Sample Category Title

Risk Rebound Fizzled Out

Markets

The risk rebound from last week’s trade and credit related noise yesterday fizzled out. US equity indices closed little changed, but kept all-time record levels within reach. The EuroStoxx50 intraday even touched a minor new record. Equity investors apparently are in a process of switching focus between macro themes (trade frictions, private & government debt sustainability …) on the one hand, and corporate earnings on the other. For now, hick-ups in one storyline mostly have (easily) been counterbalanced by the other pillar. Bond investors already for some time take a more cautious approach. With little in the way of policy relevant eco news published in the US, it is difficult to assess the real reason for the divergent bond market approach. That said, the gradual but protracted decline in core yields still also causes a further easing in financial conditions. This pattern at some point might reach its limits. However at least for now, it continues. The information stop in the US probably facilitates it as it is hardly challenged. Whatever the driver, US yields yesterday continued their gradually, but protracted downtrend moving from little changed (2-y) to 2.6 bps lower (30-y). Especially, support levels at the long of the US curve are at risk of a (sustained) break (10-y 4%; 30-y 4.6%). Germain/ EMU yields show a similar pattern. After recent decline/ repositioning, for now there is little reason to anticipate more potential ECB easing. The German 2-y yield closed unchanged yesterday. At the long end, lower yields also still was the path of least resistance (30-y -3.6 bps). The dollar continued its rebound from last week’s (US risk-off driven) setback with the DXY nearing the 99 barrier (close 98,93). EUR/USD returned to the 1.16 big figure. The yen underperformed as the new government is expected to implement a growth supportive policy, with the BoJ in no hurry to aggressively step up policy normalization. Both USD/JPY (151.9 from 150.75) but also EUR/JPY (176.24 from 175.5) gained. We also take notice of quite a sharp correction in the likes of silver and gold. Oil tries to find a bottom (Brent $62.3 p/b)

Asian equities show no unequivocal directional pattern this morning. The yen stabilizes (USD/JPY 151.9) as Japanese PM Takaichi orders a new package to address the cost of living crisis. The eco calendar is again thin. The US Treasury will sell $ 13 bln of 20-y Notes. UK inflation data of September avoided an expected rise, with headline inflation at 0% M/M and 3.8% Y/Y (unchanged vs 4% expected). Core inflation (3.5% Y/Y from 3.6%) even eased. Services inflation was unchanged at 4.7%. The September data are supposed to be the peak in this cycle. The better starting point provided by today’s data probably reinforces the case for BoE governor Bailey to give some more weight to a weaker labour market at the November 6 meeting. A rate cut might be a closer call than the low probability markets are currently discounting. EUR/GBP jumps from the 0.868 area to test the 0.87 big figure.

News & Views

The Indian newspaper Mint, citing people familiar with the matter, said that the US and India are nearing a trade deal that could cut tariffs on exports to 15-16%. President Trump raised the levy to 50% a couple of weeks ago, up from the initial 25% to pressure the country to stop buying Russian oil. New Delhi started buying Russian oil in major quantities and at a discount after Moscow’s invasion in 2022. The Mint said that India may now agree to gradually reduce its Russian oil imports adding that it would also tear down own trade barriers to allow for more US corn and soymeal imports. The newspaper floated next week’s Association of Southeast Asian Nations summit in Malaysia as an opportunity to announce the deal.

The Hungarian central bank (MNB) kept the policy rate as expected at 6.5% yesterday. It has a pretty downbeat view on the current economic conditions with retail sales slowing down, industrial production volumes falling and construction cratering since the last policy meeting. Next year, however, things should improve both internally (domestic consumption and investments) and externally (rising exports). Inflation last month stood at 4.3% in September and household inflation expectations remain elevated. The MNB expects CPI to remain above the tolerance band of 3% +1 ppt, despite government policy that prompted mandatory and voluntary price restrictions. The central bank noted strong corporate repricings on products outside the government’s scope. It considers tight monetary conditions still necessary to achieve a sustained return to the inflation target, currently estimated to happen in early 2027. The forint barely budged to trade near the strongest levels in a year around EUR/HUF 390.

