Sample Category Title

Insatiable appetite for AI and Gold

With little surprise, major US indices went on to print fresh all-time highs yesterday, again fueled by technology and AI. In fresh news, Elon Musk’s xAI secured $20 billion in funding — including from Nvidia, SoftBank bought ABB’s robotics division, intensifying its bet on what it calls “Physical AI,” which it believes will be the next big thing within artificial intelligence. Investors loved it — to say the least — with SoftBank soaring 10% in Tokyo, helping the Nikkei remain bid near record highs.

Also, earlier this week, Dell doubled its growth estimates for sales and profit for the coming two years, saying they were “wrong about how big [they] thought the AI market was two years ago” and that “it’s nothing but bigger.” That sentiment was echoed by JPMorgan CEO Jamie Dimon, who acknowledged that demand for AI has turned out to be far stronger than many anticipated. He revealed that JPMorgan is now spending about USD 2 billion per year on AI initiatives — and, strikingly, those investments are already being offset by equivalent cost savings.

So again, I won’t defend that the market is not in a bubble — but I don’t see where the reports that AI is not worth investing in are coming from. Anyway, the AI rally continues full speed in the US, with Nvidia up 2% yesterday, Tesla — which wants to internalize xAI — gaining 1.3%, Dell jumping 9%, and the Nasdaq 100 pushing to a fresh record high above 25,000.

All that came as the FOMC minutes hinted at further rate cuts down the road — but with many officials still worried about inflation risks. That means any flare-up in inflation data could quickly reverse the Federal Reserve’s (Fed) easing path. The good news is: no major data are being released right now as the US government remains shut. The 2-year yield, which best captures Fed expectations, remains steady just below 3.60%, while the 10-year yield is holding sideways after a $39 billion debt sale that fell just short of expectations.

In FX, the US Dollar is softer this morning after having bounced to a 2-month high on weaker appetite for the euro and yen. The kiwi rebounded after hitting its lowest level since April following a surprise 50 bp cut from the Reserve Bank of New Zealand (RBNZ), which left the door open for further easing, arguing that the economy’s weakness had become too pronounced to wait, while inflation is showing signs of easing. Poland also unexpectedly cut rates, citing easing inflation pressures, while the Bank of England (BoE) warned that stretched valuations for AI companies and growing concerns about the Fed’s independence increased the risk of a “sharp market correction” that could spill over into global markets. Funny enough, the UK has such limited exposure to AI — and such pressing fiscal issues — that the warning went largely unheard by investors. Sterling remains very much unloved heading into the Autumn Budget. Even though French political shenanigans have capped the upside in the EURGBP since late September, the outlook remains more supportive for continental Europe than for the UK, where sluggish growth, persistent fiscal pressures and a hesitant Bank of England continue to weigh on sentiment.

One place where there’s no hesitation is gold. The bullion finally soared past the $4,000 per ounce mark yesterday on the back of diminished appetite for traditional currencies including the euro, dollar, sterling and yen — alongside strong central bank buying and renewed uncertainty around the US government shutdown. A question that constantly comes up is whether gold has more room to run. Unlike equities, we don’t have valuation ratios to judge whether gold has become “too expensive.” The yellow metal also enjoys solid retail demand, particularly during China’s Golden Week and India’s wedding season. But the physical leg is not the major explanation. Gold rallies because investors believe it has value. How much value? As much as people think it has. If one Bitcoin is trading above $120,000, gold surely has endless upside potential, as well. So yes, even with record-high prices, the medium-term outlook for bullion remains positive. Many investors already eye a move toward $5,000 and above.

For the rest of the week, and in the absence of US economic data, investors will focus on the first batch of US earnings, with results from Delta, Pepsi, Levi’s and BlackRock due to be released. The spotlight will be on how firms are navigating a still-resilient economy, sticky costs and shifting rate expectations all of which could set the tone heading into the heavier part of the reporting season next week. Earnings expectations have improved over recent weeks, with S&P 500 companies expected to post 6.3% revenue growth and nearly 8% profit growth in Q3. Across sectors, technology stocks will continue to do the heavy lifting with a 21% profit surge expected, thanks to AI-related demand. Utilities and financials are seen rising 17.5% and 11% respectively, while energy and consumer staples are projected to see 3% declines in profits due to trade tensions and falling energy prices. Let’s see what the companies have to say!

Israel and Hamas agree on first steps in Gaza peace plan

In focus today

Today is generally light on the macro data front; however, in the US, the Fed will host a community banking conference in Washington this afternoon, and Chair Powell is scheduled to give pre-recorded opening remarks.

Economic and market news

What happened overnight

In the Israel-Palestine conflict, Israel and Hamas have agreed on the first steps of a Gaza peace plan, including a hostage-prisoner exchange and the gradual withdrawal of IDF troops from Gaza. According to FT, the first hostages are due to be released on Monday marking a pivotal moment in the ongoing conflict. This development is seen as a huge diplomatic win for Donald Trump. However, significant challenges remain regarding the next phases of the plan, especially those related to Hamas disarmament, further Israeli troops withdrawal and the role of international stability forces in the area. The next few days, and next week, will be critical as we will see whether the two sides comply with the first agreed steps and whether they can agree on the next phases.

