Sample Category Title

Crypto Market Rebounds Sharply, But What’s Next?

Market Picture

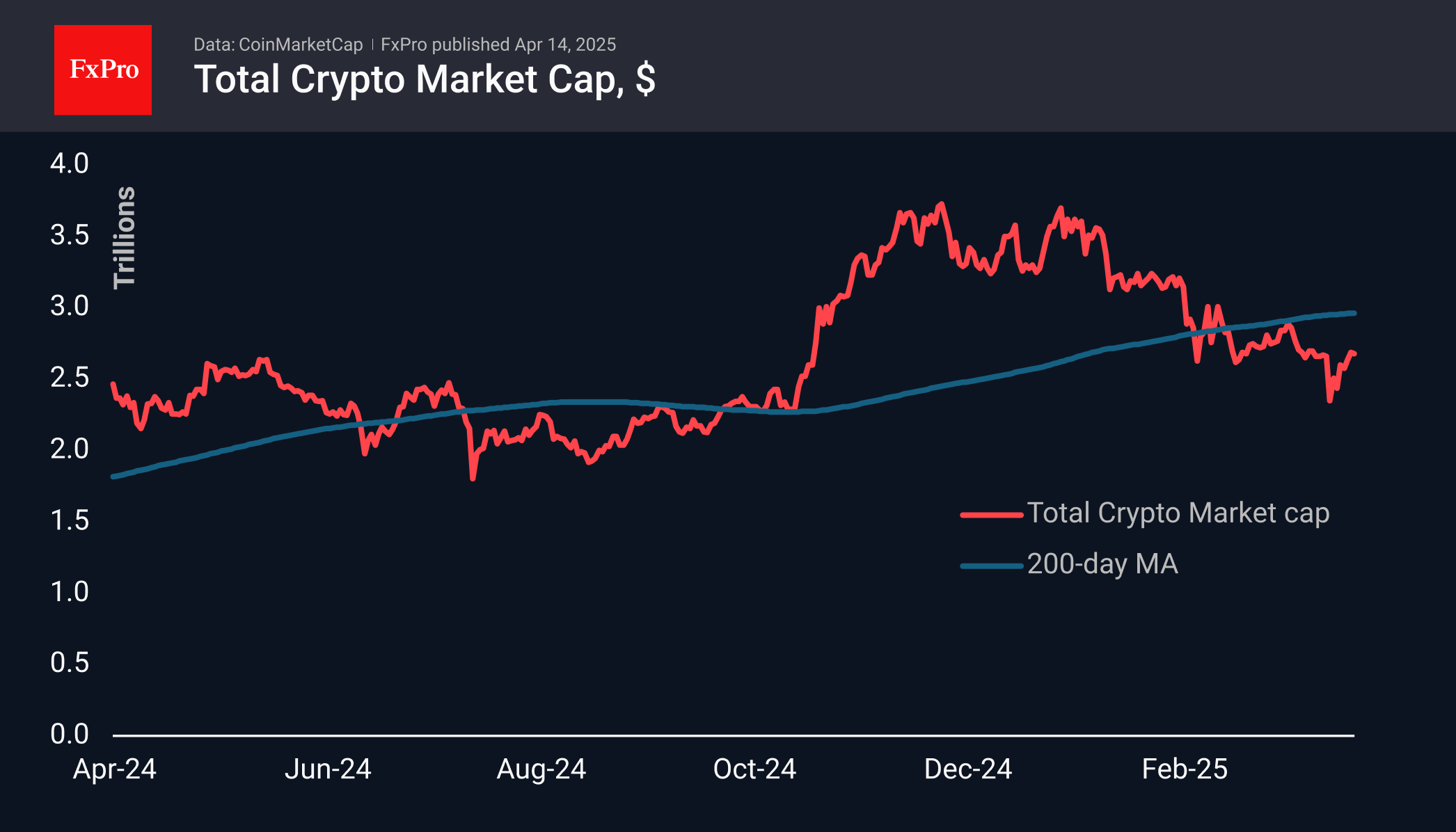

Crypto market capitalisation has risen by 13% over the past seven days, although there was no significant change over the weekend. This generally looks like a rebound after a drop. Only a rise above the local highs of $2.85 trillion will signal an upturn.