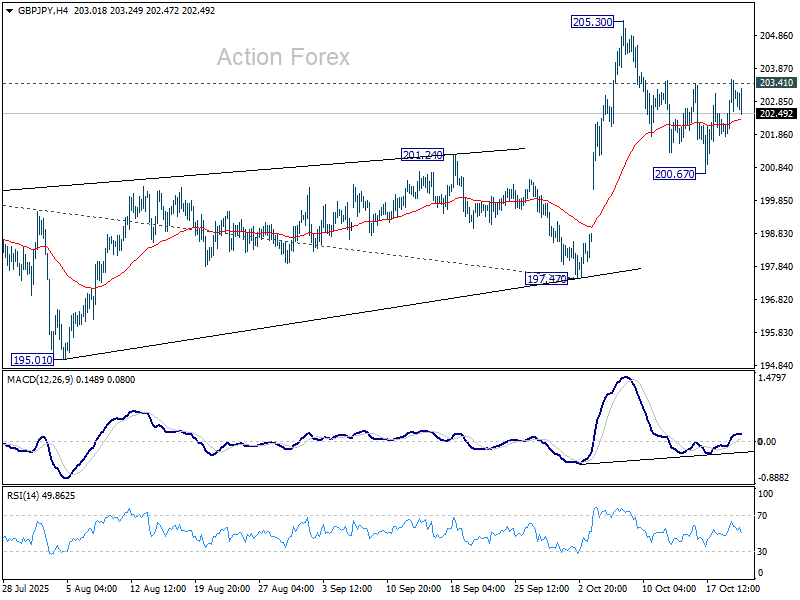

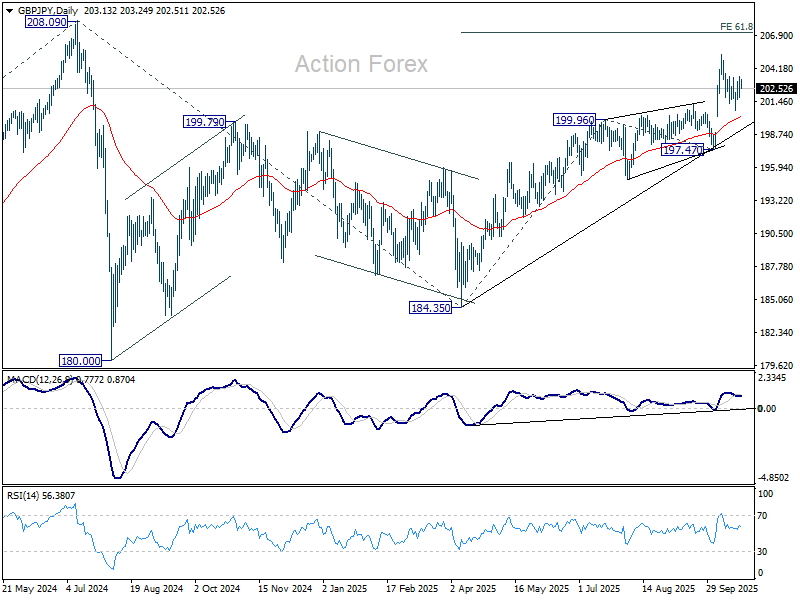

GBP/JPY Daily Outlook

Daily Pivots: (S1) 202.08; (P) 202.80; (R1) 203.79; More...

Intraday bias in GBP/JPY remains neutral at this point. On the upside, above 203.41 will suggest that pullback from 205.30 has completed, and bring retest of this high. Firm break there will resume larger rally to 61.8% projection of 184.35 to 199.96 from 197.47 at 207.11. However, break of 200.67 and sustained trading below 201.24 resistance turned support will raise the chance of bearish reversal, and bring deeper decline to 197.47 instead.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a corrective pattern which might have completed at 184.35. Firm break of 208.09 high will resume the up trend from 123.94 (2020 low). Next target is 61.8% projection of 148.93 to 208.09 from 184.35 at 220.90. However, decisive break of 197.47 will dampen this view and could extend the corrective pattern with another fall.

