Sample Category Title

Mnuchin blames WSJ and Bloomberg on fake news

US Treasury Secretary Steven Mnuchin blamed WSJ and Bloomberg on "fake news". That's regarding the report on Trump's intention to limit Chinese investments in US tech companies. Mnuchin said in his tweet that a statement will be out "not specific to China, but to all countries that are trying to steal out technology".

https://twitter.com/stevenmnuchin1/status/1011258207182966786

First of all, who else is "stealing" other than China?

Secondly, definition from Oxford dictionary on the verb "steal" - Take (another person's property) without permission or legal right and without intending to return it.

When some buy a company, is the property of the company "another person's property"?

Or now, you forbid them to buy the company, so that they have to "steal"?

Anyway we don't expect anything more than that from Trump and his team.

Trump Stokes Trade Wars With New Threat of New Tariffs against China

Just as the financial markets were beginning to the digest the first round of trade tariffs that were imposed, the U.S. President Trump kicked off the week announcing a new round of potential tariffs on imports from China.

This sent the markets into a nervous frenzy with risk appetite waning despite the fact that no one knows whether President Trump would follow through on his new threats to impose fresh tariffs on Chinese manufactured goods.

The fresh threats comes just a few weeks after news reports suggested that China and the United States were taking a reconciliatory tone against the first round of tariffs that were imposed on China which was later followed by China's own tariffs on imports from the United States.

Furthermore, the steel and aluminum tariffs that were announced previously were underway after the one-month exemption expired against Canada, Mexico and the Eurozone.

The Eurozone, for its part has filed a complaint to the World Trade Organization against the United States. The latest threats of tariffs which could potentially amount to $200 billion worth of goods imported from China saw the markets giving a nervous reaction.

The reaction was best seen in the U.S. equity markets with the Dow Jones Industrial Average seen almost giving up the gains notched during the previous months of the year. The exception was the UK's FTSE100 which gained while the Pound sterling hit a fresh seven month low.

Reports from the Financial Times showed that despite the threats, the U.S. administration was not actively seeking any talks with their Chinese counterparts. A senior member of the White House apparently said that after giving China nearly a year to discuss and address the U.S. complaints, failure to make any headway since a year resulted in no more discussions being planned.

The uncertainty comes just after China's ruling party held its annual event earlier this year where promises were made to open up China's markets including increasing foreign shareholders to a majority stake in key industries such as automobiles and insurance.

Economists continue to remain divided, but most agree that Trump is expected to play hard until the U.S. mid-term elections in an effort to put his "America First" campaign. However, this is also expected to put some of the key industries at risk.

India, which was also hit among other countries by the new tariffs retaliated by raising import taxes on luxury two-wheelers from the U.S. This was seen pushing some of the key stocks in the sector lower.

The uncertainty surrounding President Trump's rhetoric on trade was also echoed by various central bankers, especially from the G7 economies. Almost all central bank chiefs including the U.S. Federal Reserve Chairman, Jerome Powell have cited the "trade uncertainty" as a key risk that could derail the central banker's efforts towards moving their respective economies to an era of higher interest rates.

Mario Draghi, the ECB President recently said in his speech in Portugal that the global trade uncertainty remained a key factor. He also mentioned higher oil prices due to increased geo-political risks as another factor that could derail the central bank’s goals of moving towards policy normalization.

While it is still unclear, the baseline narrative is that economists and analysts remain divided on the impact of the new tariffs, if and when the U.S. administration hits China with. China, on its part is said to be preparing with retaliatory tariffs on the U.S. manufactured goods while also admitting that this would not benefit the global economy.

For the moment, the uncertainty has given way to higher volatility in the financial markets, which is also another cause for concern among policy makers.

ECB Research: Euro Area Inflation – Not Out of the Woods Yet

- There are rays of hope for the outlook on euro area inflation and accelerating wage growth raises the prospect that the gradual rise in core inflation will continue.

- We remain somewhat sceptical on the resilience of the inflation outlook, as especially domestically generated price pressures remain muted.

- While inflation is moving in the right direction, further growth deterioration may delay the ECB's next steps.

