Sample Category Title

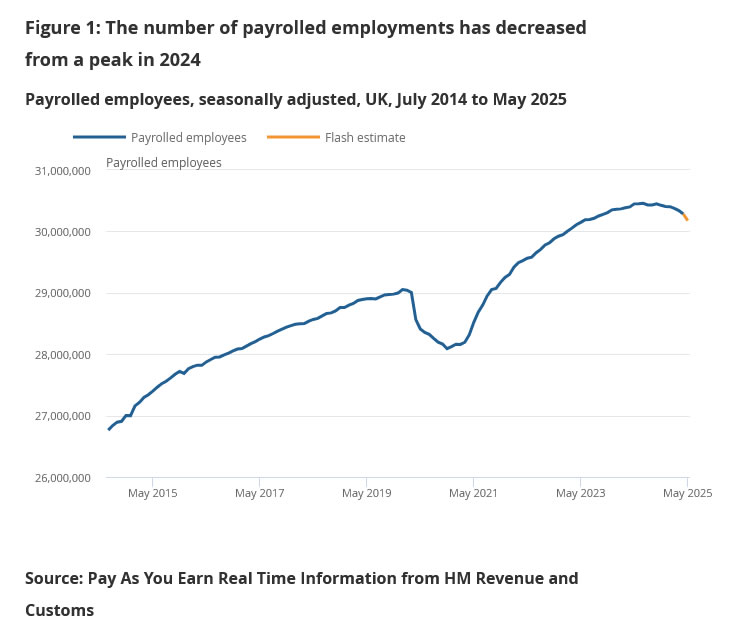

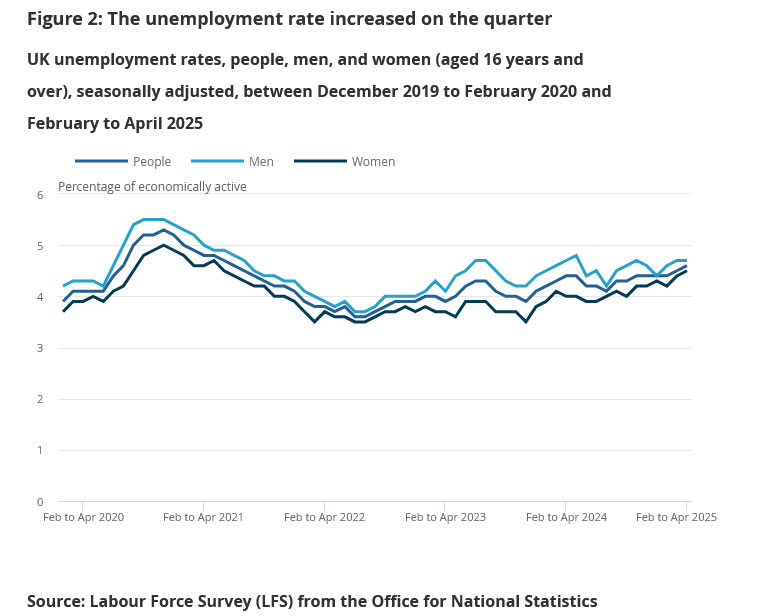

UK labor market softens as unemployment rises to 4.6% and wage growth slows

UK labor market data released today point to gradual cooling. In May, payrolled employment dropped by -109k, or -0.4% mom. Claimant count rose sharply by 33.1k, well above the expected 4.5k increase. Wage pressures are also easing, with median monthly pay rising by 5.8% yoy, down from 6.2% previously, though still within a relatively tight band seen this year.

For the three months to April, unemployment rate ticked up to 4.6% as expected, while both average earnings measures came in softer than forecast. Regular pay (excluding bonuses) rose 5.2% yoy, and total pay increased 5.3% yoy, both under the 5.5% consensus.

Trade Optimism Reins

The week started on a quiet note in the US and with some weakness in Europe, where many were off due to a religious holiday. But futures are in positive territory this morning as traders return to their desks.

One of the main drivers of optimism is the renewed momentum in US/China trade talks. The first day of the second round of negotiations reportedly went relatively well. There hasn’t been a breakthrough yet, and the talks in London continue today. Still, rumours are circulating that the US may be willing to make concessions on tech exports in exchange for China easing restrictions on rare earth metal exports. VanEck’s Rare Earth and Strategic Metals ETF rose another 2.8% on Monday. Meanwhile, Hong Kong’s Hang Seng Index looks poised to retest its March peak, with potential to extend gains if trade news is supportive. The index still trades at a 22% discount to its 2021 peak and 27% below its 2018 high, leaving ample room for upside.

In energy markets, trade optimism is helping US crude break through a key Fibonacci support level. The barrel is edging above the $65.35 mark, representing the 38.2% retracement of this year’s rally. A sustained move above this level could signal the start of a medium-term bullish consolidation, with potential to push toward $68. However, higher supply could eventually cap gains near the $68–$70 range.

