Sample Category Title

Trump-Putin Talks Falter Ahead of Zelenskiy’s Visit to the White House

In focus this week

Today, following the Trump-Putin meeting in Alaska, Ukrainian President Zelenskiy is set to meet US President Trump in the White House alongside a group of European leaders including EU commission president von der Leyen.

In the euro area, we look for final July inflation data on Wednesday, the PMI report for August on Thursday and the negotiated wages indicator released by the ECB on Friday. We will closely monitor the negotiated wages indicator, as declining domestic inflation is the biggest downside risk to our call of ECB holding rates steady for the rest of the year.

Across the Atlantic, the Fed is set to take headlines throughout the week, as the minutes of the FOMC's July meeting are released Wednesday evening. Then on Thursday and Friday the Fed's Jackson Hole Symposium will take place. This year's theme is "Labor Markets in Transition: Demographics, Productivity, and Macroeconomic Policy". The main focus of markets will be on Fed Chair Powell's speech on Friday afternoon. On the macro data front, August flash PMIs are due for release Thursday.

Economic and market news

What happened over the weekend

In the US, July retail sales came in strong at +0.5% (cons: +0.5%), while the June numbers were revised up from +0.6% to +0.9%. Control group sales, the 'core' group, came in at +0.5% m/m with solid sales reported among most sectors. While employment growth has slowed over the past months, solid wage growth continues to fuel consumption in the US. Meanwhile, US July industrial production grew -0.1% (cons: 0.0%) in July, while the June growth was revised up to +0.4% from +0.3%.

University of Michigan consumer 1-year inflation expectations rose to 4.9% (preliminary) in August from 4.5% in July. Inflation expectations declined from May to July, but the new tariffs appear to have caused renewed concerns in early August. Worries about inflation also fed into a weaker consumer sentiment which declined to 58.6 from 61.7 in July.

In Alaska, US President Trump and Russian President Putin met to discuss the war in Ukraine. The talks ended earlier than expected and were unsuccessful in making any imminent progress towards a ceasefire. Steven Witkoff, Trump's special envoy to the Middle East, said that Putin agreed that the US could provide security guarantees to Ukraine as part of a deal, which would, though, also likely require territorial concessions. Following the meetings, Trump decided to hold back on further sanctions against Russia as well as 'secondary tariffs' on countries buying Russian energy such as India and China.

Equities: Equities ended last week on a soft note, but the broader picture remains another week of gains. Under the surface, cyclicals underperformed defensives, but the real story was sector rotation - particularly a strong comeback in healthcare. We have highlighted the sector several times recently, and last week investors finally rotated back in: healthcare gained nearly 4% in Europe and more than 5% in the US, outperforming staples by 4% in relative terms. This was not a broad defensive theme, but a clear rotation story, partly reflecting easing tariff fears and the sector's prior underperformance. In the US on Friday, Dow +0.1%, S&P 500 -0.3%, Nasdaq -0.4% and Russell 2000 -0.6%. Asian equities are higher this morning, and futures in both Europe and the US are marginally in the green.

FI and FX: Risk sentiment soured through Friday's session as markets awaited the outcome of the Putin-Trump Alaska summit. Rates moved higher across regions with the solid US retail sales data and rising consumer inflation expectations adding to the move. Long-end bonds suffered the most with 30Y yields in Germany and France reaching their highest levels since 2011. EUR/USD drifted higher towards 1.17 on Friday as the USD broadly weakened, ending the week down around 0.4%. EUR/SEK and EUR/NOK rose as market sentiment worsened. Overnight, Asian stocks are trading modestly higher as focus turns towards the Trump-Zelensky meeting.