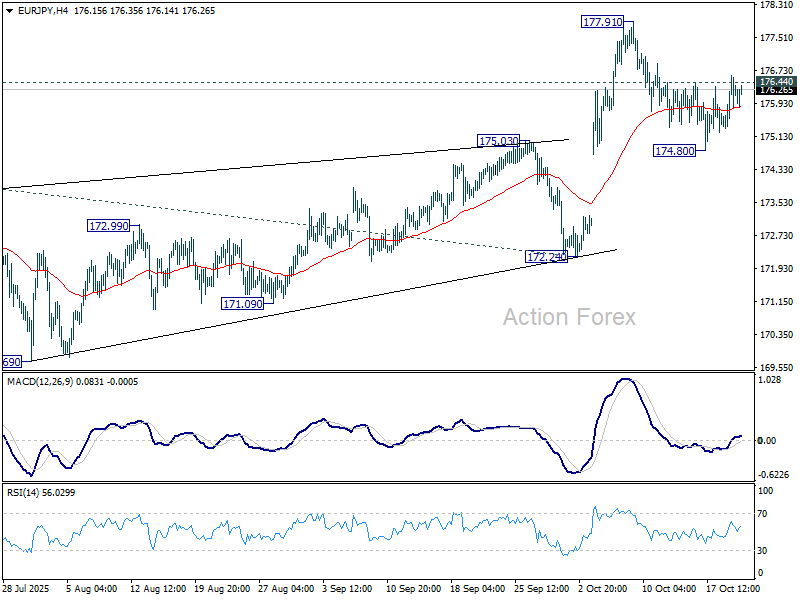

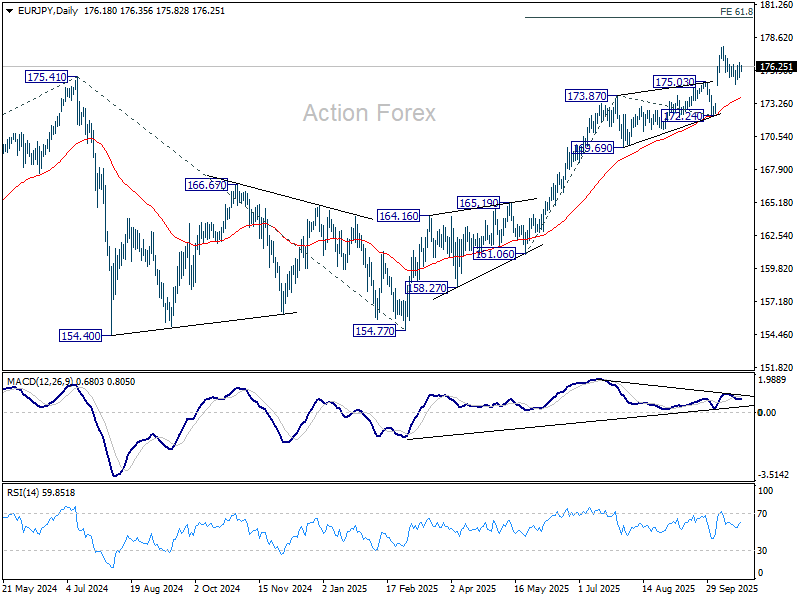

EUR/JPY Daily Outlook

Daily Pivots: (S1) 175.51; (P) 176.07; (R1) 176.78; More...

Intraday bias in EUR/JPY stays neutral first. On the upside, break of 176.44 resistance will suggest that pullback from 177.91 has completed, and bring retest of this high. Further break of 177.91 will resume larger up trend to 61.8% projection of 161.06 to 173.87 from 172.24 at 180.15 next. However, break of 174.80 and sustained trading below 175.03 resistance turned support will indicate that it's already in a larger scale correction, and target 172.24 support.

In the bigger picture, up trend from 114.42 (2020 low) is in progress and should target 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. Firm break of 172.24 support will suggests that it has turned into consolidations again. But still, outlook will continue to stay bullish as long as 55 W EMA (now at 167.43) holds, even in case of deep pullback.

