Sample Category Title

Australian dollar lower after CPI miss, NZD down on trade deficit

Both Australian Dollar and New Zealand Dollar are trading lower today after release of economic data.

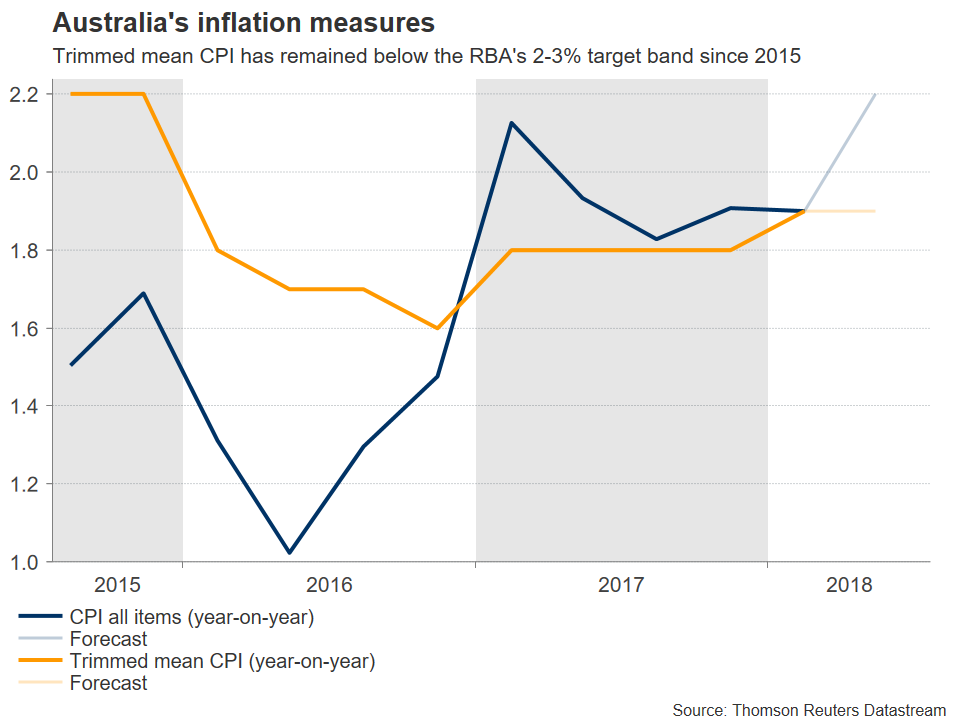

Australia CPI rose 0.4% qoq, 2.1% yoy in Q2. The annual rate accelerated from Q1's 1.9% yoy but missed expectation of 2.2% yoy. RBA trimmed mean CPI was unchanged at 1.9%, inline with expectation. RBA weighted median CPI slowed to 1.9% yoy, down from 2.0% yoy, matched expectation.

RBA is very clear with its stance that there is no compelling reason to raise interest rate in near term. And the inflation data certainly won't alter that position.

New Zealand trade balance came in at surprised NZD -113m deficit in June, versus expectation of NZD 200m surplus. Exports dropped from NZD 5.35B to NZD 4.91B. Imports also dropped from NZD 5.15B to 5.02B.

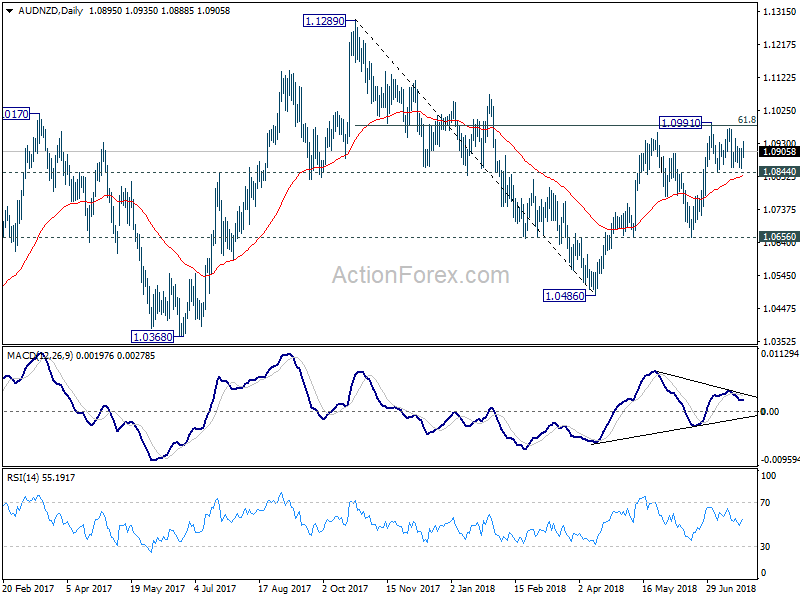

AUD/NZD has been stuck in range of 1.0884/0991 since early July and there is no sign of a breakout yet. While 61.8% retracement of 1.1289 to 1.0486 at 1.0982 looks like a strong resistance. But the cross is holding above 55 day EMA as well as 1.0844 support, thus maintains near term bullishness. For now, further rise remains in favor.

