Sample Category Title

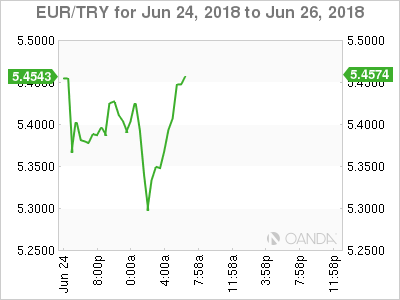

TRY Thumped After Erdogan Win

Monday June 25: Five things the markets are talking about

Global stocks remain under pressure, as investors continues to analyse the impact of a trade spat between the world's two largest economies – U.S and China.

Markets are beginning to get very nervous by the prospect of a full-blown trade war, and this despite the tariffs so far announced by the U.S administration, and China's retaliatory measures, amount only to a small amount of goods. It's the contagion effect to other major economies that the markets are really worried about.

In China overnight, the People's Bank of China (PBoC) sent a strong signal of policy easing by cutting their reserve requirement ratio (RRR) by -50 bps (as expected), to free up fresh liquidity for the real economy. This move may also fuel trade tensions between the U.S and China. The cut comes into effect on July 5, one day before the first round of U.S tariffs on Chinese goods begin.

Elsewhere, the Turkish lira (TRY) temporally surged after Erdogan claimed victory in this weekend's Turkish presidential election.

On tap: The RBNZ meets on Thursday and a 'dovish' message is expected. Stateside, U.S consumer confidence (June 26), U.S durable goods and U.S final GDP (June 28) should provide some interest for investors.

In the U.K and Canada, GDP data unfolds, while in Japan, retail sales, the unemployment rate and industrial production will peek markets interest.

1. Stocks see red

Equities in Asia led the retreat overnight in the wake of reports that the Trump administration is preparing new curbs on Chinese investments.

In Japan, the Nikkei share average dropped as sellers targeted large caps as well as defensive stocks, while the mining sector outperformed after oil prices jumped on Friday. A stronger yen also fuelled the selling pressure. The Nikkei fell -0.8%, extending the weekly drop of -1.6% in the past week. The broader Topix dropped -1%.

Down-under, A pullback in financials helped keep Australia's stock indexes lower, but the S&P/ASX 200 continued to outperform. It fell -0.2% to notch a second consecutive modest drop. In S. Korea, the Kospi closed higher, up +0.3%.

In Hong Kong, stocks touched a six-month low as the U.S plans China tech investment limits. The Hang Seng index fell -1.3%, while the China Enterprises Index lost -1.2%.

Note: The U.S is drafting plans that would block firms with at least +25% Chinese ownership from buying U.S companies with “industrially significant technology.

In China, stocks reversed early gains to close lower overnight, as an expected RRR cut was largely offset by lingering trade war fears. The blue-chip CSI300 index fell -1.3%, while the Shanghai Composite Index slid -1.1%.

In Europe, stocks have opened lower as trade concerns continue to weigh on risk sentiment. A coalition disagreement in Germany is also leading to investor concerns.

U.S stocks are set to open in the 'red' (-0.6%).

Indices: Stoxx600 -0.8% at 381, FTSE -0.8% at 7619, DAX -1.0% at 12456, CAC-40 -0.8% at 5347; IBEX-35 -1.0% at 9689, FTSE MIB -1.2% at 21621, SMI -0.9% at 8539, S&P 500 Futures -0.6%

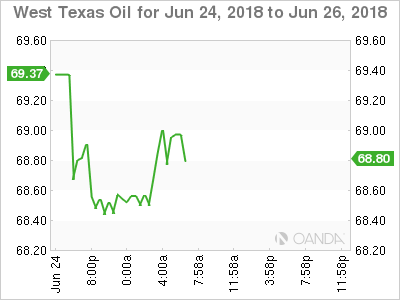

2. Oil prices drop on OPEC's output deal, gold steady

Oil prices remain on the back foot as the market factors in an expected +1m bpd output increase in the wake of last week's OPEC meeting.

