Sample Category Title

Canadian Job Market Treads Water in May, Tariff Affected Areas Show Strain

The Canadian labour market basically tread water again in May, adding only 8.8k net new positions (+0.0% month/month). The details were slightly better, with the private sector up 61k positions (+0.4% m/m), and solid gains in full-time jobs (58k). However, these were mostly offset by losses in part-time jobs (-49k).

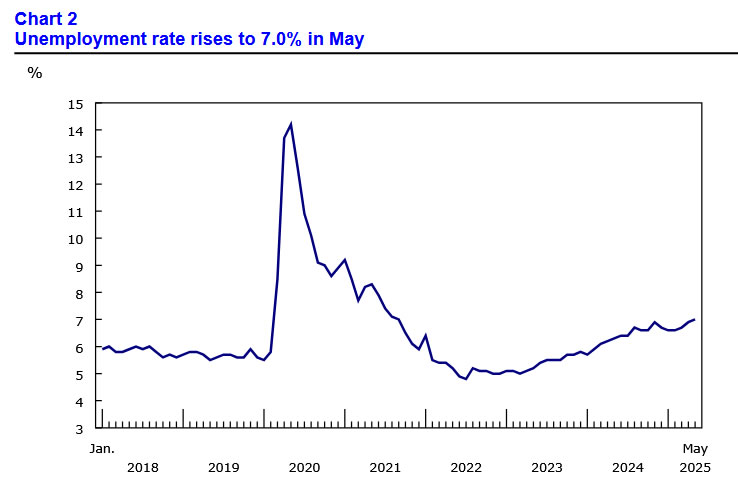

The unemployment rate rose for the third consecutive month to 7.0%, the highest rate since September 2016 (apart from the pandemic). The labour force grew by 0.2% m/m. Growth in the labour supply has slowed in recent months, but employment growth has slowed further.

The job market is even tougher for students. The unemployment rate for returning students (aged 15-24) was 20.1% -- the highest since the 2009 recession (excluding the pandemic).

The impact of tariffs shows up in the industry pattern and regional unemployment pattern. The manufacturing sector was down (-12.2k), as was transportation and warehousing (-15.5k). Manufacturing has lost jobs for four months now, totaling 55k. That said, the wholesale and retail trade sector recouped some (+43k) of the 55k jobs lost through march and April. The highest unemployment rates across CMAs were in Windsor (10.8%), Oshawa (9.1%) (three-month moving averages), which have both seen significant increases since January.

Wage growth was steady in May. Average hourly wages rose 3.4% versus a year ago, matching April's pace. Lastly, total hours worked were flat.

Key Implications

Canada's labour market continued to soften in May. The unemployment rate continued to rise, and the impact of U.S. tariffs is clearly evident in industry and regional patterns. Wage gains were steady in May but have cooled from a roughly 5% pace a year ago.

On Wednesday, the Bank of Canada opted to wait and see how tariffs would impact the Canadian economy, while also weighing recent hotter than expected inflation readings. May's jobs report puts another mark in the economic weakness tally. We think this will ultimately lead to further rate cuts from the Bank of Canada.

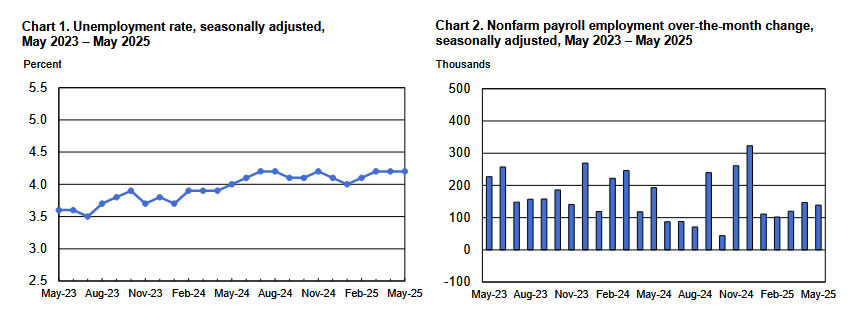

US: Payrolls Rise 139k in May, Unemployment Rate Holds at 4.2%

The U.S. economy added 139k jobs in May, slightly above the consensus forecast of 125k. But revisions for the prior two months subtracted a meaningful 95k jobs.

