Sample Category Title

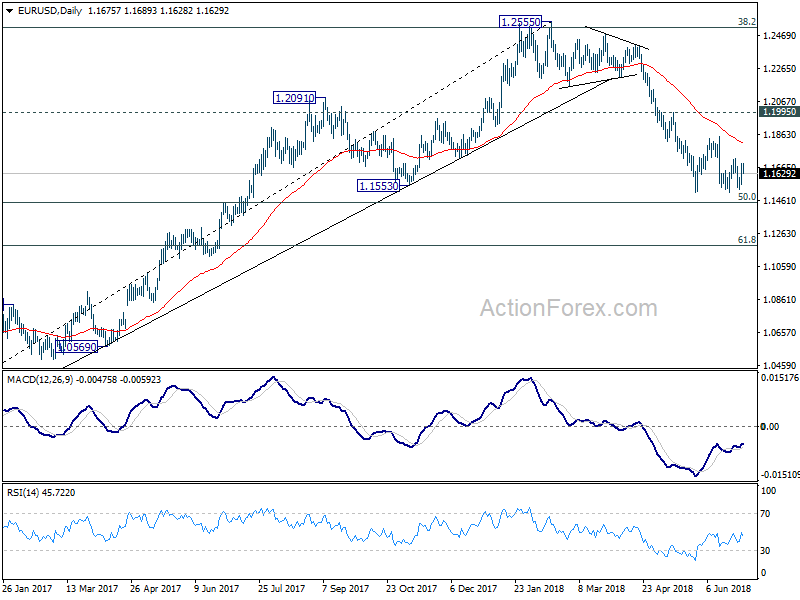

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1534; (P) 1.1568; (R1) 1.1605; More....

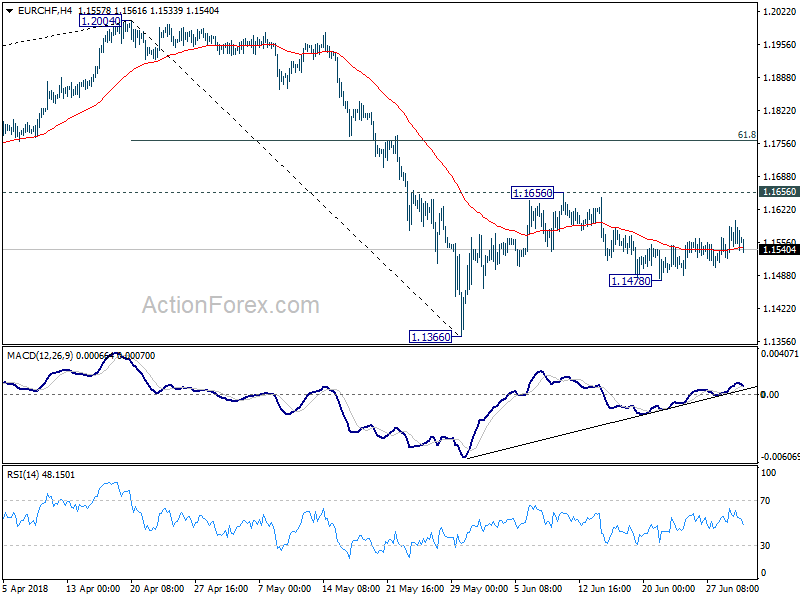

Intraday bias in EUR/CHF remains neutral at this point. On the upside, break of 1.1656 will resume the rebound from 1.1366 to 61.8% retracement of 1.2004 to 1.1366 at 1.1760. But we would expect strong resistance from there to limit upside. For now, we'd expect at least one more falling leg before the correction from 1.2004 completes. Below 1.1478 will turn bias to the downside for 1.1366 and below.

