Sample Category Title

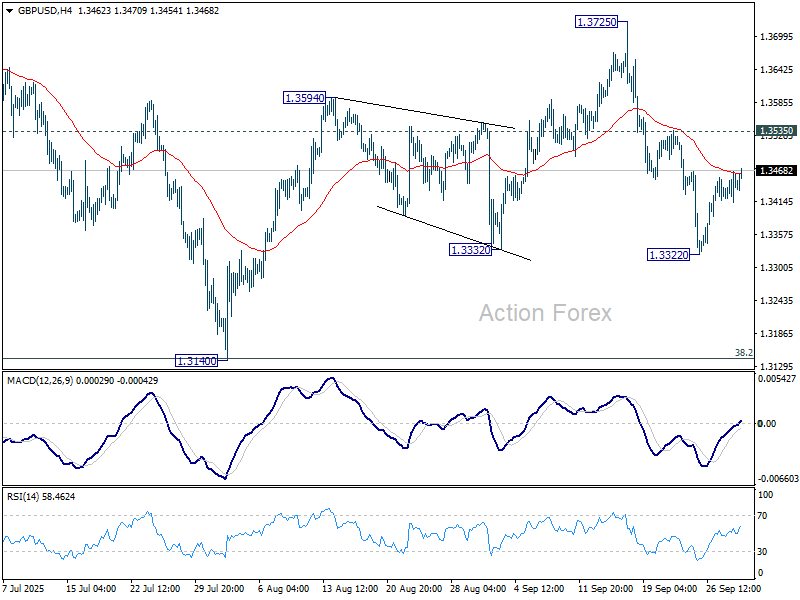

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3418; (P) 1.3442; (R1) 1.3471; More...

Outlook in GBP/USD is unchanged and intraday bias remains neutral. Further decline is expected as long as 1.3535 resistance holds. Break of 1.3322 will resume the fall from 1.3725, as the third leg of the corrective pattern from 1.3787, and target 1.3140 support.

In the bigger picture, rise from 1.0351 (2022 low) is still seen as a corrective move. Further rally could be seen to 61.8% projection of 1.0351 to 1.3433 (2024 high) from 1.2099 (2025 low) at 1.4004. But strong resistance could be seen from 1.4248 (2021 high) to limit upside. Sustained break of 55 W EMA (now at 1.3155) will argue that a medium term top has already formed and bring deeper fall back to 1.2099.