By contrast, traditional safe havens such as gold and the Swiss franc are softer, while the US dollar is better bid in Asia. The EURUSD has dipped below the 1.14 mark, the USDJPY briefly traded above 145, while the trade- and China-sensitive Aussie dollar is holding above 65 cents. Progress in trade talks should support further risk-on sentiment. Any disappointment, however, could jolt markets.

The economic calendar is light in the US today, ahead of Wednesday’s crucial CPI release. As a result, markets will remain focused on trade developments. Importantly, positive trade headlines could help offset any negative surprises in tomorrow’s inflation print, which is expected to reflect mounting price pressures in the US—partly due to higher tariff-related costs. The US 2-year yield is consolidating near 4%, while the 30-year yield is softer ahead of Thursday’s key auction. Whether the nearly 5% yield on 30-year paper attracts sufficient demand remains to be seen, particularly as many investors have shifted toward shorter maturities amid budget uncertainties. A weak auction could drive long-term borrowing costs higher and refocus attention on ballooning US debt. That, in turn, could renew demand for alternatives—even in a risk-on environment.

Gold is one such alternative, but investor interest in precious metals is now extending beyond gold. Silver and platinum have both seen impressive rallies. Platinum is up around 15% so far this month, and more than 30% since April. Gold’s strength is certainly a tailwind for sister metals like silver and platinum—platinum ETFs saw a 300% year-over-year surge in investment demand in Q1. But the story goes deeper. The platinum market remains tight, and a second consecutive annual deficit is expected. The World Platinum Investment Council forecasts a shortfall of nearly 1 million ounces this year. As a result, borrowing costs for the metal have surged above 13%—compared to a typical near-zero rate. Meanwhile, demand continues to rise, particularly from hybrid car manufacturers who use platinum in catalytic converters. Jewellery demand is also increasing, as jewellers pivot away from expensive gold. At current levels, platinum still trades nearly 50% below its 2008 peak and may appeal to investors looking to diversify away from high-priced gold.

In equities, Apple unveiled its new “Liquid Glass” interface at its Worldwide Developers Conference, focusing on design rather than AI or core technology—another sign the company may be falling behind in the AI race. So far, Apple has been given breathing room, partly due to its brand power. But a continued lack of innovation on the tech front could cost the company its leadership status, encouraging investors to rotate elsewhere. Apple shares have notably diverged from the rest of the so-called Magnificent Seven. Tech history is littered with fallen giants—Kodak and Nokia come to mind. Apple isn’t there yet, but it needs to act to stay in the top tier.

Elsewhere in tech, TSMC released its May sales figures this morning, reporting a strong 39.6% year-on-year gain. The stock rose in Taiwan on the news and may help lift Nvidia at the US open—especially amid hopes the US might relax certain chip export rules to China. Nvidia has had to halt shipments of China-specific chips due to those restrictions, so any progress on that front can’t come soon enough.

US-China Trade Talks Resume Today

In focus today

In the euro area, we follow the Sentix investor confidence indicator, which is the first confidence indicator collected in June. The indicator rebounded sharply in May following the post-liberation day plunge in April and we think there is further room for a small increase in June.

In Sweden, a collection of data is released. The highlight of the day is the Riksbank's business survey at 9:30 CET, which is crucial for future monetary policy decisions. Early insights suggest a dovish tone, and its results will significantly influence the Riksbank's policy meeting next week. Other key data releases include household consumption and the Production Value Index for April, along with the monthly GDP indicator, all at 08.00 CET. Despite typically being unreliable, a strong GDP indicator, combined with last week's robust retail sales, could suggest a Q2 growth rebound.

Norwegian inflation figures for May are released today, with an expected decline in core inflation to 2.9%. Food prices are likely to rise, but air fares may drop due to post-Easter effects. The risk is tilted slightly to the upside, as prices on imported goods ex. food dropped in May last year and could give a positive base effect. If accurate, inflation will fall below Norges Bank's March estimate of 3.1%.

US-China trade talks resume today at 11:00 CET, focusing on tech restrictions and export limits.

Economic and market news

What happened overnight

US-China trade talks will resume today after kicking off yesterday. Talks came into place after a call between Xi and Trump on Thursday last week and followed a period where both sides accused the other of violating the deal reached in Geneva on 10-11 May. The crux of the talks in London are new US tech restrictions on China and China's limits to exports of rare earth minerals to the US in response. Trump said to reporters overnight "We are doing well with China. China is not easy". The US side has expressed willingness to ease some tech restrictions but not on some of the recent controls on the advanced H20 Nvidia AI chips. China also wants the US side to withdraw new limiting guidelines on Huawei AI chips that was released shortly after the Geneva talks. Trade talks are set to resume today at 11:00 CET.

What happened over the weekend and yesterday

In China, data were released for both inflation and trade yesterday. CPI inflation was slightly better than expected, remaining unchanged at -0.1% y/y (cons: -0.2%) and the core CPI measure (excluding energy and food) increased to 0.6% y/y (prior: 0.5% y/y). Producer price inflation, however, dropped to -3.3% y/y (prior: -2.7% y/y). The numbers underline that deflationary pressures in China continue, although the rise in core inflation is slightly positive. On the trade side, Chinese export data for May were weaker than expected dropping 4.8% y/y (cons: 6.0%, prior: 8.1%). A big decline in exports to the US pulled lower but likely reflected a stand-still in the first two weeks of the month when US tariffs were around 150%. We look for a rebound in the June exports as US-China trade has picked up after the trade war truce set in on 12 May.