At the June meeting, the ECB announced an end date to its QE programme, citing growing confidence in the path of inflation towards its aim. Especially the ongoing economic expansion and the corresponding absorption of economic slack, well-anchored (long-term) inflation expectations and not least rising wage growth were mentioned by Mario Draghi as drivers behind this growing confidence.

To gauge whether SAPI (sustained adjustment in the path of inflation towards the 2% target) is fulfilled, the ECB looks at three factors: (1) convergence: (2) confidence and (3) resilience. Indeed, when comparing the ECB's inflation projections across time, there is clear evidence of convergence, (i.e. they have become more 'accurate'). HICP inflation has picked up from the low levels observed in 2015 or even early 2016. Deflation risks have disappeared and the ongoing expansion has given ECB President Mario Draghi and other members more confidence in the inflation outlook, reflected in the smaller confidence intervals of the projections. However, it is also fair to say that the ECB has persistently overestimated the actual inflationary pressures in recent years.

Is this time different?

A good starting point to answer this question is to look at the euro area labour market. We see signs that the Phillips curve relationship has started to work again and the rapid fall in unemployment in recent years coupled with increasing labour shortages in some countries has started to translate into higher wage growth. In particular, negotiated wages have risen from their subdued levels. A big driver for this development has been Germany, where recent bargaining rounds in the metal & electro industry, construction sector and public administration have all resulted in significantly higher wage increases compared to previous years.

While the increase in euro area wage growth to 1.9% in Q1 18 is clearly good news for the ECB, it also masks an underlying country divergence. Whereas wages rose by 2.7% in Germany and 2.0% in France in Q1, wage pressures in Spain and Italy remain very subdued, due in part to remaining slack in the labour market, with the unemployment rate lying above the natural ('NAIRU') level.

Several factors, not least higher inflation expectations that affect the backward looking wage formation process, speak in favour of accelerating euro-area wage growth in the future, but what ultimately matters for core inflation is the wage increase relative to productivity growth (i.e. unit labour costs). In its projections, the ECB assumes a flat profile for labour productivity growth of 0.9% over the coming years, leading it to expect a significant uptick in ULC and thereby core inflation, averaging 1.6% in 2019 and 1.9% in 2020. A rise in productivity growth, for example on the back of productivity enhancing investments, hence remains a downside risk that could weaken the wage price spiral.

Underlying inflation pressures: a mixed picture

Overall, the evidence that the recent pickup in wage growth has translated into higher underlying inflation pressures remains scant so far. Although core inflation rose back to 1.1% in May from 0.8% in April, the details reveal that the increase has been driven mostly by one-off factors (i.e. a rise in volatile travel-related items due to the different timing of Whitsun in 2017 versus 2018). Hence, we remain sceptical as to whether we will see similarly strong increases in core inflation in the coming months and expect it to reach 1.5% only towards the end of 2019.

What is the evidence for rising underlying inflation pressures when we look at alternative measures of inflation? Super core inflation (which only includes HICP items linked to the output gap) edged up to 1.3% in March, which is an encouraging sign, although its responsiveness is still lagging developments in the output gap. In terms of country composition, a similar picture to wage growth emerges with core countries such as Germany and France being the key drivers.

Another interesting measure to follow is our domestically generated inflation measure, which includes only locally sourced HICP items and aims to filter out the (mostly negative) impact of international factors and globalisation. This measure has stagnated around the 1.3-1.4% level since the beginning of 2018, indicating that domestically generated price pressures have yet to show a convincing upward trend in response to recent higher wage growth even when neglecting the impact from global factors.

Negligible effects of EU tariffs on US goods

With the EU imposing 25% tariffs on EUR2.8bn of US goods on 22 June in retaliation to US tariffs on steel and aluminium, the question arises to what extent this would affect the eurozone inflation outlook.

Judging from the list of items affected, the impact should show up mainly in food and NEIG inflation. A quick 'back of the envelope' calculation reveals that the aggregate inflation impact should be relatively muted. EUR2.8bn constitutes only roughly 0.05% of total private consumption expenditure in the euro area and even when assuming a full 25% pass-through to consumer prices, it should only lift total HICP inflation by roughly 0.01 percentage points. Furthermore, substitution and competition concerns could further dampen the actual pass-through to inflation and the effect is likely to come with a lag due to price stickiness. Hence, at least in its current form, we do not consider EU tariffs a game changer for euro area inflation.

