Sample Category Title

Canadian Employment Makes a Comeback – USD/CAD Reverses

Markets just received the Canadian labor report — and unlike the still-missing U.S. one (thanks, government shutdown), this one actually delivered. Canada added +60K jobs vs. +5K expected, a sharp rebound from last month’s -65K loss.

Even better, most of these gains came from full-time positions, signaling renewed strength in the labor market.

Being bullish on the CAD hasn’t been a winning trade this year. It’s been one of the top underperformers in FX—now only slightly ahead of the even weaker JPY—caught in the middle of a challenging macro backdrop.

As a cyclical economy, Canada cooled rapidly after its huge 2022–2023 period.

The job market softened, real estate activity slumped, and slower immigration weighed further on overall growth. Combined with tensions between Ottawa and the Trump-Administration regarding US-Canada trade, the outlook for the loonie had been anything but bright.

Oil prices (One of Canada's top export, linked to CAD performance) trending down to 5-year lows also haven't helped the Maple Dollar much.

WTI Oil actually just dipped below $60 – this may hurt US Shale producers even further and hence have less of a net-negative effect on the CAD.

Check how well Oil and the Canadian Dollar correlate throughout the years

WTI Oil and CAD/USD since 1998, Source: TradingView

But things might be starting to look better

However, the ongoing Trump–Carney talks this week are reviving optimism for improved trade conditions.

Canadian trade envoy Dominic Leblanc described the talks from this week as "successful, positive, substantive", but markets are still awaiting for decisive news on tariffs, particularly on steel.

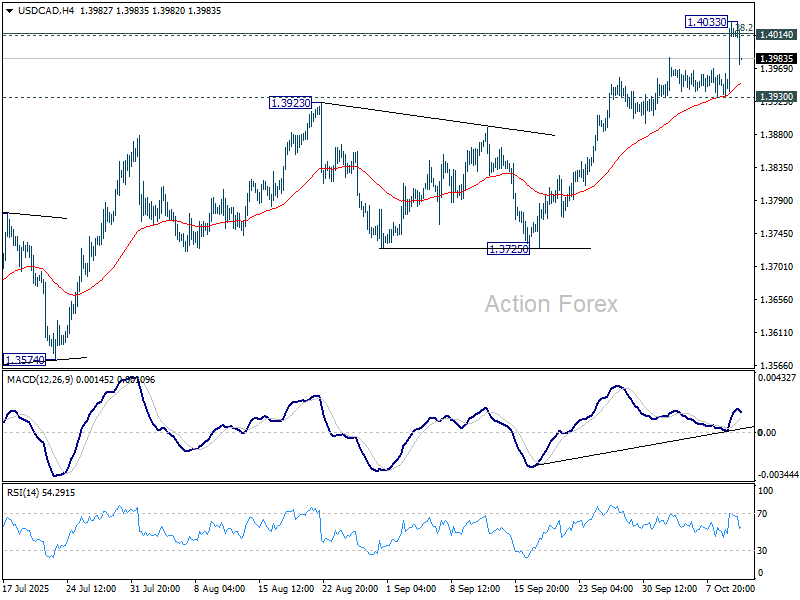

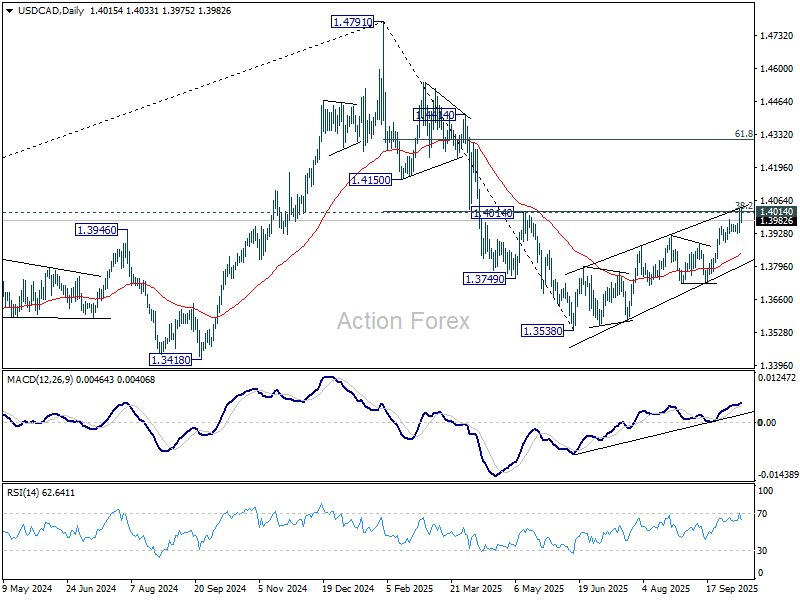

With USD/CAD testing and rejecting the 1.40 level, let’s dive into a multi-timeframe analysis to see what comes next.

