Sample Category Title

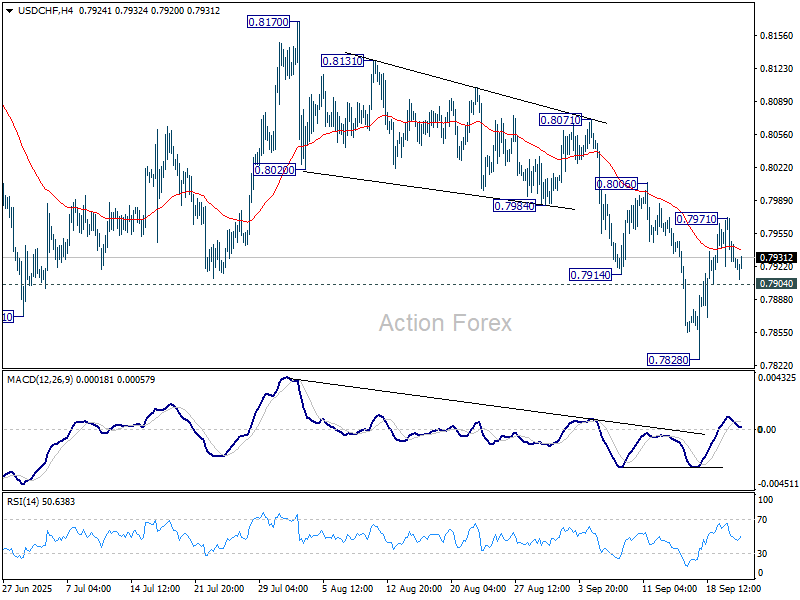

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7906; (P) 0.7940; (R1) 0.7958; More….

Intraday bias in USD/CHF is turned neutral first with current retreat. On the upside, above 0.7971 will resume the rebound from 0.7828 short term bottom to 0.8006 resistance. Firm break there will bring stronger rise back to 0.8170. On the downside though, below 0.7904 minor support will bring retest of 0.7828 low instead.