In the US, the nonfarm payrolls released on Friday for May increased by +139k (cons: +130k, prior: +147k). The unemployment rate remained steady at 4.2%, and average hourly earnings growth rose by 0.4% m/m SA, slightly exceeding expectations. However, labour supply shrunk by 625k, largely due to a reduction in foreign-born workers. These figures illustrate positive employment growth alongside a declining labour supply, suggesting a tighter labour market, which can be perceived as hawkish.

In the euro area, the final estimates for the national accounts in Q1 2025 revealed revised GDP growth of 0.6% q/q (prior: 0.4%). This growth was mainly attributed to a significant rise in gross fixed capital formation (+1.8%) and exports (+1.9%). Household consumption made a modest positive contribution, while government spending had little impact. The positive balance between exports and imports added +0.3 percentage points to the overall growth.

In Norway, data on Friday showed manufacturing experienced a notable increase in April, with production rising by 2.8% m/m, leading to 2.4% growth over the past three months. This recovery was largely driven by a 3.8% m/m surge in oil-related industries, while mainland industries also showed upward movement. Despite market volatility, the manufacturing sector remains resilient, showing no signs of impact from a global trade war or a decline in oil investments.

Equities: Equities have traded with a positive tone over the past two sessions — Friday and Monday. The key catalyst was Friday's US jobs report, which investors interpreted as a sign of underlying economic resilience. It was not just the level of gains in equities that mattered, but the nature of the move: cyclicals outperformed, defensives underperformed, and implied volatility (VIX) dropped notably. In other words, a classic pro-cyclical pattern. Notably, the move came alongside a sharp rise in both short- and long-end US Treasury yields on Friday, a combination that clearly signals increasing confidence in the US economy's ability to navigate geopolitical uncertainty - particularly the evolving US-China trade tensions. In the US yesterday, Dow 0.0%, S&P 500 +0.1%, Nasdaq +0.3%, Russell 2000 +0.6%. This morning, Asian equities are trading higher, and futures in both Europe and the US point to a continuation of that upbeat tone.

FI and FX: US-China trade talks will resume today after kicking off yesterday. The seemingly positive tone has supported Asian equities alongside European and US futures. The USD firmed with EUR/USD back at the 1.14 level. USD/CNY has been fairly calm while gold dropped. US yields and the 10y2y curve are basically flat with US10y at 4.48 ahead of this week's 3y/10y/30y auctions. Today's Swedish data and Riksbank's company survey may have a marginal impact on Riksbank pricing and, by extension, EUR/SEK which has moved toward the upper end of the 10.80-11.00 range. EUR/NOK is back below the 10.50 level while NOK being supported by risk on and higher energy prices.

