Sample Category Title

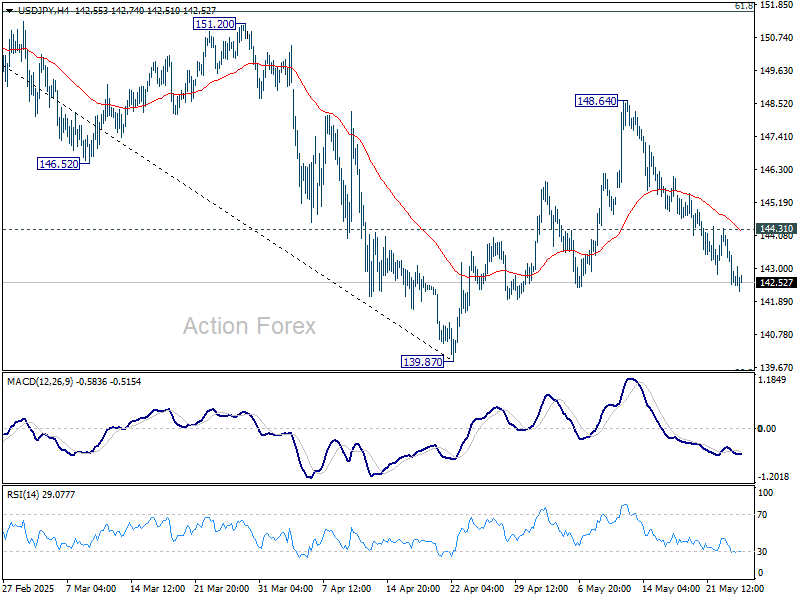

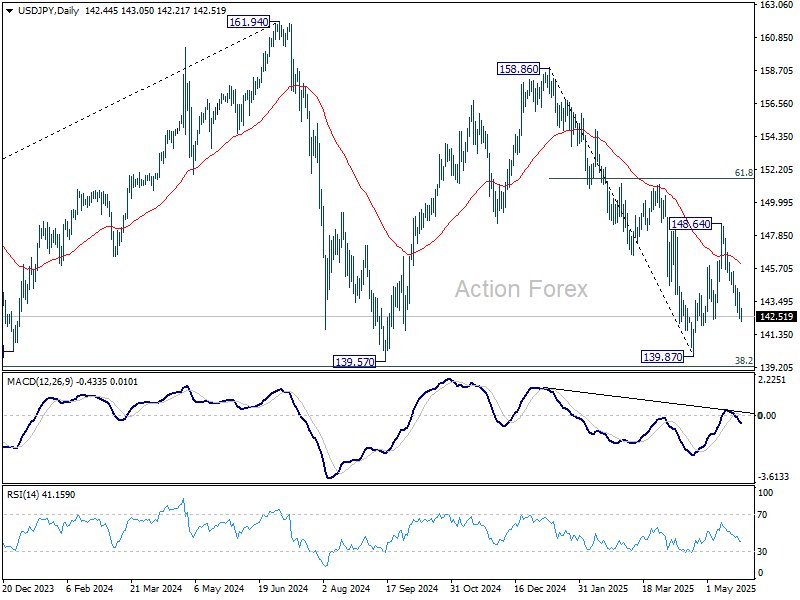

USD/JPY Daily Outlook

Daily Pivots: (S1) 141.93; (P) 143.07; (R1) 143.72; More...

Intraday bias in USD/JPY remains on the downside as fall from 148.64 is in progress for retesting 139.87. On the upside, above 144.31 minor resistance will turn intraday bias neutral again and bring consolidations first, before staging another decline.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

