Sample Category Title

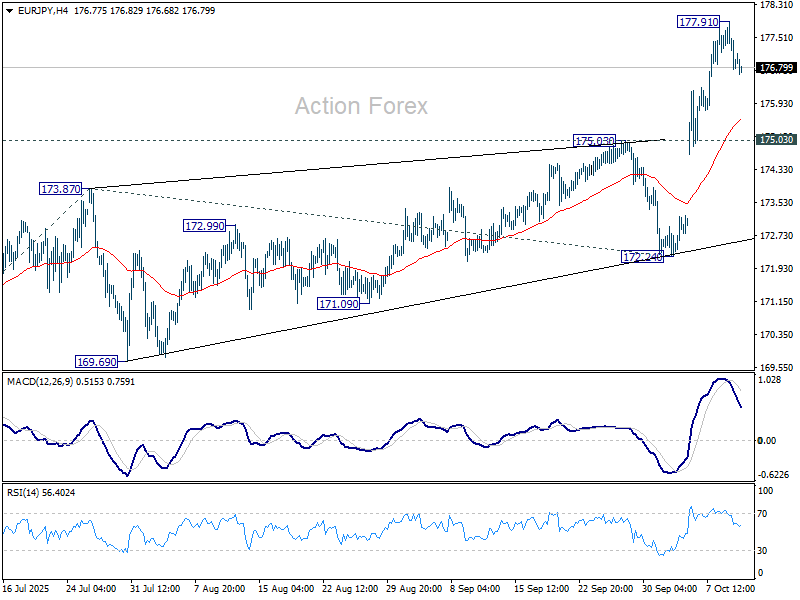

EUR/JPY Daily Outlook

Daily Pivots: (S1) 176.56; (P) 177.25; (R1) 177.74; More...

Intraday bias in EUR/JPY remains neutral and some more consolidations could be seen below 177.91 temporary top. Downside should be contained above 175.03 resistance turned support to bring another rally. On the upside, above 177.91 will resume larger up trend to 61.8% projection of 161.06 to 173.87 from 172.24 at 180.15 next.

In the bigger picture, up trend from 114.42 (2020 low) is resuming with break of 175.41 (2024 high). Next target is 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. Outlook will continue to stay bullish as long as 55 W EMA (now at 166.82) holds, even in case of deep pullback.

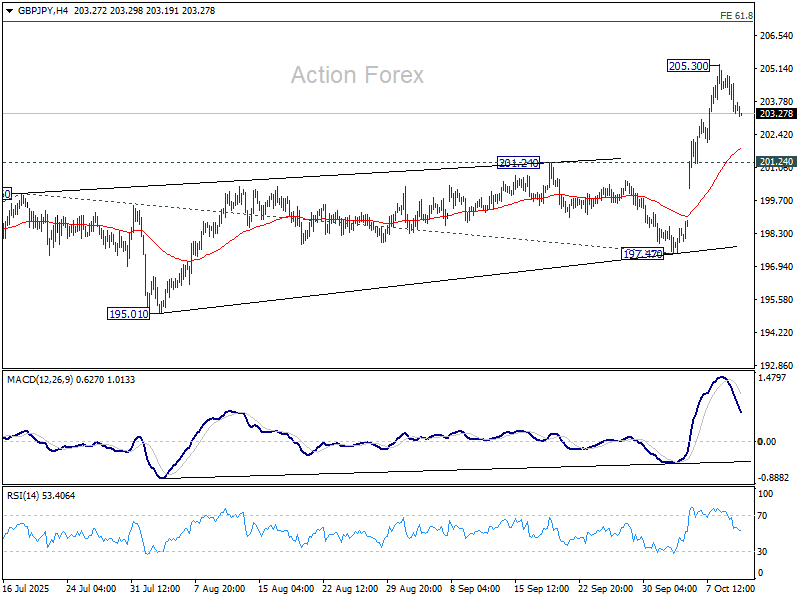

GBP/JPY Daily Outlook

Daily Pivots: (S1) 203.03; (P) 203.96; (R1) 204.61; More...