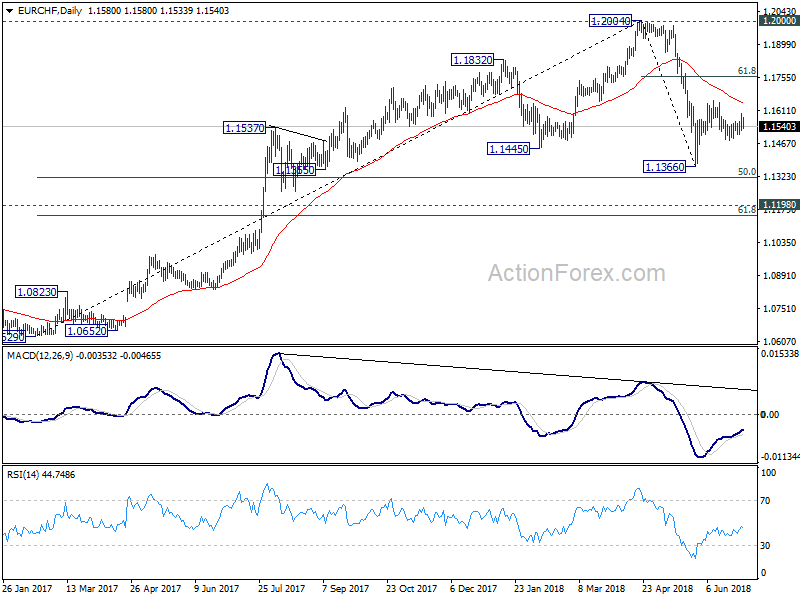

In the bigger picture, EUR/CHF was solidly rejected by prior SNB imposed floor at 1.2000. Considering bearish divergence condition in daily and weekly MACD, 1.2004 should be a medium term top. And price action from 1.2004 is correcting the up trend from 1.0629. Such correction is expected to extend for a while and therefore, we're not anticipating a break of 1.2004 in near term. Another decline cannot be ruled out yet. But in that case, strong support should be seen at 1.1198 (2016 high), 61.8% retracement of 1.0629 to 1.2004 at 1.1154 to contain downside.

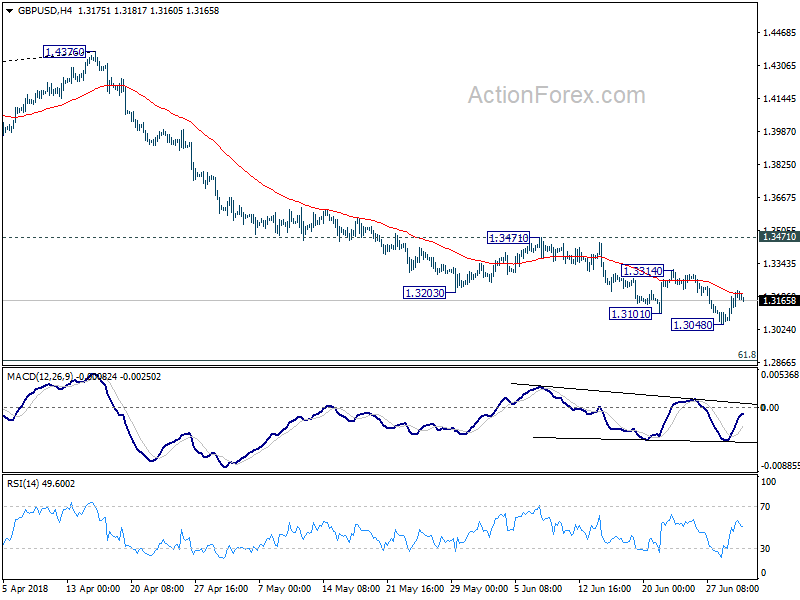

GBPUSD Bulls Need To Keep Price Above 1.3205

The British pound continues to trade towards the higher side of its recent short-term trading range against the US dollar, after a bullish weekly price-close above the 1.3200 level. If GBPUSD bulls fail to hold price above the 1.3205 level they risk losses back towards the 1.3101 level. Sterling traders now look towards the release of key June PMI Manufacturing data from the United Kingdom.

The GBPUSD pair is only intraday bullish while trading above the 1.3205 level, key resistance above 1.3205 is currently found at the 1.3280 and 1.3350 levels.

If the GBPUSD pair trades below the 1.3149 level, further losses towards the 1.3124 and 1.3101 levels remain possible.

ETHUSD Only Intraday Bullish Above $450

Ethereum has started to recover short-term bullish momentum on Monday, after sellers failed to contain price below the key $400 support level. The ETHUSD pair currently trades around the $440 region, with the $450 level the next upside hurdle for Ethereum bulls. Ethereum buyers will look to challenge the $468 level if the $450 level is broken, while sellers will look to contain price below $450.

The ETHUSD pair is intraday bullish while trading above the $450 level, key technical resistance is now located at the $468 and $482 levels.