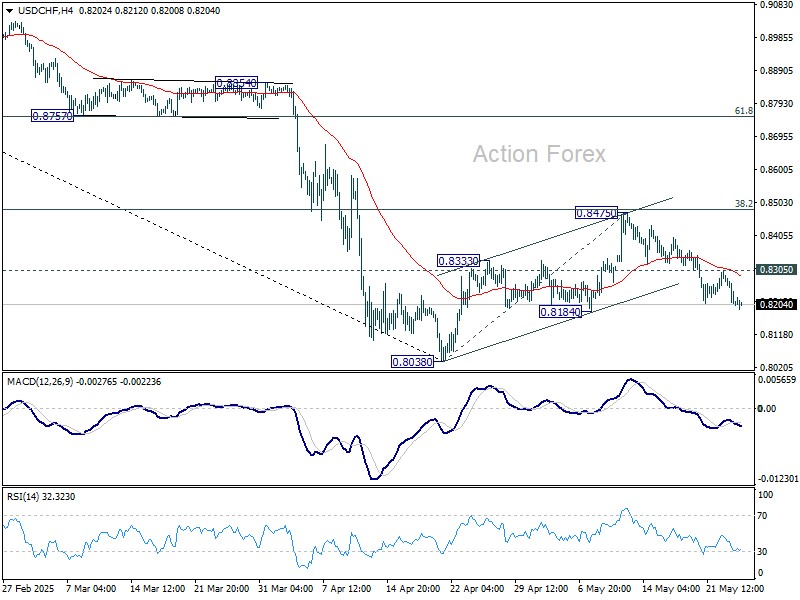

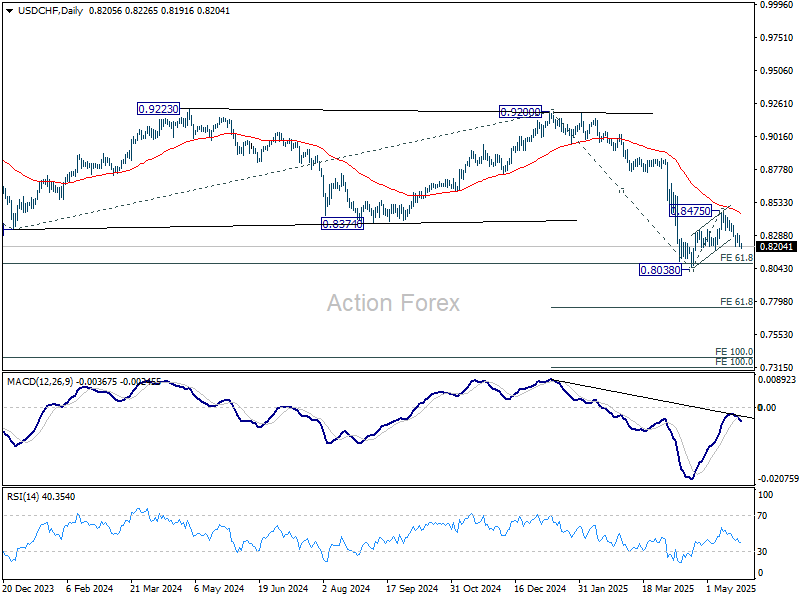

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8179; (P) 0.8238; (R1) 0.8273; More….

Intraday bias in USD/CHF remains on the downside as fall from 0.8475 is in progress for retesting 0.8038 low. Firm break there will resume larger down trend to 61.8% projection of 0.9200 to 0.8038 from 0.8475 at 0.7757 next. On the upside, above 0.8305 minor resistance will turn intraday bias neutral again.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8713) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.

