Sample Category Title

BoE’s Mann: Inflation scarring still weighing on consumption, justifies policy restraint for longer

BoE policymaker Catherine Mann cautioned in a speech today that monetary policy must remain restrictive despite signs of weak consumption, arguing that high inflation has scarred UK consumers and continues to suppress spending.

“If the consumption gap was my only concern, reducing the restrictiveness of monetary policy would be appropriate,” she said. “However, in light of elevated inflation and expectations, maintaining restrictiveness for longer would be appropriate.”

Mann said the Bank’s analysis points to two drivers of the consumption gap: first, inflation and consumer scarring, and second, the channels through which monetary policy affects consumption.

The former, she explained, is a legacy of the rapid price surge that eroded purchasing power and altered household behavior. “High inflation itself is behind income uncertainty and weak consumption growth,” she said. “Monetary policy needs to continue to focus on reducing inflation” so households can return to a sustainable spending pattern.

For the second, she emphasized that higher rates have already exerted a material drag on demand, and the tightening effect is already waning. “Monetary policy has indeed loosened,” Mann said, adding that its impact on consumption has peaked.

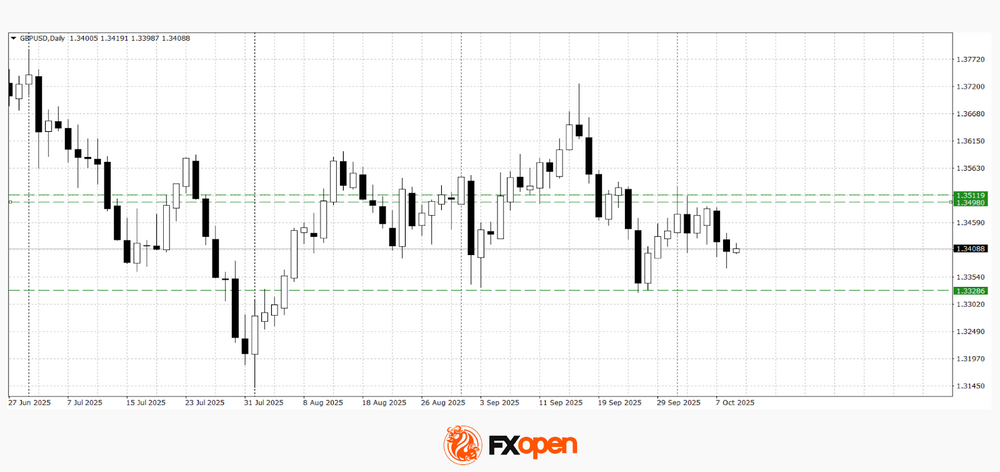

GBP/USD Halts Decline but Inflation Risks Linger

The GBP/USD pair attempted to stabilise on Thursday, trading around 1.3413 USD. However, investor sentiment remains cautious amid a weak outlook for the UK economy and uncertainty surrounding the government's November budget.

UK GDP growth is projected to remain moderate through year-end, while inflation is forecast to rise to 4% – double the Bank of England's target. Recent data confirm the economy is losing momentum after a strong start to 2025.

The pound showed a muted reaction to this data. Nonetheless, markets are concerned that potential tax increases in the upcoming budget – aimed at ensuring compliance with fiscal rules – could exert further pressure on the currency.

This week, speeches from Bank of England officials Huw Pill and Catherine Mann are in focus. Both previously supported holding rates steady in September. Monetary policymakers have previously warned that global markets could face a shock if investors begin to doubt the prospects for the artificial intelligence sector or the independence of the US Federal Reserve.

Technical Analysis: GBP/USD

H4 Chart:

A narrow consolidation range has formed around 1.3420. Following a downward breakout, the pair is developing a decline towards 1.3300. This move represents only the first half of the third declining wave within the broader downtrend, with the primary target seen at 1.3130. This scenario is technically confirmed by the MACD indicator, whose signal line lies below zero and is pointing firmly downward.

H1 Chart:

The pair has formed a consolidation range around 1.3415. The subsequent downward movement continues the bearish wave towards a local target of 1.3337. Upon reaching this level, a corrective pullback towards 1.3415 is anticipated. Following this, another decline towards at least 1.3300 is expected, with an extension of the downward structure to 1.3200 also possible. Technically, this outlook is supported by the Stochastic oscillator, whose signal line is below 80 and is turning sharply downward towards 20.

Conclusion

While the GBP/USD has paused its descent, significant downside risks remain due to domestic economic concerns and looming fiscal policy decisions. The technical structure continues to point to further declines, with key support levels at 1.3337 and 1.3300 in focus.

Euro and Pound Under Pressure as Markets Focus on Upcoming Data

The euro has resumed its decline amid political uncertainty in France, while the pound remains under pressure, following the broader weakness in European currencies. On Monday, the euro fell to its lowest level in more than a week after the surprise resignation of French Prime Minister Sébastien Lecornu, which deepened the country’s political crisis and fuelled bearish sentiment in the options market. The risk reversal indicator — a closely watched gauge of market sentiment — has turned negative, suggesting traders are bracing for further losses. With US trading subdued by the ongoing government shutdown, investor focus has shifted to European developments. In the coming sessions, attention will centre on macroeconomic releases from the eurozone and the United Kingdom, which could set the short-term direction for EUR/USD and GBP/USD.

