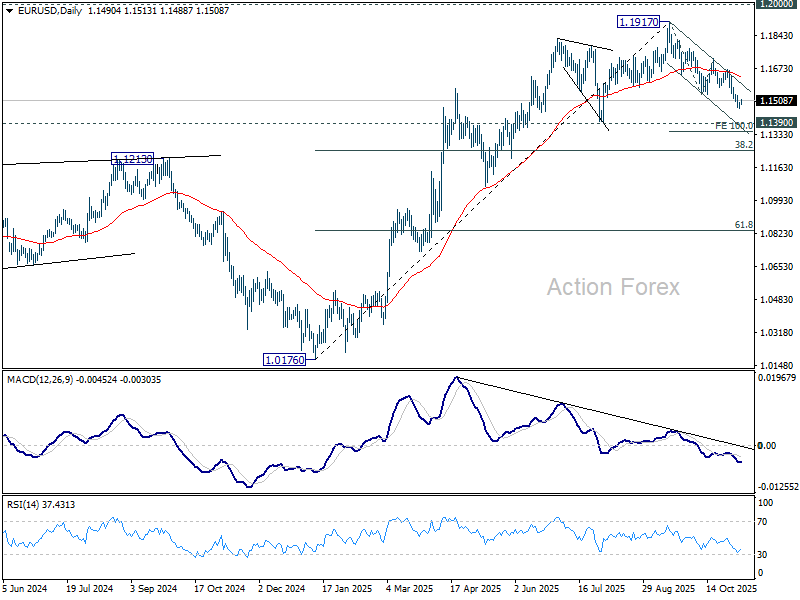

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1475; (P) 1.1487; (R1) 1.1504; More…

Intraday bias in EUR/USD is turned neutral with current recovery, and some consolidations would be seen above 1.1467 temporary low. Further decline is expected as long as 1.1727 resistance holds. Below 1.1467 will extend the fall from 1.1917 to 100% projection of 1.1917 to 1.1540 from 1.1727 at 1.1350. Decisive break there would prompt downside acceleration to 38.2% retracement of 1.0176 to 1.1917 at 1.1252.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1306) holds, the up trend from 0.9534 (2022 low) is still expected to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep outlook bearish.

