Sample Category Title

ECB Has No Intention Of Backt Racking From The Dovish Signals

Market movers today

We have a fairly quiet day and week on the data front ( the most important releases are inflation numbers in the US and the euro area on Friday), so market attention will focus most notably on the trade tensions between the US and its big trading partners Europe and China.

On the trade issue, we will watch for any react ion from Europe on Trump's pledge to levy tariffs on European car imports. Another important event is Saturday 30 June, when the US government is set to announce plans for restricting Chinese investments.

On the European side, the European Council meet ing on 28-29 June will be an important event to watch out for, as to whether the German government crisis is resolved with European agreement on immigration, what line the new Italian government will take and possibly for the Brexit process.

Selected market news

In Turkey, Tayyip Erdoğan had a clear victory with 53% of the votes, obtaining a double win in both the presidential and parliamentary elections. The main opposition leader Muharrem Ince yesterday accepted his defeat but said the elect ion had not been fair, claiming vote manipulation. TRY gained overnight .

On Friday night there was an interest ing interview with influential ECB member Peter Praet in which he said, ‘What we did last week was to express an anticipation that net asset purchases would end at the end of the year. We didn't say we were now deciding to stop the programme in December. We still have six months to go. We translated the increased confidence we expressed about developments in the economy and inflation into an anticipation about the APP'. So far most analysts have concluded that the asset purchases would definitely stop in December. But now Praet basically says that no firm conclusions have been made, though he admit s t hat , ‘... to anticipate the end of the programme is to give a strong signal'. But the conclusion is clear from our point of view: the ECB has no intention of backt racking from the dovish signals at the latest ECB meeting. In that respect also note that the voluntary repayment at TLTRO2 on Friday was a limited EUR11bn, and the risk of a tightening of the liquidity situation in the eurozone remains very low. For more see ECB research: TLTRO2 – EUR 11bn of voluntary repayments, 22 June.

On the political scene, all eyes have been on the informal mini EU summit for 16 count ries in Brussels on migration. No formal agreement was made ahead of the 28-country summit on Thursday. It also means that politically, the pressure remains on Merkel in German politics.

European equity markets took their lead from the news that Trump would levy a 20% tax on European-produced cars. The market init ially came under pressure but managed to close in positive territory. The Peoples Bank of China lowered the reserve requirements over the weekend by USD100bn for Chinese banks (the reserve rat io was lowered 0.5pp). CNY has weakened 1.6% against the US dollar over the past week. It seems that the Chinese authorities are preparing for a prolonged trade war with the US. Bloomberg reports that the US administration is planning t o curb Chinese investment in ‘industrial significant technology'.