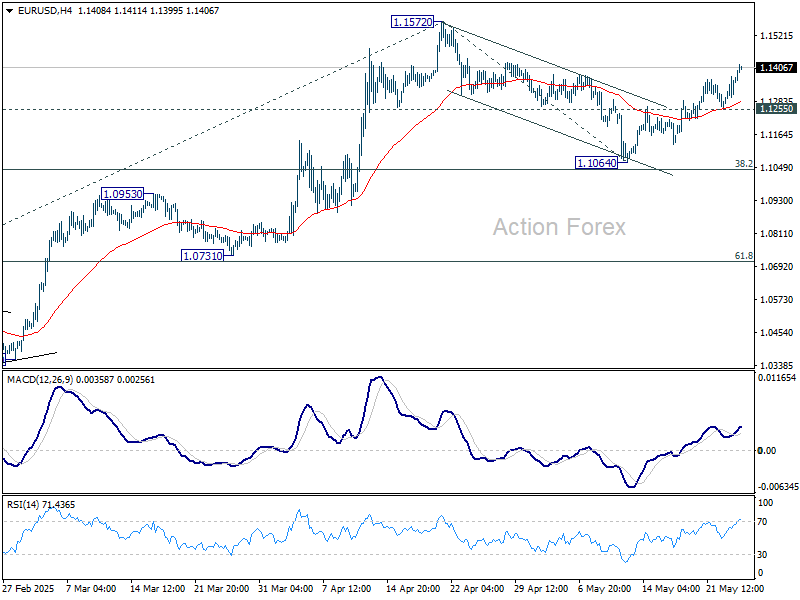

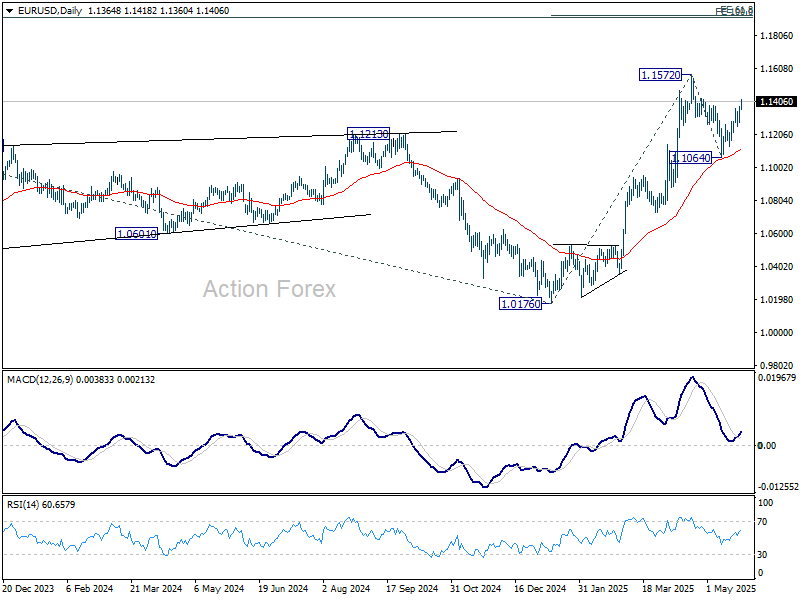

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1303; (P) 1.1339; (R1) 1.1402; More...

Intraday bias in EUR/USD remains on the upside as rise from 1.1064 is in progress for retesting 1.1572. Decisive break there will resume larger up trend to 61.8% projection of 1.0176 to 1.1572 from 1.1064 at 1.1927. On the downside, below 1.1255 minor support will turn intraday bias neutral again first.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0858) holds.

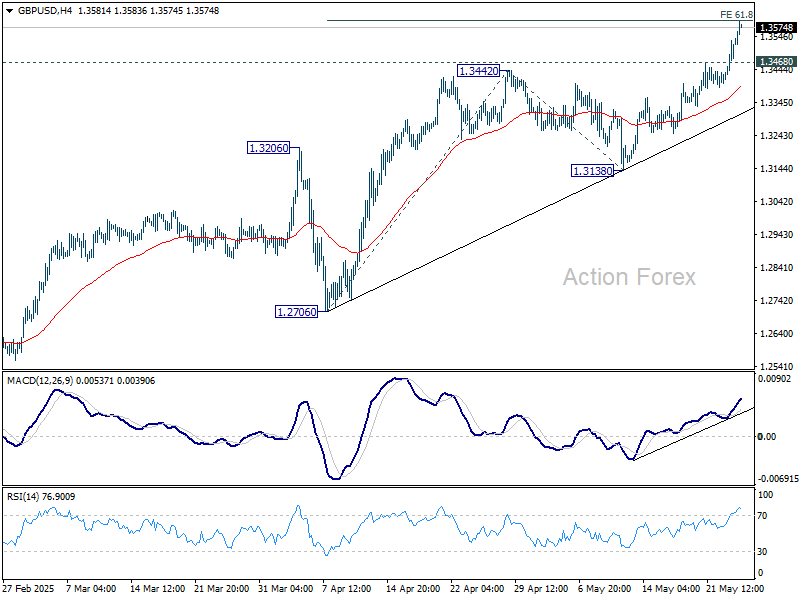

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3451; (P) 1.3496; (R1) 1.3587; More...