Eurozone inflation: growing convergence and confidence, but resilience still lacking

Overall, we share the ECB's more optimistic view on the outlook for euro area inflation. Inflation has clearly shown signs of convergence, both market- and survey-based inflation expectations have risen and accelerating wage increases make us more confident that the gradual rise in core inflation will continue going forward. However, we emphasise that it will be a gradual rise and the ECB's core inflation forecast of 1.9% in 2020 remains optimistic, in our view, not least because the economic momentum in the euro area is abating, with growth expected to fall back to potential by 2020. The last time we had core inflation at 1.9% was before the financial crisis in 2007, when GDP growth was 3.1% and significantly above potential.

We remain somewhat sceptical on the resilience of the inflation outlook. Although headline inflation will remain close to 2% over the coming months, this is mainly due to energy prices. In light of our and markets expectation that oil prices will not rise further, the positive contribution from energy prices will abate from late 2018 onwards. At the same time, different measures of the underlying inflation pressures in the euro area still paint a somewhat mixed picture, with especially domestically generated price pressures still muted. A recent ECB publication, which looks at different measures of underlying inflation for the euro area, arrives at a similar conclusion. Hence, we expect the ECB to stick to its mantra and remain patient, prudent and persistent.

In the right direction - but growth deterioration may delay ECB steps

Although the June meeting saw a significantly more upbeat assessment of the inflation outlook, it was also conditioned on the still very accommodative monetary policy stance. Regarding the APP impact on inflation, Draghi said that the overall impact on euro area inflation 'is estimated by the ECB to be […] around 1.9%-points cumulative in the period between 2016-2020'.

We have argued for a while that QE could be ended because of solid growth and vanishing deflation risks, but that the timing of the first rate hike will depend on the inflation dynamics. In line with the ECB's most recent forward guidance ('rates will remain at present levels at least through the summer of 2019'), we still believe that the first deposit rate hike will come in only 1.5 years' time.

While ECB is more confident on the inflation dynamics, we also take note of the more downbeat assessment on the growth outlook, in particular in light of the recent protectionism / trade war risks. In a recent interview, Chief Economist Peter Praet indicated that the end of the APP by the end of the year is not a firm decision but subject to incoming data. The ECB's 'anticipation' of ending QE could be derailed if data deteriorates markedly. We would expect the ECB to change stance should the growth outlook turn significantly sour from its 2.1% expected growth this year, to somewhat below the potential growth (estimated by EC around 1.5%).

Sunset Market Commentary

Markets

Today, especially equity markets started the week in risk-off modus. Ongoing trade tensions between the US and China and the conflict potentially spreading to Europe was a good reason for investors to stay cautious on global equities. European stocks and US equity futures soon showed substantial losses. Core bonds only succeeded some modest gains early in European dealings. German IFO confidence declined from 102.3 to 101.8, in line with market consensus. The forward looking expectations component of the IFO was even slightly better than expected. Core bonds soon gave up their earlier gains. At the moment of writing, changes in US and German bond yields are less than 1 bp. Overall risk-off sentiment and a positive election result of the Italian Lega Party in local elections caused Italian assets to underperform. The 10-y yield spreads of Italian government bonds versus Germany rose another 10 bp. Changes in most other spreads are modest (2 bp or less). Today’s price action suggests that core (US and European yields) have already declined to relatively low absolute levels making it more difficult for core bonds to rise just on the theme of global, trade-driven risk-aversion.

EUR-USD. Today, EUR/USD proved to be quite resilient, even as the trade conflict between the US and China (and maybe also with the EU) might escalate further. Also in a broader perspective, the gain of the dollar in this risk-off context remains modest. USD/JPY dropped to the 109.40/50 area, but there was no follow-through yen buying later in the session. EUR/USD developed a similar trading pattern. The euro lost a few ticks early this morning, but the downside proved rather solid. EUR/USD also profited slightly from a decent German IFO release. Technical factors were probably also in play. IMM data Friday suggested a substantial reduction of EUR/USD longs. However, it didn’t help to push EUR/USD below the 1.1510 support in a sustainable way. This suggests decent buying interest in the pair, at least for now. With the downside blocked, EUR/USD currently even trades in the 1.1685 area. USD/JPY also trades only marginally weaker in a daily perspective (109.65 area). So, for now there is some tentative decoupling from EUR/USD and USD/JPY from the global risk off trade.