Brent crude futures are at +$74.25 per barrel, down -1.7% from Friday's close. U.S West Texas Intermediate (WTI) crude futures are at +$68.42 a barrel, down -0.2%, supported more than Brent by a slight drop in U.S drilling activity and a Canadian supply outage.

Note: Because of unplanned disruptions (Venezuela and Angola), OPEC's output has been below the targeted cuts, which it now says will be reversed by supply increases, especially from Saudi Arabia.

Stateside, U.S energy companies last week cut one oilrig, the first reduction in three-months, lowering the total rig count to 862. While in Canada, an oil sands facility outage could leave North America short of -360K bpd of supply for all of July.

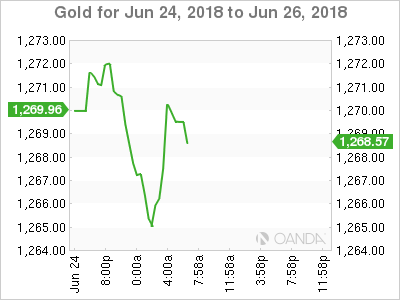

Ahead of the U.S open, gold prices have edged lower, pressured by a strong U.S dollar amid prospects of higher interest rates, while global trade tensions is keeping the 'yellow' metal above its six-month low print last week. Spot gold is down -0.3% at +$1,264.70 an ounce, while U.S gold futures for August delivery are -0.3% lower at $1,266.60 per ounce.

3. Yields fall on risk aversion trading

Global sovereign yields remain under pressure, mostly on trade tensions, but some for other reasons as well.

The yield on Germany's 10-year Bund remains under pressure after E.U leaders failed to reach a deal over the weekend on a new approach to immigration. The 10-year Bund yield fell -2 bps to +0.31%. For directional cues, dealers will now look to the E.U summit on immigration this Thursday and Friday as well as Friday's release of eurozone inflation numbers, which could see core inflation, drop to +1%.

Elsewhere, the yield on 10-year Treasuries fell -2 bps to +2.87%, the lowest in more than three-weeks, while in the 10-year Gilt yield fell -3 bps to +1.291%.

There is only one central bank meeting this week and its Thursday's RBNZ monetary policy announcement where they are expected to deliver a 'dovish' tone and signal again that the next move could be “up or down.”

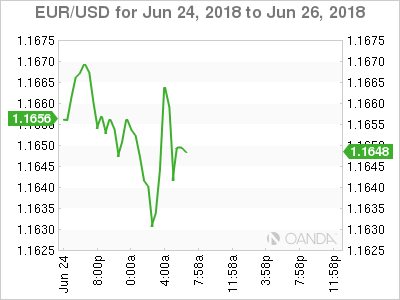

4. TRY temporarily jumped on Erdogan win

The TRY jumped after Recep Erdogan won yesterday's presidential election, and his Justice and Development Party, together with Nationalist Movement Party, grabbed the majority of the seats in the parliament.

The initial moves saw USD/TRY trade down to its lowest in nearly two-weeks of $4.5373. However, TRY is again under pressure, revisiting the concerns that the currency had come under heading into the elections. The TRY ($4.6638) continually hit record lows on the perceived lack of independence of the CBRT bank after the elections.

Elsewhere, EUR/USD (€1.1645) has reversed some of its initial overnight losses despite the continuing disappointment of German data (see below).

5. German business sentiment falls in June

Data this morning showed that German business sentiment deteriorated further this month. According to the Ifo institute, German companies are “less satisfied” with their current business situation.

The Ifo business-climate index fell to 101.8 from 102.3 in May. It marks the lowest reading in 12-months.