If the ETHUSD pair moves below the $408 level, sellers may test towards the $395 and $380 support levels.

Brexit In The Headlines On Monday

The pound is down following a report by PricewaterhouseCoopers (PwC) and the Confederation of British Industry (CBI) which revealed Brexit insecurities. According to the quarterly survey of the British financial services sector, many executives and a third of banks surveyed were “not so confident” of implementing Brexit plans by March 2019.

The report will be in the mind of Theresa May, who will meet with her divided cabinet on Friday to try and come up with a consensus proposal. In recent weeks, a number of significant manufacturers like BMW and Airbus have said that they would consider leaving the UK if a deal is not found.

Shifting gears to America, the dollar index is rising, ignoring a new report by Axios. On Friday, Axios reported that Donald Trump was considering leaving the World Trade Organisation (WTO). Today, the outlet published a proposal ordered by the president. The report, which is titled, United States Fair and Reciprocal Tariff Act, would give the president the freedom to raise tariffs at will. Traders believe that it is unlikely that the president will exit the WTO, which has been favourable to the United States. Senators from the president’s party have considered authoring a bill to prevent the president from raising tariffs.

In Japan, a report by Markit showed that the Purchasing Managers Index (PMI) was at 53.0. This was lower than the expected 53.1 but higher than May’s PMI of 52.8. On the negative side, the new order growth declined to a ten-year low and export sales fell for the first time since 2006. This could be a reflection of the ongoing trade conflict, which is affecting trade around the world. In China, data showed the manufacturing PMI at 51.0, which is the lowest level since April. Meanwhile, the Tankan Large Manufacturers Index for the second quarter was 21, which was worse than the expected 22 while the non-manufacturers index was 24, which was better than expected.

Key data is expected throughout the day from the European Union and the United States. In the EU and the UK, traders will be eagerly waiting for the manufacturing PMI data. In the US, details regarding the manufacturing PMI, construction spending, and new orders will be released.

EUR/USD

The EUR/USD pair is currently trading at 1.1660, which is 20 basis points lower than Friday’s close. The price is also in line with the 14-day moving average. Today, the key drivers for the pair will be the PMI data from the US and the EU. A stronger dollar could see the pair test the 1.1627 level which is the 61.8% Fibonacci Retracement level. If it tests this support, it could also attempt to reach the next support of 1.1608, which is the 50% Fibonacci Retracement level. On the other hand, if the dollar weakens, the pair could test the support of 1.1690.

USD/JPY

The USD/JPY pair is continuing the rally which started on Tuesday last week. The mixed data from Japan has contributed to the rally. The pair is now trading at 110.91, which is slightly above the 14-day moving average. The focus will now be on data from the United States because no major releases from Japan are expected. A better-than-expected outlook from the US will provide a catalyst for a further rally on the pair. This could see the pair testing the 111.40 resistance level. Weak data could see it drop to the 110.65 level.

GBP/USD

The GBP/USD pair is currently trading at 1.3176, which is slightly lower than Friday’s close. The decline is mostly because of the dollar strength and the uncertainty of Brexit. In recent days, the pair has been moving up and forming a cup and handle pattern. The likely scenario today will be that the pair will fall to the 1.3164 level, which is also the 61.8% Fibonacci Retracement level. If it reaches this level, it could reverse and move higher today.

Stock Markets Are Slightly Lower In Asia

Market movers today

An eventful week lies ahead, culminating in the introduction of US and Chinese tariffs and the US jobs report on Friday.

In the US, ISM manufacturing for June is being released today. Indicators for general activity and new orders fell this month, supporting our view that the US manufacturing indices should move lower in the next 3-6M. Based on the regional PMIs and Markit PMI manufacturing, we expect ISM for June to remain unchanged.

Today, we will also get final manufacturing PMI readings for the euro area, including first readings for Spain and Italy.

In the Scandies, PMI manufacturing figures are also due out for June in Sweden and Norway (see next page). The main event this week will be the Riksbank meeting tomorrow. See Riksbank Preview - Staying put, possibly soft verbal forward guidance , 28 June.

Selected market news

Stock markets are slightly lower in Asia as we enter a week of anxiety with a potential escalation of the US-China trade conflict, when tariffs on goods worth USD34bn are implemented on Friday in both China and the US. The EU warned US President Trump over the weekend that tariffs on European cars could prompt retaliation on up to USD300bn worth of US goods, see FT . Oil prices fell on a tweet by Trump saying he had asked Saudi Arabia to increase oil production 'maybe up to 2,000.000 barrels...' and that 'he has agreed'.