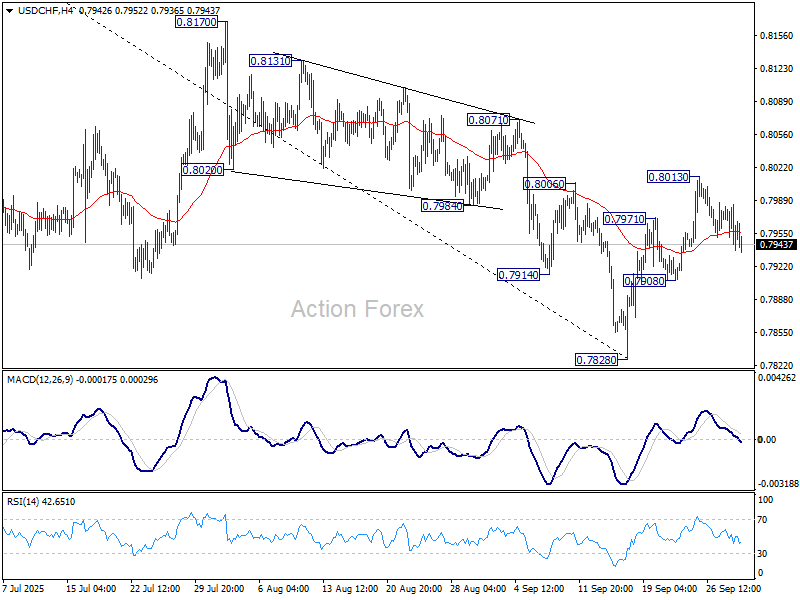

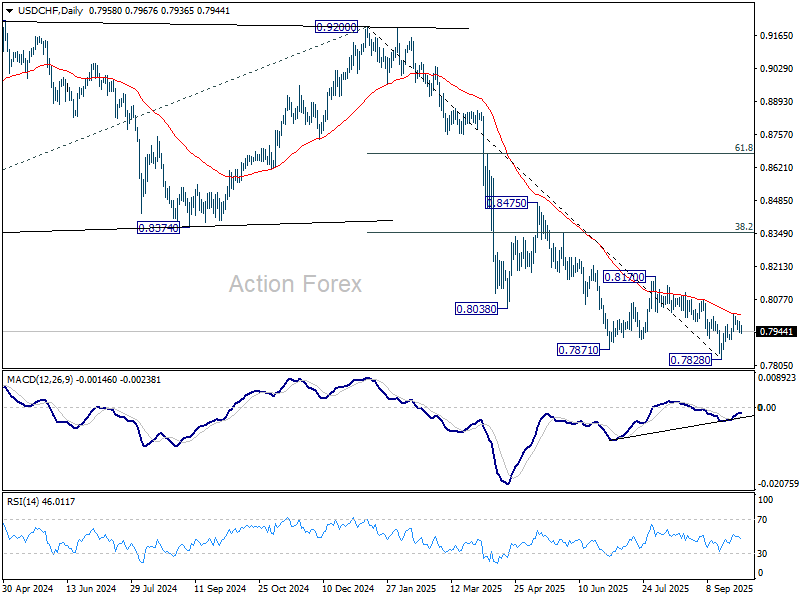

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7941; (P) 0.7963; (R1) 0.7988; More…

Intraday bias in USD/CHF stays neutral and outlook is unchanged. On the upside, sustained trading above 55 D EMA (now at 0.8014) will suggest that rise from 0.7828 is already correcting whole fall from 0.9200. Further rise should the be seen to 0.8170 resistance and possibly above. However, break of 0.7908 will turn bias back to the downside for retesting 0.7828 low.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

US Shutdown Pressures Dollar, Adds Shine to Gold

The US government has shut down from today as politicians failed to agree on a plan to continue funding it. This is not the first time this has happened, and it certainly won’t be the last. Since 1976, there have been around 20 government shutdowns, caused by funding gaps lasting at least one business day. The average duration is about 8 days. Most shutdowns last only a few days, and only a handful stretched over multiple weeks. The longest in recent history was a partial shutdown that lasted 35 days between December 2018 and January 2019.

The market impact of shutdowns is not necessarily dramatic — far from it. For bonds, the flight to safety usually benefits US Treasuries, and since the government continues servicing its debt during shutdowns, the overall impact is limited, slightly positive. That’s what we see this morning, with the US 10-year yield edging lower on shutdown headlines.

On the currency front, the US dollar tends to weaken when the government shuts down. Limited dollar appetite and a softer DXY come as no surprise today. The yen and Swiss franc are attracting safe-haven flows, the EURUSD looks set to test the 1.18 area and could clear resistance if the shutdown drags on, while Cable could push back above 1.35 despite ongoing UK political noise.

For equities, the impact of a government shutdown could be positive. In fact, the S&P500 gained during three of the last four government shutdowns, and it gained more than 10% during the 2018-2019 shutdown that also coincided with a Federal Reserve pivot.

Shutdown news is weighing on US futures this morning, but they’re not the end of the world. The most inconvenient impact will be delays to economic data — and this week, that includes the all-important jobs report.

Speaking of data: yesterday’s JOLTS figures came in stronger than expected, with last month’s number revised slightly higher. That said, job openings are now at their lowest since 2021 and weaker-than-expected consumer confidence and a sharper contraction in Chicago PMI released yesterday also supported the dovish Fed outlook. The US 2-year yield has fallen for a fourth straight session.

Today, ADP — a private data provider unaffected by the shutdown — will publish its September jobs report. It is expected to show a soft gain of around 50K jobs. Even if Friday’s official payrolls are delayed, JOLTS plus ADP could still give investors a decent picture of labour market momentum and keep Fed expectations intact. A weaker ADP reading would reinforce the dovish view, pushing US yields and the dollar lower while supporting equities. A stronger print could temper those expectations, but only a very robust figure in the 150–200K range would seriously challenge the market’s assumption of upcoming cuts — and that seems unlikely given recent labour trends. As such, the more probable scenario is continued softness in US jobs data, keeping downward pressure on the dollar.