EUR/USD

After testing and sharply rebounding from 1.1780, EUR/USD buyers lost upward momentum, allowing the price to settle below 1.1700. Yesterday, the pair hit a new September low at 1.1600 but recovered above that level following the release of the FOMC minutes. A firm move below yesterday’s low could pave the way for further declines towards 1.1530–1.1570, while a sustained rise above 1.1700 may revive bullish momentum and lead to a retest of recent highs near 1.1760–1.1780.

Key events that could influence EUR/USD pricing in the coming sessions:

- → 10:00 (GMT+3): Speech by Bundesbank’s Burkhard Balz

- → 13:00 (GMT+3): Eurogroup meeting

- → 14:30 (GMT+3): Publication of the ECB monetary policy meeting account

GBP/USD

Pound buyers failed to hold above 1.3500, prompting a renewed decline in GBP/USD and a test of key support in the 1.3370–1.3400 range. Technical analysis points to potential downside towards 1.3330. The bearish scenario would be invalidated by a confident move above 1.3500.

Key events that could affect GBP/USD in the near term:

- → 11:30 (GMT+3): Speech by Bank of England Monetary Policy Committee member Catherine Mann

- → 15:30 (GMT+3): Speech by US Federal Reserve Chair Jerome Powell

- → 15:30 (GMT+3): US initial jobless claims data

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

USD/JPY: Current JPY Weakness Driven by Short-Term Sentiment as Disconnects from US-Japan Yields

Key takeaways

- The Japanese yen has weakened sharply, losing 3.7% against the USD as markets priced in pro-stimulus expectations from new LDP leader Sanae Takaichi, fuelling the “Takaichi Trade.”

- Despite short-term JPY weakness, Japan’s consumer confidence continues to improve, supporting the Bank of Japan’s (BoJ) gradual rate hike stance.

- The BoJ’s policy rate curve remains upward trending, signalling gradual monetary tightening into 2026.

- The US–Japan 10-year yield spread has broken (intraday) below key support at 2.47%, a potential signal for medium-term USD/JPY weakness ahead.

In the past three sessions since Monday, 6 October 2025, the Japanese yen has weakened significantly as it shed -3.7% against the US dollar at the time of writing to print an intraday high of 153.00 on Wednesday, 8 October 2025 after the weekend election of fiscal and monetary dove Sanae Takaichi as the leader of the LDP ruling party in Japan and is likely to become Japan's new prime minister.

The USD/JPY shot past the 150.00 psychological level and printed a current intraday level of 152.94 as the prospects of a 25 basis points interest rate hike by the Bank of Japan (BoJ) in Q4 2025 have dampened, triggered by the “Takaichi Trade”.

Given that Takaichi is a protégée of the late former Prime Minister Shinzo Abe, the market chatter of “Abenomics 2.0” has gained traction, where the new Japanese PM may “push” the Bank of Japan (BoJ) to revert to monetary policy easing and put a pause to its current monetary policy normalisation stance of gradually increasing interest rates in Japan.

In this article, we will highlight three fundamental macro factors that suggest the current JPY weakness is likely not sustainable in the medium term and provide a short-term (1 to 3 days) outlook on the USD/JPY from a technical analysis perspective.

