Sample Category Title

Yen higher as JGB yield marches on, Canadian Dollar strongest for the week

Yen is trading broadly higher in Asia today as 10 year JGB yield extended recent rally. It hits as high as 0.098 and without sign of a retreat. For a bit perspective, it traded in range of 0.024/49 for most of July. And it's not close to 52 week high at 0.102.

Nonetheless, while Yen is firm today, it's limited below yesterday's high against all others for now. So, some more buying is needed to confirm underlying strength.

For the week so far, Canadian Dollar is the strongest one. The Loonie seems to be benefited most from the breakthrough in EU-US trade talk. The risk of auto tariffs is, at least for now, lessened. It's followed by Yen as the second strongest. Meanwhile, Euro and Dollar remain the two weakest one despite their trade talks.

Mexico and Canada targeting to speed up NAFTA negotiations

Canadian Dollar seemed to be benefited from the EU-US trade talks too. Trump's softened stance on auto tariffs is a positive to Canada, as well as NAFTA talks too. Canadian Foreign Minister Chrystia Freeland said after meeting with Mexican Economy Minister Ildefonso Guajardo that "Canada's very clear desire is to move the NAFTA negotiations back into higher gear now that we are past the Mexican election"

Guajardo said that "in the next few months and definitely before the election process in the United States, we are trying to constructively advance this negotiation." He is also optimistic that "there is the possibility of finding a safe landing zone."

Nonetheless, it should be noted that while the US would want to pursue bilateral agreements with Canada and Mexico, the latter two insist on trilateral agreement. Guajardo said "the essence of this agreement is trilateral, and it will continue being trilateral." Incoming Mexican Foreign Minister Marcelo Ebrard also said NAFTA "can be modernized but we're not thinking about it having a different nature to that of today."

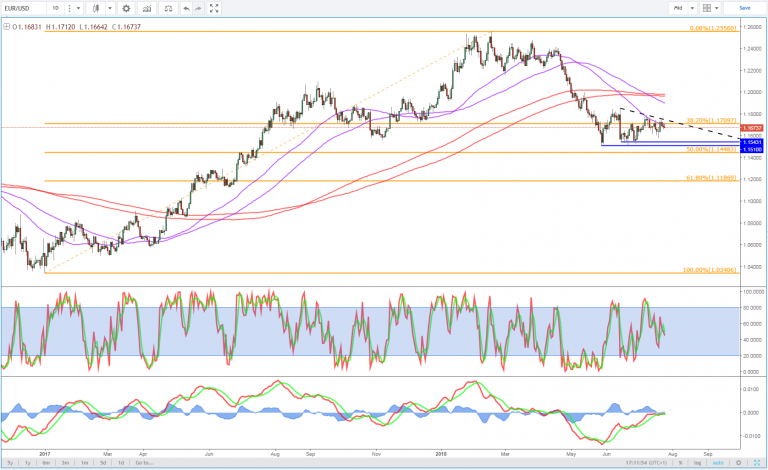

Market Morning Briefing: Euro Is Testing Resistance Near 1.174

STOCKS

Dow (25414.10, +0.68%) has clearly broken above 25250, indicating near term bullishness. While the upside momentum is in place, the index may move up towards 26000 or higher in the near term.

Dax (12579.33, -0.87%) seems to be in a whipsaw mode just now trading in the 12800-12500 region without an immediate directional clarity. While above 12500, a rise towards 12900-13000 seems possible. Else the index could drop sharply towards 12300-12200 levels in the medium term.

Nikkei (22592.23, -0.097%) has dipped slightly but could trade in the 22600-23000 region for the week. Thereafter a break on either side would trigger the further directional move next week. Currently Nikkei is trading at important levels and is yet to decide on the upcoming direction.

Nifty (11132, -0.021%) and Shanghai (2892.26, -0.39%) were both stable yesterday with no major movement. Trade in the 11200-11000 region in Nifty is likely to continue in the coming sessions while Shanghai could test resistance near 2950 before coming off from there.

