Sample Category Title

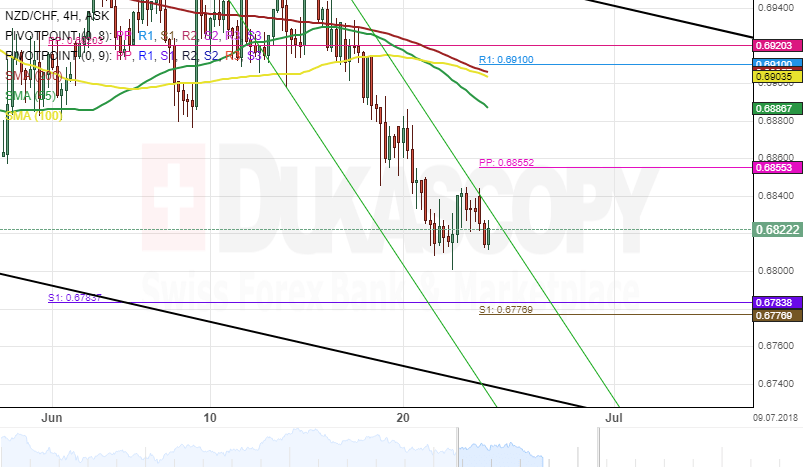

NZD/CHF 4H Chart: Bearish This Week

NZD/CHF currency pair has been trading in a descending pattern during the past two weeks. The exchange rate tested the dominant channel on June 14 and fell to a one-month low level.

A strong resistance cluster set by the combination of the 55-, 100-, 200-, hour SMAs and the weekly and the monthly PPS located near the 0.69 regions has pushed the price lower.

In the meantime, technical indicators flash sell signals during this week sessions, indicating that the currency exchange rate might decline further south toward the bottom border of the dominant pattern.

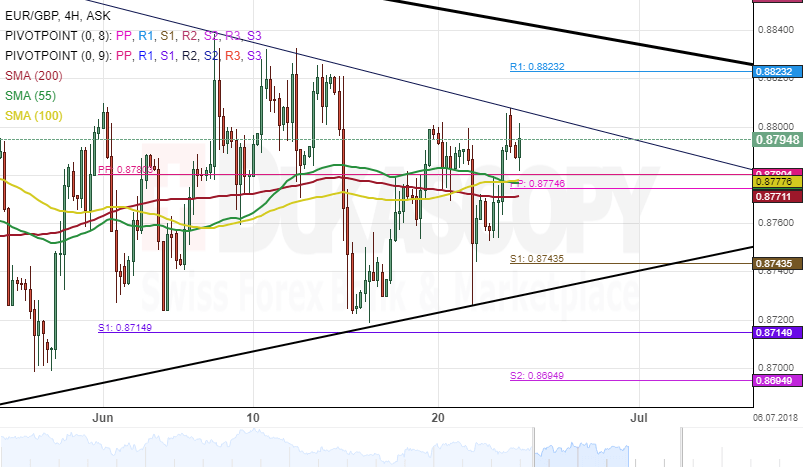

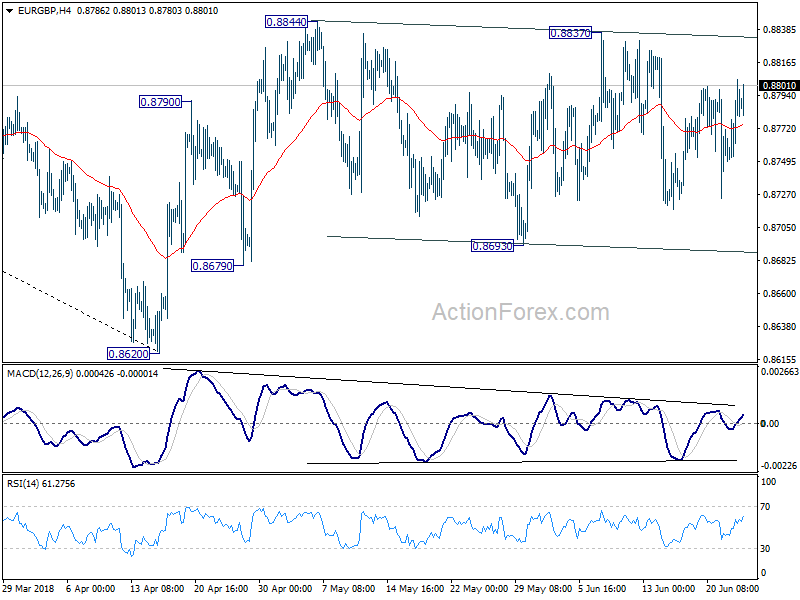

EUR/GBP 4H Chart: Trading Within Range

The Eurozone single currency has been moving in several uptrend and downtrend line against the British Pound since August 2017. The currency pair is currently trading is a triangle pattern.

