Sample Category Title

Sunset Market Commentary

Markets

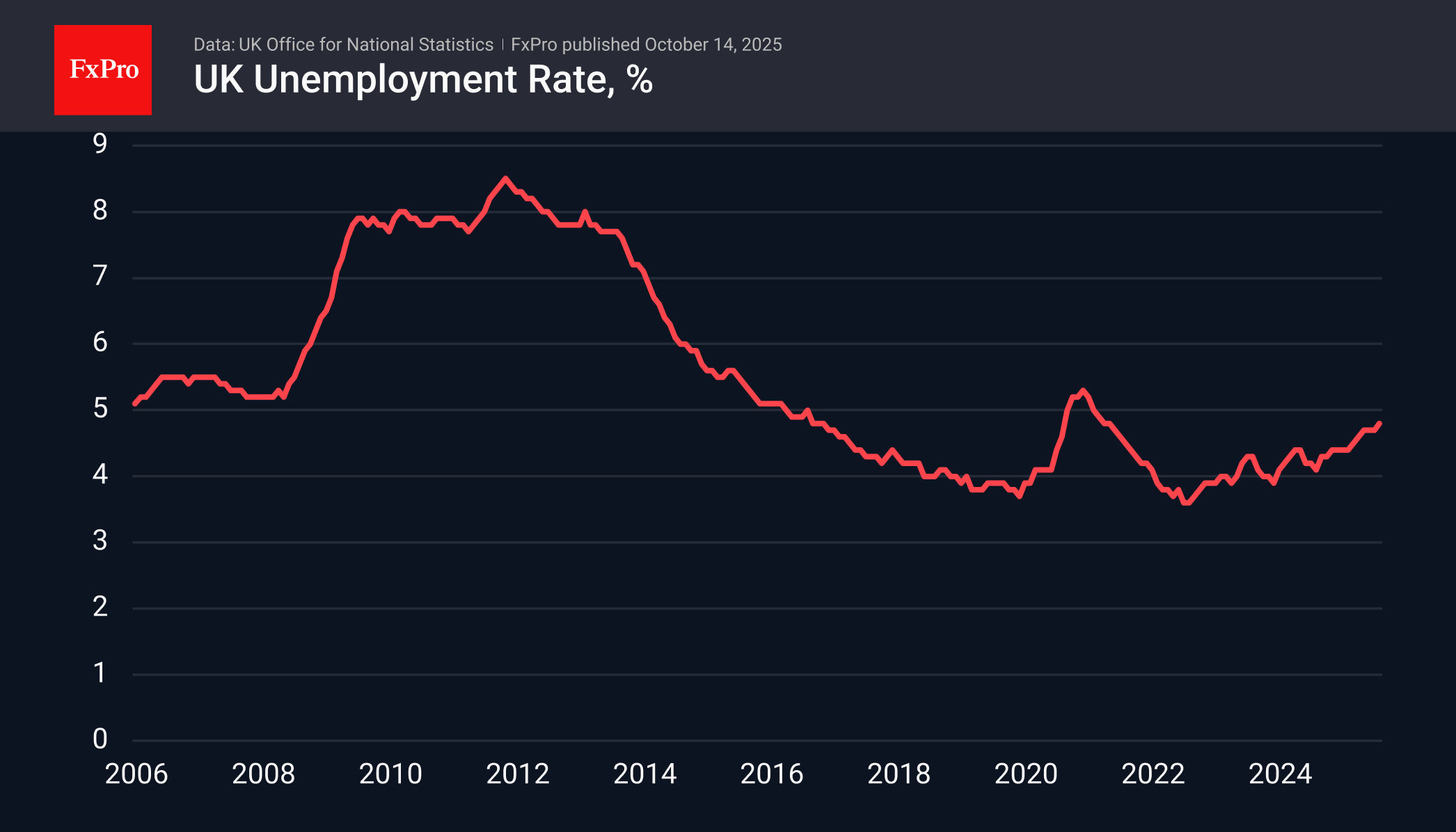

Market relevant data are rather scarce these days. UK labour market data in this respect at least provided some kind of ‘distraction’. Even so, the market reaction told least as much on reigning market sentiment as on a reassessment on the basis of the data content. The UK labour market report can be labelled as being soft. Monthly employment data declined 10k jobs in September, but indications over the previous months shows some signs of bottoming. August earnings data (3M/Y/) also were a bit mixed but markets apparently focused on private earnings excluding bonuses slowing from 4.7% Y/Y to 4.4%. It is seen as an indication of an easing of wage pressures (annex inflation). The unemployment rate also rose from 4.7% to 4.8%. ‘Optimists’ on the other hand could have pointed to revisions from data released earlier this year indicating that job losses after last year’s UK budget measures probably were less than feared. Even so, markets still saw the data as reinforcing the case for the BOE to maybe consider further easing sooner rather than later. Gilts outperform Bunds and Treasuries, declining between 6 bps (2-y) and 7 bps (10 & 30-y). In a congruent move, sterling is touching the lowest levels against the dollar since early August (Cable 1.326). EUR/GBP regains the 0.87 barrier (0.871).