COMMODITIES

Nymex WTI (69.40) and Brent (74.41) are gradually trying to move up and while the rise sustains, WTI could move up towards 71-72 while Brent could test 76+ levels in the near term.

Gold (1232.40) if sustains a rise above 1230, could head towards 1240/50 in the next few sessions. Overall near term looks bullish.

Copper (2.8395) could dip to 2.80 before again resuming the uptrend towards 2.90 and higher. Near term looks bullish.

FOREX

Dollar Index (94.165): Dollar Index is trading slightly below support near 94.2 on daily and 3 day candles. We have been expecting this support to hold in the near term and for the index to rise towards 95-96 in the next few weeks. A decisive break below 94 could negate the near term rise to 95-96. The ECB meet's outcome today could be the decider on this.

Euro (1.1736): Euro is testing resistance near 1.174 on daily and 3 day candles. 1.174 is also the 13 weeks MA and a breach of the same could make Euro bullish towards 1.185 and higher up towards the 21 weeks MA near 1.195. However, it might all depend on the ECB meet today. If the policy statement gives any indication that the 1st rate hike might happen anytime before Dec '19, it could result in Euro strengthening. If instead, the indication is for a rate hike around Dec '19, we could expect the Euro to become bearish towards 1.16.

Dollar Yen (110.76): Dollar Yen is trading slightly below support near 111 on daily, 3 day and weekly candles. There is interim support near 110.5 on daily candles and near 110 on weekly candles. Dollar Yen might still bounce back from these supports back towards 112.

Euro Yen (129.99): As per expectation, Euro Yen did test support near 129.4 on daily and 3 day candles yesterday and now seems to be rising from the support. If we assume that Euro could strengthen after the ECB meet today, near term targets of 1.18 on Euro and 111 on Dollar Yen provide a target near 131 on Euro Yen, which is likely in the next 1-2 sessions.

Pound (1.3202): As per expectation, Pound is very close to resistance on daily candles near 1.32. If the Euro strengthens towards 1.18 today, we might just see the Pound breach resistance near 1.32 and move higher. The 89 weeks MA near 1.3128 is also giving decent support to the Pound. This upmove could be a temporary upward correction in the broader downtrend for the Pound.

Dollar Rupee (68.785): Support at 68.70-65 on Dollar Rupee could break on the back of strength in the Yuan. A hold of the support however would take Dollar Rupee towards 69.10.

INTEREST RATES

News of the US President having succeeded in getting some trade concessions from the EU have lifted US yields. This is in addition to the bullish impact (on yields) of the speculation that the Bank of Japan might be rethinking its interest rate targets.

As mentioned yesterday, German 10 year yield (0.4%) is rising towards resistance near 0.45%-0.50% on short term chart and the ECB meeting today might help in this upmove. However, if the ECB's policy statement has a dovish tilt, the German 10 year yield might not rise till 0.45% and may instead drop towards 0.3%-0.2% again.

Repeating yesterday's comment on Japanese yield spreads: Japanese 30-5 Year yield spread (0.90%) has broken above resistance on medium term chart and could now find higher resistance near 0.92%-0.93%. Similarly, the Japanese 10-5 yield spread (0.187%) has also shot up from support and is testing crucial resistance on short term chart. If this resistance breaks, it might be a signal of further bullishness in Japanese 10 year yield.

US 10 year yield (2.96%), 30 Year (3.09%), 5 Year (2.84%), 2 Year (2.66%): The US 10 year yield is moving in the 2.95%-3.00% resistance zone. The longer the 10 year yield stays below this zone, the greater the chances of another correction towards 2.80%-2.75%.

EU-US statement on trade well received, but scepticism remains

The joint statement of Juncker and Trump is well received by both sides in general. .The Alliance of Automobile manufacturers said the announcement "demonstrates that bilateral negotiations are a more effective approach to resolving trade barriers, not increasing tariffs." German Economy Minister Peter Altmaier tweeted that "breakthrough achieved that can avoid trade war and save millions of jobs! Great for global economy."