GBP. There was little economic news to guide sterling trading today. A global risk-off sentiment remains a tentative negative for the UK Currency. Together with a slight intraday rise in EUR/USD, it was/is enough to bring EUR/GBP again to 0.88 area. A less buoyant USD sentiment even helped a cautious rebound in cable (1.3275 area).

News Headlines

Harley Davidson announced that it will shift production of certain motorcycles away from its US-based manufacturing sites as a result of EU’s decision to impose counter-measures. It says the financial impact of the tariffs would be up to $100m per year. This move shows that the trade war is starting to have real effects on the economy.

German business confidence reached a one-year low in June (101.8 and down from 102.2 in May), according to the Ifo business climate poll. This survey, which measures the mood among company executives, declined in all four sectors (manufacturing, services, trade and construction). The decline was in line with market expectations. The forward looking expectations component even stabilized at 98.6 (vs 98.0 expected).

Moody’s has given its support to the Greek debt relief deal of last week. It said that the Eurozone agreement “paved the way for Greece to return to capital market funding” and “the additional and much closer supervision and monitoring provides assurance that the Greek authorities will stick to its fiscal and economic reforms”.

DOW loses 300pts as selloff accelerates, 24247 support in focus

DOW is dropping more than -300 pts, or -1.2% as selloff accelerates. 24247.84 key near term support is now in focus. As noted previously, the corrective rise from 23344.52 should have completed at 25402.83. It should be in form of an ascending triangle. Sustained break of 24247.84 should confirm this view and target a test on 23344.52.

In addition, that will also affirm our view that fall from 25402.83 is the third leg of the corrective pattern from 26616.71. And we should at least see a test on 38.2% retracement of 15450.56 to 26616.71 at 22351.24 before completing the correction. Let's see how it plays out.