Intraday bias in GBP/USD stays on the upside at this point. Firm break of 61.8% projection of 1.2706 to 1.3442 from 1.3138 at 1.3593 will target 100% projection at 1.3874. On the downside, below 1.3468 minor support will turn intraday bias neutral first. But retreat should be contained well above 1.3138 support to bring another rally.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.2870) holds, even in case of deep pullback.

Dollar Drops as Tariff Confusion Reignites and Trade Talks Drag On

Dollar extended its slide as the new week opened in Asia, with investors once again thrown off balance by US President Donald Trump’s unpredictable tariff messaging. The latest development sees Trump agreeing to delay the planned 50% tariff hike on the European Union to July 9, following a direct request from European Commission President Ursula von der Leyen. While that initially offered a sense of relief, markets remain unsettled by Trump’s abrupt shifts in tone, having only days ago vowed there would be “no deal” before June and called for an immediate 50% levy.

Von der Leyen’s message on social media highlighted the EU’s readiness to move the discussions forward “swiftly and decisively”, But with Trump’s prior threats still fresh in investors’ minds, confidence in any stable outcome remains low. The tariff truce extension does little to erase concerns over the longer-term outlook for transatlantic trade, especially with the US’s broader reciprocal tariff regime still in place at a baseline of 10%.

At the same time, Japan is pushing ahead with its own talks with Washington. Prime Minister Shigeru Ishiba indicated on Sunday that Tokyo aims to reach a deal by the G7 summit next month. There appears to be some traction in the bilateral dialogue, including discussions on non-tariff measures and shipbuilding cooperation. Notably, the US has expressed interest in using Japanese shipyards to repair warships, while Japan has floated the potential for collaboration on Arctic icebreakers, an area where it claims a technological edge.

However, Japan’s chief negotiator Ryosei Akazawa struck a cautious tone upon returning from his third round of discussions in Washington. He reiterated that any agreement would be contingent on all elements falling into place as a package, and that “nothing is agreed until everything is agreed.” The scheduling of the next round, including a meeting with US Treasury Secretary Scott Bessent, is still being finalized.

With US and UK markets closed for holiday and an empty data calendar to start the week, focus is squarely on trade developments and sentiment-driven flows. Later in the week, attention will turn to RBNZ, which is widely expected to cut interest rates by 25bps. FOMC minutes, US durable goods, consumer confidence, and PCE inflation data will offer critical insight too. In addition, key releases from Australia (monthly CPI and retail sales), Canada (Q1 GDP), and Japan (Tokyo CPI) will round out the week. But given the pace of political developments on trade, economic figures may take a back seat unless they show sharp surprises.

In the currency markets, Dollar is at the bottom of the board, followed by Yen and Swiss Franc. Kiwi is leading gains, followed by Aussie and Euro. Sterling and Loonie are more mixed, hovering around the middle.