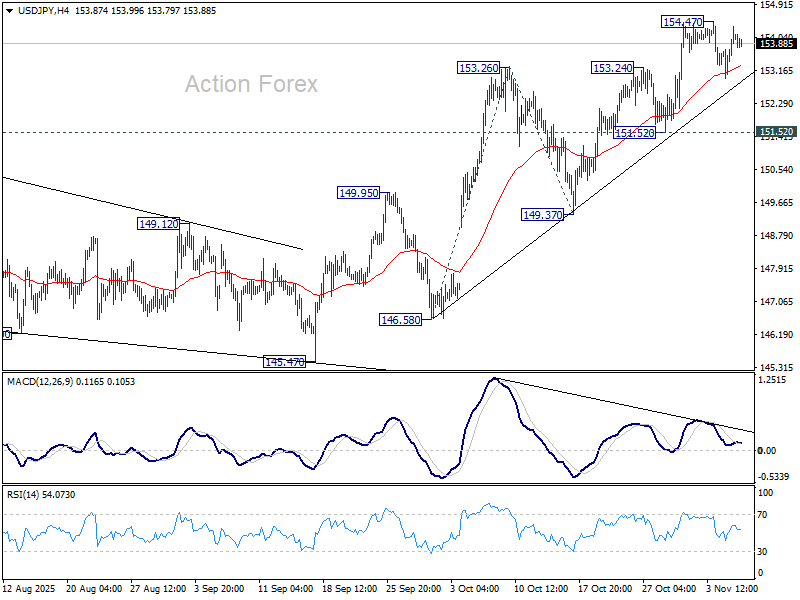

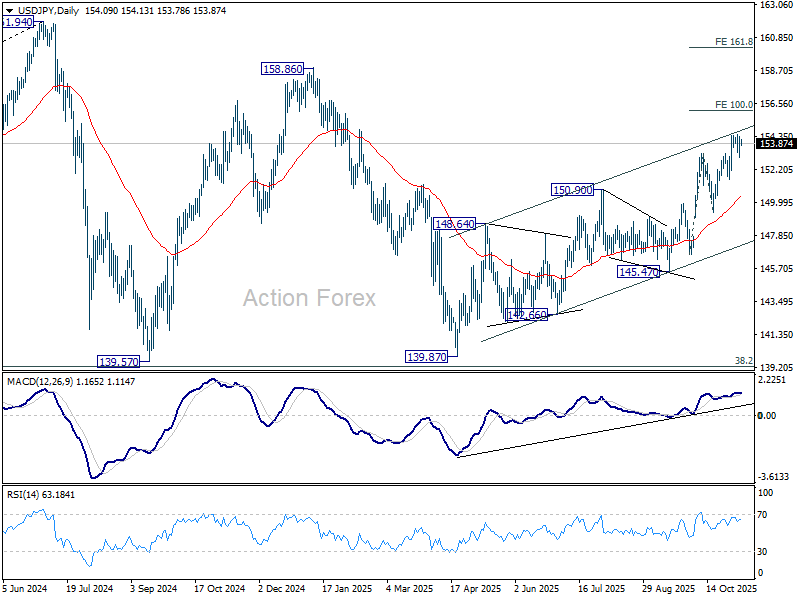

USD/JPY Daily Outlook

Daily Pivots: (S1) 153.27; (P) 153.81; (R1) 154.67; More...

USD/JPY is still bounded in consolidations below 154.47 and intraday bias stays neutral. Further rally is expected as long as 151.52 support holds. Above 154.47 will resume larger rise from 139.87 to 100% projection of 146.58 to 153.26 from 149.37 at 156.05. Break there will pave the way to 158.85 key structural resistance.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 145.47 support will dampen this bullish view and extend the corrective pattern with another falling leg.

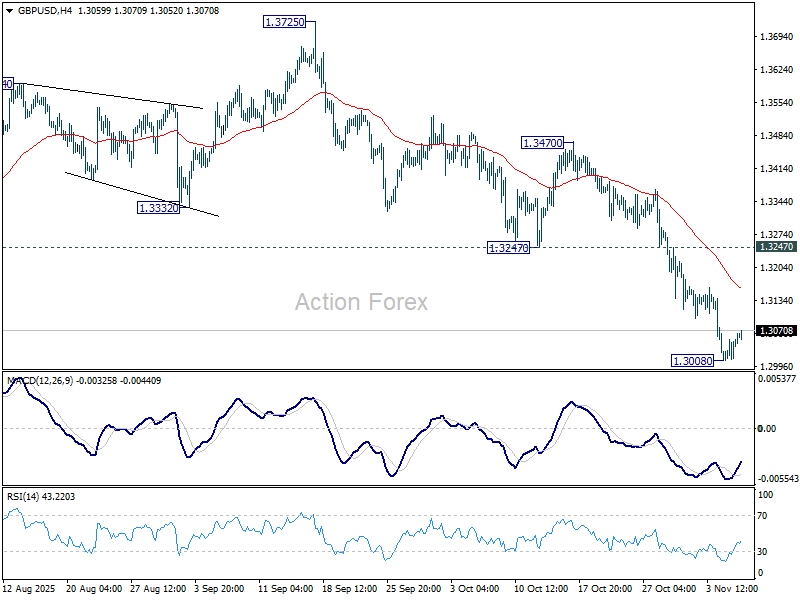

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3023; (P) 1.3038; (R1) 1.3067; More...

Intraday bias in GBP/USD is turned neutral with current recovery, and some consolidations would be seen above 1.3008. But risk will stay on the downside as long as 1.3247 support turned resistance holds. Below 1.3008 will resume the fall from 1.3787 and target 61.8% retracement of 1.2099 to 1.3787 at 1.2744 next. Sustained break there will pave the way to 1.2099 support next.

