Sample Category Title

Into US session: Euro and Dollar both weak ahead of Juncker-Trump meeting

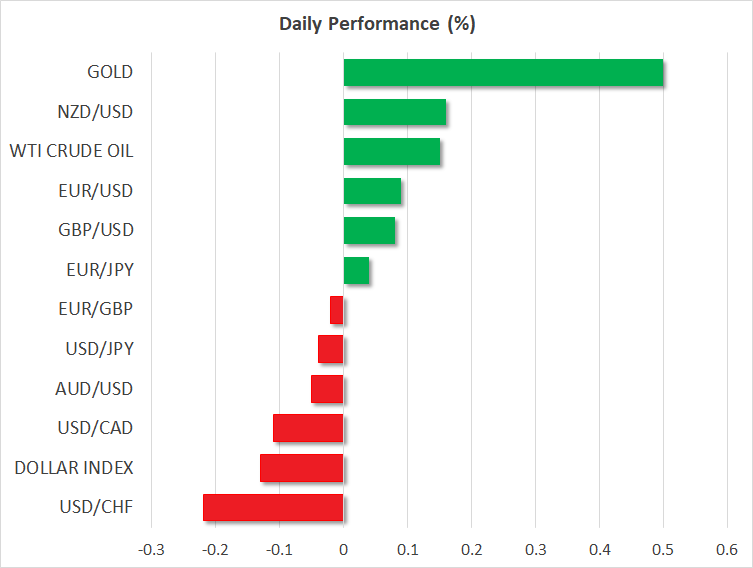

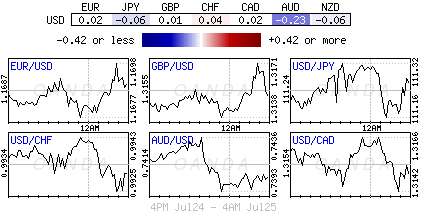

Entering into US session, Australian dollar remains the weakest one for today, as continues to be weighed down by CPI miss. Dollar and Euro are trading as the second and the third weakest one. Markets are having their eyes on the meeting between Trump and European Commission President Jean-Claude Juncker today. But it's unlikely for the "master of deal" and the "brutal killer" to achieve anything of significance. Meanwhile, Canadian Dollar and Swiss Franc are the strongest two today.

For the week, Yen remains on the strongest one so far. 10 year JGB drops slightly to 0.070 today, below this week's high at 0.090. But it's still way higher than last week's high at 0.49. Sterling is trading as the second strongest one as traders were happy with UK PM Theresa May's take over of Brexit negotiation. Euro is the weakest one followed by Australian Dollar.

Trade Tensions In Focus As Juncker Meets Trump

Here are the latest developments in global markets:

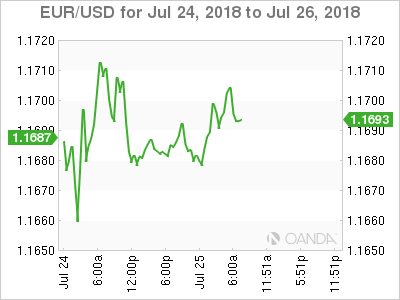

FOREX: The greenback and the single European currency barely moved on Wednesday before a meeting between US President Donald Trump and European Commission President Jean-Claude Juncker. The talks come after the US imposed tariffs on EU steel and aluminum and Trump’s recent threats to extend those measures to EU-made cars. Dollar/yen continued the bearish movement and slipped by 0.05% near 111.14, while euro/dollar jumped slightly above 1.1700 (+0.08%). The US dollar index dropped by 0.13% to 94.48. Furthermore, pound/dollar edged higher by 0.11% as Prime Minister Theresa May took control of Brexit talks yesterday. Overnight, aussie/dollar came under selling pressure after the release of Australia’s CPI data for Q2, which were a touch softer than projected. The pair managed to recover most of its losses during the European session and is currently down only by 0.05%, while kiwi/dollar advanced by 0.16%. Finally, dollar/loonie traded down by 0.10% to 1.3140.