Clemens Fuest, the president of the Ifo Institute said, “the tailwinds enjoyed by the German economy are subsiding,”

Note: The Ifo Institute last week scaled back its outlook for Europe's largest economy, forecasting growth of +1.8% in 2018 and again in 2019. Previously, it had predicted growth of +2.6% in 2018 and +2.1% in 2019.

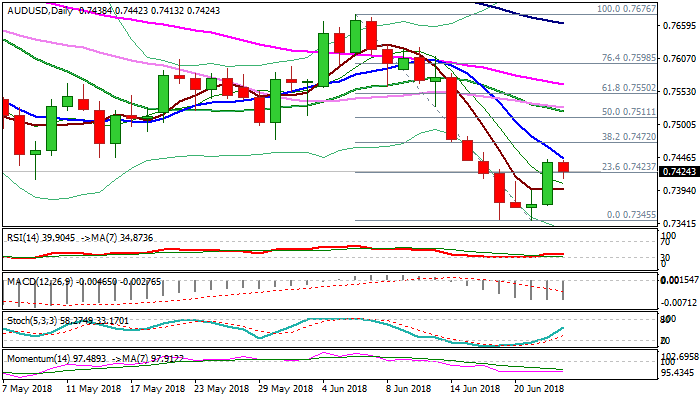

AUDUSD Outlook: Recovery Shows Signs Of Stall As Renewed Trade War Concerns Weigh On Aussie

The Aussie dollar stands at the back foot on Monday and eases from recovery high at 0.7443, posted after strong rally last Friday. Renewed fears over US – China trade conflict increased pressure on Australian dollar, with recovery action off 0.7345 base, starting to show signs of stall. Falling 10SMA capped today's action and additionally weighs (currently at 0.7446), along with bearishly aligned daily techs. The tone could be soured further if trade war concerns intensify. Bearish signal could be expected on break and close below 5SMA (0.7395) which would shift near-term focus lower and open key supports at 0.7345 (19 / 21 June lows) and 0.7325 (Fibo 61.8% of 0.6825/0.8135 recovery). Close above 10SMA is needed to ease pressure, but sustained break above 0.7473 (Fibo 38.2% of 0.7676/0.7345 bear-leg) would provide relief and open way for stronger recovery.

Res: 0.7446, 0.7472, 0.7511, 0.7527

Sup: 0.7413, 0.7395, 0.7370, 0.7345

PBOC Cut RRR, Injecting Most Liquidity to Market So Far This Year

Yesterday, PBOC announced a -50 bps reduction in reserve requirement ratio (RRR) for commercial banks. The move, effective from July 5, aims at easing the tightening in credit condition with the injection of about RMB 700B of liquidity to the market. The decision came in line with our assessment that China, struggling with growth moderation and intensification of trade conflict with the US, would have to adopt a more accommodative policy, with RRR cut a usual tool adopted by the Chinese government. Fed’s gradual rate hike, ECB’s completion of QE later in the year and a more hawkish BOE have contributed to a less easy global monetary environment. While this, together with the elevated debt environment (the need to deleverage) in China, suggests the Chinese government might actually need to adopt a less accommodative policy, the rapid deterioration in economic activities in April and May is alarming and has forced the government shift its focus from deleveraging to growth stability. We expect this dilemma would continue to haunt the government in coming years. A mishandling not only would cause disaster in the world’s second largest economy, but also the world.

"Biggest" RRR Cut in 1H18

The lately announced RRR cut applies to nearly all commercial banks. Yet, the liquidity hence released would benefit certain areas. RMB 500B of which would be injected to 17 large banks (including the big 5 state banks and 12 joint-stock banks) for their use in debt-to-equity swaps to “prudently push forward structural deleveraging”. The remaining RMB 200B would be released to postal savings banks, city commercial banks, rural commercial banks and foreign banks, for their financial support to small- and micro-sized enterprises. PBOC would also indicate how the banks use the funds to support debt-to-equity swaps and small- and micro-sized enterprises financing in their macro-prudential assessment (MPA)

Compared with previous RRR cuts, in January and April this year, the size of the latest reduction is bigger in terms of liquidity injection. Announced in September 2017 and took effect in January this year, the selective RRR cut for banks that meet certain criteria for lending to small business and the agricultural sector, released about RMB 450B to the market. Moreover, the 100 bps RRR cut in April released RMB 1300B in total but RMB 900B of which was used to replace some MLFs. As such, a net of about RMB 400B of liquidity was injected at that time.