In the bigger picture, the break of 55 W EMA (now at 1.3185) is taken as the first sign that corrective rise from 1.0351 (2022 low) has completed. Decisive break of trend line support (now at 1.2780) will solidify this case and target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 next. Meanwhile, in case of another rise, strong resistance should emerge below 1.4248 (2021 high) to cap upside to preserve the long term down trend.

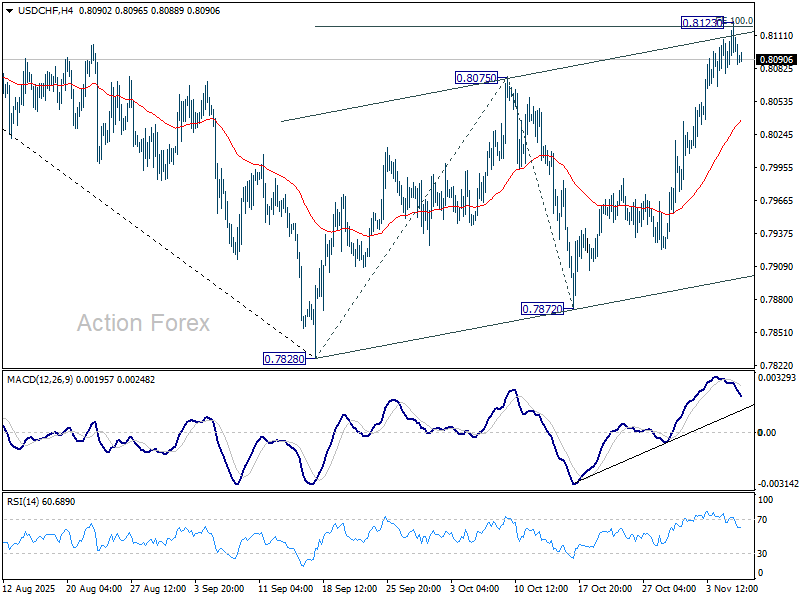

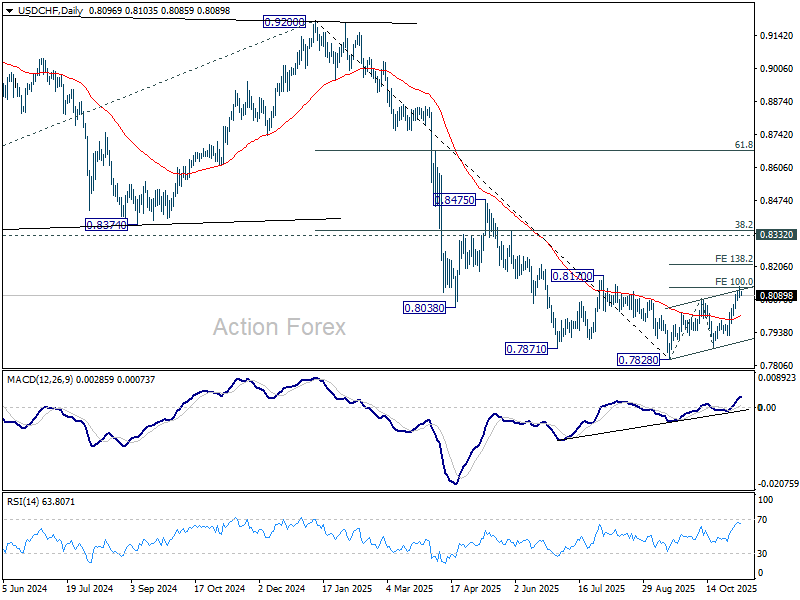

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8079; (P) 0.8102; (R1) 0.8124; More…

A temporary top was formed at 0.8123 after USD/CHF hit 100% projection of 0.7828 to 0.8075 from 0.7872 at 0.8119. Intraday bias is turned neutral first. On the upside, firm break of 0.8123 will extend the corrective rally from 0.7828 to 138.2% projections at 0.8213. On the downside, sustained break of 55 D EMA (now at 0.8002) will argue that the corrective bounce has completed and bring retest of 0.7828 low.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