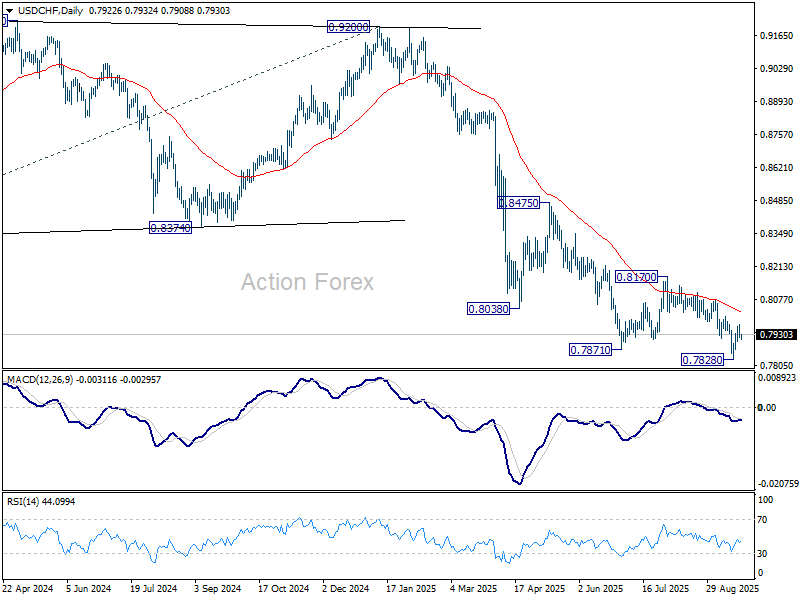

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

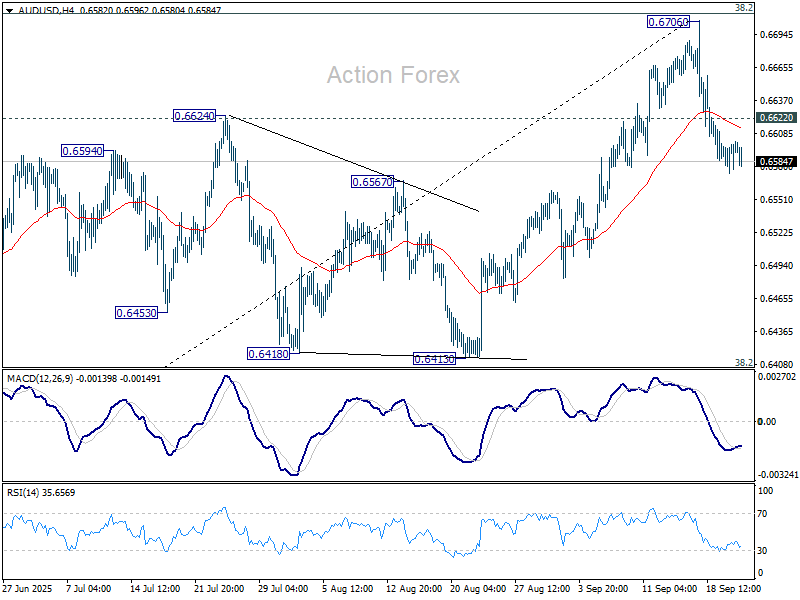

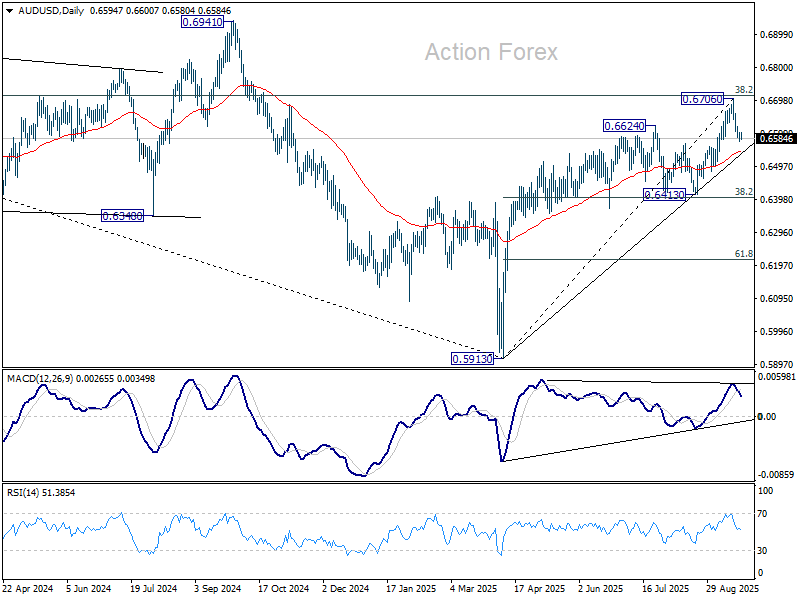

AUD/USD Daily Report

Daily Pivots: (S1) 0.6577; (P) 0.6598; (R1) 0.6622; More...

Intraday bias in AUD/USD remains on the downside as fall from 0.6705 short term top is in progress for 55 D EMA (now at 0.6540). Firm break there will target 0.6413 support. On the upside, though above 0.6622 minor resistance will bring retest of 0.6706 high.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. Outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, sustained break of 0.6713 will be a strong sign of bullish trend reversal, and path the way to 0.6941 structural resistance for confirmation.