After hitting the lower boundary of the triangle pattern late last week, bulls took control of the market, as a result, the exchange rate breached a resistance cluster formed by the weekly and the monthly PPs and the combination of the 55-,100-,-200– hour SMAs located near the 0.87 mark.

Given that the currency pair has been moving sideways for a very long time, it is expected that the EUR/GBP pair maintains its trading range during the following trading sessions.

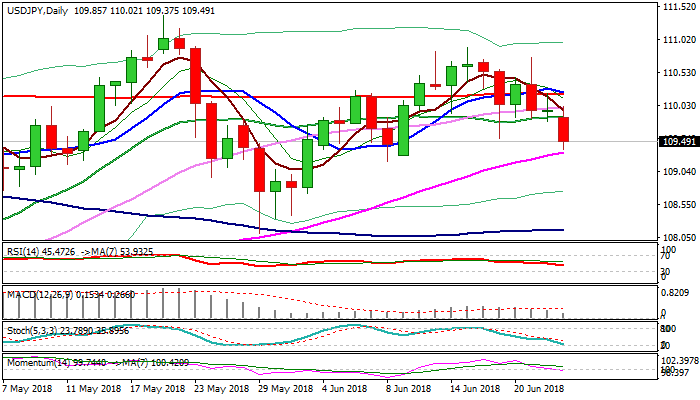

USDJPY Outlook: Fresh Bearish Signal On Close Below Daily Cloud Top/Fibo 50% At 108.50/46

The pair dipped further on Monday as risk aversion on trade war concerns keeps the greenback under pressure. Fresh weakness probed below key supports at 108.50/46 (Fibo 50% of 108.11/110.90 upleg/top of rising daily cloud), close below which would generate strong bearish signal for further weakness. Bearish configuration of daily MA's with multiple bearish crosses and 14-d momentum breaking into negative territory, support scenario. Close within daily cloud would risk test of next pivot at 109.17 (Fibo 61.8% / 08 June trough) and open way for further weakness on break. Conversely, bounce and close above 20SMA (109.86) would sideline immediate downside risk, while close above 200SMA (110.23) would bring bulls back to play.