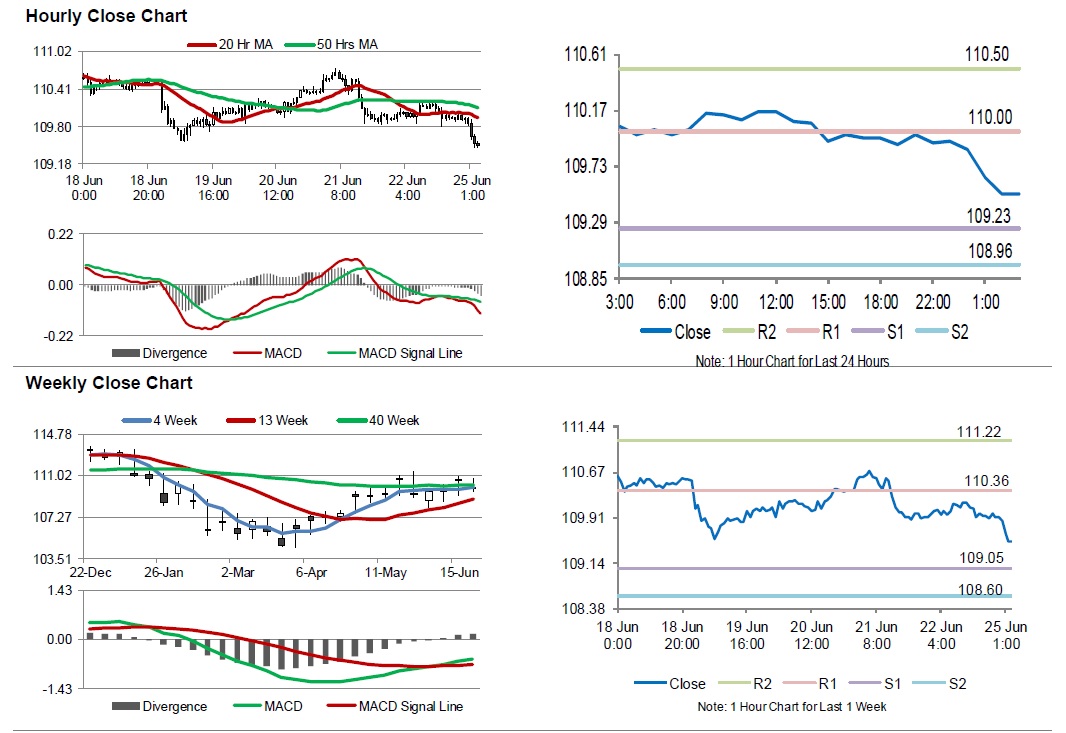

USD/JPY Daily Outlook

Daily Pivots: (S1) 109.79; (P) 110.00; (R1) 110.21; More...

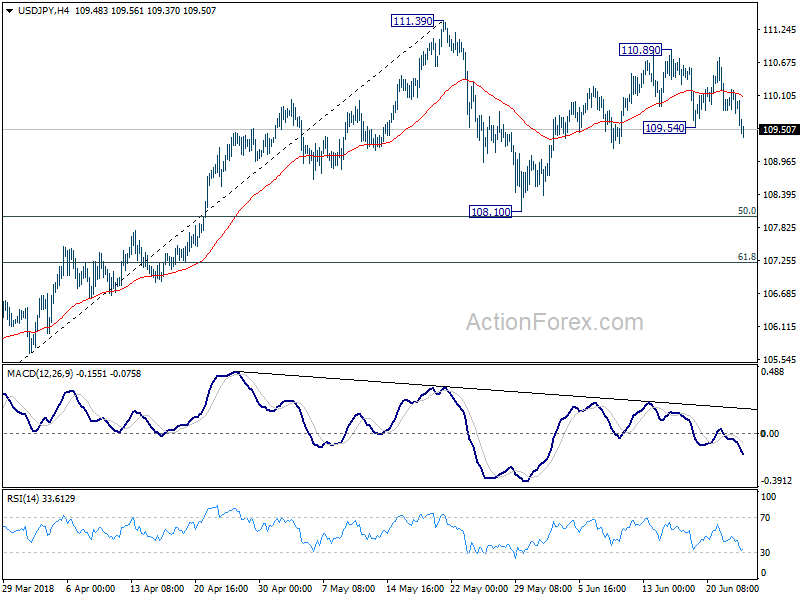

USD/JPY's break of 109.54 suggests that fall from 110.89 has resumed. Such decline is seen as the third leg of the consolidation pattern from 111.39. Intraday bias is back on the downside for 108.10 support and possibly below. But, we'd expect strong support from 61.8% retracement of 104.62 to 111.39 at 107.20 to contain downside and bring rebound. On the upside, above 110.89 will extend the rise from 108.10 towards 111.39 instead.