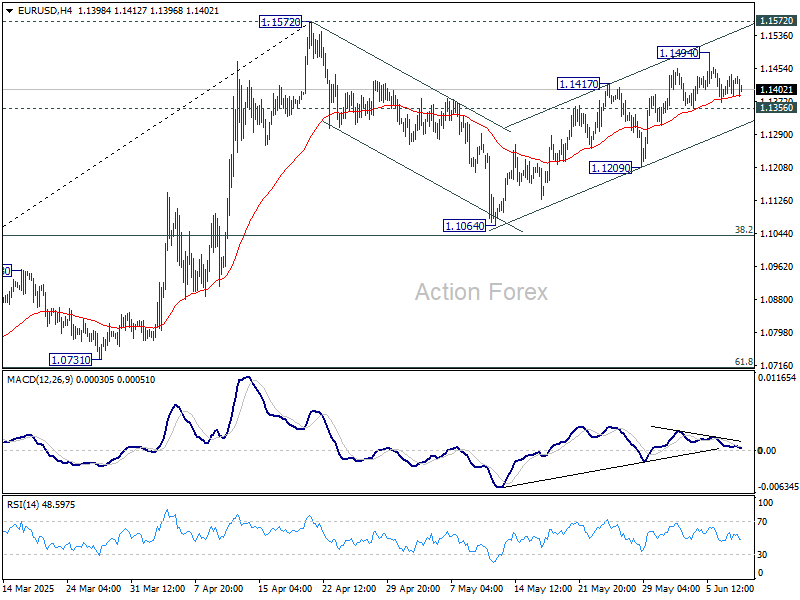

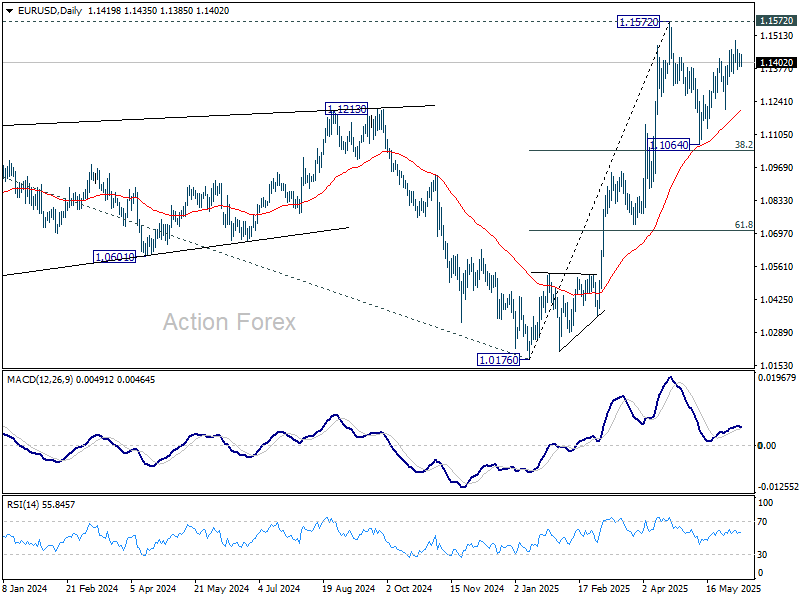

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1392; (P) 1.1415; (R1) 1.1444; More...

Range trading continues in EUR/USD and intraday bias stays neutral. Price actions from 1.1572 are seen as a corrective pattern to rally from 1.0716. While rebound from 1.1064 might extend, strong resistance should emerge from 1.1572 to limit upside. On the downside, break of 1.1356 support will argue that the correction is already in the third leg, and target 1.1209 support for confirmation.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0894) holds.

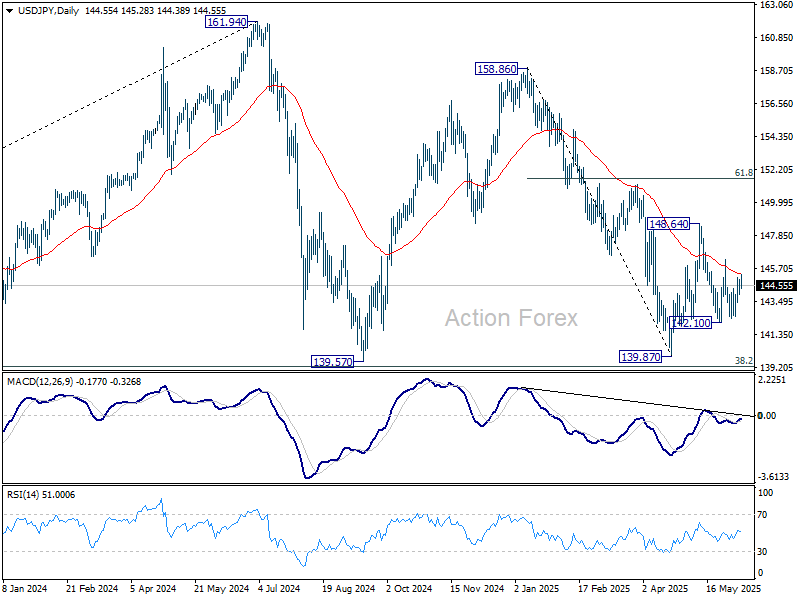

USD/JPY Daily Outlook

Daily Pivots: (S1) 144.06; (P) 144.51; (R1) 145.04; More...

Intraday bias in USD/JPY remains neutral for the moment. On the upside, above 146.27 resistance will argue that price actions from 148.64 has completed as a corrective pattern. Intraday bias will be back on the upside for 148.64 resistance and above to resume the rebound from 139.87 low. However, firm break of 142.10 will bring retest of 139.87 instead.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

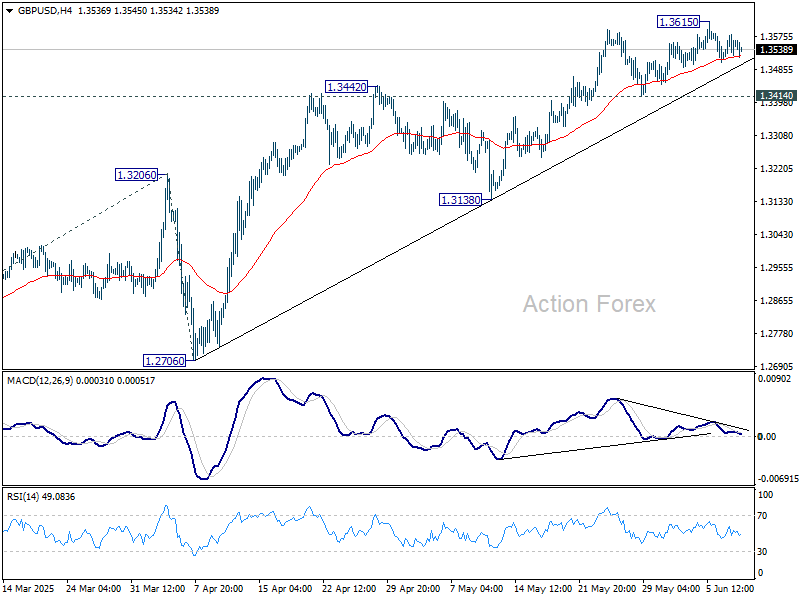

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3514; (P) 1.3547; (R1) 1.3586; More...