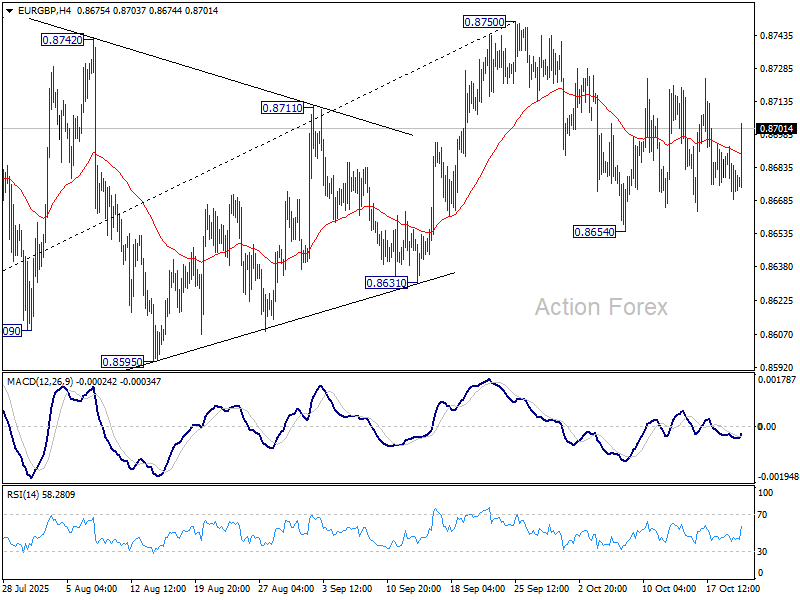

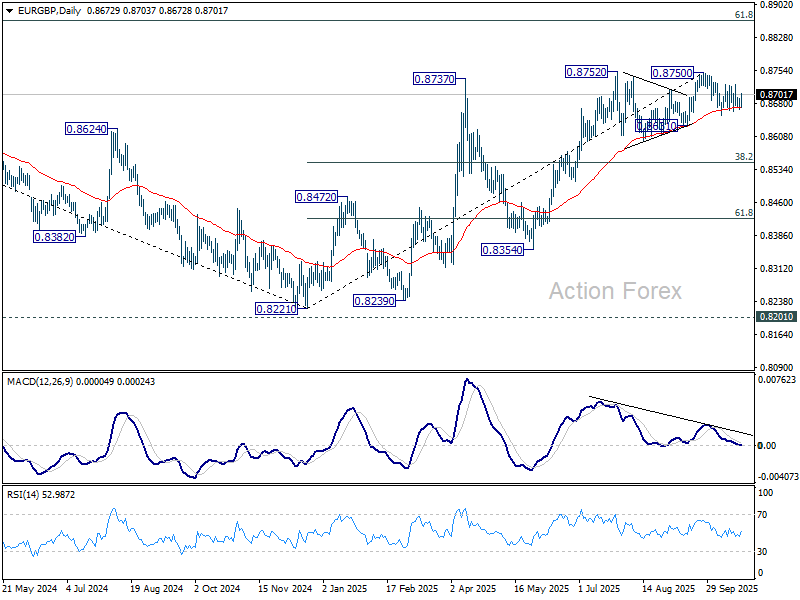

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8668; (P) 0.8681; (R1) 0.8692; More…

Range trading continues in EUR/GBP and intraday bias remains neutral. On the downside, break of 0.8654 will resume the fall from 0.8750 to 0.8631 support. Decisive break there will indicate bearish reversal and target 38.2% retracement of 0.8221 to 0.8750 at 0.8548. Nevertheless, on the upside, break of 0.8750/2 will resume the rise from 0.8221 towards 0.8867 fibonacci level.

In the bigger picture, rise from 0.8221 medium term bottom is seen as a corrective move. While further rally cannot be ruled out, upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Considering bearish divergence condition in D MACD, firm break of 0.8631 support will be the first sign that this corrective bounce has completed. Sustained trading below 55 W EMA (now at 0.8549) will confirm, and bring retest of 0.8221 low.

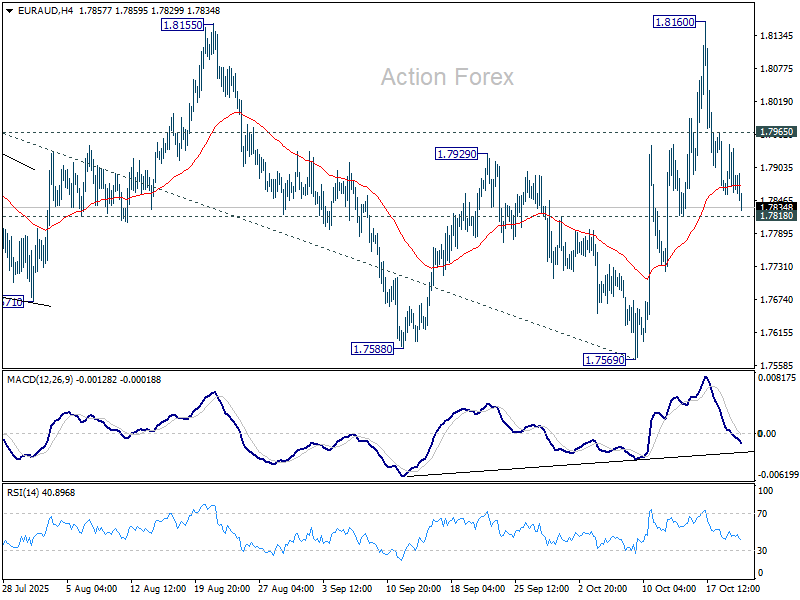

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7846; (P) 1.7896; (R1) 1.7931; More...

Intraday bias in EUR/AUD remains neutral and outlook is unchanged. With 1.7818 support intact, further rally is in favor. On the upside, above 1.7965 will turn bias back to the upside for retesting 1.8160 first. Firm break there will affirm the case that larger up trend is resuming, and target 1.8554 high next. On the downside, however, break of 1.7818 will dampen this bullish view and turn focus back to 1.7569 support instead.

