Sample Category Title

Navarro and Mnuchin sent conflicted messages on foreign investment curb

The US markets were confused by the mixed messages from Trump's administration regarding investment restrictions on foreign companies. US Treasury Secretary Steven Mnuchin tweeted saying that the statement regarding foreign investment on tech companies "will be out not specific to China, but to all countries that are trying to steal our technology. DOW dropped nearly -500 pts after the message

But later White House trade adviser Peter Navarro tried to talked down the idea of restrictions on all foreign investments. He said "there's no plans to impose investment restrictions on any countries that are interfering in any way with our country. This is not the plan.: Navarro added that "the whole idea that we're putting investment restrictions on the world -- please discount that."

DOW pared pack some losses after reaching as low as 24084.39. It closed down -1.33% or -328.09 pts at 24252.80. S&P 500 lose -1.37% or -37.81pts to close at 2717.07. NASDAQ suffered the worst decline, losing -2.09% or -160.91 pts to 7532.01.

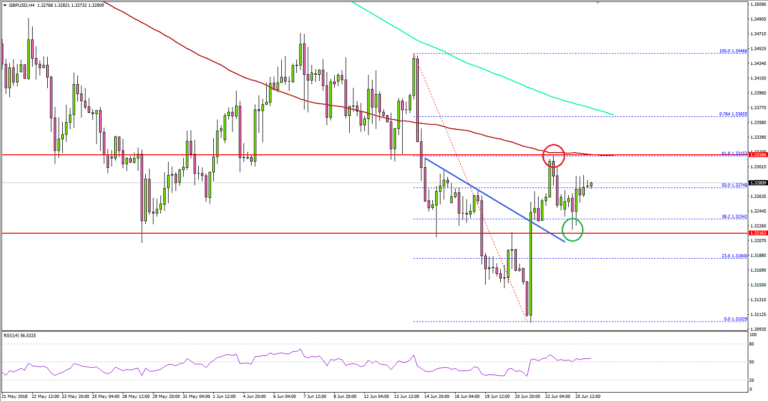

GBP/USD Turned Positive Above 1.3200

Key Highlights

- The British Pound found strong bids near 1.3100 and recovered above 1.3200 against the US Dollar.

- There was a break above a bearish trend line with resistance at 1.3235 on the 4-hours chart of GBP/USD.

- The Chicago Fed National Activity Index (CFNAI) declined in May 2018 from the last revised reading of 0.42 to -0.15.

- Today in the UK, CBI Industrial Trends Survey Realized figure for June 2018 will be released, which is forecasted to post 10% (MoM).

GBPUSD Technical Analysis

The British Pound managed to hold the 1.3100-10 support and bounced back against the US Dollar. The GBP/USD pair broke the 1.3180 and 1.3200 resistance levels to move back in a positive zone.

Looking at the 4-hours chart, the pair was successful in climbing above the 50% Fib retracement level of the last decline from the 1.3446 high to 1.3102 low. During the upside, there was a break above a bearish trend line with resistance at 1.3235 on the same chart.

However, the pair faced a major hurdle near the 1.3315 level and the 100 simple moving average (red, 4-hours). The 61.8% Fib retracement level of the last decline from the 1.3446 high to 1.3102 low also acted as a resistance.

The pair dipped slightly, but the decline was protected by the 1.3230 support zone. It seems like the pair may perhaps trade in a range above 1.3200 for some time before making the next move.

A break above 1.3315 is needed for a push above the 1.3350 level. The next resistance is near 1.3385 and the 200 simple moving average (green, 4-hours).

On the downside, supports are seen at 1.3230 and 1.3200. Below this last, the pair could move back in a bearish zone.

Recently in the US, the Chicago Fed National Activity Index (CFNAI) for May 2018 was released by the Federal Reserve Bank of Chicago. The market was looking for a decline in the index from the last reading of 0.34 to 0.09.

However, the actual result was disappointing as there was a sharp decline from the last revised reading of 0.42 to -0.15. It weighed on the US Dollar and helped pairs like EUR/USD and GBP/USD.

Economic Releases to Watch Today

- UK's CBI Industrial Trends Survey Realized June 2018 (MoM) – Forecast 10%, versus 11% previous.

- S&P/Case-Shiller Home Price Indices for April 2018 (YoY) – Forecast +6.8%, versus +6.8% previous.

France FM Le Maire on trade war: we don’t want an escalation, but we are the ones being attacked

French Finance Minister Bruno Le Maire warned yesterday that "if the United States hits us again with a 20 percent increase on cars we will respond again.." And he emphasized that "we don't want an escalation, but we are the ones being attacked."