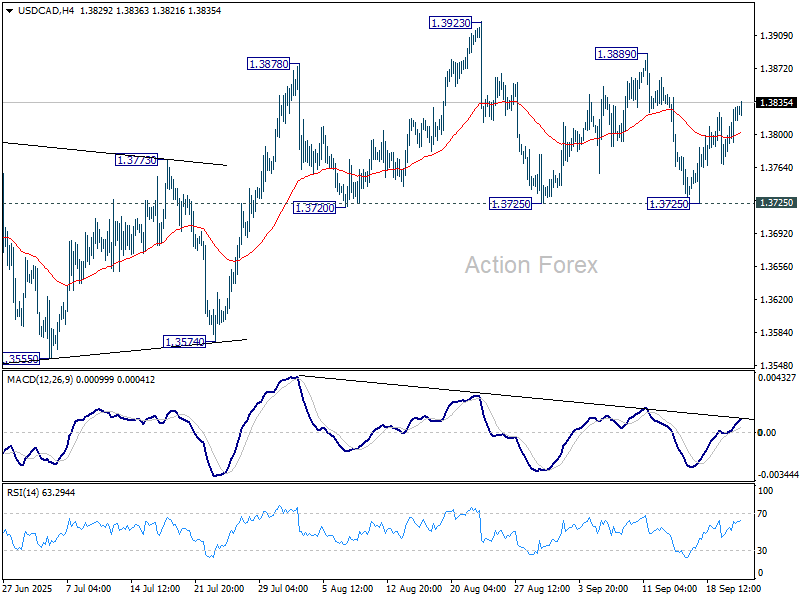

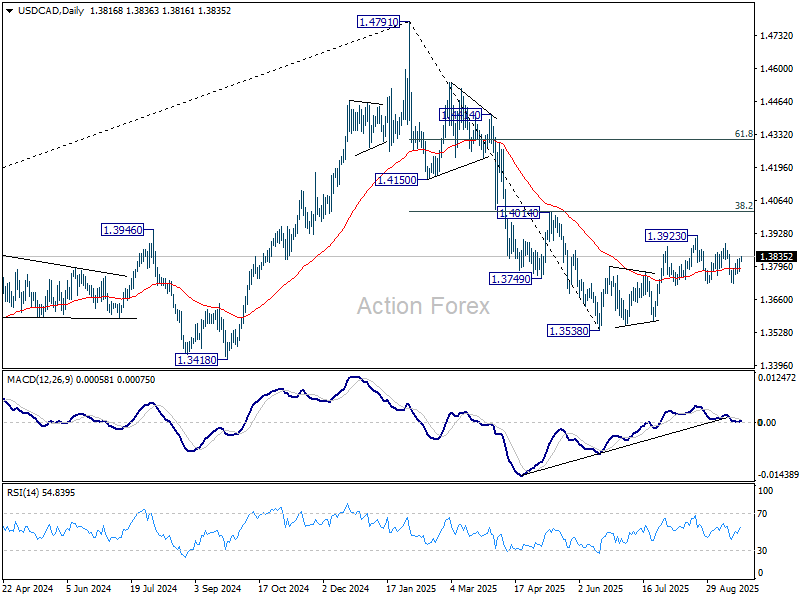

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3787; (P) 1.3810; (R1) 1.3840; More...

Range trading continues in USD/CAD and intraday bias stays neutral. On the upside, break of 1.3889 resistance will suggest that the corrective rebound from 1.3538 is resuming, and further rise should be seen through 1.3923 high towards 1.4014 cluster resistance. However, decisive break of 1.3725 will indicate that the corrective rebound has completed, and turn near term outlook bearish.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 cluster resistance (38.2% retracement of 1.4791 to 1.3538 at 1.4017) holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 (2025 high) at 1.3069.

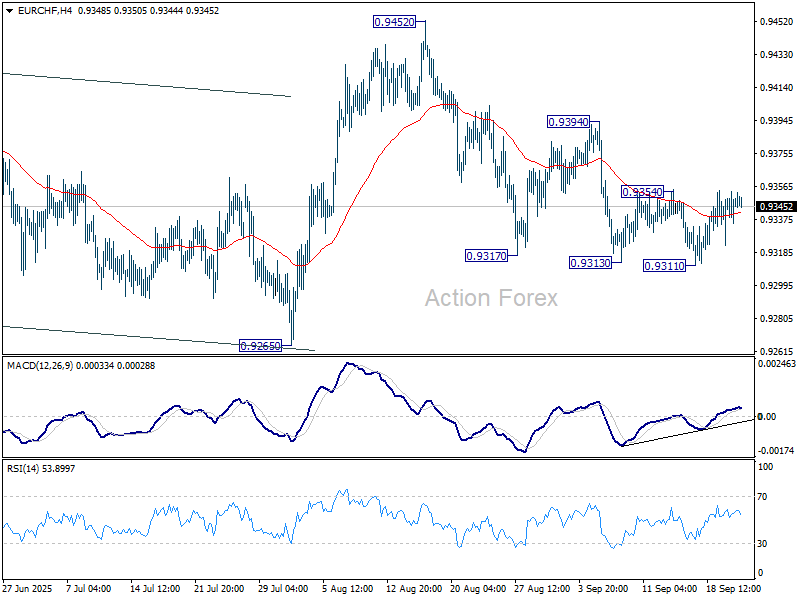

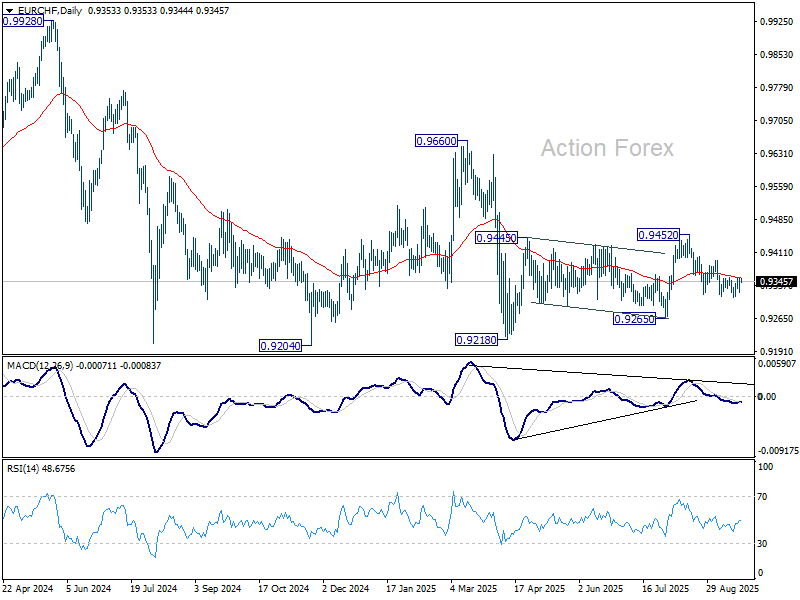

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9337; (P) 0.9346; (R1) 0.9362; More...

Sideway trading continues in EUR/CHF and intraday bias remains neutral. Considering bullish convergence condition in 4H MACD, firm break of 0.9354 resistance will confirm short term bottoming, and bring stronger rebound to 0.9394 resistance. On the downside, break of 0.9311 will resume the fall from 0.9452 to 0.9265 support.