A temporary top was formed at 205.30 with current retreat, and intraday bias in GBP/JPY is turned neutral for consolidations. Downside should b contained above 201.24 resistance turned support to bring another rally. On the upside, break of 205.30 will resume the rise from 197.47 to 61.8% projection of 184.35 to 199.96 from 197.47 at 207.11.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a corrective pattern which might have completed at 184.35. Firm break of 208.09 high will resume the up trend from 123.94 (2020 low). Next target is 61.8% projection of 148.93 to 208.09 from 184.35 at 220.90. This will now remain the favored case long as 197.47 support holds.

Yen Recovers as Tokyo Steps In, Worst of Selling May Be Past… for Now

Yen recovered modestly in Asian session as Tokyo officials reissued verbal warnings against excessive moves in the currency market. After the week's accelerated selling following Sanae Takaichi’s election as LDP leader, the latest remarks from Finance Minister Katsunobu Kato suggest Japan may be nearing an intervention threshold, at least rhetorically. For now, traders appear to be scaling back short positions, hinting that Yen’s near-term selling climax could be behind it.

Kato said authorities were closely watching “one-sided, rapid moves on the foreign exchange market,” reiterating that exchange rates should reflect economic fundamentals and move in an orderly manner. “The government will thoroughly monitor for excessive fluctuations and disorderly movements,” he emphasized. Still, he struck a balanced note on the impact of the weaker Yen, acknowledging that “the extent and nature of these effects vary depending on the domestic and global environment", suggesting that actual intervention is not imminent.

Former BoJ board member Atsushi Takeuchi also weighed in, telling Reuters that authorities would likely tolerate gradual declines but intervene if speculation about the Yen sliding to 160–170 per Dollar gains traction. “If the Yen falls that much, authorities could and must step in,” he said. While intervention “can’t change the broad market trend", it can "put a pause to sharp Yen declines.”

Meanwhile, Prime Minister-designate Sanae Takaichi is trying to walk a fine line. On one hand, she said she does not want to trigger excessive depreciation. On the other, she stressed that the BoJ’s policy decisions must align with government priorities, hinting at a preference for demand-driven inflation and cautioning against premature rate hikes. That stance could delay further BoJ tightening and leave Yen vulnerable in a risk-on environment.

Elsewhere, attention turns to Canada’s employment report due later today, a key input for the BoC’s October 29 rate decision. The BoC resumed rate cuts in September after a soft patch in the labor market and cited export weakness—linked to U.S. tariff policy—as a major uncertainty. A steady employment reading could justify a pause, but another downbeat print—particularly in manufacturing and export-heavy sectors—could tilt the balance toward more easing. USD/CAD is now pressing key resistance level at 1.4, and the next move is decisive for the near-term trend.

In the broader currency markets, Dollar is currently the week’s strongest performer, followed by Loonie and Aussie. Yen still sits at the bottom, trailed by Euro and Swiss Franc, while Sterling and the Kiwi hover in the middle of the pack.

In Asia, at the time of writing, Nikkei is down -0.98%. Hong Kong HSI is down -1.14%. China Shanghai SSE is down -0.51%. Singapore Strait Times is down -0.08%. Japan 10-year JGB yield is up 0.02 at 1.699. Overnight, DOW fell -0.52%. S&P 500 fell -0.28%. NASDAQ fell -0.08%. 10-year yield rose 0.019 to 4.148.

Fed’s Barr sees need for caution, notes stronger spending and sticky inflation

Fed Governor Michael Barr said in a speech overnight that monetary policy remains “modestly restrictive”, and supported the decision to lower the federal funds rate by 25 bps at the September meeting. He said the move brought the stance “a bit closer toward neutral,” but emphasized that further adjustments should depend on new data and the evolving balance of risks.

Barr noted that since the September meeting, consumer spending has surprised to the upside, with data showing activity on a “notably stronger trajectory” than previously thought. That, he said, prompted most observers to revise up forecasts for GDP growth through the remainder of the year. Inflation, meanwhile, “moved up as expected,” with core PCE remaining well above the 2% target.