North Korea is believed to have increased its production of fuel for nuclear weapons according to US Intelligence agencies, see NBC News . The White House has not yet responded to the reports but it could trigger a return of the US-North Korean conflict.

In Germany, the CDU-CSU dispute over immigration is still unresolved after separate meetings for the two parties over the weekend stretched into late night, see Bloomberg . The CDU and CSU are expected to hold joint talks on Monday to reach a compromise. Polls suggest Merkel has increased backing for her stand-off with the CSU. See also Flash Comment - Germany's political future at stake after EU Summit, 29 June 2018.

In China, PMIs were slightly weaker but overall still holding up quite well in contrast with other Chinese data. Caixin PMI manufacturing for June fell to 51.0 (consensus 51.1, previously 51.1) while the official PMI manufacturing fell to 51.5 (consensus 51.6, previously 51.9).

The CNY continues to face depreciation pressure, pushing towards the weakest level in 1½ years. We continue to see downside pressure on the CNY as the trade war with the US is set to escalate further this week with the implementation of tariffs on goods worth USD34bn on Friday.

In Mexico, voters elected Andrés Manuel López Obrador as their new president, the first left-wing president in decades. It could strain Mexican relations with Trump further, see Politico.

China Official PMI Misses, Markets Remain Cautious

General Trend:

- Asian equities trade mostly lower to start new quarter, Hong Kong closed for holiday

- Chinese equities decline after Friday’s gain, Shanghai property index drops over 2.5%

- Tariff implementation in focus: Canada’s retaliatory tariffs on US goods due to take effect on July 1st, China’s retaliatory measures scheduled to take effect on July 6th.

- Nissan and Australia’s Automotive Holdings each cancel deals with Chinese companies

- China June Manufacturing PMI data missed ests, exports noted

- Japan Q2 Tankan survey mixed: Capex and large manufacturer outlook above ests, big company sentiment below ests

- South Korea June exports unexpectedly decline

- Australia house prices have 9th straight m/m decline in June (Corelogic)

- New Zealand Treasury sees weak business confidence as risk to growth

- Chinese yuan (CNY) fixed stronger for first time in 9 sessions

- Mexico’s Lopez Obrador said to win presidential elections, in line with press speculation; Peso (MXN) rallies over 1%

- Germany’s CSU party said to raise concerns about recent EU deal on migration; CSU Party head Seehofer expected to talk with CDU’s Merkel later today

- Crude Oil Futures decline over 1% after US President Trump spoke with the Saudi King

- Reserve Bank of Australia (RBA) expected to hold rate decision on tomorrow’s session

- US June employment data due for release on Friday, July 6th

Headlines/Economic Data

Japan

- Nikkei 225 opened -0.3%

- TOPIX Retail Trade -2.7% index, Iron & Steel -1.6%

- (JP) Japan said to see FY19 real GDP growth 1-2% - Japanese Press

- (JP) Japan military said to have eased its defense force vigilance related to North Korea - Japanese Press

- Orix, 8591.JP Confirms to acquire NXT Capital; no terms disclosed

- (JP) JAPAN Q2 TANKAN LARGE ALL INDUSTRY MANUFACTURING INDEX: 21 V 22E; LARGE MANUFACTURING OUTLOOK: 21 V 20E; LARGE ALL INDUSTRY CAPEX 13.6% V 9.3%E

- (JP) JAPAN JUN FINAL PMI MANUFACTURING: 53.0 V 53.1 PRIOR

- (JP) Bank of Japan (BOJ) said to be planning to revise inflation forecast lower to ~1% for FY18 (prior 1.3%); FY19 to 1.5% (prior 1.8%) - Nikkei

- (JP) Japan Govt said to have finalized FY19 GDP forecast in the 1% range (prior 0.8%) - Sankei

Korea

- Kospi opened -0.2%

- (KR) Some speculation that South Korea will not meet its 3% GDP target this year due to challenges ranging from poor employment figures to weak investment and consumption - Korean press

- (KR) According to satellite imagery North Korea is completing a major expansion of a key missile-manufacturing plant - Korean press