- Smoothing through the volatility, non-farm payrolls averaged 135k over the last three-months, only a touch lower than the 144k averaged over the twelve-month period.

Private payrolls rose 140k – nearly matching April's downwardly revised gain of 147k (previously 167k) – with the largest gains seen in health care & social assistance (+78.3k) and leisure & hospitality (+48k). Trade exposed industries like manufacturing (-8k) and retail trade (-6.5k) both shed jobs. Federal hiring declined by 22k and has now lost 59k jobs since February.

In the household survey, both civilian employment (-696k) and the labor force (-625k) plummeted, resulting in the unemployment rate holding steady at 4.2%. The labor force participation rate ticked down 0.2 percentage points to 62.4%.

Average hourly earnings (AHE) rose 0.4% month-on-month (m/m) – following a gain of 0.2% m/m in April. On a twelve-month basis, AHE earnings are up 3.9%.

Aggregate weekly hours rose 0.1% m/m, down from April's gain of 0.2% m/m.

Key Implications

Non-farm payrolls remained resilient last month despite heightened trade policy uncertainty. While weakness in the household survey coupled with the significant downward revisions to prior months helped to take some of the shine off the headline payrolls print, it's fair to say that the labor market is holding up better than expected.

Heightened uncertainty surrounding trade and fiscal policy alongside still elevated inflation has left policymakers in no rush to cut rates. While the labor market is showing signs of cooling, job creation is still running at a healthy pace and underscores the ongoing need for patience. Interest rate futures are currently pricing in just 20 bps of policy easing by September and only two quarter-point cuts by year-end.

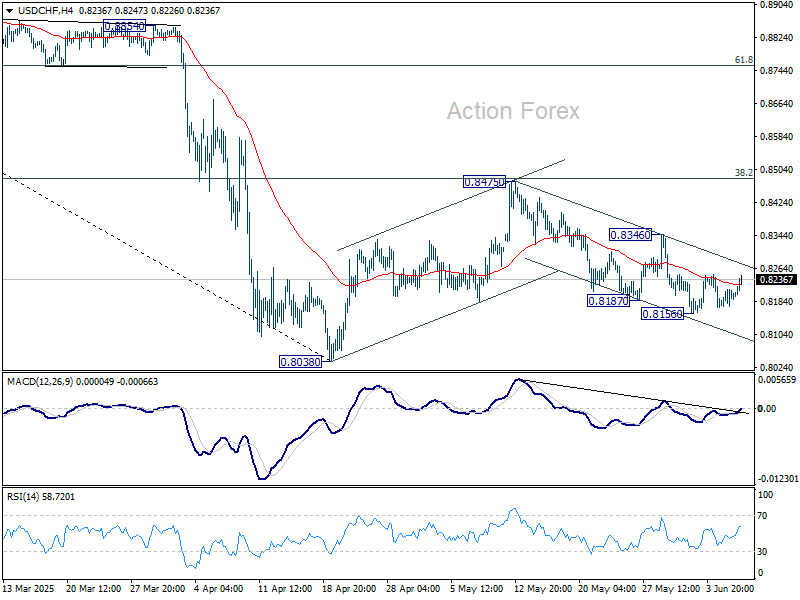

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8174; (P) 0.8195; (R1) 0.8217; More….

No change in USD/CHF's outlook and intraday bias stays neutral. Fall from 0.8475 could extend lower, and break of 0.8156 will target 0.8038 low. But strong support should be seen from there to bring rebound, at least on first attempt. On the upside, break of 0.8346 resistance will extend the corrective pattern from 0.8038 with another rising leg.