Intraday bias in GBP/USD remains neutral as consolidations continues below 1.3615. Further rise will remain in favor as long as 1.3414 support holds. Above 1.3615 will target 100% projection of 1.2099 to 1.3206 from 1.3138 at 1.3813. Considering bearish divergence condition in 4H MACD, break of 1.3414 support should confirm short term topping, and bring deeper correction to 1.3138 support instead.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.2913) holds, even in case of deep pullback.

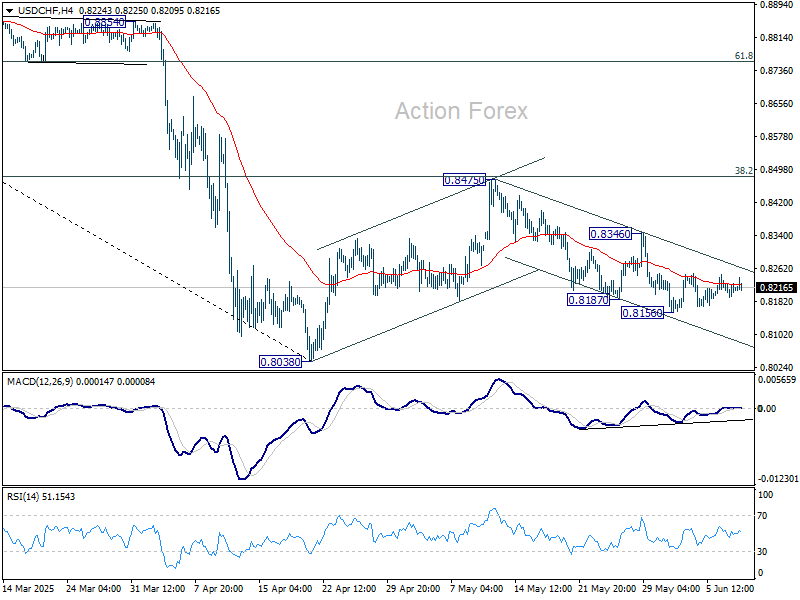

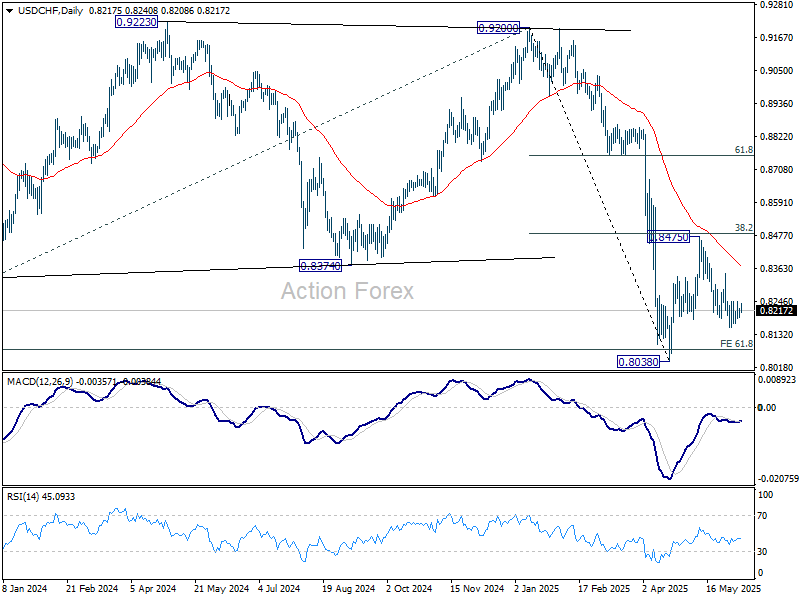

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8197; (P) 0.8213; (R1) 0.8234; More….

Intraday bias in USD/CHF stays neutral as range trading continues above 0.8156. Price actions from 0.8038 are seen as a corrective pattern to decline from 0.9200. While fall from 0.8475 might extend lower, downside should be contained by 0.8038 to bring rebound. Break of 0.8436 resistance will suggest that it's already in the third leg of the correction, and target 0.8475.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8696) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.