Overnight, China introduced extensive new export controls on rare earths and associated technologies, citing "national security". The regulations require foreign companies to obtain Chinese government approval before exporting products containing even small amounts of Chinese rare earths or those manufactured using China's rare-earth technology. Similar to the US foreign direct product rule, these measures aim to prevent the use of rare-earth materials in military and sensitive sectors.

What happened yesterday

In the US, the minutes from FOMC's September meeting, published last night, did not contain any major surprises for markets. The participants were clearly very divided in their perceptions of the inflation outlook. The minutes noted that 'a few participants emphasized that progress of inflation [towards 2%] had stalled, even excluding the effects of tariffs' and that 'few participants could have supported keeping Fed Funds rate unchanged at the September meeting'. On the other hand, 'some participants remarked that they perceived less upside risk to their outlooks for inflation than earlier in the year'. The next key inflation release, the September Consumer Price Index (CPI), is scheduled for next week's Wednesday, but it might get delayed by the ongoing government shutdown.

In Sweden, the flash estimate for September showed headline inflation at 0.9% y/y (prior: 1.1%%), CPIF excluding energy at 2.7% y/y (prior: 2.9%), and CPIF at 3.1% y/y (prior: 3.2%). This was in line with expectations of a y/y decline in inflation following the summer increase. Details will be released on Wednesday next week, with some summer-season-related components likely driving the decline. The Swedish flash print also indicates downside risks for Norwegian inflation, as similar seasonal factors may weigh on Friday's figures.

In Poland, the National Bank of Poland (NBP) cut the Base Rate by 25bp to 4.50%, citing an improved inflation outlook. Future policy decisions will depend on incoming data regarding inflation and economic activity. The zloty weakened slightly on the news, with USD/PLN trading above 3.66. Attention now shifts to NBP Governor Glapiński's press conference, scheduled for today, for further insights.

In France, outgoing caretaker PM Sebastien Lecornu expressed cautious optimism after two days of talks, stating progress had been made on budget discussions. While no deal was reached, Lecornu believes a path exists to avoid snap elections, and President Macron is expected to name a new prime minister within 48 hours. Opposition leaders, however, remain defiant, calling for elections or Macron's resignation.

Equities: Equities bounced back yesterday, fully reversing Tuesday's losses and setting a string of new all-time highs, driven mainly by cyclicals.

Volatility edged slightly lower, and perhaps most interestingly, European banks were among the best performers, while banks ranked as the worst-performing sector in the S&P 500.

One might be tempted to link the European bank strength to optimism around France and Macron's ongoing struggle to form a government, but that's not the case. The rally was led by Southern European banks, reflecting the relatively solid macro backdrop across Southern Europe these days.

In the US yesterday, Dow 0.0%, S&P 500 +0.6%, Nasdaq +1.1% and Russell 2000 +1.0%

Overnight, Asian equities are trading higher, while futures in both Europe and the U.S. are broadly unchanged.

Even news of tentative progress toward a potential peace framework in the Middle East has had virtually no impact on markets. This is consistent with the pattern we've seen throughout this conflict, where geopolitical developments in the region have carried very limited financial-market significance.

FI and FX: Israel and Hamas confirmed the hostage-release deal announced by President Trump last night. So far, market reactions in FX and fixed income have been muted. Possibly, one could tie the USD's overnight weakening to the positive developments in the Middle East rather than the FOMC minutes. The latter revealed a diverse range of views but could be interpreted as slightly hawkish overall. US interest rates showed minimal response to the minutes' release. European focus remains on France, where the outgoing PM Lecornu noted that some progress has been made on the budget discussions. President Macron is to be announcing a new PM soon.