The weaker Dollar has already been a boon for precious metals. Gold and silver remain heavily in demand, with both seen as overbought but still attracting inflows. Add in the US-China trade tensions, broader geopolitical risks, waning appetite for USD and Treasuries, and now the shutdown, and the bullish case for gold remains strong. Historical patterns and technical signals also back that view.

On top of that, China has been gradually positioning the yuan and Gold as alternatives to the US Dollar. Reports suggest Beijing encourages trade partners to convert surpluses into gold stored in Shanghai. If even 80% of China’s trade surplus were converted, it could require 15–20% of annual global gold output — creating a powerful tailwind for prices. The bigger the surplus, the stronger the demand, and the higher the support for gold.

No surprise then that gold has attracted massive inflows this year, with appetite remaining strong even at record highs — and gold miners are reaping the benefits. Fresnillo in London, for example, has seen its share price surge more than 300% since January, compared with about 110% for Nvidia since its April low.

In the same vein, Zijin Gold International made a spectacular debut in Hong Kong this week, marking the city’s second-largest IPO of the year. The stock soared 68% on day one, giving the company a market cap above HK$300 billion (nearly US$40 billion) — performance more typical of a hot tech IPO than a miner. Whether the gold rush continues is an open question, but for now, the arguments in favour of further gains outweigh the risks to the downside.

US Government Shuts Down as Political Gridlocks Deepens

In focus today

In the euro area, focus turns to the September inflation report. We expect euro area inflation to increase to 2.2% y/y from 2.0% y/y. While inflation in some countries, like France and Spain, came in lower than expected, other countries such as Germany and Italy exceeded expectations. These opposing surprises have balanced each other out, leaving the overall inflation rate on track to align with prior consensus expectations. We also receive the final euro area manufacturing PMI. The flash manufacturing PMI declined to 49.5 from 50.7 following the great improvement in 2025. We expect the final data to confirm the flash release.

From the US, ADP's September private sector employment report will provide markets with the first sense of what to expect from Friday's key nonfarm payrolls release. ISM manufacturing index is also due for release for September.

Economic and market news

What happened overnight

In the US, the government shut down at 06:00 CET as deep partisan divisions have prevented Congress and the White House from reaching a funding agreement. The direct macroeconomic impact is expected to be limited, but markets are likely to focus on two key implications: potential delays in the publication of US economic data, particularly the September NFP employment report, and the potential layoffs of public sector workers as highlighted by the White House. While these factors may not significantly alter the macroeconomic outlook, they could, all else being equal, modestly increase the likelihood of the Fed considering a rate cut in October.

In Japan, The Q3 Tankan business survey came in close to expectations with the main index for large manufacturers improving a bit to index 14. It has been quite stable for two years. The non-manufacturing index was unchanged at 34, which is close to the highest post-1991 levels. The outlook indices are a bit less rosy but still solid and with businesses' 5Y inflation expectations edging a bit higher to 2.4%, the updated Tankan survey should not stand in the way of a rate hike at the BoJ's policy meeting at the end of the month. About 10bp are priced in for now.

What happened yesterday

In the euro area, September inflation data from key countries suggest headline inflation is likely to track at 2.2% y/y, aligning with consensus as country-level surprises balance out. Headline inflation came in lower than expected in France at 1.1% y/y, while it exceeded expectations in Italy and Germany at 1.8% y/y and 2.4% y/y, respectively. Services inflation remained a consistent driver across the region, with uneven monthly trends in energy and food prices. Core inflation momentum was stable, indicating limited underlying pressures. The data reinforce the expectation that the ECB will maintain a cautious stance, monitoring further developments before reassessing its outlook.

In the US, August JOLTs job openings data landed close to expectations (7.23M, July 7.18M). Hiring slowed down, but so did involuntary layoffs, suggesting that overall labour market conditions remain broadly stable. Similarly, the ratio of job openings to the number of unemployed jobseekers remains little changed from July at 0.98 (from 0.996).

In Sweden, retail sales increased by 0.9% m/m and 4.4% y/y, driven by a 1.9% increase in durable goods, while consumables (excluding Systembolaget) remained flat. The data reflects the positive trend in retail sales and supports our forecast of gradually growing consumption.

Equities: Global equities were largely unimpressed by the decent JOLTS report yesterday, while also factoring in the weaker-than-expected Conference Board data and the looming deadline for a US government shutdown, which ultimately transpired. The US equity indices staged a late rally in the final half hour of the trading session for the quarter. The S&P500 ended 0.4% higher yesterday, while the Nasdaq rose 0.3%. Compared to the start of the quarter, both the S&P and Nasdaq have returned 8%. The comparable return was 3% for the Stoxx 600.

