Sample Category Title

Weekly Focus – US Budget Bill Not So ‘Beautiful’ If You Ask the Bond Market

The US House managed to pass the budget bill with a slim majority of just one vote on Thursday. Cuts to spending on medicare and food stamps flipped the last votes in favour of the bill, which also includes an extension of the 2017 tax cuts, and adds further tax cuts. US President Donald Trump calls it his 'one, big, beautiful bill' and while bond markets agree it is big they do not see it as 'beautiful'. The budget bill has added further steam to the rise in long bond yields following last week's downgrade by Moody's. US 30-year bond yields pushed to a new high of 5.15% on Thursday, close to the highest yield in 18 years and around 80bp above a 30-year Greek government bond yield. The anxiety over rising yields spilled into weaker US equity markets as well as a lower USD. The bill now goes to the Senate where it will take some time to pass and any changes must go back to the House for approval again, which means it could still take some time before it is all done and ready to be signed by Trump. On the data front US PMIs surprised to the upside but a sharp uptick in the inventory component suggests it is related to front loading of imports and production. This week we moved our call for the next Fed cut to September, but we still see gradual rate cuts after that until rates are around neutral at 3.25%.

Turning to Europe, PMIs for May were a mixed bag with PMI manufacturing rising from 49.0 to 49.4 while PMI service dropped yet again from 50.1 to 48.9, the lowest in more than a year. With the service sector being the biggest part of the economy, the declining activity is a concern. On Monday, the EU Commission lowered their inflation forecast for 2026 to 1.7% from 1.9%. Since the ECB uses a similar model as the Commission it would suggest we see a comparable revision at their upcoming June meeting. Markets now price a 95% probability of a rate cut at the meeting and one further cut by year-end. We expect two further cuts after June as downward pressure on inflation continues due to falling wage pressure, lower oil prices and China exporting deflation.

Chinese data for April was soft but spending may have been affected by the massive escalation of the trade war at the time. Activity is set to increase over the next three months as exports surge in the 90-day truce period and stimulus support demand. Oil prices moved lower again this week to USD64 per barrel from USD67 a week ago as OPEC+ members are weighing a third output increase in July after raising it in both May and June.

Not much happened on the trade talks agenda. After a successful meeting between US and China 10 days ago, frictions have returned. China stated that a US guideline on banning Huawei AI chips globally undermined the consensus reached at the talks. We still see a bumpy road ahead in US-China trade talks and a long way to a real deal (see also recording of our webinar on US-China trade that we held on Wednesday). US is negotiating with a long list of other countries but apart from UK, we still wait for new deals. EU sent a new proposal to the US ahead of talks on Thursday this week.

Next week is quiet on the news front. Main releases are US consumer confidence, euro inflation expectations from ECB, US consumer spending and any news on trade talks. The following week we get more action again with ECB meeting on 5 June and US non-farm payrolls on 6 June. Chinese PMIs and US ISM manufacturing is also due.

Will Gold Break Its All-Time High? Momentum Builds Ahead of Key Level

- Gold has been back on its horses towards the second part of the month after retracing 10.8% from it's April highs.

- Safe-Haven assets are bid today as President Trump reignites tariff discussions.

- Trading at $3,346, the precious metal is less than $155 (3.80%) from its all-time highs.

Technical Analysis update for the Bullion.

XAU/USD Technical Analysis

XAU/USD (Gold) 4H Chart, May 23, 2025. Source: TradingView

Gold has rebounded strongly from it's monthly lows, marked at $3,120, trading $200 dollars higher in the past week.

The precious metal found some relief from last week’s pullback, as easing tariff concerns shifted market focus toward the recent U.S. credit downgrade, triggering a fresh wave of buying interest.

XAU/USD is now at the highs of its Daily Descending Channel, though the MA 20 and 200 are not far below and acting as immediate support.

The end of session will be key to spot if the appetite for Safe-Haven assets is strong going into the week-end. Potential triggers are explained in Wednesday's gold update.

The RSI is close to overbought with a 4H bearish divergence, which has yet to be confirmed.

Technical Levels

We are eyeing at immediate resistance with prices approaching the highs of the Daily Channel.

A rejection of today's highs near the $3,350 psychological level may hint at a return towards the lows of the channel, though key Moving Averages will first have to be broken.

A return to the lows of the channel will be aiming at the $3,100 level.