USD/CAD multi-timeframe analysis

Daily Chart

USD/CAD Daily Chart, October 10, 2025 – Source: TradingView

After bearish failure in the pair throughout multiple consolidation periods, USD/CAD has rallied in steps – Initially ranging between 1.36 to 1.38, then 1.37 to 1.39 leading to today.

Some countering elements are blurring the picture looking forward: The price action is bullish, with prices just moving above the 200-Day MA acting as immediate support.

The 1.40 level on the other hand opposes a huge psychological resistance for the pair.

The session and weekly close will be important for the pair: Anything below, traders consider that the trade outlook between US and Canada is not looking too bad.

A close above 1.40 continues the bullish trend to retest April resistances.

4H Chart and levels

USD/CAD 4H Chart, October 10, 2025 – Source: TradingView

The latest move upward was more due to the broad US Dollar rally than pure Canadian Dollar weakness.

Loonie weakness was at the center of its low performance this year, whcih also invites to look at other CAD pairs for decent opportunities.

One can also track how prices react to a test of the 4H-MA 50 (1.39560) and upward trendline for upcoming trading.

Levels to place on your USDCAD charts:

Resistance Levels

- 1.40 to 1.4050 Psychological resistance

- Yesterday highs 1.40342

- April Resistance 1.41 - 1.4150

- April Pivotal resistance 1.4250

Support Levels

- Major Daily Pivot 1.39

- 200-Day MA 1.39750 (immediate support)

- 1.38 Major Support

- Major Support Zone 1.3675 to 1.37

- 1.3550 Main 2025 Support

1H Chart

USD/CAD 1H Chart, October 10, 2025 – Source: TradingView

Looking at teh keys to the current price action, USDCAD is in the middle of some key developments.

A break above the weekly highs (1.4030) should turn into a further breakout. Odds of this are increased on a daily close above 1.40.

A break below 1.3550 could accelerate towards the 1.39 Main Pivot, key for future price action.

Any daily close below the zone (1.3880 are the lows) point to a solid re-entry within the 1.36 to 1.39 5-month range.

Safe Trades!

Sunset Market Commentary

Markets

Rating agency Moody’s publishes its verdict tonight on Belgium’s Aa3 rating review. Almost exactly one year ago, they changed the outlook on that rating from stable to negative. The decision reflected the risk that the (then) next government would be unable to implement measures to stabilize the government debt burden. In the absence of a large fiscal consolidation programme, debt will continue to rise due to the material structural increase in expenditures in recent years and persistent spending pressure. Moody’s flagged structural headwinds to fiscal consolidation and the lack of intergovernmental coordination mechanisms to achieve an effort at all levels of governments as other vulnerabilities. Looking back, the Belgian federal government aimed at a 5.4% of GDP deficit by the end of this year. Latest estimates by the Planning Bureau suggest that 5.8% of GDP is the more likely outcome, coming close to the Monitoring Committee’s worst-case scenario of 5.9%. Negotiations for the 2026 budget are currently ongoing, but we’re looking at efforts to stabilize the deficit ratio at best. PM De Wever has stated that at least €10bn in cuts would be the minimum required to meet EU expectations (4.5% of GDP deficit next year), but even within the ruling coalition this is labelled excessive. The Planning Bureau even estimates the deficit to rise again to as much as 6.5% of GDP next year due to persistent structural imbalances and spending pressures. Belgium is currently under the Excessive Deficit Procedure with the EC recommending to limit net expenditure growth to 2.5% next year in order to keep the deficit reduction path toward 3% of GDP by 2029 alive. Long story cut short, there’s a reasonable risk that the downgrade criteria from Moody’s have been met, especially with the debt ratio remaining on a rising trend towards 110% of GDP next year. Back in June, rating agency Fitch was the first to strip Belgium off its AA rating. They stressed the structural weakening of Belgium’s fiscal position over the last few years. They did the same to France in September over exactly the same reasons. Rating agency S&P gives an update on Belgium’s AA rating (negative outlook) on October 24. Both Belgium and especially France are gradually evolving to “sick men in Europe”. A quick look at swapspreads shows France (83 bps) now trading above Italy (81 bps) and Belgium (57 bps) above Spain (55 bps). We continue to see risks for more relative underperformance from Belgium and again especially France. We stick to our view that markets underestimate the risks of snap legislative elections even after Macron announces a new technocrat PM tonight. The more this becomes a market theme, the more it can weigh on the single currency in the short term. EUR/USD holds below the 1.16 handle for now with next technical support at 1.1392.