Trump called for dropping all tariffs ahead of meeting with EU Juncker

European Commission President Jean-Claude Juncker's visit to the US and meeting with Trump is an highly anticipated event today. Ahead of that Trump continued to play victim with his provocational tweets and said "tariffs are the greatest! Either a country which has treated the United States unfairly on Trade negotiates a fair deal, or it gets hit with Tariffs. It's as simple as that - and everybody's talking! Remember, we are the "piggy bank" that's being robbed. All will be Great!"

And he added later that "the European Union is coming to Washington tomorrow to negotiate a deal on Trade. I have an idea for them. Both the U.S. and the E.U. drop all Tariffs, Barriers and Subsidies! That would finally be called Free Market and Fair Trade! Hope they do it, we are ready - but they won't!

According to European Union trade commissioner Cecilia Malmstrom, who's in the visit too, the meeting is to seek to " de-escalate the present situation and prevent it from worsening". Commission spokesman Margaritis Schinas said yesterday that " there are no offers."

Trump’s USD 12B aid to tariffs affected farmers … very temporary bandage to a self-inflicted wound

Overnight, Trump administration announced to offer up to USD 12B in aid to farmers that are affected by the the US trade war with other countries, notably China. The program included a mix of measures overseen by the USDA, including director payments to soybean producers, distribution assistance and international marketing. Trump said in the farmers will be the "biggest beneficiary" in what he's doing on trade and " watch, we are opening up markets, you watch what is going to happen, just be a little patient."

The program is not generally welcomed by the industry though. Zippy Duvall, president of the American Farm Bureau Federation, the largest American farmer group said, "we cannot overstate the dire consequences that farmers and ranchers are facing in relation to lost export markets ... and we will continue to push for a swift and sure end to the trade war."

American Soybean Association said in a statement that "the announced plan provides only short-term assistance ... ASA continues to call for a longer-term strategy to alleviate mounting soybean surpluses and continued low prices, including a plan to remove the harmful tariffs."

Blake Hurst, a corn and soybean farmer and president of the Missouri Farm Bureau said "the payments will be helpful to farmers facing overdue loans and angry bankers, but are completely insufficient if they mean that tariffs and the trade war will last for the foreseeable future". "They are a very temporary bandage to a self-inflicted wound."

British Pound Higher as Manufacturing Output Beats Estimate

The British pound has edged higher in the Tuesday session, erasing the losses seen on Monday. In the North American session, the pair is trading at 1.3140, up 0.30% on the day. On the release front, British CBI Industrial Order Expectations dipped to 11 points, but still beat the estimate of 8 points. In the U.S, the Richmond Manufacturing Index remained pegged at 20 points, above the estimate of 18 points. On Wednesday, the UK releases CBI Realized Sales, while in the U.S, New Home Sales is forecast to drop sharply to 669 thousand.

With U.S trade tariffs on EU products threatening to hurt British exports and the manufacturing sector, the markets are keeping a close eye on UK manufacturing indicators. Manufacturers orders showed strong growth for a second straight month, with a reading of 11 points. The CBI Manufacturing Council welcomed the strong manufacturing data, but cautioned that “rising trade tensions and ongoing uncertainty over our future trade and customs arrangements are clearly taking their toll on manufacturers’ confidence and investment.”

Relations between the U.S and EU have nosedived in recent weeks, after months of tit-for-tat tariffs and harsh rhetoric. The U.S slapped tariffs on EU steel and aluminum back in June, and the EU has since retaliated with tariffs on a range of U.S products. President Trump has not shied away from harsh criticism about the EU, and a recent NATO summit exposed the frosty relations between Trump and EU leaders. Still, there could be better news ahead, as EU President Jean-Claude Juckner meets with President Trump on Wednesday. On Friday, Trump attacked the EU and China for manipulating their currencies and keeping interest rates lower. This has raised concerns that the current global trade tensions could be followed by a currency war. Growing concerns over the dangers of the ongoing trade war were summed up in the final communiqué from the G-20 meeting in Argentina over the weekend, which noted that “heightened trade and geopolitical tensions pose an increased risk to global growth”.