- Support 1 : 3,270 - 3,290

- Support 2: 3,200 - 3,225

- Support 3: 3,100 Channel Lows

- Support 4: 3,052

- Resistance 1: 3,414 - 3,436

- Resistance 2: $3,500.20 Recent All-time Highs

- Resistance 3: 3,550 Psychological Level

- Resistance 4: 3,598 - 3,600

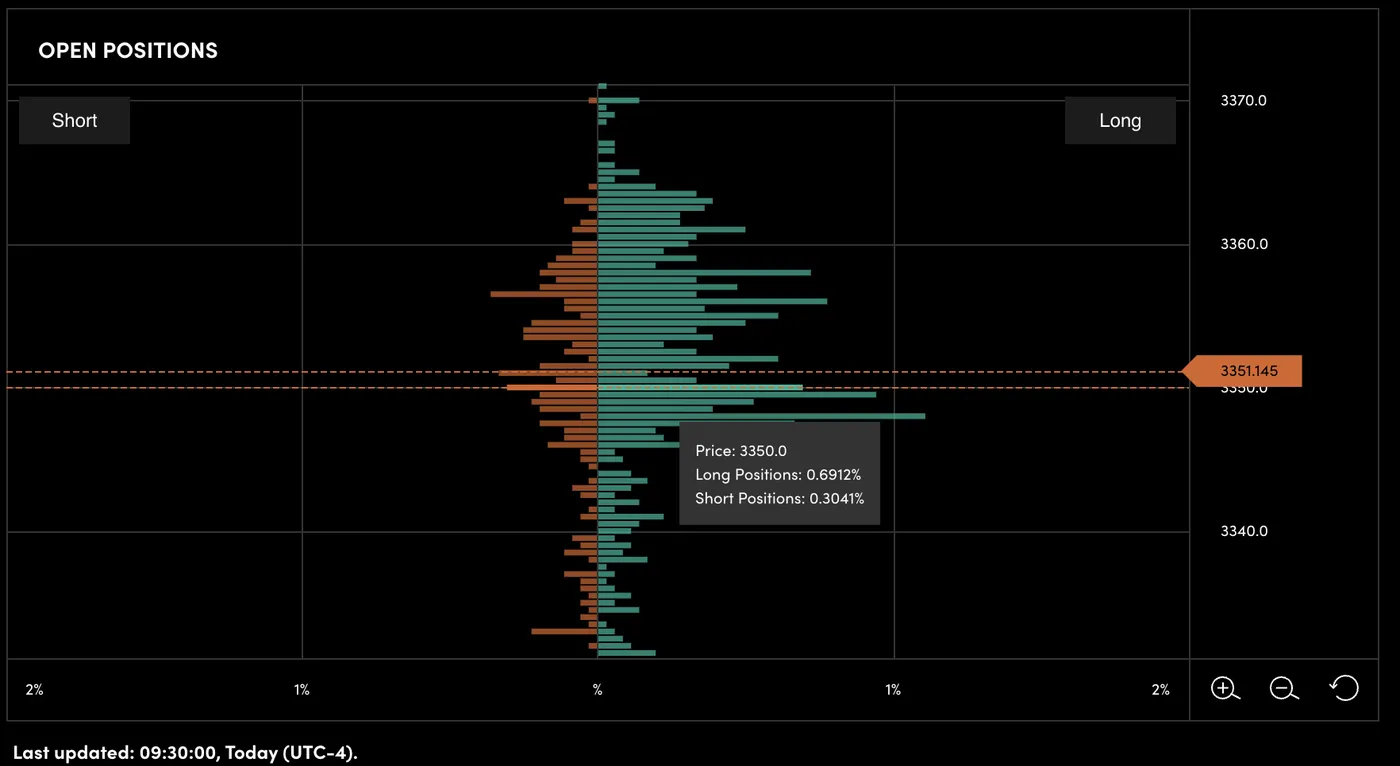

Trader's Positioning

OANDA's Trader and Position Book, May 23. Source: OANDA Labs

Trader's positioning is key to see if an extreme is attained, where one may expect reversals

Traders are about 70% Long vs 30% Short, which may indicate more downside for the precious metal - although, positioning is not at extremes.

Stay in touch with the latest news on our MarketPulse Blog as more volatility can be expected throughout the weekend.

Safe Trades!