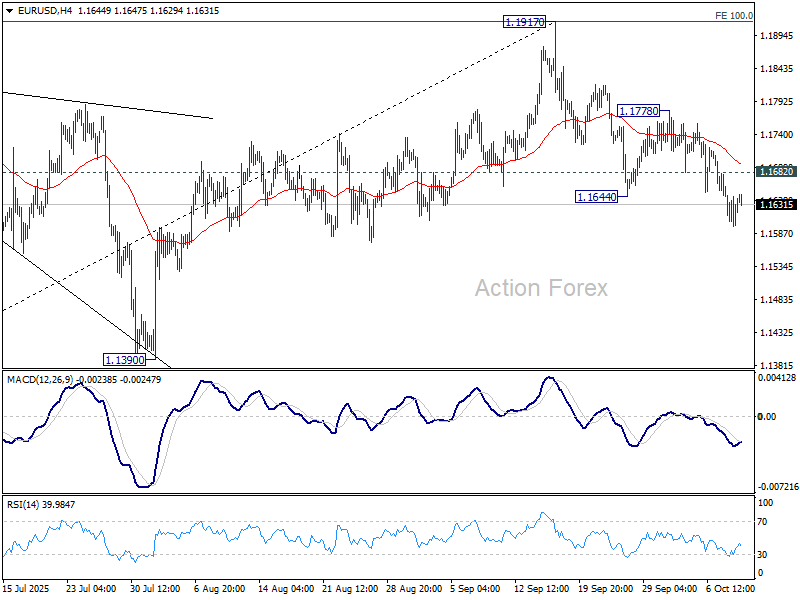

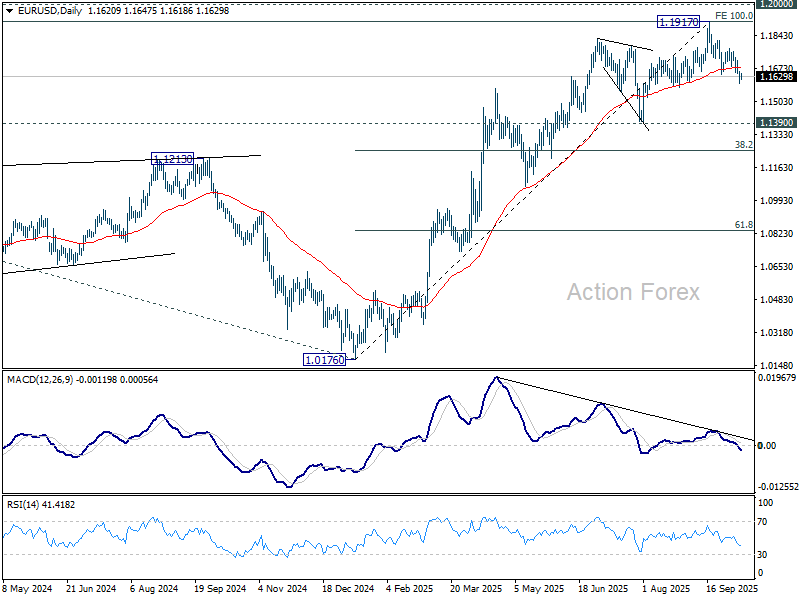

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1598; (P) 1.1631; (R1) 1.1662; More...

EUR/USD's fall from 1.1917 is in progress and intraday bias stays on the downside. Deeper decline should be seen to 1.1390 support, or even further to 38.2% retracement of 1.0176 to 1.1917 at 1.1252. On the upside, above 1.1682 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 1.1778 resistance holds, in case of recovery.

In the bigger picture, rise from 1.0176 (2025 low) is seen as the third leg of the pattern from 0.9534 (2022 low). 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916 was already met. For now, further rally will remain in favor as long as 1.1390 support holds, and firm break of 1.2000 psychological level will carry larger bullish implications. However, firm break of 1.1390 will suggest that rise from 1.0176 has already completed and bring deeper fall to 55 W EMA (now at 1.1265) and below.