In the bigger picture, price actions from 1.8554 medium term top are seen as a corrective pattern, which might have completed already. Firm break of 1.8554 will resume larger up trend from 1.4281 (2022 low), and target 61.8% projection of 1.5963 to 1.8554 from 1.7569 at 1.9170. Nevertheless, break of 1.7569 support will delay the bullish case and extend the correction from 1.8554.

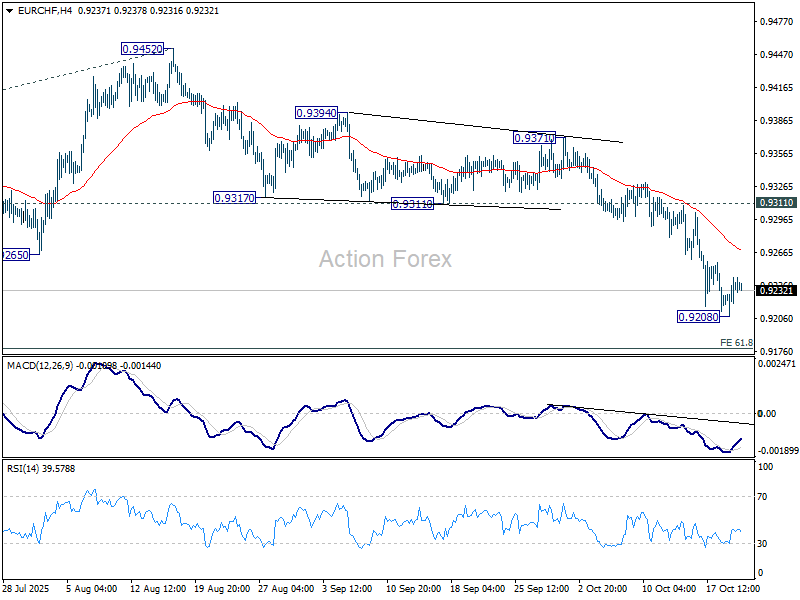

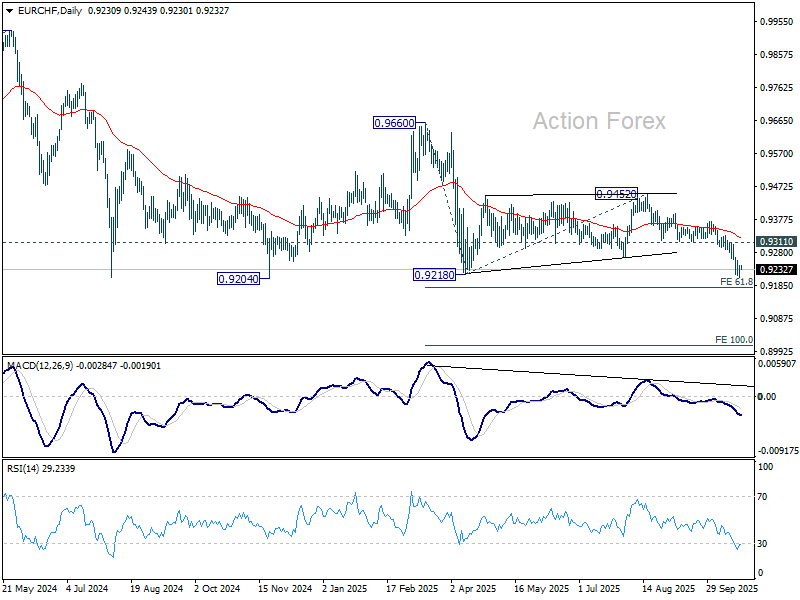

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9218; (P) 0.9231; (R1) 0.9252; More...

Intraday bias in EUR/CHF is turned neutral first with current recovery, and some consolidations could be seen. Outlook will remain bearish as long as 0.9311 support turned resistance holds. On the downside, break of 0.9208 will target 61.8% projection of 0.9660 to 0.9218 from 0.9452 at 0.9179. Firm break there will target 100% projection at 0.9010.

In the bigger picture, outlook remains bearish with EUR/CHF staying well inside long term falling channel after multiple rejection by 55 W EMA (now at 0.9390). Firm break of 0.9204 will resume the whole down trend from 1.2004 (2018 high). Next target is 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. Break of 0.9452 resistance is needed to be the first sign of medium term bottoming.

Gold, Silver Tumble, Oil Rebounds

It just took a few hours for gold and silver bulls to take profit and move to the sidelines yesterday, leading to the biggest price pullback across both precious metals. Gold fell more than 5% and silver tumbled nearly 7%. The selloff continued in early Asian trading before dip buyers kicked in. For gold, we saw a quick rebound approaching the $4,000 mark, while silver found demand near the $47.50 mark.