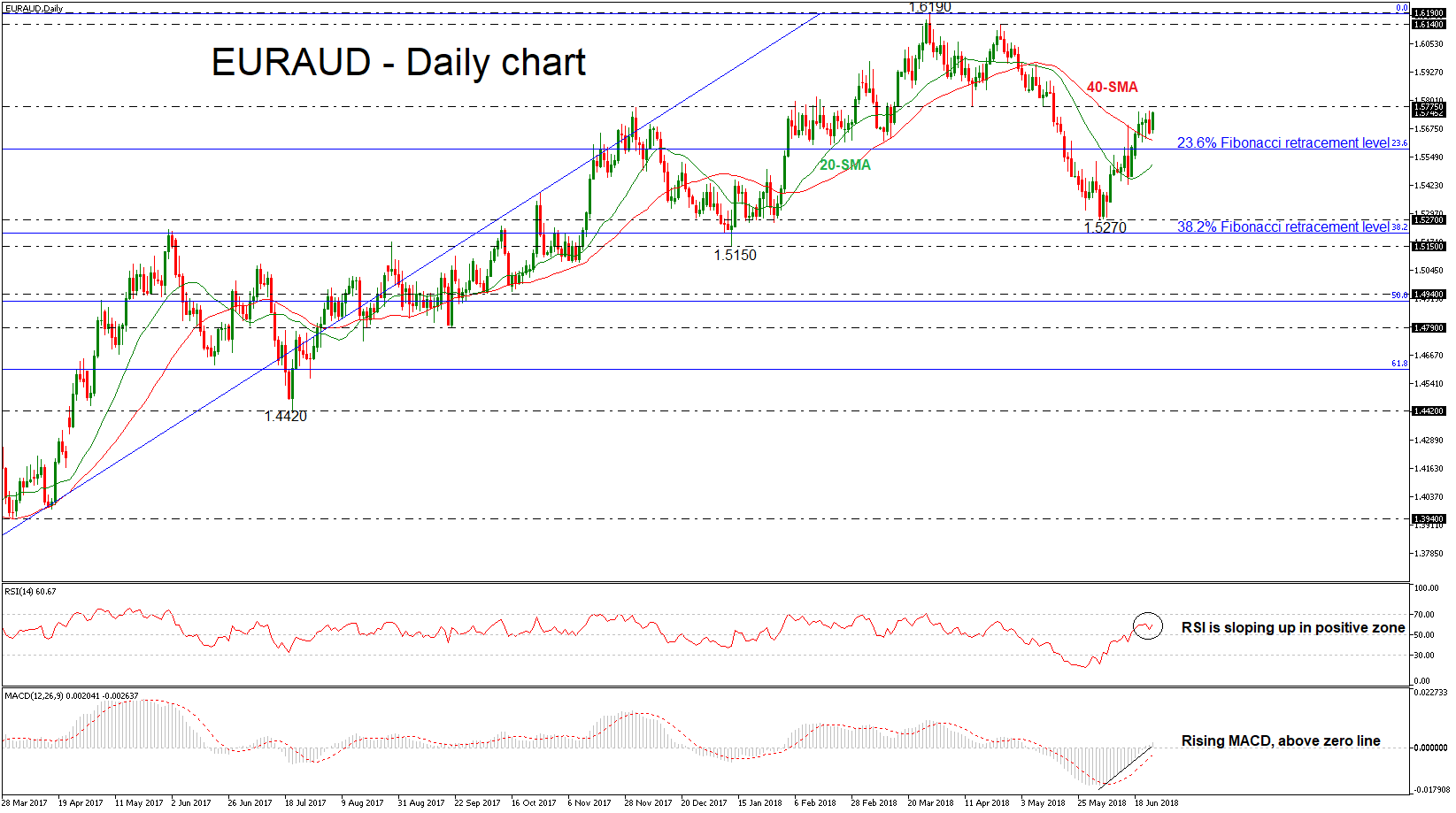

EURAUD Ready for Bullish Extensions; Holds Near 5-Week High

EURAUD has advanced considerably in Monday’s session and stands above the 40-simple moving average (SMA), while it hit a five-week high of 1.5754 last week. Price action is at the moment taking place not far below this peak.

Looking at momentum indicators, the RSI indicator is pointing north above the threshold of 50, suggesting that the market could keep rising in the near term. The MACD also supports this view in the positive territory, while it is strengthening the bullish momentum.

In the wake of more positive pressures and a climb above the 1.5775 significant resistance level, the market could meet resistance at the 1.6140 barrier, identified by the April 25 high. Slightly above this level, the 1.6190 level is acting as a strong obstacle for the bulls.

On the flip side, a move to the downside could see immediate support at the 23.6% Fibonacci retracement level of the upleg from 1.3620 to 1.6190, near 1.5583. A successful close below this level could see a retest of the previous low of 1.5270, while in case of steeper declines, the pair could breach this trough, diving to the 38.2% Fibonacci mark of 1.5205.

Turning to the medium-term picture, the market seems to be in a bullish mode given that EURAUD is trading above the 20- and 40-SMAs.

Canadian Dollar Ticks Lower

The Canadian dollar is slightly lower in the Monday session. Currently, USD/CAD is trading at 1.3291, up 0.19% on the day. On the release front, there are no Canadian releases until Thursday. In the U.S, New Home Sales is expected to climb to 665 thousand. On Tuesday, the U.S releases CB Consumer Confidence.

Canadian consumer data was dismal on Friday, but the Canadian dollar managed to hold its own against the greenback. CPI in May slipped to a weak gain of o.1%, missing the forecast of 0.4%. This marked a 5-month high. Consumer spending in April also missed expectations. Core retail sales declined 0.1%, well of the estimate of 0.5%. The indicator hasn’t posted a gain since January. Retail Sales declined 1.2%, compared to an estimate of 0.0%. This was its weakest reading since February 2016. Despite the soft numbers, the BoC remains confident about the economy, and a July rate hike remains a reasonable possibility. Inflation is still above the target of 2.0%, and in its the May policy statement the BoC removed its reference to “cautious”, replacing it with “gradual” describing its approach to rate adjustments. The markets viewed this as a signal that the bank is prepared to press the rate trigger in the second half of 2018. A rate hike would likely boost the Canadian dollar, as it makes the currency more attractive to investors.

