Sample Category Title

Euro Spread Its Wings

No matter how strong the trend, corrections are inevitable. The EURUSD pullback was driven by the closing of speculative longs after the Fed cut the federal funds rate, the fall in US stock indices, and strong macroeconomic data. However, as soon as investors bought up the S&P 500 dip and Fed officials started talking about continuing the monetary policy easing, the euro spread its wings.

Jerome Powell and his colleagues are ready to rescue the cooling labour market and ignore accelerating inflation. As a result, the futures market gives a 91% probability of a cut in the fed funds rate in October and an 81% chance of another cut to 3.75% in December. Moreover, the derivatives estimate a 27% probability of a rate cut to 3.5% by the end of the year.

ECB Chief Economist Philip Lane said that the chances of inflation in the eurozone returning to low pre-pandemic levels are slim. The probability of it rising significantly above the 2% target is negligible. Such rhetoric suggests that the European Central Bank has ended its cycle of monetary policy easing.

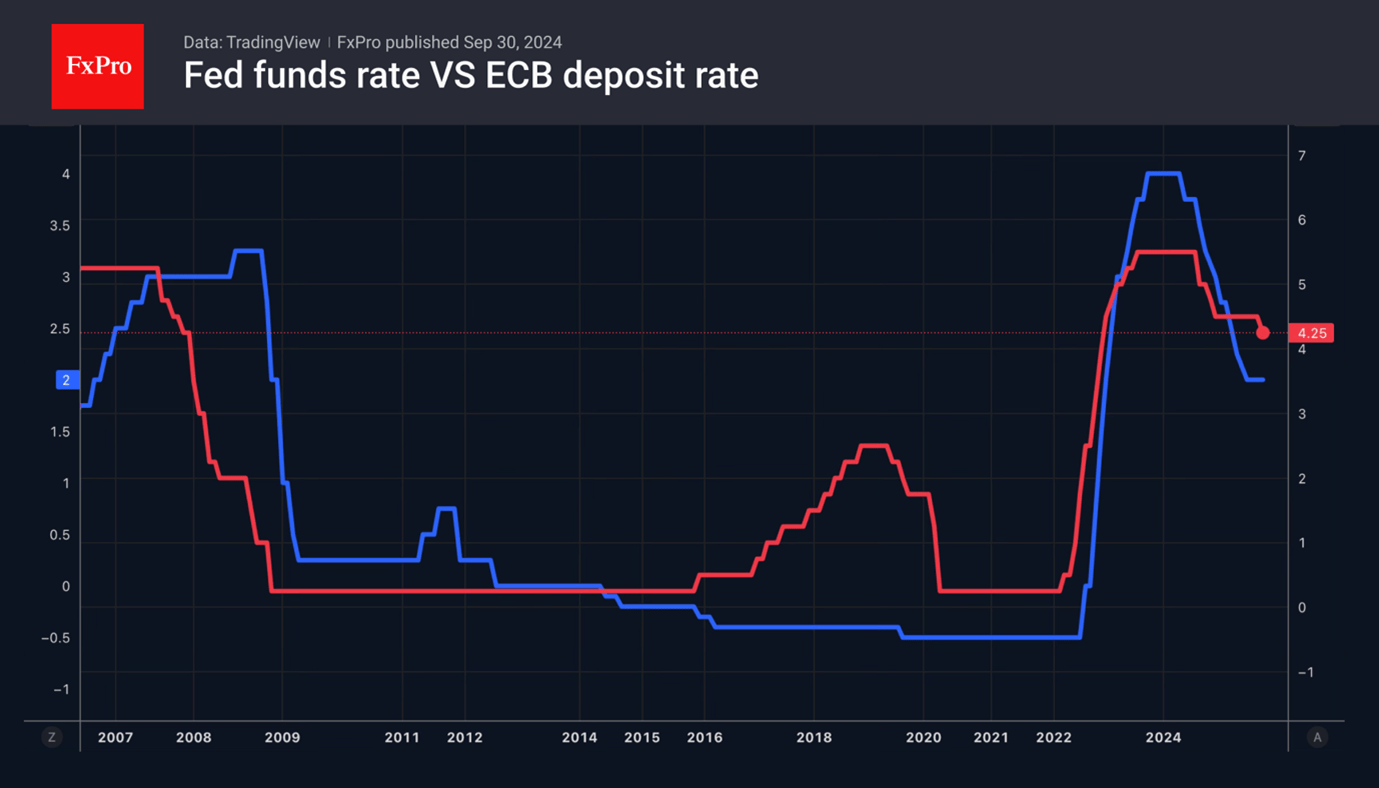

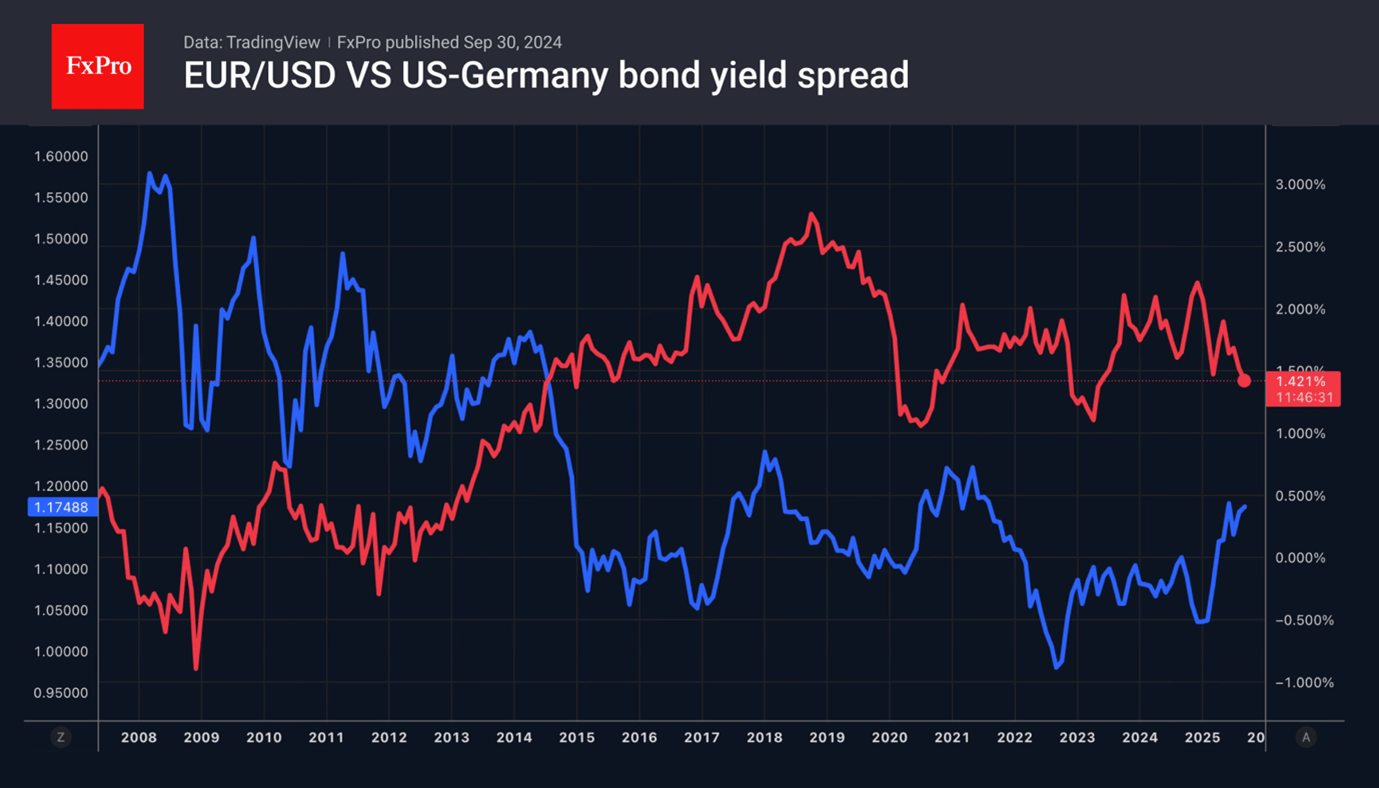

Thus, the rate differential between the ECB and the Fed will narrow, reducing the yield spread between US and German bonds. Historically, this has resulted in the euro rising against the dollar.