FI and FX: EUR/USD continues to trade around the 1.1750 mark, while SEK and NOK have been off to a week start to the week. US yields continued to drift lower during yesterday's session, particularly in the front-end with the 2-year US Treasury yield 5-6bp lower. While yesterday's JOLTS data was relatively solid, markets focused more on the softer-than-expected Conference Board consumer confidence print. Focus now turns to the first shutdown of the US government in seven years after Republicans and Democrats failed to strike an agreement to fund the federal government into the new fiscal year. On data releases, we look out for ISM manufacturing and the ADP employment report. In the euro area, yields were little changed. Regional inflation data painted a mixed picture, with Germany surprising to the upside while Spain and France came in softer. With 82% of the euro area HICP basket now released, we track today's euro area headline at 2.2% y/y, broadly in line with consensus, as opposing surprises largely offset each other.

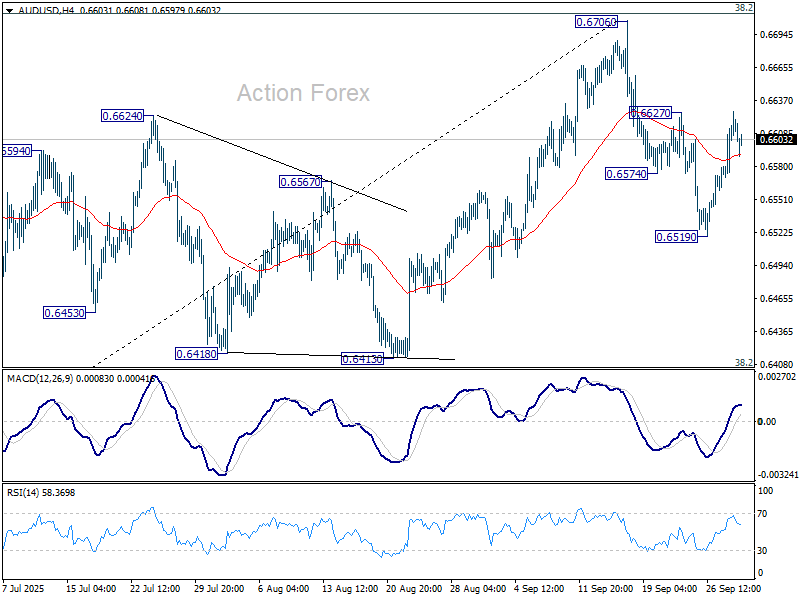

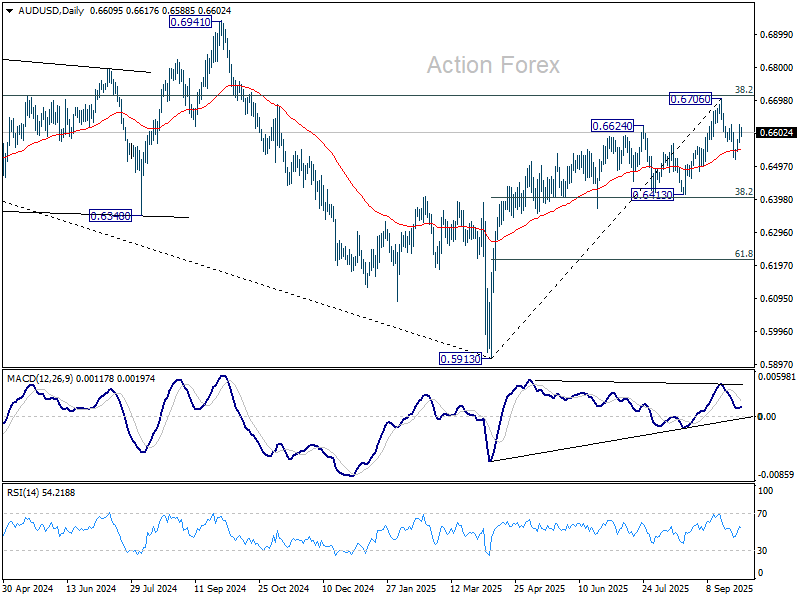

AUD/USD Daily Report

Daily Pivots: (S1) 0.6580; (P) 0.6604; (R1) 0.6638; More...