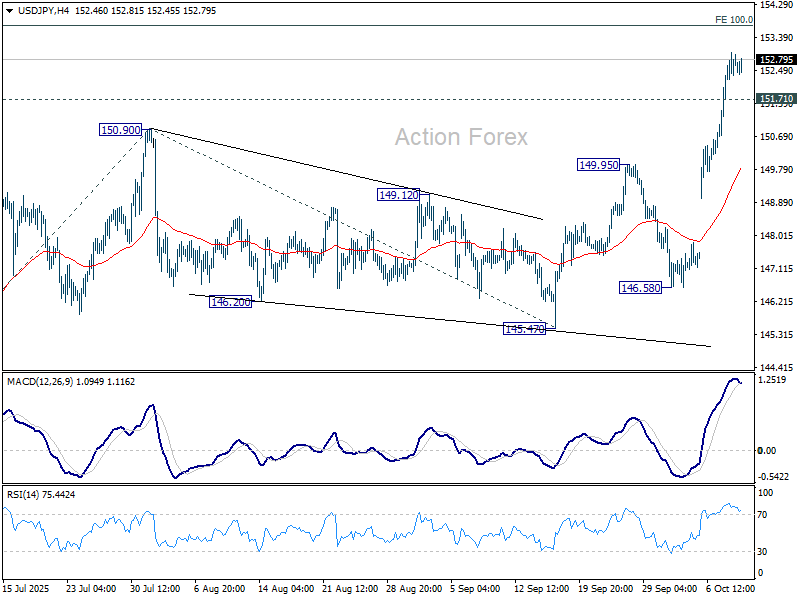

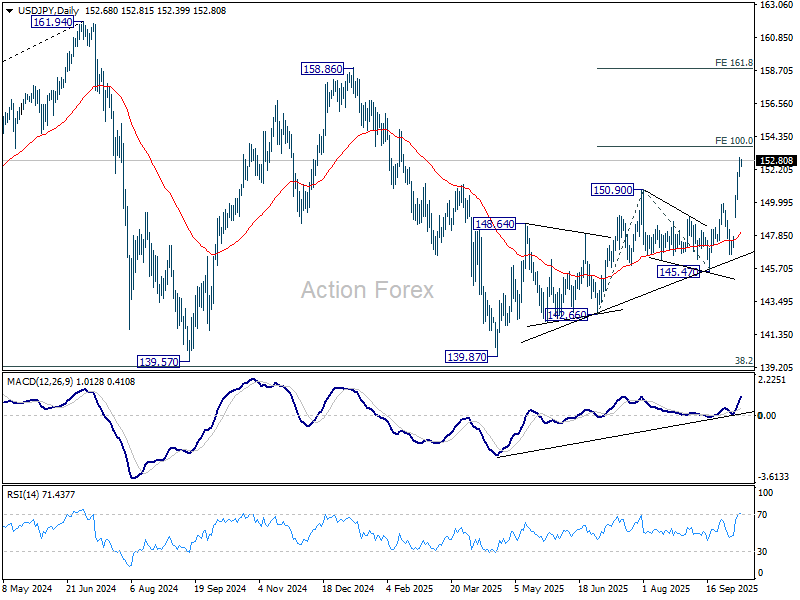

USD/JPY Daily Outlook

Daily Pivots: (S1) 151.96; (P) 152.48; (R1) 153.22; More...

USD/JPY's rally from 145.47 is in progress and intraday bias stays on the upside for 100% projection of 142.66 to 150.90 from 145.47 at 153.71. Firm break there will pave the way to 161.8% projection at 158.80. On the downside, below 151.71 minor support will turn bias neutral and bring consolidations first, before staging another rise.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 145.47 support will dampen this bullish view and extend the corrective pattern with another falling leg.

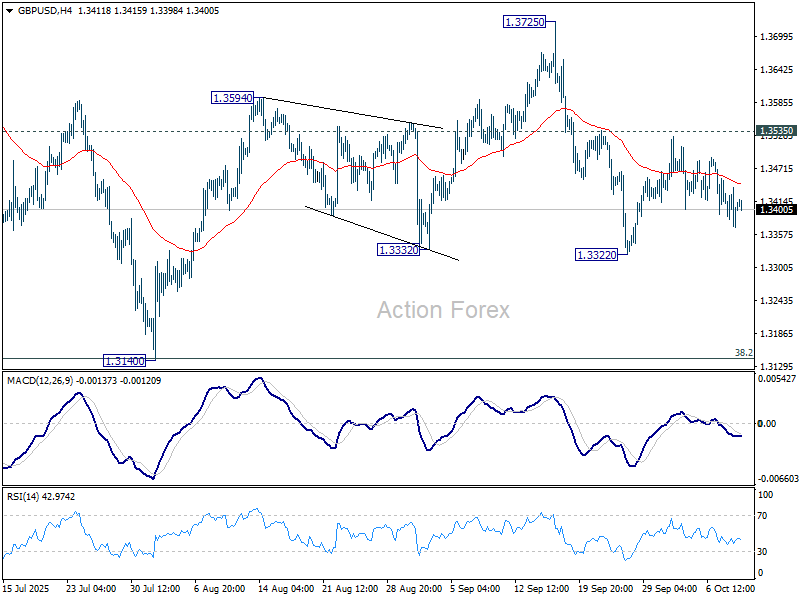

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3369; (P) 1.3407; (R1) 1.3442; More...

Intraday bias in GBP/USD remains neutral as sideway trading continues. With 1.3535 resistance intact, further decline is mildly in favor. On the downside, break of 1.3322 will resume the fall from 1.3725 to 1.3140 support. On the upside, though, firm break of 1.3535 will argue that pullback from 1.3725 has already completed, and bring stronger rise to retest 1.3725/87 key resistance zone.

In the bigger picture, rise from 1.0351 (2022 low) is still seen as a corrective move. Further rally could be seen to 61.8% projection of 1.0351 to 1.3433 (2024 high) from 1.2099 (2025 low) at 1.4004. But strong resistance could be seen from 1.4248 (2021 high) to limit upside. Sustained break of 55 W EMA (now at 1.3176) will argue that a medium term top has already formed and bring deeper fall back to 1.2099.