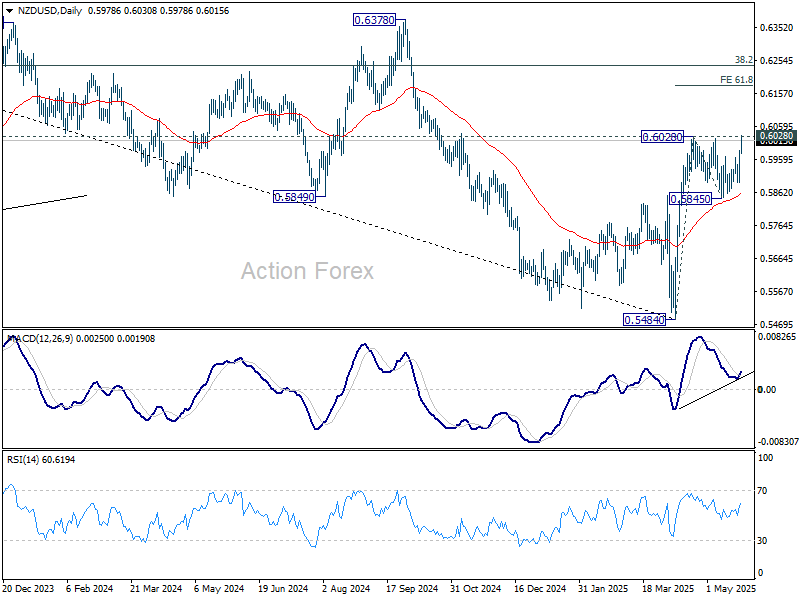

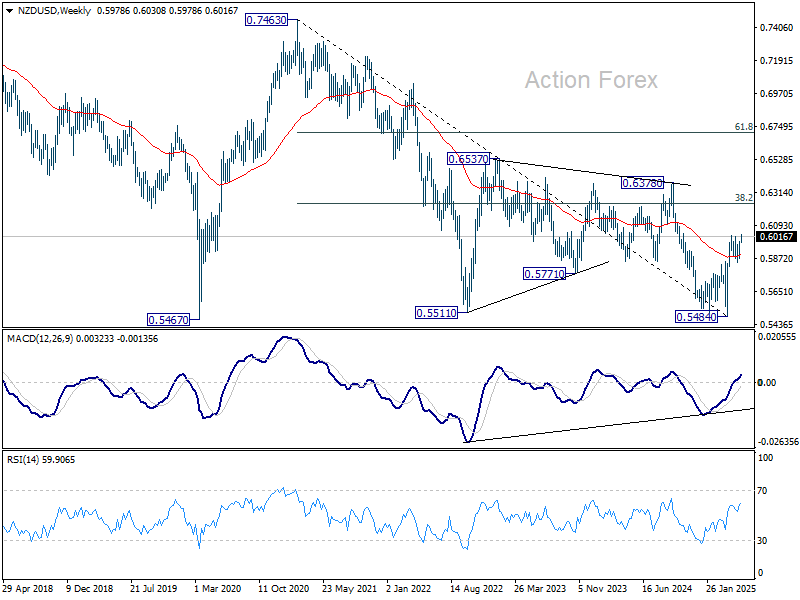

Technically, with today's rally, immediate focus is now on 0.6028 resistance in NZD/USD. Decisive break there will resume the rise from 0.5484 and target 61.8% projection of 0.5484 to 0.6028 from 0.5845 at 0.6181. Nevertheless, the real test for NZD/USD's medium term outlook is on 38.2% retracement of 0.7463 (2021 high) to 0.5484 at 0.6240.

In Asia, at the time of writing, Nikkei is up 0.83%. Hong Kong HSI is down -0.98%. China Shanghai SSE is down -0.18%. Singapore Strait Times is down -0.43%. Japan 10-year JGB yield is down -0.007 at 1.542.

Fed Kashkari: Uncertainty to delay policy at least until September

Minneapolis Fed President Neel Kashkari warned today that major shifts in US trade policies are clouding the outlook for monetary policy, making it difficult for the Fed to move on interest rates before September.

While “anything is possible,” Kashkari said in an interview with Bloomberg TV, he’s unsure whether the picture will be “clear enough” by then. Much hinges, he added, on whether trade negotiations between the US and its partners yield concrete deals in the coming months, which could “provide a lot of the clarity we are looking for.”

The uncertainty, Kashkari explained, is weighing on economic activity. He emphasized the stagflationary nature of the tariff shock, noting that its impact will depend on both the scale and duration of the levies.

On financial markets, Kashkari acknowledged that rising US Treasury yields might reflect a broader reassessment by global investors about the risks of holding American assets. He suggested that the current bond market reaction could signal a new global paradigm.

RBNZ set to ease again, FOMC minutes and PCE inflation watched

RBNZ is widely expected to lower the Official Cash Rate by 25bps to 3.25% this week, continuing its cautious policy easing cycle. Q1 CPI in New Zealand surprised to the upside and may warrant a slight upward revision in near-term inflation forecasts. Nevertheless, the outlook for growth has become increasingly clouded by external trade risks. As such, the RBNZ would probably adopt a data-dependent easing bias beyond this meeting, weighing the need for further cuts against incoming global and domestic developments.