Striking a Balance between Easing and Deleveraging

As we have reiterated in previous China Watch reports, PBOC has shifted its focus to a monetary policy stance with slight easing bias, in order to stabilize growth. We also cautioned that the easing bias might intensify as driven by US- China trade conflict. The latest RRR cut has confirmed our view. However, don’t forget the elevated debt and shadow banking problems remain live. China’s Xi Jinping reinforced in early April the firm stance on “structural deleveraging”, settling different deleveraging objectives for different types of debts and debtors. This was echoed by Guo Shuqing, PBOC party secretary and chairman of the CBIRC, earlier this month. He placed the emphasis on the deleveraging of SOEs and local governments. The question arises here is: How can one adopt monetary easing while pledging to deleverage? We expect China to do it via regulatory measures.

The merger of China Banking Regulatory Commission (CBRC) and China Insurance Regulatory Commission (CIRC) in March is a move to concentrate the regulatory power and improve regulatory coordination. Meanwhile, the Ministry of Finance over the past few months announced measures to prohibit state-owned banks from providing any form of funding to local governments and restrict corporate and financial institutions that borrow medium- to long-term foreign debt from requesting or accepting guarantees from local government. The government has also launched the “Guidance Opinions Concerning Standardization of Asset Management Operations by Financial Institutions” in April in order to contain the risk in the financial system.

Under the environment of growth slowdown, escalation of US- China trade conflict and elevated systematic risk, we expect PBOC to adopt more RRR cut in coming months in order to assist SMEs which struggle to survive US tariffs and to stabilize growth, while regulatory measures would be resorted to handle deleveraging of the financial system.

US-China Trade War Builds

US-China trade war heats up

Tensions escalated another notch over the weekend as the Trump administration undertook new retaliatory measures against China. After aiming at aluminium and steel products, then extending the tariffs to a broad range of Chinese products, the White House announced a new set of measures aiming at protecting 'industrial significant technology'. The rules would prevent any company with at least 25% Chinese ownership to invest in US technology firms. Yet the final conditions are not written in stone, as the 25% threshold could be much lower. In addition, the National Security Council and the Commerce Department is also crafting a plan to prevent shipment of key technologies to the world’s second largest economy.

As expected, equity markets reacted negatively to the news with the Nikkei erasing 0.79% and the CSI 300 falling 1.34%. In Europe, the Eurostoxx 600 dropped 0.67%, while the SMI fell 0.78%.

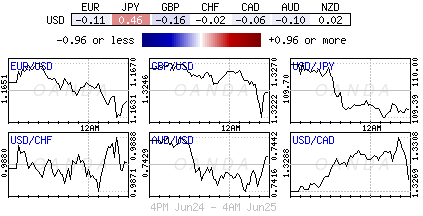

In the FX market, investors took shelter into safe haven currencies with the Japanese yen benefiting the most. USD/JPY fell 0.40% to 109.53, while the Swiss franc’s gains were more modest (+0.10%). Overall, the greenback is benefitting the most following renewed tensions between the two largest economies. It is worth noting that the PBoC lowered the reserve requirement ratio to 15.50% from 16% on Sunday, in reaction to slowing growth and, obviously, potential negative effects from the trade dispute. The pressure on Chinese securities should accelerate further as investors continue to dump equities in anticipation of escalating tensions between the US and China.