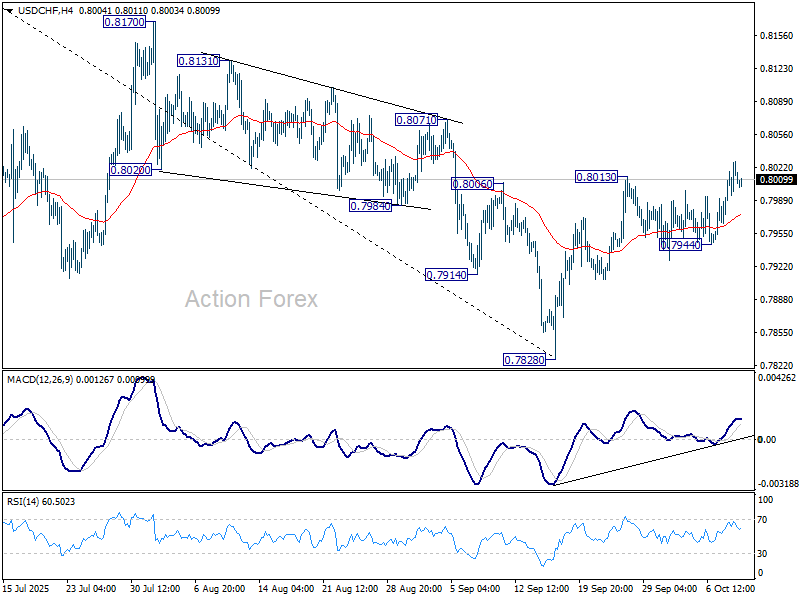

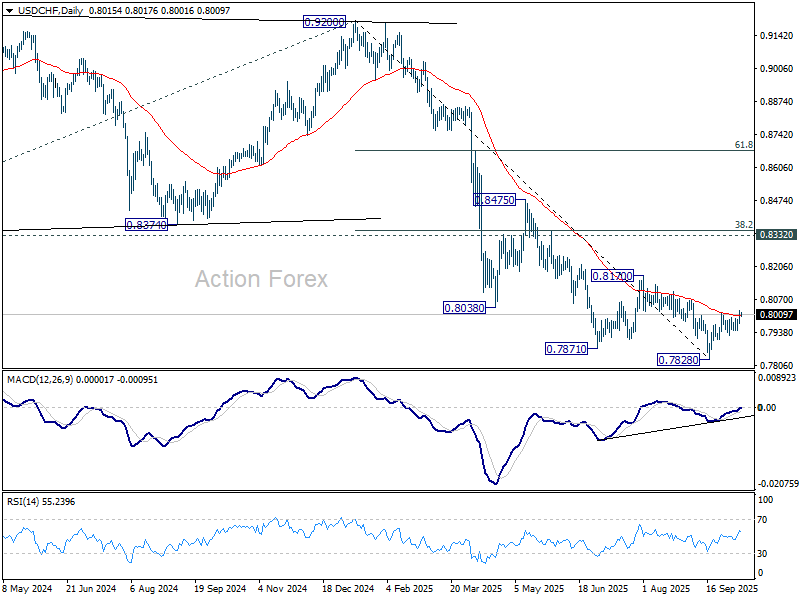

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7988; (P) 0.8008; (R1) 0.8040; More…

Intraday bias in USD/CHF remains on the upside at this point. Sustained trading above 55 D EMA (now at 0.8004) will suggest that rise from 0.7828 is already correcting whole fall from 0.9200. Further rally should the be seen to 0.8170 resistance and possibly above. For now, risk will stay on the upside as long as 0.7944 support holds, in case of retreat.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

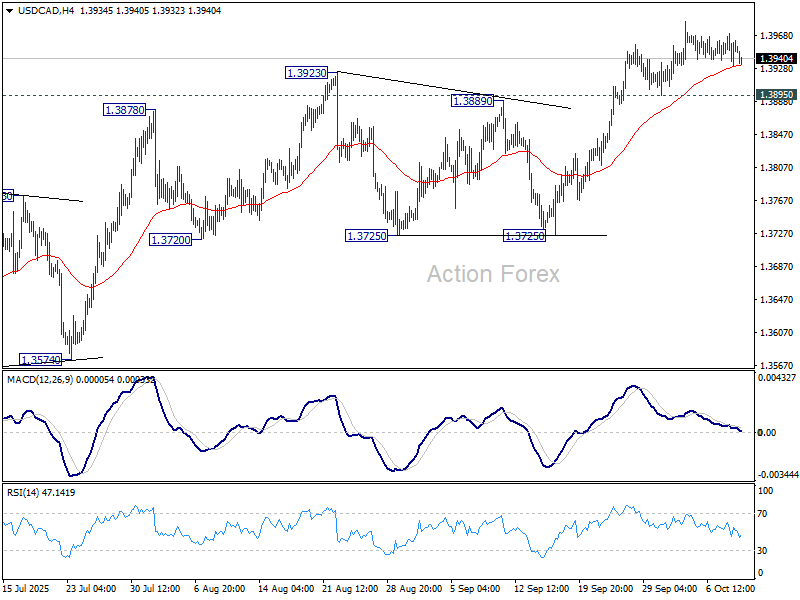

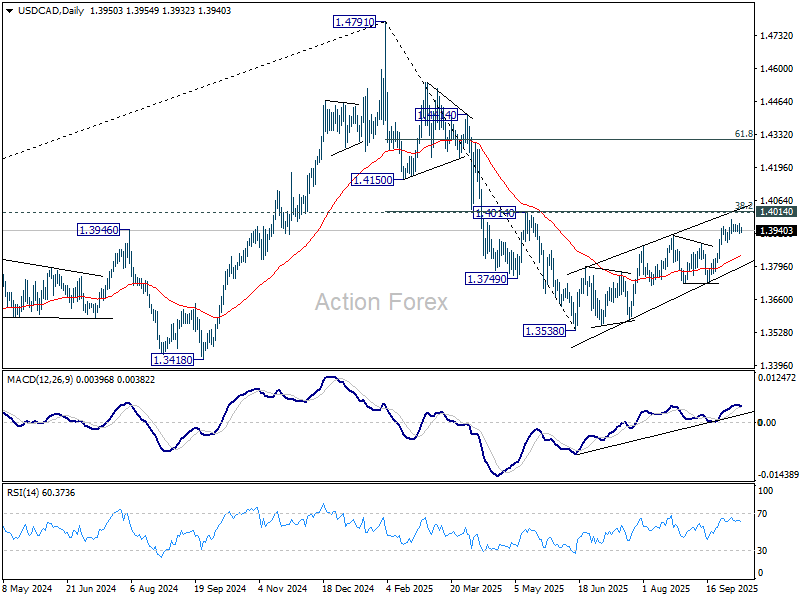

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3933; (P) 1.3952; (R1) 1.3972; More...