But Eric Schweitzer, president of the German Chambers of Industry and Commerce appeared to be a bit skeptical. He said "the proposed solutions move in the right direction, but a significant portion of scepticism remains." He emphasized that "only united as Europeans do we have sufficient economic and political weight to effectively represent our interests." And Schweitzer warned that "without strong European answers, there is a danger that only we will make concessions and in response face new unreasonable demands from the USA."

EU-US trade war temporarily averted as Trump made major concession

European Commission President Jean-Claude Juncker's meeting with US President Donald Trump seemed to have achieved a breakthrough that could avoid a full-blown EU-US trade war. A rather positive joint statement was issued pledging to work towards "zero tariffs, zero non-tariff barriers, and zero subsidies on non-auto industrial goods". This is taken well generally by both sides.

While the auto tariffs were not mentioned in the joint statement, Juncker later said that the Trump made a "major concession" for holding off on further tariffs, including autos, as long as the negotiations continue. Juncker said he expected Trump to follow through on it. Also, he noted that Trump agreed to reassess the measures in the steel and aluminum sector.

On the other hand, Trump hailed that "a breakthrough has been quickly made that nobody thought possible!" He also told reports that EU is going to start to "buy a lot of soybeans". Trump also said "they're going to be a massive buyer of LNG... and we have plenty of it".

EU-US joint statement to lower tariffs and barriers, target China for unfair practices

Below is the full text of the joint statement following the meeting between European President Jean-Claude Juncker and US President Donald Trump. In short, both sides agreed to strengthen the trade relationship and make trade fairer and more reciprocal. The agreed to worked together toward " zero tariffs, zero non-tariff barriers, and zero subsidies on non-auto industrial goods" and increase trade and services, soybeans and other products. The agricultural sector will be opened and energy partnership strengthened.

And, both sides agreed to join forces against "unfair global trade practices". And specifically, they the practices include "intellectual property theft, forced technology transfer, industrial subsidies, distortions created by state owned enterprises, and overcapacity." That's exactly talking about China.

Here is the full statement.

Joint U.S.-EU Statement following President Juncker's visit to the White House

We met today in Washington, D.C. to launch a new phase in the relationship between the United States and the European Union – a phase of close friendship, of strong trade relations in which both of us will win, of working better together for global security and prosperity, and of fighting jointly against terrorism.

The United States and the European Union together count more than 830 million citizens and more than 50 percent of global GDP. If we team up, we can make our planet a better, more secure, and more prosperous place.

Already today, the United States and the European Union have a $1 trillion bilateral trade relationship – the largest economic relationship in the world. We want to further strengthen this trade relationship to the benefit of all American and European citizens.

This is why we agreed today, first of all, to work together toward zero tariffs, zero non-tariff barriers, and zero subsidies on non-auto industrial goods. We will also work to reduce barriers and increase trade in services, chemicals, pharmaceuticals, medical products, as well as soybeans.

This will open markets for farmers and workers, increase investment, and lead to greater prosperity in both the United States and the European Union. It will also make trade fairer and more reciprocal.

Secondly, we agreed today to strengthen our strategic cooperation with respect to energy. The European Union wants to import more liquefied natural gas (LNG) from the United States to diversify its energy supply.

Thirdly, we agreed today to launch a close dialogue on standards in order to ease trade, reduce bureaucratic obstacles, and slash costs.

Fourthly, we agreed today to join forces to protect American and European companies better from unfair global trade practices. We will therefore work closely together with like-minded partners to reform the WTO and to address unfair trading practices, including intellectual property theft, forced technology transfer, industrial subsidies, distortions created by state owned enterprises, and overcapacity.

We decided to set up immediately an Executive Working Group of our closest advisors to carry this joint agenda forward. In addition, it will identify short-term measures to facilitate commercial exchanges and assess existing tariff measures. While we are working on this, we will not go against the spirit of this agreement, unless either party terminates the negotiations.

We also want to resolve the steel and aluminum tariff issues and retaliatory tariffs.