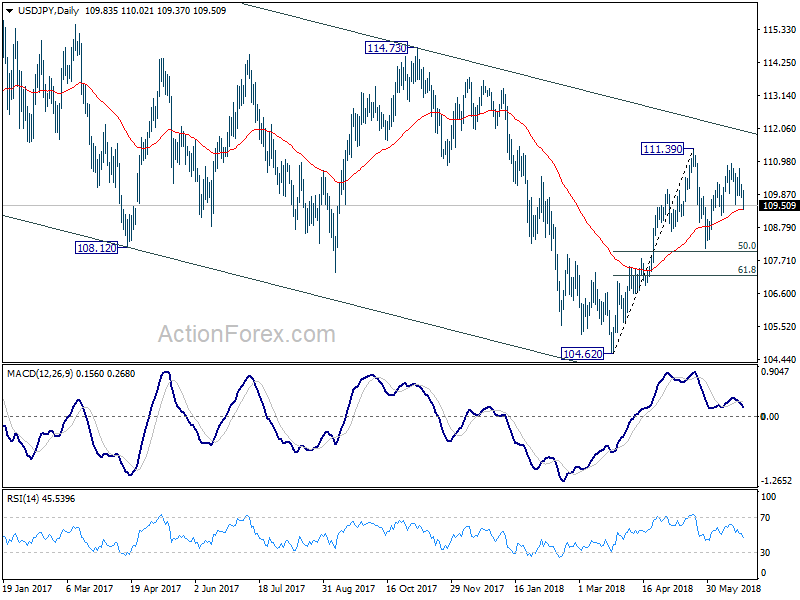

In the bigger picture, at this point, we're slightly favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 will affirm this view and target 114.73 for confirmation. However, it should be noted that USD/JPY is bounded in medium term falling channel from 118.65 (2016 high). Sustained break of 61.8% retracement of 104.62 to 111.39 at 107.20 will likely resume the fall from 118.65 through 104.62 low.

Yen Rally Continues as Trade Spat Escalates

Yen trades broadly higher today, followed by Dollar and Swiss Franc as sentiments are weighed down by escalating trade rhetorics. Nikkei closed down by -0.79% at 22339.15, after hitting session low at 22312.79. China's Shanghai composite opened higher, as lifted by PBoC's RRR cut, but turned red soon after. Commodity currencies are trading as the weakest ones in risk aversion environment as usual, with Aussie leading the way down.

Technically, USD/JPY's break of 109.54 reaffirm the case that near term rebound from 108.10 has completed at 110.89 already. And recent consolidation pattern from 111.39 is starting the third leg for 108.10 and below. EUR/JPY and GBP/JPY both staged slightly stronger than expected rebound last week. But with today's selloff, focuses are back on recent support at 126.62 and 144.37 respectively.

Trump escalates trade war threats to the world

Concerns of global trade war is a factor driving stocks down. Trump stepped up his rhetoric as he is now pushing all countries to remove "artificial trade barriers and tariffs". Or, he warned of "more than reciprocity by the USA". He tweeted that "The United States is insisting that all countries that have placed artificial Trade Barriers and Tariffs on goods going into their country, remove those Barriers & Tariffs or be met with more than Reciprocity by the U.S.A. Trade must be fair and no longer a one way street!"

This was a follow up to his warning to EU on Friday that 20% tariffs could be imposed to their cars. That's a response to EU's retaliation to US steel and aluminum tariffs. He tweeted "Based on the Tariffs and Trade Barriers long placed on the U.S. & its great companies and workers by the European Union, if these Tariffs and Barriers are not soon broken down and removed, we will be placing a 20% Tariff on all of their cars coming into the U.S. Build them here!"

European Commission Vice President Jyrki Katainen told French newspaper Le Monde that "if they decide to raise their import tariffs, we'll have no choice, again, but to react. And, he added that "We don't want to fight (over trade) in public via Twitter. We should end the escalation."

BoJ: Inappropriate to adopt policy that forcibly push up demand in a short time

In the summary of opinions at the June 14/15 BoJ monetary policy meeting, the central noted that the economy is "expanding moderately". But it also cautioned that the effect of US "protectionist trade policy" warrant "close attention". In addition to that, other concerns include "political situation in southern Europe and volatile movements in some emerging markets. Though, the latter have "limited" effects on the global economy at this point.

Regarding inflation, BoJ noted that "upward pressure on wages has been weak despite the increased tightness in the labor market". And, "if wages do not rise in line with inflation, this would pose a burden on people." BoJ said "close attention should be paid to developments in labor productivity and real wages, while taking into account mainly the effects of a reduction in overtime work hours under working-style reforms."

On monetary policy, since there is "still a long way" to meet 2% inflation target, it is "appropriate to pursue powerful monetary easing with persistence under the current guideline". But BoJ also noted that "the reason for the sluggishness in prices is unlikely to be merely a shortage of demand". Therefore, "it is not appropriate to adopt a policy that would forcibly push up demand in a short period of time.