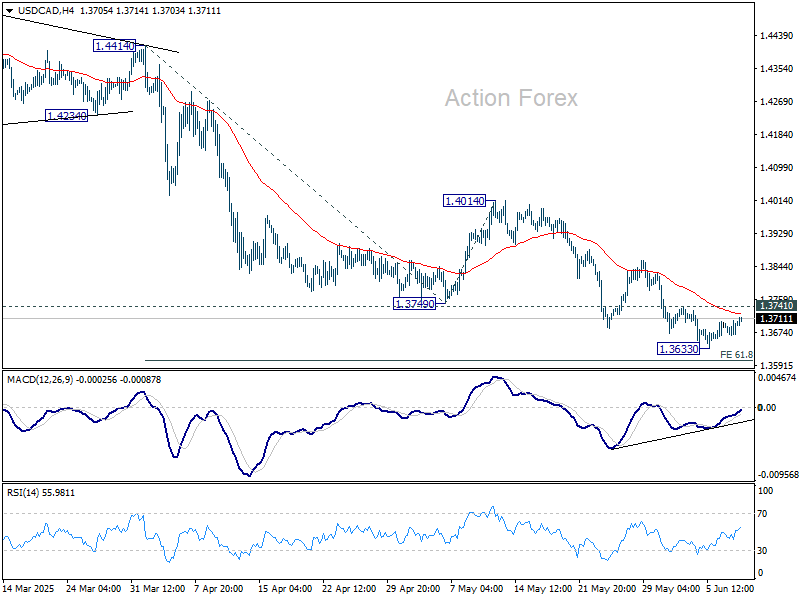

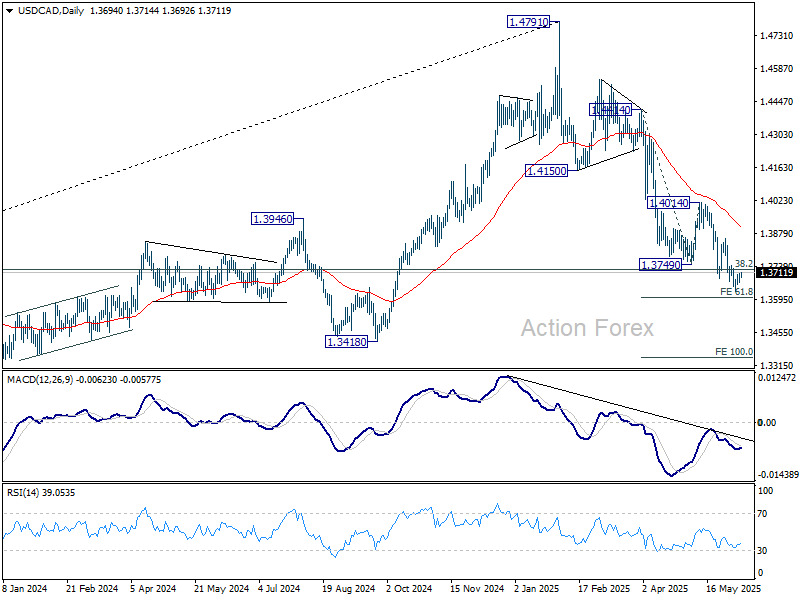

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3677; (P) 1.3692; (R1) 1.3715; More...

USD/CAD is staying in tight range above 1.3633 and intraday bias remains neutral. Considering bullish convergence condition in 4H MACD, firm break of 1.3741 will indicate short term bottoming at 1.3633. Intraday bias will turn back to the upside for stronger rebound to 1.4014 resistance, as a correction to fall from 1.4791. Nevertheless, decisive break of 61.8% projection of 1.4414 to 1.3749 from 1.4014 at 1.3603 will pave the way to 100% projection at 1.3349.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 resistance holds. Firm break of 38.2% retracement of 1.2005 (2021 low) to 1.4791 at 1.3727 will pave the way back to 61.8% retracement at 1.3069.