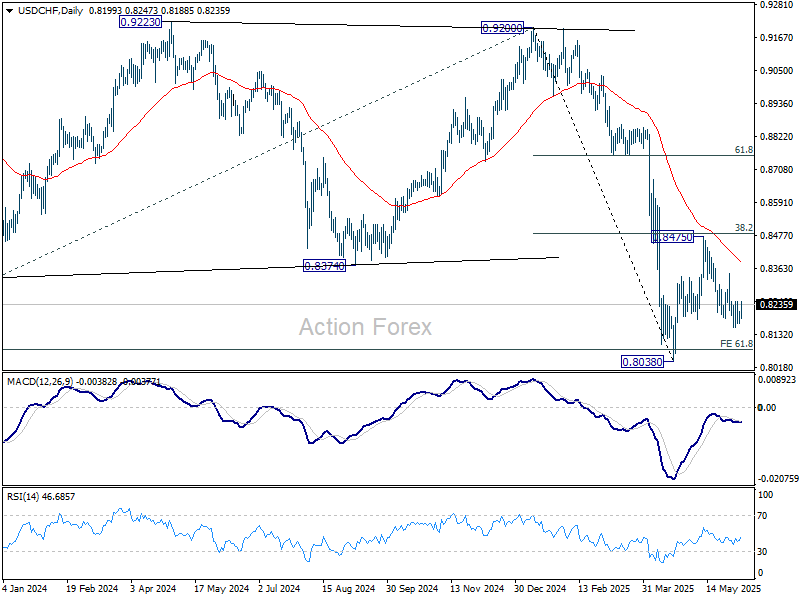

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8732) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.

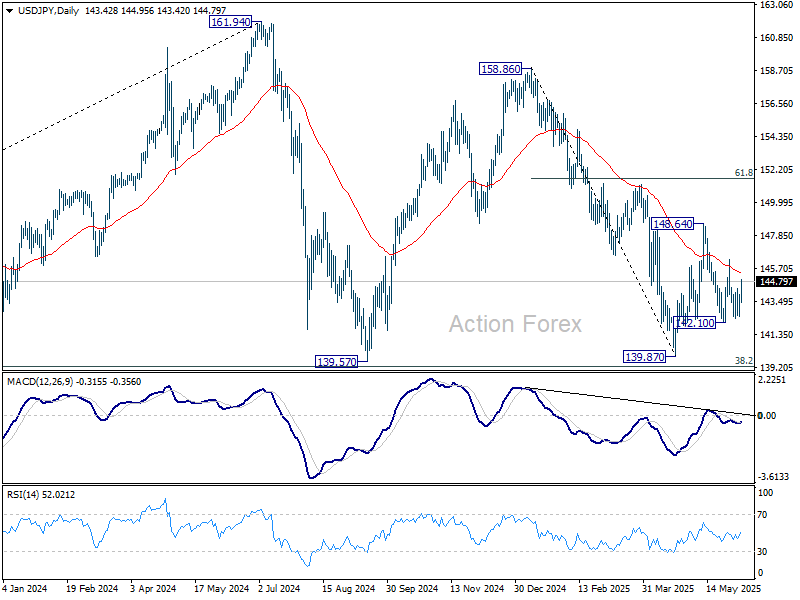

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 142.75; (P) 143.36; (R1) 144.20; More...

USD/JPY's is staying in established range despite today's rebound. Intraday bias remains neutral. On the upside, above 146.27 will target 148.64 resistance first. Firm break there will resume the rebound from 139.87. Nevertheless, break of 142.10 will bring deeper fall back to 139.87 low.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

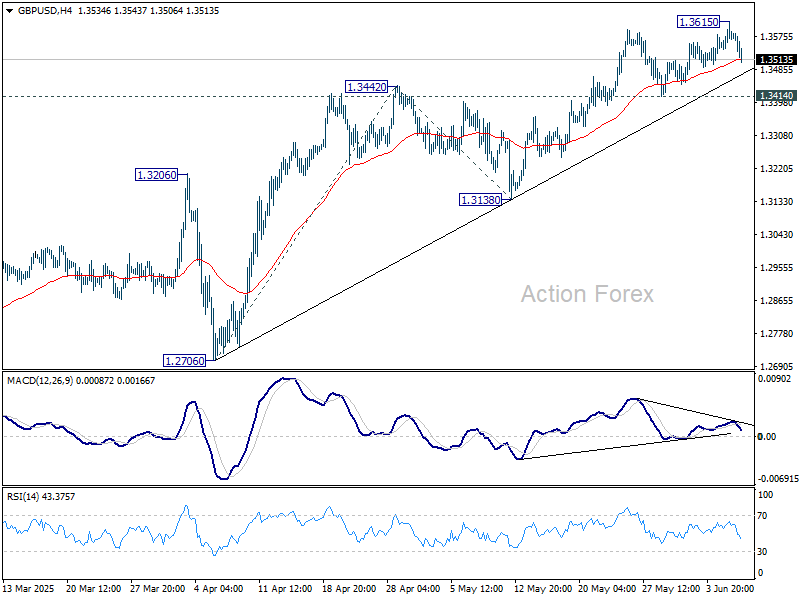

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3536; (P) 1.3577; (R1) 1.3612; More...