The Fed governor cautioned that “considerable uncertainty” continues to cloud the outlook. Slower payroll growth could be a “harbinger of worse to come,” he said, though it might also stabilize given the low unemployment rate and solid growth backdrop. On inflation, he warned that tariffs could have only a modest effect on prices—or, conversely, trigger renewed price pressures if expectations begin to rise.

Barr concluded that the FOMC should remain “cautious” about adjusting policy until more evidence clarifies the direction of the economy. “If we see inflation moving further away from our target, it may be necessary to keep policy at least modestly restrictive for longer,” he said. “If we see heightened risks in the labor market, we may need to move more quickly to ease policy.”

Fed’s Williams sees lower rates this year, tariff impact on inflation as limited

New York Fed President John Williams said in an interview with The New York Times that he still expects interest rates to be lower by year-end, but emphasized that the pace and extent of easing will depend on incoming data.

When asked about the possibility of two additional 25bps reductions, Williams said that would depend on whether inflation and employment evolve broadly in line with his outlook. He expects inflation to “move up a bit to around near 3%” and unemployment to edge slightly higher, in which case “policy should evolve the way we expect.”

But he warned against complacency, noting that it would be “very damaging to the economy and the Fed’s credibility” if inflation were allowed to rise well above 2% without action.

Williams downplayed fears that President Donald Trump’s tariffs were fueling persistent inflation. He estimated the measures have lifted the price level by only 0.25 to 0.5 percentage point, adding that “underlying inflation seems to be moving gradually lower toward 2%.” He also said there were no signs of second-round effects, suggesting tariffs are having limited spillovers on broader price dynamics.

At the same time, Williams pointed to rising downside risks to employment, which he said were offsetting some of the upside risk to inflation.

Japan producer prices hold at 2.7% as import declines ease in September

Japan’s corporate goods price index rose 2.7% yoy in September, unchanged from August and slightly above expectations of 2.5%. The data suggest that while upstream cost pressures remain contained, they have yet to fade meaningfully.

Yen-based import price index declined -0.8% yoy, a much smaller drop than August’s -3.9%, pointing to easing import deflation as Yen’s weakness and rising global input costs filter through.

In terms of components, food and beverage prices climbed 4.7% yoy, following a 4.9% in August. Agricultural goods prices, including rice, jumped 30.5%, moderating from August’s 41% surge.

RBA’s Bullock: Inflation back in band but services still sticky, jobs market tight

RBA Governor Michele Bullock told lawmakers today that the economy is in a “pretty good spot,” with inflation back within the 2–3% target band and the labor market still tight. Speaking before a parliamentary committee in Canberra, she said, "the key now is to make sure it stays there sustainably.”

She said that services inflation remains the main concern, running “a little sticky” at around 3%, even as goods inflation continues to moderate. That offset has kept headline inflation contained for now.

On employment, Bullock said the labor market is in “a pretty good place”, though “possibly a little bit tight” in certain sectors. The RBA expects unemployment to edge higher over the coming months, a move consistent with a gradual rebalancing.

She also highlighted that household consumption is picking up, filling the gap left by weaker public demand—an important transition, she said, to keep growth on track.

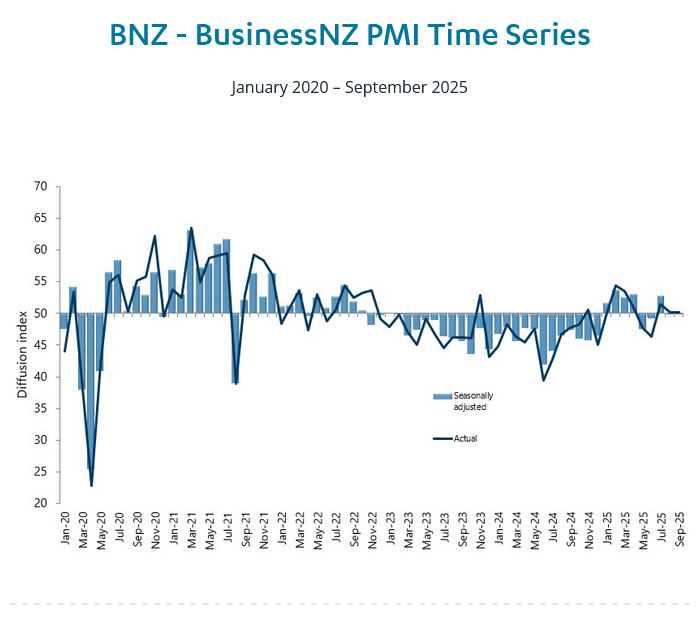

NZ BNZ manufacturing flat at 49.9, firms cite soft demand and rising costs

New Zealand’s BNZ Performance of Manufacturing Index held steady at 49.9 in September, marking another month of contraction and remaining below its long-term average of 52.4.