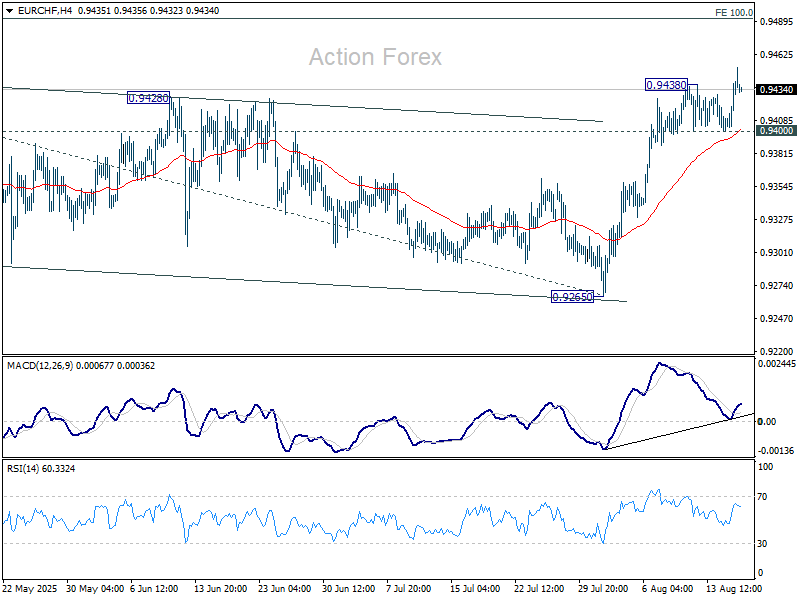

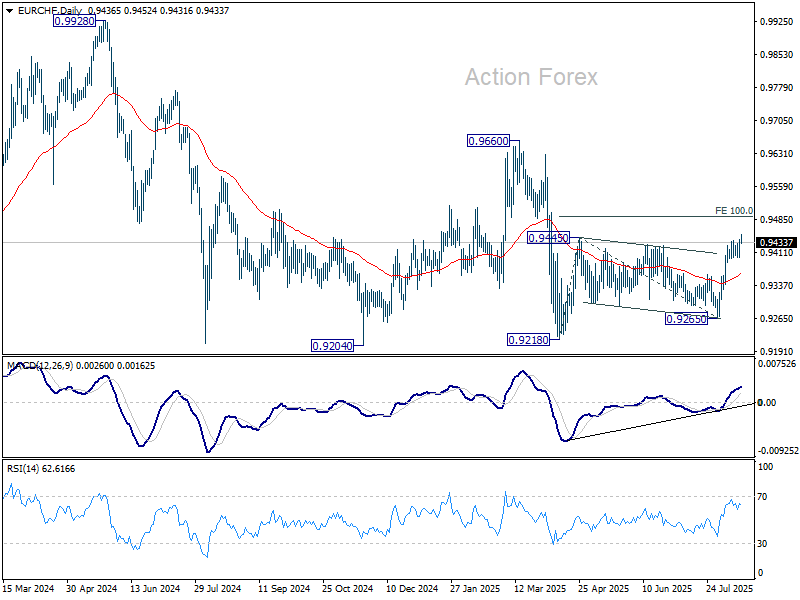

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9417; (P) 0.9431; (R1) 0.9457; More....

EUR/CHF's rally resumed by breaking 0.9438 temporary top and intraday bias is back on the upside. Rise from 0.9218 should target 100% projection of 0.9218 to 0.9445 from 0.9265 at 0.9492. For now, further rise is expected as long as 0.9400 support holds, in case of retreat.

In the bigger picture, the down trend from 0.9204 (2018 high) might still be in progress considering that EUR/CHF is staying well inside the long term falling channel. However, with bullish convergence condition in W MACD, downside potential should be limited in case of another fall. Instead, firm break of 0.9660 resistance will be an important sign of medium term bullish trend reversal.

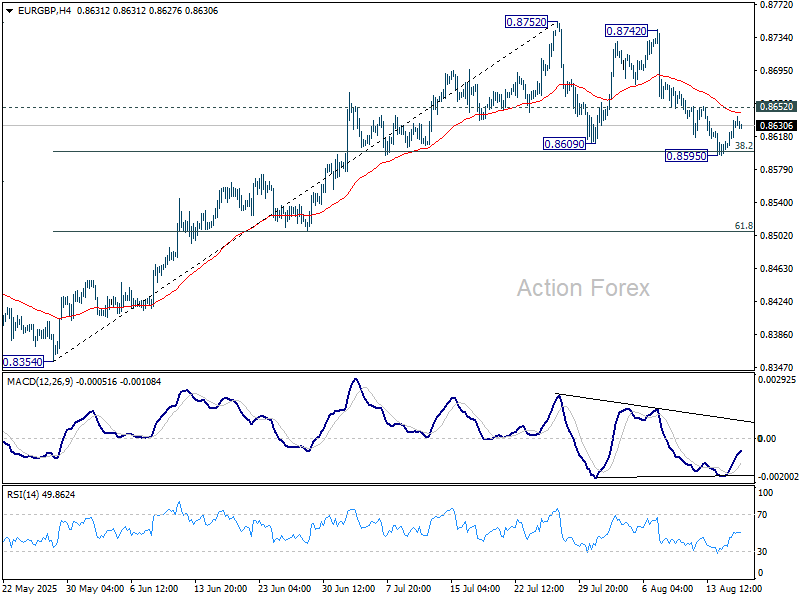

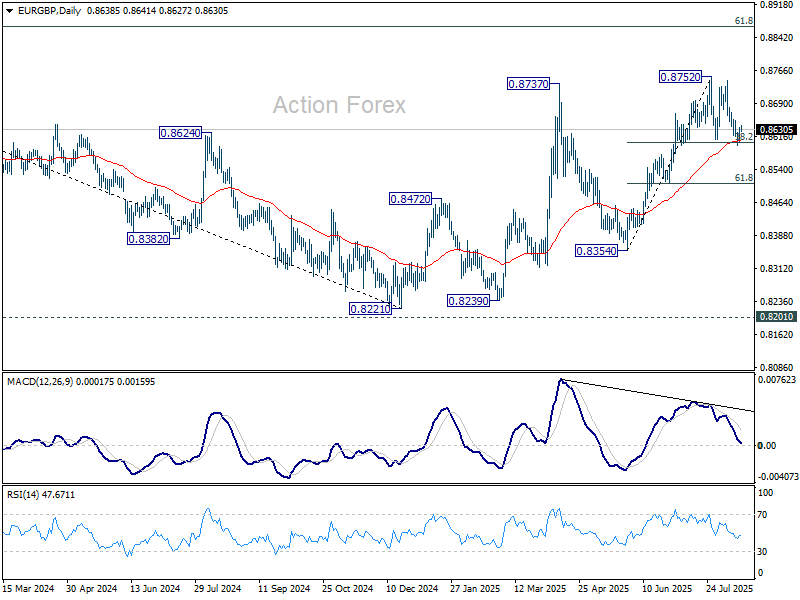

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8614; (P) 0.8626; (R1) 0.8648; More...

Intraday bias in EUR/GBP remains neutral for the moment. On the upside, break of 0.8652 will suggest that the corrective pattern from 0.8752 has completed after drawing support from 38.2% retracement of 0.8354 to 0.8752 at 0.8600, and retain near term bullishness. Intraday bias will be back on the upside for retesting 0.8752 high next. However, sustained break of 0.8600 will indicate near term bearish reversal and target 61.8% retracement at 0.8506.

In the bigger picture, the structure from 0.8221 medium term bottom are not impulsive enough to suggest that it's reversing the down trend from 0.9267 (2022 high). But even if it's a correction, further rise is expected to 61.8% retracement of 0.9267 to 0.8221 at 0.8867. This will remain the favored case as long as 55 W EMA (now at 0.8501) holds.