Why precious metals sold off yesterday—and whether this is the beginning of a broader correction—remains to be seen. But looking at yesterday’s action, the pullback was triggered by hopes of easing trade tensions between the US and China and a rebound in the US dollar. Yet, tensions are far from guaranteed to ease—not this week and probably not during Trump’s entire mandate at the White House—and the US dollar’s rebound may be reversed by persistent, and very much alive, dovish Federal Reserve (Fed) expectations. Plus, the US government remains shut, and debt worries in the Western world have not eased. On the contrary, French debt was just downgraded last Friday and the divided government there makes any budget deal look terribly complex. The UK just printed its second-biggest borrowing for April to September since records began in 1993 (the other was during the pandemic), while Japan just appointed Takaichi as its next PM—and she is willing to expand government spending.

So, what probably better explained yesterday’s precious metals selloff was mainly the fact that the metals are now trading in deeply overbought market conditions with heightened volatility. The gold volatility index has spiked this October to its highest level since March 2022. If history is any guide, gold retreated 20% following that volatility spike. And given the latest euphoria, crowded speculative long positions and overbought conditions, a further price pullback is possible—without, however, threatening gold’s role in long-term portfolios. Gold has become the go-to asset for global investors—from retail to institutions and central banks—seeking protection from sovereign debt worries, trade and geopolitical jitters and inflation: factors that have become today’s reality. That won’t change overnight. Some, therefore, see the price pullback as an opportunity to strengthen long positions.

While gold and silver bulls were having a hard time yesterday, oil traders breathed a sigh of relief, with a more than 1% rebound yesterday followed by another 1.2% gain in Asia. But here, the opposite scenario is unfolding. Oil has fallen near oversold territory on murky global demand outlooks and ample OPEC supply, which are expected to lead to a supply surplus this year. While a softer dollar—normally improving EM demand for energy—and prospects of Fed rate cuts haven’t boosted crude appetite since summer, cheaper oil could improve appetite for US 10-year Treasuries by taming inflationary pressures and justifying lower Fed rates. The US 10-year yield fell below the 4% mark yesterday, while the US dollar strengthened despite the ongoing US government shutdown—which, fundamentally, is not good news for US fiscal health. Go figure!

This morning, the US dollar is offered, as the EURUSD meets support near the 1.16 mark—which, by the way, is technically insignificant and wouldn’t necessarily hold bears back from further selling. The USDJPY is also retreating from above 152—again, technically insignificant apart from being a round number. With the French downgrade and the Japanese Takaichi trade mostly factored in, the next direction in major FX pairs will likely depend on the US dollar—and that will most likely hinge on the CPI figures due this Friday.

The good news is that earnings are coming in quite nicely, keeping stock market appetite alive, and there are signs investors are preparing for further Fed dovishness by closing short positions. Speaking of earnings, Coca-Cola delivered better-than-expected quarterly results, while GM raised its full-year profit target as it trims its struggling EV business and refocuses on its money-making gas-powered models in an environment where climate concerns are out of the window. GM also now expects the tariff impact to be half a billion dollars less than previously estimated. Elsewhere, Zions Bancorp—which was part of last week’s bad-loan stress—topped profit estimates despite a $50 million loss tied to alleged fraud, easing bad-credit concerns among regional US banks. Netflix disappointed after the bell and fell 6.5% in after-hours trading, though the miss was due to a tax dispute—without which results would have been broadly in line. Tesla and IBM report today.

And speaking of short positions being closed into next week’s much-expected Fed cut, Beyond Meat—one of the most shorted stocks on the market—jumped around 127% on Friday and another 146% yesterday. Yesterday’s rally was also fueled by the announcement of its new US distribution deal with Walmart, but other heavily shorted names such as Krispy Kreme and 1-800-Flowers.com also gained more than 10% each. Affaire à suivre.

Bank of England Eyes CPI Figures Ahead of November Interest Rate Decision

In focus today

The data front remains relatively quiet; however, keep an eye on the UK CPI inflation data for September, which will likely determine whether a Bank of England rate cut will be considered in November.

Economic and market news

What happened overnight

In the Ukraine war, a summit between US President Trump and Russian President Putin was cancelled, following productive talks between US secretary of state Rubio and Russian foreign minister Lavrov. The summit was expected to further talks on ending the war.

In Japan, September exports rebounded to 4.2% y/y after four months of contraction. However, this fell slightly short of market expectations of 4.6%, despite support from the weak yen. Imports also climbed back in the positives to 3.3%, severely overshooting consensus expectations of just 0.6%. While the Japanese economy does appear to be regaining its footing, US tariffs continue to weigh on the economy.