Res: 109.86, 110.00, 110.23, 110.75

Sup: 109.37, 109.17, 108.77, 108.38

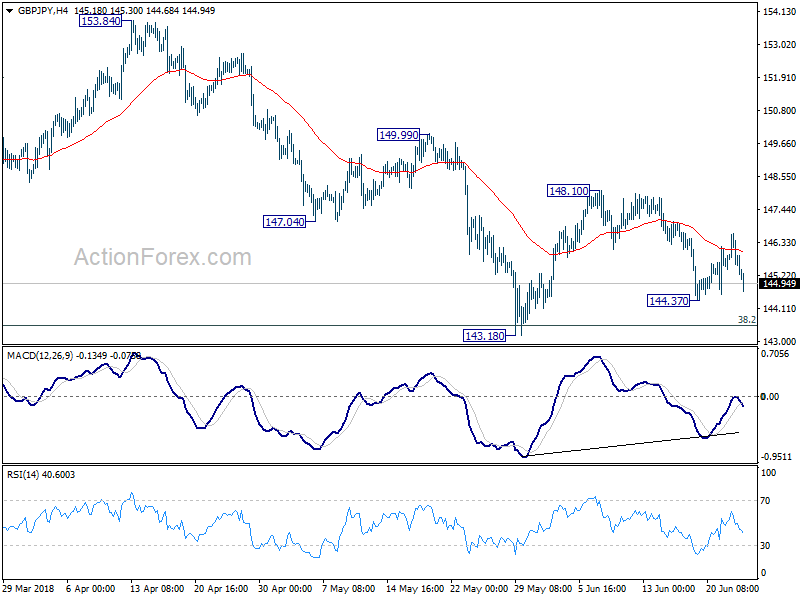

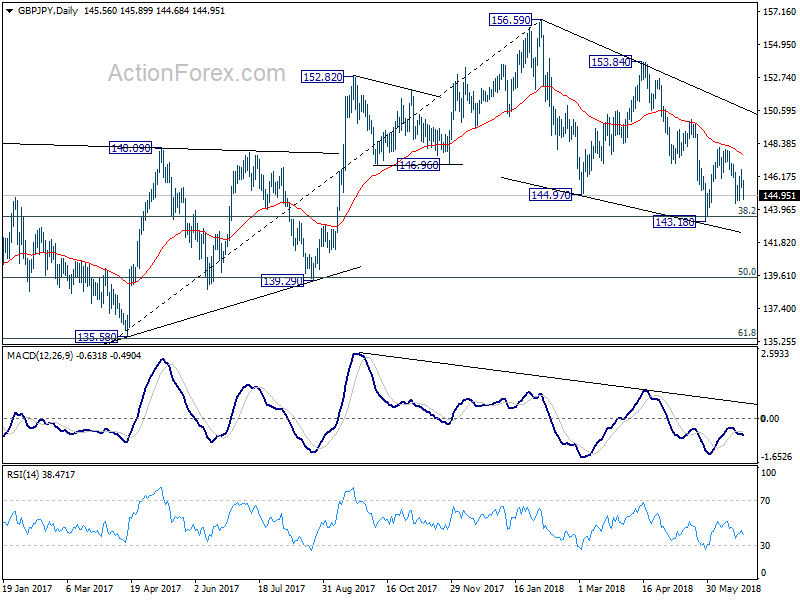

GBP/JPY Daily Outlook

Daily Pivots: (S1) 145.34; (P) 146.00; (R1) 146.54; More...

Intraday bias in GBP/JPY remains neutral at this point. On the downside, below 144.37 will target 143.18 first. Break will resume larger decline from 156.59 and target 139.25/47 cluster support level. However, break of 148.10 will resume the rebound from 143.18 and that will also be the first sign of near term reversal.

In the bigger picture, no change in the view that decline from 156.59 is a corrective move. In case of another fall, strong support should be seen above 139.29 cluster support (50% retracement of 12  2.36 to 156.59 at 139.47) to contain downside and bring rebound. Meanwhile, break of 153.84 should confirm that the correction is completed and target 156.59 and above to resume the medium term up trend.

2.36 to 156.59 at 139.47) to contain downside and bring rebound. Meanwhile, break of 153.84 should confirm that the correction is completed and target 156.59 and above to resume the medium term up trend.

Risk Off Sentiment Forces Market Participants Out Of Risk Assets

Over the weekend President Trump indicated that if trade barriers and tariffs against the US were not removed that he would have no choice but to add further sanctions against those countries targeting the US. Meanwhile China and the EU have agreed to defend against the US position of multilateralism and to promote globalism. The PBOC cut the RRR over the weekend to ease the impact from US tariffs and the stock market fall, giving Chinese banks a 500 Billion Yuan cushion. This led to a small gain in Chinese equities, but with tension still high, that quickly evaporated and European equity futures are pointing to a bearish open. AUDUSD fell to 0.74150 while the Japanese Nikkei 225 is trading around 22300.00 with the yen gaining against GBP, USD and EUR. Oil was up on Friday after OPEC agreed on maintaining current production levels but has pared some of the gains today.

Eurozone Markit Manufacturing PMI (Jun) was 55.0 against an expected 55.0 from 55.5 previously. Markit Services PMI (Jun) was 55.0 against an expected 53.7 from 53.8 previously. Markit PMI Composite (Jun) was 54.8 against an expected 53.9 from 54.1 prior. This data stabilized somewhat, with Services and Composite readings beating expectations and previous readings. EURUSD reached down to support at 1.16408 before heading higher to 1.16747 after the released data hit the market.

Canadian Consumer Price Index (May) was 0.1% (MoM) and 2.2% (YoY) against an expected 0.3% (MoM) and 2.5% (YoY) against 0.3% (MoM) and 2.2% (YoY) previously. Consumer Price Index – Core (MoM) (May) came in at -0.1% from 0.0% previously. BOC Consumer Price Index Core (May) was -0.1% (MoM) and 1.3% (YoY) against an expected 0.2% (MoM) and 1.4% (YoY) from 0.1% (MoM) and 1.4% (YoY) previously. Canadian Retail Sales ex Autos (MoM) (Apr) were -0.1% against an expected 0.5% from -0.2% previously which was revised up to 0.0%. Retail Sales (MoM) (Apr) were -1.2% against an expected 0.0% from 0.6% previously which was revised up to 0.8%. These data points came in softer this month with all missing their consensus reading and most down since last month. Retail sales fell into negative territory this month. USDCAD spiked higher from 1.32776 to set a high for the day at 1.33810 on the back of the disappointing data.

US Markit Services PMI (Jun) was 56.5 against an expected 56.4 from 56.8 previously. Markit PMI Composite (Jun) was 55.1 against an expected 55.1 from 56.6 prior. This data shows a drop in the metrics since last month although it was not as bad as forecast. GBPUSD fell from 1.32901 to 1.32490 as a result of this data.