The escalating trade dispute between the U.S. and its major trading partners remains a critical issue for global markets. The heads of central banks are concerned, and last week, Jerome Powell and Mario Draghi sounded gloomy about the repercussions that a trade war could have on economic growth and monetary policy. On Sunday, the Bank of International Settlements (BIS), also weighed in. The BIS acts as an umbrella group for some 60 central banks. The head of the BIS, Augustin Carstens, warned that recent protectionist moves could hamper global growth and financial stability, and could have negative side effects on the currency markets. At the same time, the BIS expressed support for the Federal Reserve raising interest rates gradually and for the ECB heading towards normalization as it winds up its massive asset program.

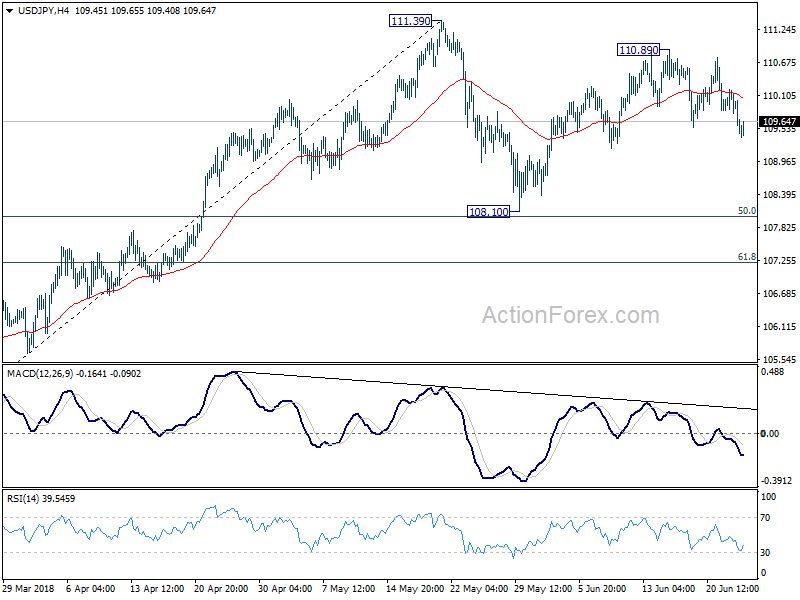

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 109.79; (P) 110.00; (R1) 110.21; More...

Intraday bias in USD/JPY remain son the downside for the moment. Current fall from 110.89 is see as the third leg of the consolidation pattern from 111.39. Deeper decline would be seen to 108.10 support and possibly below. But, we'd expect strong support from 61.8% retracement of 104.62 to 111.39 at 107.20 to contain downside and bring rebound. On the upside, above 110.89 will extend the rise from 108.10 towards 111.39 instead.

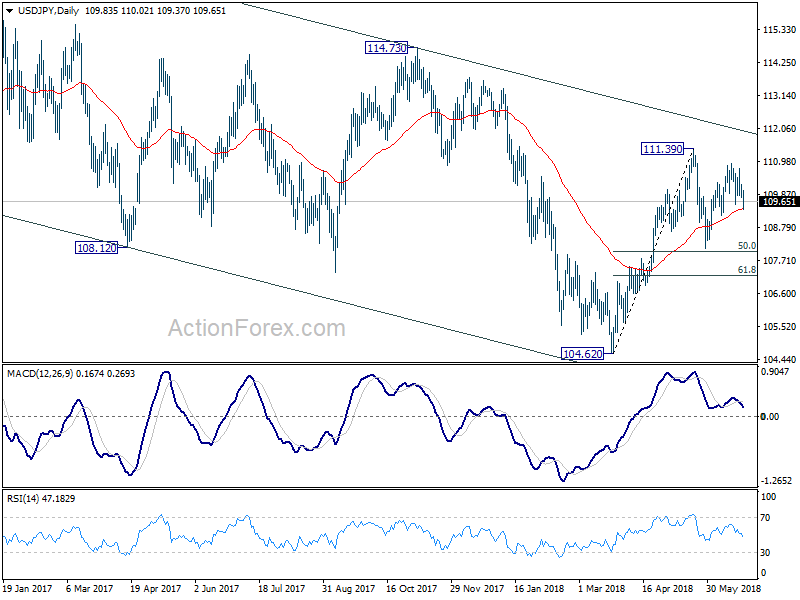

In the bigger picture, at this point, we're slightly favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 will affirm this view and target 114.73 for confirmation. However, it should be noted that USD/JPY is bounded in medium term falling channel from 118.65 (2016 high). Sustained break of 61.8% retracement of 104.62 to 111.39 at 107.20 will likely resume the fall from 118.65 through 104.62 low.