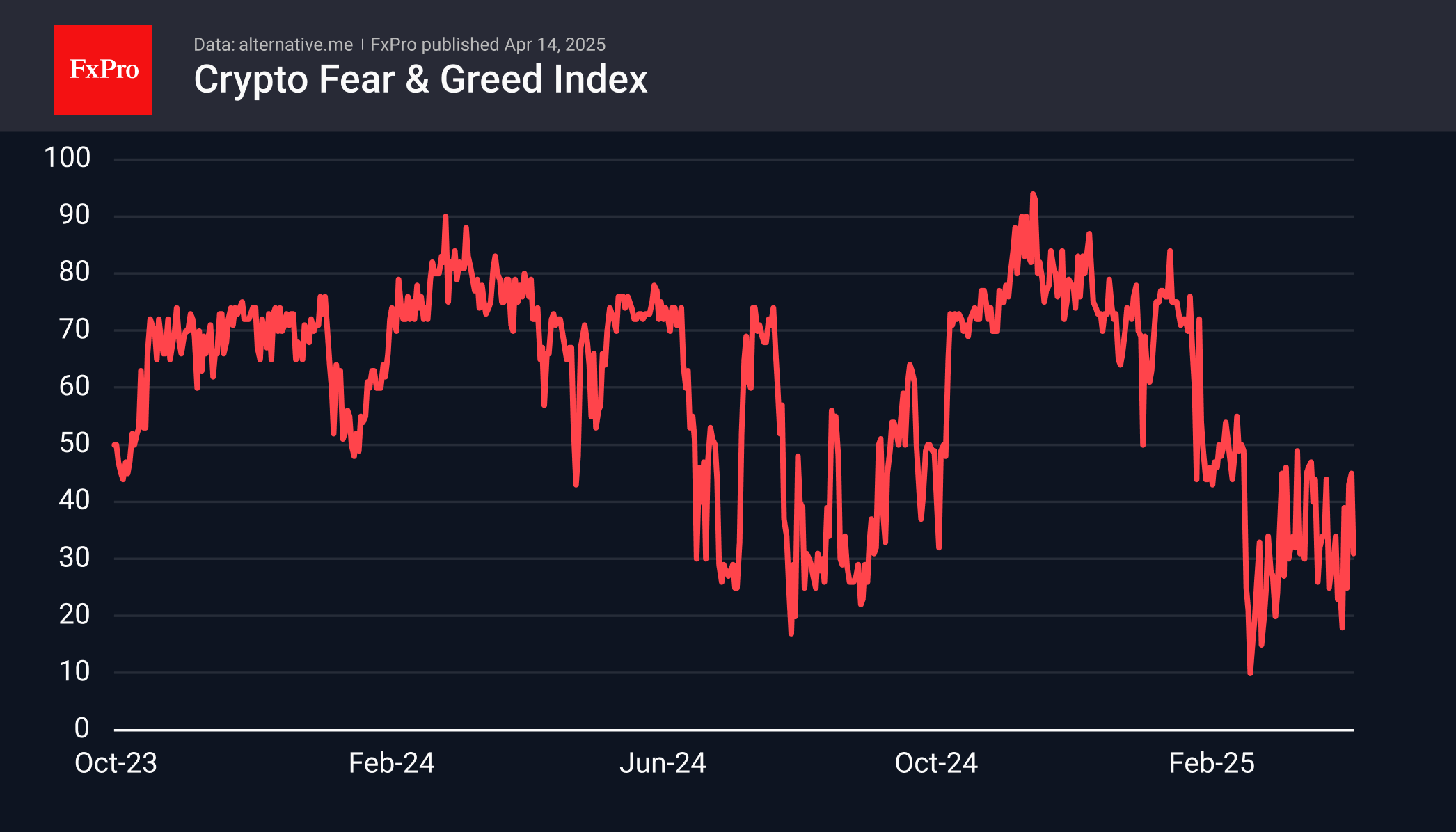

Market sentiment has moved out of the ‘extreme fear’ area into the ‘fear’ area, reaching 31. The index has been in the range of 18-45 for the last seven days, showing positive dynamics and supporting the improvement of market sentiment.

