Sample Category Title

Crude Oil: Oil Trading On A Weaker Footing This Morning

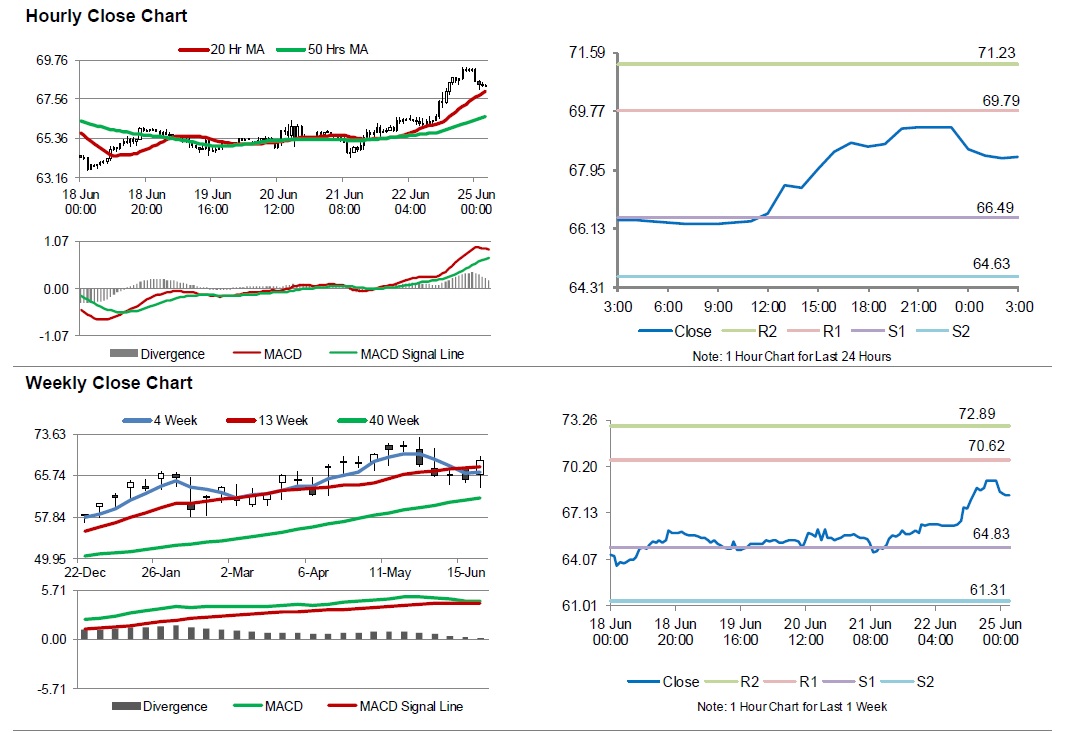

For the 24 hours to 23:00 GMT, Crude Oil climbed 5.28% against the USD and closed at USD69.25 per barrel on Friday, after oil producers agreed to a modest rise in crude output. Additionally, Baker Hughes disclosed that the number of active oil rigs in the US fell by 1 to 862 in the week ended 22 June.

In the Asian session, at GMT0300, the pair is trading at 68.34, with oil trading 1.31% lower against the USD from Friday’s close.

The pair is expected to find support at 66.49, and a fall through could take it to the next support level of 64.63. The pair is expected to find its first resistance at 69.79, and a rise through could take it to the next resistance level of 71.23.

Crude oil is trading above its 20 Hr and 50 Hr moving averages.