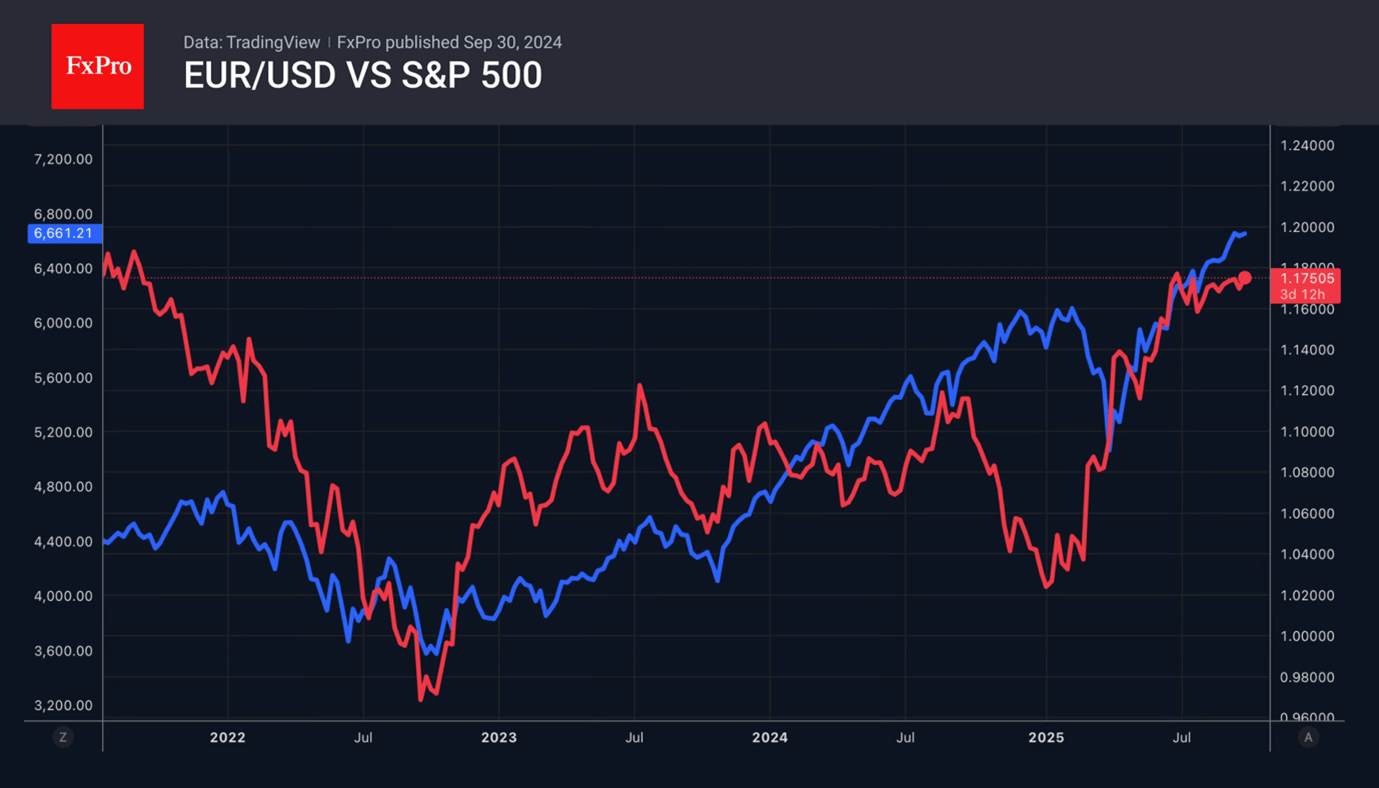

The rally in US stock indices is putting pressure on the USD. Foreign investors did not flee the US market after the White House introduced tariffs. They increased their stock holdings to $18 trillion, equivalent to 30% of the value of all US stocks. At the same time, non-residents are hedging currency risks by selling the dollar. As a result, a direct correlation between the euro and stock indices has become apparent.

As long as US stock indices continue to climb and the Fed lowers rates amid a cooling labour market, the chances of euro growth will increase. The main risks are a pleasant surprise from US employment in September and consolidation of the S&P 500 against the backdrop of seasonal volatility in October. A shutdown could be the reason for this.