In the bigger picture, the down trend from 0.9204 (2018 high) might still be in progress considering that EUR/CHF is staying well inside the long term falling channel. However, with bullish convergence condition in W MACD, downside potential should be limited in case of another fall. Instead, firm break of 0.9660 resistance will be an important sign of medium term bullish trend reversal.

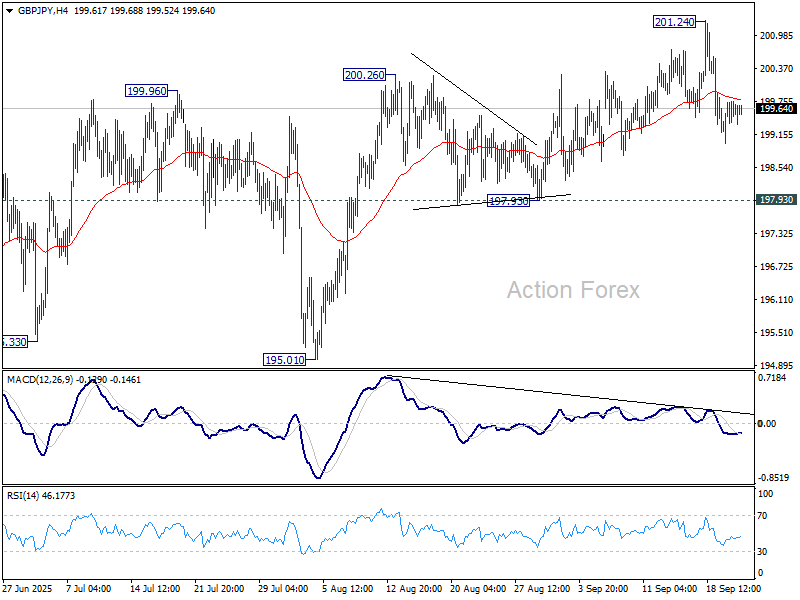

GBP/JPY Daily Outlook

Daily Pivots: (S1) 199.27; (P) 199.53; (R1) 199.89; More...

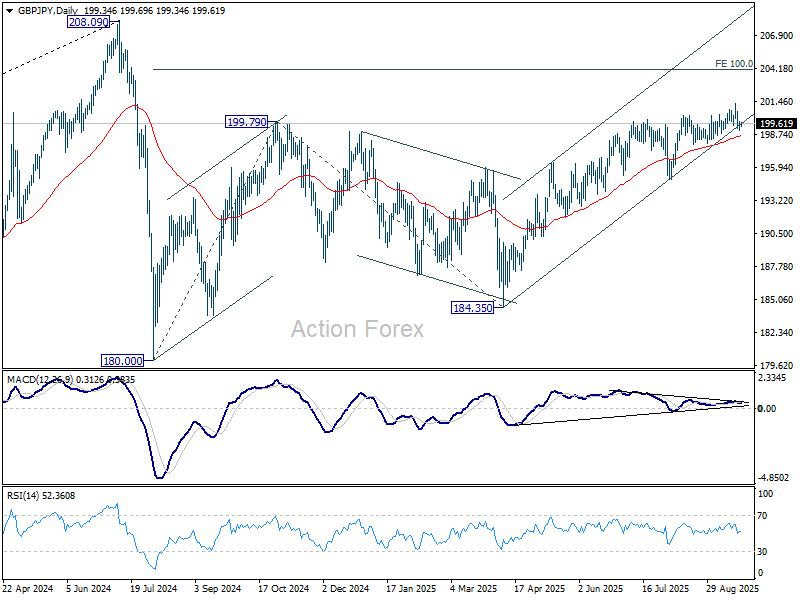

GBP/JPY is staying in consolidations below 201.24 and intraday bias remains neutral. Further rise is expected as long as 197.93 support holds. Firm break of 201.24 will target 100% projection of 180.00 to 199.79 from 184.35 at 204.14. However, considering bearish divergence condition in both D and 4H MACD, firm break of 197.93 will indicate bearish reversal and bring deeper fall back to 195.01 support first.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a correction to rally from 123.94 (2020 low). The pattern might still extend with another falling leg. But in that case, strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. Meanwhile, decisive break of 208.09 will confirm long term up trend resumption.