Harley Davidsons plans to move production of motorcycles shipped to EU from US to other international facilities to avoid the tariffs. Regarding that news, Le Maire said "whatever allows jobs to be created in Europe goes in the right direction. We don't want a trade war, but we will defend ourselves."

France, Germany and the UK have requested for exemptions from sanctions on their companies for doing businesses with Iran. Le Maire said there was no positive signs from the US. And "for the moment, our requests remain unanswered".

Not Out Of The Weeds Yet

Not out of the weeds yet

After yet another Monday morning equity meltdown in Asia and an equally poor showing across global equity markets. President Trump’s lieutenants Mnuchin & Navarro issued an unequivocal denial the US is considering investment restriction on China. US equity markets have subsequently bounced off session lows were the S&P was down as much -2% at maximum bearish mode to close ~1.3- 1.4 % on the day. Despite the rebound, there remains a considerable degree of scepticism as investors are still no less confident if this is a case of diplomatic doublespeak or a meaningful denial. And keep in mind, we expect to hear about in more details the real Trump administration’s actions taken under Section 301 to respond to China’s alleged theft of US intellectual property which likely means more headaches for investors later in the week and by no means are we out of the weeds just yet. The abundance of mixed and no less confusing signals are causing massive consternations across all asset classes.

Oil Market

Overshadowing oil markets on Monday was a cloud of uncertainty post-OPEC not to mention the web of confusion regarding President Trump’s trade policy.

But at the heart of the matter traders are trying to digest the fact that while OPEC will add more supplies back to the market US inventories will run tight on the prospect of North American supply outages.

As highlighted yesterday, a report that a 350,000 bpd Canadian oil sands upgrader could be offline for the next month, which should lead to increased shortages in the North American supply and deplete vital inventory supplies in Cushing. The anticipated shortfall should be supportive of the U.S. benchmark prices all the while narrowing WTI’s discount to Brent.

Besides declining US commercial inventories, OPEC is adding international supplies back to the market which is naturally weighing on Brent prices and narrowing the spread.

Gold Market

There continues to be less safe-haven demand for Gold as the US dollar continues to be the significant driver behind Gold prices. But with confusing signals on the dollar index that slid back from last weeks highs, while CNH which is plumbing the 2016 depths after the Pboc announced an RRR cut, we’re getting bombed with mixed currency signals across the board.

But with confusion on the dollar front and ongoing chaos in equity markets gold should continue to find a bid at the lower end of the current ranges. But market speculators remain sellers on any rallies to 1275 until further notice as the hawkish Fed has all but taken the wind out of Gold bulls sails.

But it’s hard to ignore this escalating trade war rhetoric and if it does blow up the ensuing equity market purge will undoubtedly attract haven gold demand. And while the dollar currently remains the go-to hedge into US bonds, I suspect longer-term investors will start to look at this gold dip in a favourable light and begin gingerly buying ahead of the US mid-term elections which should add another level of political uncertainty in the US markets. Also, as we approach the significant US refunding periods with an unprecedented amount of bonds coming to markets in August and September, it difficult to see how the dollar will be a winner in this case even more so if trade war drags on and China becomes a lukewarm buyer of the US’s new issues.

Asia Currency Market

Not too unexpectedly $Asia is trading higher in sympathy with the Yuan weakness. While the RRR cut was not that unexpected, the market is starting to read into more aggressive policy shift from the Pock and covering RMB currency risk. As such, the market should remain firmly in buy the dip mode.

The USDKRW is trading off yesterdays highs as the KOSPI held up reasonably well while dealers are respecting month end exporter flow. But today is another day with the Kospi struggling to find traction suggesting some currency pain in the offing.

The much-maligned Ringgit didn’t are so well and getting little support from foreign interest, and with local markets under tremendous stress from capital outflow and the prospect of escalating trade war, indeed the path of least resistance appears higher with the next key focus on 4.05 USDMYR.

G-10 Currency Market

EUR: Despite persistent global and domestic headwinds the Germany Ifo expectations index for June was stable at 98.6 vs the 98.0 expected and continues to support the EUR as dealers continue to trade singularly focused on economic data this week.

JPY: The USDJPY has found some legs overnight, but I’m not convincingly inspired with as risk aversion abounds limiting upside test of 110 where trader remain better sellers.

EM-Currency Market

TRY: Savage price action on bond and swaps markets as traders start to price in a sooner rather than later policy easing has seen the USDTRY reverse all the post-election relief rally and some. Again, the TRY is establishing itself as one of the weakest links in the EM chain and we should expect more pain with little gain.

