Sample Category Title

Economic Data In Focus On Wednesday

Headline data releases from Europe and the United States will preoccupy currency traders on Wednesday ahead of an active second half of the week that includes US GDP and a European Central Bank policy decision.

Action on Wednesday begins with a report on German business sentiment courtesy of the CESifo Group. At 08:00 GMT, the organization will release three indicators on German business sentiment, including: business climate, current assessment, and expectations. All three readings are expected to fall for July.

The Centre for European Economic Research (ZEW) will issue a report on Swiss business conditions at 08:00 GMT. The expectations index provides a snapshot of underlying business conditions in the Swiss economy.

Elsewhere in Europe, the British Bankers Association (BBA) will report on mortgage approvals at 08:30 GMT. Approvals are projected to decline to 39,000 for June compared with 39,244 the month before.

Housing data will headline North American trading beginning at 11:00 GMT with a report on US mortgage applications courtesy of the Mortgage Bankers Association (MBA). Later in the morning, the Department of Commerce will issue its monthly report on new home sales, which account for roughly a tenth of the US housing market.

The sale of new homes is projected to fall 2.8% in June to a seasonally adjusted annual rate of 670,000. Sales rose 6.7% the month before.

Commodity traders will also be keeping track of crude inventory data courtesy of the US Energy Information Administration (EIA). Stockpiles are projected to fall by nearly 3.2 million barrels in the week ended 16 July after surging by more than 5.8 million barrels the week before.

EUR/USD

Europe’s common currency traded choppy on Tuesday, with prices fluctuating between 1.1660 and 1.1708. At the time of writing, EUR/USD was trading at 1.1687, where it was little changed compared with the previous close. Support levels are seen at 1.1650/60 ahead of the European Central Bank’s policy decision, which is scheduled on Thursday.

GBP/USD

Cable stabilized on Tuesday after hitting an intraday low of 1.3076. GBP/USD now trades at 1.3148, where it was little changed. The bulls are eyeing 1.3200 as the next resistance level. On the opposite side of the spectrum, immediate support is located in the vicinity of 1.3110, followed by 1.3070.

USD/CAD

The North American pair’s recovery attempt fell short on Tuesday, as prices retraced back down to the mid-1.3100 region after hitting a high north of 1.3190. USD/CAD currently sits at 1.3147, where it is virtually unchanged compared with the previous close. The pair faces a strong support level in the low 1.3100 region, which corresponds to the double-bottom formed on 20 July. Immediate resistance is located at Tuesday’s interim high.

Aussie CPI Soft But Moving Into Target Range

General Trend:

- Asian equities trade mixed, in line with Tuesday’s US session

- Shanghai Composite moves between gains and losses following advance on Tuesday’s session

- China Merchants Bank reported H1 Net profit +14% y/y

- Sinopec rises over 3%, expects to swing to an H1 profit

- HNA Investment trades limit down after being resumed for trading

- Telecom China Tower issued the expected pricing range for HK IPO

- Mitsubishi Motors declines over 3% following quarterly earnings and guidance

- LG Display reported mixed Q2 results, expects oversupply issue to remain prevalent for display industry

- PBoC set the yuan at the weakest since June 2017

- Australia Q2 CPI data mixed, headline inflation moves within target range while core remains below

- New Zealand reports unexpected trade deficit in June amid higher fuel imports and decline in milk powder exports

- Japanese automation company Fanuc may report earnings later today

- Line Corp, Shin-Etsu Chemical, Advantest, Hitachi Construction and Nidec may also report.

- US and European companies expected to report earnings on Wed include AMD, Boeing, Clariant, Coca-Cola, Dassault Systems, Deutsche Bank, Facebook, Fiat, Ford, Freeport McMoran, General Motors, Glaxo, STM, Santander, UPS, Visa and Vodafone.