STOCKS: European shares traded mixed on Wednesday after a green session in Asia, however, trade tensions are still in focus ahead of a meeting between Trump and Junker later in the day. The pan-European STOXX 600 moved lower by 0.04% as investors digested mixed earnings from Deutsche Bank and Banco Santander. The blue-chip Euro STOXX 50 opened lower by 0.24%, while the German DAX 30 retreated by 0.23%. The French CAC 40 gained 0.08%, while the Italian FTSE MIB 100 declined by 0.15%. The British FTSE 100 was in negative territory as well, losing 0.52%. Futures tracking US stock indices were flashing green, pointing to a positive open today.

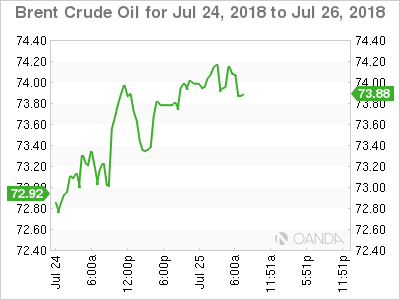

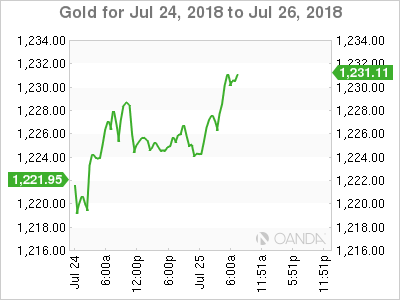

COMMODITIES: Oil prices moved higher today and are set to post the second consecutive green day after private API data yesterday showed that US crude inventories declined more than expected in the preceding week. WTI and Brent crude were both up by 0.13% and 0.87%, at $68.61 and $74.08 a barrel respectively, ahead of the release of official EIA inventory data today. In precious metals, gold prices are trying to recover some losses. The yellow metal is up by 0.5% on the day, currently hovering just above the $1230 per troy ounce mark.

Day ahead: Juncker meets Trump, all eyes on trade; corporate earnings also in focus

In a relatively light day in terms of data releases, the main event will likely be a meeting between US President Donald Trump and European Commission President, Jean-Claude Juncker in Washington. The two are expected to discuss trade, with any material comments having the capacity to affect broader market sentiment.

Juncker will likely seek a waiver of the US tariffs on EU steel imports, and Trump will look for the EU to lower its levies on US imports in general. Crucially, a failure to reach an agreement could even provoke fresh tariffs on European cars imported into America – as Trump threatened a month ago. In light of this, the stocks of popular European carmakers like Daimler and BMW will probably be extremely sensitive to any developments. Besides equities, safe-haven currencies like the Japanese yen could also be impacted, attracting inflows in case of an escalation in tensions, or coming under selling pressure on signs of a potential deal. The opposite holds true for risk-sensitive currencies like the Australian dollar. In this sense, aussie/yen looks like a good proxy for how trade tensions may play out.