Sunset Market Commentary

Markets

Today’s release of some national inflation figures points, if any, to slight upside risks for tomorrow’s euro area outcome. Consensus expects upward price pressures to intensify from 2% in August to 2.2% while the core measure should match last month’s 2.3%. Both being above the ECB’s 2% target validates the central bank’s steady-barring-shocks approach. As ECB’s VP de Guindos put it yesterday: “The ECB’s rates level at 2% is adequate under the current circumstances.” Going into the individual numbers, a French miss (1.1% y/y vs 1.3% expected, up from 0.8% in August) was offset by both Italy and Germany. Prices in the former country rose 1.8% vs a 1.7% consensus while German inflation quickened to 2.4% from 2.1%, to be compared to 2.2% analysts had penciled in. Germany’s statistical office referring to the national (non-harmonized) CPI showed that price gains in the services sector and a smaller drag coming from energy supported the inflation uptick. Goods inflation meanwhile intensified to 1.4%, an 18 month year high on par with December 2024. It barely made a dent in FX and FI markets. German rates fluctuated in a 2 bps trading range and currently trade flat on the day. The euro is similarly lacking inspiration. EUR/USD’s intraday swing amounts to half a big figure with the pair currently trading slightly higher than yesterday in the 1.174 area. JPY and AUD show some of the biggest moves, with the former benefiting from rising rate hike expectations and the latter on signs of a long(er) break in the easing cycle. US Treasuries outperform marginally with yields down around 2 bp across the curve. Stock markets are treading water.

The muted moves may be rooted in uncertainty going into a midnight (US time) deadline to prevent the US government from shutting down for the first time in seven years. House Speaker Johnson said he was skeptical on a last-minute deal, echoing Vice-President Vance yesterday. President Trump repeated his threat that a lot of employees would be sacked instead of being furloughed. If anything, it adds do the downside risks the labour market many at the Fed say is facing. Fed vice chair Jefferson was the latest to do so, though he added that it comes with upside risks to inflation. He sees disinflation to resume after this year and to return to 2% in the coming years. Jefferson supported this month’s 25 bps rate cut but refrained from making calls for the future. Fed Collins said she doesn’t expect the labour market to soften much further but sees some risk of a more meaningful unemployment increase. According to the Boston Fed president it may be appropriate to ease a bit further this year.

News & Views

The KOF Swiss economic institute’s economic barometer rebounded from a 23-month low (96.22) in August to 97.96 in September. The barometer remains below its medium-term average, continuing to paint a subdued picture for the Swiss economy. Separately, the Swiss National Bank announced that it sold CHF 5.1bn in the second quarter, its biggest interventions since Q4 2023 and the largest amount of selling since Q1 2022. Unwanted CHF-strength in the wake of US liberation day triggered the FX interventions. The data came a day after Switzerland and the US Treasury released a joint declaration in which they aligned views on FX matters. Both promised not to “target exchange rates for competitive purposes” but also recognised that such market interventions are a valid tool for addressing currency volatility or “disorderly” moves.

Polish inflation remained steady on a monthly basis for a second consecutive month in September. Preliminary details showed rising electricity, gas & other prices (+0.2% M/M) cancelling out lower prices for food & non-alcoholic drinks (-0.5% M/M) and for fuel (-0.4% M/M). In annual terms, price growth was also unchanged at 2.9% Y/Y. Compared with September of last year, fuel prices fell by 4.9% while prices for food & non-alcoholic drinks and for electricity, gas & other rose by respectively 4.2% and 2.4%. Detailed and final figures will be published on October 15 with the National Bank of Poland releasing its core inflation numbers the day after.

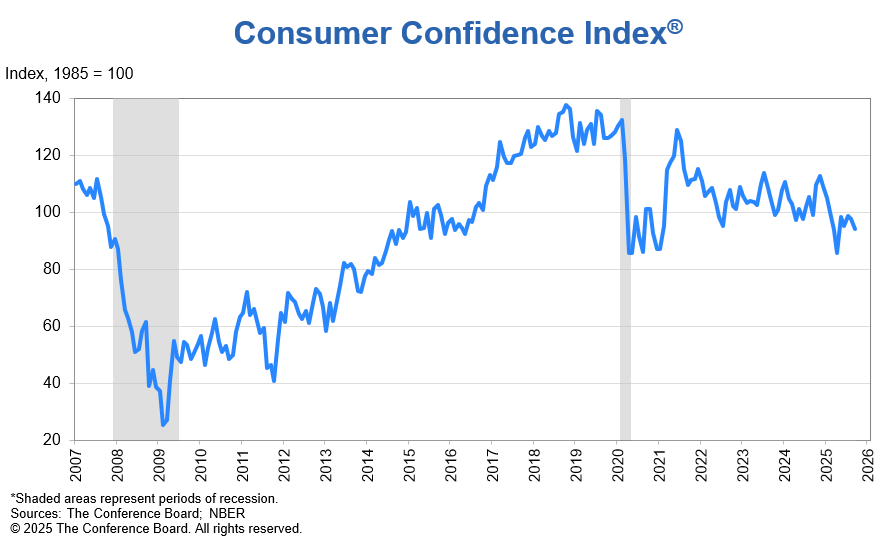

US consumer confidence weakens to 94.2, job views hit multi-year low

US consumer confidence fell in September, with Conference Board index slipping to 94.2 from 97.8, missing expectations of 95.9 and marking the weakest reading since April. Present Situation Index dropped -7 points to 125.4, its largest decline in a year. Expectations Index edged lower by -1.3 points to 73.4, remaining below the recession threshold of 80 for the eighth consecutive month.