USD/CAD's outlook is unchanged and intraday bias stays neutral at this point. While another rise cannot be ruled out, strong resistance is expected from 1.4014/7 cluster to complete the corrective rally from 1.3538. On the downside, below 1.3895 support will turn bias back to the downside for 1.3725. However, sustained break of 1.4014 will carry larger bullish implications.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 cluster resistance (38.2% retracement of 1.4791 to 1.3538 at 1.4017) holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 (2025 high) at 1.3069. However, sustained break of 1.4014 will argue that fall from 1.4791 has completed, and bring stronger rally to 61.8% retracement at 1.4312.

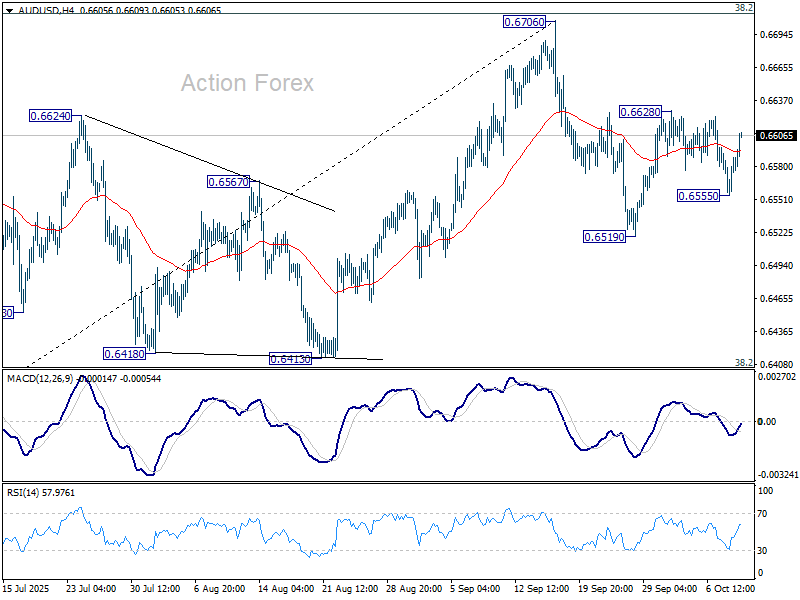

AUD/USD Daily Report

Daily Pivots: (S1) 0.6566; (P) 0.6578; (R1) 0.6598; More...

AUD/USD recovered after dipping to 0.6555 but stays below 0.6628 resistance. Intraday bias stays neutral first. On the upside, break of 0.6628 will resume the rebound from 0.6519 to retest 0.6706 high. However, on the downside, sustained trading below 55 D EMA (0.6558) will confirm rejection by 0.6713 fibonacci resistance, and bring deeper fall to 0.6413 cluster support (38.2% retracement of 0.5913 to 0.6706 at 0.6403).

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. Outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, sustained break of 0.6713 will be a strong sign of bullish trend reversal, and pave the way to 0.6941 structural resistance for confirmation.

Aussie Rises on Regional Tech Rally; Dollar Soft After Cautious Fed Minutes

Australian Dollar advanced in Asian session today, lifted by broad gains across regional equities and improving investor confidence. Japan led the advance, with a technology-driven rally pushing the Nikkei higher. Shares of SoftBank surged over 10% after the company announced plans to acquire the robotics division of Swiss engineering firm ABB, a deal that deepens its ambitions in the AI sector. Founder Masayoshi Son described that as part of the company’s push into “Physical AI.” Son said the deal would merge “Artificial Super Intelligence and robotics” to fuel the next phase of innovation.

Chinese markets also reopened firmly after the holiday break, with AI and gold stocks spearheading gains. The recovery helped offset disappointing consumer data and shifted attention toward the Communist Party’s October 20–23 meeting, where the 15th five-year plan will be unveiled. Investors are watching for signals on technology investment, infrastructure policy, and more importantly, potential stimulus measures to sustain China’s growth narrative into 2026 and beyond.

Meanwhile, Dollar slipped modestly as investors digested the FOMC minutes released overnight. The minutes showed that while policymakers see little scope for rapid easing, they still agree that interest rates are on a downward path, and cuts are in pipeline for the rest of the year. The ongoing government shutdown also weighed on the greenback, with traders hesitant to build new long positions amid fiscal uncertainty and political deadlock.

Among major currencies, Yen remains pinned at the bottom of the performance table, pressured by risk-on flows and expectations that the BoJ will postpone its next rate hike until 2026. Euro is the second weakest, with attention turning to ECB minutes, expected to confirm a continued pause. However, France’s political paralysis continues to overshadow monetary discussions, leaving Euro vulnerable. Swiss Franc also softened as safe-haven demand faded.