Markets will be particularly attentive to any forward guidance on July from RBNZ. A hawkish tilt, such as hinting at an openness to pause depending on how trade and inflation evolve—could dampen expectations for a follow-up cut. Nonetheless, the baseline remains tilted toward continued easing unless global risks recede or domestic data markedly improve.

In the US, the release of the FOMC minutes from the May meeting will draw scrutiny, though Fed is unlikely to deviate from its current stance. Policymakers have made clear they are in no rush to resume easing, preferring to wait for clearer signs from inflation and trade.

With the 90-day trade truce now at the halfway mark and tensions reemerging—especially with Trump's threats toward the EU, uncertainty still dominates the outlook. More clarity may arrive with Fed’s next meeting on June 17–18, when updated economic projections will be published.

Investors will also focus on key US data including durable goods orders, consumer confidence, and the core PCE price index.

Elsewhere, Australia's monthly CPI and retail sales will shed light on the pace of disinflation and consumption ahead of the RBA's July decision. Canada’s GDP, Japan’s Tokyo CPI, retail sales, and industrial output will also be important inputs for their respective central banks.

Here are some highlights for the week:

- Tuesday: Japan corporate service price; Swiss trade balance; Germany Gfk consumer sentiment; US durable goods orders, consumer confidence.

- Wednesday: Australia CPI; RBNZ rate decision; Germany import prices, unemployment; France consumer spending; Swiss UBS economic expectations; FOMC minutes.

- Thursday: New Zealand ANZ business confidence; US GDP revision, pending home sales.

- Friday: New Zealand building permits; Japan Tokyo CPI, industrial production, retail sales; Australia retail sales; Germany retail sales, CPI flash; Swiss KOF economic barometer; Eurozone M3 money supply; Canada GDP; US trade balance, personal income and spending, PCE inflation, Chicago PMI.

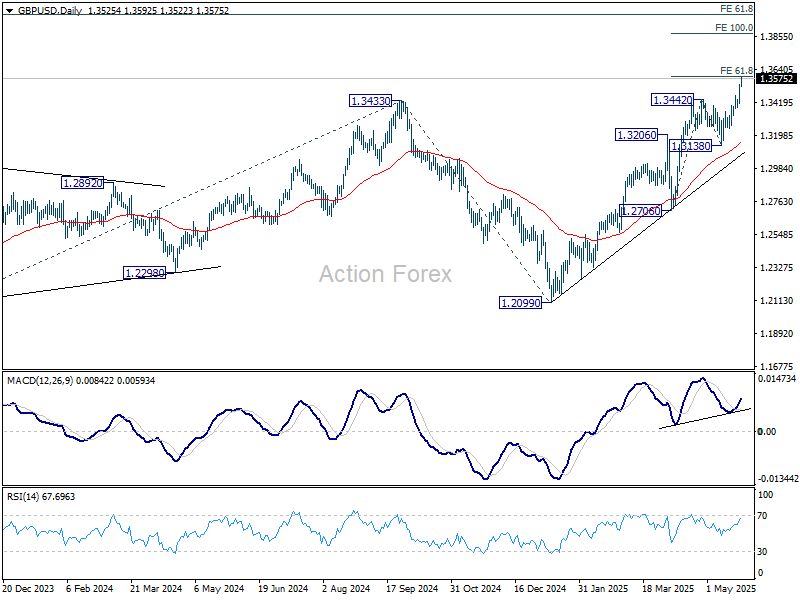

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3451; (P) 1.3496; (R1) 1.3587; More...

Intraday bias in GBP/USD stays on the upside at this point. Firm break of 61.8% projection of 1.2706 to 1.3442 from 1.3138 at 1.3593 will target 100% projection at 1.3874. On the downside, below 1.3468 minor support will turn intraday bias neutral first. But retreat should be contained well above 1.3138 support to bring another rally.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.2870) holds, even in case of deep pullback.

Fed Kashkari: Uncertainty to delay policy at least until September

Minneapolis Fed President Neel Kashkari warned today that major shifts in US trade policies are clouding the outlook for monetary policy, making it difficult for the Fed to move on interest rates before September.