- South Korea Q2 prelim GDP data due for release on Thursday

Headlines/Economic Data

Japan

- Nikkei 225 opened +0.4%

- TOPIX Iron and Steel index +2.5%, Electric Appliances +0.6%, Securities +0.6%

- (JP) According to ‘BoJ watchers’ the central bank is not likely to make any policy changes until at least Oct 2018 – Nikkei

- Toyota Motor, 7203.JP To close plant in Shizuoka Prefecture by 2020; US auto tariffs may make it difficult to meet 3M domestic vehicle production target – Nikkei

- 7203.JP Planning to double China production by early 2020s, targeting China production of 2M units/year - Japan press

- (JP) Japan PM Abe increasingly likely to secure a 3rd consecutive term as LDP president with a key rival Fumio Kishida declining to declare candidacy for the vote this fall - Nikkei

Korea

- Kospi opened +0.2%

- LG Display, 034220.KR Reports Q2 (KRW) Net -297B v -226Be; Op -228B v -247Be; Rev 5.6T v 5.6Te

- LG Chem, [+5%], 051910.KR Reports Q2 (KRW) Net 477.2B v 484.4Be; Op 703.3B v 696.8Be; Rev 7.1T v 6.9Te

- (KR) South Korea Economic Affairs Aide Yoon Jong-won: South Korea economy in general doesn't seem problematic

China/Hong Kong

- Hang Seng opened +0.9%, Shanghai Composite +0.2%

- Hang Seng Services index +3%, Energy +1.8%, Consumer Goods +0.9%, Info Tech +0.8%, Property/Construction +0.7%, Industrial Goods +0.7%, Financials +0.6%

- (CN) China PBoC to be more flexible in implementing monetary policy - Chinese Press

- (CN) China PBoC Open Market Operation (OMO): Skips OMO for the 4th consecutive session; Net drains CNY60B v drains CNY70B prior

- (CN) CHINA PBOC SETS YUAN REFERENCE RATE AT 6.8040 V 6.7891 PRIOR (weakest setting since late June 2017)

Australia/New Zealand

- ASX 200 opened +0.2%

- ASX 200 Telecom index -0.8%, Utilities -0.7%, Financials -0.5%

- (NZ) NEW ZEALAND JUN TRADE BALANCE (NZ$): -113M V +200ME; 12-MONTH YTD: -4.03B V -3.68BE

- (AU) AUSTRALIA Q2 CPI Q/Q: 0.4% V 0.5%E; Y/Y: 2.1% V 2.2%E (1st reading in target range in 10 quarters)

- (NZ) New Zealand Q2 working age population +18.1K (smallest rise since 2014)

- (AU) Australia Jun Skilled Vacancies m/m: -1.0% v -1.2% prior

- CSR, [+2.5%], CSR.AU Confirms starting review of Virdian, looking at all options including sale; seeing improvement in ANZ, on track to boost earnings

- Medical Developments International, [-15%], MVP.AU Penthrox clinical program put on hold by FDA pending a letter outlining outstanding issues and concerns

- (AU) Analysts note that Australia CPI was soft despite large rise in fuel prices which leaves room for RBA to hold rates well into 2019 - US press

Other Asia

- (PH) IMF: Affirms Philippines 2018 GDP growth forecast at 6.7%, also sees 2019 growth at 6.7%; may need to further tighten monetary policy, rate moves are appropriate for price stability

North America

- US equity markets ended mixed: Dow +0.8%, S&P500 +0.5%, Nasdaq flat, Russell 2000 -1.1%

- S&P 500 Materials +1.3%, Energy +1.3%

- (US) Weekly API Oil Inventories: Crude: -3.2M v +0.6M prior

- (US) SEMI: Jun North America Billings $2.48B, -8.0% m/m and +8.1% y/y

- PIR Comments on Proposed Tariff: does not expect financial results in fiscal 2019 to be materially affected; of net sales expected to be derived from products produced in China ~50% is expected to consist of product classes subject to the proposed tariffs