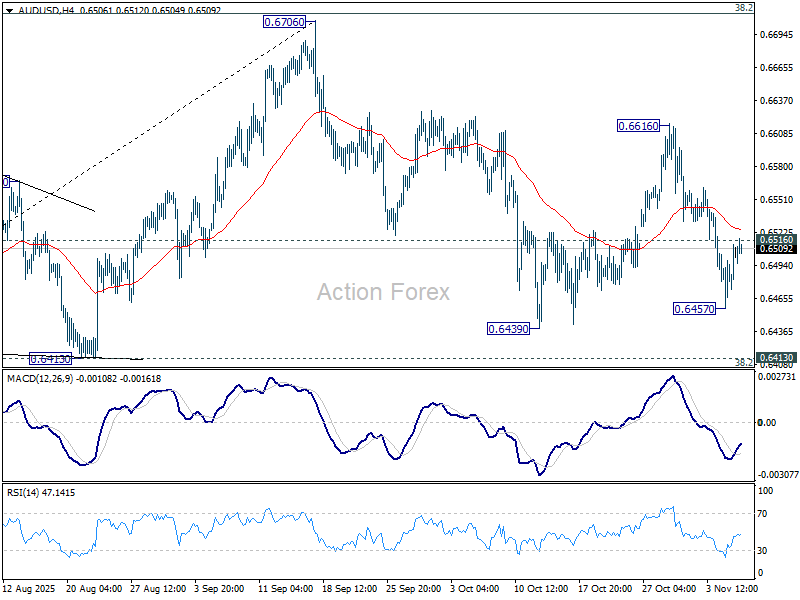

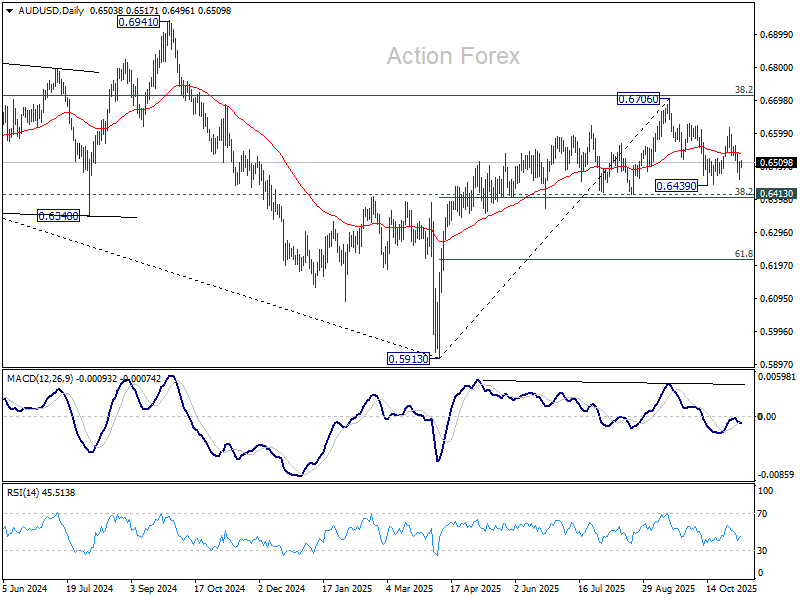

AUD/USD Daily Report

Daily Pivots: (S1) 0.6472; (P) 0.6493; (R1) 0.6526; More...

Intraday bias in AUD/USD is turned neutral first with current recovery. Fall from 0.6706 could still extend lower, but strong support would likely be seen from 0.6413 cluster (38.2% retracement of 0.5913 to 0.6706 at 0.6403) to bring rebound. Above 0.6616 will bring retest of 0.6706. However, sustained trading below 0.6403/13 will carry larger bearish implications.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. Outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Break of 0.6413 support will suggest rejection by 0.6713 and solidify this bearish case. Nevertheless, considering bullish convergence condition in W MACD, sustained break of 0.6713 will be a strong sign of bullish trend reversal, and pave the way to 0.6941 structural resistance for confirmation.