Japanese Yen Trading Sideways, BoJ Inflation Misses Mark

The Japanese yen has posted slight gains in the Tuesday session. In the North American session, USD/JPY is trading at 111.24, down 0.09% on the day. On the release front, Japanese Flash Manufacturing PMI slipped to 51.6, short of the estimate of 53.2 points. The indicator is at its lowest level since November 2016. On the inflation front, BoJ Core Inflation dipped to 0.4%, shy of the forecast of 0.6%. There are no major U.S events on the schedule. On Wednesday, U.S New Home Sales is forecast to drop sharply to 669 thousand.

The yen has posted slight gains this week and touched a 2-week high in response to a report that the Bank of Japan was considering changes to its monetary policy, in particular, its interest rate targets. This has raised speculation that the Bank could be making plans to reduce its massive stimulus program. Japan's 10-year yield climbed to 5-month high on Monday in response to the report. If there are further signals from the BoJ that policymakers are considering reducing stimulus, the yen could move higher.

The yen jumped on the bandwagon on Friday, as the U.S dollar was broadly lower after U.S President Trump made comments critical of Federal Reserve monetary policy. U.S presidents traditionally do not comment on moves by the Fed, but that did not prevent Trump from tweeting on Thursday that "tightening now hurts all that we have done". On the weekend, Treasury Secretary Steven Mnuchin engaged in damage control, saying at the G-20 meeting that Trump was not interfering with the Fed policy of gradually raising rates. However, investors weren't buying Mnuchin's apologetics, and the U.S dollar continued to lose ground in Monday's Asian session. There was more for investors to fret over, as Trump also attacked the EU and China for manipulating their currencies and keeping interest rates lower. This has raised concerns that the current global trade war could be followed by a currency war. Growing concerns over the dangers of the ongoing trade war were summed up in the final communiqué from the G-20 meeting in Argentina over the weekend, which noted that "heightened trade and geopolitical tensions pose an increased risk to global growth".

Eco Data 7/25/18

[php_everywhere instance="1"]

Australian Inflation Data Next on the Docket for the Aussie

Australia’s quarterly inflation data for Q2 will be released on Wednesday, at 0130 GMT. Forecasts point to an overall lackluster report, expected to show an energy-driven pickup in the headline rate but an otherwise subdued picture for underlying inflation, which could cement expectations the RBA will remain on hold for the foreseeable future.

Expectations that the Reserve Bank of Australia (RBA) will take any form of policy action over the foreseeable future have moderated dramatically in recent months. Whereas back in January markets were placing approximately even odds on the Bank raising rates or remaining on hold by year-end, the probability for a 25bps rate increase has now plunged to below 3%.

On the bright side, the labor market is strong, but that has failed to manifest into higher wages for Australian households that are heavily indebted already, and hence could really benefit from a pay rise. Meanwhile, trade tensions between the US and China are casting a long shadow on the prospects for Australia’s export-driven economy. Add on top an overall weak inflation picture, with measures of underlying inflation remaining stubbornly below the RBA’s 2-3% target, and one begins to grasp the severe repricing in hike expectations. The aussie has moved accordingly, declining by roughly 9% against the dollar since late January.

The upcoming inflation data are not expected to show a material improvement in Q2 either. While the headline inflation rate is projected to have risen to 2.2% in yearly terms, from 1.9% previously, the pickup appears to be owed mainly to an increase in oil prices, and not the healthy demand-driven inflation the RBA would like to see. The trimmed mean CPI rate is expected to have remained unchanged at 1.9% while the weighted median CPI is anticipated to have eased slightly to 1.9% from 2.0% previously.

Even if the upcoming inflation data were to surprise to the upside, it’s doubtful whether that would be enough to lead to a sustained recovery in the aussie. Markets may need to see much more before putting the prospect of an RBA rate hike back on the table, and most notably a pickup in wages. The next set of wage data will be released on August 15.

Finally, trade tensions will also play a large role in determining the aussie’s forthcoming direction. Besides relying heavily on commodity exports, Australia also has very close economic ties to China, so any escalation in the US-China standoff would probably have severe consequences for Australia. While the rhetoric has continued to escalate, with the US President recently threatening to impose tariffs on all Chinese imports to the US, investors appear not to have taken that at face value, judging by the relatively limited market reaction.

Technically, looking at aussie/dollar, further declines could encounter an initial line of support around the 18-month low of 0.7308 posted on July 2. A downside break may pave the way for the 0.7245 zone, marked by the inside swing high on 30 December 2016. Lower still, declines could stall around the low of 23 December 2016, at 0.7155.