News & Views

Norwegian headline inflation quickened from -0.6% to 0.4% in September, lifting the annual print from 3.5% to 3.6%. Clothing & footwear (4% m/m), education (2.5%),communications (1.1%) and housing (0.7%) showed some of the largest price increases. Core CPI rose by 0.2% m/m. The yearly 3% that marked the first deceleration (from August’s 3.1%) in four months came as a slight downside surprise, both for consensus (3.1%) and the Norges Bank (3.2%). The central bank last month cut the policy rate to 4% but still-elevated inflation meant it saw virtually no more room for further normalization. The updated forecast indicated one move annually over the next three years. Markets slightly add to the easing bets but nevertheless expect nothing to happen at least through 2026Q1. The Norwegian krone underperforms global peers. EUR/NOK rises to 11.68.

Canadian employment growth blew away expectations, adding 60.4k jobs in September. Analysts braced for a meagre 5k after the combined 105k contraction in July & August. Full-timers more than offset a 45.6k decline in part-time jobs. The unemployment rate stabilized at a four-year high of 7.1% while the participation rate marginally recovered to 65.2% to remain amongst the lowest readings in both the pre- and post-Covid era. The better-than-expected outcome should alleviate some of the concerns at the Bank of Canada. Ottawa lowered rates to 2.5% in September. Aside from diminished upside inflation risks it referred to the two previous disappointing reports as a sign of a weakening labour market which would weigh on household spending in the months ahead. Canadian money markets assumed the BoC to cut rates more or less one more time this year but start doubting now. The market implied probability dropped from 90% to 65%. The Canadian dollar strengthens with USD/CAD dropping back below 1.40 after closing above that level yesterday for the first time since mid-April.

US UoM consumer sentiment ticks down to 55.0, inflation expectations remain stubbornly high

US consumer sentiment softened slightly in October, with the University of Michigan index slipping marginally from 55.1 to 55.0, in line with expectations. The details painted a mixed picture—Current Economic Conditions improved to 61.0 from 60.4, while the Expectations Index edged lower to 51.2 from 51.7.

The survey showed that improvements in current personal finances and year-ahead business conditions were offset by a deterioration in future personal finance expectations and current buying conditions for durable goods. That combination points to a fragile confidence backdrop, as households continue to wrestle with elevated prices and high borrowing costs, even amid a resilient job market.

On inflation, expectations remain uncomfortably high. Year-ahead inflation eased slightly from 4.7% to 4.6%, while long-run expectations were unchanged at 3.7%, both well above the Fed’s 2% target.

Canada’s Jobs Jump Up in September, Unemployment Rate Steady as Labour Force Surges

Canada's economy added a staggering 60k jobs in September (+0.3% month/month), 55k more than consensus expectations for a 5k gain. The details were similarly strong with full-time positions jumping 106k, and the private sector rising 22K.

The unemployment rate held steady at 7.1% in September, as the labour force more than made up for the past two months of losses, adding 72k workers.

Job gains were concentrated in manufacturing (+28k), health care and social assistance (+14k), and agriculture (+13k). The biggest losses were seen in wholesale and retail trade (-21k), construction (-8.2k), and transportation and warehousing (-7.4k).

Wage growth was steady in September with average hourly wages up 3.6% versus a year ago.

Key Implications

Well, that's quite the surprise. Canada's job market looks like it recovered all of August's losses in September. Importantly, even for a noisy data series, this is a strong result. That said, it's important to note that the unemployment rate remained unchanged as the labour force jumped by an even greater amount. Considering population growth slowed to 28k people, the biggest surprise was a large influx of new workers despite a weak job market.