- (MX) Mexico Incoming Foreign Minister Marcelo Ebrard: Trump disclosed in letter that the 2 countries should increase cooperation

- (US) US President Trump: Reiterates the US and EU should drop all tariffs and trade barriers

Europe

- (DE) Germany DIHK Head says US President Trump's tariffs may cost Germany €5.0B - German Press

- (EU) EU Budget Commissioner Oettinger: EU would react in kind if Pres Trump levies new tariffs

Levels as of 01:30ET

- Hang Seng +0.8%; Shanghai Composite +0.1%; Kospi -0.3%; Nikkei225 +0.4%; ASX 200 -0.3%

- Equity Futures: S&P500 -0.2%; Nasdaq100 -0.1%, Dax -0.0%; FTSE100 +0.7%

- EUR 1.1676-1.1698; JPY 111.15-111.38; AUD 0.7360-0.7449;NZD 0.6785-0.6812

- Aug Gold -0.0% at $1,225/oz; Sept Crude Oil +0.3% at $68.72/brl; Sept Copper +0.3% at $2.81/lb

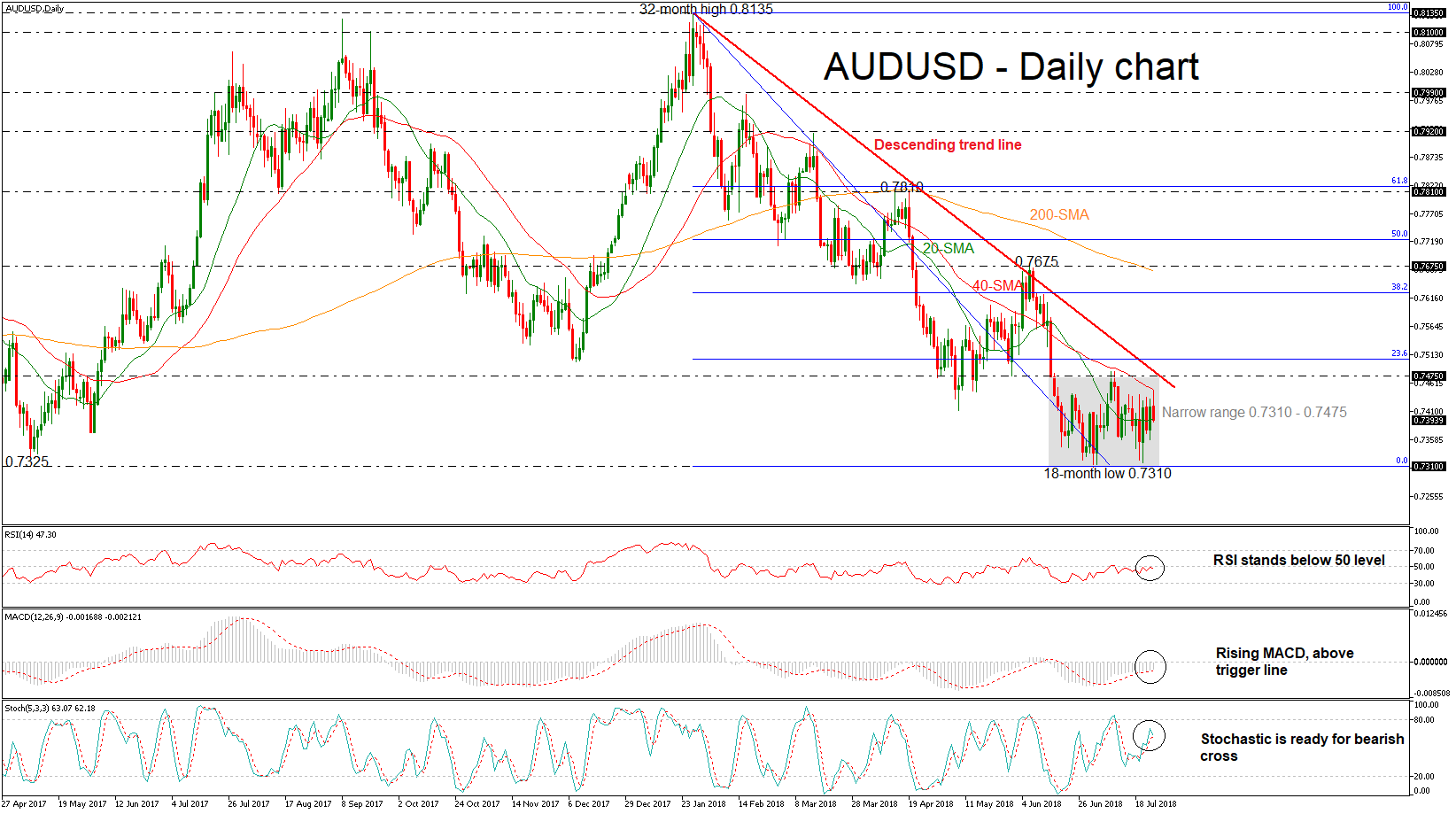

AUDUSD Eases Below Descending Trend Line, Neutral Bias In Short Term

AUDUSD has been moving sideways over the last five weeks as the 0.7475 resistance level acted as a strong obstacle for the bulls and the 0.7310 support as a hurdle for the bears in the previous sessions. Also, the price failed to dip below the 18-month low of 0.7310, achieved on July 2 and holds near the 20- and 40-simple moving averages (SMAs) after the rebound on the latter level, in the daily timeframe.

From the technical point of view, momentum indicators are endorsing the neutral to bearish weakness in the market. The RSI indicator is sloping slightly downwards and stands below the threshold of 50, while the stochastic oscillator is ready for a bearish cross within the %K and %D lines, indicating further losses. However, the MACD oscillator is moving higher in the negative territory above its trigger line and is approaching the zero line.

Should prices drop further lower, this could open the way towards the 18-month low of 0.7310. Further downside extensions could drive the pair until the 0.7160 hurdle, taken from the bottom on December 2016. There are no significant support obstacles before that level.