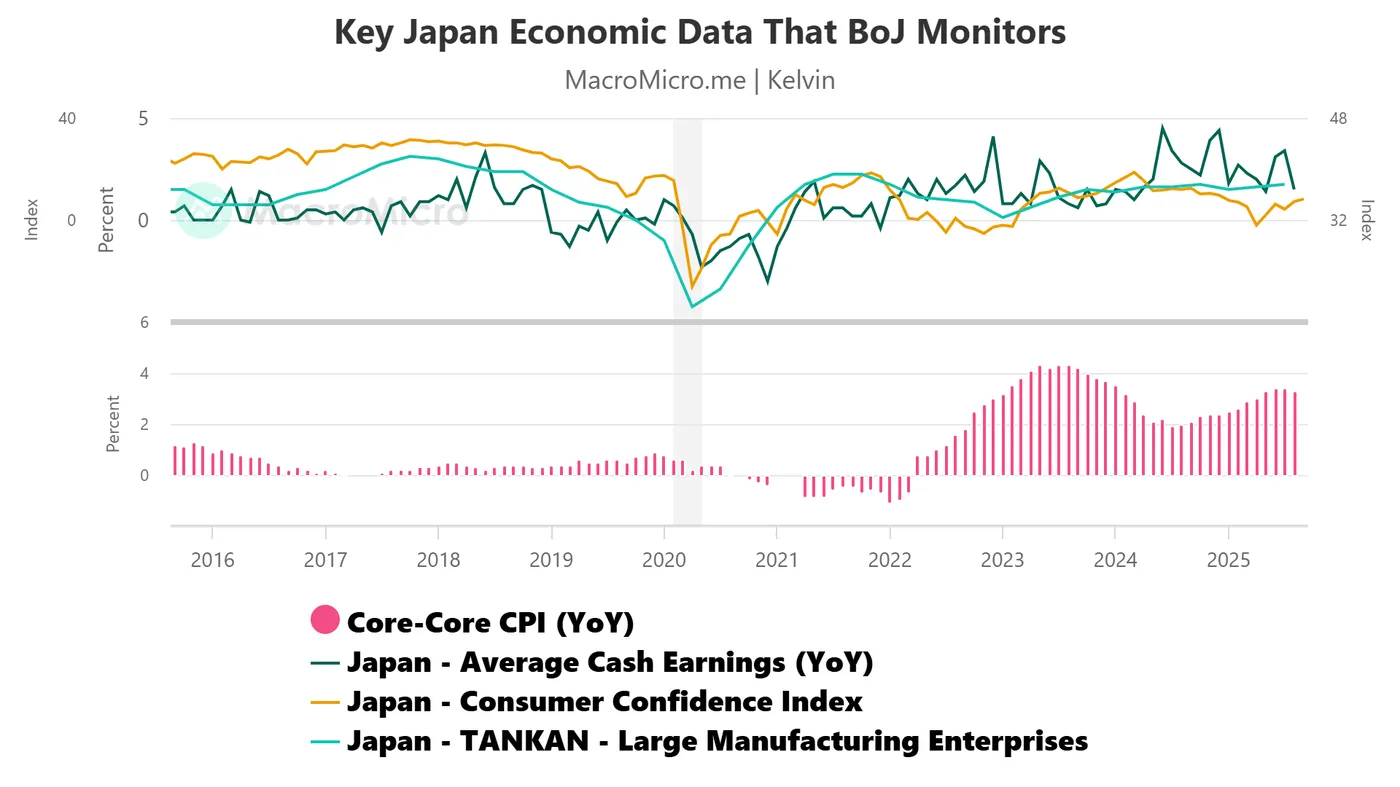

Japan’s consumer confidence continues to improve

Fig. 1: Japan core-core CPI, Average Cash Earnings, Tankan Survey, Consumer Confidence as of Sep 2025 (Source: MacroMicro)

One of the key economic data points, other than the inflation trend, that the BoJ monitors to determine and set the path of monetary policy in Japan, is consumer sentiment.

The latest Japanese consumer confidence index, released last week, rose to 35.3 in September 2025 from 34.9 in August, hitting its highest level since December 2024 (see Fig. 1).

A further improvement in consumer sentiment is likely to boost domestic demand in Japan, in turn, supporting the BoJ’s current monetary policy stance of a gradual rise in interest rates from the current level of 0.5%.