The Bank of Canada's next decision is due at the end of the month and this surprise from the labour market could change the calculus on the decision. However, underlying inflation continues to hover within the target range and the unemployment rate suggest that the labour market still has excess slack. The next inflation report is due on the 21st and the bar will be even higher for inflation to underperform and bring the BoC onside for another rate cut. Markets seems to agree as the pricing for a rate cut materially deteriorated this morning.

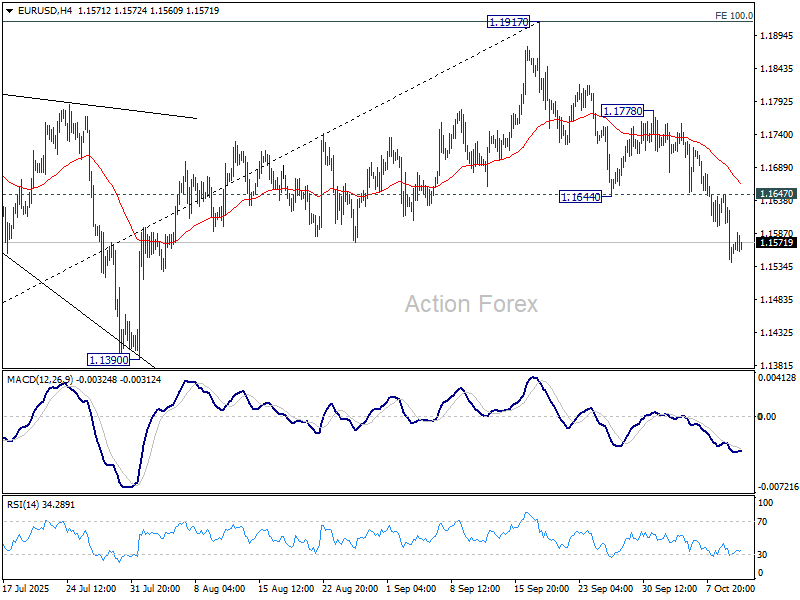

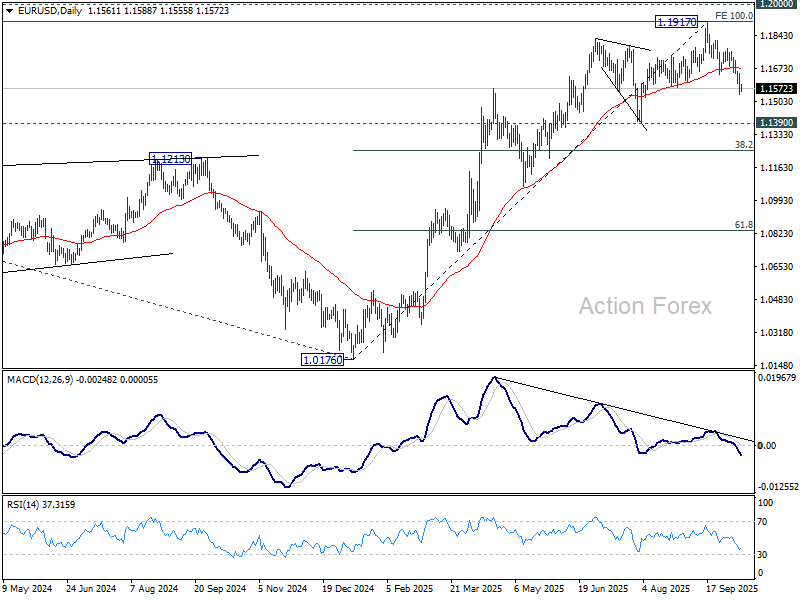

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1521; (P) 1.1585; (R1) 1.1627; More…

Intraday bias in EUR/USD remains neutral. Fall from 1.1917 is in progress for 1.1390 support. Break there will target 38.2% retracement of 1.0176 to 1.1917 at 1.1252. On the upside, above 1.1647 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 1.1778 resistance holds, in case of recovery.