Intraday bias in GBP/USD is turned neutral with current retreat. Some consolidations could be seen but further rally is expected as long as 1.3414 support holds. Break of 1.3615 will resume larger rally to 100% projection of 1.2706 to 1.3442 from 1.3138 at 1.3874. However, break of 1.3414 will turn bias back to the downside for deeper pullback to 1.3138 support.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.2866) holds, even in case of deep pullback.

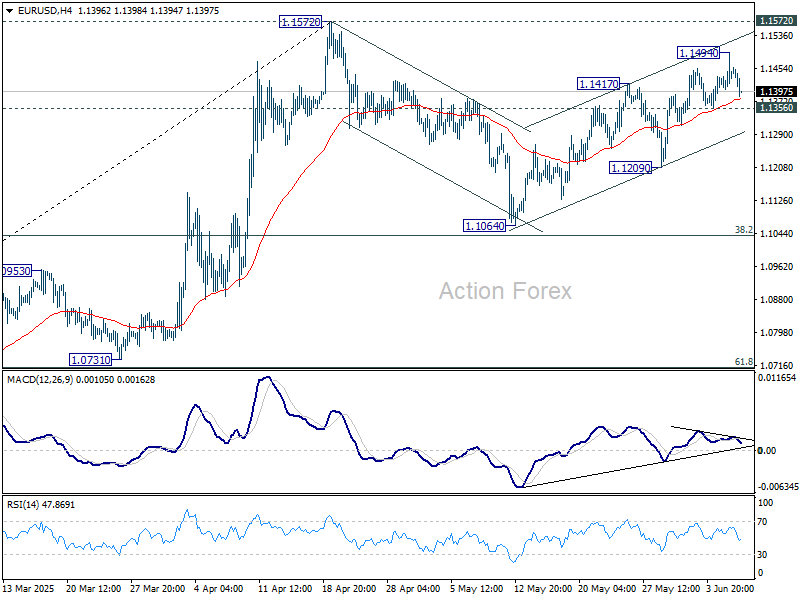

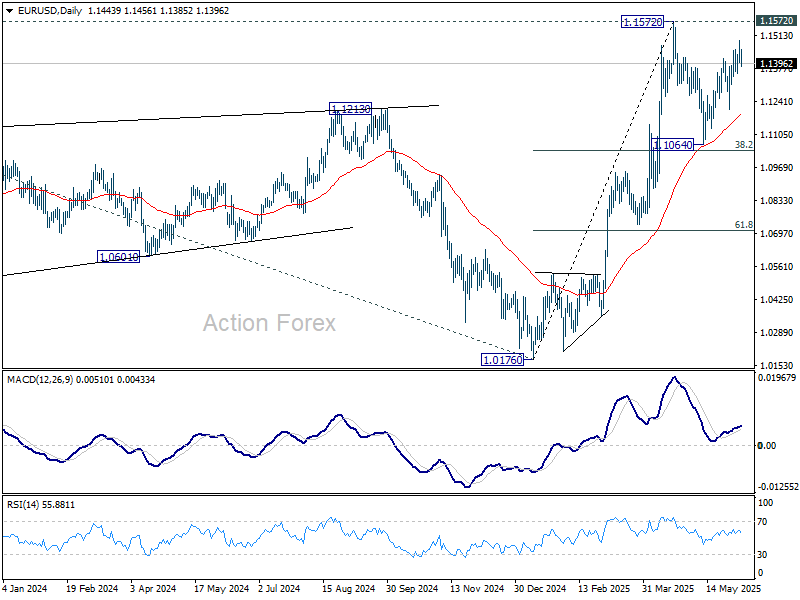

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1401; (P) 1.1448; (R1) 1.1491; More...

Intraday bias in EUR/USD is turned neutral with current retreat. While another rise might be seen, strong resistance could emerge from 1.1572 to limit upside, at least on first attempt. On the downside, break of 1.1356 support will indicate that the corrective pattern from 1.1572 might have started the third leg, and target 1.1209 support for confirmation.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0856) holds.