Eco Data 6/26/18

[php_everywhere instance="1"]

Gold Starts Week with Losses as Tariff Spat Continues

Gold is has posted slight losses in the Monday session. In North American trade, the spot price for one ounce of gold is $1266.80 down 0.26% on the day. It's a quiet start to the week, with only one event. New Home Sales New Home Sales jumped to 689 thousand, well above the estimate of 665 thousand. On Tuesday, the U.K publishes CBI Realized Sales and the U.S will release CB Consumer Confidence.

The escalating trade war between the U.S and China has spooked investors and sent global equity markets sharply lower. Although gold, a safe-haven asset, usually benefits from geopolitical crises, that has not proven the case this time around. Instead, this latest round of trade battle rhetoric has boosted the U.S. dollar, which continues to gain ground against a basket of currencies. In essence, investors and traders have been betting on the greenback rather than on gold. On Thursday, gold dropped to $1261, as it recorded a new low for 2018.

With little in the way of fundamental releases early in the week, the markets are keeping a wary eye on the escalating trade dispute between the U.S. and its major trading partners. The heads of central banks have expressed alarm, and last week, Jerome Powell and Mario Draghi sounded gloomy about the repercussions that a trade war could have on economic growth and monetary policy. On Sunday, the Bank of International Settlements (BIS), which acts as an umbrella group for some 60 central banks also weighed in. The head of the BIS, Augustin Carstens, warned that recent protectionist moves could hamper global growth and financial stability, and could have negative side effects on the currency markets. At the same time, the BIS expressed support for the Federal Reserve raising interest rates gradually and for the ECB heading towards normalization as it winds up its massive asset program.

British Pound Subdued on Lack of Fundamentals

The British pound is unchanged in the Monday session. In North American trade, GBP/USD is trading at 1.3272, up 0.05% on the day. On the release front, there are no British events and only one U.S indicator. New Home Sales New Home Sales jumped to 689 thousand, well above the estimate of 665 thousand. On Tuesday, the U.K publishes CBI Realized Sales and the U.S will release CB Consumer Confidence.

There were no surprises as the Bank of England held the course on interest rates, pegging the benchmark rate at 0.50% for a sixth straight month. However, the markets had expected the vote on rates to be 7-2, so the vote of 6-3 was unexpectedly hawkish. Still, the pound managed only slight gains following the announcement. Attention will now shift to the August policy meeting, with a reasonable chance that the BoE will press the rate trigger and raise rates by a quarter-point to 0.75 percent.

Trade tensions between the U.S and its trading partners continue to escalate, and friction between the EU and the Trump administration could have a negative impact on British workers and companies. On Friday, the EU slapped retaliatory tariffs of some 25% on $3.3 billion of U.S goods. This move was in response to U.S tariffs on EU steel and aluminum imports. However, President Trump has more cards up his sleeves and has threatened to impose 20% tariffs on EU vehicles. The EU has enough on its plate without a trade war with the U.S, and has launched a complaint over the U.S tariffs with the World Trade Organization. Still, the EU has not shied away from retaliatory moves, with EU Commission President Jean-Claude Juncker saying that the EU’s response would be “clear but measured”.

With little in the way of fundamental releases early in the week, the markets are keeping a wary eye on the escalating trade dispute between the U.S. and its major trading partners. The heads of central banks have expressed alarm, and last week, Jerome Powell and Mario Draghi sounded gloomy about the repercussions that a trade war could have on economic growth and monetary policy. On Sunday, the Bank of International Settlements (BIS), which acts as an umbrella group for some 60 central banks also weighed in. The head of the BIS, Augustin Carstens, warned that recent protectionist moves could hamper global growth and financial stability, and could have negative side effects on the currency markets. At the same time, the BIS expressed support for the Federal Reserve raising interest rates gradually and for the ECB heading towards normalization as it winds up its massive asset program.