Pound Shines as Strong Data Limits Room for BoE’s Rate Cut

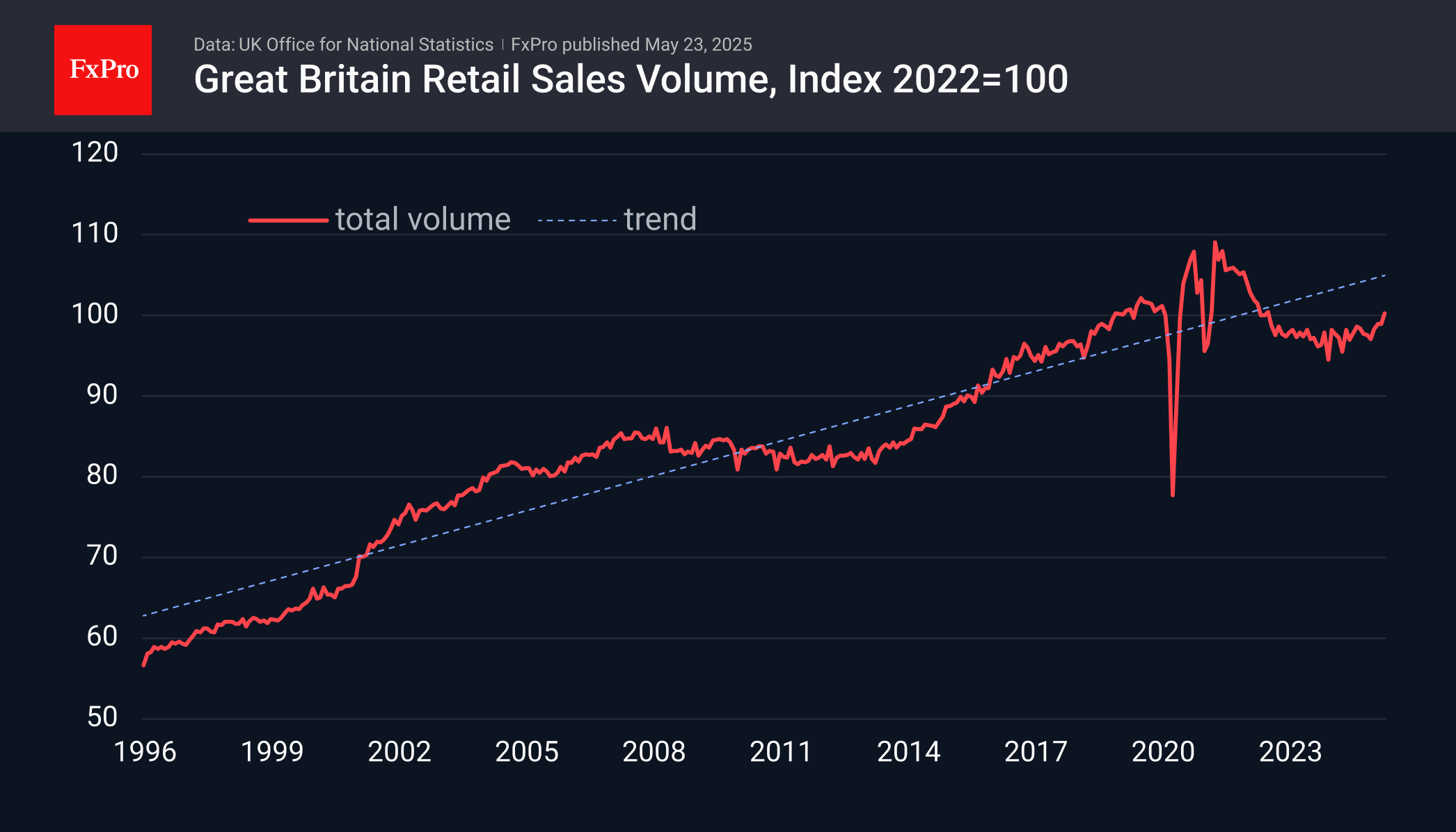

Britain continues to be surprised by strong retail sector data. Data on consumer inflation accelerating to an annualised pace of 3.5% was complemented by strong retail sales figures, renewing buying momentum in GBPUSD.

For April, sales excluding fuel rose by 1.3%, and by the same month last year, the increase was 5.3%. This is much stronger than the average forecasts of economists, who expected to see +0.3% and +4.4%, respectively. Total sales rose 1.2% m/m and 5.0% y/y, equally impressively beating expectations.