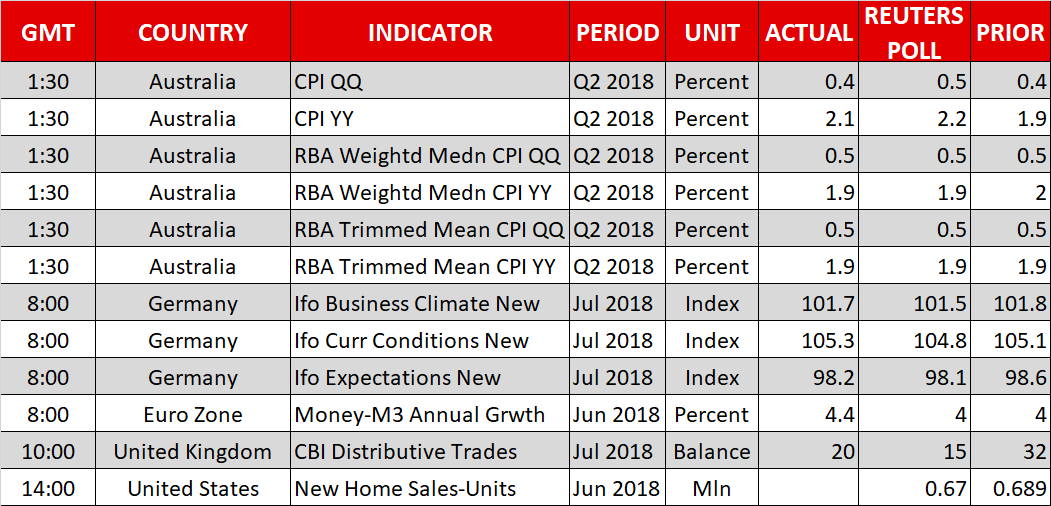

In terms of economic data, the only notable release will be US new home sales for June, due out at 1230 GMT. They are expected to have declined by 2.8%, a turnaround following a 6.7% gain in May.

Turning to equities, the earnings season continues with Boeing, Facebook, Paypal, and Qualcomm being some of the companies reporting their quarterly results today. Boeing’s earnings will go public before Wall Street’s opening bell, while the other three will report their own after the market close.

In energy markets, the weekly EIA inventory data are slated for release at 1430 GMT. The forecast is for a 2.3mn drawdown in crude stockpiles, after a 5.8mn rise in the previously tracked week.

As for other public appearances, a meeting between Canadian Foreign Minister Freeland and Mexican President-elect Obrador could attract the interest of loonie and peso-traders.

Trump And Juncker To Set The Dollar’s Tone

Wednesday July 25: Five things the markets are talking about

Euro equities have found some support, following Asian stocks as earnings season continues, although trade tensions remain to the fore ahead of today's meeting between President Trump and E.C chief Jean-Claude Junker.

Most G10 currency pairs trade in a tight range awaiting today's development from the U.S/EU meeting. In fixed income, most U.S Treasuries prices have edged a tad higher along with E.U government bonds.

Markets are struggling to build on Tuesday's upbeat session as trade relations worries between the world's biggest economic powers return to the fore.

Elsewhere, the AUD (A$0.7419) has had a mixed reaction with G20 currency pairs after inflation data missed estimates last night, backing the case for the Reserve Bank of Australia (RBA) to keep interest rates at a record low. The pound (£1.3155) is currently on to gains initiated by PM May taking control of Brexit talks.

In commodities, crude prices are higher, supported by lower inventory levels.

On tap: As the week continues, more corporate earnings come on line, while the ECB's monetary policy will be the markets focus on Thursday. On Friday, Trump and his economic team are increasingly convinced the GDP numbers will be strong – he expects Q2 GDP to rise to as much as +4.8%!

1. Stocks get the green light

Overnight, Japanese stocks rallied for a second consecutive session, supported by gains in steelmakers and metal producers, as the market welcomed China's pledges of a more forceful fiscal policy.

The benchmark Nikkei share average rallied +0.46%, expunging a significant of Monday losses on hearsay reports that the BoJ may adjust its policy at next weeks monetary policy meeting (July 30/31). The broader Topix gained +0.47%.

Down-under, Aussie stocks underperformed as the major banks faltered again following a soft CPI print. The S&P/ASX 200 fell -0.3%, with only the resources sectors showing a meaningful gains, supported by higher commodity prices. In S. Korea, the Kospi struggled overnight, barely getting back into positive territory. The benchmark fell -0.3% to move back toward its 14-month lows. Drug stocks were a noted sore point, while tech stocks eliminated those declines.

In Hong Kong, stocks rallied overnight led by the energy sector as investor sentiment improved on signs that the PBoC is loosening monetary and fiscal policies to prevent a domestic economic slowdown. The Hang Seng index rose +0.9%, while the China Enterprises Index also gained +0.9%.

In China, equities ease after three-straight days of gains. The blue-chip CSI300 index ended down -0.1% while the Shanghai Composite Index also eased -0.1%.