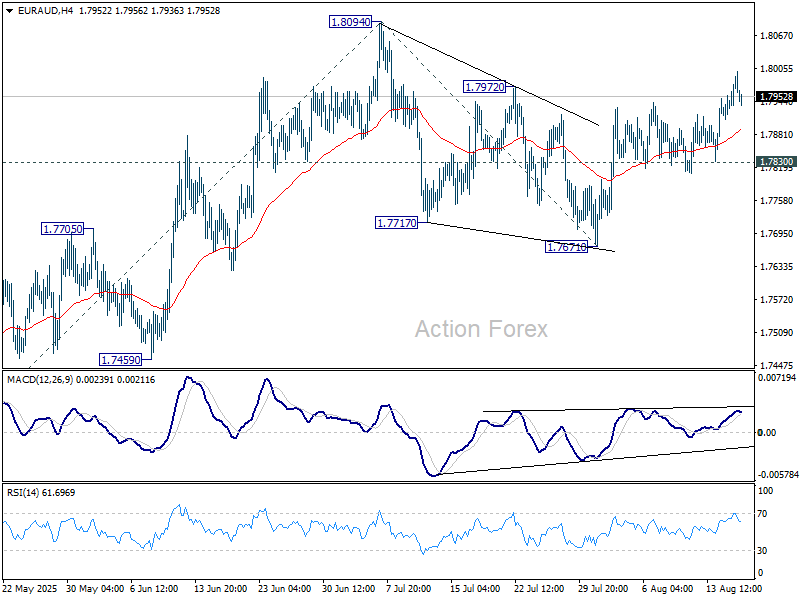

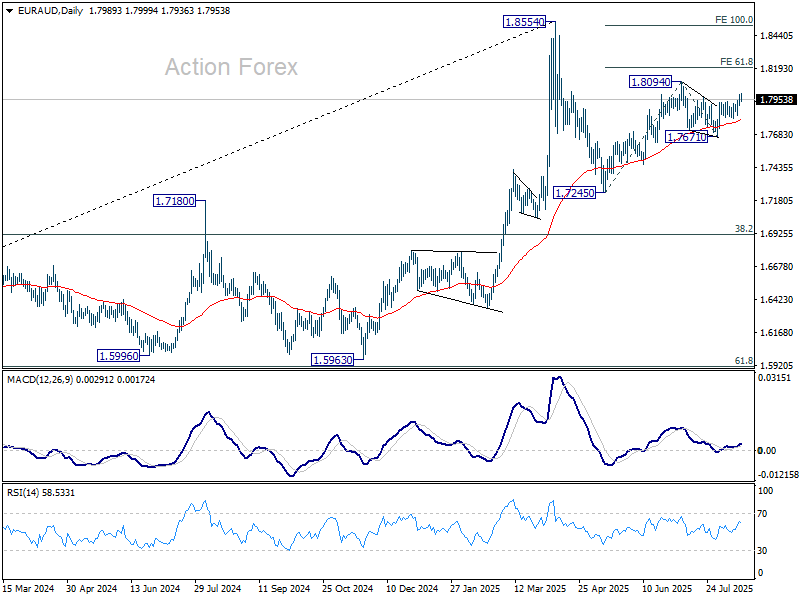

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7934; (P) 1.7963; (R1) 1.8017; More...

Intraday bias in EUR/AUD stays mildly on the upside for the moment. Correction from 1.8094 should have completed with three waves down to 1.7671. Further rally should be seen to 1.8094 first. Break there will resume the rally from 1.7245 to 61.8% projection of 1.7245 to 1.8094 from 1.7671 at 1.8196. This will now remain the favored case as long as 1.7830 support holds.

In the bigger picture, price actions from 1.8554 medium term top are seen as a corrective pattern. Such pattern could extend further with another falling leg. But even in that case, downside should be contained by 38.2% retracement of 1.4281 (2022 low) to 1.8554 at 1.6922 to bring rebound. Uptrend from 1.4281 is expected to resume at a later stage.