UK consumer activity has strengthened since the end of last year, beginning an active return to its long-term linear trend. This news, combined with the latest jump in inflation, limits the room for the Bank of England to cut rates.

This is good news for the currency, so it is no surprise that the pound is hitting 39-month highs. Along with a strong economy comes rising long-term bond yields in Britain, which are historically higher than their US, European and Japanese counterparts. There is a lot of talk now about how difficult it is for America to service its debt at current yields; we can’t forget the 95.5% debt-to-GDP ratio in the UK and the 5.5% yield on local 30-year notes versus the 5% yield in the US. Attention to this issue at the Ministry of Finance or the Bank of England could dramatically change the trend of the pound.

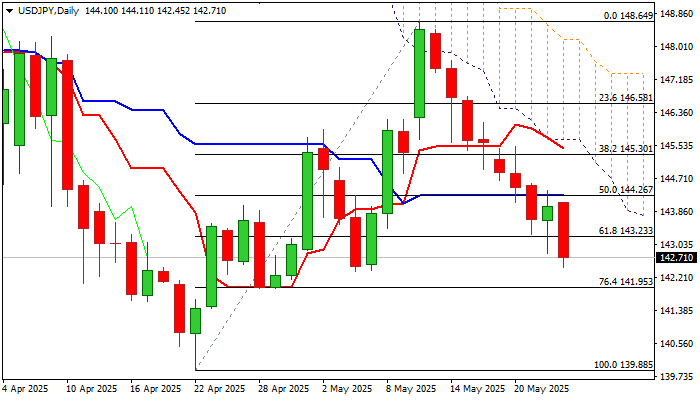

USD/JPY: Hit by Latest Tariff Threats and Hotter than Expected Japan’s Inflation

USDJPY fell further on Friday, driven by the latest comments from President Trump about 25% tariff on Apple phones that were manufactured abroad and Japan’s inflation above forecasts in April that may question BOJ’s intentions to proceed with policy tightening.

The pair is trading at two-week low in early US session on Friday, after the latest drop further weakened near-term structure.

Important Fibo support at 143.23 (61.8% of 139.88/148.64 has been taken out, with weekly close below this level to add to negative stance (MA’s turned to full bearish setup, 14-d momentum remains below the centreline and falling and thickening daily cloud continues to weigh).

Completion of reversal pattern on weekly chart also contributes to bearish outlook.

Bears pressure target at 142.35 (May 6 trough) and eye a higher base at 141.95 (late Apr higher base / Fibo 76.4%) violation of which to unmask key supports at 140.00/139.88 (psychological / 2025 low).

Limited corrective action should be capped under broken daily Kijun-sen / 50% retracement (144.26).

Res: 143.23; 143.92; 144.26; 144.62.

Sup: 142.35; 141.95; 141.42; 140.47.

Fed’s Goolsbee: Tariff-driven stagflation would be the worst-case scenario

Chicago Fed President Austan Goolsbee emphasized a cautious stance on monetary policy, citing the high level of uncertainty surrounding the economic outlook.

Speaking on CNBC, Goolsbee said “everything’s always on the table,” but that the bar for further action is “a little higher” until more clarity emerges.

He flagged the stagflationary effects of trade policy shifts as a key concern, calling such an environment “the central bank’s worst situation,” and adding that policymakers will need to closely assess how much tariffs push prices higher.

While markets are pricing in two Fed cuts this year, likely starting in September Goolsbee avoided committing to any timeline.

He stressed the need for flexibility, saying, “I don’t like even mildly tying our hands at the next meeting.” Still, he maintained that, heading into April 2, inflation appeared to be easing and the labor market was stable, conditions under which interest rates could “come down a fair amount” over the next 12 to 18 months.