- (KR) South Korea announces records on currency market intervention for H2 2018 will be posted on the website of the Bank of Korea in March of 2019

- (KR) South Korea Jun PMI Manufacturing: 49.8 v 48.9 prior

- (KR) South Korea sells KRW350B in 6-month Monetary Stabilization Bonds (MSBs); avg yield 1.73%

- (KR) South Korea sells KRW1.55T v KRW1.55T indicated in 3-year bonds, avg yield 2.14%

China/Hong Kong

- Hang Seng opened closed for holiday, Shanghai Composite -0.2%

- (CN) CHINA JUN OFFICIAL GOVT MANUFACTURING PMI: 51.5 V 51.7E; Non-manufacturing PMI: 55.0 v 54.8e; Composite PMI: 54.4 v 54.6 prior

- (CN) China GDP expected to grow by 6.6% in 2018 - Chinese Press

- (HK) Macau June Gaming Rev MOP22.5B, Y/Y: 12.5% v 18%e (2nd consecutive missed estimate)

- (CN) China Ministry of Commerce (MOFCOM) Min Zhong Shan: Reiterates China will oppose any kind of protectionism, will widen market access significantly

- (CN) China NDRC will improve price mechanism for green development

- (CN) China property investment seen slowing in H2 2018 - Chinese Press

- (CN) China PBoC Open Market Operation (OMO): skips OMO operations v CNY80B injected in 7-day reverse repos prior; Net: CNY20B drain v CNY20B drain prior

- (CN) China PBoC set yuan reference rate at 6.6157 v 6.6166 prior

- (CN) CHINA JUN CAIXIN PMI MANUFACTURING: 51.0 V 51.1E (prior 51.1)

Australia/New Zealand

- ASX 200 opened 0.0%

- ASX 200 Consumer Discretionary index -0.7%, Energy -0.6%, Resources -0.4%, Financials -0.3%; REIT +0.5%, Telecom +0.4%

- RIO.AU Labor costs at iron ore mines in Australia said to rise by up to 10% - AFR

- SIG.AU Revises FY18/19 Underlying EBIT guidance to ~A$75M; unable to reach agreement with Chemist Warehouse regarding terms for contract extension

- (AU) Australia Jun CBA Australia PMI Manufacturing: 55.0 v 53.2 prior

- GTY.AU Hometown announces intention to make cash takeover offer equal to A$2.25/stapled security, represents A$2.3035/stapled security before being adjusted for distribution; willing to raise offer to A$2.30/stapled security (A$2.3535 before being adjusted for distribution)

- (AU) Australia sees 2018 commodity exports at a record A$226B, +18% y/y

- (AU) Australia buys back A$300M in Oct 2019 and April 2020 bonds, bid to cover 4.55x

- (AU) Certain banks in Australia said to have raised mortgage rates amid higher funding costs – US financial press

- (AU) Reserve Bank of Australia (RBA) is now expected by market economists to leave rates hold for another year v 2 rate hikes expected by mid-2019 in March poll- AFR

- (AU) Australia sells A$300M v A$300M indicated in 2.25% Nov 2022 bonds, avg yield 2.2034% v 2.2716% prior, bid to cover 7.68x v 4.03x prior

- (NZ) New Zealand Treasury monthly economic indicators report: Soft business confidence is a risk to GDP outlook; seeing signs of less momentum in the economy

Other Asia

- (ID) Indonesia Jun PMI Manufacturing: 50.3 v 51.7 prior

- (TW) Taiwan Jun PMI Manufacturing: 54.5 v 53.4 prior

- (VN) Vietnam Jun PMI Manufacturing: 55.7 v 53.9 prior (highest level since March 2011)

North America

- (US) President Trump: Will wait until midterm elections to decided on NAFTA, no plans to back down on China tariffs; OPEC is manipulating the oil market - Fox interview

- (SA) President Trump: Just spoke to King Salman of Saudi Arabia and explained to him that, because of the turmoil & disfunction in Iran and Venezuela, I am asking that Saudi Arabia increase oil production, maybe up to 2.0M barrels to make up the difference...Prices to high! He has agreed! – tweet

- (SA) White House corrects Trump tweet on Saudi Arabia oil boost; statement that the Saudis have 2M barrels per day of spare capacity, which would be used prudently if and when necessary to ensure market balance and stability