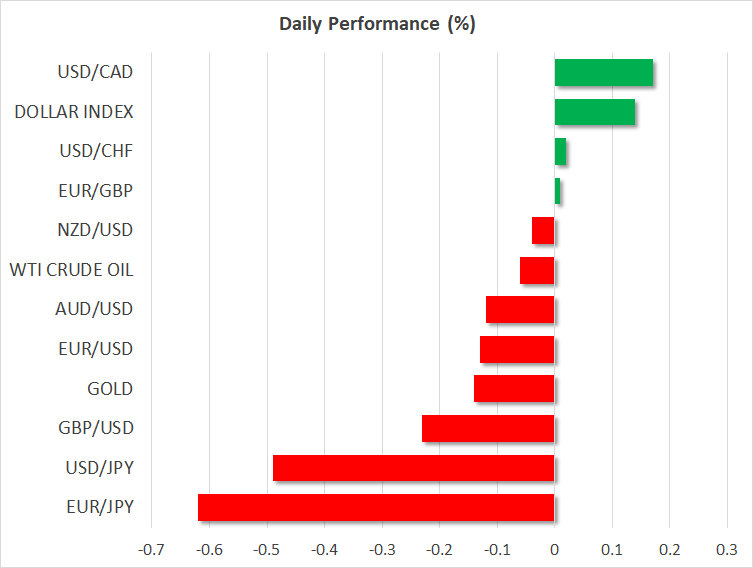

EURUSD is down -0.12% overnight, trading around 1.16414.

USDJPY is down -0.49% in the early session, trading at around 109.440

GBPUSD is down -0.03% this morning trading around 1.32541

Gold is down -0.32% in early morning trading at around $1,265.00

WTI is down -1.44% this morning, trading around $67.97

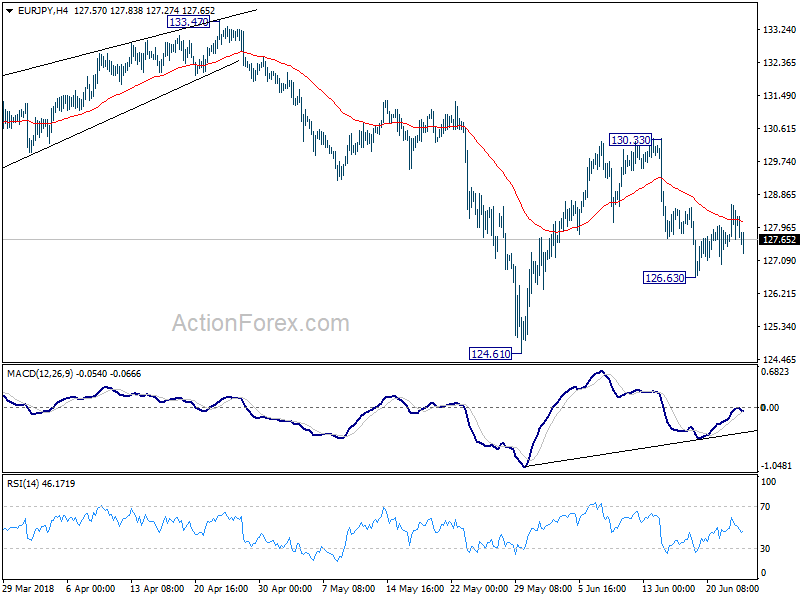

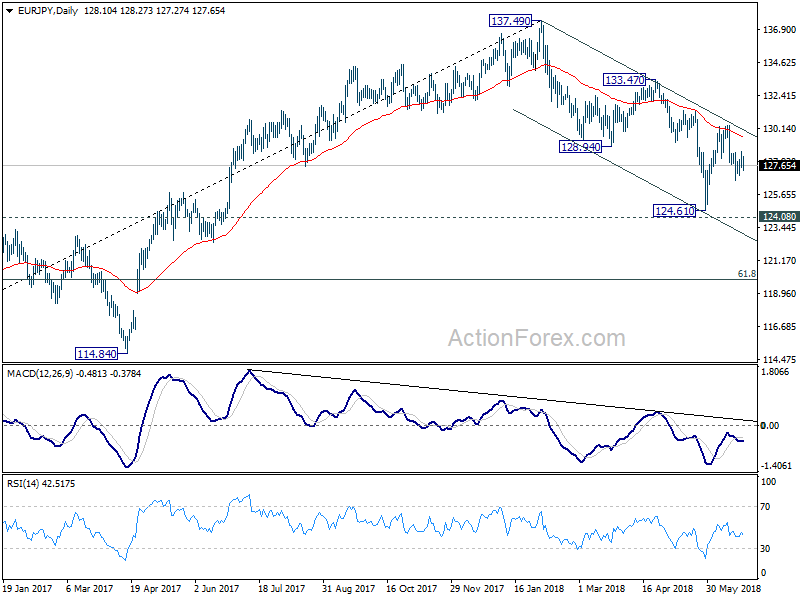

EUR/JPY Daily Outlook

Daily Pivots: (S1) 127.59; (P) 128.09; (R1) 128.73; More....