Erdogan to govern Turkey for a second term

Turkish elections of Sunday closed as widely expected with a majority of 53% for President Tayyip Erdogan AK party, out of a 99% counting. Erdogan’s main opponent, Muharram Ince from Republican People’s Party gained 31% of the votes, remaining the second largest political party of the country.

Counting in total five political parties in the parliament (threshold of 10% electoral votes reached), the possible collusion among parliamentary members seems reasonable at first sight, but the situation is rather divergent. Indeed, since the constitutional reform in April 2017, which reinforces the power of the leading president (Prime Minister seat abolition, immediate appointment right for top officials positions, right of intervention on legal system and state of emergency enforcement power) and further support of its allies from Nationalist Movement Party in the parliament, Erdogan’s 'People’s Alliance' is projected to win 342 seats out of 600 in the parliament, thus giving a rather weak power to existing opposition.

Following the news, the lira, which depreciated by -21% against the dollar since the beginning of the year is currently strengthening. USD/TRY is valued at 4.5942, trading lower since 4.7456 high (22/06/22018 high) and approaching the 4.5839 range in the short-term. Our scenario remains however a stronger USD/TRY due to current events in the mid-term. We think that recent lira rally is unsustainable, as the situation should lead the leading party to take unilateral actions (politically and economically), without consulting diverging opinions from opposition and which could have negative consequences on both the domestic economy and its relationship with commercial partners.

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 1.1652

The outlook is positive above 1.1600, for a break through 1.1670, towards 1.1730.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.1675 | 1.1730 | 1.1600 | 1.1480 |

| 1.1730 | 1.1830 | 1.1510 | 1.1300 |

USD/JPY

USD/JPY

Current level - 109.46

The downtrend from 110.80 is still underway, aiming at 109.20, en route to 108.60. Initial hurdle lies at 109.80.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 109.80 | 111.40 | 109.20 | 107.80 |

| 110.80 | 114.40 | 108.60 | 106.70 |

GBP/USD

Current level - 1.3241

Current slide after 1.3312 peak should be considered corrective and 1.3215 support is expected to provide a reliable base for another leg upwards. Intraday trigger lies at 1.3270.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3270 | 1.3618 | 1.3215 | 1.3040 |