- (MX) Mexico Presidential election results: Andrés Manuel López Obrador (AMLO) of the MORENA party winner of election

- (MX) Mexico President-elect Lopez Obrador: To respect central bank autonomy; Will seek friendship with US and mutual respect

- (US) US President Trump draft executive order said to authorize the Commerce Secretary to use national security grounds to block transactions which involve US and foreign telecom equipment manufacturers – Washington Post

- TSLA Panasonic Exec said co. is willing to consider investing more in Tesla's gigafactory if requested - financial press

- (CA) Canada Foreign Minister Freeland: tariffs on U.S. products to take effect on 7/1

Europe

- (DE) Germany Interior Minister/CSU Chairman Seehofer said to have offered resignation to colleagues in CSU Party over migrant issue; CSU Caucus chief Dobrindt said to oppose Seehofer quitting - financial press

- (DE) Follow Up: Germany Interior Minister/CSU Chairman Seehofer said to remain in politics if Merkel's CDU party backs down over migration - German Press

- (DE) Germany CSU Party Head Seehofer: Wants to avoid collapse of Merkel's government; seeking one more talk with the CDU party

- (UK) UK PM May Representative in Brexit talks Robbins said to have told ministers that there is no chance for 'bespoke' trade deal - UK Press

- (UK) Tory MP Rees-Mogg: Cautions PM May of Tory rebellion if Brexit promise is broken; May must deliver the Brexit she promised or risk collapsing the government - US financial press

- (EU) EU makes written submission to US Commerce Dept warning that EU and others will likely respond to tariffs on foreign autos, by targeting $294B in US goods in retaliation - FT

Levels as of 01:30ET

- Hang Seng closed; Shanghai Composite -1.4%; Kospi 0.0%; Nikkei225 -1.8%; ASX 200 -0.1%

- Equity Futures: S&P500 -0.3%; Nasdaq100 -0.3%, Dax -0.5%; FTSE100 -0.5%

- EUR 1.1527-1.1692; JPY 110.62-111.06; AUD 0.7373-0.7410;NZD 0.6765-0.6792

- Aug Gold -0.2% at $1,252/oz; Aug Crude Oil -1.0% at $73.42/brl; Sept Copper -0.2% at $2.96/lb

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1598; (P) 1.1645 (R1) 1.1730; More.....

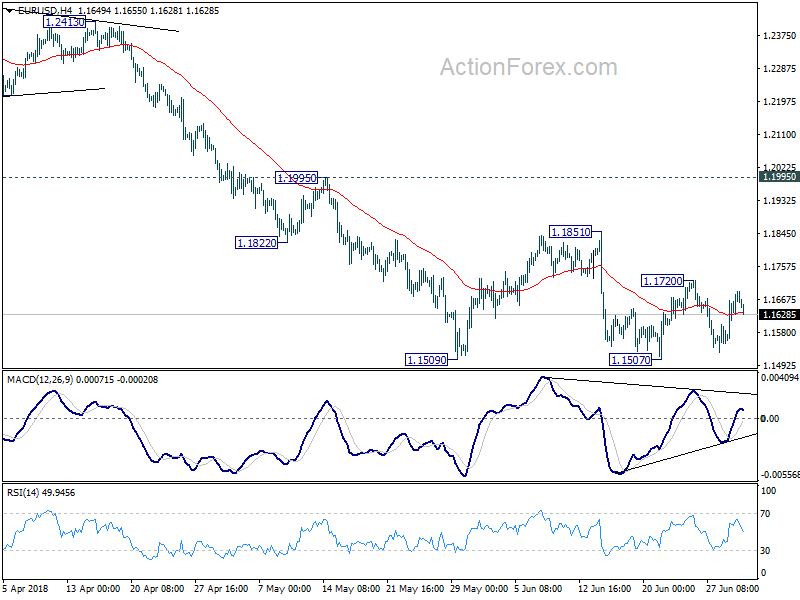

Intraday bias in EUR/USD remains neutral at hit point. Further recovery could be seen. But upside should be limited by 1.1851 resistance to bring fall resumption. Decline from 1.2555 is still in progress. Firm break of 1.1507 will send EUR/USD through 50% retracement of 1.0339 to 1.2555 at 1.1447 to 61.8% retracement at 1.1186.