Weekly Wave Analysis EUR/USD, GBP/USD, USD/JPY

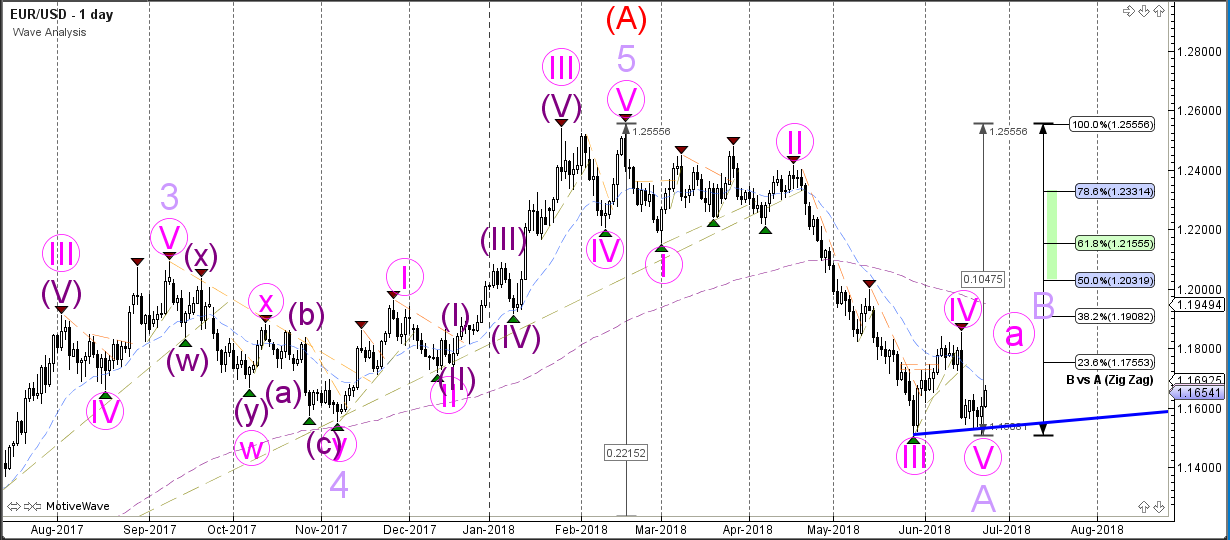

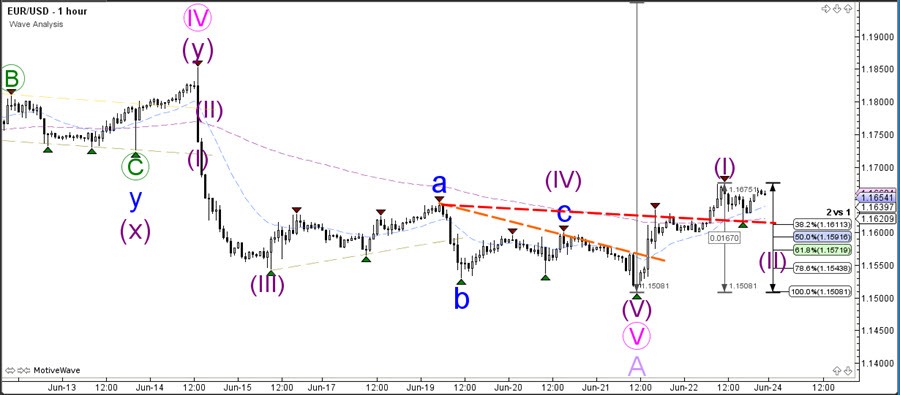

EUR/USD

The EUR/USD bounced at the support trend line (blue) which either means that price has completed a truncated wave 5 (pink) within wave A (purple) or that wave 4 (pink) is building an expansion.

Daily chart:

The EUR/USD seems to be building a bearish ABC (purple) correction within wave B (red). The 50% Fibonacci level could be a key support zone.

Weekly chart:

The EUR/USD has probably completed wave A (red) and price is now most likely retracing to the Fibonacci levels of wave B (red).