The data highlighted a mixed picture across key components — production edged up from 47.8 to 50.1, barely returning to expansion, while employment dropped from 49.1 to 47.5, weighing on the overall index. New orders also slipped from 54.7 to 50.3, suggesting softening demand momentum.

BusinessNZ Director of Advocacy Catherine Beard said it was encouraging that the PMI did not show deeper contraction, but the sector remained “agonizingly close to returning to expansion mode.” She added weakness in employment prevented the headline figure from crossing the 50 threshold.

Survey respondents continued to highlight muted customer demand and rising cost pressures, with 60% of comments negative, up from August. Manufacturers reported lower order volumes, tight margins, and competitive pricing pressures, reflecting both domestic uncertainty and subdued export demand.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 203.03; (P) 203.96; (R1) 204.61; More...

A temporary top was formed at 205.30 with current retreat, and intraday bias in GBP/JPY is turned neutral for consolidations. Downside should b contained above 201.24 resistance turned support to bring another rally. On the upside, break of 205.30 will resume the rise from 197.47 to 61.8% projection of 184.35 to 199.96 from 197.47 at 207.11.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a corrective pattern which might have completed at 184.35. Firm break of 208.09 high will resume the up trend from 123.94 (2020 low). Next target is 61.8% projection of 148.93 to 208.09 from 184.35 at 220.90. This will now remain the favored case long as 197.47 support holds.