In Europe, regional bourses trade mixed amid another busy day for earnings.

U.S stocks are set to open in the 'red' (-0.1%).

Indices: Stoxx600 -0.1% at 388.0, FTSE -0.6% at 7659, DAX -0.2% at 12662, CAC-40 +0.2% at 5444, IBEX-35 -0.3% at 9742, FTSE MIB +0.1% at 21,897, SMI +0.1% at 9016, S&P 500 Futures -0.1%

2. Oil rises as U.S crude inventories fall, gold higher

Oil prices remain supported after U.S data yesterday showed that domestic crude inventories fell more than expected last week, easing worries about oversupply.

Global benchmark Brent crude was up +50c, or +0.7% at +$73.94 a barrel, after gaining +0.5% yesterday. U.S light crude is +5c higher at +$68.57, having risen nearly +1% in its previous session.

API data yesterday showed that U.S crude inventories fell by -3.2M barrels in the week to July 20 to +407.6M barrels. Consensus was expecting a decrease of -2.3M barrels.

Dealers will take their cues from today's DoE report (10:30 am EDT).

Ahead of the U.S open, gold prices have inched higher as the 'big' dollar held steady ahead of today's U.S and E.C meetings. Spot gold is up +0.2% an ounce. U.S. gold futures for August delivery are +0.1% higher.

3. Yields play in a tight range

Most sovereign bond yields continue to consolidate as dealers search for fresh impetus to head in a new direction. The economic calendar provides no new hints ahead of tomorrow's ECB meeting.

However, today's meeting between E.C Commission President Jean-Claude Juncker and President Trump could fuel further trade concerns, while cross-market themes and the lack of market liquidity can still provide erratic price moves.

The yield on U.S 10-year Treasuries has dipped -1 bps to +2.94%. In Germany, the 10-year Bund yield has fallen -1 bps to +0.39%, while in the U.K, the 10-year Gilt yield has decreased -1 bps to +1.264%.

4. FX markets trade sideways

The FX market trades in a tight range ahead of the today's key Trump/Juncker trade talks stateside.

The EUR/USD (€1.1703) is slightly higher, but contained within this months trading range. E.U data continues to take the back-stage ahead of tomorrows ECB policy decision.

Note: The ECB is widely expected to leave its key policy settings and guidance unchanged after it announced its plans for monetary policy beyond September last month

USD/JPY (¥111.14) is holding above the psychological ¥111 level as fixed income dealers price-in that the BoJ would not likely make any policy changes until at least October.

Elsewhere, China is letting the yuan slide primarily to combat a slackening economy, as the government rolls out more pro-growth measures amid an intensifying trade feud with the U.S.

5. German July Ifo business expectations lowest in four-months

German data this morning revealed that domestic business expectations fell further this month, albeit only marginally, according to the Ifo Institute's monthly survey.

While the Ifo measure of the current business situation improved a bit, the expectations component hit its lowest level in two-years.

The Ifo business-climate index fell to 101.7 from 101.8 in June.

Note: It marks the lowest reading in 16-months.

“The German economy continues to expand, but at a slower pace,” said Clemens Fuest, the president of the Ifo Institute.

Digging deeper, uncertainty about global trade policy remains high, with potential tariffs on the auto sector being a key concern for Germany.

DAX Slips As Markets Eye EU-US Trade Talks

The DAX index has lost ground in the Wednesday session. Currently, the DAX is at 12,627, down 0.50% on the day. On the release front, German Ifo Business Climate ticked lower to 101.7, just above the estimate of 101.6 points. On Thursday, Germany releases GfK Consumer Climate and the ECB will set its minimum bid rate.

Tit-for-tat tariffs between the U.S and the EU has seen the trade relationship between them reach a low point. More tariffs could be coming, as the EU has vowed to impose $20 billion in tariffs on U.S products if the Trump administration slaps $50 billion on European goods. Will the nasty trade war worsen or will the sides pull back? There could be important developments on Wednesday, as an EU delegation led by European Commission President John-Claude Juckner meets with President Trump at the White House on Wednesday. If the sides can make progress on car tariffs, automaker shares could jump and boost the DAX.