PBoC cuts RRR by 50bps to release CNY 700B in funds

China's central bank, PBoC, announced to lower some banks' reserve requirement ratios by 50 bps, effective July 5. The targeted banks include large state-owned commercial banks, joint-stock commercial banks, postal savings banks, urban commercial banks, non-county rural commercial banks and foreign banks.

PBoC also encourages the five state-owned large-scale commercial banks and 12 joint-stock commercial banks to use directional RRR cuts and funds raised from the market to implement the "debt-to-equity swap" project.

It's estimated that the RRR cut will release around CNY 700B in funds that could help ease credit strain for small and micro businesses.

BIS: Protectionism, snapback in yields, politics in Euro area are possible triggers of downturn

The Bank for International Settlements warned in its annual report that escalation of protectionist measures is one possible trigger of global economic slowdown or downturn. It said that "its impact could be very significant, if such escalation was seen as threatening the open multilateral trading system." And, there are already signs that the these measures and the "ratcheting-up of rhetoric" are "inhibiting investment". And, trade negotiations would "become more complicated" with recent reversal US Dollar depreciation.

Sudden "decompression" of historically low bond yields, or "snapback" in core sovereign market yields could be another trigger. And, Biassed it could take place "in response to an inflation surprise" and "the perception that central banks will have to tighten more than anticipated. In the US, "the prospective heavy issuance of government debt, combined with the gradual unwinding of central bank purchases, could add to this risk." BIS also noted that the surprise "need not be a large one", yet the impact could spread globally.

General reversal in risk appetite is a third possible trigger. And, such reversal could reflect a range of factors, including disappointing profits, the drag of the contraction phase of financial cycles where these have turned, a souring of sentiment vis-à-vis EMEs, or untoward political events threatening stability in some large economies. BIS added that from this perspective, "recent events in the euro area are a source of concern."

Looking ahead

RBNZ is the main central bank event this week and it's widely expected to stand pat again. Other than that, there are quite a number of economic data to watch. German Ifo business climate and Eurozone CPI flash are important for the Euro. US durable goods, trade balance will be watched too but the impacts on markets may not be long lasting. Canada GDP is another key event that could finally remove the already slim chance of a July BoC hike. Here are some highlights for the week:

- Monday: German Ifo; US new home sales

- Tuesday: Japan CSPI; UK BBA mortgage approvals, CBI realized sales; US S&P Case-Shilller house price, consumer confidence

- Wednesday: New Zealand trade balance, business confidence; Eurozone M3; US durable goods, trade balance, wholesale inventories, pending home sales

- Thursday: RBNZ rate decision; Japan retail sales; German CPI flash; US Q1GDP final, jobless claims

- Friday: New Zealand building permits; Japan Tokyo CPI, unemployment rate, industrial production, housing starts, consumer confidence; German retail sales, import prices, unemployment; Swiss KOF; UK Q1 GDP final, M3, mortgage approvals; Eurozone CPI flash; Canada GDP, IPPI and RMPI; US personal income and spending, Chicago PMI

USD/JPY Daily Outlook

Daily Pivots: (S1) 109.79; (P) 110.00; (R1) 110.21; More...

USD/JPY's break of 109.54 suggests that fall from 110.89 has resumed. Such decline is seen as the third leg of the consolidation pattern from 111.39. Intraday bias is back on the downside for 108.10 support and possibly below. But, we'd expect strong support from 61.8% retracement of 104.62 to 111.39 at 107.20 to contain downside and bring rebound. On the upside, above 110.89 will extend the rise from 108.10 towards 111.39 instead.