According to Stephanie Guichard of the Conference Board, the present situation component registered its largest drop in a year, with consumers less positive on business conditions and increasingly cautious about job availability. She noted that the appraisal of current job openings has now declined for nine straight months to a multi-year low.

While consumers were somewhat more pessimistic on future jobs and business conditions, optimism over future incomes improved. That helped limit the drop in the Expectations Index, but overall sentiment points to lingering household caution heading into Q4.

Fed’s Collins says further easing may be appropriate this year

In a speech today, Boston Fed President Susan Collins acknowledged that the outlook is “highly uncertain." However, she acknowledged that inflation risks tied to the labor market have diminished. Thus, "the upside inflation risks I was concerned about a few months ago are more limited," she added.

Against this backdrop, Collins said she is open to more cuts if conditions justify them. “In this context, it may be appropriate to ease the policy rate a bit further this year – but the data will have to show that,” she cautioned.

Overall, She emphasized that policy should remain “modestly restrictive” to restore price stability while guarding against further labor market weakening.

Lagarde: ECB not facing classic policy trade-off

ECB President Christine Lagarde said in a speech today the central bank is “in a good place” as the inflation shock of recent years has largely faded in the Eurozone. She cited three additional reasons underpinning the current stance: trade shocks are "not creating new inflationary pressures", inflation risks are “quite contained in both directions,” and with policy rates at 2%, the ECB is "well placed" to respond if circumstances change.

Lagarde noted that the ECB is not facing the “classic policy trade-off” of slowing growth and rising inflation. Instead, risks appear balanced, allowing policymakers more space to focus on stabilizing the medium-term outlook.

Still, she cautioned that uncertainty persists. Companies are still adjusting to US tariffs by running down inventories and absorbing higher costs in margins, leaving the full impact on prices and growth unclear. She also acknowledged that in a world of shifting geopolitics, “unknown unknowns” will continue to shape the policy environment.

Lagarde emphaized that the ECB cannot pre-commit to any rate path, stressing the need to remain agile and data-dependent.