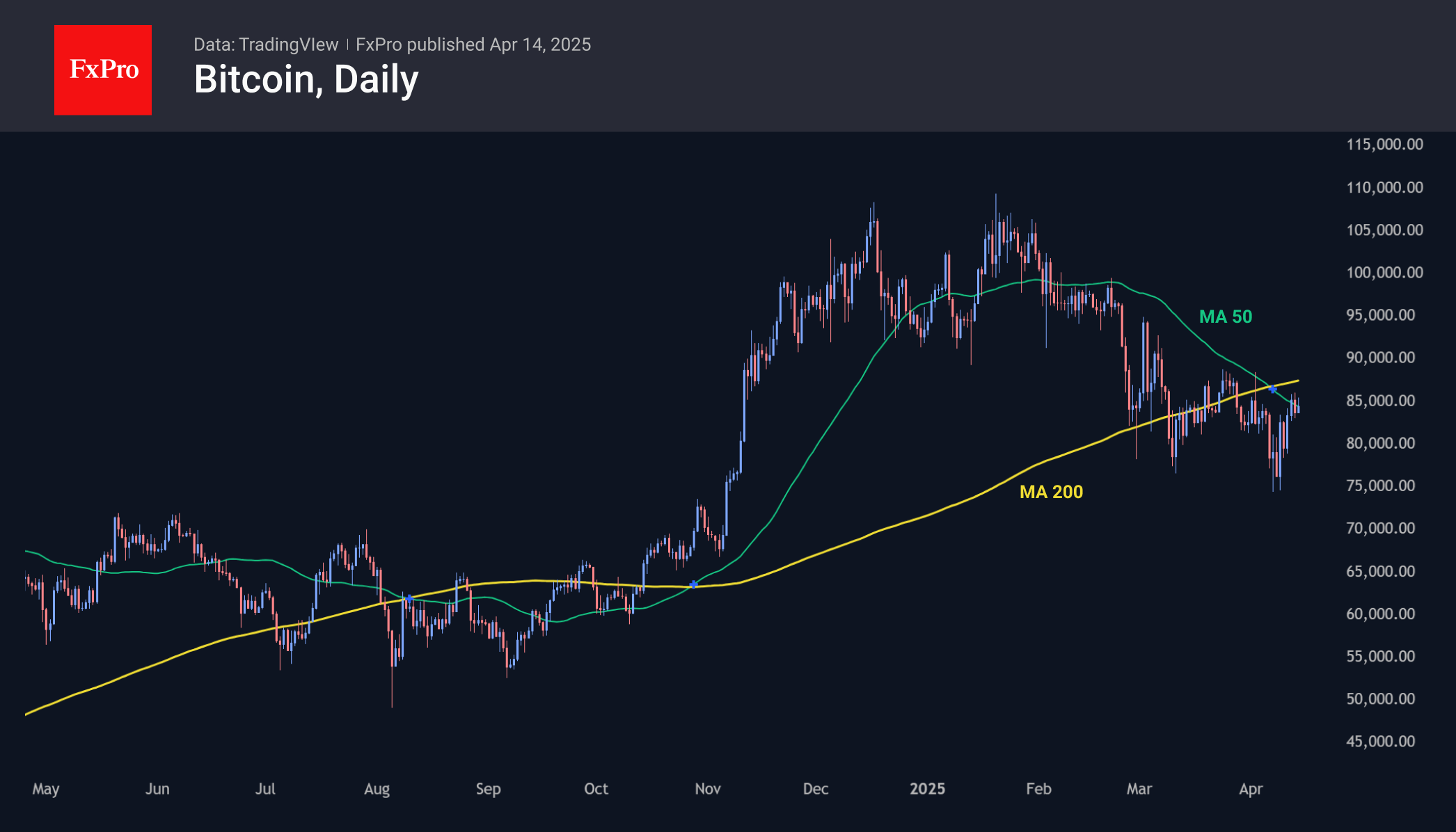

Bitcoin came close to the $85K level, making attempts to break through the 50-day moving average. A sustained consolidation above this level will be an important signal of a trend change. For long-term traders, overcoming the 200-day average, which is directed upwards and passes through $87,500, will be a more reliable reference point.

News Background

Net outflows from spot Bitcoin ETFs quadrupled last week to $713.3 million, continuing for the second week in a row, SoSoValue notes. Cumulative inflows since Bitcoin ETFs were approved in January 2024 fell to $35.36bn.

Outflows from spot Ethereum-ETFs in the US have now lasted for seven consecutive weeks, reaching $82.5 million in the past week. Since the ETF’s launch in July, cumulative net inflows have fallen to $2.28bn.

At the end of the first quarter, BlackRock’s total crypto assets under management were $50.3bn, equivalent to about 0.5% of its $11.6 trillion in total assets.

The New Hampshire House of Representatives has approved a bitcoin reserve bill. If the Senate and governor approve the document, up to 5% of the state’s funds will be dedicated to precious metals and BTC investments. In North Carolina, lawmakers proposed using cryptocurrencies as a means of payment.

Dollar Index: Limited Upticks to Precede Fresh Push Lower

The dollar edges higher on Monday as larger bears show signs of fatigue following last week’s massive losses.

Weekly close below psychological 100 support (also near Fibo 61.8% of 89.15114.72 uptrend) and probe below the floor of larger range (99.20) has generated fresh bearish signal, which requires sustained break below these levels to be confirmed, however, bears may take a breather before fresh push lower.

Long tails daily candles of past two days signal fresh bids, but bounce is unlikely to be strong, as overall sentiment remains weak and daily technical picture firmly bearish.

Solid barriers at 100 and 100.30 (psychological / broken lower boundary of larger bear channel) followed by 100.90 zone (Fibo 38.2% of 104.29/98.77 bear-leg / Apr 3 spike low) are expected to provide stronger headwinds and to ideally cap recovery upticks.

The dollar, as a safe haven asset, reacted exactly opposite to what markets expected and what was supposed to be a textbook reaction in situation of growing tensions and high uncertainty,.

Instead, the greenback lost its safe haven appeal, with Swiss franc, Japanese yen and the Euro (which took dollar’s duties and accommodated many who migrated into safety).

Following this logic, the dollar should remain under increased pressure as trade tension between the USA and China, two largest world economies) mainly offset positive signals on President Trump’s latest decision to put all remaining tariffs on hold for 90 days.

Weakening fundamentals on growing signals that the US economy is in downward trajectory with strong warnings of recession and more dovish signals on US monetary policy (markets increased bets for 3 or 4 rate cuts this year) should also contribute to dollar’s weakness.

Res: 100.00; 100.30; 100.90; 101.23

Sup: 98.90; 98.68; 98.14; 97.81

Sunset Market Commentary

Markets

Last Friday’s tariff reprieve on some consumer electronics from China entering the US was enough for a sigh of relief in the “Sell America” trade. Even though president Trump later warned that some specific levy will be announced later, European stocks still add about 2.5% while Wall Street opens with gains of up to 1.5% (Nasdaq). It’s telling of how markets are craving for any positive news and that is exactly why we’re cautious on the depth and width of the current risk on move. Either way, the incredible US Treasury sell-off took a breather as well. US yields last week ripped more than 50 bps higher at the long end of the curve. The longest tenor, 30-year, neared the symbolical 5% barrier which, if surpassed, would likely have added even more fuel to the raging fire. Yields at the start of the new week ease between 5.8 and 9.8 bps, the belly outperforming the wings. German Bunds, which acted as the preferred safe haven last week, continue to rise with net daily changes ranging from -2.3 to -6 bps and underperforming vs swap. Intra-European yield spreads ease further from their recent highs, both against Bund and swap. Italian BTPs outperform regionally, profiting from a rating upgrade to BBB+ (stable outlook) by S&P late Friday. Looking at the other side of the globe, we noticed a sharp 12 bps (!) move higher in Japan’s long-dated bond yields (30-y) to a 21-year high. At least part of the move is said to be fiscally related with rumours of the Japanese government readying another stimulus package as soon as this week to offset the negative growth impact from US tariffs. These strained government finances are also a key reason for the curve’s long end heightened vulnerability in the likes of the UK and US.

Dollar sales in fixed income markets also shifted in lower gear. The greenback still lost some ground in Asian dealings but was able to recoup most of that during the European session. DXY returned from intraday lows around 99.21 to close to but below 100. USD/JPY similarly recovered from Asian lows around 142.2 to 144. And EUR/USD’s second attempt to take out the 1.14 big figure failed with the couple currently changing hands around 1.13. Sterling catches a nice bid. EUR/GBP surged from the 0.83 area towards 0.87 in a matter of days and is currently hovering north of 0.86. The Swiss franc is the G10 underperformer, losing out both against EUR and USD. EUR/CHF rebounds to back above 0.93(3), USD/CHF above 0.82, the latter still among the lowest in 15 years.