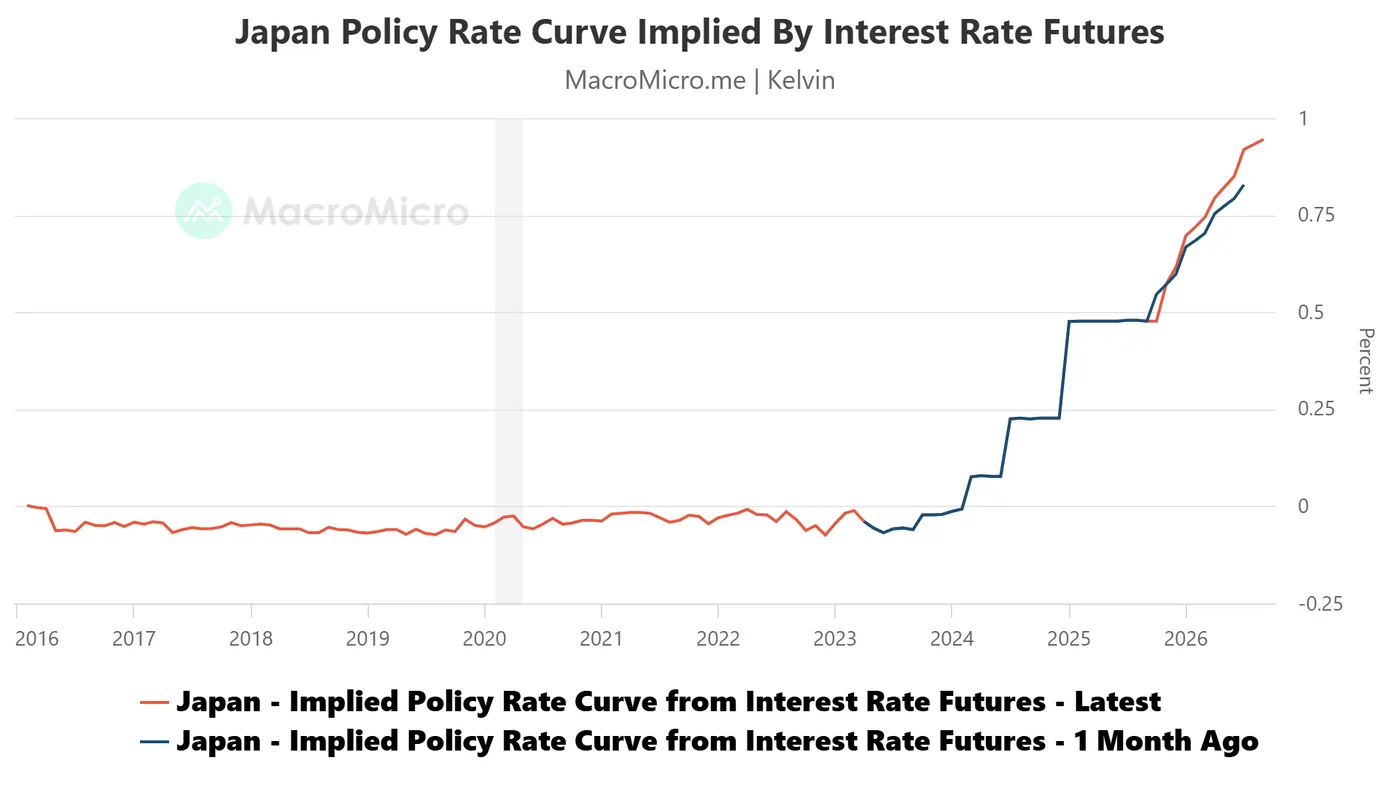

BoJ remains on its path of interest rate hikes

Fig. 2: Japan's implied policy rate curves as of 8 October 2025 (Source: MacroMicro)

Based on the latest data from the short-term interest rate futures market, the current policy rate curve has continued to trend upwards heading into next year (0.62% in December 2025 to 0.95% in September 2025) (see Fig. 2).

Also, the current policy rate curve has shifted upwards from a month ago.

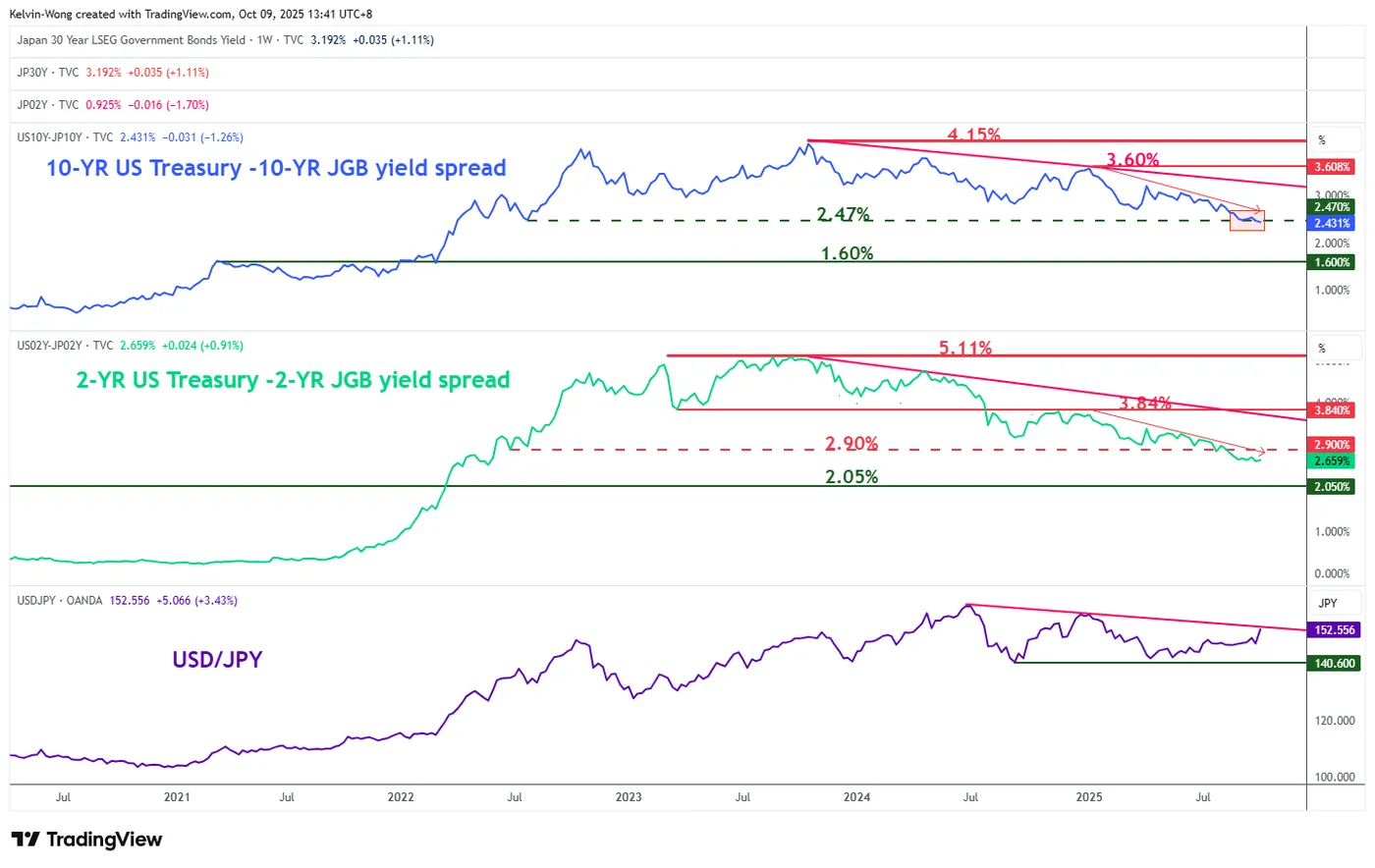

The 10-year US Treasury/JGB yield spread has broken below a major support level on an intraday basis

Fig. 3: Yield spreads of US Treasury/JGB with major trend of USD/JPY as of 9 Oct 2025 (Source: TradingView)

The 10-year yield spread between the US Treasury note and JGB has broken below the 2.47% major support after it managed to trade above it for the entire month of September 2025. Right now, it is still trading at an intraday level of 2.43% at the time of writing (see Fig. 3).