Sunset Market Commentary

Markets

It’s been relatively quiet around US President Trump the past fortnight. Too quiet now it seems… Two weeks ago, the POTUS was too busy collecting money in the Middle East. This week, he needed to align House Republicans to pass his big beautiful, deficit-augmenting, bill. They narrowly did so yesterday, giving way to the Senate to deliberate on the bill. Overall, the bill remains on track to make the president’s self-imposed Independence Day deadline. With those issues out of the way, Trump went back to one of his favorite pastimes: ranting on social media. It started rather innocent with an attack at the very untalented Bruce Springsteen, morphed into a treat of 25% tariffs on Apple if iPhones aren’t made in the US (Apple is pivoting production from China to India) and ended with the recommendation of a straight 50% tariff on the EU, effective June 1st as talks with the bloc are “going nowhere”. So far for the 90-day truce in the trade war. The Truth Social post covered an otherwise calm trading session with risk aversion. European stock markets fell off a cliff, currently registering losses of over 2%. US equity futures also dived up to 2% lower. Core bonds rallied with German Bunds outperforming. Yields currently cede 9 bps to 7.5 bps in a bull steepening move. More ECB rate cuts beyond the June meeting are all of a sudden back into play. US Treasuries build on yesterday’s sell-the-rumour, buy-the-fact gains (House vote) with yields losing 6 bps (2-yr) to 1.5 bps (30-yr) in a similar steepening move. The euro suffered only a marginal setback against the dollar whose losing more and more international appeal. EUR/USD dipped from 1.0375 to 1.0325. EUR/GBP trades below 0.84 for the first time since early April on EUR weakness after UK markets ignored strong April UK retail sales. Safe haven currencies JPY (USD/JPY 142.50) and CHF (EUR/CHF 0.93) excel. US Treasury Secretary Bessent hopes that Trump’s threat “lights a fire under the EU”. He called EU negotiations an exception to the rule as talks with many Asian nations move quickly in the right direction. Last time around Trump had a tariff recommendation (80% for China to unlock trade talks), Bessent managed to eventually agree on a 30% tariff. Going into the long US (and UK) weekend, we can only hope for the best and expect the worse. The stakes at the G7 meeting of finance ministers and central bankers in Canada are high. Bank of Japan governor Ueda at the sidelines of that meeting was asked late last night on this week’s sell-off in long-term Japanese government bonds. They pushed Japanese 20-yr (>2.5%), 30-yr (>3.2%) and 40-yr (3.7%) yields to their highest levels since 1999. Ueda declined to comment specifically on short-term developments, “but of course we will continue to monitor the market carefully”. These comments echo the Japanese MoF’s first verbal firing shots in the run-up to FX interventions in case of an uncontrolled weakening of the Japanese currency. Markets took notice with Japanese government bonds leading the way higher this morning. In a corrective move, the local yield curve bull flattened with the Japanese 30-yr yield ending 12.7 bps lower.

News & Views

German Q1 GDP growth upwardly revised from 0.2% to 0.4% Q/Q, with positive contributions from private consumption (0.5% Q/Q from 0.2%) and capital investments (0.9% Q/Q from 0.2%). Net exports added a strong 0.9% ppts (after being negative for the previous three quarters). Also today, the German IFO Institute reported that its survey series on export expectations improved significantly in May. The index rebounded from -9.4 in April to -3 in May. Head of Ifo Surveys Klaus Wohlrabe assessed that the easing in the tariff conflict brought relief for exporters. This improvement obviously seems outdated all of a sudden following today’s Trump tariff threat.

Previewing next week’s policy decision, KBC expects the National Bank of Hungary to keep its policy rate unchanged at 6.5%, in line with consensus. The MNB has to maintain cautious approach amid persistent inflationary pressures and global uncertainties. CPI inflation slowed from 5.7% in February to 4.2% in April, but stays above the 2%-4% MNB target range. In addition, the slowdown was helped by margin caps introduced on food prices. Caps on other goods kicked in in May. They might slow inflation short-term, but don’t solve the issue further out. KBC expects inflation to average 4.5% in 2025. The MNB signals that tight monetary conditions are needed to slow inflation and anchor inflation expectations. Global uncertainty also advocates caution. We expect MNB to keep rates unchanged throughout summer, but if the ECB and the Fed ease policy further there might be some room for one or two 25 bps steps in autumn. The valuation of the forint, a further deterioration of the Hungarian fiscal position and global risk sentiment are main risks to this scenario.

DAX Tumbles 2.7% as President Trump Sets Tariff Deadline for EU

President Trump Reignites Tariff Discussion

US President Donald Trump just reignited market volatility with a series of tweets and comments around tariffs.

The President posted to his Truth Social platform that tariffs of at least 25% would be put in place for iPhones not made in the US. The move sent the S&P lower but the comments on EU tariffs really hampered risk sentiment and risk assets.

In a separate Truth Social post, President Trump criticized the European Union, accusing it of engaging in unfair trade practices that have contributed to a significant trade deficit with the United States. Highlighting issues such as trade barriers, VAT taxes, and corporate penalties, Trump expressed frustration over stalled negotiations with the EU.