While “anything is possible,” Kashkari said in an interview with Bloomberg TV, he’s unsure whether the picture will be “clear enough” by then. Much hinges, he added, on whether trade negotiations between the US and its partners yield concrete deals in the coming months, which could “provide a lot of the clarity we are looking for.”

The uncertainty, Kashkari explained, is weighing on economic activity. He emphasized the stagflationary nature of the tariff shock, noting that its impact will depend on both the scale and duration of the levies.

On financial markets, Kashkari acknowledged that rising US Treasury yields might reflect a broader reassessment by global investors about the risks of holding American assets. He suggested that the current bond market reaction could signal a new global paradigm.

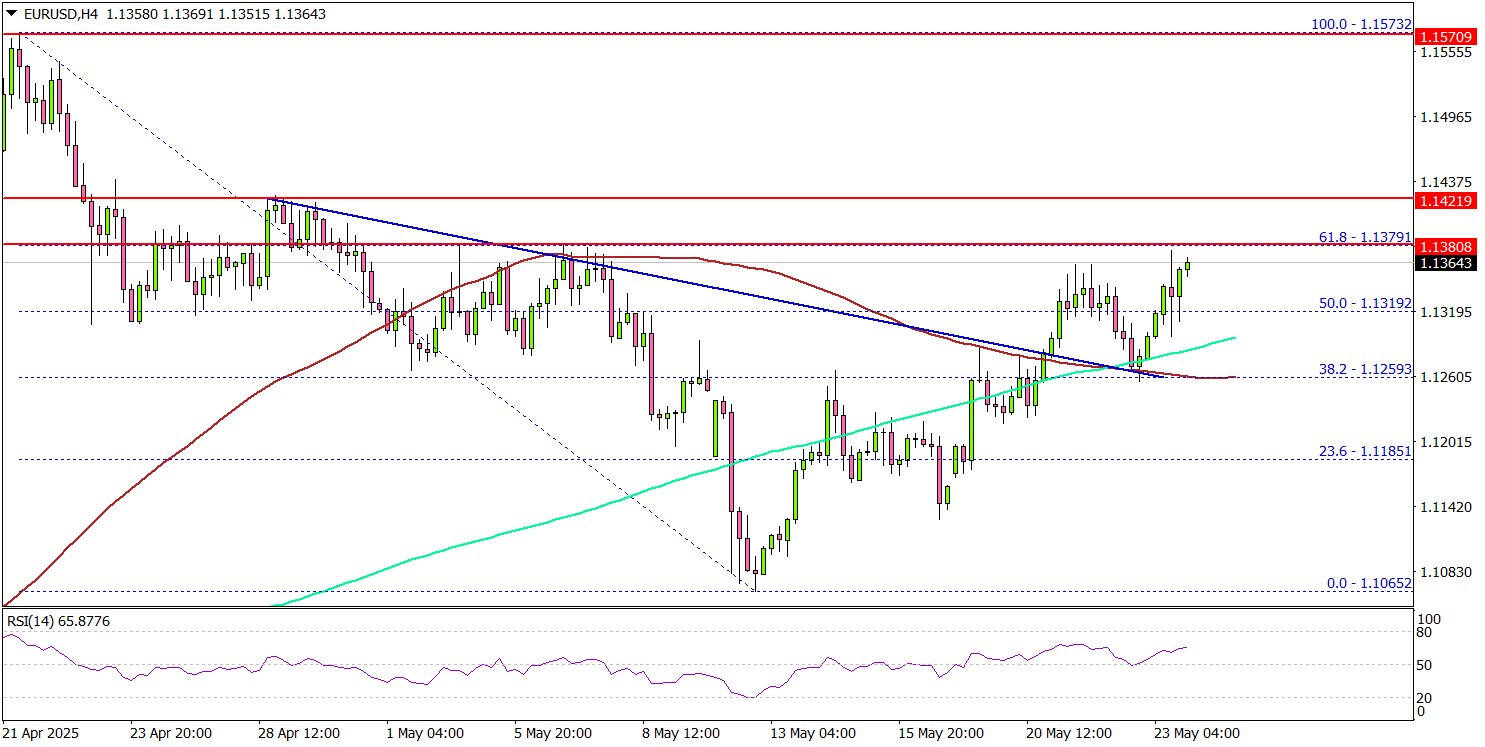

EUR/USD Regains Traction, Can It Surpass 1.1500 Again?