With the global tariff war threatening to hurt German and eurozone exports, investors have been keeping a close eye on manufacturing data. There was positive news on Tuesday, as Eurozone and German manufacturing PMIs continue to point to expansion. The German release improved to 57.3, easily beating the estimate of 55.5, while the eurozone reading of 55.1 was above the forecast of 54.7. Both indicators had dropped over six consecutive months and the July releases put an end to that nasty streak. Services PMIs were not as strong, as the German and eurozone releases missed their estimates.

EUR/USD – Euro Steady As Investors Eye Trump-Juckner Meeting

EUR/USD continues to stay close to the 1.17 level. In the Wednesday session, the pair is trading at 1.1697, up 0.11% on the day. On the release front, German Ifo Business Climate ticked lower to 101.7, just above the estimate of 101.6 points. In the U.S, New Home Sales is forecast to drop sharply to 669 thousand. On Thursday, Germany releases GfK Consumer Climate and the ECB will set its minimum bid rate. The U.S will release durable goods reports and unemployment claims.

The EU and the U.S. are engaged in a nasty trade war, and the EU has promised to impose $20 billion in tariffs on U.S products if the Trump administration slaps $50 billion on European goods. Will the trade war worsen or will the sides pull back and make up? We could be a bit wiser after an EU delegation, led by European Commission President John-Claude Juckner, meets with President Trump at the White House on Wednesday. The euro has been fairly steady in recent weeks, despite the growing trade tensions. If, however, the trade talks between Trump and Juckner fall flat, the euro could lose ground.

With the global tariff war threatening to hurt German and eurozone exports, investors have been keeping a close eye on manufacturing data. There was positive news on Tuesday, as Eurozone and German manufacturing PMIs continue to point to expansion. The German release improved to 57.3, easily beating the estimate of 55.5, while the eurozone reading of 55.1 was above the forecast of 54.7. Both indicators had dropped over six consecutive months and the July releases put an end to that nasty streak. Services PMIs were not as strong, as the German and eurozone releases missed their estimates.

Awaiting Trump-Junker Trade Meeting, German IFO Data Mixed

Notes/Observations

- German IFO data mixed; Business Climate beats expectations but still has fallen in 7 of the last 8 months

- Focus on Trump-Juncker/Malmstrom trade talks in Washington later today

Asia:

- BoJ watchers’ the central bank is not likely to make any policy changes until at least Oct 2018

- BoJ maintained its JGB purchase amounts unchanged during regular ops

- Australia Q1 CPI Q/Q: 0.4% v 0.5%e; Y/Y: 2.1% v 2.2%e; data soft despite large rise in fuel prices which left room for RBA to hold rates well into 2019

Europe:

- EU's Juncker: EU was prepared to retaliate immediately if auto tariffs were introduced; Stressed the EU was not a foe of the US

- EU Trade Min Malmstrom reiterated view of still hoping to find a solution with the US on trade; EU was preparing counter tariffs of $20B on US goods

Americas

- Mexico Incoming Foreign Minister Marcelo Ebrard: Trump disclosed in letter that the 2 countries should increase cooperation. Trump said that he agreed with the four priorities laid out by the President-elect Lopez Obrador in prior letter

- President Trump reportedly to announce billions of dollars in trade aid for farmers with size of aid package said to be ~$12B

Energy:

- Weekly API Oil Inventories: Crude: -3.2M v +0.6M prior

Economic Data:

- (FR) France Jun PPI M/M: 0.1% v 0.7% prior; Y/Y: 3.4% v 3.0% prior

- (AT) Austria May Industrial Production M/M: 1.6% v 1.0% prior; Y/Y: 6.2% v 5.9% prior