In his post, Trump stated:

"The European Union has been very difficult to deal with. Their powerful Trade Barriers, VAT Taxes, ridiculous Corporate Penalties, Non-Monetary Trade Barriers, Monetary Manipulations, unfair and unjustified lawsuits against Americans Companies, and more, have led to a Trade Deficit with the US of more than $250,000,000 a year, a number which is totally unacceptable. Our discussions with them are going nowhere! Therefore, I am recommending a straight 50% Tariff on the European Union, starting on June 1, 2025. There is no Tariff if the product is built or manufactured in the United States. Thank you for your attention to this matter!"

The proposed 50% tariff, set to take effect on June 1, 2025, would exempt products manufactured within the United States, signaling a push to encourage domestic production. This announcement is likely to spark significant debate and could have far-reaching implications for US-EU trade relations.

Market Reaction - DAX Falls 2.7%, S&P Down 1.5%

Risk assets have taken a hit with the Wall Street's "fear gauge", the CBOE Volatility Index .VIX, spiked to a more than two-week high and was last at 24.6 points.

S&P 500 has tumbled 1.5% as megacap and growth stocks turned sharply lower, with Amazon AMZN.O and Nvidia NVDA.O sliding more than 2% each.

The DAX index slid as much as 2.7%.

This is what i would consider a major escalation in the tariff conversation. Markets had hoped that most of the proposed tariffs by the US administration would be negotiated away.

Concerns will now rise that if these tariffs are implemented, growth in the European Union may be affected. This comes after disappointing PMI data from the EU earlier this week.

Germany's two-year bond yield fell 10 basis points to 1.73%, while the 10-year yield dropped 9 basis points to 2.55%.

In currency markets, the Japanese yen was the top performer, with the dollar down 0.9% at 142.77 yen and the euro down 0.56% at 161.43 yen.

Gold saw renewed safe haven flows as the precious metal is tarding above the $3350/oz mark at the time of writing.

The euro was steadier against the dollar, rising 0.3% to $1.1311, as traders weighed U.S. tariff concerns against eurozone growth worries.

DAX Index Daily Chart, May 23, 2025

Source: TradingView.com

Support

23212

22800

22405

Resistance

23750

24000

24250

EUR/USD Technical Outlook: Weekly Timeframe Hints at Further Gains

- EUR/USD is showing bullish momentum on the weekly chart with a potential bullish engulfing candle, suggesting further gains and possible new yearly highs.

- On the daily chart, a close above 1.1366 is needed for a structural change.

- The RSI on the daily timeframe indicates a bullish bias, but a US Dollar recovery could trigger a pullback in EUR/USD.

EUR/USD is enjoying a good run this week despite weak PMI data reigniting stagflation concerns. However, US Dollar weakness continues to help the Euro as it trades around 1.6% higher against the greenback.

The performance of the Euro has surprised me to say the least. This morning we saw traders fully price ECB rate cuts in April for the first time. This was followed by Morgan Stanley lowering the Euro area's 2025 GDP forecast to 0.8% vs prior forecast of 1.0% while also saying that they expect the ECB benchmark rate to reach 1.5% in December 2025 vs the prior forecast of June 2026.

It is no surprise then that the rally in EUR/USD has largely been driven by US Dollar weakness as was evident this week. Weak Euro Area data was once again ignored as the US Dollar continued its struggles.

The technicals are also painting an interesting picture so let's take a look.

Technical Analysis on EUR/USD

Let us start with the technical picture on the weekly chart.

As you can see below, the recent pullback in EURUSD appears to have found support with last week's candle closing as a doji indecision candle at the trendline which was broken on April 7.

This was a sign that a potential reversal may be incoming this week and that has come to fruition thus far as the US Dollar struggled.

EUR/USD is currently up around 1.6% for the week with the weekly candle on course to close as a bullish engulfing candle. At present, the weekly candle is on course to engulf the past three weeks of bearish price action hinting at significant buying pressure.

Looking at this picture and further gains at this stage look likely with fresh yearly highs also not out of the question.

EUR/USD Weekly Chart, May 23, 2025

Source: TradingView.com

On the daily chart below, the swing high at 1.1366 needs to be broken with a daily candle close above this level needed for a change in structure.

If such a move develops this may embolden bulls further that the rally has the legs to take out the April 21 highs at 1.1572.