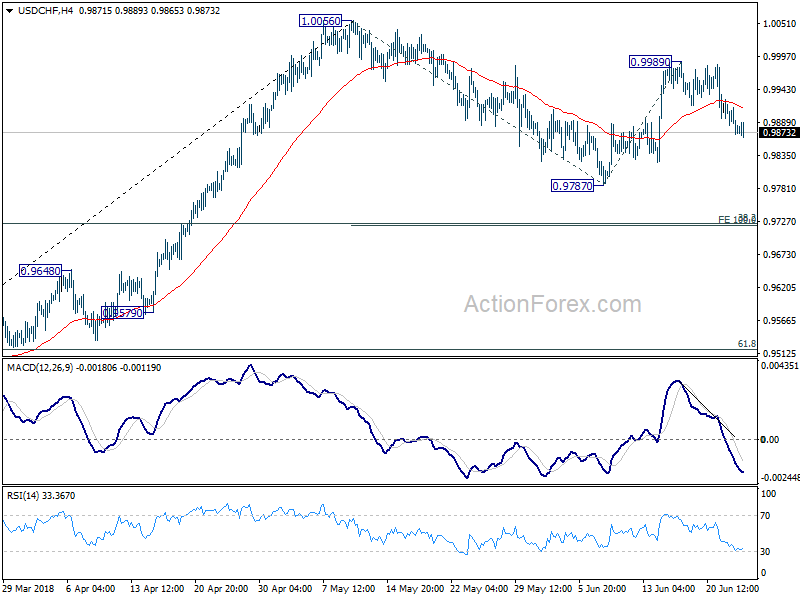

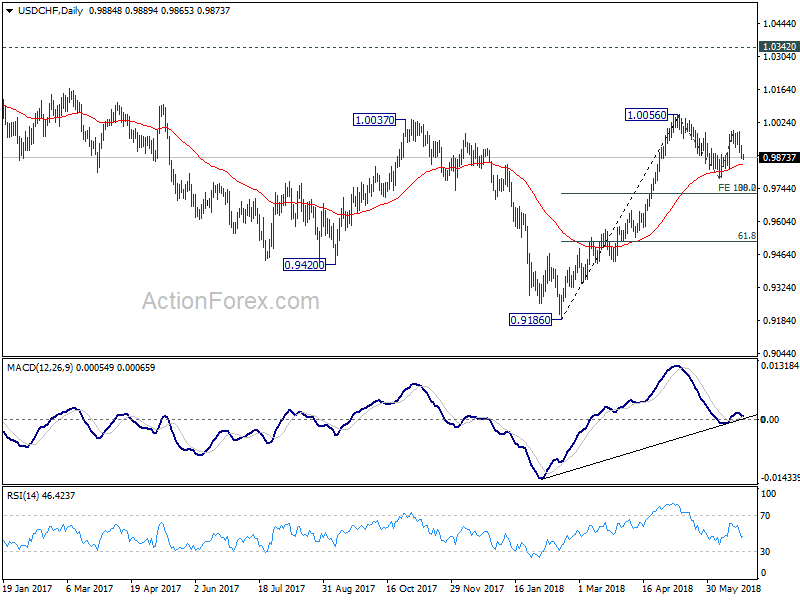

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9856; (P) 0.9894; (R1) 0.9915; More...

No change in USD/CHF's outlook. Correction from 1.0056 is still in progress and intraday bias stays on the downside for 0.9787 support and possibly below. But we'd expect strong support from 0.9720/4 cluster support (38.2% retracement of 0.9186 to 1.0056 at 0.9724, 100% projection of 1.0056 to 0.9787 from 0.9989 at 0.9720) to bring rebound. On the upside, above 0.9989 will bring retest of 1.0056 high first.