Intraday bias in EUR/JPY remains neutral at this point. On the upside, break of 130.33 resistance will confirm resumption of rise from 124.61. That will also revive the case of near term reversal and turn bias to the upside for 133.47 key resistance. On the downside, break of 126.63 will bring retest of 124.61 low instead.

In the bigger picture, despite rebounding strongly ahead of 124.08 resistance turned support, there was no clear follow through buying. Note again that there is bearish divergence in daily MACD. Firm break of 124.08 will confirm trend reversal. That is, whole rise from 109.03 (2016 low) has completed at 137.49 already. In that case, deeper fall should be seen back to 61.8% retracement of 109.03 to 137.49 at 119.90 and below. Nonetheless, decisive break of 133.47 key resistance will likely extend the rise from 109.03 through 137.49 high.

Major Data Releases For Today: Focus On Sentiment On A Quite Calendar Day

At 12:30 GMT, Chicago Fed National Activity Index (May) is expected to be 0.09 from a previous 0.34. This data has held above the zero level for 2018 with a high set at 0.88 in the February reading. This shows a healthy economy with the 2018 average at a higher level than previous years. A slip under zero can cause a market reaction but is not a worry in itself with the normal range being re-established. USD crosses can see spikes in volatility during this time.

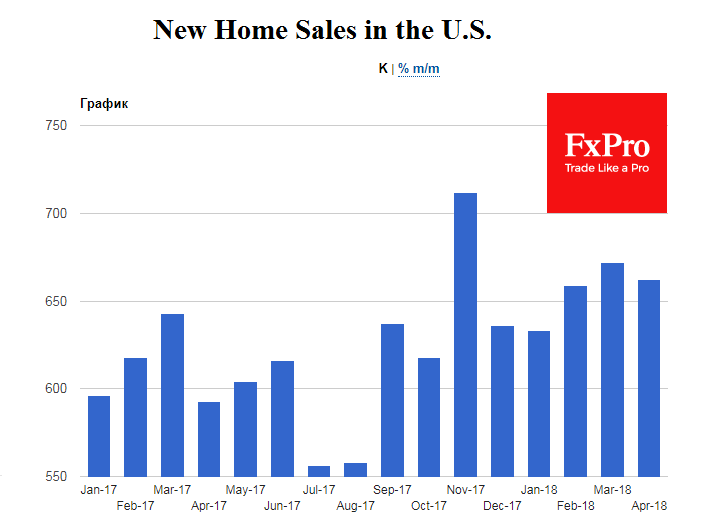

At 14:00 GMT, US New Home Sales (MoM) (Apr) is expected to come in at 0.666M from 0.662M previously. The data is expected to gain some ground on last month and is holding steady between 0.600M and 0.700M. Further improvement in these figures shows a pickup in confidence in the US housing market. USD crosses may be volatile due this data and could lead to further USD strength.

Major data releases for this week:

On Tuesday at 13:00 GMT, US S&P/Case-Schiller Home Price Index data will be released.

On Wednesday at 08:30 GMT, BOE Governor Mark Carney will speak and the Financial Stability Report will be published.

At 12:30 GMT, US Durable Goods data will be out.

At 21:00 GMT, the RBNZ Rate Statement and Interest Rate decision will be released.

On Thursday at 12:00 GMT, German Consumer Price Index data will be published.

At 12:30 GMT, US Gross Domestic Product and Personal Consumption Expenditure data will be out.

On Friday at 09:00 GMT, Eurozone Consumer Price Index data will be released.

At 12:30 GMT, US Personal Consumption Expenditure – Price Index data will come out

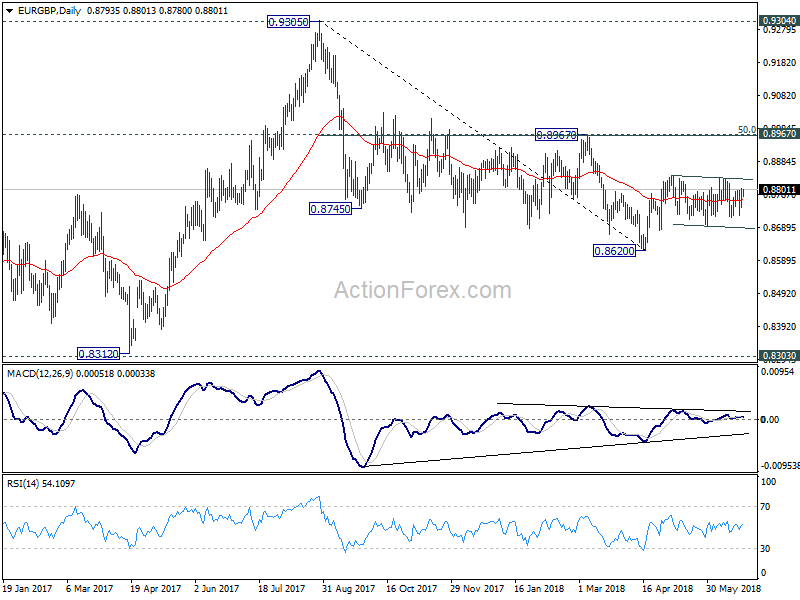

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8758; (P) 0.8783; (R1) 0.8814; More...