Dollar Rebounds as NFP and Wages Beat Forecasts, Tariff Impact Yet to Materialize

Dollar staged a firm comeback today following slightly better-than-expected non-farm payroll figures, with job growth at 139k and wage growth coming in strong at 0.4% mom. While not a blowout report, the data was enough to alleviate immediate concerns of a sharp labor market slowdown. Stock futures also advanced, suggesting that investors are reassessing the near-term risks from tariffs and focusing instead on the resilience in headline economic indicators.

Despite ongoing caution over the economic toll of US trade policy, particularly with the expiration of the 90-day tariff truce looming in July, the effects haven’t yet registered decisively in labor markets. In fact, the stronger-than-expected wage growth might reinforce some Fed officials’ inflation concerns, supporting the market consensus that the next rate cut, if any, is unlikely before September.

Outside of the US, Loonie is also showing strength, underpinned by solid domestic jobs data. Aussie and Kiwi are mildly firmer too, buoyed by broader risk appetite. Meanwhile, safe havens are under pressure, with Yen and Swiss Franc the weakest of the day as investors rotate into higher-yielding and risk-correlated assets. Euro and Sterling are softer, but holding within familiar ranges.

In Europe, at the time of writing, FTSE is up 0.10%. DAX is down -0.15%. CAC is up 0.14%. UK 10-year yield is up 0.03 at 4.656. Germany 10-year yield is down -0.11 at 2.573. Earlier in Asia, Nikkei rose 0.50%. Hong Kong HSI fell -0.48%. China Shanghai SSE rose 0.04%. Japan 10-year JGB yield fell -0.002 to 1.459.

US NFP grows 139k in May, unemployment rate steady at 4.2%

US non-farm payroll employment rose 139k in May, above expectation of 130k. That's slightly below average monthly gain of 149k over the prior 12 months.

Unemployment rate was unchanged at 4.2%, matched expectations. Participation rate fell from 62.6% to 62.4%.

Average hourly earnings rose 0.4% mom, above expectation of 0.3% mom. Over the past 12 months, average hourly earnings have increased by 3.9% yoy.

Canada's employment grow 8.8k in May, unemployment rate rises to 7%

Canada's employment grew 8.8k in May, better than expectation of -11.9k fall. Growth in full-time employment (+58k; +0.3%) was offset by a decline in part-time work (-49k; -1.3%).

Unemployment rate rose from 6.9% to 7.0%, matched expectations. Employment rate held steady at 60.8%.

Average hourly wages among employees increased 3.4% you, same as in April.

ECB officials signal pause yesterday's rate cut, emphasize flexibility

One day after ECB delivered its eighth rate cut in this easing cycle, a coordinated message emerged from several Governing Council members: ECB is not committing to further immediate action.

Latvian central banker Martins Kazaks was particularly blunt, stating that markets should not expect a rate cut at every meeting. He emphasized the value of preserving "policy space".

"We don’t get much data between now and the July meeting so it may well be the case that we pause," Kazaks said. "But uncertainty remains very high, the political situation may change every day. So forward guidance isn’t your friend in these circumstances."

Greek central bank chief Yannis Stournaras echoed this sentiment, calling ECB’s work on inflation “nearly done,” while warning that further cuts would require growth to fall short of current forecasts.

Estonian Governor Madis Muller also struck a cautious tone, suggesting the rate-cutting cycle may be “almost finished,” but acknowledged that visibility is limited. All three policymakers stressed that decisions ahead would remain data-driven, and that it was too early to rule out any scenario.

French Governor François Villeroy de Galhau and Lithuania’s Gediminas Šimkus declared victory over inflation. However, both underlined the importance of maintaining flexibility in the face of mounting global uncertainty. Villeroy also reassured that “We have tools to react if there's deflation.”

Eurozone retail sales inch up 0.1% mom April, mixed national trends

Eurozone retail sales rose just 0.1% mom in April, falling short of expectations for a 0.2% mom rise. Modest gains in food, drink, and tobacco sales (+0.5%) and a solid rebound in automotive fuel purchases (+1.3%) were offset by a -0.3% decline in non-food product sales.