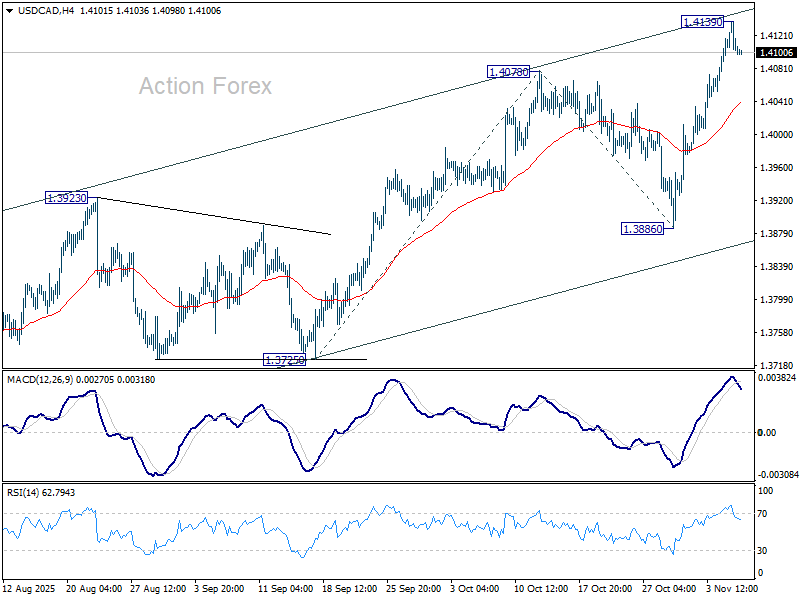

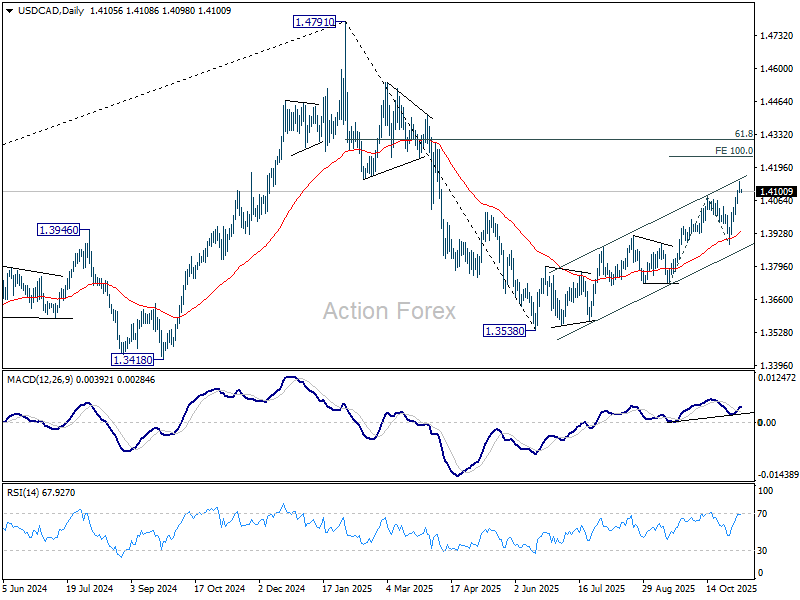

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4092; (P) 1.4116; (R1) 1.4134; More...

A temporary top is in place in USD/CAD with 4H MACD crossed well below signal line. Intraday bias is turned neutral for some consolidations. On the upside break of 1.4139 will resume larger rally from 1.3538 to 100% projection of 1.3725 to 1.4078 from 1.3886 at 1.4239. However, sustained break of 55 4H EMA (now at 1.4040) will bring deeper fall back to 1.3886 support instead.

In the bigger picture, price actions from 1.4791 medium term top is likely just unfolding as a correction to up trend from 1.2005 (2021 low). Based on current momentum, rise from 1.3538 is the second leg, and a third leg should follow before up trend resumption. That is, range trading is set to extend for the medium term. For now, this will remain the favored case as long as 1.3886 support holds. However, firm break of 1.3886 will revive the case that fall from 1.4791 is indeed a larger scale correction.