Intraday bias in EUR/GBP stays neutral as rang trading continues, inside 0.8693/8844. As long as 0.8693 minor support holds, further rally is in favor. On the upside, break of 0.8844 will resume the rebound from 0.8620 for 0.8967 cluster resistance (50% retracement of 0.9305 to 0.8620 at 0.8963). However, break of 0.8693 will bring deeper fall back to retest 0.8620 low.

In the bigger picture, for now, the decline from 0.9305 is seen as a leg inside the long term consolidation pattern from 0.9304 (2016 high). Such consolidation pattern could extend further. Hence, in case of strong rally, we'd be cautious on strong resistance by 0.9304/5 to limit upside. Meanwhile, in another decline attempt, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

Risk-Off Mood On Back Of Trade Worries Weighs On Equities, Boosts Yen

Here are the latest developments in global markets:

FOREX: The dollar was slightly higher versus a basket of currencies, though it was losing ground versus the safe-haven perceived yen which attracted flows on the back of uncertainty relating to global trade. Specifically, dollar/yen was trading at two-week low levels.

STOCKS: Asian equities were a sea of red after the latest concerns over global trade acted to the detriment of riskier assets. Japan’s Nikkei 225 and Topix indices finished lower by 0.8% and 0.95% correspondingly, while Hong Kong’s Hang Seng shed 1.3%. The negative sentiment looks set to reverberate into Europe with all major benchmarks set to open in negative territory. The same holds true for futures tracking the Dow, S&P 500 and Nasdaq 100; they’re all down by more than 0.5%.

COMMODITIES: WTI and Brent crude were lower at $68.52 and $74.51 per barrel respectively, after surging on Friday following OPEC’s agreement to a modest increase in production relative to what markets expected. In precious metals, gold was again unable to attract safe haven flows, perhaps owed to a US currency that remains relatively elevated; gold is denominated in dollars. The yellow metal was down by around 0.15% at $1,266.74 per ounce.

Major movers: Trade anxiety boosts the yen; commodity-currencies retreat; Turkish lira surges

The dollar index, which gauges the greenback against the currencies of six major US trading partners, edged higher, though by less than 0.2%. Still, the US currency was coming under pressure versus the yen, as safe-haven flows on the back of uncertainty over global trade elevated the Japanese currency, at one point pushing dollar/yen to 109.35, its lowest since June 11.

Also despite trading higher, it is worth pointing that at 94.52, the dollar index was at a relative distance to last week’s 11-month high of 95.53.

US President Donald Trump threatened on Friday to impose a 20% tariff on cars imported from the EU. Adding insult to injury of rising trade tensions, was a report by the Wall Street Journal saying the US Treasury Department is working on blocking investments in US companies involved in “industrially significant technology” by corporations with at least 25% Chinese ownership.

Besides the fall in equities, the risk-off mood was also reflected by the falling Treasury yields; investors were seeking the safety of US government bonds.

Euro/dollar traded lower by around 0.15%, at 1.1640. Besides the trade spat with the US, other near-term drivers for the currency are expected to be Tuesday’s talks between German Chancellor Angela Merkel and the leaders of the other parties in her coalition government; immigration policy is seen as threatening her government.

Sterling was 0.2% down against the dollar ahead of an important EU summit on Brexit on June 28-29.

The commodity-linked aussie, kiwi and loonie, which tend to lose in a risk-off environment, were all lower against their US counterpart on Monday. The Canadian dollar was also sensitive to volatility in oil prices following OPEC’s supply decision.

In emerging markets, the Turkish lira was a big gainer, with dollar/lira trading lower by around 2% after Turkish President Tayyip Erdogan and his AK Party secured victory in Sunday’s presidential and parliamentary elections.

Day ahead: Ifo surveys for Germany and US new home sales due out on quiet data-day; updates on trade to be closely watched

Monday’s calendar is a rather light one, with the Ifo business sentiment surveys for Germany, as well as new home sales data out of the US being the day’s important releases. Any trade updates would either way attract attention, but will perhaps be more closely watched in light of a calendar that is lacking much in terms of releases.

The Ifo Institute’s reports gauging business morale in Germany are scheduled for release at 0800 GMT. The business climate, current conditions and expectations indices are all anticipated to slightly ease compared to May’s respective readings and thus point to worsening sentiment in the eurozone’s largest economy. Specifically, the business climate index, which perhaps generates most interest, is projected to record its seventh monthly decline, while falling to its lowest since H1 2017.