On the upside, preliminary resistance to advances may come around 0.7484, defined by the peak of July 9. If the bulls manage to pierce through it, the June 6 peak of 0.7675 would increasingly come into view. Even higher, the high of April 19 at 0.7810 could attract attention.

IMF: Escalation of protectionist policies will not help current account imbalances

IMF warns in its latest 2018 External Sector Report (ESR) that "excess imbalances are increasingly concentrated in advanced economies" that "both deficits and surpluses—pose risks for individual countries, and for the global economy." Global current account surpluses and deficits "remained relatively unchanged over the past five years" at around 3.25% of global GDP. And 40-50% is concentrated in advanced economies.

Higher-than-desirable current account balances prevail in northern Europe—in countries such as Germany, the Netherlands, and Sweden—as well as in parts of Asia—in economies like China, Korea, and Singapore. Lower-than-desirable balances remain largely concentrated in the United States and the United Kingdom.

IMF also pointed out that "persistence of global imbalances and mounting perceptions of an uneven playing field for trade are fueling protectionist sentiment." And "these impulses are misguided. It warned that "escalation of protectionist policies would mainly hurt domestic and global growth, without much of an effect on current account imbalances, as this year's report also finds."

It urged countries to tackle imbalances together. In particular:

- Countries with lower-than-warranted external current account balances should reduce fiscal deficits and encourage household saving, while monetary normalization proceeds gradually.

- Where current account balances are higher than warranted, the use of fiscal space, if available, may be appropriate to reduce excess surpluses.

- Well-tailored structural policies should play a more prominent role in tackling external imbalances, while boosting domestic potential growth. In general, reforms that encourage investment and discourage excessive saving—through the removal of entry barriers or stronger social safety nets—could support external rebalancing in excess surplus countries, while reforms that improve productivity and workers' skill base are appropriate in countries with excess external deficits.

Also from the report, the Real effective exchange rate (REER) gap average in "2017" were:

- USD was moderately overvalued by 8-16%, compared with the level

implied by medium-term fundamentals and desirable policies. - EUR REER gap average in 2017 was in the range of -8% to 0% for Eurozone as a whole. But it ranged from undervaluation of 10-20% in Germany to overvaluation of 0-10% in small to mid-sized Eurozone member states.

- GBP was 0-15% overvalued. But it noted the assessment is subject to a greater margin of uncertainty due to trade relationship with the EU.

- JPY REER gap in the range of -13% to 6%. Broadly in line with medium-term fundamentals and desirable policies.

- CHF REER gap average in 2017 was in the range of -5.3% to 2.3%.

- Canada was overvalued by 1-13% relative to medium-term fundamentals and desirable policies.

- AUD overvalued by 0-17%, above the level implied by medium-term fundamentals and desirable policy settings. 1

- China: The REER to be broadly consistent with fundamentals and desirable policies, with the gap being in the range of -13 to +7 percent.

The blog post can be found here.

The full report here.

UK PM May takes over Brexit negotiations from now on

UK Prime Minister Theresa May said she will lead the Brexit negotiation with EU from now on.

In a written statement to the Parliament, May said that "I will lead the negotiations with the European Union, with the Secretary of State for Exiting the European Union deputizing on my behalf."

"DExEU (Department for Exiting the EU) will continue to lead on all of the government's preparations for Brexit: domestic preparations in both a deal and a no deal scenario, all of the necessary legislation, and preparations for the negotiations to implement the detail of the Future Framework."

Japan 225 Index Finds Support Near 20-SMA; Neutral Bias Still in Place

Japan 225 index is paring some of the previous three days’ losses after the bounce off the 20-day simple moving average (SMA). Having a look at the medium-term picture the price has been developing within a consolidation area since April with upper boundary the 23000 handle and lower boundary the 21445 support.

Momentum indicators in the daily chart are currently supporting the neutral to positive momentum and are likely to strengthen in the short-term. Specifically, the RSI is picking up speed above 50, while the MACD continues to move sideways above its trigger and zero lines.

Should the price decisively close above the ceiling of the trading range, seen at 23000, bulls could extend the latest upswing towards 23336. If there are further advances above this level, the index could then target the area around 24191 which had successfully halted upside movements during January.

On the other side, a decline could meet the 20-day moving average at 22366 and a successful drop below this level could push the index towards the lower boundary (21445). A breach of this area would open the door for the 20322 support zone.

To sum up, Japan 225 index has been standing above a long-term ascending trend line over the last two years but has struggled in a trading range over the past three months.