In the bigger picture, EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

The Swings In Core US And German Bonds Were Moderate

Markets

On Friday, the swings in core US and German bonds were moderate. US yields rose about 2 bp across the curve with the short end slightly outperforming. End of quarter positioning probably played a role. German Bunds outperformed with the very long end doing best (30-y -3.5 bp). A Reuters article suggested that the ECB is considering buying more long-dated bonds when reinvesting maturing bonds from the APP purchases. It also indicated that ECB, to some extent, could deviate from the capital key when reinvesting bonds. In the end, the article had little lasting impact on trading. Intra-EMU spreads narrowed.

This morning, the 10-y note gains gradual ground. Asian equities are losing momentum as the session proceeds. A decline in Japan Tankan confidence and a mediocre China Caixin manufacturing PMI highlight the risk of trade tensions filtering through into the economy. A (modest) rise of the dollar and the yuan again losing ground suggests that we might be heading for a risk-off session. Regarding the data, the US manufacturing ISM will be published. Consensus expects a small decline from 58.7 to 58.5. Markets will look for any fall-out from trade tensions. There might still be additional noise from the US tariffs/trade policy. (European) Bond traders will also keep an eye at the political developments in Germany. At the end of last week, there were tentative signs that, in particular US yields, might develop a short-term bottoming. However, a risk-off context combined with ongoing ‘trade noise' and political uncertainty probably will keep core US and German bonds well supported at the start of the new quarter.

On Friday, the euro enjoyed a remarkable short-squeeze after the announcement of a EU migration deal. In a broader perspective, the dollar rally also took a breather as global sentiment on risk improved, at least temporary. EUR/USD finished the day at 1.1684. USD/JPY understandably decoupled from the broader pause in the USD rally. The pair closed the session at 110.76. This morning, the risk-off trade supports modest USD gains. (DXY trade-weighted dollar at 94.75). The data (US manufacturing ISM) will probably only be of second tier importance for FX trading. Global market sentiment will probably be the main driver. The combination of risk-off (amongst others due to lingering trade tensions) and ongoing political uncertainty in EMU might be a negative for the euro and supportive for the dollar. First short-term resistance in EUR/USD comes in at 1.1720 ahead of the key 1.1851 correction top. For now we maintain the working hypothesis that it won't be easy for the euro to regain that area short-term.

On Friday, the initial euro short squeeze also propelled EUR/GBP above the 0.8850 range top. However, during the day, sterling gained some support as ONS revised upward the Q1 UK GDP from 0.1% Q/Q to 0.2% Q/Q. EUR/GBP finished the day at 0.8847. Today, UK Manufacturing PMI is expected to ease slightly from 54.4 to 54.0. Usually, a risk-off context isn't GBP supportive. However, a euro decline due to European/German political uncertainty might also be a slightly negative for EUR/GBP too. So, for now, the break of the 0.8850 ST range top isn't confirmed yet.

News Headlines

On Sunday the German interior minister, Horst Seehofer, rejected Merkel's negotiated migration deal, saying it was "inadequate" and "not as effective" as his own proposal. Seehofer backpedalled on his initial decision to resign from both interior minister and CSU leader. Instead the party will now seek talks with Merkel's CDU on Monday after which he would make his final decision.

The Chinese Caixin Manufacturing PMI edged lower from 51.1 to 51.0 as trade war concerns are weighing. The BoJ's quarterly Tankan survey of business sentiment highlighted a cooling confidence among Japan's large manufacturers with the index sliding further from 24 to 21 (vs. 22 expected).

Andrés Manuel López Obrador won Mexico's presidential election on Sunday. He's the first left-leaning (anti-establishment) head of the state in four decades. He promised to boost infrastructure spending, increase pensions and revive the economy, all in which the state is to play an important role.