In the bigger picture, at this point, we're slightly favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 will affirm this view and target 114.73 for confirmation. However, it should be noted that USD/JPY is bounded in medium term falling channel from 118.65 (2016 high). Sustained break of 61.8% retracement of 104.62 to 111.39 at 107.20 will likely resume the fall from 118.65 through 104.62 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BOJ Summary of Opinions | ||||

| 08:00 | EUR | German IFO Business Climate Jun | 101.7 | 102.2 | ||

| 08:00 | EUR | German IFO Expectations Jun | 98 | 98.5 | ||

| 08:00 | EUR | German IFO Current Assessment Jun | 105.6 | 106 | ||

| 14:00 | USD | New Home Sales May | 665K | 662K |

Euro Trading Lower In The Asian Session

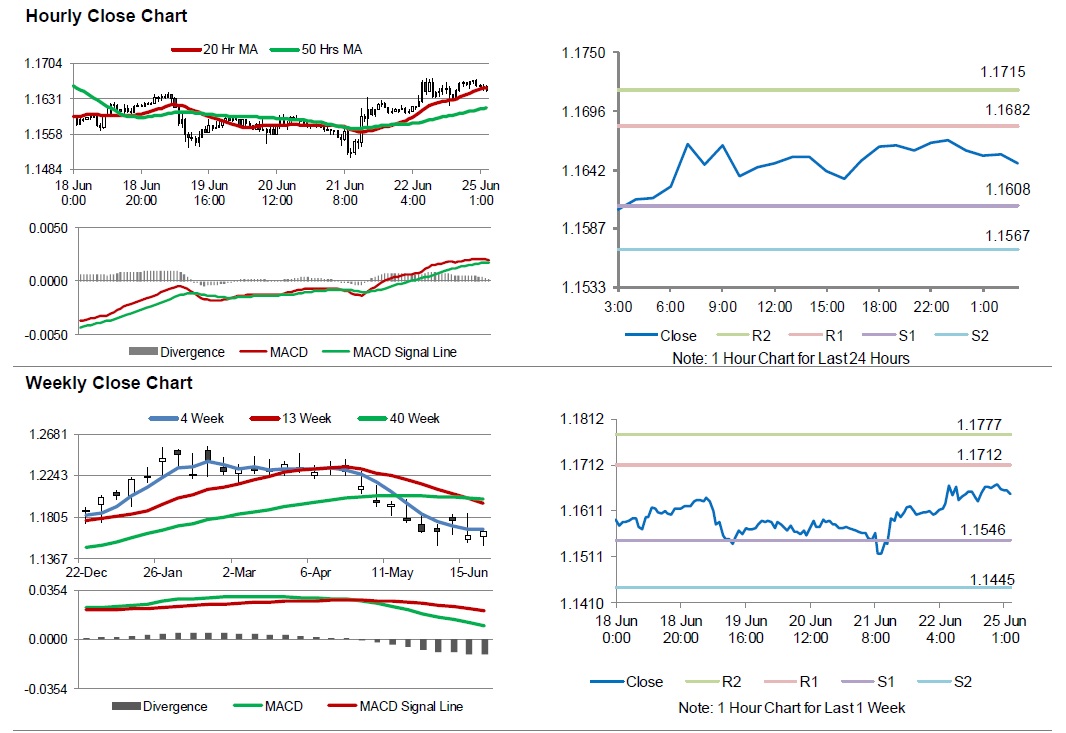

For the 24 hours to 23:00 GMT, the EUR rose 0.45% against the USD and closed at 1.1660 on Friday.

Data indicated that the Euro-zone's flash Markit manufacturing PMI dropped to a level of 55.0 in June, in line with expectations. In the prior month, the PMI had recorded a level of 55.5. On the contrary, the region's preliminary Markit services PMI climbed more than expected to a level of 55.0 in June, compared to a level of 53.8 in the previous month. Market expectations was for the PMI to report an unchanged reading.

Separately, Germany's flash Markit manufacturing PMI declined to an eighteen-month low level of 55.9 in June, more than market expectations for a fall to a level of 56.2. In the previous month, the PMI had registered a level of 56.9. On the other hand, the nation's flash Markit services PMI advanced to a 3-month high level of 53.9 in June, after recording a reading of 52.1 in the prior month, while investors had envisaged it to rise to a level of 52.2.

The US Dollar declined against a basket of currencies, following downbeat economic releases in the US.

Data indicated that the flash Markit manufacturing PMI in the US declined to a level of 54.6 in June, more than market expectations for a fall to a level of 56.1. In the previous month, the PMI had registered a level of 56.4. Moreover, the nation's preliminary Markit services PMI fell to a level of 56.5 in June, at par with market expectations. In the preceding month, the PMI had registered a level of 56.8.