- (ES) Spain Jun PPI M/M: 1.0% v 1.3% prior; Y/Y: 4.1% v 3.0% prior

- (SE) Sweden Jun PPI M/M: 0.8% v 1.4% prior; Y/Y: 8.0% v 6.3% prior

- (EU) Euro Zone Jun M3 Money Supply Y/Y: 4.4% v 4.0%e

- (DE) Germany July IFO Business Climate: 101.7 v 101.5e; Current Assessment: 105.3 v 104.9e, Expectations Survey: 98.2 v 98.3e

- (CH) Swiss July Credit Suisse Expectations Survey: -4.0 v +8.0 prior

- (UK) Jun BBA Loans for House Purchases: 40.5K v 39.0Ke (highest since Sept)

Fixed Income Issuance:

- (IN) India sold total INR180B vs. INR180B indicated in 3-month, 6-month and 12-month bills

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 -0.1% at 388.0, FTSE -0.6% at 7659, DAX -0.2% at 12662, CAC-40 +0.2% at 5444, IBEX-35 -0.3% at 9742, FTSE MIB +0.1% at 21,897, SMI +0.1% at 9016, S&P 500 Futures -0.1%]

- Market Focal Points/Key Themes: European Indices trades mixed in consolidating trade amid another busy day for earnings. Elior, LVMH, Telefonica Deutschland, Lonza among the notble risers this morning after earnings and guidance. Dassault Systems trades lower after results, with Konecranes, Kesko and DWS among other fallers. Indivior trades sharply lower after delaying the guidance following a decline in earnings. In the M&A space Ageas trades higher after Fosun expressed interest in the company. Looking ahead notable earners include DOW components Boeing, Coca Cola alongside General Motors, UPS and General Dynamics among others.

Movers

- Consumer Discretionary Elior [ELIOR.FR] +4.6% (Earnings), TF1 [TFI.FR] +4.1% (Earnings), LVMH [MC.FR] +1.8% (Earnings), Kesko [KESKOB.FI] -6.0% (Earnings), ITV [ITV.UK] +0.8% (Earnings)

- Materials Lonza [LONN.CH] +6.1% (Earnings)

- Healthcare Indivior [INDV.UK] -20% (Delays guidance)

- Financials DWS [DES.DE] -2.2% (Earnings)

- Industrials Sulzer [SUN.CH] -3.9% (Earnings), Victrex [VCT.UK] +2.1% (Earnings), Konecranes [KCR.FI] -5.1% (Earnings)

- Technology Dassault Systems [DSY.FR] -2.7% (Earnings), Ricardo [RCDO.UK] -12% (Earnings)

- Telecom Telefonica Deutschland [O2D.DE] ++8% (Earnings)

Speakers

- Ireland Dep PM Coveney (also foreign Min) reiterated view that a 'no-deal' Brexit was unlikely to happen. Ireland would support an extension of Article 50 if UK govt asked

- German IFO Economists maintained its German 2018 GDP growth forecast at 1.8%. It noted that the construction sector was booming with sentiment at strongest level since unification. Export expectations rose for the 1st time in 7 months. US trade policy and recent German govt crisis increased uncertainty among business

- Poland Central Bank Q3 Business Condition Survey noted that domestic companies were less positive as costs could rise, signaled lower wage growth and fewer workers needed in quarter

- Russia Energy Min Novak: Russia estimate for 2018 oil output 551M tons and 2019 oil output at 555M tons

- China State Planner (NDRC): To provide policy support for workers impacted by trade frictions and structural adjustments; will not allow 'large-scale' unemployment from ongoing trade frictions with US

Currencies

- FX markets were quiet ahead of the key Trump/Juncker trade talks later Today.

- EUR/USD slightly higher but contained within the July trading range. EU data continued to take the back-stage ahead of the ECB policy decision on Thursday. ECB is widely expected to leave its key policy settings and guidance unchanged at Thursday's meeting after it announced its plans for monetary policy beyond September last month

- USD/JPY was holding above the 111 level as dealers believed that the BoJ would not likely to make any policy changes until at least Oct.