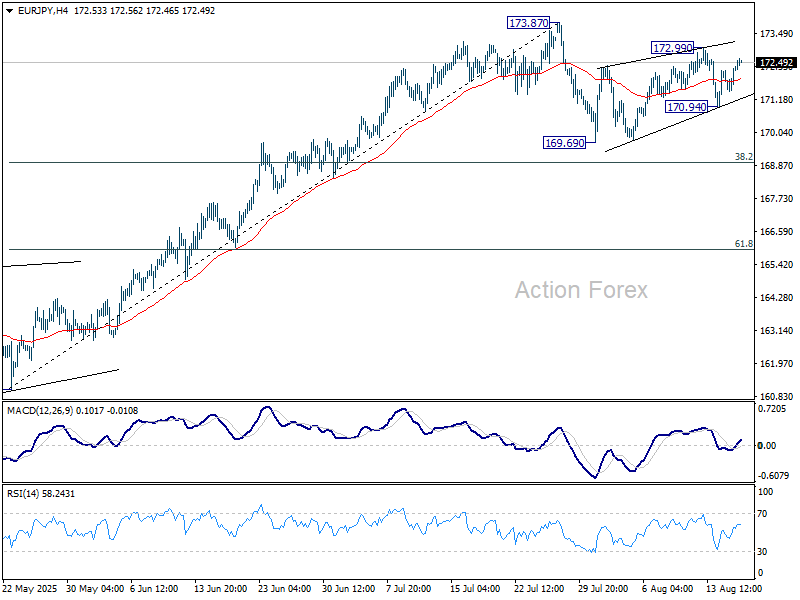

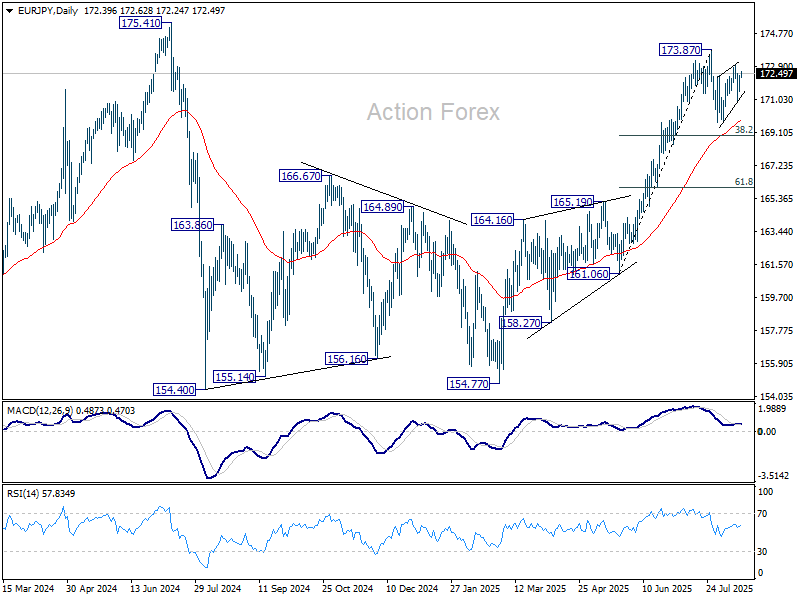

EUR/JPY Daily Outlook

Daily Pivots: (S1) 171.72; (P) 172.05; (R1) 172.59; More...

Intraday bias in EUR/JPY remains neutral for the moment. Corrective pattern from 173.87 is still extending, and break of 170.94 will bring deeper fall to 169.69 support. But downside should be contained by 38.2% retracement of 161.06 to 173.87 at 168.97 to bring rebound. On the upside, above 172.99 will bring retest of 173.87.

In the bigger picture, considering current strong momentum as seen in the rally from 154.77, corrective pattern from 175.41 could have already completed. Decisive break of 154.77 will confirm long term up trend resumption. Next target is 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. However, rejection by 175.41, followed by firm break of 55 D EMA (now at 169.87) will delay this bullish case.

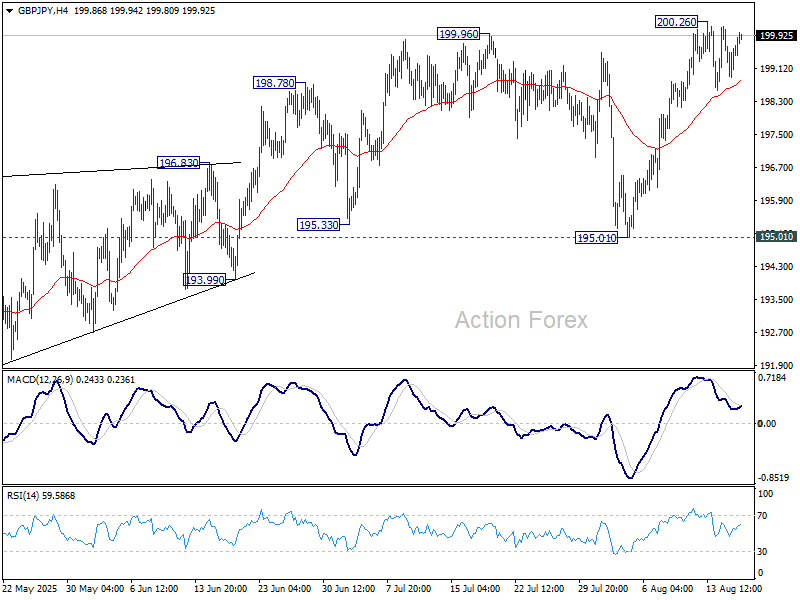

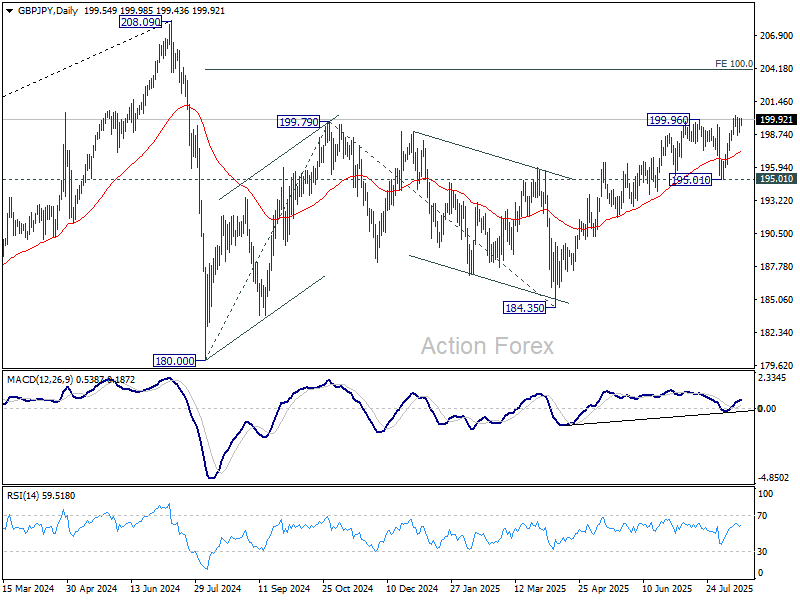

GBP/JPY Daily Outlook

Daily Pivots: (S1) 198.92; (P) 199.57; (R1) 200.23; More...

GBP/JPY recovers today but stays below 200.26 resistance and intraday bias remains neutral. Some more consolidations could be seen, but in case of another fall, downside should be contained well above 195.01 support. On the upside, firm break of 200.26 will resume the whole rise from 184.35 to 100% projection of 180.00 to 199.79 from 184.35 at 204.14.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a correction to rally from 123.94 (2020 low). The pattern might still extend with another falling leg. But in that case, strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. Meanwhile, decisive break of 208.09 will confirm long term up trend resumption.