In the bigger picture, rise from 1.0176 (2025 low) is seen as the third leg of the pattern from 0.9534 (2022 low). 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916 was already met. For now, further rally will remain in favor as long as 1.1390 support holds, and firm break of 1.2000 psychological level will carry larger bullish implications. However, firm break of 1.1390 will suggest that rise from 1.0176 has already completed and bring deeper fall to 55 W EMA (now at 1.1265) and below.

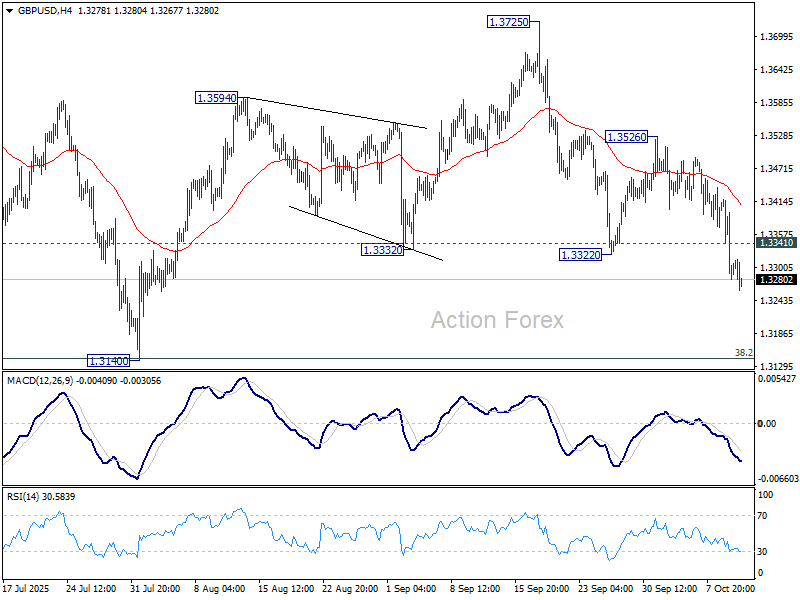

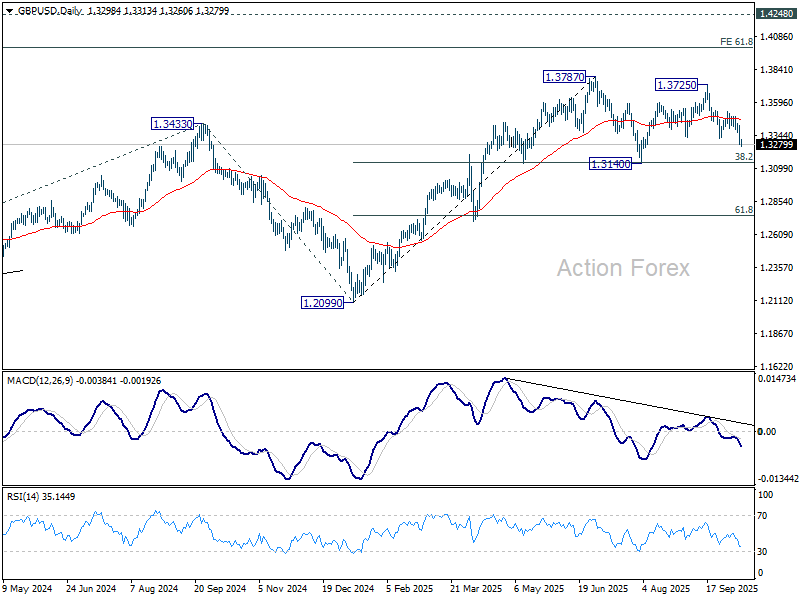

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3250; (P) 1.3334; (R1) 1.3389; More...

Intraday bias in GBP/USD remains on the downside, as fall from 1.3725 is in progress for 1.3140. Strong support is expected from there to bring rebound to complete the corrective pattern from 1.3787 high. On the upside, above 1.3341 minor resistance will turn intraday bias neutral again first.

In the bigger picture, rise from 1.0351 (2022 low) is still seen as a corrective move. Further rally could be seen to 61.8% projection of 1.0351 to 1.3433 (2024 high) from 1.2099 (2025 low) at 1.4004. But strong resistance could be seen from 1.4248 (2021 high) to limit upside. Sustained break of 55 W EMA (now at 1.3176) will argue that a medium term top has already formed and bring deeper fall back to 1.2099.