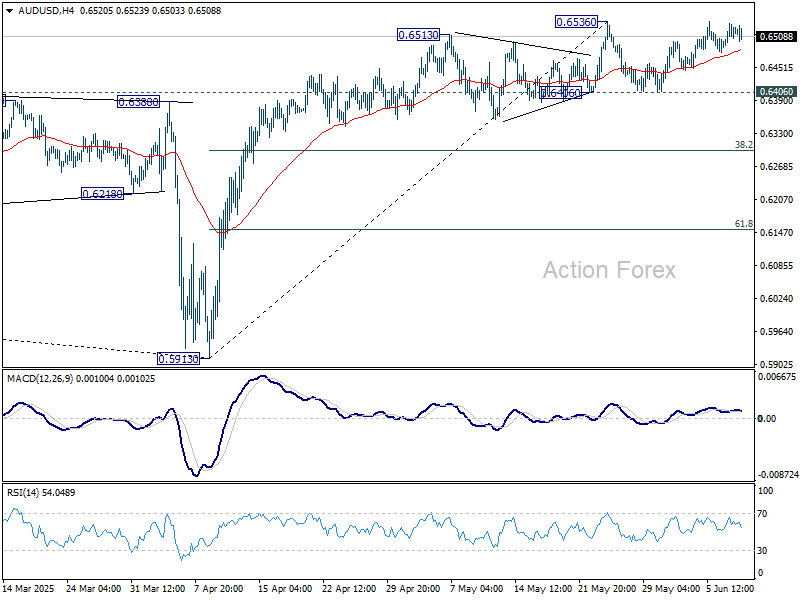

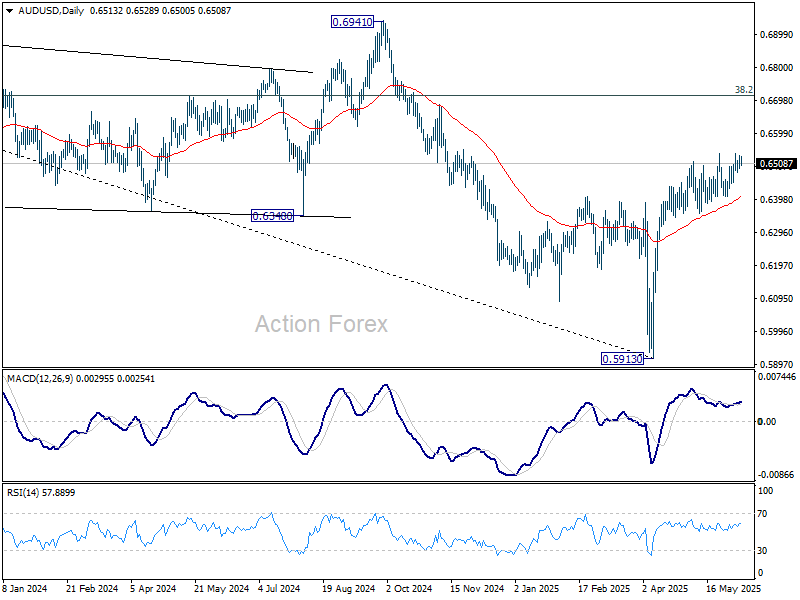

AUD/USD Daily Report

Daily Pivots: (S1) 0.6496; (P) 0.6515; (R1) 0.6536; More...

Intraday bias in AUD/USD remains neutral as it's still staying below 0.6536 resistance. More consolidations could be seen, but even in case of another dip, further rise is in favor favor as long as 0.6406 support holds. On the upside, decisive break of 0.6536 will resume the rally from 0.5913 to 61.8% retracement of 0.6941 to 0.5913 at 0.6548. However, firm break of 0.6406 will turn bias to the downside for 38.2% retracement of 0.5913 to 0.6536 at 0.6298.

In the bigger picture, AUD/USD is still struggling to sustain above 55 W EMA (now at 0.6443) cleanly, and outlook is mixed. Sustained trading above 55 W EMA will indicate that rise from 0.5913 is at least correcting the down trend from 0.8006 (2021 high), with risk of trend reversal. Further rise should be seen to 38.2% retracement of 0.8006 to 0.5913 at 0.6713. However, rejection by 55 W EMA will revive medium term bearishness for another fall through 0.5913 at a later stage.

Aussie Firmer in Quiet Markets as US-China Trade Talks Continue

Global markets remain in a state of cautious anticipation as high-level trade negotiations between the US and China continue for a second day in London. While there’s no definitive outcome yet, mild optimism lingers. Asian equities reflected that mood, with Japan’s Nikkei and Hong Kong’s Hang Seng Index both trading slightly higher. Yet the prevailing sense is one of hesitation, with limited conviction behind the moves. Investors are still waiting for substantive developments before making bolder positioning decisions.

In the currency markets, Kiwi and Aussie continue to outperform for the week so far, buoyed by broad risk resilience and perhaps early hopes that renewed dialogue could reduce global trade frictions. However, upside momentum in both currencies has been sluggish. At the other end, Loonie is trading as the weakest, followed by Swiss Franc and Japanese Yen. Dollar, Euro, and British Pound are largely directionless, trading in the middle of the weekly performance board.

The London meetings between US and Chinese officials mark the second day of high-stakes negotiations aimed at resolving the fallout from earlier tariff escalations. While Monday’s talks yielded no breakthrough, the inclusion of Commerce Secretary Howard Lutnick in this round is notable. His agency oversees export controls, signaling the centrality of rare earths in the ongoing discussions. These magnets, vital to EV production and defense equipment, have become a leverage point for Beijing as it holds a near-monopoly over global supply.

Markets are not pricing in a full resolution just yet. Most expectations center around a tentative agreement on technical issues or interim concessions, such as expanded export licenses. However, structural divisions persist, particularly over technology and national security. Without more substantive signs of compromise, the fragile sentiment boost from the talks could quickly fade, especially if either side issues a combative post-meeting statement.