On other markets, a risk-off sentiment again reigns after yesterday’s (equity) rebound as markets are pondering a new flaring up of trade tensions between the US and China. China retaliated against the US shipping sector after president Trump end last week threatened with additional tariffs and restrictions on US chips exports to China. US indices show losses between 1.3% (Dow) and 2% (Nasdaq) even as some major US reported stronger than expected/solid Q3 results. The EuroStoxx 50 is ceding 0.75%. In this risk-off context, US Treasuries only show modest gains, if any (2-y yield -1 bp, 30-y little changed). 2-y and the 10-y yields nearing key support at 3.5% and 4% respectively probably makes markets cautious on a stronger safe haven bid. Bunds outperform with yields declining between 2.5 bps (2-y) and 4 bp (30-y). We assume this move is also mainly due to the global risk-off sentiment rather than markets really positioning for additional ECB easing. Even so, EMU money markets now again see a >50% chance of one additional ECB rate cut next year. On FX markets, the trade-weighted dollar fails to maintain initial modest gains (DXY 99.3). The Aussie dollar is a major victim of escalating trade tensions between the US and China (AUD/USD 0.645). At the same time USD/JPY even drifts marginally lower just (152 area). EUR/USD tested the 1.1550 area. European markets are assessing the potential consequences of the budget speech of French PM Lecornu before Parliament. Amongst others, the PM apparently is prepared to suspend the pension reform to get support for some 2026 budget consolidation. At EUR/USD 1.158, the euro at least trades off the intraday lows and so do European equities. Markets apparently favour a French ‘kicking-the-can-down-the road’ scenario, rather than outright chaos.

News & Views

The International Energy Agency expects next year’s oil oversupply will be even bigger than previously thought. It now pencils in a record overhang of almost 4 mln barrels a day, or roughly 18% more than last month’s update. The revision came amid the oil producing cartel OPEC+ continuing to revive output. The IEA also assumes that non-OPEC output will increase by 1.2 mln a day next year, up 200k from the September projection. As far as demand is concerned, they forecast an increase by a well-below-trend 700k barrels a day for both this year and the next. The supply-demand mismatch led to a sharp rise in inventories by 1.9 mln barrels a day this year. While the impact on oil prices has been mitigated by China absorbing up the majority, the IEA warned that’s now beginning to change. Brent oil today drops to $62/b and is set to close at its lowest level since early May.

Chinese companies looking to operate in the European Union may soon be forced to hand over technology to EU firms, according to people familiar with the matter. The measures would apply to those seeking access to what it considers key digital and manufacturing markets such as cars and batteries. The rules would additionally require the firms to use a set amount of EU goods or labour and to create added value on EU soil. The people said they expect the measures to be applicable from November and to all non-EU firms. However, one said that the goal is to keep China’s manufacturing from overwhelming the European industry. Key to the proposal is the focus on the transfers of battery technology know-how, aimed at reducing reliance on China while strengthening the European EV industry.