Fixed Income

- Bund Futures trades at 162.41 up 14 ticks after the latest German orders data showed a stronger than expected recovery and this helped stabilize the Ifo reading. A move back above 162.75 would target 163.47 then 163.63, with a move below 161.75 targeting 161.45 then 160.45.

- Gilt futures trades at 123.33 up 10 ticks as PM May takes control of Brexit negotiations, with continuing upside targeting 124.18 then 124.44, with a move lower seeing initial support at 123.23 then 122.85.

- Wednesday's liquidity report showed Tuesday's excess liquidity rose from €1.809T to €1.8093T. Use of the marginal lending facility fall from €100M to €50M.

- Corporate issuance saw 2 high-grade issuers raise $1.7B in the primary market

Looking Ahead

- (GR) Bank of Greece: Jun Bank Deposits: N est v €128.1B prior

- (BR) Brazil July CNI Consumer Confidence: No est v 98.3 prior

- (BR) Brazil Jun Total Federal Debt (BRL): No est v 3.717T prior

- (CO) Colombia Jun Industrial Confidence: No est v 0.5 prior; Retail Confidence: No est v 27.0 prior

- (IT) Italy Debt Agency (Tesoro) announcement on upcoming BTP auction for July 30th

- 05:30 (DE) Germany to sell €4.0B in new 0% Oct 2023 BOBL

- 05:30 (EU) ECB allotment in 3-month LTRO operation

- 06:00 (UK) July CBI Retailing Reported Sales: 15e v 32 prior; Total Distribution: No est v 18 prior

- 06:00 (FR) France Q2 Total Jobseekers: No est v 3.436M prior

- 06:00 (RO) Romania to sell €100M in Feb 2021 bonds

- 06:45 (US) Daily Libor Fixing

- 07:00 (RU) Russia to sell combined RUB35.2B in 2024 and 2028 OFZ bonds

- 07:00 (US) MBA Mortgage Applications w/e July 20th: No est v -2.5% prior

- 07:30 (TR) Turkey July Capacity Utilization: No est v 78.3% prior

- 07:30 (TR) Turkey July Real Sector Confidence (Seasonally Adj): No est v 102.5 prior; Real Sector Confidence (NSA): No est v 104.6 prior

- 08:05 (UK) Baltic Dry Bulk Index

- 09:00 (BE) Belgium July Business Confidence: 0.4e v 0.6 prior

- 09:00 (MX) Mexico May Retail Sales M/M: +0.5%e v -1.1% prior; Y/Y: 1.9%e v 3.3% prior

- 09:45 (UK) BOE to buy £955M in in APF Gilt purchase operation (7-10 years+)