What happened yesterday

In Canada, September's CPI figures slightly exceeded expectations, reaching 2.4% y/y (cons: 2.3%), largely driven by rising food prices. The Bank of Canada's core measure climbed to 2.8% y/y from 2.6% y/y and may be a deciding factor ahead of the monetary policy meeting one week from now.

In Hungary, the central bank decided to maintain interest rates at 6.50% as expected.

Equities: Equity markets ended marginally higher yesterday, led by gains in the Far East, while Europe and the US were largely unchanged. There was a modest tilt toward cyclicals, but it was not a macro-driven session, rather, another day where earnings dictated sector moves. With few macro or geopolitical headlines, earnings are now firmly in the driver's seat, and dispersion across sectors is being dictated by micro fundamentals. From our perspective, it was encouraging to see both healthcare and industrials deliver strong earnings and solid performance yesterday. That said, the real story yesterday came from the commodity space, where gold and silver both suffered heavy losses, gold down almost 6%, silver more than 7%. This hit sentiment in the broader materials complex. In the US yesterday, Dow +0.5%, S&P 500 +0.00%, Nasdaq -0.2% and Russell 2000 -0.5%. This morning with a mixed picture in Asia, while European futures are lower and US futures are marginally higher.

FI and FX: The positive risk appetite took a breather, with precious metals notably lower, while front-end US yields were largely unchanged. The bullish flattening trend continued, as long-end US yields declined further, with the 10-year Treasury yield down 2bp. EUR/USD is consolidating around 1.16 in another session dominated by a broadly stronger dollar, while USD/JPY trades near 152 following continued JPY weakness. Both EUR/SEK and EUR/NOK extended their declines.