Key Highlights

- EUR/USD is moving higher above the 1.1320 resistance.

- It cleared a key bearish trend line with resistance at 1.1280 on the 4-hour chart.

- GBP/USD gained pace for a move above the 1.3500 level.

- USD/JPY declined steadily below the 145.00 level.

EUR/USD Technical Analysis

The Euro formed a base and started a fresh increase above the 1.1250 resistance against the US Dollar. EUR/USD even surpassed 1.1280 to enter a positive zone.

Looking at the 4-hour chart, the pair settled above the 1.1300 level, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). The pair cleared a key bearish trend line with resistance at 1.1280.

There was a break above the 50% Fib retracement level of the downward move from the 1.1573 swing high to the 1.1065 low. On the upside, the pair could face resistance near the 1.1380 level.

The next key resistance sits near the 1.1420 level. The first major resistance sits at 1.1500. A close above the 1.1500 level could set the pace for another increase. In the stated case, the pair could even clear the 1.1550 resistance. The next major stop for the bulls could be near the 1.1620 resistance.

On the downside, immediate support sits near the 1.1300 level. The next key support sits near 1.1280. Any more losses could send the pair toward the 1.1250 pivot level in the near term. The main support could be near 1.1165.

Looking at GBP/USD, the pair started a major increase and was able to clear the 1.3500 resistance zone to move into a bullish zone.

Upcoming Economic Events:

- ECB's President Lagarde speech.

- ECB's Nagel speech.

Greenback at Risk

Trouble is piling up for the US. After trade wars, fiscal issues are now weighing on the dollar. Moody’s became the latest major agency to strip the US of its highest credit rating. Lawmakers passed a controversial, sweeping tax cut bill by a slim margin. A weak auction of 20-year Treasury bonds gave rise to concerns about cooling demand for treasuries from foreign investors. Finally, threats to raise tariffs on imported iPhones to 25% and on EU goods to 50%, brought back the relevance of the early April trade with simultaneous declines in stocks, bonds and the dollar.

As a result, the ‘sell America’ trade returned with renewed vigour. Among the main casualties has been the US dollar. The White House policy has shaken confidence in it, and rumours of coordinated currency intervention after the G7 summit in Canada are stirring the imagination of USD bears. And then there are the fiscal problems. Should we be surprised by the fall of the US currency?

After the Plaza Accord in 1985, the main beneficiaries of interventions were European currencies and the Japanese yen. Now, they are EUR and JPY, with a weight in DXY of 57.6% and 13.6%, respectively, so the dollar has nothing to do but return to decline.

The retreat in the last five days after four weeks of recovery has taken the dollar index back to the area below 2023 and 2024. All eyes are now on the area of this year’s lows, which are 1.5% below current levels. A failure below them will confirm the end of the corrective rebound and the beginning of the downside momentum into the 90 area to the 2021 and 2018 lows.

GBPUSD Wave Analysis

GBPUSD: ⬆️ Buy

- GBPUSD broke multi-month resistance level 1.3430

- Likely to rise to resistance level 1.3600

GBPUSD currency pair recently broke above the key multi-month resistance level 1.3430, which stopped the previous sharp daily uptrends in September and April.

The breakout of the resistance level 1.3430 should accelerate the active impulse wave 5 from the start of May.

Given the clear daily uptrend and strongly bearish US dollar sentiment seen today, GBPUSD currency pair can be expected to rise to the next resistance level 1.3600 (the target for the completion of the active impulse wave 5).

USDCAD Wave Analysis

USDCAD: ⬇️ Sell

- USDCAD reversed from strong resistance area

- Likely to fall to support level 1.3755

USDCAD currency pair recently reversed down from the strong resistance area between the round resistance level 1.4000 intersecting with the upper daily Bollinger Band and the resistance trendline of the daily down channel from March.

The downward reversal from this resistance area started the C-wave of the active ABC correction (2).

USDCAD currency pair can be expected to fall to the next support level 1.3755 (the former low from the start of May and the target for the completion of the active ABC correction (2)).