- 10:00 (US) Jun New Home Sales: 668Ke v 689K prior

- 10:30 (US) Weekly DOE Crude Oil Inventories

- 11:30 (US) Treasury to sell 2-Year Floating Rate Notes Reopening

- 12:00 (CA) Canada to sell 10-year notes

- 13:00 (US) Treasury to sell 5-Year Notes

- 13:30 (US) President Trump’s meets EU Commission President Juncker

- 15:00 (AR) Argentina July Trade Balance: -$0.6Be v -$1.3B prior

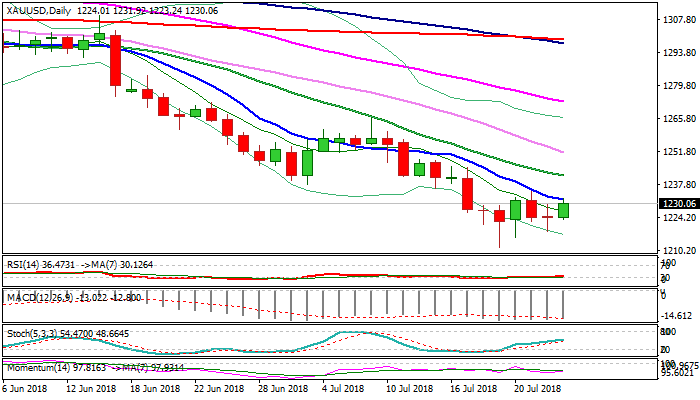

XAUUSD Outlook: Fresh Advance Could Extend On Break Of $1232/35 Pivots

Spot Gold advanced on Wednesday as the greenback eased ahead of meeting between US president Trump and EU Commission President Juncker on trade-focused talks, due today. The yellow metal rose around $9 for the session and pressures pivotal barriers at $1232 (falling 10SMA/Fibo 38.2% of $1265/$1211 bear-leg), looking for stronger bullish signal on break here and nearby lower top of 23 July at $1235. North-heading daily indicators are supportive, but falling MA's in firm bearish setup warn of possible recovery stall as overall structure remains bearish. Failure to close above $1232/35 would generate initial warning that rally might be running out of steam, with return below session low ($1223) to signal reversal. Bullish scenario on break above $1232/35 would open way for extension towards Fibo targets at $1238/45 (50% and 61.8% of $1265/$1211 fall respectively).

Res: 1232, 1235, 1238, 1245

Sup: 1226, 1223, 1218, 1215

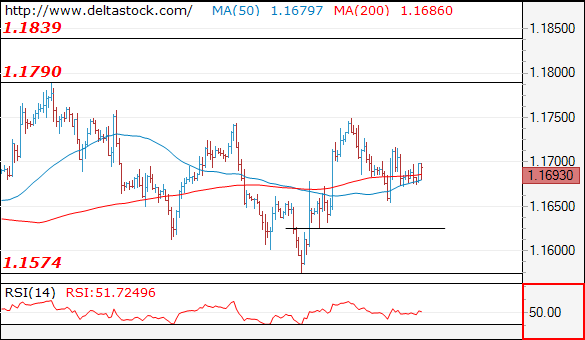

EURUSD Muted Ahead Of Key Risk Events

The euro continues to trade with a cautious tone against the US dollar as traders await US President Donald Trump’s meeting with EU trade negotiator Jean-Claude-Juncker in Washington. The EUR/USD pair looked past stronger than expected German IFO survey for the month of July during today’s European trading session. Buyers need sustained gains above the 1.1724 resistance level, while sellers simply need to hold price below the 1.1650 level.

The EURUSD pair is only intraday bullish while trading above the 1.1724 level, key resistance above the 1.1724 level is found at the 1.1750 and 1.1790 levels.

If the EURUSD pair holds price below the 1.1650 level, key support remains at the 1.1630 and 1.1600 technical levels.

USDJPY To Weaken Below 110.87 Support Level

The US dollar continues to drift-lower against the Japanese yen currency on Wednesday, as financial markets remain nervous about ongoing trade wars. The USDJPY is likely to weaken further if the 110.87 level is broken, as it represents the pairs 200-period moving average on the four-hour time frame. Sellers will likely target strong losses towards the 110.00 region, while buyers continue to aim for price stabilization back above the 111.39 level.

The USDJPY pair is strong bearish while trading below the 111.39 level, key support is found at the 110.87 and 110.70 levels.

If the USDJPY pair trades back above the 111.39 level, buyers may test back towards the 111.90 and 112.20 levels.

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 1.1693

Allow a bit of ranging activity between 1.1720-1.1625 before bouncing towards 1.1790 area.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.1750 | 1.1750 | 1.1650 | 1.1510 |

| 1.1790 | 1.1830 | 1.1570 | 1.1300 |

USD/JPY

Current level - 111.21

The rebound above 110.70 has been capped at 111.40, so allow another dip to the mentioned low, en route to 110.25.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 111.40 | 114.50 | 110.70 | 110.25 |

| 112.10 | 114.50 | 110.25 | 109.30 |

GBP/USD

Current level - 1.3154

Expect a reversal below 1.3190, for another slide towards 1.3080.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3190 | 1.3460 | 1.3080 | 1.2960 |

| 1.3360 | 1.3620 | 1.2960 | 1.2770 |