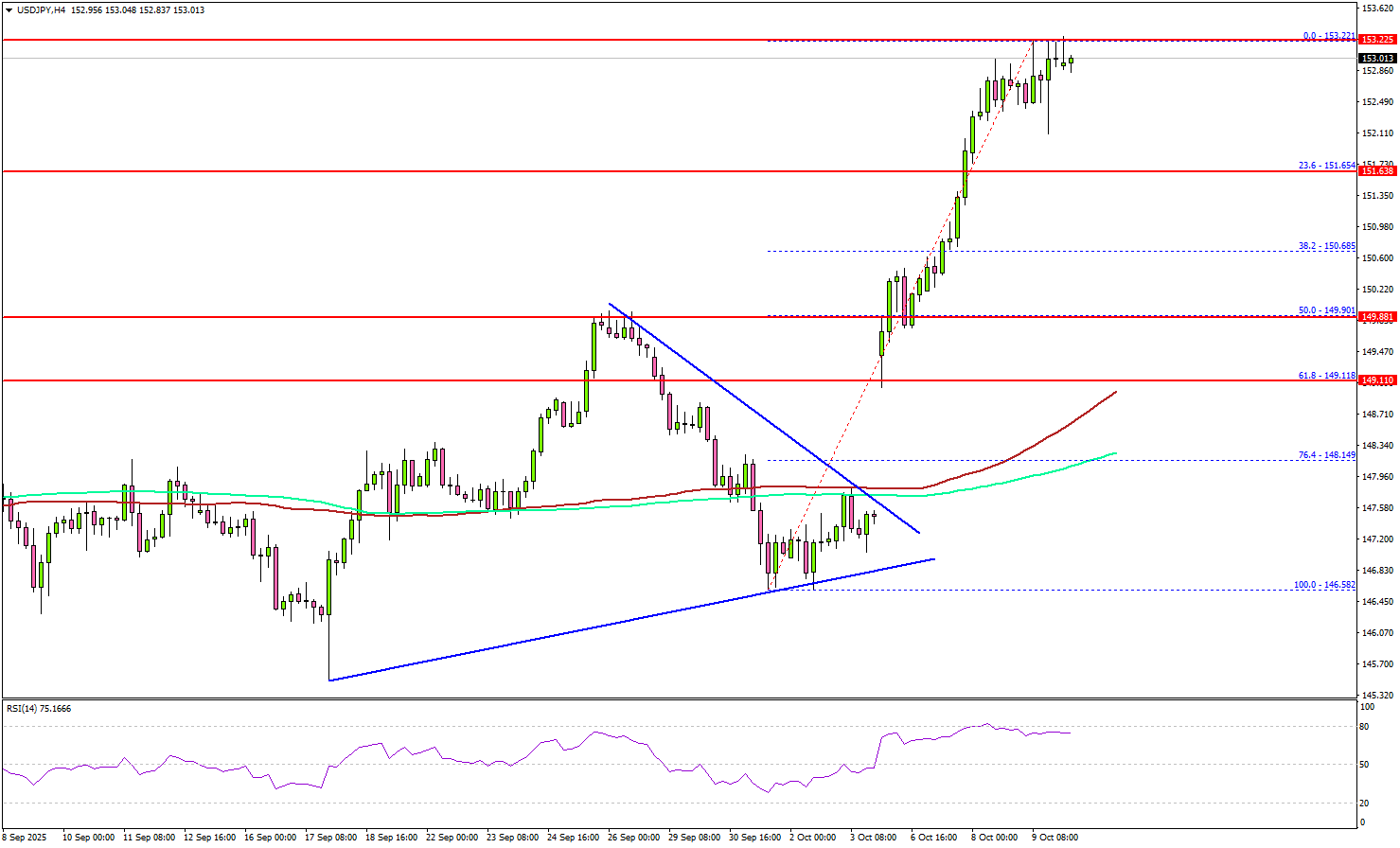

USD/JPY Rally Could Extend – Bulls Eye Fresh Gains Amid Momentum

Key Highlights

- USD/JPY rallied above 150.50 and 152.00.

- The pair could aim for more gains if it clears the 153.20 resistance on the 4-hour chart.

- EUR/USD extended losses below 1.1620 and 1.1600.

- GBP/USD is also moving lower below the 1.3450 pivot level.

USD/JPY Technical Analysis

The US Dollar started a fresh surge above 150.00 against the Japanese Yen. USD/JPY cleared many hurdles near 150.50, 151.20, and 152.00.

Looking at the 4-hour chart, the pair climbed above 153.00 before the bears appeared. The pair started a short-term consolidation phase and corrected some pips. On the downside, there is key support at 152.50.

The next area of interest might be near the 23.6% Fib retracement level of the upward move from the 146.58 swing low to the 153.22 high. The main support could be 150.00.

Any more losses might increase selling pressure and send the pair toward the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour) at 148.20. It is close to the 76.4% Fib retracement level of the upward move from the 146.58 swing low to the 153.22 high.

To start a decent increase, USD/JPY must settle above 153.20. The main hurdle could be 153.80. A close above 153.80 could start a steady increase to 155.00.

Looking at EUR/USD, the pair faced an increase in selling pressure, resulting in a drop below the 1.1620 support zone.

Upcoming Key Economic Events:

- Michigan Consumer Sentiment Index for Oct 2025 (Prelim) – Forecast 54.2, versus 55.1 previous.

- Canada’s Employment Change for Sep 2025 – Forecast 5K, versus -65.5K previous.

- Canada’s Unemployment Rate for Sep 2025 - Forecast 7.2%, versus 7.1% previous.

RBA’s Bullock: Inflation back in band but services still sticky, jobs market tight

RBA Governor Michele Bullock told lawmakers today that the economy is in a “pretty good spot,” with inflation back within the 2–3% target band and the labor market still tight. Speaking before a parliamentary committee in Canberra, she said, "the key now is to make sure it stays there sustainably.”

She said that services inflation remains the main concern, running “a little sticky” at around 3%, even as goods inflation continues to moderate. That offset has kept headline inflation contained for now.

On employment, Bullock said the labor market is in “a pretty good place”, though “possibly a little bit tight” in certain sectors. The RBA expects unemployment to edge higher over the coming months, a move consistent with a gradual rebalancing.