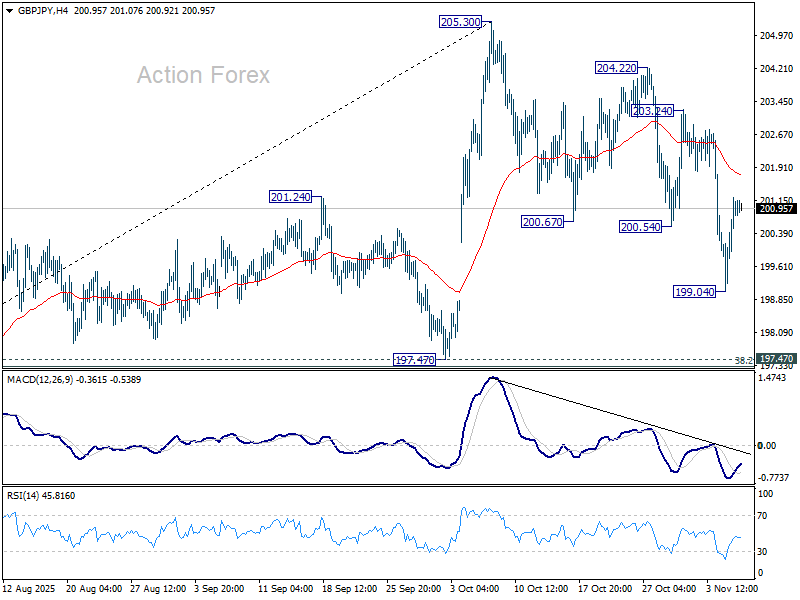

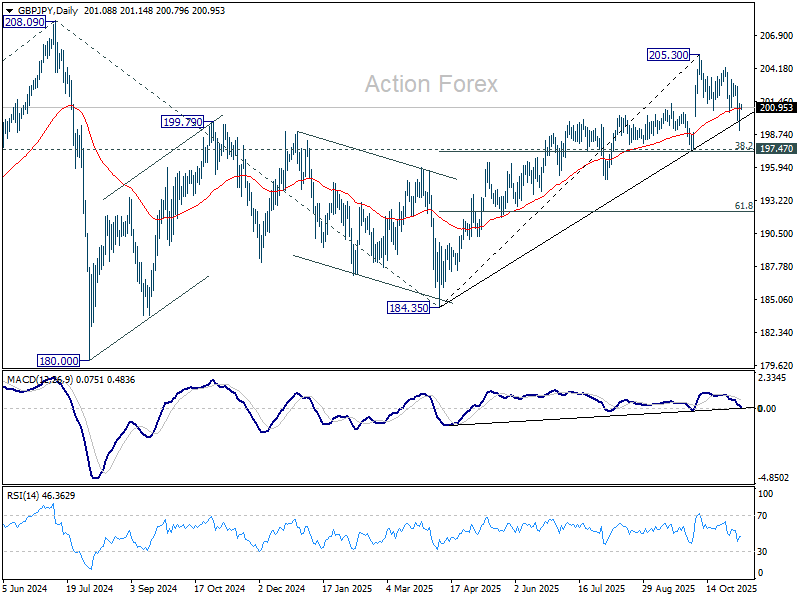

GBP/JPY Daily Outlook

Daily Pivots: (S1) 199.74; (P) 200.49; (R1) 201.92; More...

Intraday bias in GBP/JPY is turned neutral first with current recovery. Risk will stay on the downside as long as 203.24 resistance holds. Below 199.04 will resume the fall from 205.30 to 194.47 cluster (38.2% retracement of 184.35 to 205.30 at 197.29). However, sustained break of 197.39/47 should confirm near term reversal, and target 61.8% retracement 192.35 next.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a corrective pattern which might have completed at 184.35. Firm break of 208.09 high will resume the up trend from 123.94 (2020 low). Next target is 61.8% projection of 148.93 to 208.09 from 184.35 at 220.90. However, decisive break of 197.47 support will dampen this view and extend the corrective pattern with another fall.