News & Views

OPEC cut its global oil demand forecasts slightly for this year and next. They target around 150k b/d less growth, projecting an expansion of 1.3mn b/d for 2025 and 1.28mn b/d for 2026 but also adding a growing level of uncertainty surrounding the projections which are still way more than the US government’s EIA for example which eyes 900 b/d growth this year. The International Energy Agency releases an update tomorrow (currently 1.03mn b/day for 2025). The downgrade comes as US tariffs negatively impact the global economy and crude consumption. Oil demand is still expected to be supported by strong air travel demand and healthy road mobility. The downgraded growth outlook comes weeks after OPEC+ raised production levels by more than expected. Brent crude prices currently trade around $65/b, up from last week’s <$60/b bottom but still significantly below “Liberation Day” levels (>$75/b).

The European Union is set to unveil a roadmap in early May to phase out Russian fossil fuels. This plan aims to balance reducing dependency on Russian energy with lowering energy costs for industries. The roadmap, delayed due to the US's stance on Ukraine and the need for EU unity, will explore options like quotas or tariffs to cut Russian energy imports. A legal proposal will follow later. While sanctions on Russian gas are unlikely due to opposition from Hungary and Slovakia, trade measures could be adopted by a qualified majority. Despite reduced pipeline gas supplies, Russia remains a major LNG supplier to the EU, with record purchases last year by Spain, France, and Belgium.

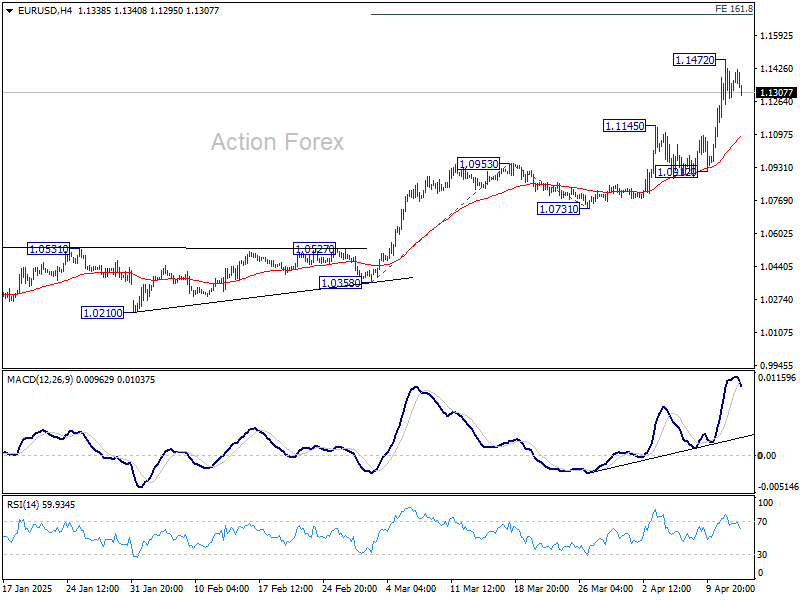

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1207; (P) 1.1340; (R1) 1.1494; More...

A temporary top is formed at 1.1472 with current retreat. Intraday bias in EUR/USD is turned neutral for consolidations first. Downside should be contained above 1.0912 support to bring another rise. On the upside, break of 1.1472 will target 161.8% projection of 1.0358 to 1.0953 from 1.0731 at 1.1694.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0745) holds.