| 1.3460 | 1.3990 | 1.3100 | 1.3040 |

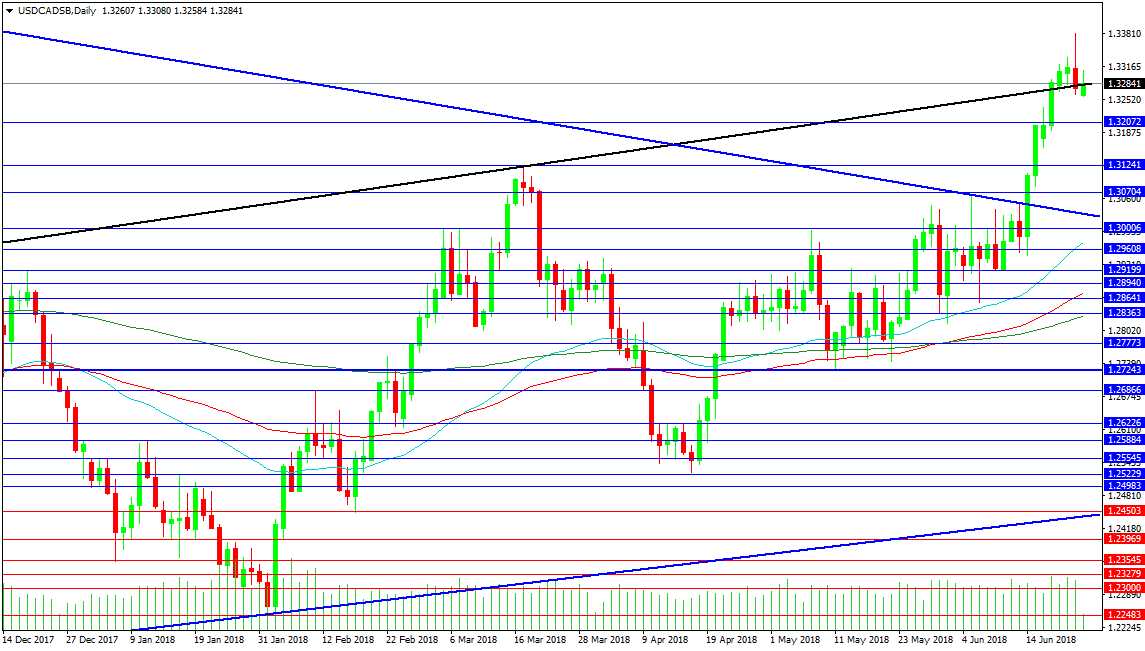

Forex Analysis: USDCAD

The USDCAD pair has been trading over the past week with one eye on the OPEC meeting in Vienna. When the announcement was made on Friday that production levels would remain on hold with a greater focus on compliance, the pair moved lower to retest the rising black trend line at 1.32765. Today there is a push back higher after news that OPEC plans a small production boost. Resistance is now set at today's high of 1.33080 and the 1.33000 level. A breakout higher would wish to test last week's high at 1.33810.

Support at today's low comes in at 1.32584 with the 1.32000 level below. This is followed by the 1.31240 level and the 1.30700 area. A retest of the trend line at 1.30300 could see a resumption of the move higher as buyers step in to take advantage of lower prices. As the trend line falls through time it will be supported by 1.30000. The 50 DMA is found at 1.29738 and as it rises will also support the level. The 100 DMA is at 1.28750 and the 200 DMA is slowly rising past 1.28300.

Forex Analysis: AUDJPY

This pair is testing its weak support trend line also after rejecting from the 84.500 area early in the month. The pair moved lower today on fresh fears of an escalation in the trade war between the US and China with US President Trump calling for countries imposing tariffs on the US to remove them or face fresh tariffs from the US. The PBOC also took action to ease the burden of the tariffs on Chinese companies by cutting the RRR. Support for the pair now comes in at the 81.000 area followed by the 80.500 area. A key test will be the 80.000 level with a push below targeting 79.162. The Japanese are perusing a policy of requesting exemptions from US tariffs.

Resistance for the AUDJPY pair comes from Friday’s retest of the 81.952 level. A break higher looks to test the 82.563 level with the 50 DMA at 82.682 and the 100 DMA at the next resistance point at 83.320. There is a stronger resistance zone at 84.000 containing the 200 DMA at 84.133 and the 84.500 ceiling. This would be a key line to break for those expecting higher prices and this would become supportive should price break higher to 85.594 and beyond. Ultimately a move back to the January highs at 89.000 provides traders with a target to aim for.

Oil Drops Lower On Hedge Fund Bets | Global Trade War Under Focus

- Hedge funds have reduced their long bets

- Iran, Venezuela and other OPEC members were clearly not on the same page

- Trade tensions remain the main focal point for investors

Oil traders want able to celebrating the OPEC decision for long and the oil price has moved lower as a result of this. A moderate increase was the phrase which saved the day for oil but investors have decided to play a waiting game. Looking at the WTI net long positions, it becomes clear that hedge funds have reduced their long bets and they are expecting a lower move in the oil price. Similarly, oil explorers decided that it is time to ease off their drilling operation and last week for the first time in three months we have seen a reduction in their activity.

Opec decided to bring another one million barrel per day back on the market starting next month. The question is if OPEC members would comply with this or if we are going to see more oil on the market given that the cartel is surely divided now. Iran, Venezuela and other OPEC members were clearly not on the same page with OPEC’s decision.