On the flip side, the first resistance for investors to have in mind is the 0.7475 barrier. If there is a jump above this region, the price could challenge the 23.6% Fibonacci retracement level of 0.7505 of the downleg from 0.8135 to 0.7310. Above this barrier, if there is an upside penetration of the falling trend line, the focus shifts to the upside until the 38.2% Fibonacci of 0.7625.

To sum up, AUDUSD has been trading within a descending move since January 26 and is in progress to create a consolidation area within the 0.7475 and 0.7310 in the medium-term.

Currencies: Turmp-Juncker Meeting To Decide On Next EUR/USD Move

Rates: Core bond sell-off grinds to a halt

The two-day core bond sell-off grinded to a halt yesterday with the Bund even recording small gains. Today's eco calendar is thin with only German Ifo while the Juncker/Trump meeting is a wildcard. Technical charts still suggest that core bonds are prone for more losses. European investors will take tomorrow's ECB meeting into account. We expect a non-event.

Currencies: Turmp-Juncker meeting to decide on next EUR/USD move.

Yesterday, changes in core yields were too small to inspire further guidance for FX trading after Monday's move. Today, the focus of global markets will be on the Trump-Juncker meeting. The euro probably needs a constructive outcome of this meeting. Sterling rebounds further as UK PM May will take the lead in the EU-UK Brexit negotiations.

The Sunrise Headlines

- US stock markets did well yesterday, with most major indices closing with gains and NASDAQ Comp ending unchanged (-0.01%). Asian markets is following the US example but with Chinese underperforming.

- US President Trump and European Commission president Jean-Claude Juncker will meet later today to discuss EU-US tariffs. Meanwhile, US agriculture officials announced a $12bn aid programme for US farmers being hurt by tariffs.