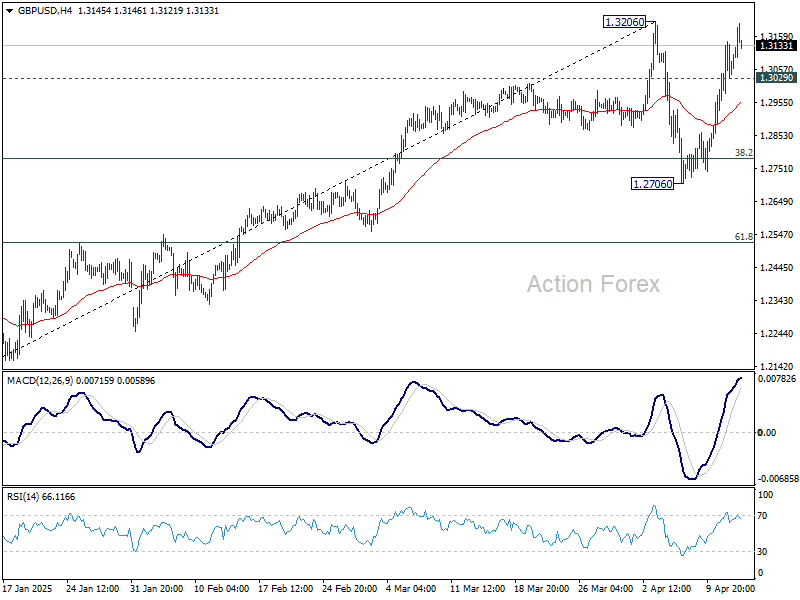

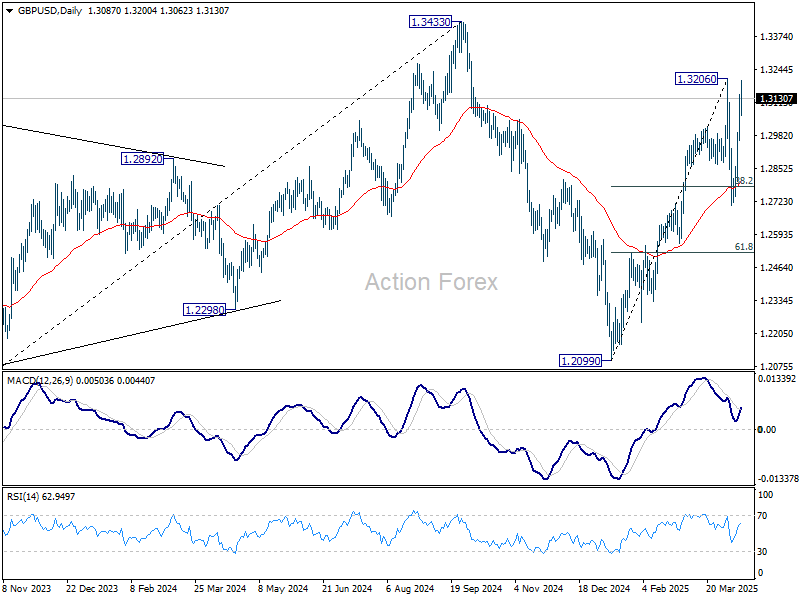

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2987; (P) 1.3067; (R1) 1.3168; More...

No change in GBP/USD's outlook and intraday bias stays on the upside. Firm break of 1.3206 resistance will will resume the rally from 1.2099 to retest 1.3433 high. On the downside, below 1.3029 minor support will turn intraday bias neutral again first. But overall near term outlook will stay bullish as long as 1.2706 support holds.

In the bigger picture, price actions from 1.3433 are seen as a corrective pattern to the up trend from 1.3051 (2022 low). Rise from 1.2099 could be the second leg. Overall, GBP/USD should target 1.4248 key resistance (2021 high) on break of 1.3433 at a later stage.

USD/JPY Daily Outlook

Daily Pivots: (S1) 142.16; (P) 143.44; (R1) 144.81; More...

A temporary low should be in place at 142.05 and intraday bias in USD/JPY is turned neutral at this point. Stronger recovery might be seen but outlook will stay bearish as long as 151.20 resistance holds. Below 142.05 will resume the fall form 158.86 to 139.57 support.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

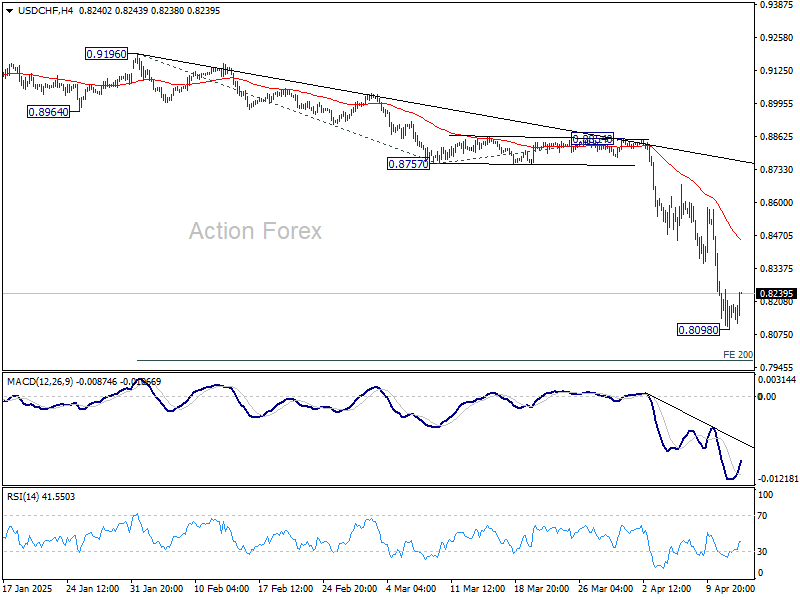

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8079; (P) 0.8173; (R1) 0.8246; More…

A temporary low is formed at 0.8098 in USD/CHF with current recovery. Intraday bias is turned neutral first for consolidations. While stronger rise might be seen, upside should be limited by 55 4H EMA (now at 0.8449) to bring another fall. On the downside, break of 0.8098 will resume recent down trend to 200% projection of 0.9196 to 0.8757 from 0.8854 at 0.7976 next.

In the bigger picture, the break of 0.8332 (2023 low) confirms resumption of long term down trend from 1.0342 (2017 high). Next target is 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9196 at 0.8075. Firm break there will target 100% projection at 0.7382.

Global Markets Rebound in Quiet Trade, Aussie Awaits RBA Insight

The global financial markets are enjoying a modest recovery today, with gains seen across Asia and Europe. US futures also point to a higher open, suggesting the bounce from last week’s dramatic selloff are having further legs. News flow is relatively light, with no major economic data releases, and tariff headlines have also slowed. The next big development on that front is expected to involve semiconductors, but traders will have to wait for details. In the meantime, markets appear to be taking a breather from the chaos.

Several Fed officials are due to speak today, though they are unlikely to provide fresh forward guidance given the highly fluid environment. Fed has so far emphasized the need for patience and data dependence, and that message is likely to be reinforced.

In the currency markets, Swiss Franc is underperforming as risk sentiment stabilizes, followed by Loonie and then Dollar. Sterling leads the day, buoyed by its risk-sensitive nature, while Kiwi and Aussie are also firm. Euro and Yen are relatively steady in the middle of the pack.

Looking ahead, RBA meeting minutes in the upcoming Asian session will be closely watched. The minutes may reiterate that the previous rate cut doesn’t necessarily start a new easing cycle. But the views may already be somewhat outdated, as the meeting occurred just before the US reciprocal tariff announcement and the subsequent market chaos. Still, they could offer insights into whether RBA board is leaning more toward inflation control or concerned about downside growth risks.