The global battle over trade is going to impair global economic growth and it is also rattling investor's confidence. These trade tensions remain the main focal point for investors today as the situation has intensified further. Europe has warned that it will react harshly if the US levies tariffs on EU cars. Donald Trump has intentions to impose 20% tariffs on European cars, he reasons adopting such a strategy would surge the demand for American cars. He could change his policy if the EU removes barriers to all American goods. Trumps’s action has a serious reaction and the evidence is available in Turkey, the country has already imposed tariffs on American rice, cars and whiskey and this was effective from June 21. There is no doubt that the EU, China and other countries would react in the same manner.

Back in the U.K., after a series of threat from major corporates, the prime minister Theresa May is under major pressure to carve up a contingency plan under a no deal Brexit scenario. Major corporates which add a considerable amount of growth and support employment in the U.K. decided to show Theresa May that the government needs to put its act together.

Bitcoin dropped below a key level of $6K over the weekend before bouncing back above this mark. There is very little good news for the crypto king and most of the bull momentum has faded and this lead us to believe that it is likely that we would see the price dropping below the $6K mark again. The key support level remains at 5605 which was the lowest point back in November last year. If we break this low, the selling pressure would intensify further.

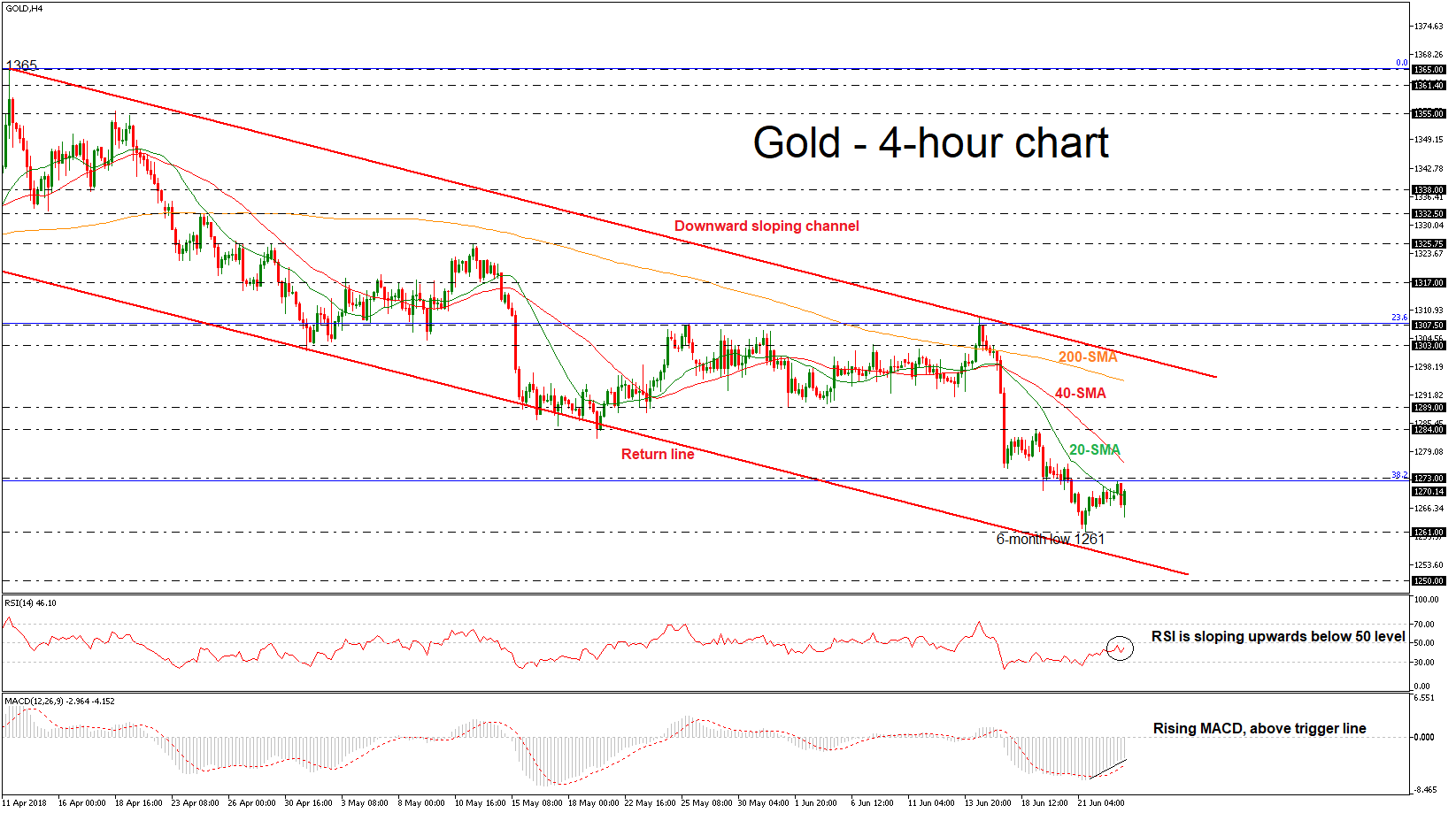

Gold Finds Strong Obstacle On 38.2% Fibonacci, Remains In Bearish Mode In Long Term