Nikkei Soars, Yen Struggles Ahead of Packed Global Week With Jackson Hole Symposium

Asian markets opened the week on a positive note, with Japan’s Nikkei 225 extending its rally to fresh record highs. The interplay between Nikkei and Yen remains crucial. A softer yen improves exporters’ competitiveness, lifting equities. At the same time, robust equity performance can in turn weigh on the currency as investors channel funds into riskier assets. The feedback loop is evident again today, with Yen sliding broadly.

In the currency markets, Yen leads losses, followed by Dollar and Euro. On the flip side, Kiwi, Aussie and Loonie are outperforming, reflecting demand for higher-beta plays in a risk-on environment. Sterling and Swiss Franc sit in the middle of the pack.

With the economic calendar light today, some attention is turning to geopolitics. US President Donald Trump’s meeting with Ukrainian President Volodymyr Zelenskiy and European leaders will be closely followed. The talks come after Trump’s summit with Russian President Vladimir Putin last Friday, which Trump called “productive” despite yielding no breakthrough.

Before European leaders join the broader conversation, Trump and Zelenskiy are due to meet one-on-one. European capitals are keen to help Zelenskiy avoid another public confrontation like the one in February, when Trump and Vice President JD Vance criticized him in the Oval Office.

To bolster Zelenskiy’s position, German Chancellor Friedrich Merz, French President Emmanuel Macron, and UK Prime Minister Keir Starmer convened allies on Sunday. Their aim is to secure stronger security guarantees for Ukraine, ideally with the US playing a central role.

Beyond geopolitics, the macro calendar is heavy later this week. Markets will parse Canada CPI on Tuesday, RBNZ, UK CPI, and FOMC minutes on Wednesday, global PMIs on Thursday, and Japan CPI on Friday. All of this culminates with the Jackson Hole Symposium from Thursday to Saturday, where Fed officials’ comments will set the tone for September policy expectations.

In Asia, at the time of writing, Nikkei is up 0.87%. Hong Kong HSI is up 0.67%. China Shanghai SSE is up 1.24%. Singapore Strait Times is down -0.84%. Japan 10-year JGB yield is up 0.013 at 1.579.

NZ BNZ services uptick to 48.9, contraction persists

New Zealand’s BusinessNZ Performance of Services Index improved slightly in July, rising from 47.6 to 48.9. But the sector remained in contraction for the sixth consecutive month. Also, the latest reading is still well below the long-run survey average of 52.9.

Details showed mixed conditions. Activity/Sales stayed in contraction at 47.5, and New Orders stalled at 50.0. On the positive side, Inventories expanded for the second month at 51.4. Employment component slid to 47.1, extending its losing streak to 20 months.

Business sentiment, while slightly less negative, continued to reflect difficult conditions. Around 58.5% of comments were pessimistic, down from 66.2% in June. Firms pointed to declining sales, reduced spending, and persistent cost-of-living pressures. Inflation, high interest rates, weather disruptions, staffing shortages, and global uncertainty all weighed on confidence.

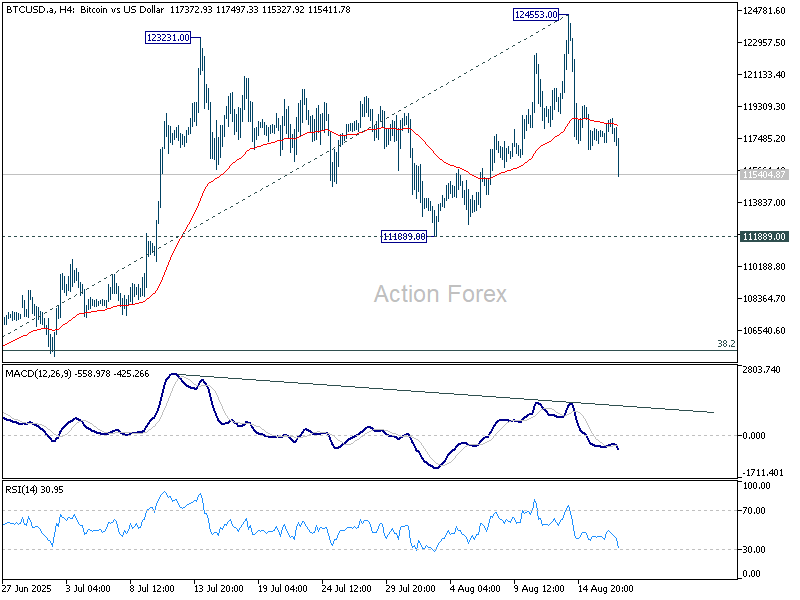

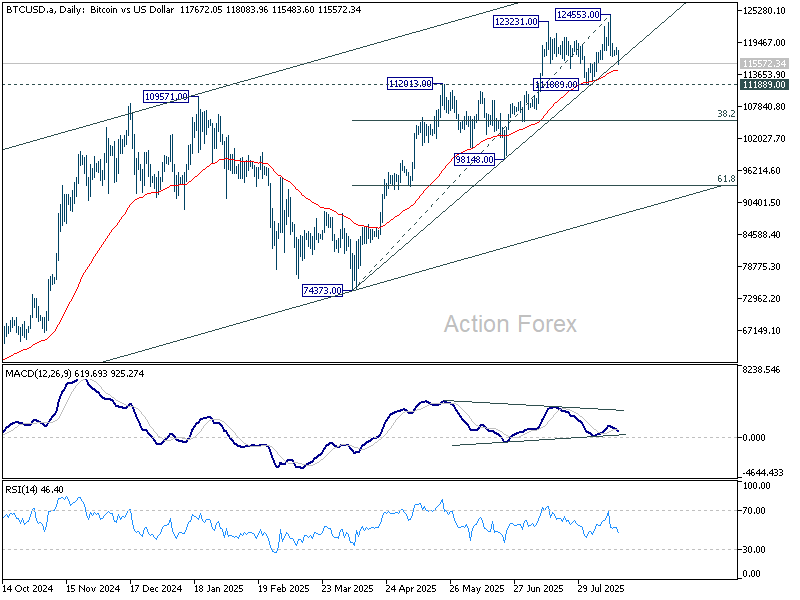

Key 112K level in focus as Bitcoin reverses from record

Bitcoin’s near-term outlook now hinges on whether 112,000 zone can hold as support after last week’s brief breakout to a record 124,553. The sharp reversal has shifted attention to this key level, with selling pressure still visible as the new week begins.