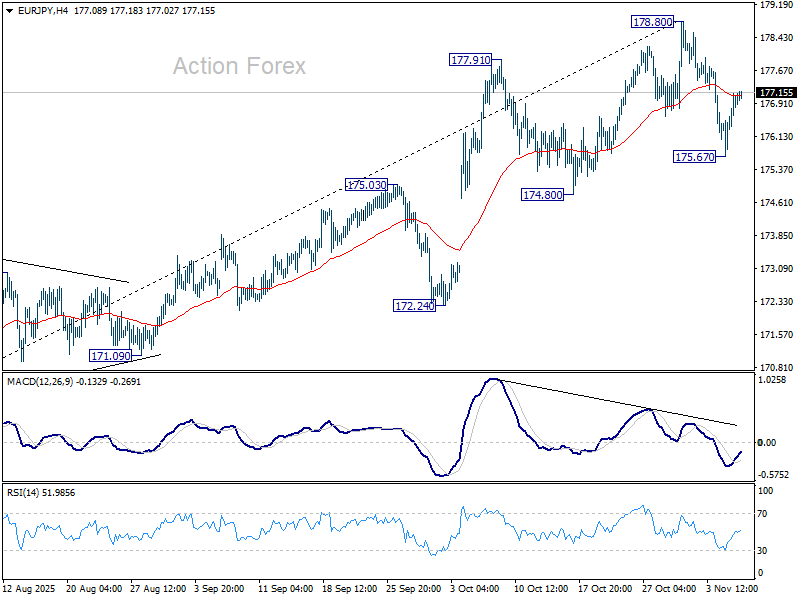

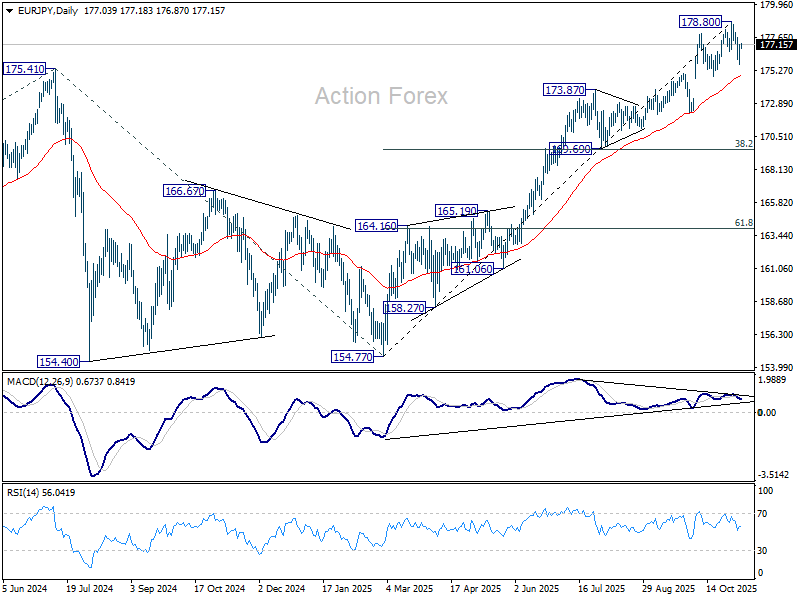

EUR/JPY Daily Outlook

Daily Pivots: (S1) 176.17; (P) 176.65; (R1) 177.61; More...

Intraday bias in EUR/JPY is turned neutral first with current recovery. But risk will stay on the downside as long as 178.80 short term top holds. Below 175.67 will target 55 D EMA (now at 174.76). Sustained break there will should confirm that EUR/JPY is correcting whole rise from 154.87, and target 169.69 cluster (38.2% retracement of 154.77 to 178.80 at 169.69.

In the bigger picture, up trend from 114.42 (2020 low) is in progress and should target 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. Firm break of 174.80 support will suggests that it has turned into consolidations again. But still, outlook will continue to stay bullish as long as 55 W EMA (now at 167.87) holds, even in case of deep pullback.