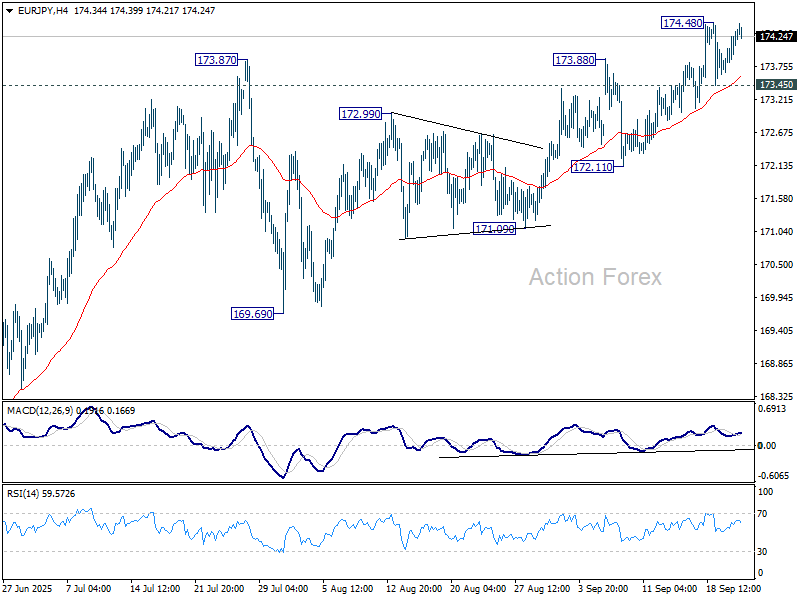

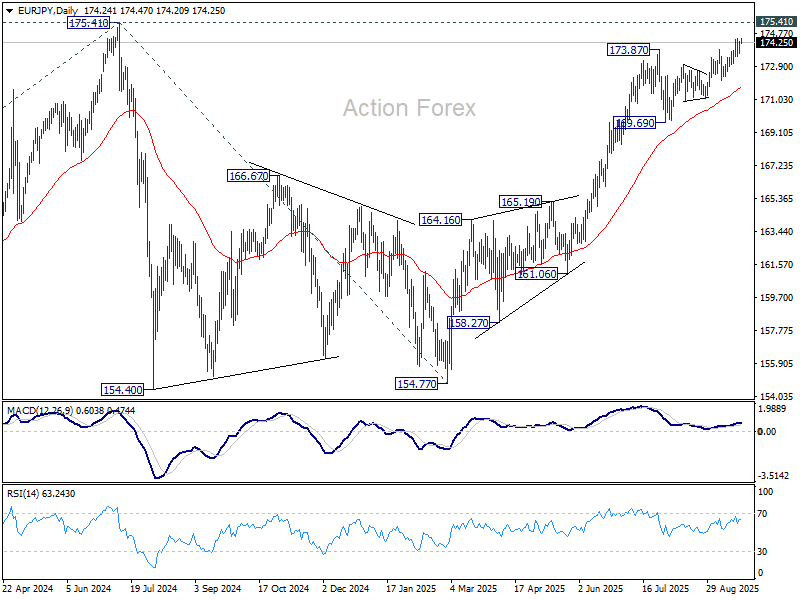

EUR/JPY Daily Outlook

Daily Pivots: (S1) 173.91; (P) 174.15; (R1) 174.61; More...

Intraday bias in EUR/JPY stays neutral and more consolidations could be seen. Further rise is expected as long as 173.45 minor support holds. Above 174.48 will target a retest on 175.41 high. However, firm break of 173.45 will turn bias back to the downside for deeper pullback to 172.11 support instead.

In the bigger picture, current rally from 154.77 is still tentatively seen as resuming the larger up trend. Firm break of 175.41 (2024 high) will confirm and target 61.8% projection of 124.37 (2022 low) to 175.41 from 154.77 (2025 low) at 186.31. However, sustained break of 169.69 support will delay this bullish case, and probably extend the correction from 175.41 with another fall.