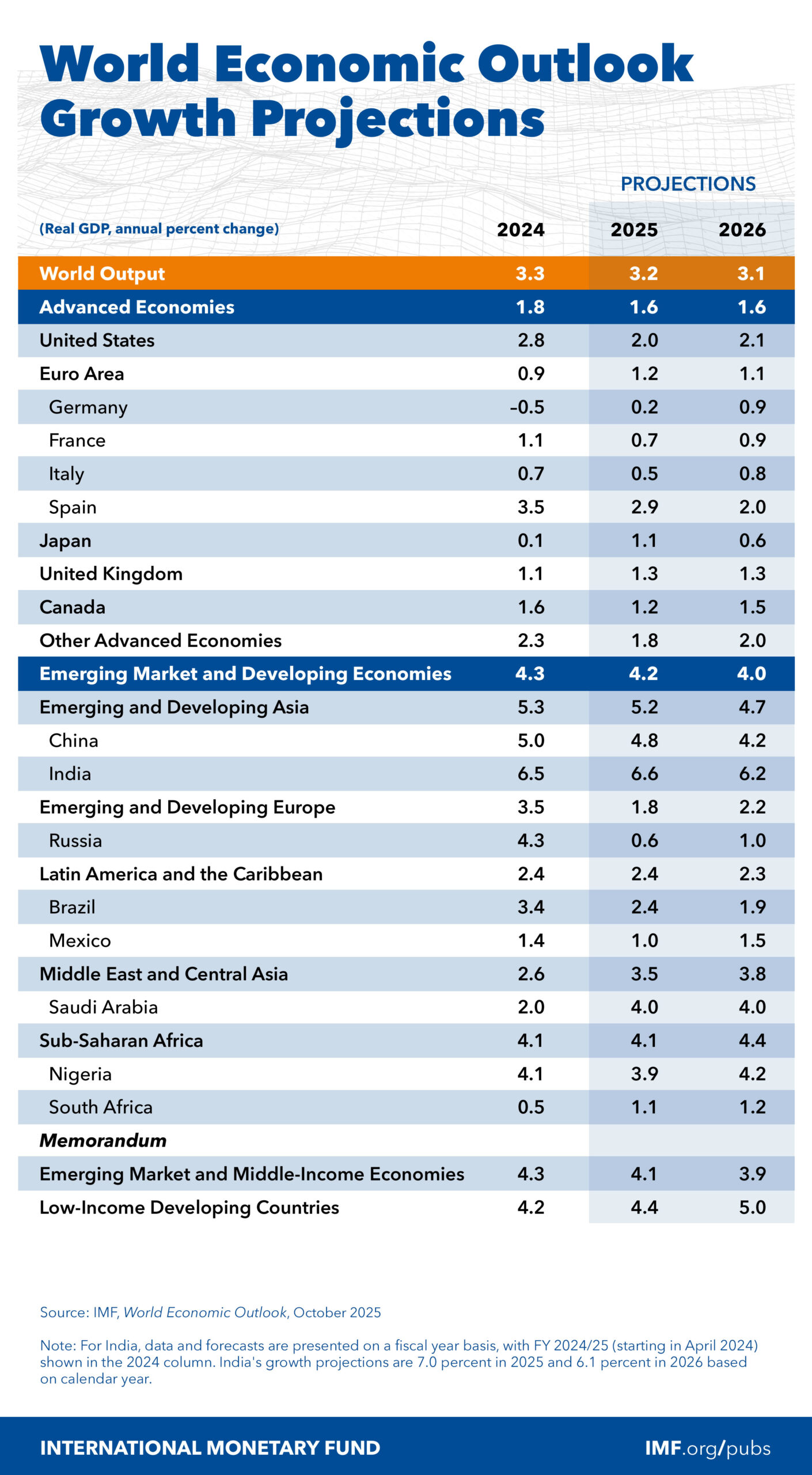

IMF: Global growth seen at 3.2% in 2025, risks tilted to downside

The IMF’s World Economic Outlook had global growth projections revised modestly higher from April. The Fund now expects global growth to ease from 3.3% in 2024 to 3.2% in 2025 and 3.1% in 2026.

The update shows mixed regional outlook. The U.S. economy is projected to grow 2.0% in 2025 and 2.1% in 2026. Eurozone is expected to grow only 1.2% in 2025 and 1.1% in 2026. The U.K. is forecast to expand at a steady 1.3% pace in both years, while Japan’s growth is seen slowing from 1.1% to 0.6%. Meanwhile, China’s output is expected to decelerate from 4.8% in 2025 to 4.2% in 2026.

Despite the incremental upgrades, the balance of risks remains tilted to the downside. The IMF warned that prolonged geopolitical uncertainty, rising protectionism, and labor supply shocks could further constrain growth, while fiscal vulnerabilities and potential market corrections pose threats to global financial stability. It also cautioned that a continued erosion of institutional credibility in several economies could weigh on investment and confidence.

On prices, the IMF said global inflation is set to continue moderating, but the pace will vary widely. Inflation is projected to remain above target in the US where upside risks persist.

US: Small Business Optimism Retreats in September

The NFIB's Small Business Optimism Index fell 2 points to 98.8 in September, marking the first decline in three months. As optimism declined, the level of uncertainty rose, with the corresponding index rising 7 points to 100 – the fourth-highest reading in about 50 years.

Five out of ten subcomponents fell on the month, two improved, and three remained unchanged. The largest pullbacks were in expectations about an improvement in the economy (-11 points to 23%), current inventory (-7 points to -7%), expected credit conditions (-3 points to -7%) and the belief that now is a good time to expand (-3 points to 11%).

Labor market indicators were mixed. The average change in employment per firm was negative for the fourth month in a row. The net share of businesses planning to increase employment rose one point for the fourth month in a row to 16%, while the share of firms with unfilled job openings remained unchanged at 32%. The latter has fallen notably over the last several quarters, though it remains comfortably above its long-term average of 22%.

Quality of labor concerns fell 3 points, with 18% of business owners identifying this as their top business problem – tied with the share of owners reporting taxes as their top business problem. Meanwhile, the share of firms reporting "few or no qualified workers for job openings" surged 7 points to 50%, completely reversing the decline of the two months prior.

Inflation concerns appeared to make a comeback, with 14% of businesses reporting this as their top problem (up 3 points on the month, and the first increase since mid-2024). The share of businesses 'raising' average selling prices rose 3 points to 24%, while the share of firms 'planning’ to raise average selling prices ahead rose 5 points 31% – both measures remain above their historical averages.

Key Implications

While a weaker showing, September's NFIB reading is basically in line with its historical average, but the subcomponents reveal a nuanced backdrop. In the absence of last month's (BLS) jobs report, today's NFIB report adds credence to the view that there was little progress made on the hiring front in September, with small business job creation stuck in shallow negative territory for several months now. On a more positive note, hiring intentions have trekked consistently higher in recent months. This could work in favor of a moderate turnaround in job creation, but the fact that uncertainty is near record highs is likely to take some wind out of these plans.