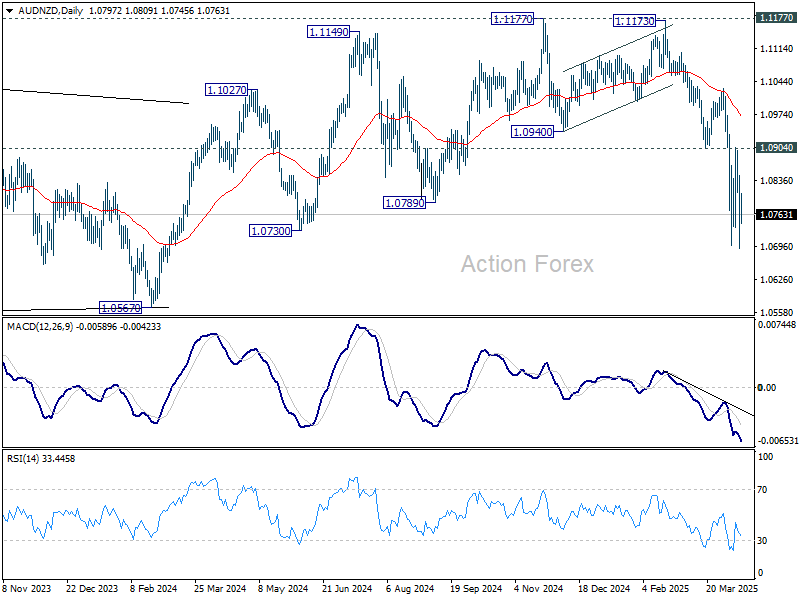

Technically, Aussie remains under pressure. It's the second-worst performer for the month, trailing only Dollar. Technically, while some extraordinarily volatility was even seen in AUD/NZD, near term outlook stays bearish with 1.0904 support turned resistance intact. Fall from 1.1177 is expected to continue to 1.0567 key medium term support next.

In Europe, at the time of writing, FTSE is up 1.78%. DAX is up 2.56%. CAC is up 2.24%. UK 10-year yield is down -0.102 at 4.665. Germany 10-year yield is down -0.051 at 2.523. Earlier in Asia, Nikkei rose 1.18%. Hong Kong HSI rose 2.40%. China Shanghai SSE rose 0.76%. Singapore Strait TImes rose 1.04%. Japan 10-year JGB yield fell -0.005 to 1.341.

OPEC trims 2025 oil demand outlook, WTI recovers mildly

OPEC has cut its forecast for global oil demand growth in 2025, now expecting an increase of 1.30m barrels per day, down -150k bpd from last month’s estimate.

In its latest monthly report, the group also lowered its projections for world economic growth for both 2024 and 2025, citing mounting uncertainties surrounding international trade policy and rising tariff tensions.

“The global economy showed a steady growth trend at the beginning of the year, however, recent trade-related dynamics have introduced higher uncertainty to the short-term global economic growth outlook,” OPEC noted.

WTI crude oil recovers mildly today. But overall development suggests that it's still in consolidations above last week's low at 55.20. Outlook will stay bearish as long as 65.24 cluster resistance holds (38.2% retracement of 81.01 to 55.20 at 65.05 holds. Larger down trend is still in favor to resume through 55.20 at a later stage.

BoJ's Ueda: US tariffs add downside risks to Japan through various channels

BoJ Governor Kazuo Ueda warned today that the recently imposed U.S. tariffs are likely to exert “downward pressure” on both the global and Japanese economies through “various channels.”

While he did not specify the transmission mechanisms, the remarks reflect growing concerns that escalating trade tensions could weigh on exports, dampen corporate sentiment, disrupt supply chains, as well as trigger volatility in the financial markets including currencies.

Ueda reiterated BoJ’s commitment to achieving its 2% inflation target sustainably, noting that monetary policy would be guided appropriately based on evolving economic, price, and financial developments. He emphasized that the central bank will maintain a data-dependent approach and continue to scrutinize conditions “without any pre-conception”.

NZ BNZ services rises to 49.1, subdued despite hints of stabilization

New Zealand’s services sector remained in contraction in March, with the BusinessNZ Performance of Services Index inching up slightly to 49.1 from 49.0. This marks another month below the long-run average of 53.0 highlighting the ongoing weakness.

While the headline improvement was minimal, underlying components showed a mixed picture—activity/sales dropped from 49.1 to 47.4. But new orders/business climbed from 49.5 to 50.8, the highest since February 2024, suggesting some pickup in future demand. Employment rose from 49.1 to 50.2, ending a 15-month streak of contraction, and offering early signs that firms may be regaining confidence in hiring.

The share of negative comments from survey participants fell slightly to 56.7%, with ongoing concerns about high interest rates, inflation, weak consumer sentiment, and broader economic uncertainty. Businesses also cited external pressures such as global tariffs and rising input costs.

China’s export surge 12.4% yoy in Mar, imports down -4.3% yoy

China's exports jumped an impressive 12.4% yoy to USD 313.9B in March, significantly beating expectations of 4.4% yoy and marking a sharp acceleration from the 2.3% yoy growth recorded in January-February.

Particularly notable was the 9.18% yoy rise in shipments to the US, likely due to front-loading ahead of tariff tensions. Exports to ASEAN also strengthened with 11.6% yoy growth , with double-digit growth to major partners like Thailand (27.8% yoy) and Vietnam (18.9% yoy).

However, Vietnam, a key intermediary in China's export supply chain, is now under pressure to tighten controls on the origin of goods and materials. According to a ministry document, authorities in Hanoi are urging companies to clamp down on origin fraud to avoid punitive US tariffs, highlighting growing scrutiny on Chinese goods routed through third countries.

Meanwhile, the strength in exports contrasted with a -4.3% yoy decline in imports, resulting in a larger-than-expected trade surplus of USD 102.6B.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8079; (P) 0.8173; (R1) 0.8246; More…

A temporary low is formed at 0.8098 in USD/CHF with current recovery. Intraday bias is turned neutral first for consolidations. While stronger rise might be seen, upside should be limited by 55 4H EMA (now at 0.8449) to bring another fall. On the downside, break of 0.8098 will resume recent down trend to 200% projection of 0.9196 to 0.8757 from 0.8854 at 0.7976 next.