She also highlighted that household consumption is picking up, filling the gap left by weaker public demand—an important transition, she said, to keep growth on track.

Japan producer prices hold at 2.7% as import declines ease in September

Japan’s corporate goods price index rose 2.7% yoy in September, unchanged from August and slightly above expectations of 2.5%. The data suggest that while upstream cost pressures remain contained, they have yet to fade meaningfully.

Yen-based import price index declined -0.8% yoy, a much smaller drop than August’s -3.9%, pointing to easing import deflation as Yen’s weakness and rising global input costs filter through.

In terms of components, food and beverage prices climbed 4.7% yoy, following a 4.9% in August. Agricultural goods prices, including rice, jumped 30.5%, moderating from August’s 41% surge.

NZ BNZ manufacturing flat at 49.9, firms cite soft demand and rising costs

New Zealand’s BNZ Performance of Manufacturing Index held steady at 49.9 in September, marking another month of contraction and remaining below its long-term average of 52.4.

The data highlighted a mixed picture across key components — production edged up from 47.8 to 50.1, barely returning to expansion, while employment dropped from 49.1 to 47.5, weighing on the overall index. New orders also slipped from 54.7 to 50.3, suggesting softening demand momentum.

BusinessNZ Director of Advocacy Catherine Beard said it was encouraging that the PMI did not show deeper contraction, but the sector remained “agonizingly close to returning to expansion mode.” She added weakness in employment prevented the headline figure from crossing the 50 threshold.

Survey respondents continued to highlight muted customer demand and rising cost pressures, with 60% of comments negative, up from August. Manufacturers reported lower order volumes, tight margins, and competitive pricing pressures, reflecting both domestic uncertainty and subdued export demand.

Fed’s Barr sees need for caution, notes stronger spending and sticky inflation

Fed Governor Michael Barr said in a speech overnight that monetary policy remains “modestly restrictive”, and supported the decision to lower the federal funds rate by 25 bps at the September meeting. He said the move brought the stance “a bit closer toward neutral,” but emphasized that further adjustments should depend on new data and the evolving balance of risks.

Barr noted that since the September meeting, consumer spending has surprised to the upside, with data showing activity on a “notably stronger trajectory” than previously thought. That, he said, prompted most observers to revise up forecasts for GDP growth through the remainder of the year. Inflation, meanwhile, “moved up as expected,” with core PCE remaining well above the 2% target.

The Fed governor cautioned that “considerable uncertainty” continues to cloud the outlook. Slower payroll growth could be a “harbinger of worse to come,” he said, though it might also stabilize given the low unemployment rate and solid growth backdrop. On inflation, he warned that tariffs could have only a modest effect on prices—or, conversely, trigger renewed price pressures if expectations begin to rise.

Barr concluded that the FOMC should remain “cautious” about adjusting policy until more evidence clarifies the direction of the economy. “If we see inflation moving further away from our target, it may be necessary to keep policy at least modestly restrictive for longer,” he said. “If we see heightened risks in the labor market, we may need to move more quickly to ease policy.”

They’ll Go with the (Data) Flow

The RBA has almost certainly not yet decided whether or not to cut the cash rate in November. The data flow from here will determine the outcome, with hesitation now likely to result in more cuts later.

- There is still enough data to come before the next RBA meeting to justify a November cut, even though currently available information would suggest a hold is more likely.

- Some recent data on inflation and household spending may contain less signal about the outlook for subsequent quarters than the RBA’s September communication seems to imply. A hold in November could be followed by a downside inflation surprise in the December quarter and a cash rate cut in February, similar to the flow of surprises in late 2023 and early 2024.

- If the RBA does hold the cash rate steady at the November meeting, the chance increases that it cuts in February and ends up at a trough of 2.85% rather than something higher.

It’s almost certain that RBA has not yet decided whether or not to cut the cash rate at its November meeting. If the meeting were held today, they would keep rates on hold, awaiting further data. Several potentially decisive data releases are due before the actual meeting, though, including the September labour data and the full quarterly CPI. Until then, we need to hold two possible futures in mind: hold or cut.