The Fed has put more of an emphasis on its 'maximum employment' mandate recently as it restarted rate cuts, and while recent labor market data lend support to this narrative, more work also remains to be done on the inflation front. The uptick in the NFIB price metrics and inflation concerns in September speak to difficulties that the Fed will continue to face as it leans toward additional rate cuts, at a time when inflation is still elevated. A recent rekindling to the U.S.-China trade conflict is likely to add to that difficulty.

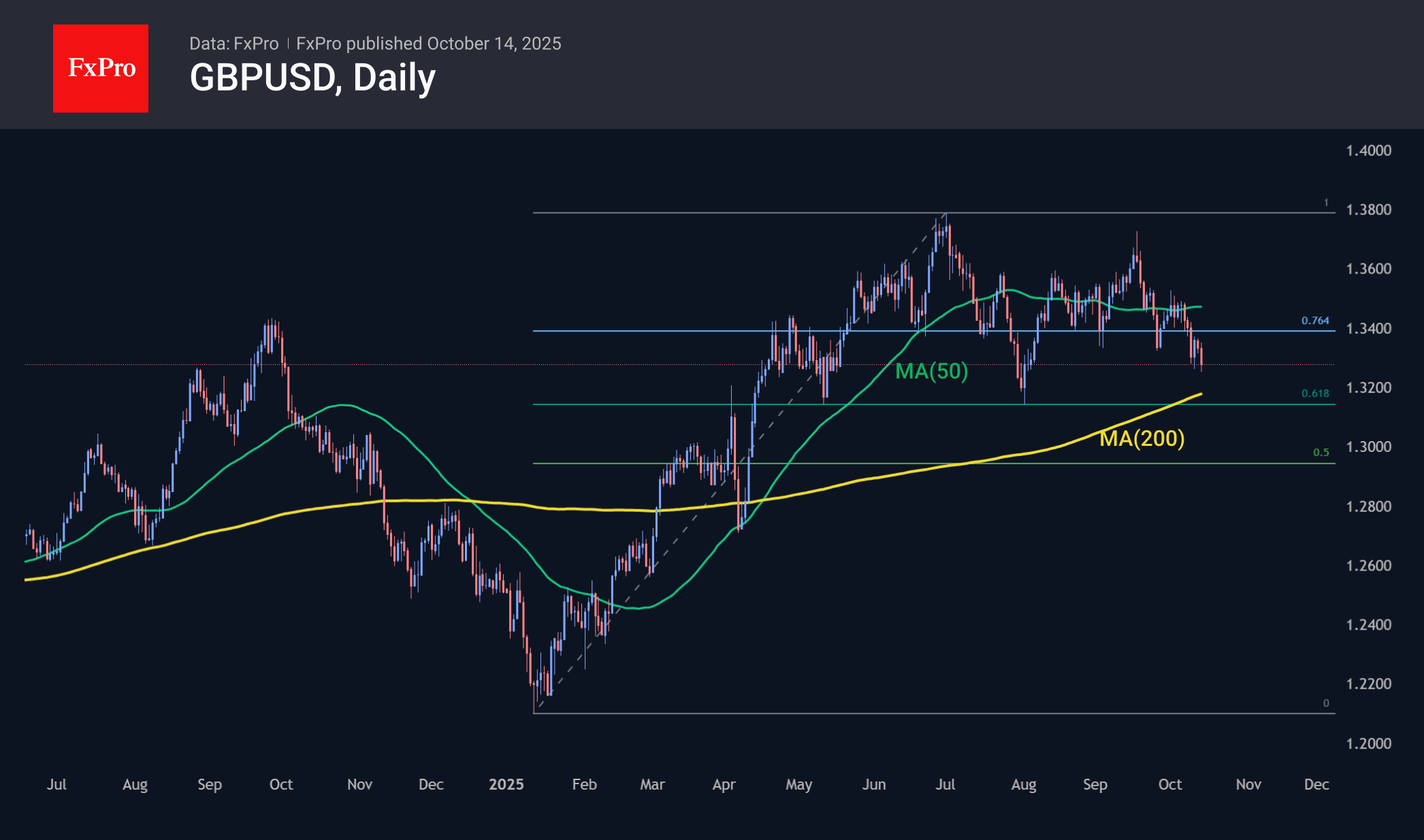

Pound Continues to Decline, Important Support Test Ahead

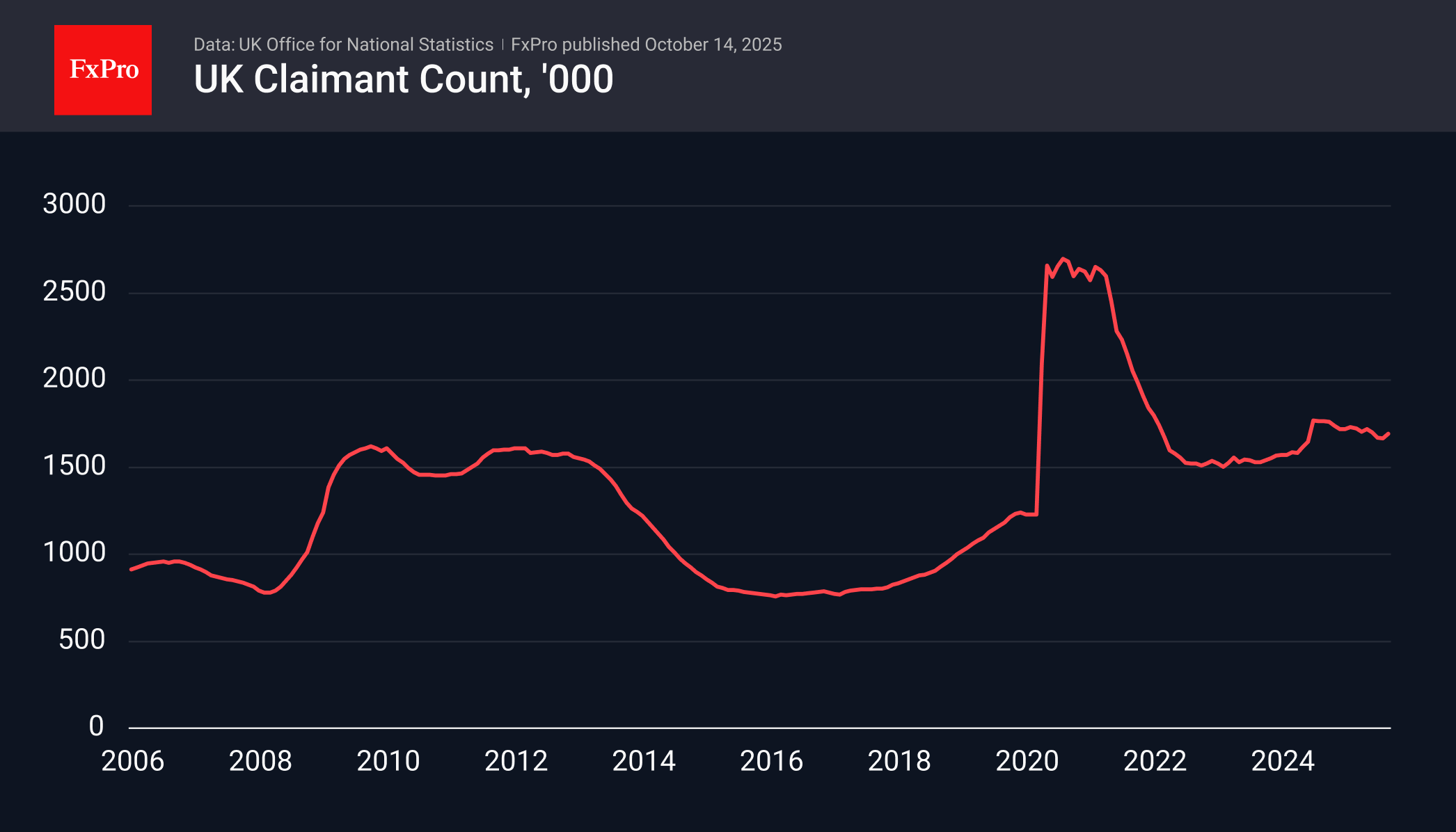

The number of applications for unemployment benefits in the UK rose by 25.8K in September after three months of decline, totalling 50.8K and a stronger-than-expected 10K increase. The unemployment rate for the three months to August rose to 4.8%, the highest since May 2021, although average forecasts had predicted no change.

The deterioration in the labour market opens the door for softer rhetoric from the Bank of England. In modern history, major developed economies have often moved in lockstep with the Fed when it eased policy. Although the Bank of England did its part earlier this year, it is possible that the slowdown in the US economy will also put pressure on Britain, in addition to tariff disputes, and will be a sobering factor after a period of strong growth in the service sector, which drove GDP upwards after 2022.

The worse-than-expected figures triggered a decline in the pound, which had been gaining on Friday and remained steady on Monday. GBPUSD touched 1.3250, its lowest level since early August. The pair has been on a short-term downward trend for the past seven days. It is also worth noting that the pair reached a local peak on the day of the Fed’s key rate cut on 17 September, after which dollar buyers became more active, despite the dovish tone of the news.

Taking a step back, we can see the formation of a double top with highs at the end of June and mid-September.

In its decline over almost a month, GBPUSD is heading towards 1.3140, the 61.8% area of growth from the lows at the beginning of the year to the peaks at the start of July. This level stopped the pair’s correction in July, maintaining its growth pattern. Just above, at 1.3180, is the 200-day moving average. Consolidation below these levels would be two confirming signals of a reversal in the dollar trend. But it is also important for us that the dollar has turned to growth despite weak data. Working against fundamental news is a very important indicator of the internal strength and confidence of the bulls.