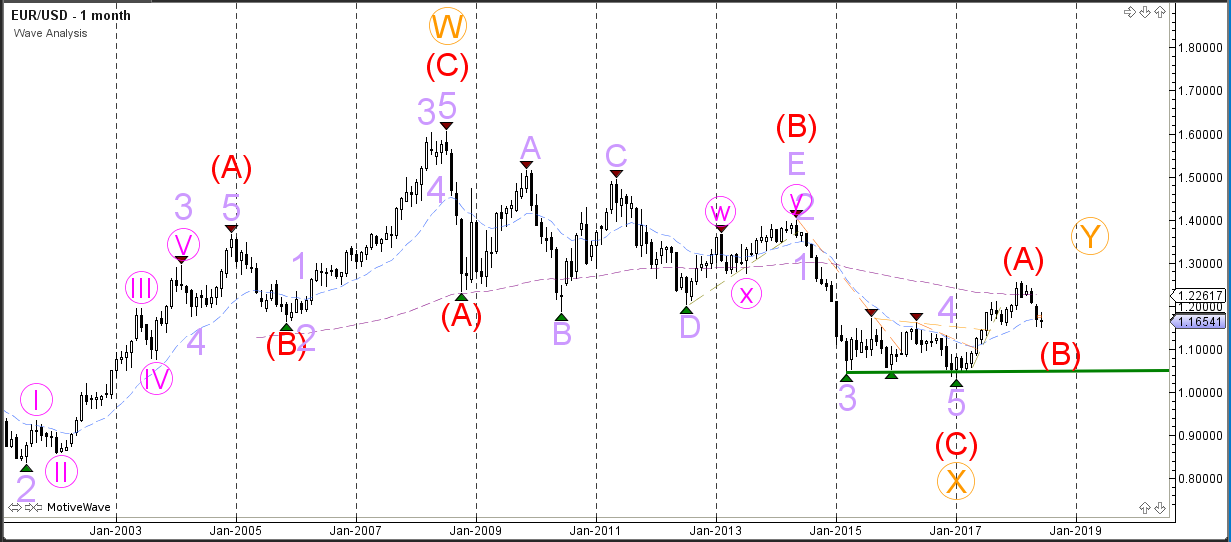

Monthly chart:

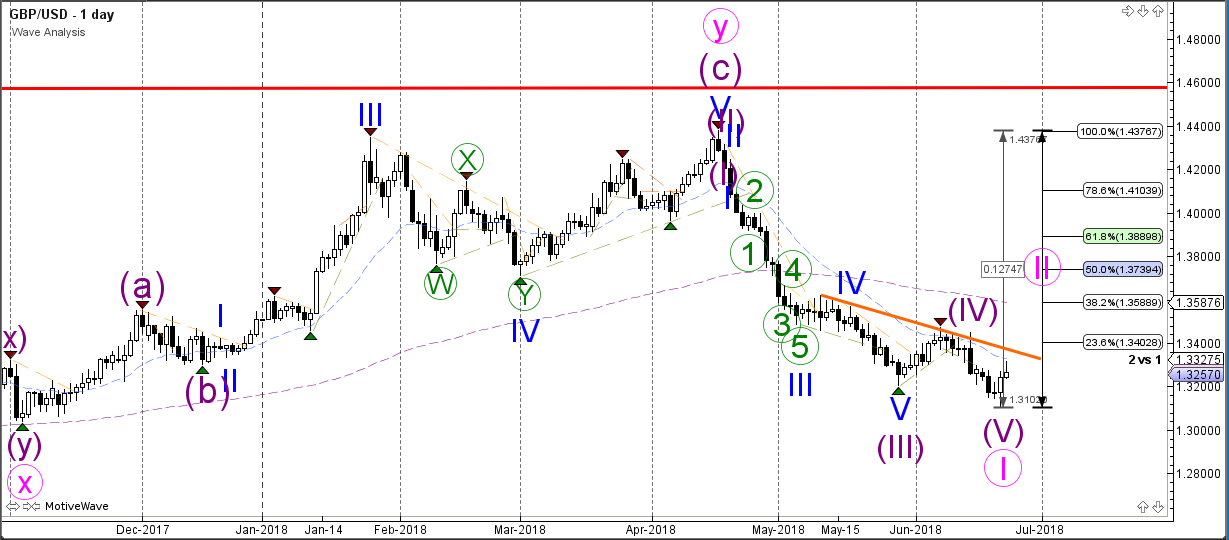

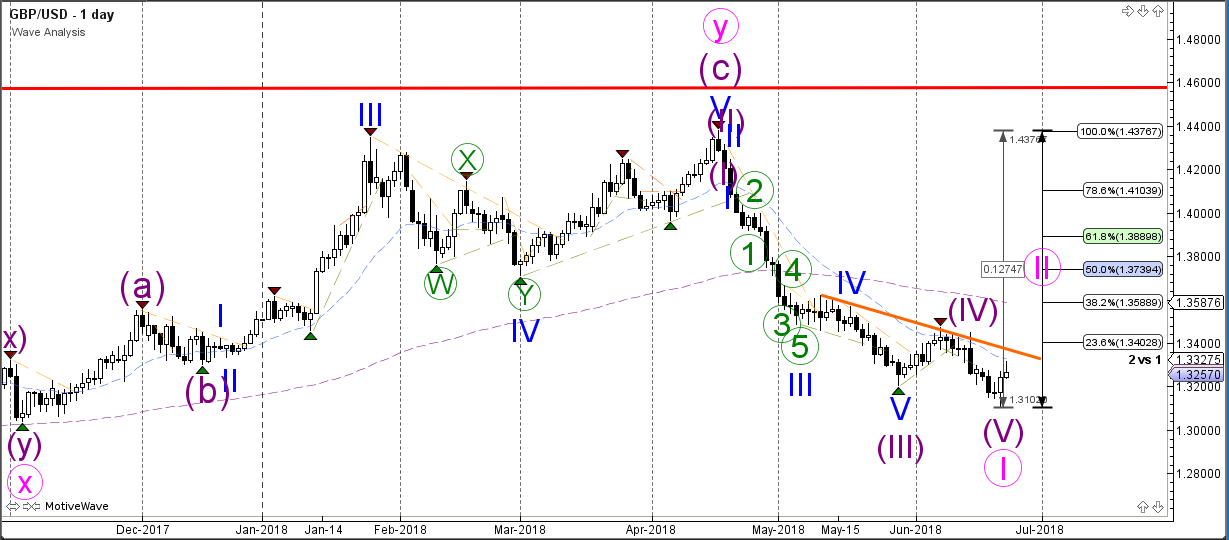

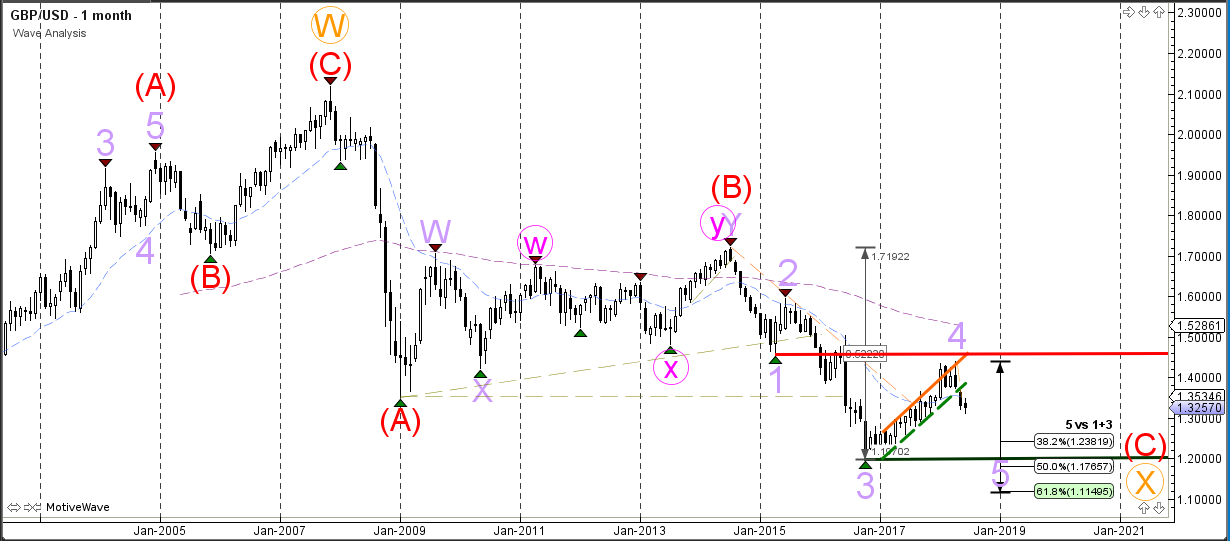

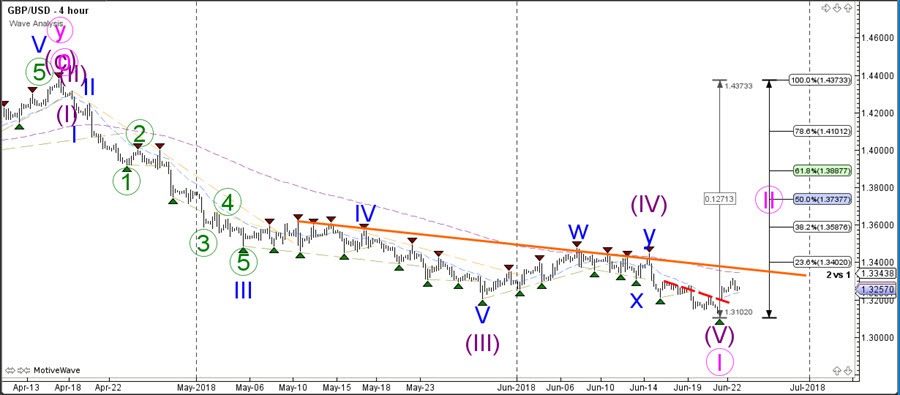

GBP/USD

The GBP/USD could now have completed a wave 5 (purple) of a potential wave 1 (pink).