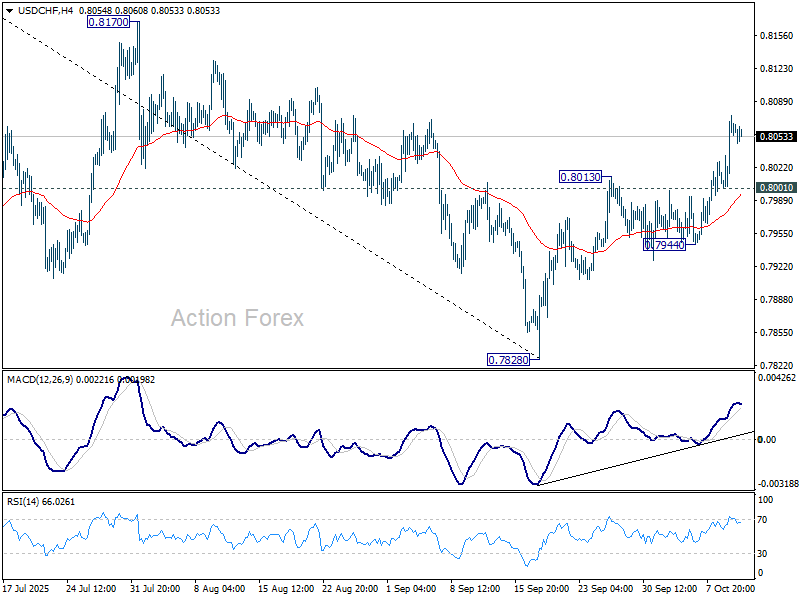

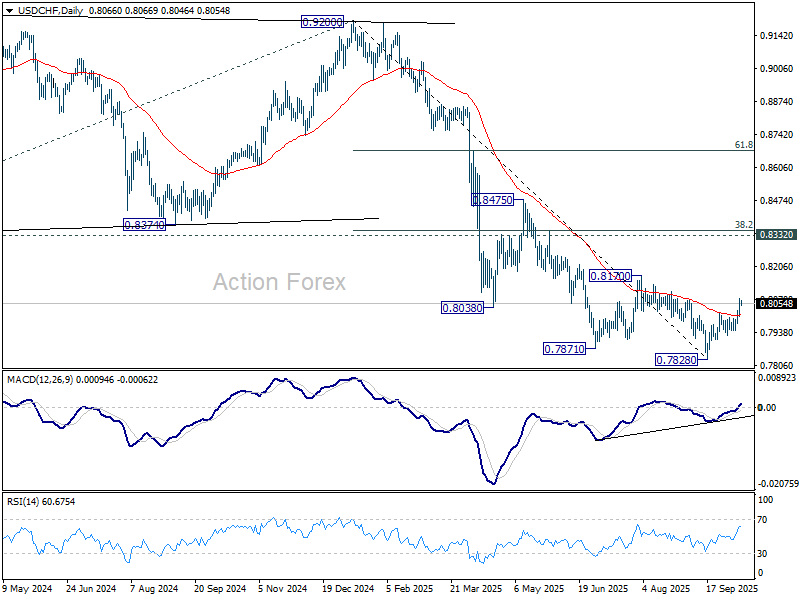

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8019; (P) 0.8047; (R1) 0.8092; More…

Intraday bias in USD/CHF remains on the upside at this point. Rise from 0.7828 is seen as correcting whole fall from 0.9200. Further rise should be seen to 0.8170 resistance. Firm break there will target 38.2% retracement of 0.9200 to 0.7828 at 0.8352. On the downside, below 0.8001 minor support will turn intraday bias neutral and bring consolidations first, before staging another rally.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