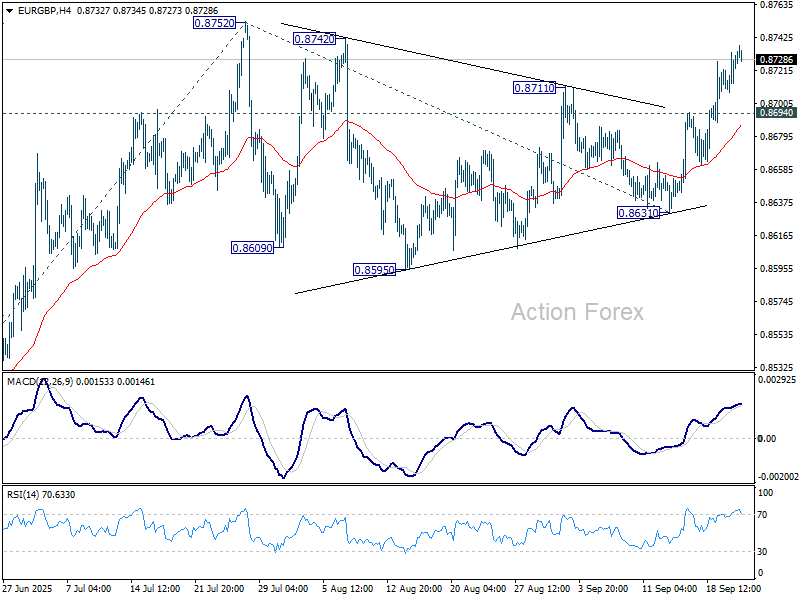

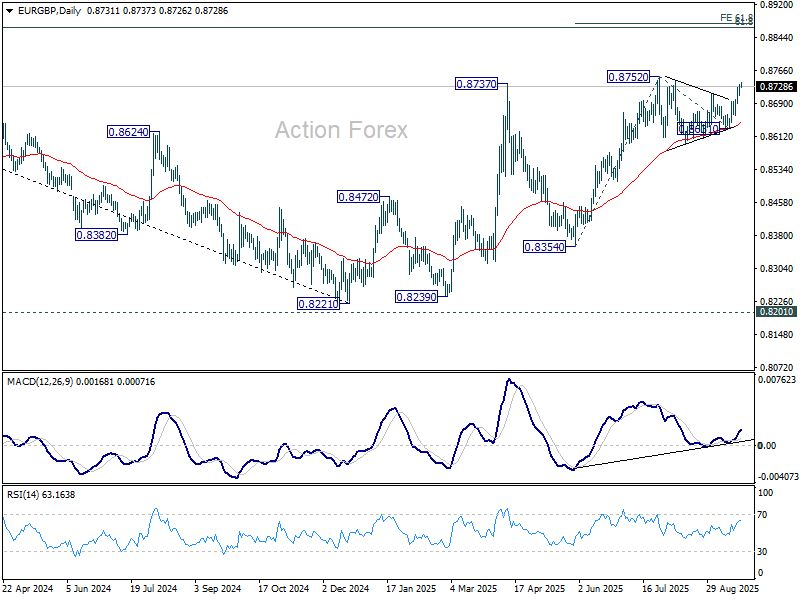

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8717; (P) 0.8726; (R1) 0.8743; More...

EUR/GBP's rally from 0.8631 is in progress and intraday bias stays on the upside for retesting 0.8752. Firm break there will resume larger rally to 61.8% projection of 0.8354 to 0.8752 from 0.8631 at 0.8877, which is close to 0.8867 fibonacci level. On the downside, though, below 0.8694 minor support will turn bias neutral first.

In the bigger picture, the structure from 0.8221 medium term bottom are not impulsive enough to suggest that it's reversing the down trend from 0.9267 (2022 high). But even if it's a correction, further rise could still be seen to 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Nevertheless, sustained trading below 55 W EMA (now at 0.8518) will argue that the pattern has completed and bring retest of 0.8221 low.

Holy Nvidia

Every time you think the AI rally has topped out, it finds another gear. Yesterday was one of those days... Nvidia surged nearly 4% to a fresh ATH after reports that it will deepen its partnership with OpenAI to build massive new data centers and AI infrastructure. We’re talking about a capacity of around 10 gigawatts – roughly the output of 10 large nuclear reactors – it is HUGE. So basically, OpenAI will need to buy an enormous amount of Nvidia chips to make this happen, and Nvidia is making sure it has a seat at the table. It’s a genius move. It will not only help them sell more chips to one of the world’s most famous – if not the most famous – AI chatbot makers, but it also ties them closer to OpenAI’s future. Investors loved the idea. Nvidia rallied nearly 4% and hit a fresh ATH on the news – and proved again that the company constantly finds ways to cooperate, integrate, navigate political and geopolitical jungles with grace and make its way through. Holy Nvidia. It is now worth nearly $4.5 trillion.

Anyway, Oracle did even better yesterday – with a more than 6% rally – on news that they will rebuild and secure the new US version of TikTok’s algorithm.

As such, the technology rally led the major US indices to fresh ATHs yesterday. The S&P 500 extended gains while the Nasdaq 100 is less than 250 points away from the 25K psychological mark. Yet the non-tech names look a bit less cheery – with the equal-weighted version of the S&P 500 trading flat, and European carmakers tanking as Porsche and VW cut their outlook for the year.

In the bond space, the US 2-year yield rebounded past 3.60% even after Trump-linked economist Stephen Miran – now in the headlines for his push for lower rates – argued that the neutral rate is much lower than current levels and that he would cut rates by 150bp very quickly to get there. He even added that such a move wouldn’t be “panic,” while a 75bp cut would be. The kind of comments that are so far-stretched they can’t be taken seriously enough to shift market expectations. Proof? The 2-year didn’t budge – on the contrary, it went higher. That’s a sign that lowering rates wouldn’t necessarily bring down long-term borrowing costs if the size and the speed of easing aren’t warranted. Because lower rates also boost inflation expectations and limit room for further cuts down the road. So Miran is in, and he will be pushing for cuts. The White House is too. But the reality is that the Fed can’t hand out rate cuts like candy at a party. The economic data – growth, jobs and inflation – will matter for market pricing.