Beyond the 1.1366 handle, there is also resistance around the 1.1400 level and 1.1482 which could prove a challenge for bulls to overcome.

The RSI period - 14 on the daily timeframe though also appears to support a bullish narrative for now. Having broken back above the neutral 50 level on May 19, this supports the idea that momentum is currently favoring a bullish bias.

However, indicators are not always correct and thus a pullback cannot be ruled out if the US dollar finds support next week.

EUR/USD Daily Chart, May 23, 2025

Source: TradingView.com

Support

- 1.1270

- 1.1200

- 1.1100

Resistance

- 1.1366

- 1.1400

- 1.1482

Canada: Retail Sales Bounced Back in March

Retail sales saw their first increase in 2025, up 0.8% month-on-month (m/m) in March, a tick above Statistics Canada's advanced estimate. After adjusting for inflation, the volume of retail sales posted a 0.9% m/m increase.

For the first quarter, retail sales volumes saw mild growth (+0.2% quarter-on-quarter, q/q) after two quarters of relatively strong gains.

Motor vehicles and parts sales (4.8% m/m) contributed most to the headline print, reversing the decline from the two months prior.

Lower crude oil prices in March drove a -6.5% m/m decline in receipts at gas stations and fuel vendors (-2.6% m/m on a price-adjusted basis).

Excluding auto sales and receipts at gas stations, core retail sales increased for a second consecutive month (0.2% m/m), driven primarily by higher sales of building materials (+2.6% m/m) and clothing/jewelry/leather goods (+2.6% m/m). A -2.7% m/m pullback from general merchandise retailers tempered core retail gains.

E-commerce sales fell 2.1% m/m in March.

Statistics Canada's advanced estimate for April points to a 0.5% m/m rebound.

Key Implications

March retail sales data came in a bit warmer than expected. Consumers pulled forward their auto purchases, something we expected as buyers front-ran counter tariffs imposed in April. The surprise was in the 5 of 7 non-auto retail components that advanced on the month, which may represent stockpiling of non-discretionary items ahead of other incoming tariffs.

Expectations for another solid month of sales growth in April may offer some positive momentum for total consumer spending into the second quarter, though we expect spending weakness to dominate the broader trend. Canadian consumer confidence has nosedived in recent months and the labour market has started to shed jobs. Against this backdrop, we expect consumers to stay relatively hesitant until confidence and clarity are restored, which we think will occur in the later stages of this year. A few more Bank of Canada rate cuts in the coming months may help soften the blow.

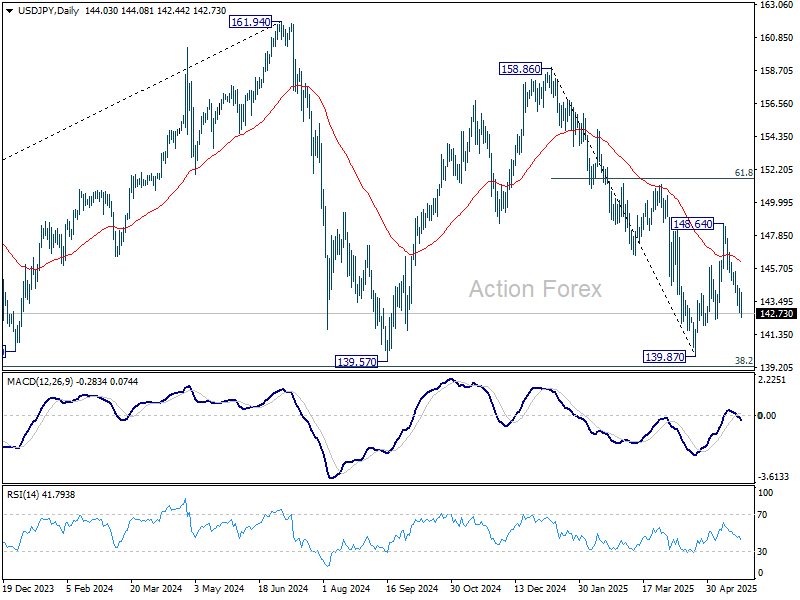

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 143.08; (P) 143.75; (R1) 144.68; More...

USD/JPY's fall from 148.64 resumed after brief recovery. Intraday bias is back on the downside for retesting 139.87 low. On the upside, above 144.31 minor resistance will turn intraday bias neutral again first.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.