On the other side of the ledger,Loonie leads the week, supported by optimism on trade. Prime Minister Mark Carney said bilateral deals with the U.S. were progressing alongside the continental trade framework, noting that discussions with President Donald Trump were “very granular” and showing tangible progress. Aussie ranks second among top performers, just behind the Loonie, while Dollar holds the third place. Kiwi and Sterling are mixed in the middle, with Kiwi staging a mild rebound after its RBNZ-driven selloff.

In Asia, at the time of writing, Nikkei is up 1.53%. Hong Kong HSI is up 0.10%. China Shanghai SSE is up 1.12%. Singapore Strait Times is down -0.17%. Japan 10-year JGB yield is down -0.006 at 1.698. Overnight, DOW closed flat, S&P 500 rose 0.58%. NASDAQ rose 1.12%. 10-year yield rose 0.002 to 4.129.

Fed minutes leans dovish, but no scope for rapid easing

Minutes from the Fed’s September 16–17 meeting, released overnight, show the Committee leaning toward additional rate cuts this year while emphasizing the need for caution in the pace of easing. “Most judged that it likely would be appropriate to ease policy further over the remainder of this year,” the minutes said.

But, officials also acknowledged a “range of views” about how restrictive policy currently is and how fast it should be relaxed. Some members cautioned that “financial conditions suggested monetary policy may not be particularly restrictive,” arguing for patience.

In a key passage, the Committee “stressed the importance of taking a balanced approach” to achieving its dual goals, mindful of “the extent of departures from those goals” and the “different time horizons” for inflation and employment to normalize.

Currently, Core PCE is at 2.9% and unemployment at 4.3%. The Summary of Economic Projections showed inflation to rise to 3.1% by year end, and then only decline gradually to 2.6% in 2026, and 2.1% in 2027. Unemployment is forecast to edge up modestly to 4.5% and then stabilizes.

That combination means the economy is at risk of policy over-restriction: keeping rates too high for too long could cause a sharper, sustained rise in unemployment. But — and this is the key point — the pace of that easing must be gradual as inflation would only slow over the next two years. That means the Fed can’t risk loosening so fast that it reignites price pressures or unanchors expectations.

At the meeting, Fed cut interest rates by 25bps to 4.00-4.25%, with Governor Stephen Miran as the only dissenter voting for a 50bps reduction.

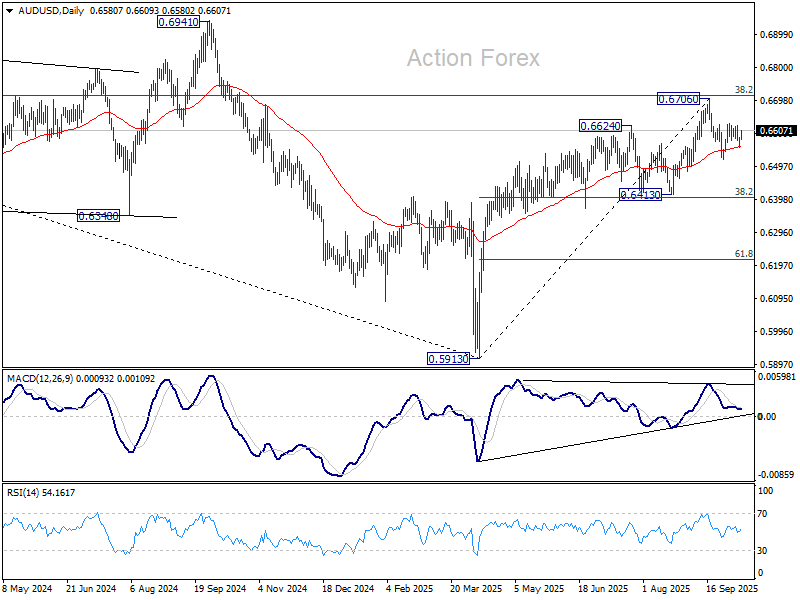

AUD/USD Daily Report

Daily Pivots: (S1) 0.6566; (P) 0.6578; (R1) 0.6598; More...

AUD/USD recovered after dipping to 0.6555 but stays below 0.6628 resistance. Intraday bias stays neutral first. On the upside, break of 0.6628 will resume the rebound from 0.6519 to retest 0.6706 high. However, on the downside, sustained trading below 55 D EMA (0.6558) will confirm rejection by 0.6713 fibonacci resistance, and bring deeper fall to 0.6413 cluster support (38.2% retracement of 0.5913 to 0.6706 at 0.6403).

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. Outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, sustained break of 0.6713 will be a strong sign of bullish trend reversal, and pave the way to 0.6941 structural resistance for confirmation.