The current decline was triggered by U.S. Treasury Secretary Scott Bessent, who unsettled markets by revealing government Bitcoin reserves were worth only USD 15–20 billion, far below estimates. He added that Washington would not buy new Bitcoin for its strategic reserve, instead relying on confiscated assets to build holdings.

While he later clarified on X that Treasury remained open to “budget-neutral pathways” to expand reserves, confidence took a hit. Investors interpreted the comments as a sign Washington is unlikely to bolster demand in the near term.

Combined with stretched technicals, the backdrop encouraged traders to lock in profits, ending Bitcoin’s latest rally attempt prematurely.

Technically, momentum is fading. Bearish divergences in both the daily and 4-hour MACD highlight loss of upside strength. While another test of the highs cannot be ruled out, gains above 124,553 appear constrained.

Instead, focus has shifted to the 111,889 structural support. Decisive break there would confirm correction of the rally from 74,373, opening the door for a pullback to 38.2% retracement of 74,373 to 124,553 at 105,384.

That could set the stage for either prolonged consolidation or a deeper pullback before any fresh bullish leg.

Jackson Hole to test Fed’s September cut resolve; RBNZ cut as last?

The coming week is dominated by the Jackson Hole Economic Policy Symposium on August 21–23, which traditionally serves as the Fed’s most important policy forum outside of formal FOMC meetings. This year, markets are focused less on abstract long-term themes and more on whether Fed officials drop any clues about the likelihood of a rate cut at the September 16-17 meeting.

For now, the Fed still has two critical data points in hand before that decision — August CPI and the next Nonfarm Payrolls report. That gives officials room to remain cautious. Some may argue it is too early to commit, but their tone at Jackson Hole will be parsed carefully for signs of whether the committee is leaning toward action if those reports come in broadly in line with expectations.

The balance of voices will matter. Doves like Christopher Waller and Michelle Bowman dissented at the July meeting in favor of an immediate cut, suggesting internal debate is more intense than usual. The minutes of that meeting, due earlier in the week, will shed light on the arguments for and against moving sooner. Traders will be keen to see whether more members are quietly sympathetic to the dovish camp.

Chair Jerome Powell’s Friday speech is the highlight of Jackson Hole. But investors have learned not to expect Powell to deviate much from his hallmark cautious, even-handed style. He sees himself more as a moderator of the FOMC rather than its chief ideological driver, and is unlikely to give away a firm commitment. Still, even subtle phrasing shifts could tilt expectations on whether the Fed is preparing to cut as soon as September.

Beyond the Fed, markets also turn to New Zealand, where the RBNZ rate decision will be closely watched. A Reuters poll showed 28 of 30 economists expect a 25bps cut to 3.00%, with only two calling for a hold. Inflation has slowed to 2.7% in Q2, inside the bank’s 1–3% target, while unemployment rose to 5.2%, the highest since 2020. These conditions give the RBNZ reason to ease policy further.

The debate is now about where the easing cycle ends. Of 29 economists forecasting year-end levels, half see rates steady at 3.00%, half at 2.75%, with one outlier expecting no further cuts. Local banks are also split: ASB and Westpac think the RBNZ pauses after this week, BNZ sees a path to 2.75%, while ANZ and Kiwibank expect easing down to 2.50% next year. Markets will weigh not just the cut, but also how Governor Christian Hawkesby frames the road ahead.

In the UK, attention will turn to CPI and retail sales after last week’s strong Q2 GDP print reinforced Sterling’s outperformance. With inflation still elevated, the BoE’s cautious approach to cutting rates is unlikely to change, and fresh data could give the Pound another leg higher if it confirms persistent price pressures.

Elsewhere, CPI from Japan, CPI and retail sales from Canada, and global PMI readings will round out the week’s calendar.

Here are some highlights for the week:

- Monday: New Zealand BNZ services; Japan tertiary industry index; Eurozone trade balance; Canada housing starts; US NAHB Housing.

- Tuesday: New Zealand PPI; Australia Westpac consumer sentiment; Canada CPI; US new residential construction.

- Wednesday: Japan trade balance, machine orders; China rate decision; RBNZ rate decision; Germanny PPI; UK CPI; Eurozone CPI final; US FOMC minutes.

- Thursday: New Zealand trade balance; Australia PMIs; Japan PMIs; Swiss Trade balance; Eurozone PMIs; UK PMIs; Canada IPPI and RMPI; US jobless claims, Philly Fed survey, PMIs, existing home sales.

- Friday: UK Gfk consumer sentiment; Japan CPI; Germany GDP final; UK retail sales; Canada retail sales.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 198.92; (P) 199.57; (R1) 200.23; More...

GBP/JPY recovers today but stays below 200.26 resistance and intraday bias remains neutral. Some more consolidations could be seen, but in case of another fall, downside should be contained well above 195.01 support. On the upside, firm break of 200.26 will resume the whole rise from 184.35 to 100% projection of 180.00 to 199.79 from 184.35 at 204.14.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a correction to rally from 123.94 (2020 low). The pattern might still extend with another falling leg. But in that case, strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. Meanwhile, decisive break of 208.09 will confirm long term up trend resumption.