AUD/USD retreated after touching 0.6627 resistance and intraday bias stays neutral. Firm break of 0.6627 will suggest that pullback from 0.6706 has completed as correction, after drawing support from 55 D EMA (now at 0.6550). That will keep the larger rally from 0.5913 alive and bring retest of 0.6706 high. However, on the downside, sustained trading below 55 D EMA will confirm rejection by 0.6713 fibonacci resistance, and bring deeper fall to 0.6413 cluster support (38.2% retracement of 0.5913 to 0.6706 at 0.6403).

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. Outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, sustained break of 0.6713 will be a strong sign of bullish trend reversal, and pave the way to 0.6941 structural resistance for confirmation.

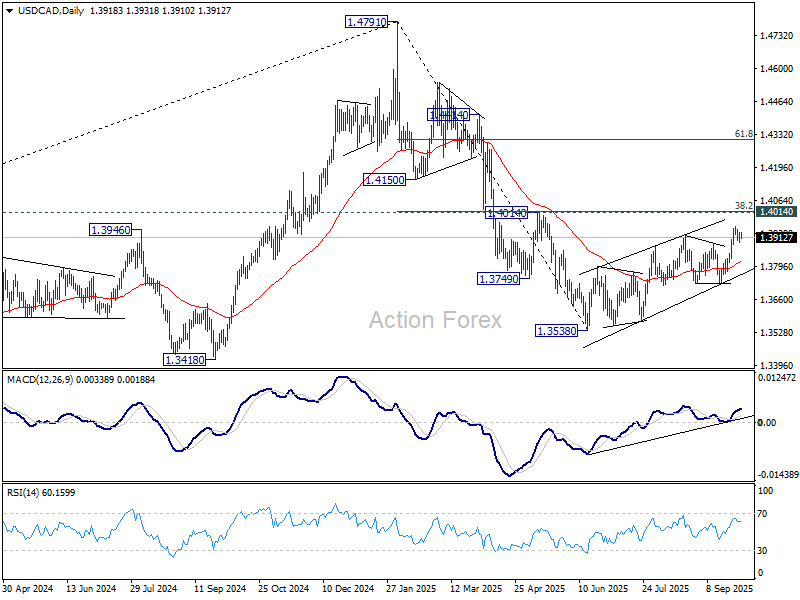

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3900; (P) 1.3918; (R1) 1.3939; More...

USD/CAD is staying in consolidations below 1.3957 temporary top and intraday bias remains neutral. On the upside, break of 1.3957 will resume the corrective rebound from 1.3538. But upside should be limited by 1.4014 cluster resistance to bring reversal. Meanwhile, sustained trading below 55 4H EMA (now at 1.3880) will bring deeper fall back to 1.3725 support.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 cluster resistance (38.2% retracement of 1.4791 to 1.3538 at 1.4017) holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 (2025 high) at 1.3069. However, sustained break of 1.4014 will argue that fall from 1.4791 has completed, and bring stronger rally to 61.8% retracement at 1.4312.

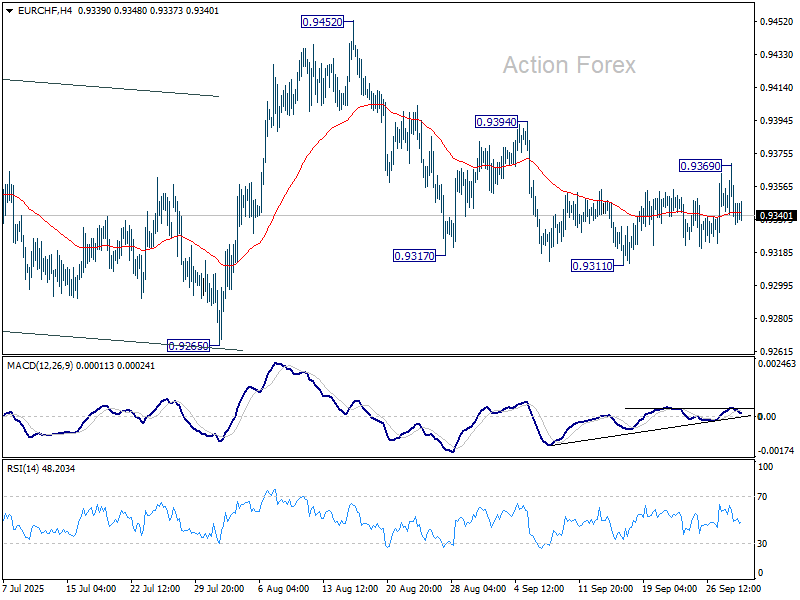

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9324; (P) 0.9357; (R1) 0.9378; More...