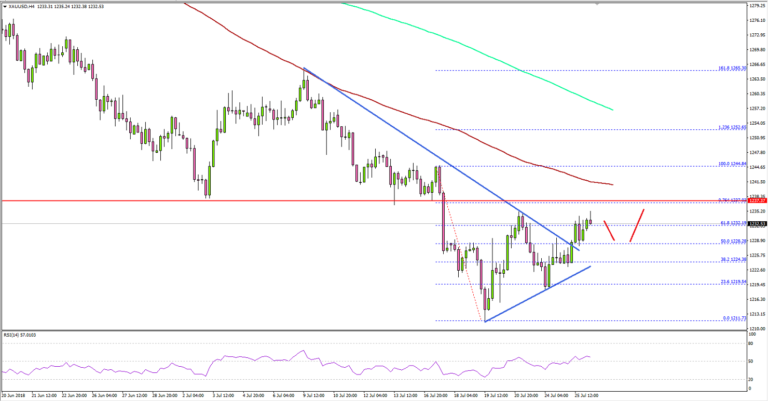

Gold Price Remains In Downtrend Below $1,240

Key Highlights

- Gold price declined heavily and traded towards $1,210 before correcting higher against the US Dollar.

- There was a break above a major bearish trend line with resistance near $1,228 on the 4-hours chart of XAU/USD.

- The US New Home Sales in June 2018 decreased 5.3% (MoM), more than the forecast of -2.8%.

- Today in the US, the Initial Jobless Claims will be released, which is forecasted to increase from 207K to 215K.

Gold Price Technical Analysis

There were heavy declines in gold price during the past few days below $1,240 against the US Dollar. The price traded below the $1,230 and $1,220 support levels before it found support near $1,210.

The 4-hour chart of XAU/USD indicates that the price traded as low as $1,211 before buyers appeared. Later, the price started an upward correction and moved above the 50% Fib retracement level of the last decline from the $1,244 high to $1,211 low.

Moreover, there was a break above a major bearish trend line with resistance near $1,228 on the same chart. The price is currently showing a few positive signs above the $1,220 level.

However, there are many hurdles on the upside near the $1,240 level, which was a support earlier. It now coincides with the 76.4% Fib retracement level of the last decline from the $1,244 high to $1,211 low.

Only a close above the $1,240 level could open the doors for a larger recovery in gold in the near term. If not, the price may resume its decline once the current correction is over.

Recently in the US, the number of New Home Sales in June 2018 was released by the US Census Bureau. The market was looking for a decline of 2.8% in sales compared with the previous month.

However, the result was below the market forecast, as there was a decline of 5.3% in the US New Home Sales. Moreover, the last reading was also revised down from +6.7% to +3.9%.

The US Dollar was under pressure after the release, and pairs like EUR/USD and GBP/USD moved higher. Gold price also moved higher and traded towards $1,234.

Economic Releases to Watch Today

- Germany’s GfK Consumer Confidence for August 2018 – Forecast 10.7, versus 10.7 previous.

- ECB Interest Rate Decision – Forecast 0%, versus 0% previous.

- US Initial Jobless Claims – Forecast 215K, versus 207K previous.

- US Durable Goods Orders for June 2018 – Forecast +3.0% versus -0.6% previous.

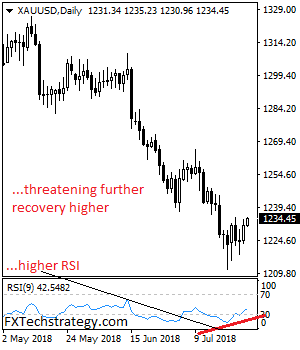

GOLD – Faces Further Recovery Threats

GOLD - The commodity looks to recover higher after closing higher on Wednesday. On the downside, support comes in at the 1,220.00 level where a break will turn attention to the 1,210.00 level. Further down, a cut through here will open the door for a move lower towards the 1,200.00 level. Below here if seen could trigger further downside pressure targeting the 1,190.00 level. Conversely, resistance resides at the 1,240.00 level where a break will aim at the 1,250.00 level. A turn above there will expose the 1,260.00 level. Further out, resistance stands at the 1,270.00 level. All in all, GOLD looks to strengthen further.