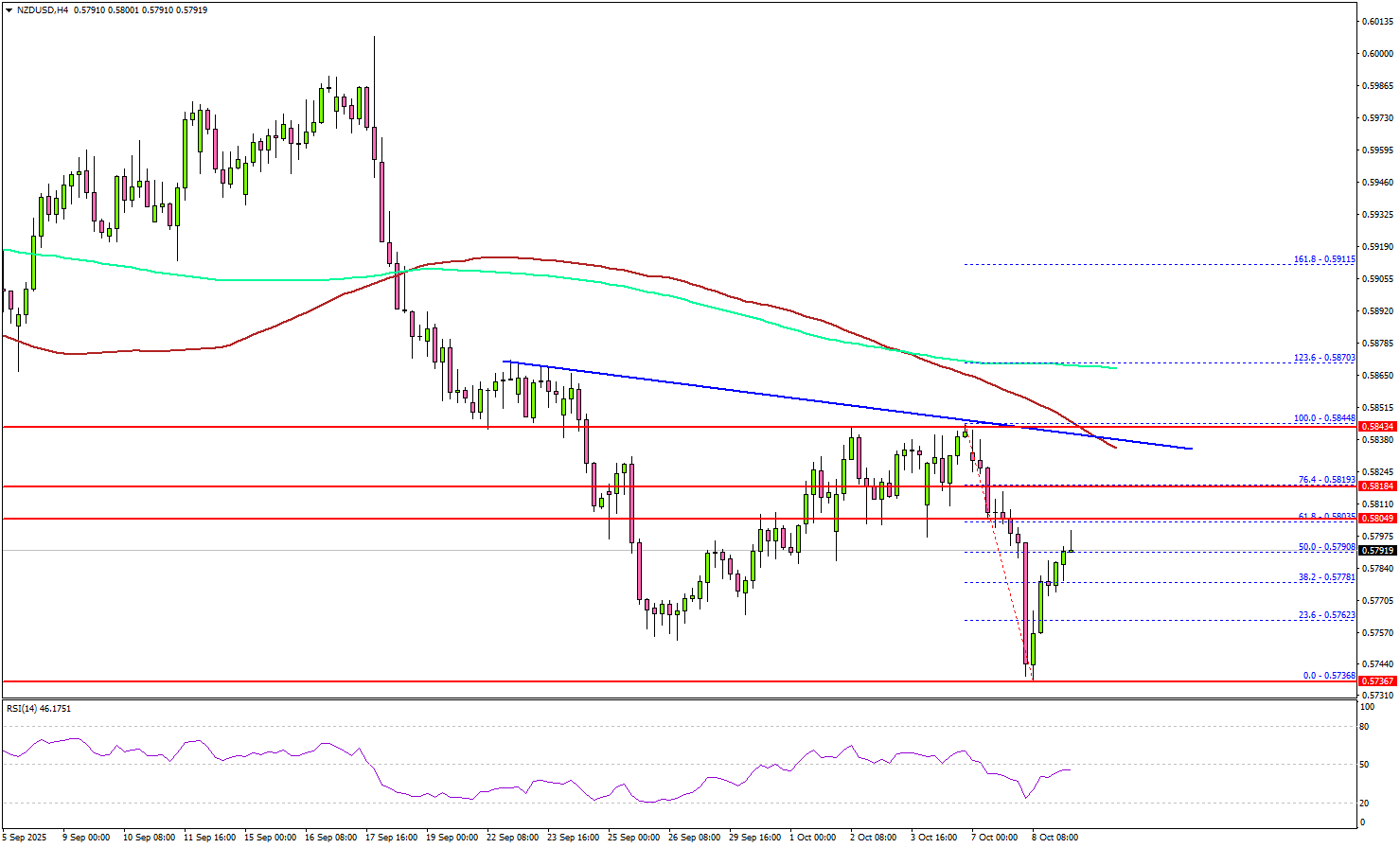

NZD/USD Attempts Recovery – But Bears Lurk Near Resistance Levels

Key Highlights

- NZD/USD is attempting to recover from 0.5735.

- A major bearish trend line is forming with resistance near 0.5830 on the 4-hour chart.

- EUR/USD extended losses below 1.1640 and might test 1.1580.

- Gold extended gains and rallied to a new record high above $4,020.

NZD/USD Technical Analysis

The New Zealand Dollar dived below 0.5850 against the US Dollar before the bulls appeared. NZD/USD tested 0.5735 and recently started a minor recovery.

Looking at the 4-hour chart, the pair recovered above the 23.6% Fib retracement level of the recent decline from the 0.5844 swing high to the 0.5736 low. However, the pair is still well below the 0.5850 pivot level, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour).

Besides, there is a major bearish trend line forming with resistance near 0.5830. To start a decent increase, NZD/USD must settle above the trend line and 0.5850.

The main hurdle could be near 0.5870 and the 200 simple moving average (green, 4-hour). A close above 0.5870 could start a steady increase. If not, the pair could decline again.

On the downside, there is key support at 0.5750. The next area of interest might be 0.5730. The main support could be 0.5680. Any more losses might increase selling pressure and send the pair toward 0.5620.

Looking at Gold, the bulls remained in full control as they were able to pump the price to new highs above $4,000 and $4,020.

Upcoming Key Economic Events:

- US Initial Jobless Claims - Forecast 227K, versus 218K previous.

- Fed's Chair Powell speech.