A weekly close below 2.47% is likely to cement a further narrowing of the 10-year US-Japan yield differential, and such a dynamic managed to trigger a medium-term decline in the USD/JPY from late December 2024 to mid-April 2025.

Let’s now focus on the latest short-term trajectory (1 to 3 days), relevant key elements, and key levels to watch on the USD/JPY.

Fig. 4: USD/JPY minor trend as of 9 October 2025 (Source: TradingView)

Fig. 5: USD/JPY medium-term trend as of 9 October 2025 (Source: TradingView)

Preferred trend bias (1-3 days)

Potential squeezed up for USD/JPY towards a major resistance. Bullish bias in any minor setbacks above 151.15 key short-term pivotal support for the next intermediate resistance to come in at 153.65/153.90 before the major resistance of 154.50 (also a Fibonacci extension) (see Fig. 4).

Key elements

- The USD/JPY has broken above the “Ascending Wedge” range resistance on Monday, 6 October 2025 now turns into a pull-back support at 150.50 (see Fig. 5).

- The major descending trendline of the USD/JPY in place since the 3 July 2024 swing high is now acting as a major resistance at 154.50 (see Fig. 5).

- The hourly RSI momentum indicator of the USD/JPY has exited from its overbought level and has not reached its oversold zone (below 30). These observations suggest a potential minor pull-back for the USD/JPY before a bullish move materializes (see Fig. 4).

Alternative trend bias (1 to 3 days)

A break below 151.15 key short-term support negates the bullish tone for a slide towards the next intermediate supports at 150.50 and 149.80.

ECB Minutes an Avalanche of Fed Speakers

Markets

Caretaking French PM Lecornu reported back to president Macron that there are still possibilities for a compromise in parliament. He warned though that it would still be a difficult path ahead and immediately added some conditions. The next PM can’t have any presidential ambitions in 2027 elections and a suspension of Macron’s signature pension reform from 2023 (raising minimum retirement age to 64 from 62) must at least be worth reconsidering. Lecornu suggested that 210 or more lawmakers want a “platform of stability” to guide next year’s budget through 577-seat parliament. These numbers are MP’s of the ruling minority government, implying that they still need to lure in opposition lawmakers. The largest opposition blocks, the extreme-right (RN) and extreme-left (LFI), stand with their preference to push for new legislative elections, hoping to build on current polling momentum. Together, they account for 198 MP’s. Mutual distrust between socialists and republicans for the moment rules out any centrist (majority) formations. President Macron will on Friday in a final attempt likely announce a technocrat PM whose only task is to try pass a budget by year-end with a technocrat government to avoid snap elections. Chances that any government will rapidly face no confidence motions and eventually derail remain high. The extremely narrow path ahead helps explain the euro’s lackluster reaction to “positive” news that there’s still a chance. EUR/USD closed at 1.1628 from a start at 1.1657. The French CAC 40 equity index (+1%) slightly outperformed other European indices (0.6%-1%). The 10-yr OAT/swap spread narrowed by 2 bps.

During US dealings, the US Treasury sold $39bn of 10-yr Notes as part of its mid-month refinancing operation. The auction stopped above the pre-sale WI yield with the bid cover also down from the previous auction (2.48 from 2.65). It sets the stage for a difficult $22bn 30-yr bond sale tonight as well. Minutes of the September FOMC meeting confirmed division between Fed members. A few would have supported an unchanged decision before eventually backing the consensus 25 bps rate cut. A majority also emphasized upside risks to the inflation outlook but the overall view was that it most likely appropriate to ease policy more this year. Money markets almost completely discount back-to-back 25 bps rate cuts in October (95%) and December (80%). The auction caused slight intraday underperformance at the long end of the US yield curve while FOMC minutes were rapidly classified. Today’s eco calendar contains ECB Minutes an avalanche of Fed speakers. They (including Fed chair Powell) feature at the Fed’s community bank conference and are unlikely to touch on monetary policy. Israel and Hamas agreeing to the first phase of the US peace plan gets a lot of media coverage and helps supporting risk sentiment this morning.

News & Views

The National Bank of Poland (NBP) yesterday unexpectedly reduced its policy rate by 25 bps to 4.50%. The NBP statement was not that much different from the previous meeting, but the central bank took notice that annual CPI inflation remained unchanged at 2.9% Y/Y in September. It expects that core inflation net of food and energy prices (reported at 0.2% M/M and 3.2% Y/Y for August) remained close to the level of August, amidst still elevated services price growth. The communiqué also assesses that, despite a slight decline, annual wage growth in Q2 2025 remained elevated, but that data from the enterprise sector indicate a gradual slowdown. The central bank concluded that an improved inflation outlook for the coming period justified adjusting the level of the NBP interest rates. It wasn’t explicitly mentioned in the statement, but the improvement in the short-term inflation outlook might be related to the government prolonging the energy price caps during Q4. The market reaction was muted. The Polish 2-y swap yield eased 4 bps. The zloty hardly reacted (EUR/PLN 4.25) suggesting that markets mainly see the rate cut as a timing issue rather than profoundly changing expectations on the NBP rate expected rate path.