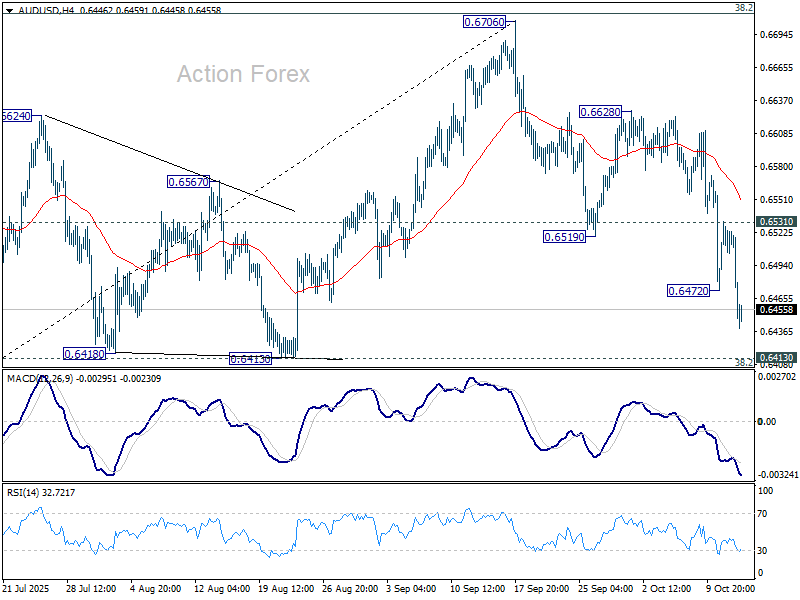

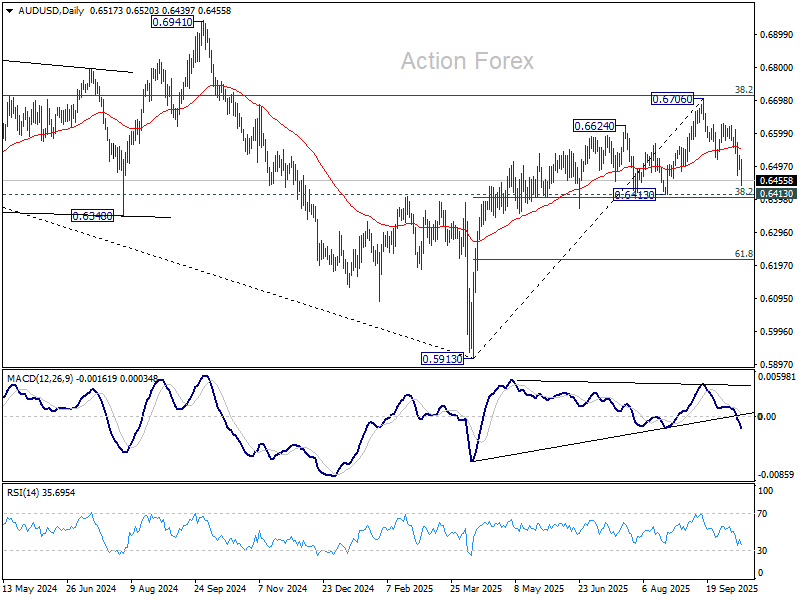

AUD/USD Mid-Day Report

Daily Pivots: (S1) 0.6492; (P) 0.6513; (R1) 0.6534; More...

AUD/USD's fall from 0.6706 resumed by breaking through 0.6472 and intraday bias is back on the downside for 0.6413 cluster support (38.2% retracement of 0.5913 to 0.6706 at 0.6403). Sustained break there will pave the way to 61.8% retracement at 0.6216. On the upside, above 0.6513 minor resistance will turn intraday bias neutral again first.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. Outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, sustained break of 0.6713 will be a strong sign of bullish trend reversal, and pave the way to 0.6941 structural resistance for confirmation.