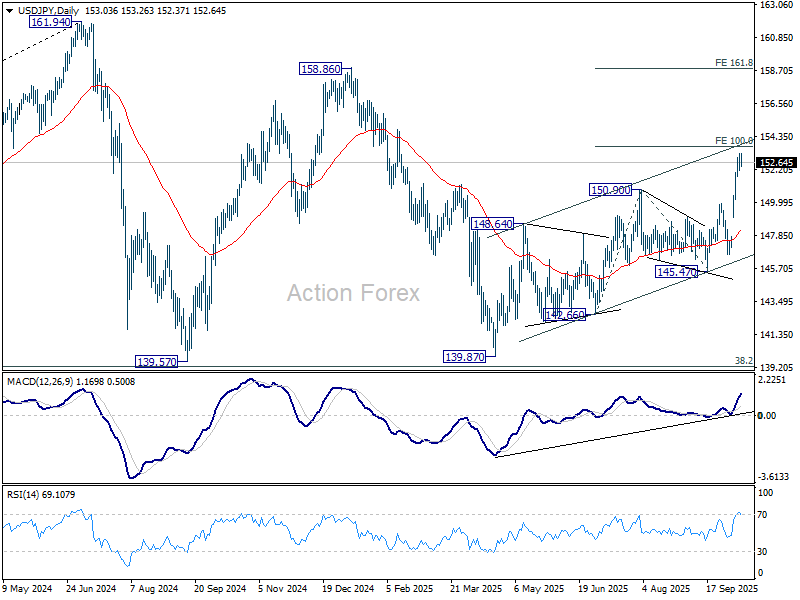

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 152.40; (P) 152.81; (R1) 153.51; More...

Intraday bias in USD/JPY stays neutral and more consolidations could be seen below 153.26 temporary top. Downside should be contained above 149.95 resistance turned support to bring another rally. On the upside, above 153.26 will resume larger rise to 100% projection of 142.66 to 150.90 from 145.47 at 153.71. Firm break there will pave the way to 161.8% projection at 158.80.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 145.47 support will dampen this bullish view and extend the corrective pattern with another falling leg.

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3959; (P) 1.3996; (R1) 1.4059; More...

Intraday bias in USD/CAD is turned neutral again with current retreat. On the downside, firm break of 1.3930 support will indicate rejection by 1.4014/7 cluster resistance. That would keep the rebound from 1.3538 corrective, and turn bias to the downside for 1.3725 support. Nevertheless, sustained break of 1.4014/7 cluster resistance will suggest that USD/CAD Is already reversing the whole fall from 1.4719, and target 61.8% retracement at 1.4312.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 cluster resistance (38.2% retracement of 1.4791 to 1.3538 at 1.4017) holds. However sustained trading above 1.4014 will suggest that it's more likely just a correction, and the larger up trend would be in favor to resume through 1.4791 at a later stage.

Loonie Rises on Strong Jobs Data, BoC Pressure Eases

Canadian Dollar strengthened notably in the early U.S. session after robust September employment data signaled that Canada’s economy was more resilient than anticipated in face of U.S. tariffs.. The upbeat data provided a welcome boost to the Loonie, which had already been one of the week’s top performers, and may prompt markets to reassess expectations for further rate cuts from the BoC later this month.

The strength of the report should ease pressure on the BoC ahead of its October 29 policy meeting. The central bank resumed rate cuts in September amid a softening labor market and persistent trade uncertainty, but the latest data point to renewed momentum, particularly in full-time employment and manufacturing. That may give policymakers room to pause and evaluate whether recent easing has already stabilized conditions.

The next major test will come from September CPI on October 21, which will help determine whether the recent easing has struck the right balance between supporting growth and containing inflation.

Meanwhile in Japan, political uncertainty returned to the spotlight as Sanae Takaichi’s premiership bid was thrown into doubt. The ruling LDP’s coalition partner Komeito announced its withdrawal from the alliance after disputes over the handling of a political funding scandal, ending a 26-year relationship. Komeito leader Tetsuo Saito said the party would not support Takaichi in the parliamentary vote expected later this month, leaving her leadership uncertain.

Takaichi called the decision “extremely regrettable,” vowing to continue efforts to form a government. The political split adds to the uncertainty surrounding Japan’s policy direction, particularly with Takaichi’s fiscally expansionary and dovish leanings toward monetary policy. Nonetheless, the Yen managed to stabilize, aided by verbal intervention from Japanese officials stressing that FX moves must reflect fundamentals.

Overall, Dollar remains the week’s strongest performer, followed by Loonie, which now has a chance to overtake if post-jobs momentum continues. Aussie remains third strongest. At the other end, Yen remains the weakest, with Euro and Sterling trailing just ahead. Swiss Franc and Kiwi are holding in the middle.