Gold rebounded on the six-month low of 1261 on Thursday and drove the price until the 38.2% Fibonacci retracement level of the upleg from 1122 to 1365, around 1273. Currently, the precious metal is trading above the 20-simple moving average (SMA) in the 4-hour chart, increasing the chances for upside movement. Technical indicator in the short-term are suggesting further advances.

The Relative Strength Index (RSI) is sloping upwards below the threshold of 50, while the MACD oscillator is rising in the negative territory and above its red-trigger line.

Should prices reverse higher, immediate resistance could come at 1273, which is the 38.2% Fibonacci level. Above that, would take the price closer to the 40-SMA, which could act as major obstacle near 1276.55 at the time of writing. A successful surpass of this zone would open the way towards the 1284 barrier.

To the downside, there is immediate support at the six-month low of 1261, while below that, the next support to watch is the 1250 hurdle, which holds below the descending channel.

In the bigger picture, the yellow metal has been developing within a downward sloping channel since April 11, indicating that the price remains in bearish mode in the long term.

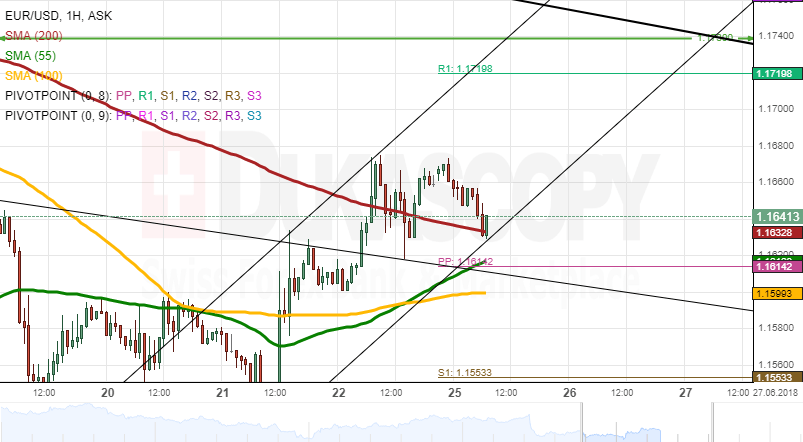

EURUSD Analysis: Reveals New Pattern

After the breaking of the previously mapped channel down pattern, the common European currency has traded sideways against the US Dollar. However, as the consolidation occurred, a new junior channel pattern was spotted.

The pair is trading in a junior ascending channel pattern, which was set to guide the currency exchange rate up to the first weekly resistance near the 1.1720 mark.

However, in the short term the rate looked like waiting for additional support to begin the mentioned surge. The support most likely would be provided by the approaching 55-hour simple moving average, which would strengthen the support cluster near the 1.1630 mark.