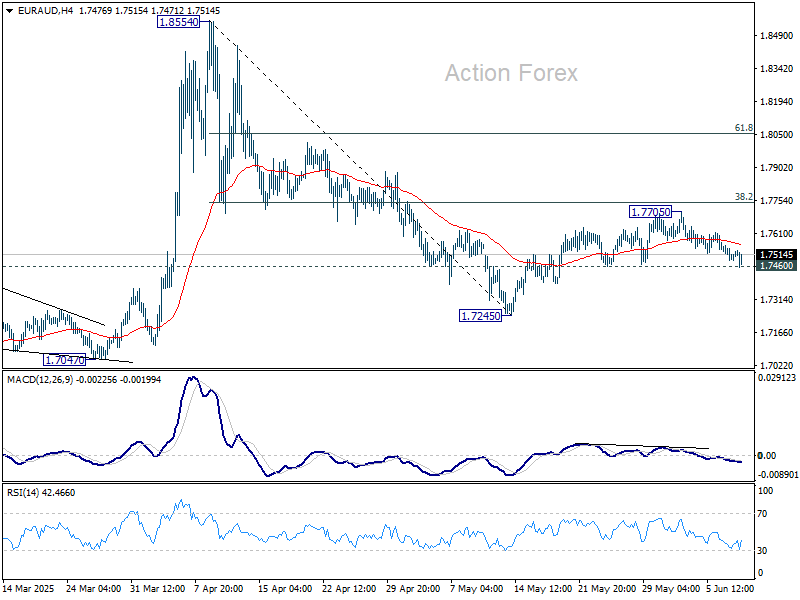

Technically, EUR/AUD is now pressing 1.7460 support as the decline from 1.7705 extends. Firm break there will argue that choppy recovery from 1.7245 has completed as a correction, ahead of 38.2% retracement of 1.8554 to 1.7245. That would also suggest that fall from 1.8854 is ready to resume through 1.7245 low.

In Asia, at the time of writing, Nikkei is up 0.89%. Hong Kong HSI is up 0.15%. China Shanghai SSE is down -0.13%. Singapore Strait Times is down -0.13%. Japan 10-year JGB yield is down -0.002 at 1.476. Overnight, DOW closed down -0.00%. S&P 500 rose 0.09%. NASDAQ rose 0.31%. 10-year yield fell -0.028 to 4.482.

BoJ’s Ueda reaffirms gradual tightening path, cites limited room for rate cuts

BoJ Governor Kazuo Ueda reiterated to parliament today that interest rate hikes will continue, though cautiously, once the central bank gains "more conviction that underlying inflation will approach 2% or hover around that level".

Ueda explained that BoJ still maintains negative real interest rates to support inflation momentum and ensure price growth remains both stable and sustained.

However, Ueda also flagged a significant limitation in policy space should economic conditions deteriorate. With the short-term policy rate still only at 0.5%, the BoJ has "limited room" to cut rates in response to any sharp downturn in growth.

Australia's Westpac consumer sentiment edges higher as rate cuts clash with growth worries

Australia's Westpac Consumer Sentiment index rose a modest 0.5% mom in June to 92.6, reflecting a population still mired in what Westpac called a “holding pattern of cautious pessimism.”

The data reveal "two clear opposing forces" shaping household attitudes: easing inflation and RBA’s May rate cut have improved perceptions around major purchases. On the other hand, sluggish domestic growth and global trade uncertainties continue to weigh heavily on expectations.

Looking ahead, attention turns to the RBA’s next meeting on July 7–8. With economic data remaining mixed and labor market tightness still evident, Westpac expects the central bank to proceed with caution and keep the cash rate on hold. Nonetheless, a fresh round of economic projections in August could pave the way for another 25 basis point cut, as RBA recalibrates its stance amid still-sluggish growth.

Australia’s NAB business confidence lifts to 2, but employment conditions erode

Australia’s NAB Business Confidence index turned positive in May, rising from -1 to 2. However, the improvement in confidence was not matched by underlying business conditions, which weakened further. Business Conditions index slipped from 2 to 0, with trading conditions dipping slightly from 6 to 5, profitability remaining in the red at -4, and employment conditions dropping from 4 to 0 — all pointing to a stagnating environment.

On the inflation front, cost indicators presented a mixed picture. Labor cost growth remained firm at a quarterly equivalent pace of 1.7%. Purchase cost and final product price growth eased to 1.1% and 0.5%, respectively. Retail price growth held steady at 1.2%, suggesting persistent margin pressures.

NAB Chief Economist Sally Auld emphasized that business conditions are still weak and warned that continued softness could cap any recovery in confidence. She also flagged the labor market as a key area to monitor, with the employment index now below average.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6496; (P) 0.6515; (R1) 0.6536; More...

Intraday bias in AUD/USD remains neutral as it's still staying below 0.6536 resistance. More consolidations could be seen, but even in case of another dip, further rise is in favor favor as long as 0.6406 support holds. On the upside, decisive break of 0.6536 will resume the rally from 0.5913 to 61.8% retracement of 0.6941 to 0.5913 at 0.6548. However, firm break of 0.6406 will turn bias to the downside for 38.2% retracement of 0.5913 to 0.6536 at 0.6298.

In the bigger picture, AUD/USD is still struggling to sustain above 55 W EMA (now at 0.6443) cleanly, and outlook is mixed. Sustained trading above 55 W EMA will indicate that rise from 0.5913 is at least correcting the down trend from 0.8006 (2021 high), with risk of trend reversal. Further rise should be seen to 38.2% retracement of 0.8006 to 0.5913 at 0.6713. However, rejection by 55 W EMA will revive medium term bearishness for another fall through 0.5913 at a later stage.