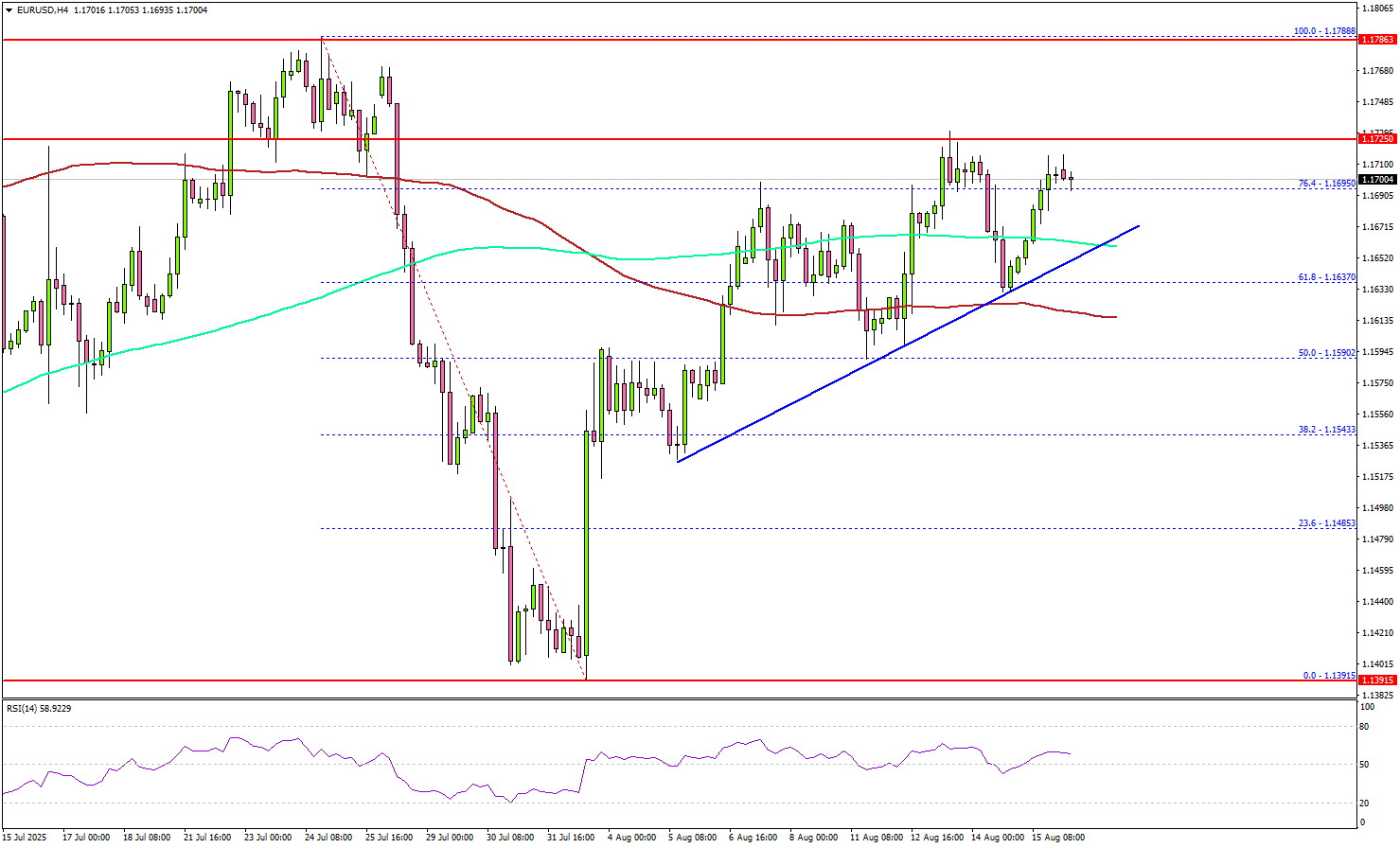

EUR/USD Maintains Strength as Buyers Target Another Strong Move

Key Highlights

- EUR/USD started a fresh increase above the 1.1620 resistance.

- A major bullish trend line is forming with support at 1.1665 on the 4-hour chart.

- GBP/USD rallied and tested the 1.3590 resistance zone.

- USD/JPY is consolidating losses below the 148.00 resistance.

EUR/USD Technical Analysis

The Euro formed a base and started a fresh increase above 1.1550 against the US Dollar. EUR/USD cleared 1.1620 to enter a positive zone.

Looking at the 4-hour chart, the pair settled above the 1.1620 level, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). The pair even surpassed the 61.8% Fib retracement level of the downward move from the 1.1768 swing high to the 1.1391 low.

On the upside, the pair now faces resistance near the 1.1720 level. The next key resistance sits near 1.1750. A close above 1.1750 could set the pace for another increase.

In the stated case, the pair could rise toward 1.1800, above which the bulls could aim for a move toward 1.1880. If the pair fails near 1.1720, there could be another decline. On the downside, immediate support is 1.1665.

There is also a major bullish trend line forming with support at 1.1665 on the same chart. The next key support sits at 1.1620. Any more losses could send the pair toward the 1.1550 support zone.

Looking at USD/JPY, the pair started a recovery wave above 147.00, but the bears were active above the 147.50 level.

Upcoming Key Economic Events:

- NAHB Housing Market Index for August 2025 – Forecast 33, versus 33 previous.

Dow and Nikkei Hit Record Highs as Rate Cut Bets Rise, Oil Weakens Before Trump–Putin Talks

Last week, markets focused on the rising chance of a U.S. rate cut in September. U.S. CPI was weaker than expected, boosting hopes for a cut, while PPI was higher, showing the impact of tariffs on U.S. companies. Despite the mixed data, traders still expect a rate cut next month, helping drive U.S. and Japanese stocks to record highs.