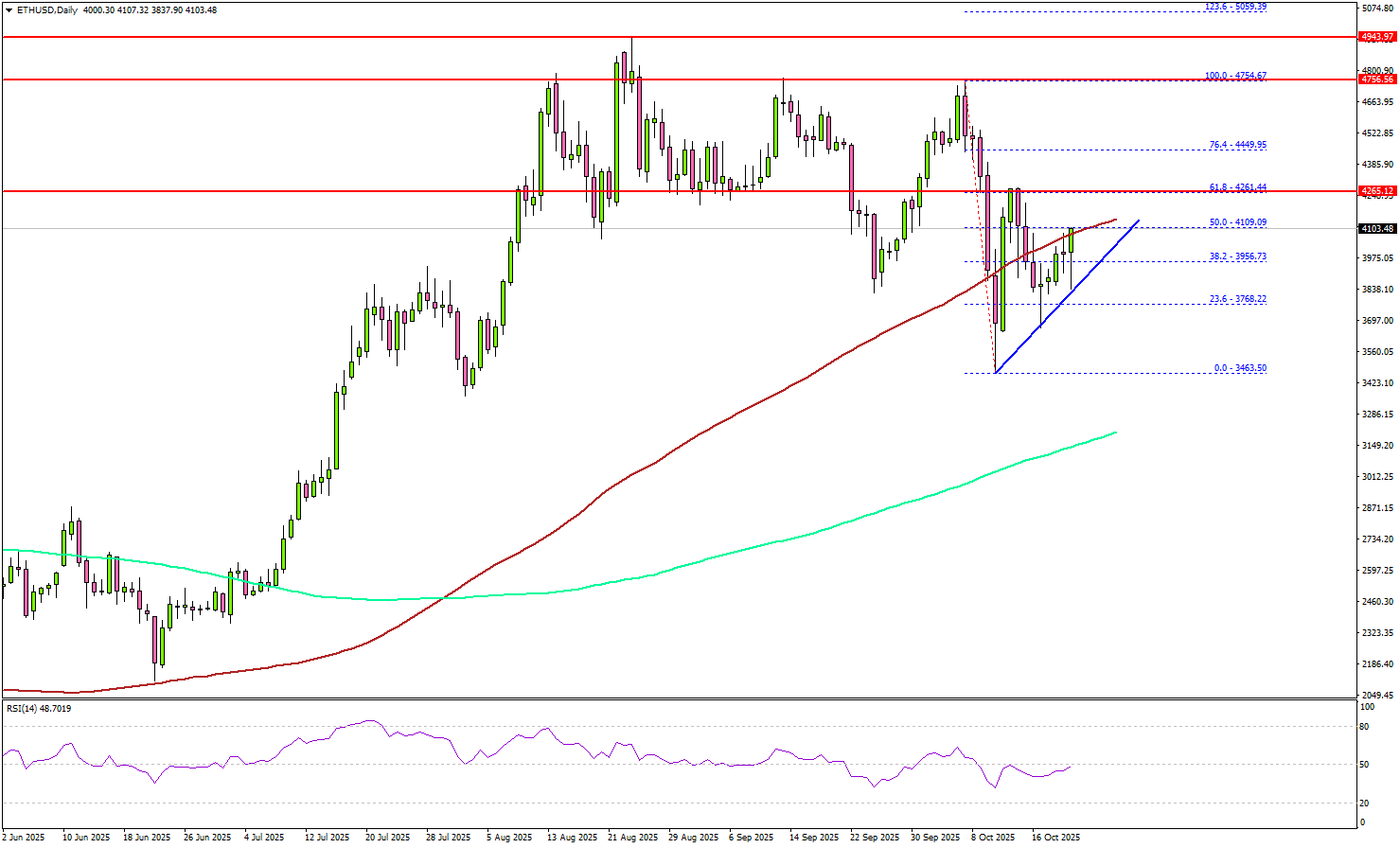

Ethereum Recovery Gains Traction, Yet Resistance Looms Large

Key Highlights

- Ethereum found support near $3,450 and started a decent upward move.

- ETH is following a connecting bullish trend line with support at $3,950 on the daily chart.

- Bitcoin price rallied over 5% but faced hurdles near $115,000.

- XRP is eyeing an upside break above the $2.650 barrier.

Ethereum Technical Analysis

Ethereum dipped below $3,800 before the bulls appeared. ETH found support near $3,450, bounced higher, and surpassed $3,650.

Looking at the daily chart, the price surpassed the 50% Fib retracement level of the downward move from the $4,754 swing high to the $3,463 low. The current price action is positive, near the 100-day simple moving average (red).

On the upside, the price is facing hurdles near the $4,260 level or the 61.8% Fib retracement level of the downward move from the $4,754 swing high to the $3,463 low.

The next major resistance is near the $4,450 level. A daily close above the $4,450 resistance zone could start another steady increase. In the stated case, the price may perhaps rise toward the $4,750 level. The next stop for the bulls may perhaps be $5,000.

On the downside, the bulls might be active near $3,950 and a connecting bullish trend line. The main support is now forming near $3,720, below which the price could slide toward $3,550. Any more losses might call for a move toward $3,450.

Looking at Bitcoin, there was a sharp upward move, and the bulls were able to clear the $111,500 and $112,500 resistance levels.

Economic Releases

- Fed's Musalem speech.

- ECB's President Lagarde speech.

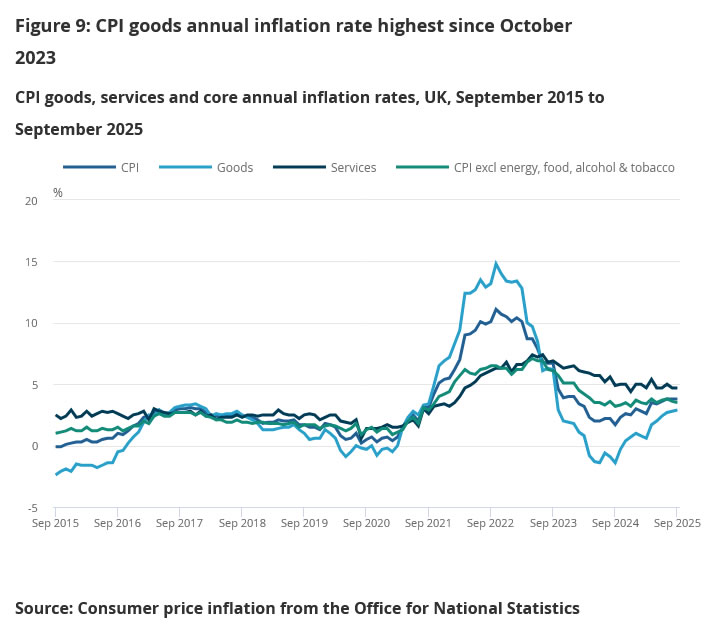

UK CPI at 3.8% in September, undershoots expectations of 4.0%

UK inflation came in softer than expected in September. Headline CPI was unchanged at 3.8% yoy, below consensus of 4.0%. Core CPI (excluding energy, food, alcohol and tobacco) eased to 3.5% from 3.6%.

Breakdowns showed a mixed picture under the surface. CPI goods component rose marginally from 2.8% yoy to 2.9%, highest since October 2023. Services inflation held unchanged at 4.7%.

On a monthly basis, consumer prices were flat, another sign that the inflation pulse has moderated heading into the final quarter of the year.