- UK Prime Minster Therese May has taken control over the Brexit negotiations. The current Department for Exiting the EU would be downgraded and May will continue her drive to keep the UK close to the European Union.

- The European Commission laid out plans to fund the cost of setting up controlled centres to process asylum claims within 8 weeks and send back failed migrants to their country of origin. Italy has already said that it rejects the idea.

- Mexico's new NAFTA negotiator, Jesus Seade, said to believe it is almost inevitable that a deal will be reached in the coming months. Seade will travel to Washington later this week to revive the NAFTA talks with the US.

- Republicans in the US House of Representatives unveiled an election-year tax plan that promises tax cuts for individuals and business owners days before they head home to campaign for the congressional elections of November.

- Today's eco calendar contains the IFO Expectations for July in Germany and of course most importantly the Trump-Juncker summit in Washington

Currencies: Turmp-Juncker Meeting To Decide On Next EUR/USD Move

Trump-Juncker meeting to decide on next move ?

Yesterday, there was little follow-through price action Monday's rise in US yields that also lifted the dollar. Changes in yields/yield differentials were small. EMU PMI's were mixed, but a manufacturing performance temporarily supported the euro. Risk sentiment (while positive) was also no clear guide for FX trading. EUR/USD closed the day at 1.1687, little changed from Monday. Similar picture for USD/JPY. Investors stay cautious on yen shorts ahead of next week's BOJ meeting. USD/JPY closed unchanged at 111.20. Overnight, Asian equities are trading mixed. Japan slightly outperforms. The yuan is holding near yesterday's low, but there are no additional losses (USD/CNY 6.80 area). Australia headline inflation was marginally softer than expected at 0.4% Q/Q and 2.1% Y/Y, indicating no hurry for the RBA to raise rates. The Aussie dollar eased back to the 0.74 area. Today, the eco calendar contains German IFO confidence and US new home sales. IFO confidence is expected to ease slightly further, but yesterday's (manufacturing) PMI suggests that the negative fall-out from the trade war might still be modest, at least for now. The meeting of president Trump with EU's Juncker, will be key for trading. The euro probably needs a constructive outcome (at least no escalation in the tariff war). It is impossible to predict Trump's tactics. In the run-up to the meeting, investor cautious might prevail, being a tentative supportive for the dollar. EUR/USD is holding the 1.15/1.1850 range. This range won't be easy to break. Trump's comments on Fed policy might still cap a leap higher of the USD. Still, the upside momentum of USD/JPY looks to be broken. Investor nervousness on trade might be a slightly supportive for the yen, especially as the Japanese currency is again better bid ahead of next week's BOJ meeting.

Yesterday, EUR/GBP held a tight range in the 0.8920 area for most of the day. However, late in the session, UK PM May declared that she will take the lead of the Brexit negotiations. This move contains several political risks. However, markets apparently still consider it as slightly reducing the risk of a no deal Brexit. EUR/GBP dropped a few ticks below the 0.89 barrier. Today the CBI retail data are expected to have eased in July. Yesterday's EUR/GBP price action is slightly positive for sterling short-term. The pair moves further away from the key 0.8968 resistance. A cautiously sterling positive momentum might persist going into next week's BoE meeting

EUR/USD: Trump-Juncker meeting to decide on next EUR/USD move?