The Reserve Bank of Australia cut rates as expected. In the U.K. and Japan, stronger GDP results lifted both the pound and yen. President Trump also signed an order extending the tariff truce with China for another 90 days, pushing the next key deadline to November 10, 2025, and avoiding an immediate escalation in trade tensions.

Oil prices fell ahead of the Trump–Putin summit where they will discuss ending the war in Ukraine, with markets watching closely for the outcome. Overall, risk sentiment improved as investors weighed trade uncertainty against central bank support and stronger global growth.

Markets This Week

U.S. Stocks

The Dow hit record highs last week, supported by growing expectations of a U.S. rate cut at the September meeting after weaker-than-expected CPI data. However, concerns remain over the negative impact of tariffs, with higher PPI showing the pressure on U.S. companies, and the market is waiting for more data to see the full effect. Overall, the Dow is expected to trade sideways to higher, making buying opportunities more attractive in the near term. Key resistance levels are at 45,000 and 46,000, while support is seen at 44,000, 43,000, and 42,000.

Japanese Stocks

Japanese stocks posted another week of strong gains, with the Nikkei 225 surging to record highs as optimism from the U.S. trade deal continued and momentum followed U.S. equities higher. The index is now up nearly 10% over the past month, so some consolidation is likely, making it better to wait for a pullback to the 10-day moving average before buying or selling in the short term. Key resistance levels are at 44,000円 and 45,000円, while support is seen at 42,000円, 41,500円, and 41,000円.

USD/JPY

The USD/JPY came under selling pressure last week as expectations of a U.S. interest rate cut encouraged selling, while stronger-than-expected Japanese GDP data raised the chances of a rate hike in Japan. The market looks balanced at current levels, so range trading remains the preferred strategy for now. Resistance is at 148, 149, and 150, while support is at 146 and 145.

Gold

Gold prices fell last week as profit-taking at the top of the recent range and record highs in equities reduced demand for the metal. This came despite U.S. rate cut expectations, which remain supportive for gold in the bigger picture. The market is expected to stay well supported at lower levels, creating potential buying opportunities in the week ahead. Resistance is at $3,400 and $3,450, while support is at $3,300, $3,250, and $3,200.

Crude Oil

WTI crude continued its recent downtrend, staying under pressure as bearish sentiment dominated. Prices were weighed down by OPEC+ production increases, weak Chinese economic data, and concerns that tariffs could further reduce demand. In addition, talks between Trump and Putin to end the war in Ukraine raised the risk of more Russian oil supply hitting the market, adding to downside pressure. Selling into strength remains the preferred strategy, with the 10-day moving average pointing lower. Resistance is seen at $65, $70, and $75, while support is at $60 and $55.

Bitcoin

Bitcoin hit record highs last week as traders continued to buy risk assets on expectations of lower U.S. interest rates. However, the market saw a sharp sell-off from the highs after comments from the U.S. Treasury Secretary confirmed there were no plans for further government Bitcoin purchases. A key reversal on Thursday, where the market made a new high but closed lower, along with a close below the 10-day moving average, could limit further upside in the short term. The preferred strategy is to buy on weakness and sell into strength. Resistance is at $120,000, $125,000, and $150,000, with support at $112,000, $110,000, and $105,000

This Week’s Focus

- Monday: E.U. Trade Balance

- Tuesday: U.S. Building Permits, U.S. Housing Starts

- Wednesday: Japan Trade Balance, U.K. CPI, E.U. CPI

- Thursday: U.S. FOMC Meeting Minutes, E.U. HCOB Eurozone Manufacturing PMI, U.K. S&P Global Manufacturing PMI, U.S. Initial Jobless Claims, U.S. S&P Global Manufacturing PMI, U.S. Existing Home Sales, U.S. US Leading Index

- Friday: Japan National Core CPI, U.K. Retail Sales, Germany GDP, U.S. Fed Chair Powell Speaks

This week, traders will stay focused on U.S. interest rate cut expectations. Inflation reports from the U.K. and Japan will also be important, as markets look for clues on when the Bank of England may cut again and if Japan could raise rates after last week’s strong GDP and the new trade deal with the U.S. The Federal Reserve will release minutes from its July meeting, giving more detail on how officials see inflation, growth, and the timing of future moves.

The Jackson Hole Economic Policy Symposium takes place later in the week, bringing together central bankers and policymakers from around the world to discuss the economy and monetary policy. On Thursday, flash PMI data from the U.S., Eurozone, U.K., and Japan will provide an early look at business activity in August. The week ends with Fed Chair Powell’s speech on Friday, which could give new signals on the U.S. economy and interest rates.

Key 112K level in focus as Bitcoin reverses from record

Bitcoin’s near-term outlook now hinges on whether 112,000 zone can hold as support after last week’s brief breakout to a record 124,553. The sharp reversal has shifted attention to this key level, with selling pressure still visible as the new week begins.

The current decline was triggered by U.S. Treasury Secretary Scott Bessent, who unsettled markets by revealing government Bitcoin reserves were worth only USD 15–20 billion, far below estimates. He added that Washington would not buy new bitcoin for its strategic reserve, instead relying on confiscated assets to build holdings.

While he later clarified on X that Treasury remained open to “budget-neutral pathways” to expand reserves, confidence took a hit. Investors interpreted the comments as a sign Washington is unlikely to bolster demand in the near term.

Combined with stretched technicals, the backdrop encouraged traders to lock in profits, ending Bitcoin’s latest rally attempt prematurely.

Technically, momentum is fading. Bearish divergences in both the daily and 4-hour MACD highlight loss of upside strength. While another test of the highs cannot be ruled out, gains above 124,553 appear constrained.

Instead, focus has shifted to the 111,889 structural support. Decisive break there would confirm correction of the rally from 74,373, opening the door for a pullback to 38.2% retracement of 74,373 to 124,553 at 105,384.

That could set the stage for either prolonged consolidation or a deeper pullback before any fresh bullish leg.