EUR/CHF retreated after brief spike to 0.9369 and intraday bias is turned neutral again. On the upside, above 0.9369 will target 0.9394 resistance. Firm break there should confirm that the pullback from 0.9452 has completed, and bring retest of this resistance. Nevertheless, break of 0.9311 will resume the fall from 0.9452 to 0.9265 support.

In the bigger picture, the down trend from 0.9204 (2018 high) might still be in progress considering that EUR/CHF is staying well inside the long term falling channel. However, with bullish convergence condition in W MACD, downside potential should be limited in case of another fall. Instead, firm break of 0.9660 resistance will be an important sign of medium term bullish trend reversal.

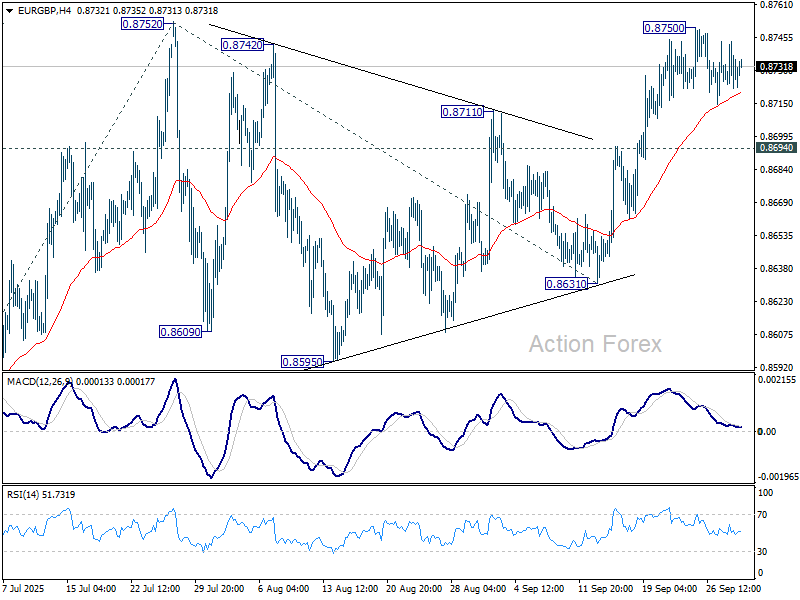

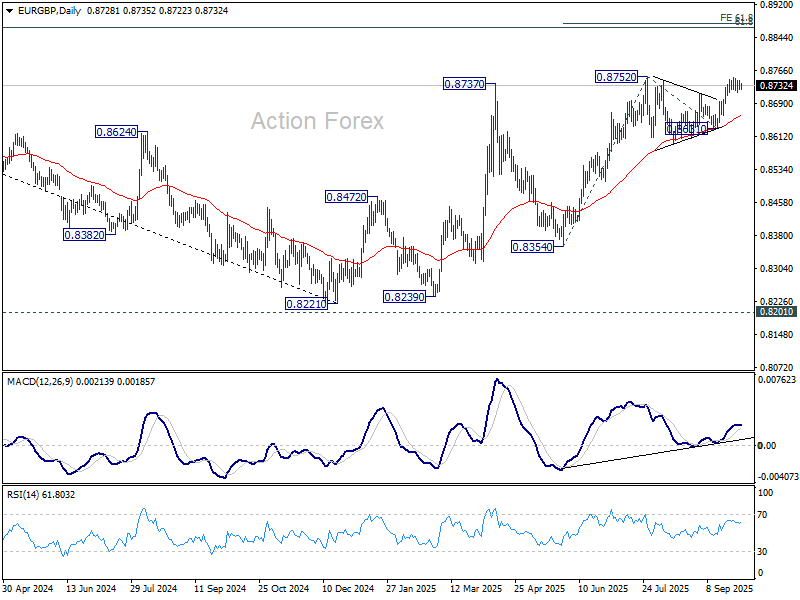

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8718; (P) 0.8732; (R1) 0.8740; More...