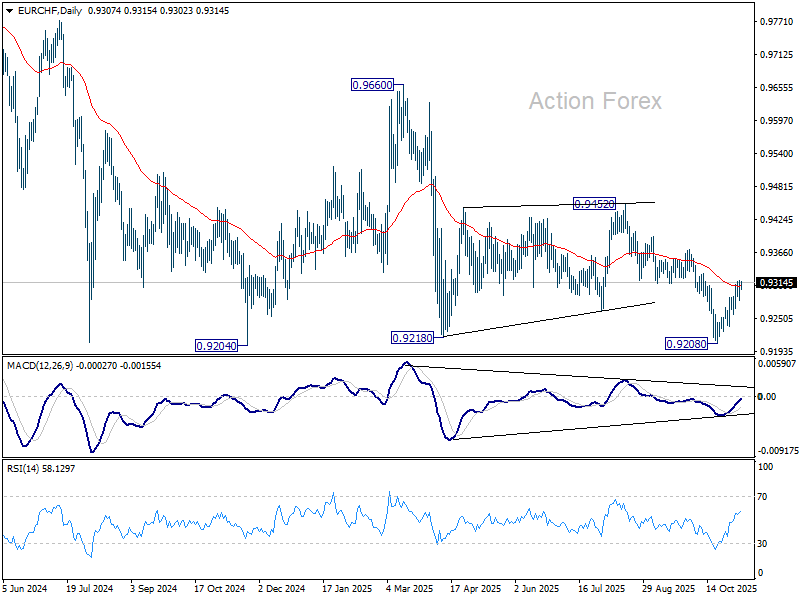

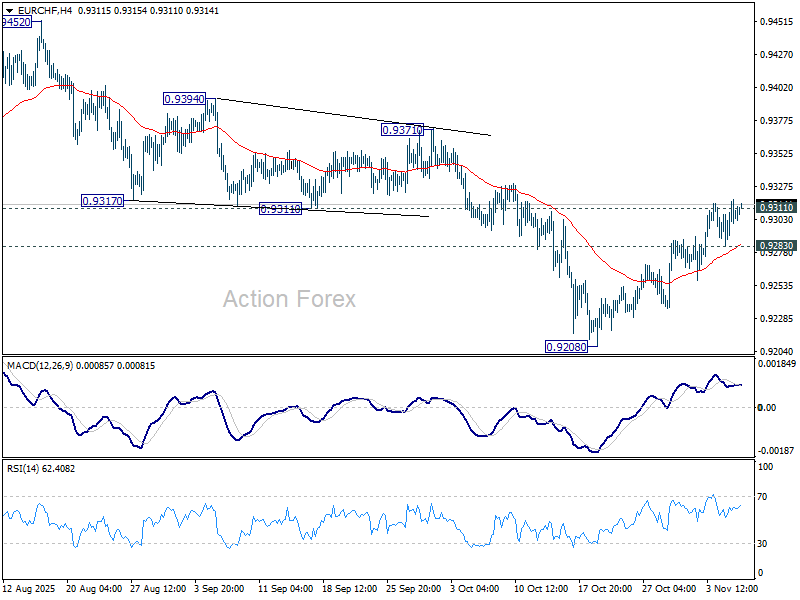

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9291; (P) 0.9306; (R1) 0.9326; More....

EUR/CHF's break of 0.9311 support turned resistance argues that fall from 0.9452 has completed at 0.9208, ahead of 0.9204 low. Intraday bias is back on the upside for 0.9371 resistance first. Firm break there will target 0.9452 next. On the downside, below 0.9283 minor support will turn intraday bias neutral again.

In the bigger picture, outlook remains bearish with EUR/CHF staying well inside long term falling channel after multiple rejection by 55 W EMA (now at 0.9386). Firm break of 0.9204 will resume the whole down trend from 1.2004 (2018 high). Next target is 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. Break of 0.9452 resistance is needed to be the first sign of medium term bottoming.