Good news is that many Federal Reserve (Fed) members are convinced that the weakening jobs market should be addressed – but carefully, by keeping inflation in mind. And good news is that US core inflation – the Fed’s favourite gauge – is expected to have eased in August. If that’s the case, dovish Fed expectations will continue to weigh enough to keep equity traders on the back of a bull, and the US dollar under pressure. The EURUSD is timidly testing the 1.18 offers, while Cable is flirting with the 1.35 resistance after holding near its 50-DMA yesterday.

Today, investors will have an eye on early PMI data for September. Encouraging eurozone numbers could cement the expectation that the European Central Bank (ECB) won’t need to deliver another cut this year and help euro bulls gain ground, while weak UK numbers could confirm slower activity and fuel worries ahead of the next budget announcement – not expected to be a sweet moment for taxpayers. Fundamentally, the euro benefits from relatively stronger conditions than sterling or the dollar. Therefore, the bullish move in EURGBP is backed by diverging outlooks. For EURUSD and Cable, it’s trickier. The divergence between more hawkish ECB/Bank of England (BoE) vs the Fed is already largely priced in. The long-term outlook for the dollar remains bearish as the US exceptionalism trade wanes. But in the short run, a minor USD rebound is still possible, fueled by yields reminding traders: hey, rates won’t come down that fast.

Interestingly, yesterday’s tech-led rally couldn’t save crypto. Bitcoin lost more than 2% and slipped below its 100-DMA, while altcoins took a heavier hit – Ethereum fell more than 5% and Solana slid over 6%.

Gold, on the other hand, extended its rally to a fresh ATH near $2,600 per ounce, on tense geopolitical risks in Ukraine and Gaza. For Gaza, an increasing number of developed nations are recognizing the state of Palestine, straining relations with Israel and the US – the latest being France. In Europe, meanwhile, countries close to Russia’s border worry that Moscow is testing NATO’s nerves with repeated airspace violations. Surprisingly, oil bulls remain muted despite the rising geopolitical risks. US crude is testing the $62pb support regardless of tensions, hinting that the bears could gain the upper hand and push the price of a barrel to $60/62pb range – and potentially below.

Eyes on EA, UK, and US PMIs

In focus today

Focus turns to the highly important September flash PMI indicator for the euro area (EA), the UK, and the US. For the EA, manufacturing has continued to improve lately while the services sector has softened. We expect this development to have continued in September with EA manufacturing PMIs rising slightly to 50.9, while services are likely to have declined marginally to 50.2. Following better-than-expected growth in the first half of the year, we expect the EA economy to be close to stagnant in the second half of the year with 0.1% q/q growth in both Q3 and Q4. This is in line with PMIs just marginally above the 50-mark.

In Sweden, the Riksbank is set to announce its rate decision. We expect an unchanged policy rate at 2.00%, but that they keep the door open for further easing, aligning with our expectations of a 25bp rate cut to 1.75% in November.

Economic and market news

What happened overnight

France, Luxembourg, Malta, Belgium, and Monaco officially recognised Palestine as a state during a high-level UN event in New York. This adds to the growing list of countries advocating for a two-state solution amidst the ongoing Gaza conflict, despite strong objections from Israel and the US.

What happened yesterday

In the US, White House officials announced progress on the deal to divest TikTok's US operations from its Chinese owner, ByteDance, which will retain less than 20% ownership. The new entity will include investors such as Oracle and Silver Lake, with Oracle managing all US user data on domestic cloud infrastructure. President Trump is expected to certify the deal with an executive order, granting a 120-day enforcement pause to finalise the agreement. While US officials are confident China has approved the deal, Beijing has yet to confirm its position.

A US federal judge ruled in favour of Ørsted, allowing the USD 5bn Revolution Wind project off Rhode Island to resume after a month-long halt ordered by the Trump administration. The court called the halt "arbitrary and capricious," boosting Ørsted's US shares by nearly 9%.

US Treasury Secretary Scott Bessent announced plans for "large and forceful" support for Argentina, including options like swap lines and currency purchases. Actions will follow today's meeting between President Trump and Argentina's President Milei.

Trump's new USD 100,000 H-1B visa fee drew backlash from the tech industry, with critics warning it could hurt start-ups, reduce talent inflow, and weaken US productivity. Some executives, however, praised the focus on high-value roles, while others predicted firms may shift hiring abroad.

In the euro area, consumer confidence rose as expected in September to -14.9 (cons: -15.0) from -15.5. The weak consumer confidence should dampen growth in private consumption, but we do still expect a gradual normalisation in confidence due to real income gains and lower borrowing costs. These factors should also contribute to a modest rise in private consumption the coming year.

In Denmark, consumer confidence continued its decline to -18.7 (prior: -17.2), driven by concerns over personal finances and food price increases despite overall inflation being under control. This contrasts with positive economic indicators like job growth, rising wages, and a strong housing market.