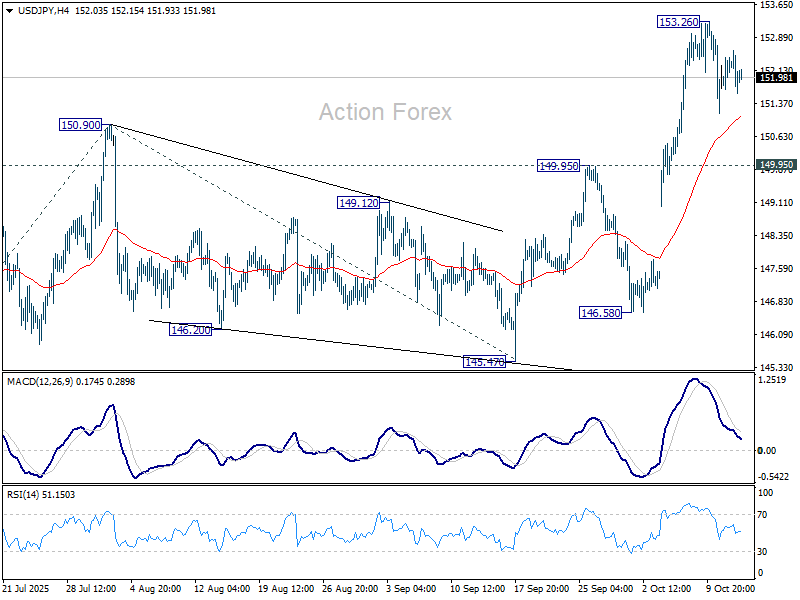

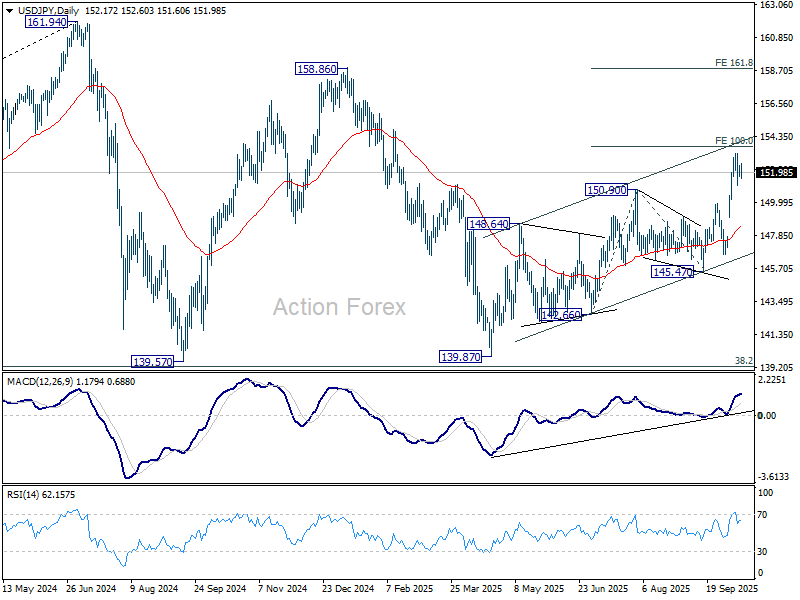

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 151.86; (P) 152.16; (R1) 152.59; More...

USD/JPY is staying in consolidations below 153.26 and intraday bias stays neutral. Downside should be contained above 149.95 resistance turned support. Break of 153.26 will target 100% projection of 142.66 to 150.90 from 145.47 at 153.71. Firm break there will pave the way to 161.8% projection at 158.80. However, decisive break of 149.95 will bring deeper pullback to 55 D EMA (now at 148.48) instead.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 145.47 support will dampen this bullish view and extend the corrective pattern with another falling leg.

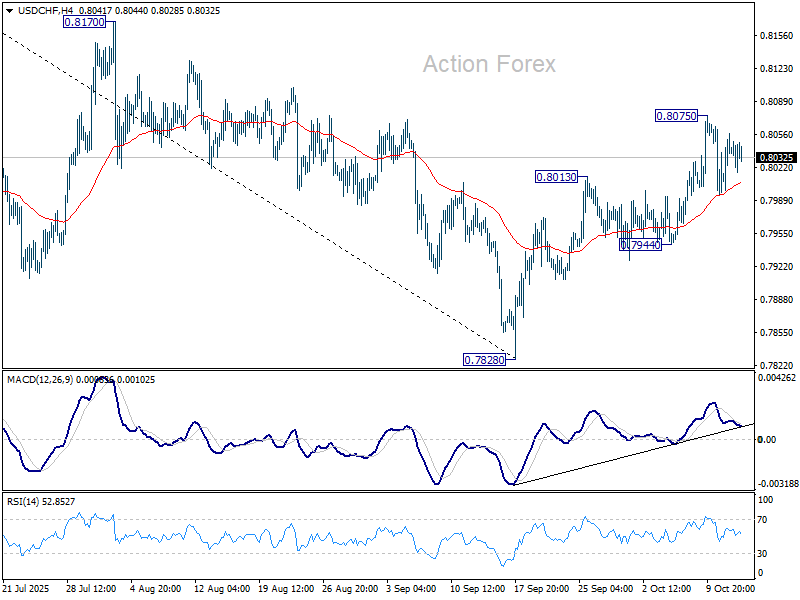

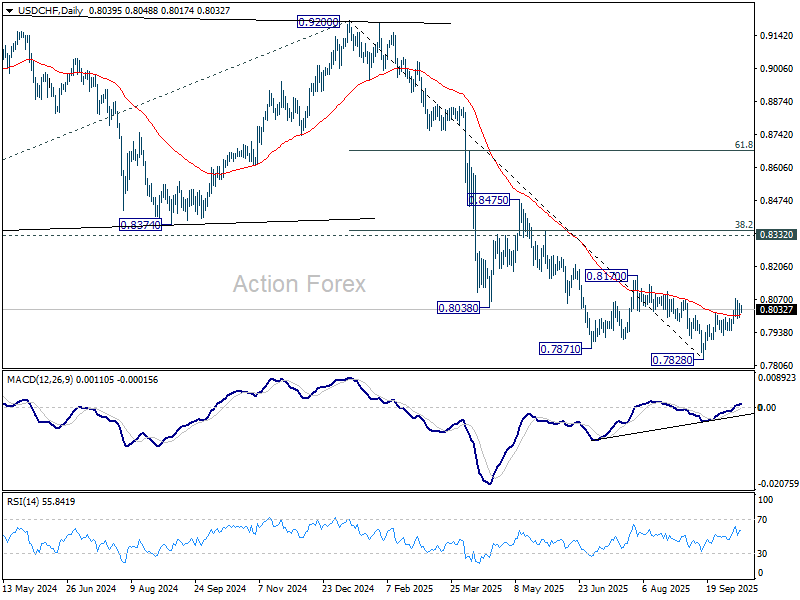

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8009; (P) 0.8033; (R1) 0.8067; More…