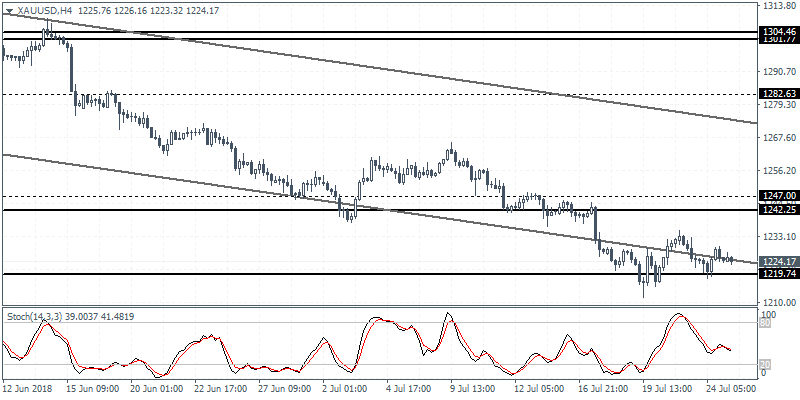

XAUUSD Intraday Analysis

XAUUSD (1224.17): Gold prices were seen trading subdued as price action continues to remain support above the 1219 level. We expect to see this sideways pattern continue ahead of a potential breakout. To the upside, the resistance level at 1247 - 1242 remains a prime target. Establishing resistance here could, however, keep gold prices range bound within the current levels. To the downside, in the event of a break down below 1219, we expect to see the declines sending gold prices lower to test the 1200 level.

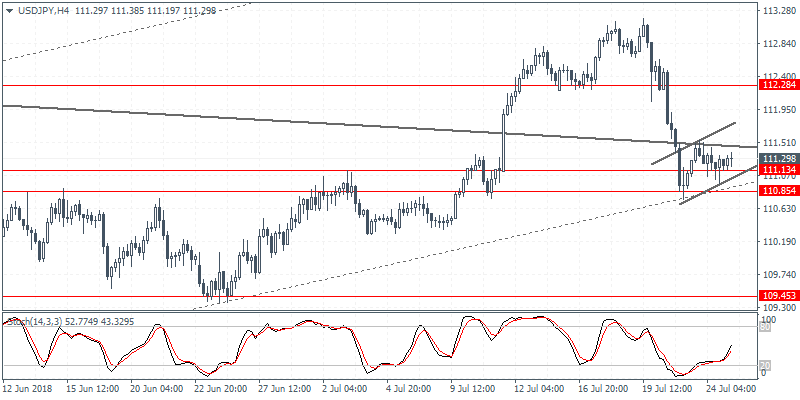

USDJPY Intraday Analysis

USDJPY (111.29): The USDJPY currency pair was seen bouncing off the support level at 111.13 - 110.85 region. The brief rebound off this level was met with resistance from the falling trend line. The failure to break above the trend line indicates further consolidation. This also improves the prospects of a downside breakout. A close below 110.85 could send the U.S. dollar lower toward the 109.45 level of support. This will also validate the bearish flag pattern that is likely to emerge.

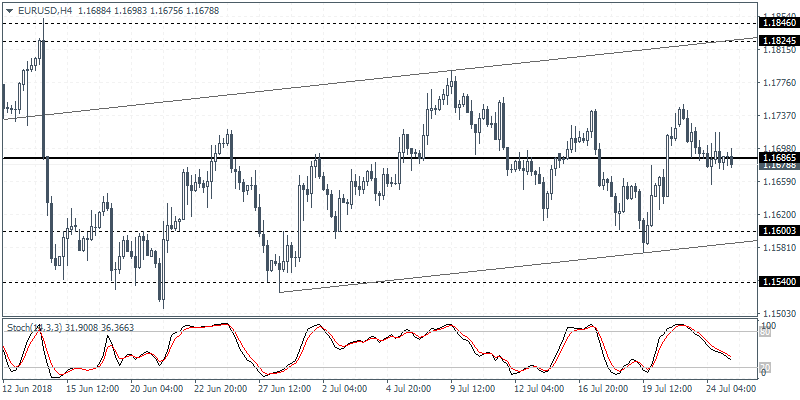

EURUSD Intraday Analysis

EURUSD (1.1678): The EURUSD currency pair was seen closing with a doji pattern following Monday's reversal of the resistance level near 1.1730. A bearish follow through on the day could potentially push the common currency lower. Price action is seen consolidating around the short-term support/resistance level near 1.1686 region. To the downside, we could expect a decline back to 1.1600 level. A break down below this level could trigger further declines toward 1.1540 region. With the ECB meeting coming up tomorrow, the EURUSD is likely to remain subdued.