Daily chart:

The GBP/USD has probably started the bearish wave 5 after price has completed a wave 4 (light purple) correction.

Weekly chart:

The GBP/USD bearish breakout could see the continuation of the wave 5 (purple) whereas a bullish break above resistance (red) could indicate that the wave C has been completed at the bottom.

Monthly chart:

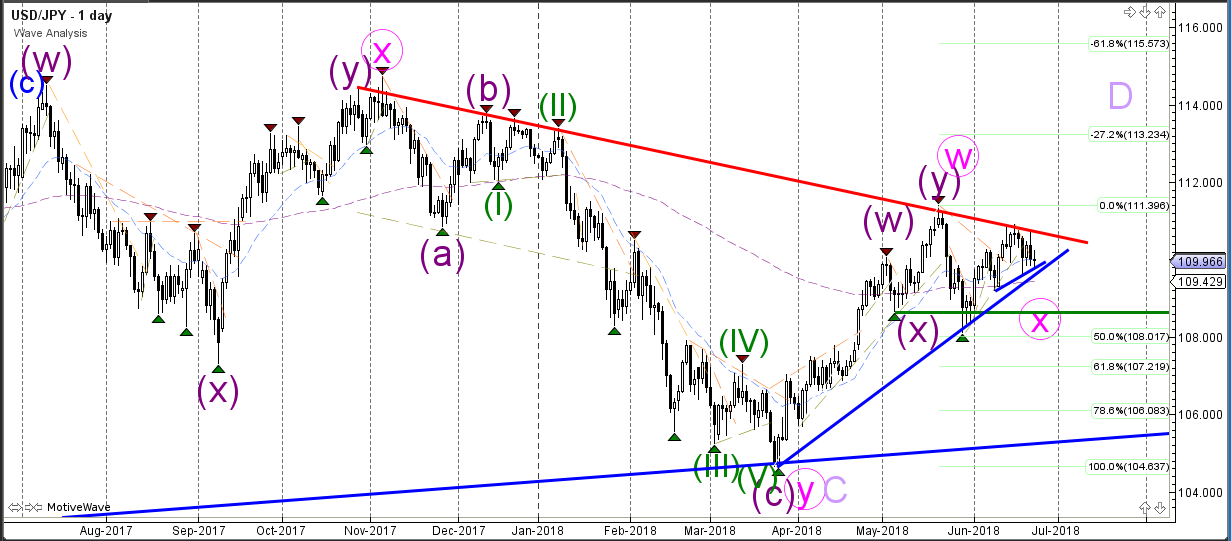

USD/JPY

The USD/JPY is testing the support trend lines (blue) and a bearish breakout could see price fall towards the next trend line (green) and Fibonacci levels.

Daily chart:

The USD/JPY could be building an ABCDE triangle (light purple) within wave B (red – see monthly chart).

Weekly chart:

The USD/JPY is in the wave D (light purple) of the triangle pattern.

Monthly chart:

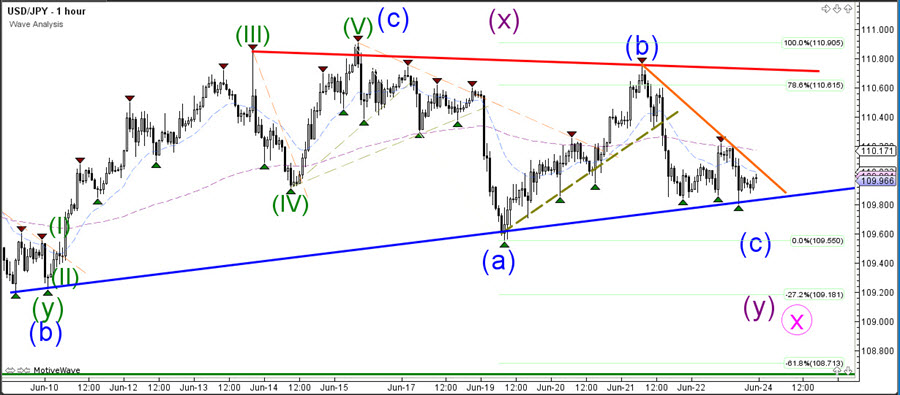

USD/JPY Bearish Break Of Triangle Pattern Aims At 108.75

The USD/JPY remains in a triangle chart pattern for the moment. A break below the support trend line (blue) could indicate a deeper correction within wave X (purple) whereas a break above the resistance trend line could end of wave X and start a bullish correction of wave D (purple).