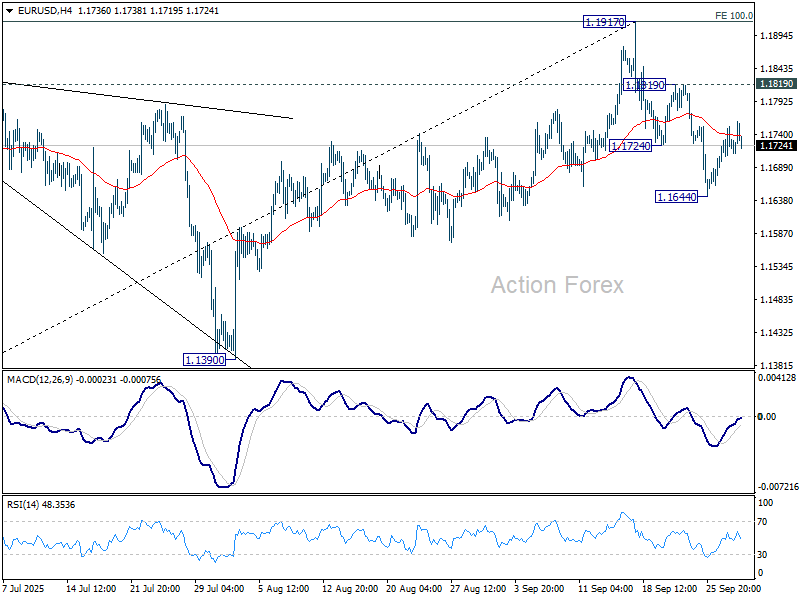

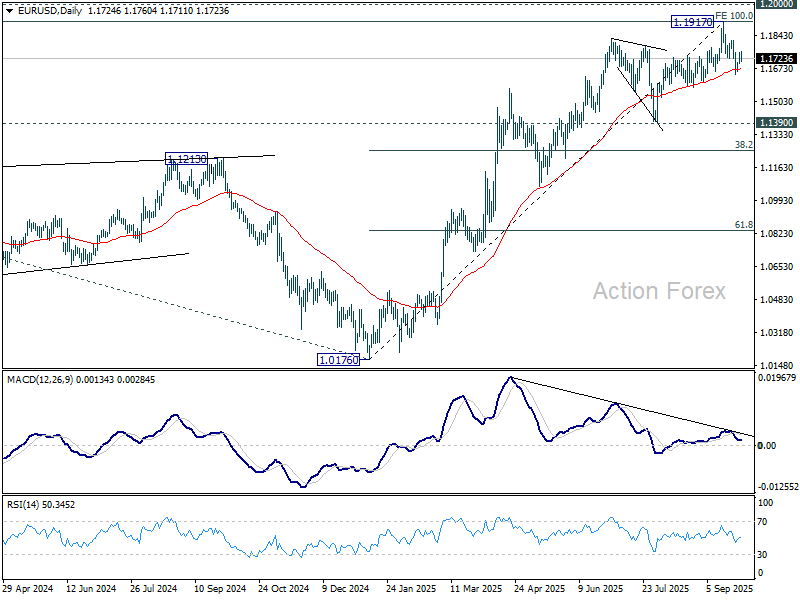

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1700; (P) 1.1728; (R1) 1.1754; More...

Intraday bias in EUR/USD stays neutral for the moment. Further fall is expected as long as 1.1819 resistance holds. Considering bearish divergence condition in D MACD, sustained trading below 55 D EMA (now at 1.1670) will argue that 1.1917 was already a medium term top. Deeper fall should then be seen to 1.1390 support next.

In the bigger picture, rise from 1.0176 (2025 low) is seen as the third leg of the pattern from 0.9534 (2022 low). 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916 was already met. For now, further rally will remain in favor as long as 1.1390 support holds, and firm break of 1.2000 psychological level will carry larger bullish implications. However, firm break of 1.1390 will suggest that rise from 1.0176 has already completed and bring deeper fall to 55 W EMA (now at 1.1231).