Australia Inflation Rises Modestly In Q2

The U.S. dollar was seen trading rather mixed on Tuesday. Economic data was sparse. The commodity-linked currencies got a boost after reports of China’s new spending plans were released.

In the overnight trading session, the Australian inflation report showed that consumer prices advanced 0.4% on the month. This was the same pace of increase seen the month before. The trimmed mean CPI increased 0.5% on the quarter, matching the median forecasts.

On an annualized basis, inflation in Australia was seen rising2.1%, just shy of the 2.2% increase that was forecast.

Looking ahead, the economic data for the day is relatively light. The NY trading session will see the release of the new home sales report. New home sales are forecast to rise 671k during the month. This marks a slower pace of increase compared to 689k in the previous month.

The data comes following a weaker existing home sales report.

In The US, New Home Sales Are Up For Release

Market movers today

Focus turns to the trade war again as EU Commission President Jean-Claude Juncker meets with US President Donald Trump. Juncker will be accompanied by EU trade commissioner Cecilia Malmström, who last week said that Juncker would try to persuade Trump to de-escalate the conflict and not impose tariffs on autos. The EU has also said it would not negotiate with a 'gun to its head'. On 23 May, Trump ordered an investigation into whether to increase tariffs on cars from the EU and other countries. Trump said in late June that he expected it to be completed in three to four weeks.

On the data front, the key release today will be German ifo business confidence. Following a rebound in German PMI yesterday, we may see a rebound in the ifo index as well, suggesting that the recent escalation in the trade conflict is not having a big negative effect on business sentiment.

In the US, new home sales are up for release. Other housing data has been weak recently in response to higher house prices and increasing mortgage rates .

Selected market news

It has been fairly quiet overnight, with Asian markets trading sideways and notably the Chinese equity rally levelling off following Monday's announcement of additional easing by the Chinese authorities. In Japan, long-dated government bonds have stabilised again and this morning's regular market operation from Bank of Japan (BoJ) gave no policy hints for markets to trade on. Yesterday, we released our BoJ preview ahead of the 31 July meeting. In short, we do not expect any policy changes but the risk of policy fine-tuning has admittedly risen. See full preview here .

In FX markets, EUR/USD initially gained yesterday on the better-than-expected set of eurozone manufacturing PMIs. The rise eventually faded, but the initial price action was in our view the key driver behind the rebound in Scandi FX, which has been under pressure recently from a bid USD, looming trade wars and thin summer markets. Manufacturing confidence data out of Norway yesterday morning supported the case for a September Norges Bank rate hike, see chart . Yet, we think the synchronous price action in EUR/SEK and EUR/NOK rather suggests that the NOK's and SEK's high beta to eurozone developments were the driving forces behind the rebounds. In the very near term, we still regard EUR/SEK and EUR/NOK as range plays.

Yesterday evening, UK Prime Minister Theresa May announced a reshuffling of the team responsible for the UK/EU Brexit negotiations, in a move essentially giving herself more responsibility. May announced that going forward her Cabinet Office ' will have overall responsibility for the preparation and conduct of the negotiations' , thereby taking over the role from the Department for Exiting the EU, which was downgraded to focusing on domestic preparations. The decision gives May's chief European adviser Oliver Robbins a key role following a period where Robbins frequently clashed with former Brexit Secretary David Davis. Markets reacted positively to the news with EUR/GBP falling moderately on the announcement.

Crude Oil The Upside Prevails

Pivot (invalidation): 67.95

Our preference Long positions above 67.95 with targets at 69.30 & 69.80 in extension.

Alternative scenario Below 67.95 look for further downside with 67.55 & 67.20 as targets.

Comment The RSI is mixed to bullish.