Out of the US, new home sales are expected to have increased by 1.5% m/m in May, after declining by the same proportion in April. The numbers are due at 1400 GMT.

Of course, trade developments (discussed above) will also be eyed, having implications not just for currency markets, but also equities, bonds and commodities.

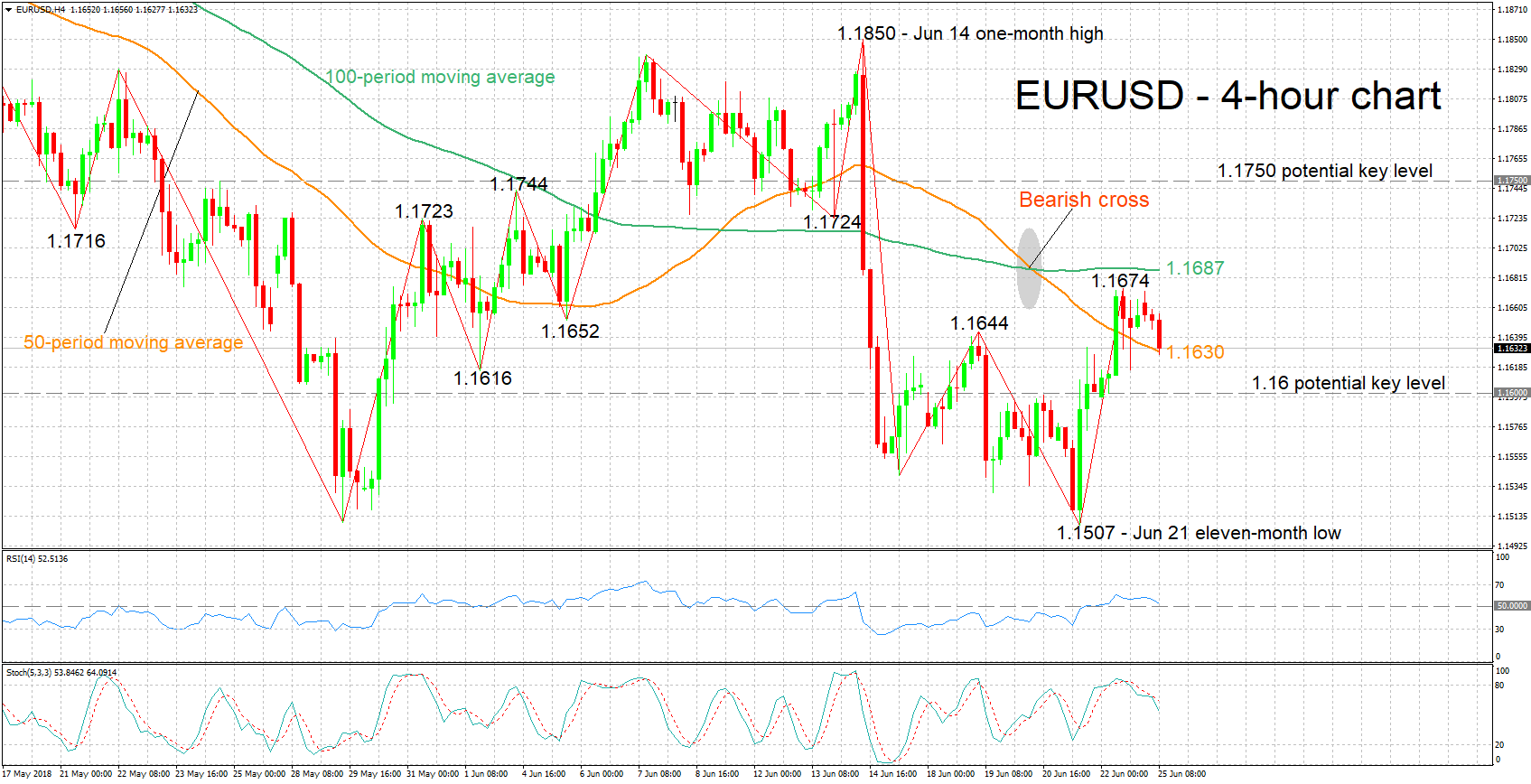

Technical Analysis: EURUSD looking neutral in the short-term; bearish signal by stochastics in very short-term

EURUSD has retreated a bit from Thursday’s 11-day high of 1.1674. The RSI remains in bullish territory above 50 – it is not far above this level – though it has halted its advance and is projecting a largely neutral picture in the short-term at the moment. The stochastics though are giving a bearish signal in the very short-term: the %K line has moved below the slow %D one and both lines are heading lower.