In the bigger picture, the break of 0.8332 (2023 low) confirms resumption of long term down trend from 1.0342 (2017 high). Next target is 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9196 at 0.8075. Firm break there will target 100% projection at 0.7382.

OPEC trims 2025 oil demand outlook, WTI recovers mildly

OPEC has cut its forecast for global oil demand growth in 2025, now expecting an increase of 1.30m barrels per day, down -150k bpd from last month’s estimate.

In its latest monthly report, the group also lowered its projections for world economic growth for both 2024 and 2025, citing mounting uncertainties surrounding international trade policy and rising tariff tensions.

“The global economy showed a steady growth trend at the beginning of the year, however, recent trade-related dynamics have introduced higher uncertainty to the short-term global economic growth outlook,” OPEC noted.

WTI crude oil recovers mildly today. But overall development suggests that it's still in consolidations above last week's low at 55.20. Outlook will stay bearish as long as 65.24 cluster resistance holds (38.2% retracement of 81.01 to 55.20 at 65.05 holds. Larger down trend is still in favor to resume through 55.20 at a later stage.

EUR/USD Outlook: Major Bullish Breakout Supported Stagflation Risk in the US

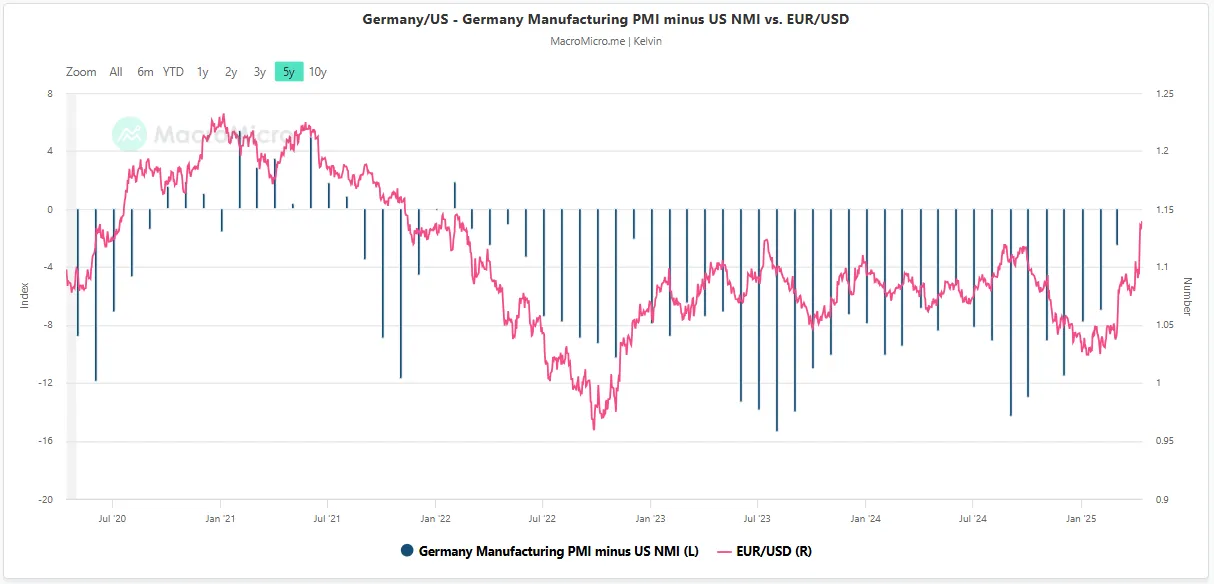

- The narrowing of the Germany Manufacturing PMI to U.S. ISM Services PMI spread suggests that Germany's growth prospects have improved relative to those of the US.