EUR/GBP is staying in consolidations below 0.8750 and intraday bias remains neutral. Further rally is expected as long as 0.8694 support holds. Firm break of 0.8752 will resume larger rally to 61.8% projection of 0.8354 to 0.8752 from 0.8631 at 0.8877, which is close to 0.8867 fibonacci level. However, break of 0.8694 will turn bias back to the downside for 0.8631 support instead.

In the bigger picture, the structure from 0.8221 medium term bottom are not impulsive enough to suggest that it's reversing the down trend from 0.9267 (2022 high). But even if it's a correction, further rise could still be seen to 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Nevertheless, sustained trading below 55 W EMA (now at 0.8533) will argue that the pattern has completed and bring retest of 0.8221 low.

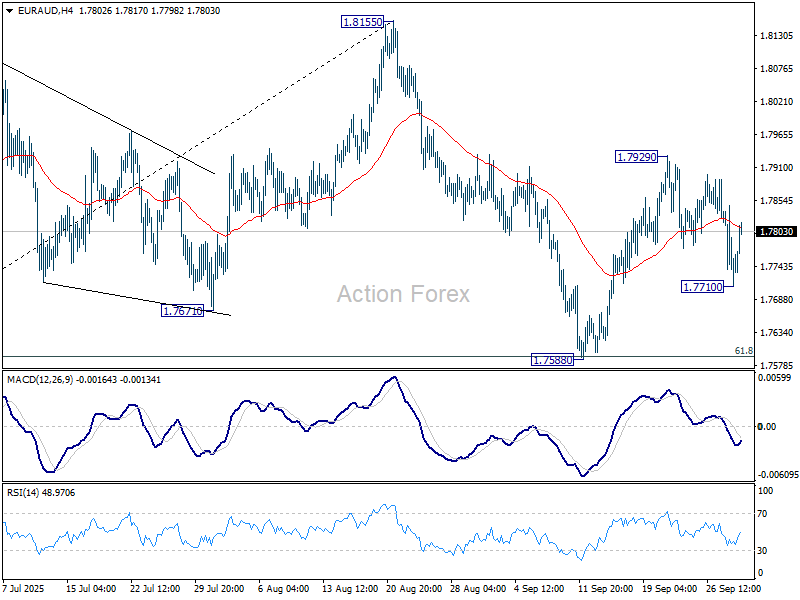

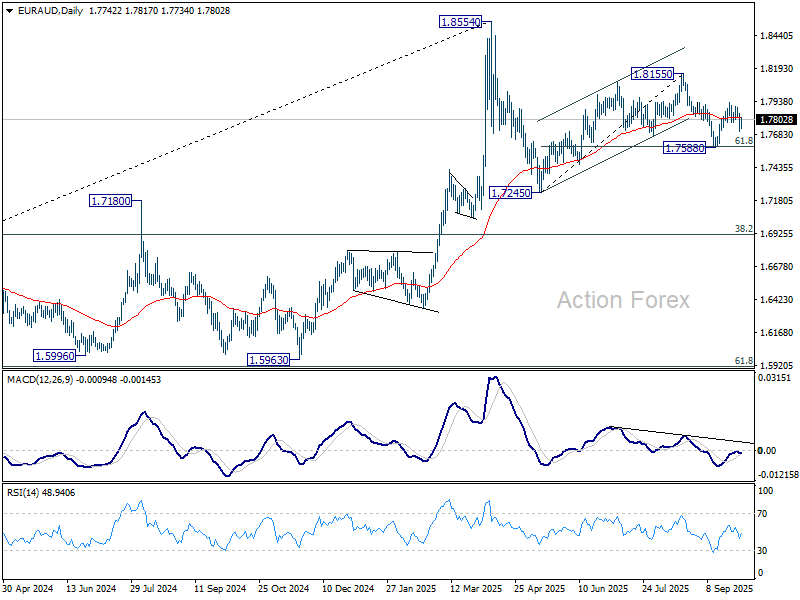

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7689; (P) 1.7769; (R1) 1.7824; More...

Intraday bias in EUR/AUD remains neutral and more consolidations could be seen below 1.7929. On the upside, above 1.7929 will resume the rebound from 1.7588 to retest 1.8155. However, sustained break of 61.8% retracement of 1.7245 to 1.8155 at 1.7593, will resume the fall from 1.8155 to 1.7245 resistance, as part of the corrective pattern from 1.8554 high.