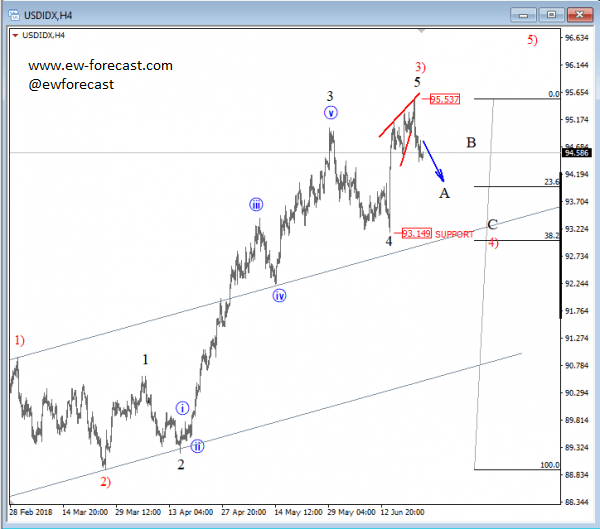

USD Index Pushing into A Temporary Correction; Support at 93.14

On USD Index we see latest recovery from 93.14 as final leg of a bigger impulse that may have found a top at the 95.53 level. A suggestion that a temporary top has been found is intra-day weakness which can be part of a bigger retracement and can push price towards the 93.14 level support region.

This bigger retracment can be a simple A-B-C correction or a more complex pattern as a flat or triangle.

USD Index, 4h

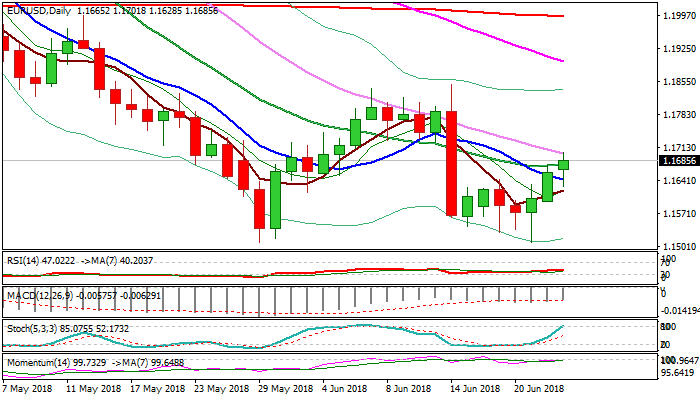

EURUSD Break above 20SMA Could Extend to 1.1717 Fibo Barrier

The Euro holds steady in the US session and cracked psychological 1.17 barrier (also falling 30SMA) on probe above key barrier at 1.1676 (20SMA / converged daily Tenkan/Kijun-sen).

The single currency regained traction after hitting session low at 1.1628 in early European trading, boosted by slightly better than expected German Ifo data for June.

Bulls need close above daily 20SMA for initial bullish signal, confirmation of which would come on break and close above next pivot at 1.1718 (Fibo 61.8% of 1.1848/1.1508).

Bullish hourly / 4-hr studies support near-term action, as rising and thickening hourly cloud (spanned between 1.1640 and 1.1591) underpins.

Corrective dips should be contained by hourly cloud top while extension below cloud would be bearish.

Res: 1.1701; 1.1718; 1.1767; 1.1800

Sup: 1.1676; 1.1660; 1.1640; 1.1591

Japanese Yen Edges Higher, Inflation Report Next

The Japanese yen has posted gains in the Monday session. In the North American trade, USD/JPY is trading at 109.69, down 0.27% on the day. On the release front, the BoJ released its summary of opinions. Later in the day, Japan releases the Services Producer Price Index, which is expected to edge up to 1.0%. In the US, New Home Sales jumped to 689 thousand, well above the estimate of 665 thousand. On Tuesday, the Bank of Japan releases Core CPI and the U.S will publish CB Consumer Confidence.

On Monday, the BoJ published the summary of opinions of last week’s June policy meeting. The summary, which precedes the minutes, indicated that policymakers urged the bank to ‘patiently continue’ its massive easing program. At the same time, some board members expressed concern that the program had undesirable side effects, such as ultra-low rates hurting the profitability of banks. At the June meeting, the bank maintained monetary policy but lowered its inflation forecast. With inflation mired below the BoJ’s target of just under 2 percent, the BoJ is widely expected to continue with its easing scheme well into 2019.

With little in the way of fundamental releases early in the week, the markets are keeping a wary eye on the escalating trade dispute between the U.S. and its major trading partners. The heads of central banks have expressed alarm, and last week, Jerome Powell and Mario Draghi sounded gloomy about the repercussions that a trade war could have on economic growth and monetary policy. On Sunday, the Bank of International Settlements (BIS), which acts as an umbrella group for some 60 central banks also weighed in. The head of the BIS, Augustin Carstens, warned that recent protectionist moves could hamper global growth and financial stability, and could have negative side effects on the currency markets. At the same time, the BIS expressed support for the Federal Reserve raising interest rates gradually and for the ECB heading towards normalization as it winds up its massive asset program.