The August CPI indicator did imply an ugly result for the September quarter. Our own nowcast for the trimmed mean measure is a ‘big’ 0.8%qtr that could easily round up to a 0.9%, a result that would surely stay the RBA’s hand. Looking at the detail, though, outside home-building costs it is not clear that the August data provided much signal of an ongoing higher rate of inflation than expected. As we noted at the time, the result in market services was mixed, with some personal services inflation below our forecasts while the cost of eating out was stronger. The latter suggests that, following a period of retrenchment in hospitality (evident in the labour account employment data), improving conditions have allowed for some margin repair. Some of the price gains may also indirectly relate to recent annual award wage increase; though this is a normal seasonal effect, its size will depend on how margins react. Neither of these influences on price growth are likely to be sustained if demand remains patchy.

We therefore think the economy could be in for something like a re-run of late 2023, when an upside surprise in September quarter inflation was followed by a downside surprise (to something more like our own near-cast) in the December quarter. The result was a hike in late 2023 followed by an ‘on-the-fly’ pivot following the February 2024 meeting – from flagging possible further hikes in the post-meeting statement to ‘not ruling anything in or out’ in the media conference. That message landed a lot better, and sure enough, the next move was, eventually, a cut.

We are also mindful of the two-sided risks around both the labour market and household spending data. We will know more about the labour market shortly when the September monthly labour force data is released next week, completing the picture for the quarter. So far, we see a gradual softening in employment growth as demand pivots away from the jobs-rich ‘care economy’. The unemployment and underemployment consequences of this are being masked by an unwind in the extra labour supply induced by earlier cost-of-living pressures. With demographic drivers still implying an upward trend in labour force participation, we see more latent labour market slack emerging over time and weighing on wages growth and inflation. There is precedent for this outcome in Australia’s experience in the late 2010s.

On household spending, the August Household Spending Indicator, released after the September RBA Monetary Policy Board (MPB) meeting, was notably below market expectations. This accords with our assessment that the expected recovery in consumer spending has been patchy and that the strength in national accounts consumption in Q2 partly reflected some one-off factors such as insurance payouts and the unwinding of some electricity rebates. Though we see two-sided risks around the consumption outlook, the more downbeat tone from consumer sentiment in recent months certainly suggests that underlying momentum is still subdued. Given how weak real household incomes have been for a number of years, this ongoing pessimistic tone does not surprise us.

Recall also that a recovery in household spending is necessary to counterbalance the slowdown in public sector demand growth that is already underway. Faster growth in household spending should only stay the MPB’s hand from further rate cuts if the pick-up is stronger than implied by the RBA’s August forecasts. These were constructed on an assumption of a couple more cash rate cuts, as the market was pricing at the time. Far too many observers are in the habit of seeing any pick-up in demand or housing prices as something for policy to react against, rather than as the expected and intended transmission of monetary policy. The Governor’s comments at the latest media conference show that the RBA, at least, does understand the difference.

The rates outlook boils down to the issue of how much signal to take from an upside surprise in one quarter in terms of what that means for subsequent quarters. RBA Governor Bullock has on several occasions insisted that ‘we will be guided by our forecasts’. However, that statement sits a bit uncomfortably with the flat profile for the RBA’s trimmed mean inflation forecasts and the unemployment rate. These give the impression of a set of forecasts being used as a communication device to explain and frame a policy decision rather than an independent input into that decision. This is understandable and perhaps inevitable given the judgement involved in synthesising the output of many different models and information sources. However, it does hold the risk that the policy view helps shape the forecast rather than the other way around.

What’s left in these circumstances is reactivity to incoming data – that is, to the recent past. As well as making policy less predictable – contrary to the MPB’s stated intentions – it is not a great way to run an economy policy setting that affects the economy with a lag, especially when inflation has been within the target range for a little while now at the same time as policy is likely still restrictive.

Bottom line: the odds that the RBA cuts in November are, at this point, below 50% but still a long way from zero. The data flow could change things again. Frankly, the prospect of flip-flopping a ‘call’ as the month goes on is unattractive, especially when it is quite obvious that the policymakers have not made up their mind yet. We must hold the two possibilities in mind at least until the labour market data come in. (A good-enough labour market result would make it unlikely that the RBA would cut, even if the September quarter CPI comes in a little more benign than we currently expect.)