USD/CHF is staying in consolidations below 0.8075 and intraday bias stays neutral. Price actions from 0.7828 are currently seen as correcting whole fall from 0.9200. Above 0.8075 will target 0.8170 resistance next. On the downside, though, break of 0.7944 support will bring retest of 0.7828 low instead.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

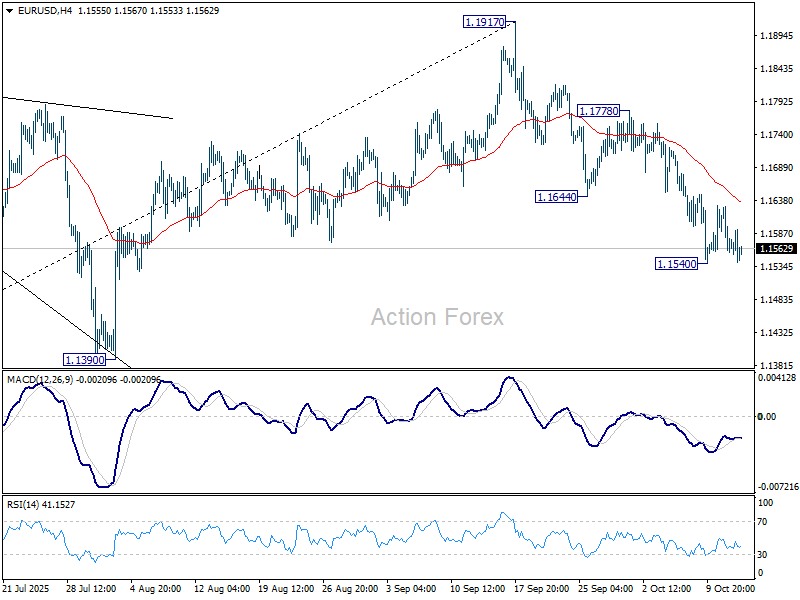

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1542; (P) 1.1586; (R1) 1.1614; More…

EUR/USD is staying in range above 1.1540 and intraday bias stays neutral. Deeper decline is expected as long as 1.1778 resistance holds. On the downside, break of 1.1540 will resume the fall from 1.1917 to 1.1390 , or further to 38.2% retracement of 1.0176 to 1.1917 at 1.1252.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1274) holds, the up trend from 0.9534 (2022 low) is still extended to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep outlook bearish.

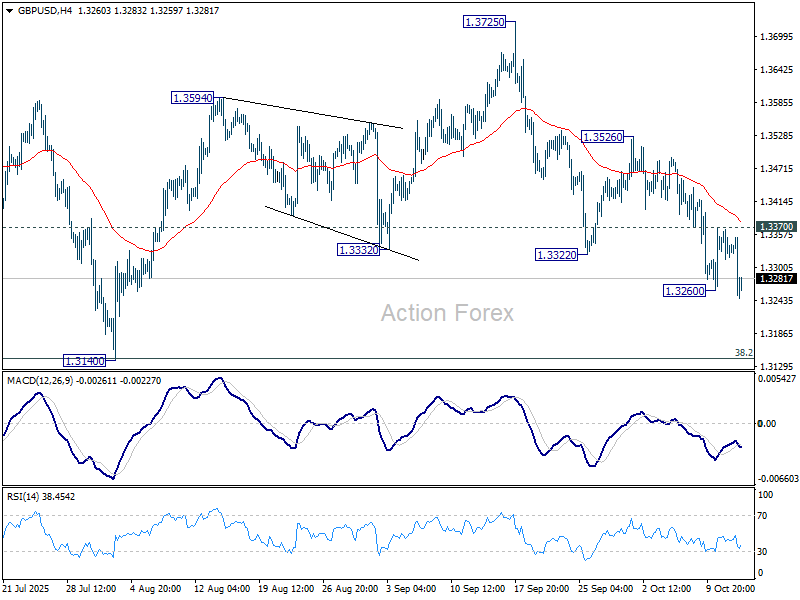

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3309; (P) 1.3338; (R1) 1.3360; More...

Breach of 1.3260 suggests that GBP/USD's fall is resuming. Intraday bias is back on the downside for 1.3140 cluster (38.2% retracement of 1.2099 to 1.3787 at 1.3142). Strong support is expected from there to complete the corrective pattern from 1.3787. On the upside, above 1.3370 minor resistance will turn intraday bias neutral first.

In the bigger picture, rise from 1.0351 (2022 low) is still seen as a corrective move. Further rally could be seen to 61.8% projection of 1.0351 to 1.3433 (2024 high) from 1.2099 (2025 low) at 1.4004. But strong resistance could emerge from 1.4248 (2021 high) to limit upside. Sustained break of 55 W EMA (now at 1.3173) will argue that a medium term top has already formed and bring deeper fall back to 1.2099.