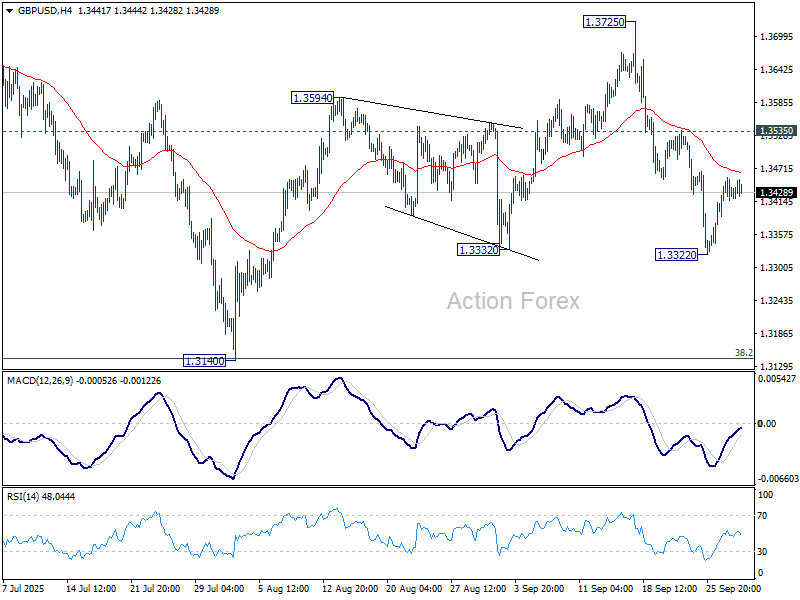

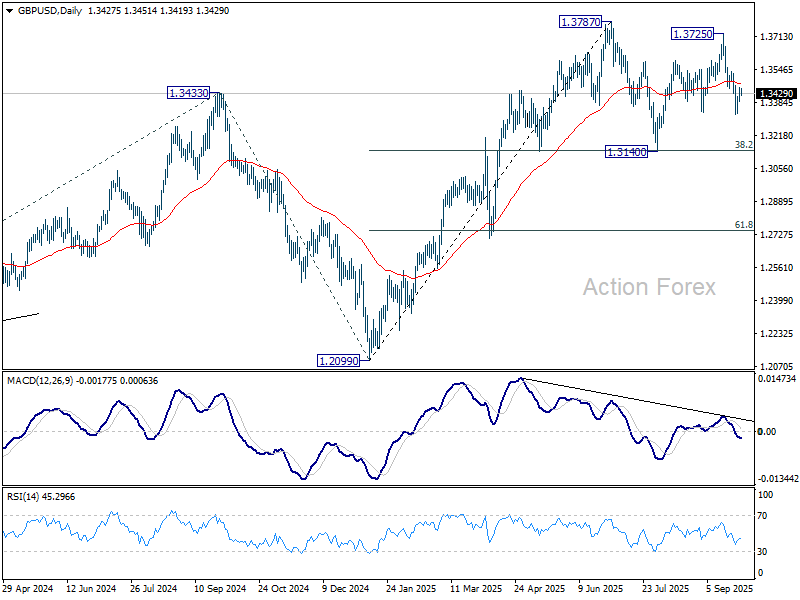

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3394; (P) 1.3426; (R1) 1.3458; More...

Intraday bias in GBP/USD remains neutral for the moment. Further decline is expected as long as 1.3535 resistance holds. Break of 1.3322 will resume the fall from 1.3725, as the third leg of the corrective pattern from 1.3787, and target 1.3140 support.

In the bigger picture, rise from 1.0351 (2022 low) is still seen as a corrective move. Further rally could be seen to 61.8% projection of 1.0351 to 1.3433 (2024 high) from 1.2099 (2025 low) at 1.4004. But strong resistance could be seen from 1.4248 (2021 high) to limit upside. Sustained break of 55 W EMA (now at 1.3155) will argue that a medium term top has already formed and bring deeper fall back to 1.2099.

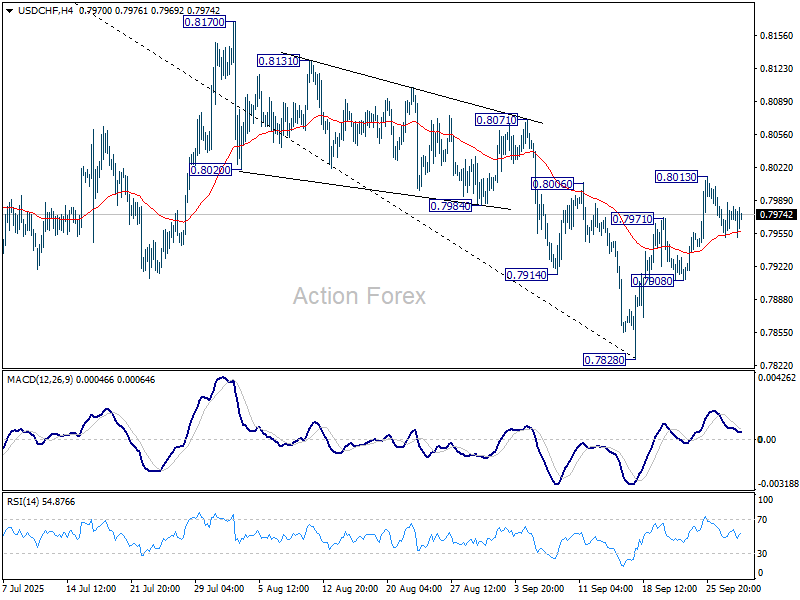

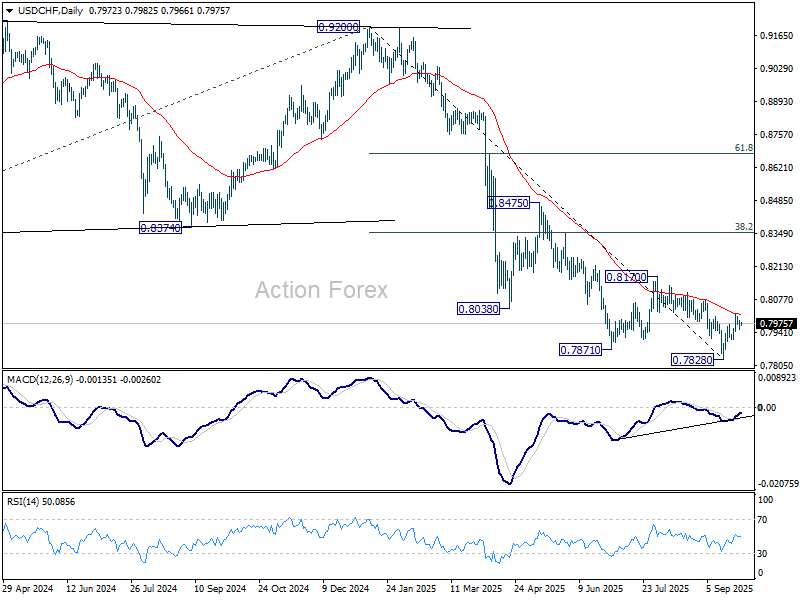

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7957; (P) 0.7972; (R1) 0.7993; More…