In the bigger picture, medium term decline from 1.0342 has completed with three waves down to 0.9186. Rise from there is currently viewed as a leg inside the long term range pattern. Hence, while further rally would be seen, we'd be cautious on strong resistance from 1.0342 to limit upside. For now, further rise is expected as long as 38.2% retracement of 0.9186 to 1.0056 at 0.9724 holds. However, sustained break of 0.9724 will dampen this bullish view and would at least bring deeper fall to 61.8% retracement at 0.9518.

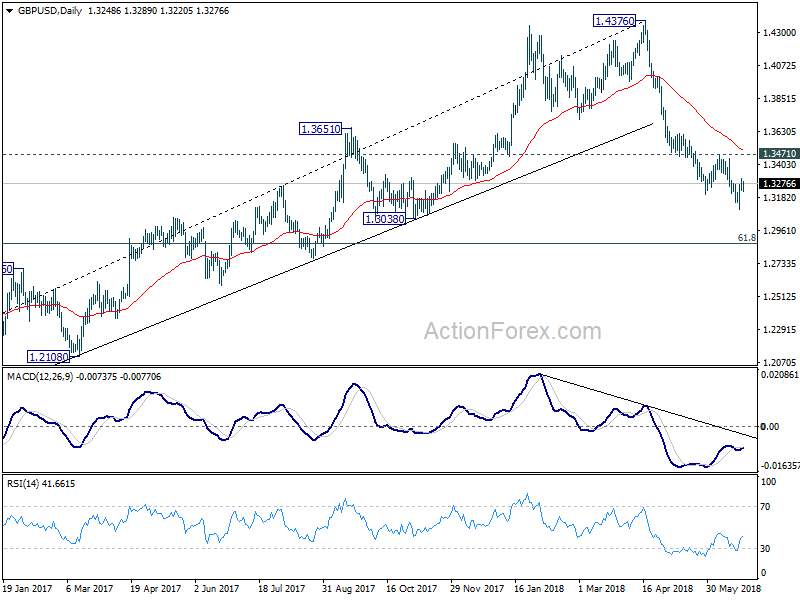

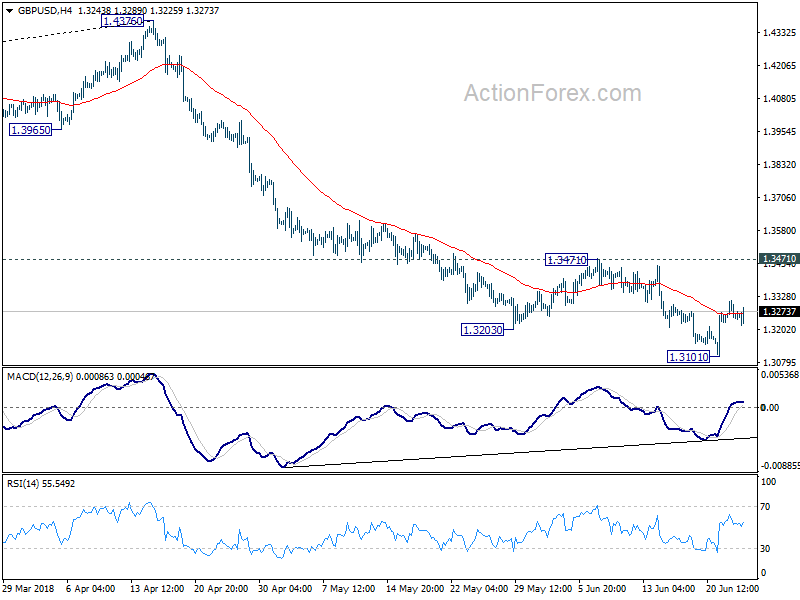

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3230; (P) 1.3273; (R1) 1.3307; More...

GBP/USD's rebound from 1.3101 is still in progress and further rise could be seen. But upside is expected to be limited by 1.3471 resistance to bring fall resumption. On the downside, break of 1.3101 will resume the whole decline from 1.4376 and target 61.8% retracement of 1.1946 to 1.4376 at 1.2875 next.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4177). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 55 day EMA (now at 1.3507) holds, even in case of strong rebound.