The RBA communications schedule has half a dozen speeches between now and the November meeting that will be opportunities for it to provide guidance on some of its key forecast judgements, though they all pre-date the release of the September quarter CPI. If the RBA does hold in November, though, our conviction that they end up cutting in February rises, as does our expectation that the trough will be 2.85% rather than something higher. The more the MPB hesitates in the face of uncertainty, the more likely it is that domestic inflation pressures surprise it on the downside next year, and trimmed mean inflation turns out more like the Westpac Economics forecast than the August RBA one.

Cliff Notes: Risks to the Downside

Key insights from the week that was.

In Australia, the only update of note this week was October’s Westpac-MI Consumer Sentiment Survey, which ultimately disappointed with a –3.5% decline to 92.1. Combined with last month’s fall, all gains over May to August have been erased and sentiment is now back into outright pessimistic territory. The most recent fall appears to be largely a consequence of renewed fears over the cost-of-living following the latest stronger-than-expected inflation update.

This looks to have fed through to households’ opinions on family finances. Both sub-indexes tracking current views and expectations deteriorating sharply back below long-run averages (–4.8% and –9.9% respectively). This coincided with the lift in expectations around mortgage interest rates. That said, while some consumers appeared to be ‘bracing for the worst’ as far as last week’s RBA’s decision was concerned, the Board’s non-committal and cautious language accompanying the decision went some way towards calming these fears. On the economy, consumers have become more downbeat on the year-ahead outlook (–2.5%) but remain fairly agnostic on the medium-to-longer term outlook (+1.4%).

Against this backdrop, consumers’ spending intentions remain a clear laggard in the survey detail. At 97.2, the ‘time to buy a major household item’ sub-index is some 21% below long-run average levels. This strikes a similar tone to official household spending data which is pointing to a more modest recovery following a solid showing in Q2 (which was buoyed by temporary factors including insurance payouts, abnormal seasonality, and EOFY sales). Going forward while a recovery is clearly underway, households’ ‘value-conscious’ attitude suggests that underlying momentum is still subdued. As a result, spending growth may remain patchy over the coming months and quarters.

This implies that the projected recovery in household spending is unlikely to be a decisive factor in the RBA’s near-term policy decision. Instead, as Chief Economist Luci Ellis highlights in this week’s essay, attention will be focused on upcoming labour market and inflation data ahead of the RBA’s November decision – the RBA has almost certainly not yet decided whether or not to cut the cash rate in November with these updates set to be the big deciding factor.

Offshore, the US government failed to reach an agreement on spending extending the shutdown and continuing to disrupt the release of official data. Consequently, attention was focused on the minutes of the FOMC’s September meeting.

The minutes struck a balanced tone with members highlighting both upside risks to inflation and growing downside risks to employment. The decision to cut rates by 25bps was motivated by weaker labour market conditions which also led them to "no longer characterize labor market conditions as solid". Though downside risks were emphasised, the FOMC also affirmed they did not see a sharp deterioration in labour market conditions and that softer job gains were a function of both labour demand and supply, the latter reflecting the impact of fewer migrants. The view on inflation was more encouraging with the minutes noting that "excluding the effects of this year’s tariff increases, inflation would be close to target" and that they "perceived less upside risk to their outlooks for inflation than earlier in the year". While concerns around inflation had subsided, the committee continues to expect an increase in inflation in the near-term and are attuned to how this is being transmitted into inflation expectations. We anticipate the FOMC will cut the federal funds rate once more this year, consistent with their view that " it likely would be appropriate to ease policy further over the remainder of this year".

Closer to home, the Reserve Bank of New Zealand cut its OCR by 50bps, a move that was out of consensus with the market but anticipated by our New Zealand colleagues. The Committee's concern around excess capacity motivated the larger move though a 25bp cut was also considered. Forward guidance provided in the Media Release suggests further reductions are likely, we expect a 25bp cut in November. Further details on RBNZ's announcement can be found here.