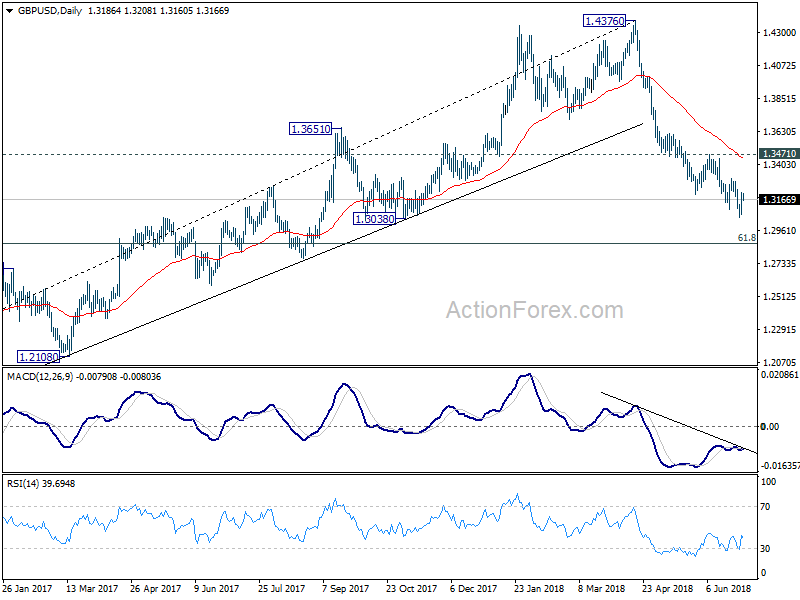

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3111; (P) 1.3163; (R1) 1.3258; More...

Intraday bias in GBP/USD remains neutral for consolidation above 1.3048. At this point, we'd expect upside of recovery to be limited by 1.3314 resistance to bring fall resumption. Below 1.3048 will resume the fall from 1.4376 and target 61.8% retracement of 1.1946 to 1.4376 at 1.2875 first. However, break of 1.3314 will bring stronger rebound back to 1.3471 key resistance.

In the bigger picture, whole medium term rebound from 1.1936 (2016 low) should have completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4179). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 1.3471 resistance holds, even in case of strong rebound.

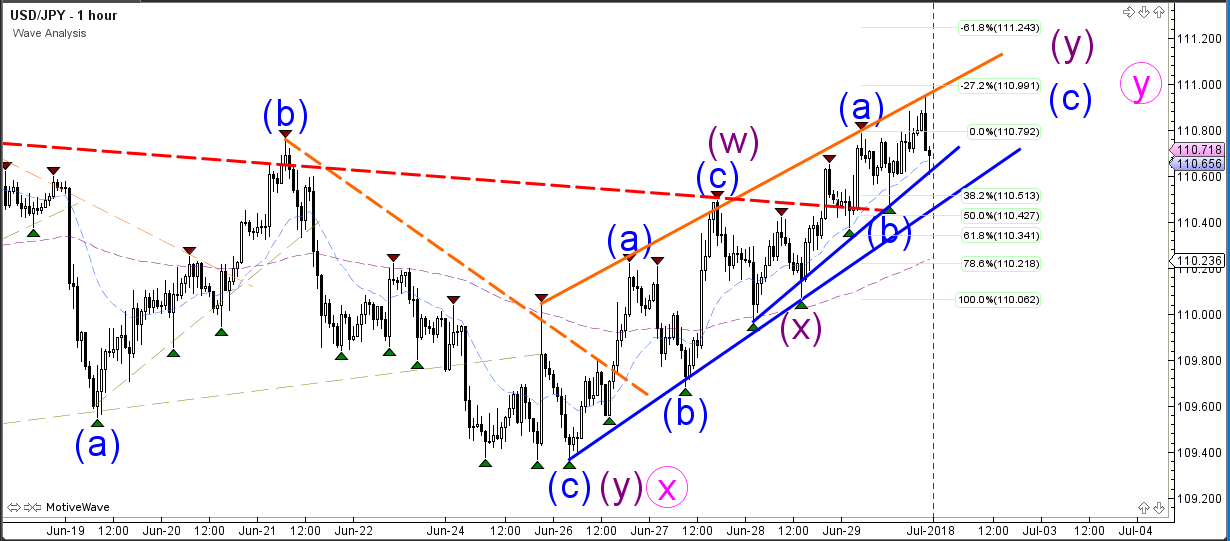

USD/JPY Bullish Channel Breaks Triangle Chart Pattern

The USD/JPY bullish channel is breaking above a key resistance trend line (dotted red) of a triangle chart pattern, which could indicate a larger bullish continuation within wave Y (pink). A break above the previous top at 111.40 could confirm the wave Y of a larger wave D of the daily chart, which is building a triangle pattern.

The USD/JPY could find support at the bottom of the channel and move higher towards the Fibonacci targets. A break below the support trend lines indicates a change of perspective, direction, and most likely wave patterns.