China announced measures to have tighter control on the exports of rare earth and on related technologies. With the measures they want to keep control on products and technologies that have already left the country. In this respect, foreign companies will need the approval from the Chinese Ministry of Commerce to export products that even contain small fractions of the minerals. Chinese authorities also want to ban technologies that are related to extraction and recycling of rare earths unless permitted by the ministry. Some rare earth items that will be used in developing Chips will be revied on a case-by-case basis. The action is said to have the intention to protect national security and also is said to target the misuse of rare earth materials in military and other sensitive sectors.

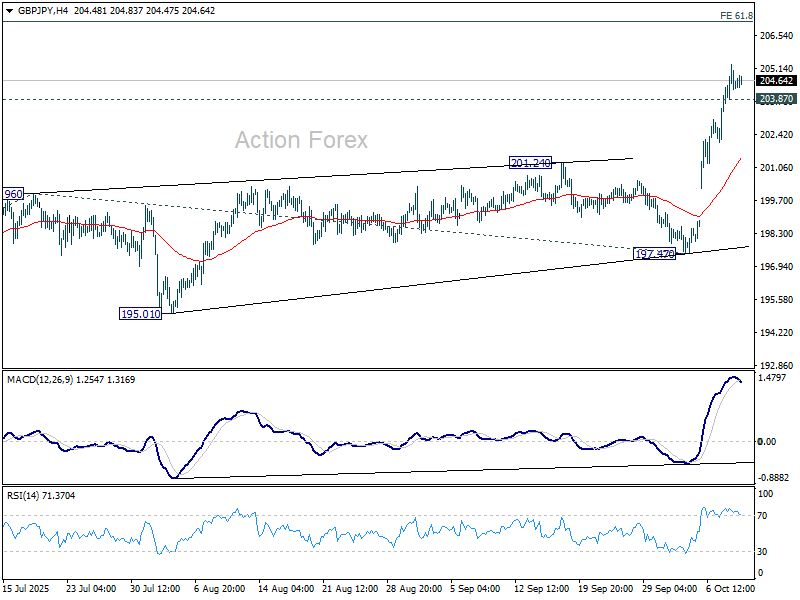

GBP/JPY Daily Outlook

Daily Pivots: (S1) 203.84; (P) 204.58; (R1) 205.42; More...

GBP/JPY's rally from 197.47 is in progress and intraday bias stays on the upside for 61.8% projection of 184.35 to 199.96 from 197.47 at 207.11. On the downside, below 203.870minor support will turn intraday bias neutral and bring consolidations first. But outlook will remain bullish as long as 201.24 resistance turned support holds, in case of retreat.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a corrective pattern which might have completed at 184.35. Firm break of 208.09 high will resume the up trend from 123.94 (2020 low). Next target is 61.8% projection of 148.93 to 208.09 from 184.35 at 220.90. This will now remain the favored case long as 197.47 support holds.

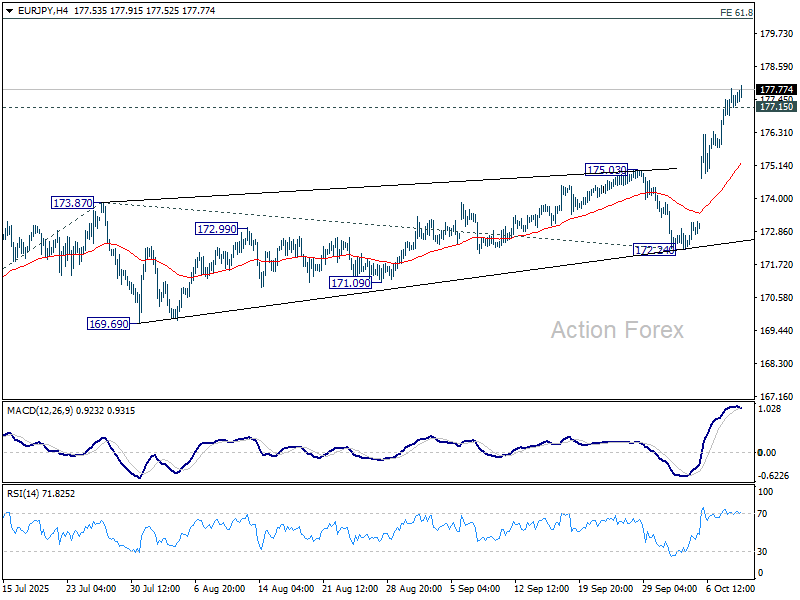

EUR/JPY Daily Outlook

Daily Pivots: (S1) 177.03; (P) 177.44; (R1) 177.99; More...

EUR/JPY's up trend is in progress and intraday bias stays on the upside. Further rise should be seen to 61.8% projection of 161.06 to 173.87 from 172.24 at 180.15 next. On the downside, below 177.15 minor support will turn intraday bias neutral and bring consolidations. But retreat should be contained above 175.03 resistance turned support to bring another rally.