In the bigger picture, price actions from 1.8554 medium term top are seen as a corrective pattern. Deeper fall could be seen as the pattern extends, but downside should be contained by 38.2% retracement of 1.4281 (2022 low) to 1.8554 at 1.6922 to bring rebound. Uptrend from 1.4281 is expected to resume at a later stage.

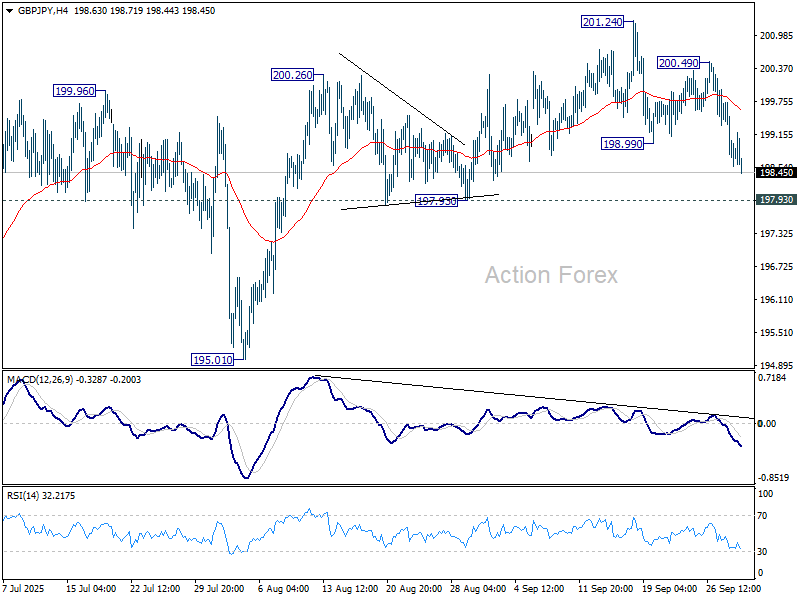

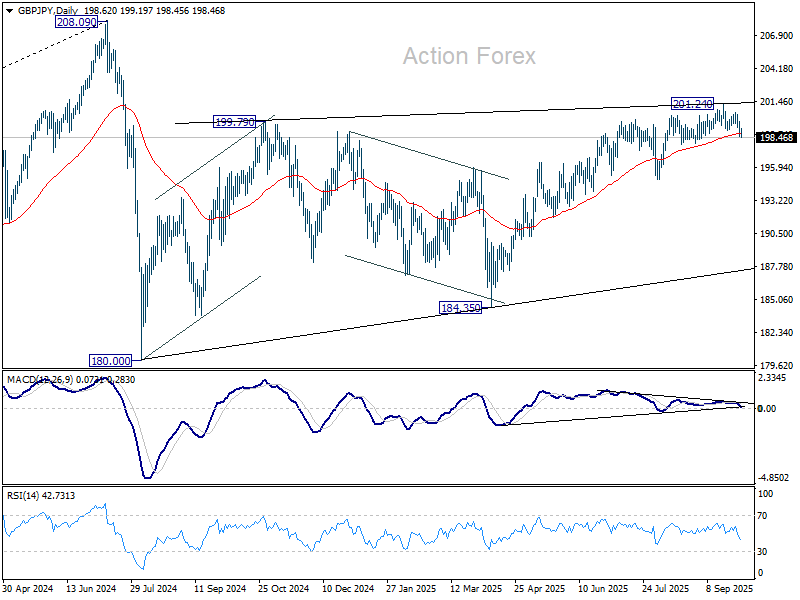

GBP/JPY Daily Outlook

Daily Pivots: (S1) 198.39; (P) 199.09; (R1) 199.59; More...

Intraday bias in GBP/JPY remains on the downside. Fall from 201.24 short term top should continue to 197.93 support. Firm break there will argue that whole rise from 184.35 has completed too and target 195.01 support next. For now, risk will stay on the downside as long as 200.49 support holds, in case of recovery.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a correction to rally from 123.94 (2020 low). The pattern might still extend with another falling leg. But in that case, strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. Meanwhile, decisive break of 208.09 will confirm long term up trend resumption.