Will ECB Offer Any Surprises on Thursday?

Euro climbs ahead of ECB meeting

While we may not look back at the ECB meeting on Thursday as one of the defining moments in the eurozone’s long recovery from the global financial and debt crises, or even remember it much at all for that matter, that doesn’t mean there won’t be anything to take away from it, or that markets won’t react.

- ECB left little to the imagination in June

- Never a good idea to assume an uneventful meeting

- Will Draghi succeed in talking down the euro again?

At its meeting last month, the ECB laid out plans for its bond buying program (quantitative easing) beyond the current expiry date of September, opting to extend it until the end of the year at half the pace – €15 billion – and warned that interest rates will remain at present levels “at least through the summer of 2019”.

In providing such a clear path for asset purchases and interest rates for the next year, the central bank effectively covered all bases and barring a significant shift in the data or a change in the global landscape, left few questions if any to be answered, making this meeting a potential non-event.

Should we ever anticipate a “non-event”?

One thing we’ve learned in the past though is not to become complacent when the central banks are involved and in the current environment of trade conflicts and Brexit, things can change very quickly. We have to remember that while the recovery is gathering momentum and making encouraging progress, it is still fragile and could be derailed by a number of events which would require the ECB to step back in and offer its support.

Only this week it has been reported that US President Donald Trump intends to slap 25% tariffs on European auto imports and significantly escalate the trade conflict between the US and EU. Jean-Claude Juncker is currently in Washington looking to calm the growing tensions between the two but it seems that unless he is offering concessions, he may not get very far.

What’s more, the UK and EU don’t appear to be getting much closer to agreeing on the divorce and with eight months to go until exit day, this is a notable downside risk for both economies, with the IMF recently warning that a no-deal Brexit that sees the two revert to WTO rules could wipe 1.5% and 4% off EU and UK output, respectively, by 2030.

In terms of the data, the ECB will likely be relatively content, with unemployment continuing to drop – now at 8.4%, the lowest since December 2008 – the economy growing well despite the dip in the first quarter and inflation gradually increasing, albeit less so on from a core perspective. Nothing has really changed on this front since the last meeting that will concern policy makers.

While the euro has been climbing over the course of the last month, after falling following the ECB announcement and very dovish accompanying statements, it’s now only trading back where it was before the meeting which will be a relief to policy makers. It will be interesting to see if anything they say changes this or if Draghi focuses on talking it lower once again.

British Pound Shrugs off Strong Retail Sales Report

The British pound is unchanged in the Wednesday session. In the North American session, the pair is trading at 1.3141, down 0.02% on the day. On the release front, British CBI Realized Sales dropped to 20, but still beat the estimate of 16 points. In the U.S, New Home Sales dropped sharply to 631 thousand, well off the estimate of 669 thousand.

Retail sales growth remained strong in July at 20 points, although it was weaker than the sizzling release of 32 points in June, which was largely due to the unseasonable heat wave. However, the indicator is expected to drop in August. On Tuesday, manufacturer orders showed strong growth for a second straight month, with a reading of 11 points. The CBI Manufacturing Council welcomed the strong manufacturing data, but cautioned that “rising trade tensions and ongoing uncertainty over our future trade and customs arrangements are clearly taking their toll on manufacturers’ confidence and investment.” With U.S trade tariffs on EU products threatening to hurt British exports and the manufacturing sector, the markets are keeping a nervous eye on UK manufacturing indicators.

Tit-for-tat tariffs between the U.S and the EU has seen the trade relationship between them reach a low point. More tariffs could be coming, as the EU has vowed to impose $20 billion in tariffs on U.S products if the Trump administration slaps $50 billion on European goods. Will the nasty trade war worsen or will the sides pull back? There could be important developments on Wednesday, as an EU delegation led by European Commission President John-Claude Juckner meets with President Trump at the White House on Wednesday. Although the UK has one foot out the door, tariffs against the EU are having a negative impact on the British economy, and an improvement in relations between the US and the EU could boost the British pound.