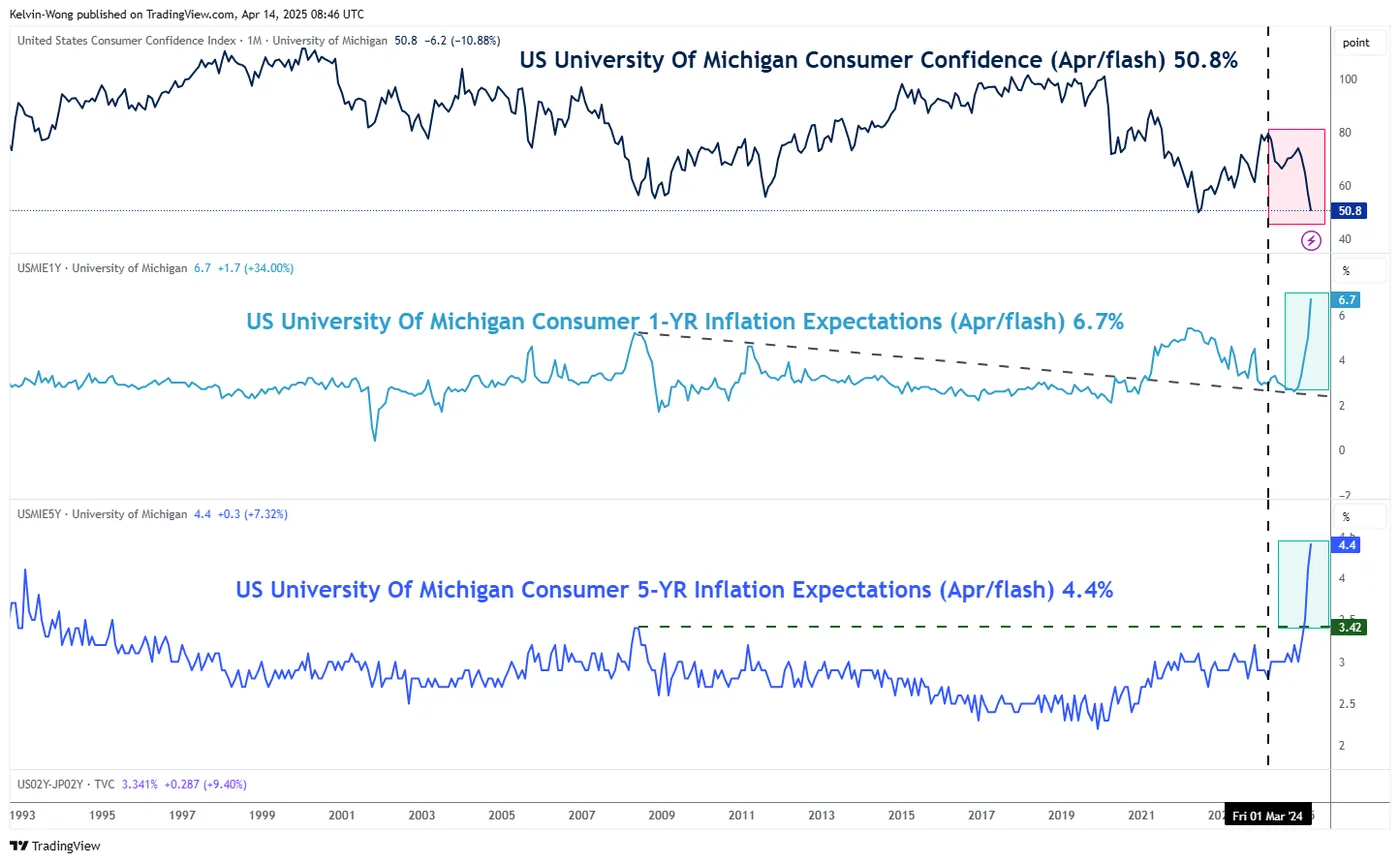

- The preliminary April data from the University of Michigan’s Consumer Sentiment survey has heightened concerns about stagflation in the U.S.

- EUR/USD rallied to a 52-week high and may have kick-started a multi-month impulsive up move sequence.

This is a follow-up analysis of our prior publication, “EUR/USD Outlook: Germany's fiscal bazooka ignites Euro bulls, but a minor pullback is imminent as ECB looms” dated 5 March 2025.

Since our last analysis, the price actions of the EUR/USD have rallied towards 1.0940 on 17 March before it staged the expected minor corrective pull-back to retest the key 200-day moving average acting as a support at 1.0730 (printed an intraday low of 1.0733 on 27 March) as highlighted.

Thereafter, the EUR/USD resumed its bullish impulsive up move sequence with a rally of 6.9% to hit a 52-week high of 1.1474 on last Friday, 11 April, on the backdrop of the uncertainty surrounding the implementation of US reciprocal and sectoral-based trade tariffs.

US dollar confidence eroded due to rising stagflation risk

Fig 1: Germany Manufacturing PMI/US ISM Services PMI ratio with EUR/USD as of 14 Apr 2025 (Source: MacroMicro)

Fig 2: University of Michigan consumer sentiment with inflation expectations as of Apr 2025 (Source: TradingView)

Following the victory of the centre-right CDU/CSU in Germany's federal election on February 23, and with newly appointed Chancellor Friedrich Merz proposing aggressive fiscal policies aimed at boosting infrastructure and defence spending, business sentiment in Germany's key manufacturing sector has improved notably. This uptick contrasts with a decline in confidence within the U.S. services sector, an essential pillar of the American economy.

Reflecting this shift, the spread between Germany’s Manufacturing PMI and the U.S. ISM Services PMI narrowed to -2.5 in March, from -7.0 in February, highlighting a relative improvement in German economic momentum (see Fig 1)

Meanwhile, consumer confidence in the U.S, a leading indicator of future retail spending—has continued to deteriorate. According to preliminary data from the University of Michigan, sentiment fell for the fourth consecutive month, dropping to 50.8 in April from 57 in March. This marks the lowest reading since June 2022.

Adding to concerns, inflation expectations among U.S. consumers have surged. One-year-ahead inflation expectations jumped to 6.7% in April, the highest since November 1981 from 5.0% in March. Long-term five-year expectations also climbed to 4.4%, the highest since June 1991, up from 4.1% in the previous month (see Fig 2)

This combination of slowing growth and persistent inflation—hallmarks of a stagflation environment, poses a significant challenge for the U.S. Federal Reserve, which may find it increasingly difficult to implement counter-cyclical monetary policies to support the economy.

As a result, global investors may begin to question the “U.S. exceptionalism” narrative that has underpinned markets over the past five years. A shift in sentiment could prompt a reallocation away from U.S. fixed income and risk assets, potentially triggering a sustained weakening trend in the U.S. dollar.

Start of a multi-month bullish impulsive up move for EUR/USD

Fig 3: EUR/USD medium-term & major trends as of 14 Apr 2025 (Source: TradingView)

The recent strong up move seen in the EUR/USD on last Friday, 11 April, where it has staged a daily and weekly close above a former long-term secular descending channel resistance from its July 2008 major swing high.

In addition, the significant rebound sequence has occurred after a retest on the key 200-day moving average on 27 March, which suggests a major bullish breakout has occurred on the EUR/USD (see Fig 3).

Watch the 1.1050/1.0940 key medium-term pivotal resistance where a potential multi-month impulsive up move sequence may unfold for the EUR/USD for the next medium-term resistances to come in at 1.1715/1.1755, and 1.1910 in the first step.

However, a breakdown below 1.0940 negates the bullish tone to expose the major supports at 1.0730 (intersection point of the 50-day and 200-day moving averages), and 1.0600.