In the bigger picture, up trend from 114.42 (2020 low) is resuming with break of 175.41 (2024 high). Next target is 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. Outlook will continue to stay bullish as long as 55 W EMA (now at 166.82) holds, even in case of deep pullback.

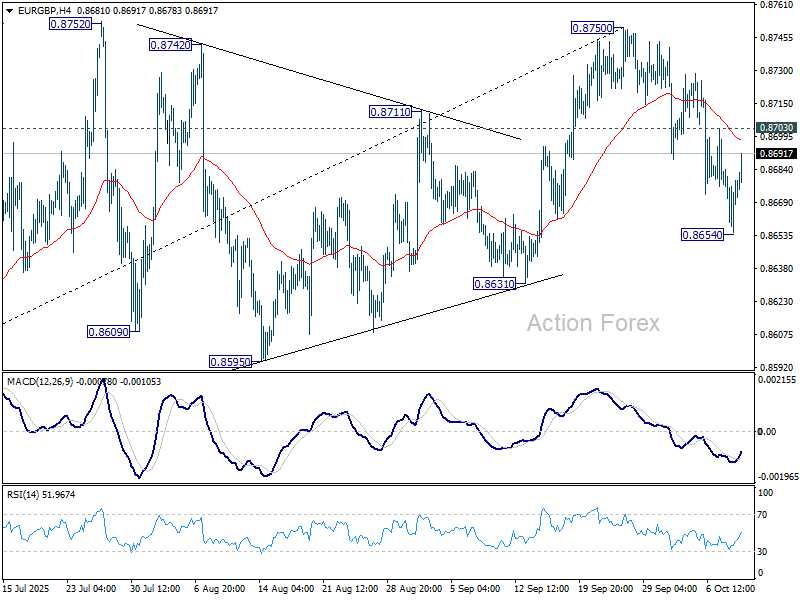

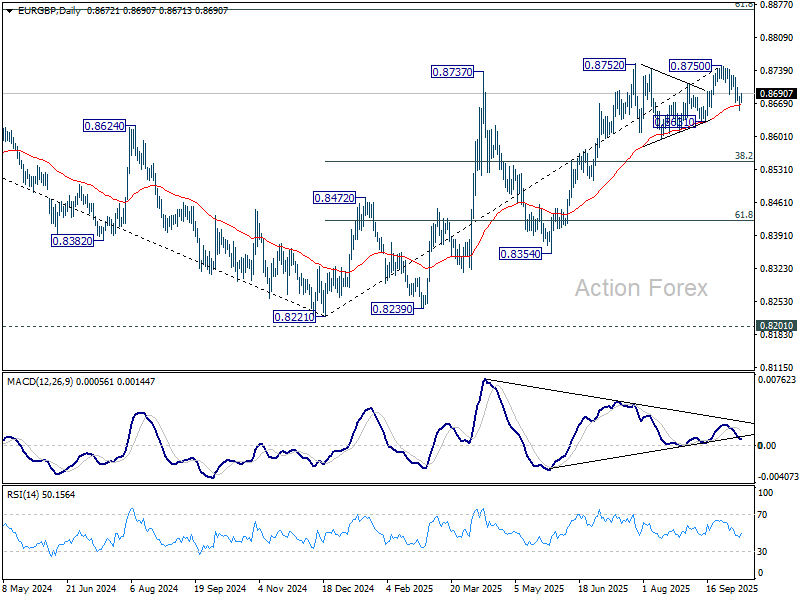

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8660; (P) 0.8672; (R1) 0.8689; More…

Intraday bias in EUR/GBP is turned neutral with current recovery. On the downside, below 0.8654 will resume the fall from 0.8750 to 0.8631 support. Decisive break there will indicate near term reversal and turn outlook bearish for 38.2% retracement of 0.8221 to 0.8750 at 0.8548. However, break of 0.8703 will suggest that pull back from 0.8750 has completed and bring retest of this resistance instead.

In the bigger picture, rise from 0.8221 medium term bottom is seen as a corrective move. While further rally cannot be ruled out, upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Considering bearish divergence condition in D MACD, firm break of 0.8631 support will be the first sign that this corrective bounce has completed. Sustained trading below 55 W EMA (now at 0.8539) will confirm, and bring retest of 0.8221 low.

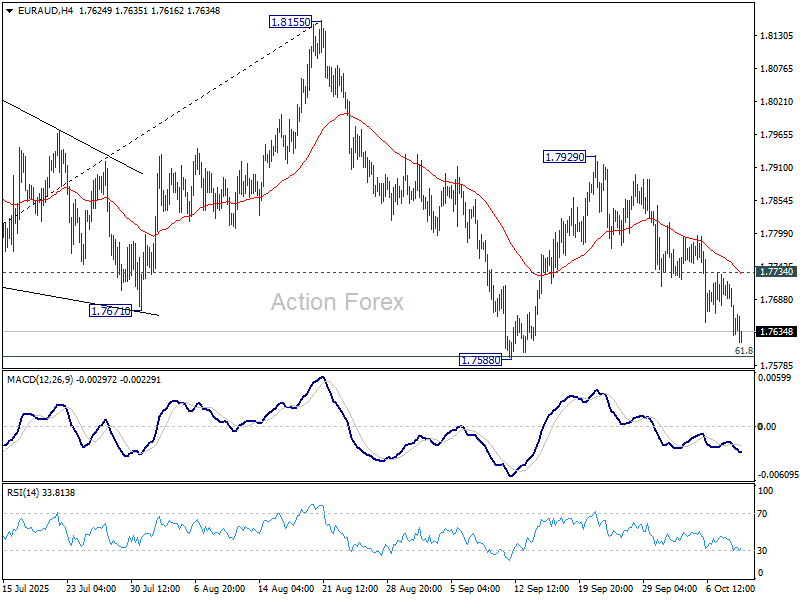

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7612; (P) 1.7667; (R1) 1.7703; More...