The USD/JPY is building a consolidation pattern around the support trend line (blue) which is a key bounce or break spot. A bearish breakout seems more likely at the moment due to the bearish structure of the price patterns and could signal a continuation towards the Fibonacci targets on this chart.

EUR/USD Extends Corrective Zone After Bullish Breakout

The EUR/USD broke above multiple resistance trend lines and could be ready to test the previous top at around 1.18.

The EUR/USD is either expanding the wave 4 (pink) via a triangle pattern or expanding the correction sideways via an ABC (pink) in wave B (purple).

The EUR/USD could be building a wave 1-2 (purple) unless price breaks below the bottom and 100% Fibonacci level of wave 2 (purple). A break above the previous top could indicate a bullish continuation.

GBP/USD Decision Time: Downtrend Or Bullish Correction?

The GBP/USD is in a critical phase where price will either show a continuation of the downtrend or larger bullish retracement.

The GBP/USD could either start a wave 2 (pink) correction once price breaks above the resistance trend line (orange) or continue with the downtrend if price breaks below the previous bottom at 1.31.

The GBP/USD could be building a potential wave 1-2 (blue) if price breaks below the support trend line (green). A break below the 100% Fib invalidates the bullish wave 2 reversal (blue).

China PBOC Cuts RRR 50bps, Releasing More Liquidity Than Expected

General Trend:

Asian equities trade generally lower, US said to consider additional trade actions on China

Shanghai Composite pares gains as PBoC cut the RRR following recent market speculation

HK IPOs in focus, money market rates hit 10-year high: Xiaomi set maximum offering price for floatation, Meituan files for ~$6.0B IPO

BoJ June Meeting Summary of Opinions: Not appropriate to adopt policy that would ‘forcibly’ push up demand in short period of time, reason for sluggishness in prices is not likely to be merely shortage of demand

Turkish Lira (TRY) rises over 1.5%, country’s election board said Erdogan received a ‘simple majority’ (97.2% of the votes counted); Currency later pares gains

Yen (JPY) trades broadly firmer in the face of general equity weakness and focus on trade; AUD/JPY drops over 0.5%; yuan (CNY) declines over 0.5%

Brent Crude futures decline over 1.5% as OPEC+ agreed to raise production

Offshore yuan falls to lowest level this year and its longest consecutive decline in 2-yrs

Japan auto makers under pressure, expected to be caught up in US trade wars

US President Trump said to plan new restrictions on technology exports to China and Chinese investment; announcement expected by the end of the week

Headlines/Economic Data

Japan

Nikkei 225 opened +0.1%

TOPIX Retail trade index -1%, Information & Communication -1%, Real Estate -0.9% Electric Appliances -0.5%; Securities +0.8%, Marine Transportation +0.6%

(JP) Japan ruling Liberal Democratic Party (LDP) lawmaker Shigeru Ishiba said to consider announcing candidacy for LDP leader - Japanese Press

(JP) According to NHK survey, economist see headline BOJ large manufacturers' business conditions for June at 20-23 v 24 in March, would mark second consecutive decline - NHK

Toshiba, 6502.JP US SEC has completed accounting investigation of unit; did not receive any warning nor fine

(JP) Japan PM Abe reiterates will keep requesting US tariff exemptions for Japan companies

Korea

Kospi opened -0.2%

Lotte, LOTZ.KR Chairman Shin Dong-bin raised stake ~10.5% v ~8.6% prior - Japanese Press

(KR) Three South Korean vehicle brands, all belonging to Hyundai Motor Group, surpassed their Japanese and German rivals in a United States quality ranking - Korean press

(KR) According to analysts South Korean shares are expected to remain in a relatively tight range this week as investors take to the sidelines amid global trade tensions - Korean press

(KR) South Korea sells KRW700B in 20-yr bonds, avg yield 2.60% v 2.76% prior

China/Hong Kong

Hang Seng opened 0.0%, Shanghai Composite +0.5%

Hang Seng Materials index -1.9%, Services -1.8%, Industrial Goods -1.1%, Property/Construction -1%, Info Tech -0.7%, Consumer Goods -0.6%, Financials -0.4%; Energy +1.5%, Utilities +0.5%