In Europe, at the time of writing, FTSE is up 0.03%. DAX is up 0.04%. CAC is up 0.01%. UK 10-year yield is down -0.062 at 4.687. Germany 10-year yield is down -0.031 at 2.671. Earlier in Asia, Nikkei fell -1.01%. Hong Kong HSI fell -1.73%. China Shanghai SSE fell -0.94%. Singapore Strait Times fell -0.30%. Japan 10-year JGB yield fell -0.001 to 1.696.

Canada jobs surge 60.4k in September, unemployment steady at 7.1%

Canada’s labor market delivered a strong upside surprise in September, with employment rising by 60.4k, well above expectations of just 2.8k. The gains were concentrated in manufacturing (+28k), health care and social assistance (+14k), and agriculture (+13k), while wholesale and retail trade saw a notable decline of -21k.

The report reinforces signs of resilience across key sectors even amid broader uncertainty over the impact of U.S. trade and tariff policies.

The data also showed a healthy quality of job growth, with full-time employment surging 106k while part-time positions dropped -46k, suggesting improved job stability.

Unemployment rate held steady at 7.1%, defying expectations for a modest uptick to 7.2%. Wage growth also firmed slightly, with average hourly earnings up 3.3% yoy, from 3.2% yoy in August.

Japan producer prices hold at 2.7% as import declines ease in September

Japan’s corporate goods price index rose 2.7% yoy in September, unchanged from August and slightly above expectations of 2.5%. The data suggest that while upstream cost pressures remain contained, they have yet to fade meaningfully.

Yen-based import price index declined -0.8% yoy, a much smaller drop than August’s -3.9%, pointing to easing import deflation as Yen’s weakness and rising global input costs filter through.

In terms of components, food and beverage prices climbed 4.7% yoy, following a 4.9% in August. Agricultural goods prices, including rice, jumped 30.5%, moderating from August’s 41% surge.

RBA’s Bullock: Inflation back in band but services still sticky, jobs market tight

RBA Governor Michele Bullock told lawmakers today that the economy is in a “pretty good spot,” with inflation back within the 2–3% target band and the labor market still tight. Speaking before a parliamentary committee in Canberra, she said, "the key now is to make sure it stays there sustainably.”

She said that services inflation remains the main concern, running “a little sticky” at around 3%, even as goods inflation continues to moderate. That offset has kept headline inflation contained for now.

On employment, Bullock said the labor market is in “a pretty good place”, though “possibly a little bit tight” in certain sectors. The RBA expects unemployment to edge higher over the coming months, a move consistent with a gradual rebalancing.

She also highlighted that household consumption is picking up, filling the gap left by weaker public demand—an important transition, she said, to keep growth on track.

NZ BNZ manufacturing flat at 49.9, firms cite soft demand and rising costs

New Zealand’s BNZ Performance of Manufacturing Index held steady at 49.9 in September, marking another month of contraction and remaining below its long-term average of 52.4.

The data highlighted a mixed picture across key components — production edged up from 47.8 to 50.1, barely returning to expansion, while employment dropped from 49.1 to 47.5, weighing on the overall index. New orders also slipped from 54.7 to 50.3, suggesting softening demand momentum.

BusinessNZ Director of Advocacy Catherine Beard said it was encouraging that the PMI did not show deeper contraction, but the sector remained “agonizingly close to returning to expansion mode.” She added weakness in employment prevented the headline figure from crossing the 50 threshold.

Survey respondents continued to highlight muted customer demand and rising cost pressures, with 60% of comments negative, up from August. Manufacturers reported lower order volumes, tight margins, and competitive pricing pressures, reflecting both domestic uncertainty and subdued export demand.

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3959; (P) 1.3996; (R1) 1.4059; More...

Intraday bias in USD/CAD is turned neutral again with current retreat. On the downside, firm break of 1.3930 support will indicate rejection by 1.4014/7 cluster resistance. That would keep the rebound from 1.3538 corrective, and turn bias to the downside for 1.3725 support. Nevertheless, sustained break of 1.4014/7 cluster resistance will suggest that USD/CAD Is already reversing the whole fall from 1.4719, and target 61.8% retracement at 1.4312.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 cluster resistance (38.2% retracement of 1.4791 to 1.3538 at 1.4017) holds. However sustained trading above 1.4014 will suggest that it's more likely just a correction, and the larger up trend would be in favor to resume through 1.4791 at a later stage.