In geopolitics, Russian President Putin proposed a one-year extension of the New START treaty, which limits US and Russian nuclear arsenals, citing global non-proliferation interests. The offer, conditional on US reciprocity, comes amid heightened tensions over Ukraine and as the treaty's expiration in February 2026 approaches.

Equities: US equities were slightly higher on the day, while non-US equities were mixed during a session with little new data. The S&P500 rose 0.4%, while Nasdaq was up 0.7%. European indices were marginally lower at around -0.3%. European consumer confidence was slightly higher than in previous months but remains gloomy, especially in a historical context, as it has yet to recover from the 2022 inflation fallout. That said, the employment expectations were slightly higher in August relative to July, thus pointing to lower unemployment rates.

FI and FX: The US Treasury curve continues its modest selloff with yields edging slightly higher ahead of tonight's speech by Jerome Powell and Friday's important PCE data. EUR/USD found support at 1.1730 and is now back close to 1.18. Small moves with G10 FX overnight, though. Today, the Scandi market is all about Riksbank's rate decision and communication where the money market is pricing in 9bp of cuts. We expect them to stay on hold, which should lend some temporary support to the SEK.

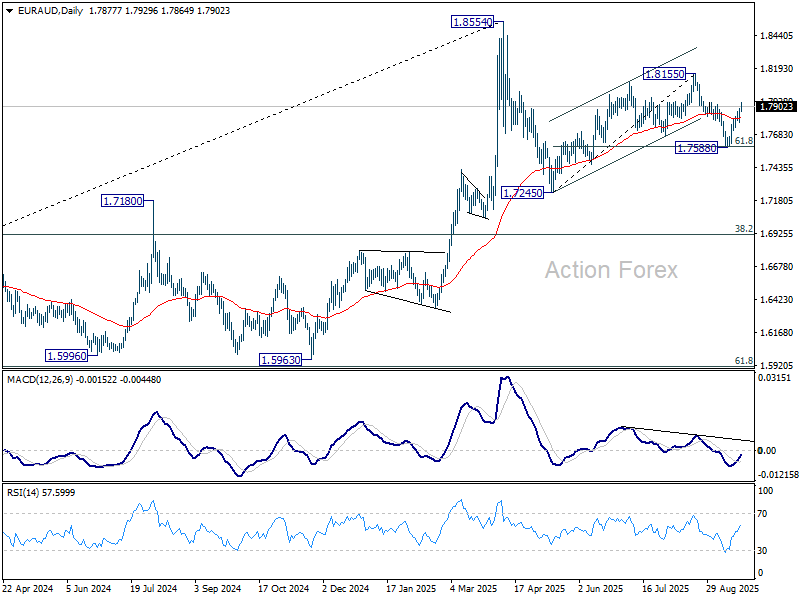

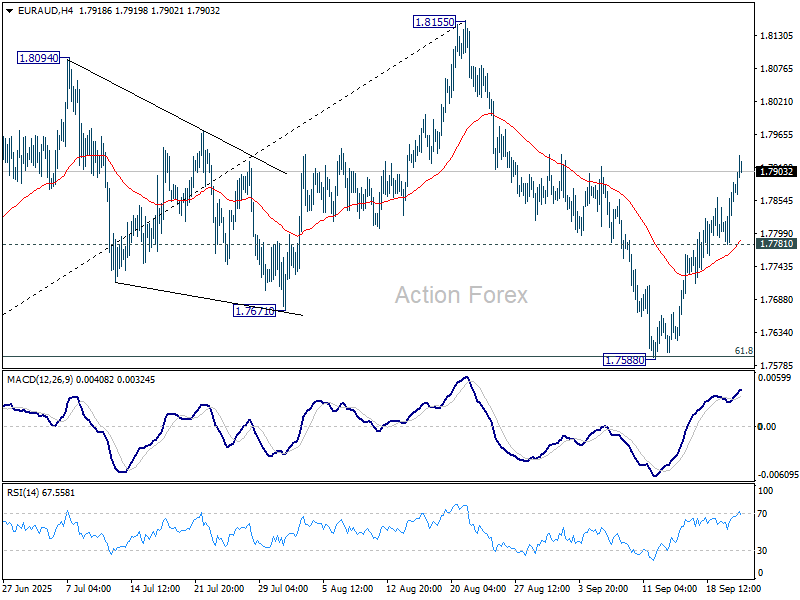

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7812; (P) 1.7850; (R1) 1.7916; More...

EUR/AUD's rally from 1.7588 continues today and intraday bias stays on the upside. Further rally should be seen to retest 1.8155 resistance next. Firm break there will resume the whole rise from 1.7245. On the downside, below 1.7781 minor support will turn intraday bias neutral first.

In the bigger picture, price actions from 1.8554 medium term top are seen as a corrective pattern. Deeper fall could be seen as the pattern extends, but downside should be contained by 38.2% retracement of 1.4281 (2022 low) to 1.8554 at 1.6922 to bring rebound. Uptrend from 1.4281 is expected to resume at a later stage.