Across the EU, retail sales rose a more robust 0.7% mom, but the underlying data painted a sharply divided picture. Poland led with a remarkable 7.5% surge, followed by Slovakia and Sweden at 2.4%. In contrast, Germany—the region’s largest economy—saw a -1.1% drop, dragging on the overall Eurozone figure.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1401; (P) 1.1448; (R1) 1.1491; More...

Intraday bias in EUR/USD is turned neutral with current retreat. While another rise might be seen, strong resistance could emerge from 1.1572 to limit upside, at least on first attempt. On the downside, break of 1.1356 support will indicate that the corrective pattern from 1.1572 might have started the third leg, and target 1.1209 support for confirmation.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0856) holds.

Canada’s employment grow 8.8k in May, unemployment rate rises to 7%

Canada's employment grew 8.8k in May, better than expectation of -11.9k fall. Growth in full-time employment (+58k; +0.3%) was offset by a decline in part-time work (-49k; -1.3%).

Unemployment rate rose from 6.9% to 7.0%, matched expectations. Employment rate held steady at 60.8%.

Average hourly wages among employees increased 3.4% you, same as in April.

US NFP grows 139k in May, unemployment rate steady at 4.2%

US non-farm payroll employment rose 139k in May, above expectation of 130k. That's slightly below average monthly gain of 149k over the prior 12 months.

Unemployment rate was unchanged at 4.2%, matched expectations. Participation rate fell from 62.6% to 62.4%.

Average hourly earnings rose 0.4% mom, above expectation of 0.3% mom. Over the past 12 months, average hourly earnings have increased by 3.9% yoy.

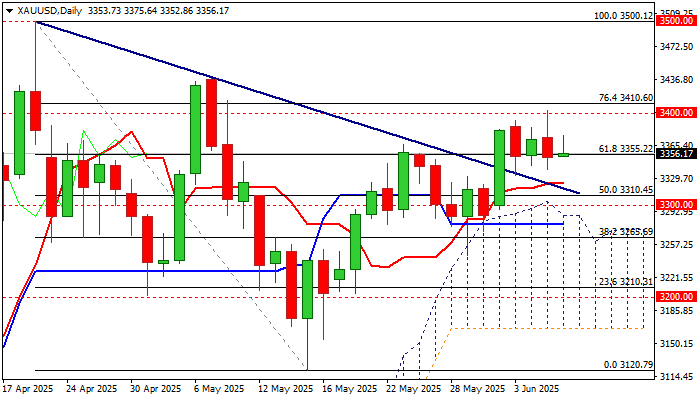

XAU/USD: Gold in Quiet Mode Ahead of Key US Labor Data

Gold is moving within a narrow range in European trading on Friday, but still being constructive after Thursday’s strong upside rejection at pivotal $3400 zone and daily close in red.

Near-term action stays around support at $3355 (broken Fibo 61.8%) and above 10DMA ($3335) which gives a dash of optimism, as several attacks already failed at this zone.

Technical structure on daily chart remains predominantly bullish (despite the evident loss of positive momentum) however, negative signals are developing on hourly chart (the price broke below the base of hourly Ichimoku cloud / 14-momentum is heading south and approaching the centreline), but this is initial signal that still requires confirmation.

Fundamentals are likely to be metal’s main driver again, after surprise talk between US President Trump and Chinese President Xi cooled trade fears and US jobless claims disappointed on jump to new multi-month high.

All eyes are on US May Nonfarm payrolls (130K f/c vs Apr 177K), with gold expected to receive strong boost if May numbers disappoint, while smaller negative impact could be expected on upbeat results.

The data are to provide more clues about the condition in the US labor market that will contribute to Fed’s short-term policy outlook.

First support lays at $3335 (10DMA) followed by $3318 (broken triangle’s upper trendline) and breakpoints at $3300 (psychological) and $3290 (daily cloud top).

Immediate resistance lays at $3368 (hourly cloud top, followed by $3375 (session high) and upper triggers at $3392 (Jun 3 high) $3400/03 (psychological / yesterday’s spike high) and $3310 (Fibo 76.4% of $3500/$3120 correction).

Res: 3375; 3403; 3410; 3437.

Sup: 3335; 3318; 3300; 3290.