(CN) China cuts Reserve Ratio Requirement (RRR) for some banks by 50bps, effective July 5th; (3rd cut this year) as a result releasing CNY700B v CNY400Be in liquidity

Aluminum Corporation of China Limited, 2600.HK Controlling shareholder Chinalco to increase shareholding in company for not less than CNY400M and no more than CNY1.0B within 12-months

(HK) Certain banks in Hong Kong said to reduce commissions at mortgage brokerage units - Local Press

(US) US President Trump said to plan new restrictions on technology exports to China and Chinese investment; announcement expected by the end of the week - US financial press

(CN) China PBoC Open Market Operation (OMO): Skips OMO operations v CNY70B injected in 7 and 14 day reverse repos prior: Net: injection CNY10B v CNY20B injection prior

(CN) China PBoC sets yuan reference rate at 6.4893 v 6.4804 prior

(CN) China Vice Premier Liu He and EU agree to resolutely oppose trade protectionism, defend multilateral system - speaking after summit with EU

Australia/New Zealand

ASX 200 opened +0.2%

ASX 200 Financials index -1.2%, Telecom -0.4%, REIT -0.4%; Energy +1.7%, Resources +1.4%, Utilities +0.6%

Gateway, GTY.AU Hometown raises indicative bid to A$2.35/share (prior A$2.10 prior)

CBA.AU To demerge wealth management and mortgage broking units; to undertake strategic review of general insurance business including a possible sale

HT1.AU Confirms to sell Adshel business to oOh!media for A$570M; to conduct A$275M capital raise; fully franked special dividend worth A$220M

North America

Xerium [XRM]: To be acquired by Andritz for $13.50/shr cash in a $833M deal, includes $590M liabilities

GE [GE]: Follow Up: Said to be near agreement to sell industrial-engines unit to Advent; sale speculated to raise at least $3.0B – US financial press

Europe

Erytech, ERYP.FR To discontinue development program for acute lymphoblastic leukemia; announces refocusing of development activities

(TR) Turkey Elections Board: With 97.2% of votes counted, Erdogan has simple majority

Levels as of 01:30ET

Hang Seng -0.8%; Shanghai Composite -0.1%; Kospi -0.1%; Nikkei225 -0.5%; ASX 200 -0.3%

Equity Futures: S&P500 -0.4%; Nasdaq100 -0.4%, Dax -0.4%; FTSE100 -0.4%

EUR 1.1646-1.1673; JPY 109.40-110.03; AUD 0.7417-0.7442;NZD 0.6896-0.6922

Aug Gold -0.2% at $1,268/oz; Aug Crude Oil -0.2% at $68.44/brl; Jul Copper +0.1% at $3.05/lb

BoJ: Inappropriate to adopt policy that forcibly push up demand in a short time

In the summary of opinions at the June 14/15 BoJ monetary policy meeting, the central noted that the economy is "expanding moderately". But it also cautioned that the effect of US "protectionist trade policy" warrant "close attention". In addition to that, other concerns include "political situation in southern Europe and volatile

movements in some emerging markets. Though, the latter have "limited" effects on the global economy at this point.

Regarding inflation, BoJ noted that "upward pressure on wages has been weak despite the increased tightness in the labor market". And, "if wages do not rise in line with inflation, this would pose a burden on people." BoJ said "close attention should be paid to developments in labor productivity and real wages, while taking into account mainly the effects of a reduction in overtime work hours under working-style reforms."

On monetary policy, since there is "still a long way" to meet 2% inflation target, it is "appropriate to pursue powerful monetary easing with persistence under the current guideline". But BoJ also noted that "the reason for the sluggishness in prices is unlikely to be merely a shortage of demand". Therefore, "it is not appropriate to adopt a policy that would forcibly push up demand in a short period of time.