Intraday bias in EUR/AUD remains neutral at this point. On the downside, sustained break of 61.8% retracement of 1.7245 to 1.8155 at 1.7593 will bring deeper fall to 1.7245 resistance, as part of the corrective pattern from 1.8554 high. On the upside, above 1.7734 will bring stronger rebound back to 1.7929 resistance.

In the bigger picture, price actions from 1.8554 medium term top are seen as a corrective pattern. Deeper fall could be seen as the pattern extends, but downside should be contained by 38.2% retracement of 1.4281 (2022 low) to 1.8554 at 1.6922 to bring rebound. Uptrend from 1.4281 is expected to resume at a later stage.

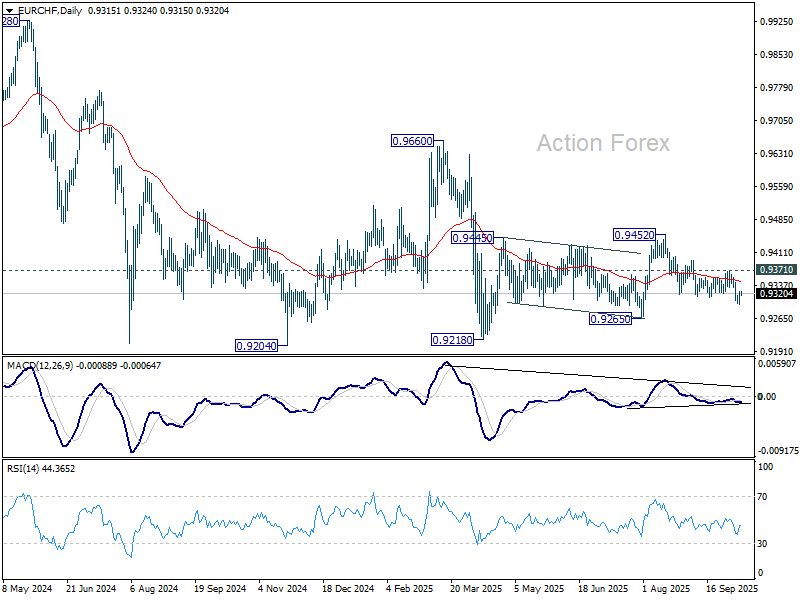

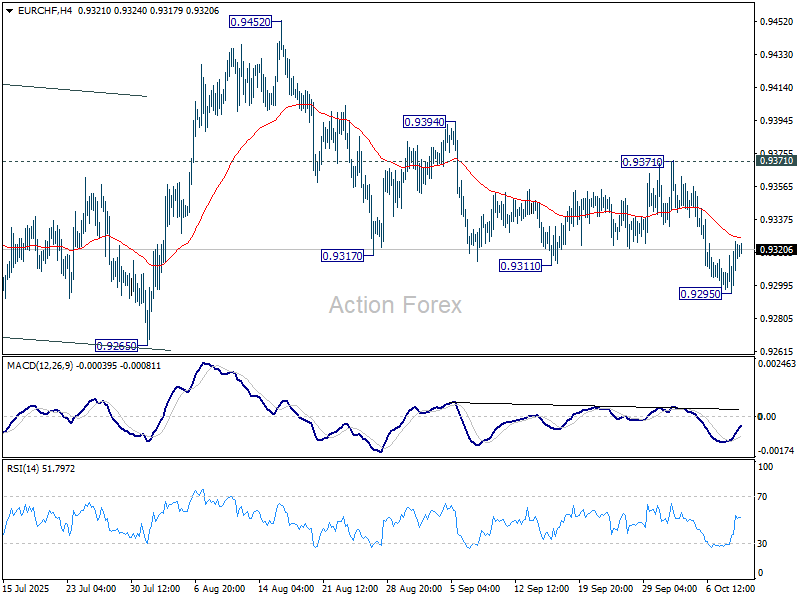

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9306; (P) 0.9317; (R1) 0.9337; More...

Intraday bias in EUR/CHF is turned neutral with current recovery and some consolidations could be see. Risk will stay on the downside as long as 0.9371 resistance holds, in case of recovery. Below 0.9295 will resume the fall from 0.9425 to 0.9265 support. Firm break there will bring deeper decline to 0.9218 low.

In the bigger picture, the down trend from 0.9204 (2018 high) might still be in progress considering that EUR/CHF is staying well inside the long term falling channel. However, with bullish convergence condition in W MACD, downside potential should be limited in case of another fall. Instead, firm break of 0.9660 resistance will be an important sign of medium term bullish trend reversal.