Upbeat views on Germany out of the Ifo surveys later today could boost the pair, with immediate resistance to gains possibly coming around the current level of the 100-period moving average at 1.1687; the area around this point includes the 1.17 figure that may hold psychological significance, as well as Friday’s high of 1.1674. Further above, the zone around the 1.1750 mark that encapsulates numerous tops and bottoms from the recent past and which was relatively congested in previous sessions, may act as an additional barrier to stronger bullish movement.

Conversely, worse-than-expected releases out of Germany may push EURUSD lower. Support seems to be taking place at the moment around the 50-period MA at 1.1630. A downside violation would turn the attention to the 1.16 handle for additional support.

Trade deliberations can also move the pair.

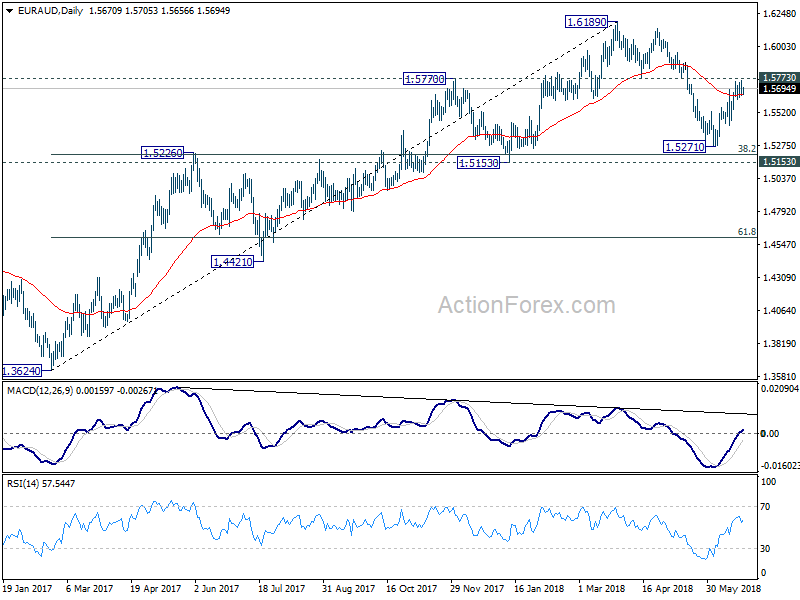

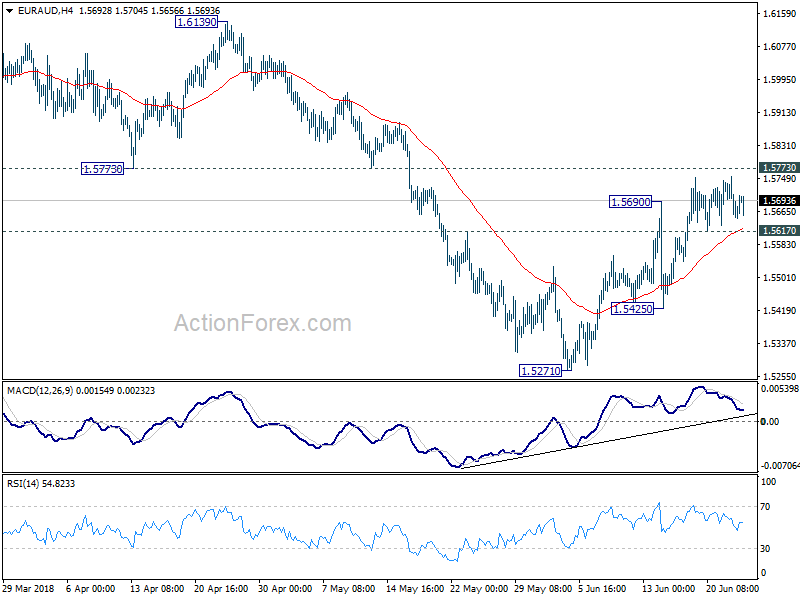

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5628; (P) 1.5692; (R1) 1.5731; More....

Intraday bias in EUR/AUD remains neutral at this point. On the upside, sustained break of 1.5773 will indicate that whole decline from 1.6189 has completed with three waves down to 1.5271 already. And retest of 1.6189 should be seen next. On the downside, break of 1.5617 minor support will turn bias to the downside for 1.5425. Break there will confirm completion of rebound from 1.5271 and target this low again.

In the bigger picture, focus is back on 1.5773 support turned resistance with the current strong rebound. Firm break there will argue that medium term rise from 1.3624 (2017 low) is not completed yet. Further break of 1.6189 will target 1.6587 key resistance (2015 high). Though, rejection by 1.5773 will revive the case of bearish trend reversal and target 61.8% retracement of 1.3624 to 1.6189 at 1.4604.