OPEC/ Non-OPEC Deal Has Limited Impact. Here is Why

Oil bulls are relieved after the OPEC/ non-OPEC decision on production. At the joint statement released on June 23, the oil producers announced that they would “strive to adhere to the overall conformity level, voluntarily adjusted to 100%, from July 1 and for the rest of the year. The Joint Ministerial Monitoring Committee (JMMC) would continue to monitor the overall conformity level. According to Saudi Energy Minister Khalid Al-Falih, “we have an agreement” for a “nominal” production increase of 1M bpd. Yet, the actual increase would be much less than that as many producers have already reached their “full capacity”. Oil ministers from Oman and Iraq estimated that the decision would result in production increase of about 600-700K bpd. The market was thrilled by the decision as it had anticipated a bigger increase in output (over 1M bpd). Both crude oil benchmarks rallied after the announcement. The front-month WTI contract jumped +4.64% while the Brent contract was up +3.42%. Wall Street’s energy shares also rallied with Exxon Mobil and Chevron gaining +2.1% and 2% on Friday. The S&P Energy index rose+2.2%, marking the sector’s biggest one-day increase since June.

Adherence to Compliance Represents a Boost

According the OPEC’s estimate, the conformity level (or compliance level) was at 149% in May 2018. Therefore, the decision to return the compliance level to 100%, meaning that the participants would cut production no more than the 1.2M bpd agreed in November 2016, implies an increase in production from the current levels. However, the statement was ambiguous in that it did not give details on which country would produce how much from July onwards, leaving the situation somehow uncertain.

Some producers Are Unable to Raise Output

Taking a look at May’s compliance level of above 150%, the key drive for the “over-compliance” was output disruption in Venezuela, where the oil sector collapsed as a result of US sanctions and economic crisis. The country had agreed to cut output by -0.1M bpd from the baseline supply of 2.07M bpd as of October 2016. Yet, the actual had reached -0.68M bpd in May, resulting in a 680% compliance level! Venezuelan president Nicolas Maduro pledged last month that his government aims at recovering the lost output by +1M bpd bpd this year. Yet, he admitted that it is “very challenging”. Angola and Iran also recorded “over-compliance” of about 280% and 132%, respectively. For non-OPEC producers, Mexico had cut its output by -0.29M bpd in May, almost tripling the agreed reduction of -0.1M bpd. These indicated that disruption at home has prohibited some producers from increasing output even though they might want to.

Saudi Arabia and Russia to Fill the Gap

The decision to “raise” output was in part a response to oil consuming countries. For instance, US’ Donald Trump has repeatedly complained about the rising oil price, urging OPEC to raise production, while Saudi Arabia has sent multiple signals, hoping to meet its demand. We expect Saudi Arabia and Russia would should much of the promised output increase. Indeed, Saudi already boosted its exports to 7.5M bpd, up +0.6M bpd, in June. Possessing over 20% of the world's proven petroleum reserves and being the world’s largest exporter of petroleum, Saudi has both the interest and the capability to raise output. Meanwhile, Russia has from time signaled the intention to raise output and boost exports.

BIS: Protectionism, snapback in yields, politics in Euro area are possible triggers of downturn

The Bank for International Settlements warned in its annual report that escalation of protectionist measures is one possible trigger of global economic slowdown or downturn. It said that "its impact could be very significant, if such escalation was seen as threatening the open multilateral trading system." And, there are already signs that the these measures and the "ratcheting-up of rhetoric" are "inhibiting investment". And, trade negotiations would "become more complicated" with recent reversal US Dollar depreciation.

Sudden "decompression" of historically low bond yields, or "snapback" in core sovereign market yields could be another trigger. And, Biassed it could take place "in response to an inflation surprise" and "the perception that central banks will have to tighten more than anticipated. In the US, "the prospective heavy issuance of government debt, combined with the gradual unwinding of central bank purchases, could add to this risk." BIS also noted that the surprise "need not be a large one", yet the impact could spread globally.

General reversal in risk appetite is a third possible trigger. And, such reversal could reflect a range of factors, including disappointing profits, the drag of the contraction phase of financial cycles where these have turned, a souring of sentiment vis-à-vis EMEs, or untoward political events threatening stability in some large economies. BIS added that from this perspective, "recent events in the euro area are a source of concern."

PBoC cuts RRR by 50bps to release CNY 700B in funds

China's central bank, PBoC, announced to lower some banks' reserve requirement ratios by 50 bps, effective July 5. The targeted banks include large state-owned commercial banks, joint-stock commercial banks, postal savings banks, urban commercial banks, non-county rural commercial banks and foreign banks.

PBoC also encourages the five state-owned large-scale commercial banks and 12 joint-stock commercial banks to use directional RRR cuts and funds raised from the market to implement the "debt-to-equity swap" project.

It's estimated that the RRR cut will release around CNY 700B in funds that could help ease credit strain for small and micro businesses.