Intraday bias in USD/CHF remains neutral for the moment. On the upside, sustained trading above 55 D EMA (now at 0.8014) will suggest that rise from 0.7828 is already correcting whole fall from 0.9200. Further rise should the be seen to 0.8170 resistance and possibly above. However, break of 0.7908 will turn bias back to the downside for retesting 0.7828 low.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

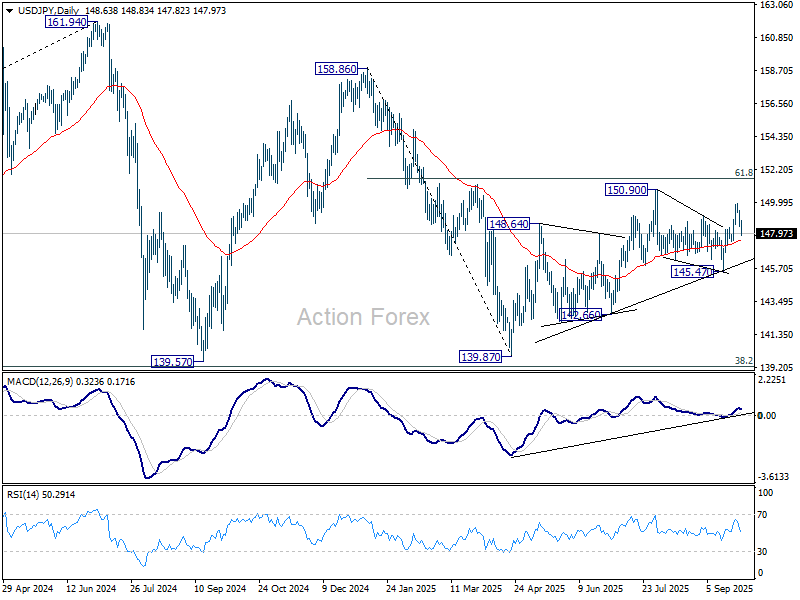

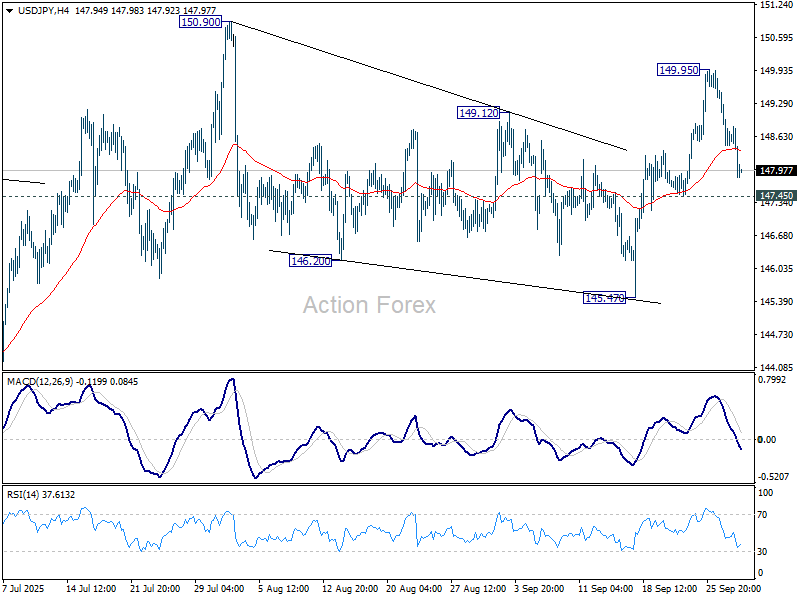

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 148.15; (P) 148.92; (R1) 149.37; More...

No change in USD/JPY's outlook and intraday bias stays neutral first. Further rally is expected as long as 147.45 support holds. Corrective pattern from 150.90 should have completed at 145.47. Above 149.95 will bring retest of 150.90 first. Firm break there will target 151.22 fibonacci level. However, sustained break of 147.45 will dampen this bullish view and bring deeper fall back to 145.47 support instead.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.