In the Asian session, at GMT0300, the pair is trading at 1.1648, with the EUR trading 0.10% lower against the USD from Friday's close.

The pair is expected to find support at 1.1608, and a fall through could take it to the next support level of 1.1567. The pair is expected to find its first resistance at 1.1682, and a rise through could take it to the next resistance level of 1.1715.

Moving ahead, investors would look forward to Germany's IFO survey indices for June, scheduled to release in a few hours. Moreover, the US new home sales data for May followed by the Dallas Fed manufacturing activity index for June, set to release later in the day, will be on investors' radar.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

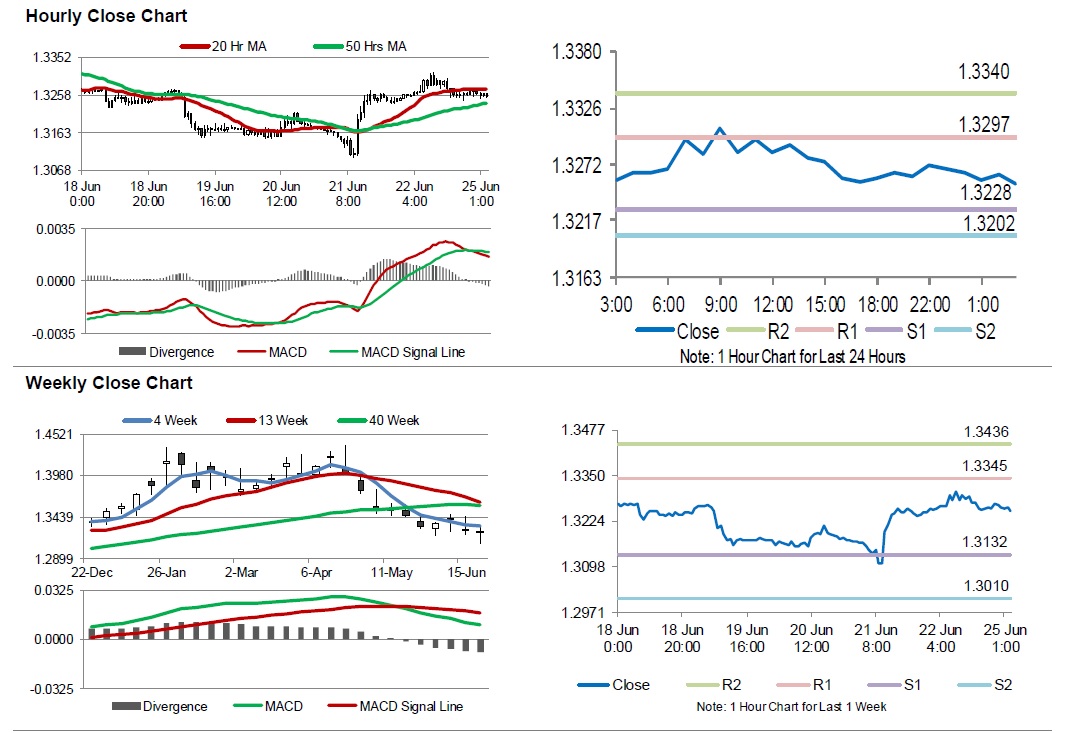

Pound Trading On A Negative Footing This Morning

For the 24 hours to 23:00 GMT, the GBP rose 0.10% against the USD and closed at 1.3260 on Friday.

In the Asian session, at GMT0300, the pair is trading at 1.3253, with the GBP trading 0.05% lower against the USD from Friday’s close.

The pair is expected to find support at 1.3228, and a fall through could take it to the next support level of 1.3202. The pair is expected to find its first resistance at 1.3297, and a rise through could take it to the next resistance level of 1.3340.

With no macroeconomic releases in UK today, investor sentiment would be determined by global macroeconomic news.

The currency pair is trading between its 20 Hr and 50 Hr moving average.

Japanese Yen Trading On A Stronger Footing This Morning

For the 24 hours to 23:00 GMT, the USD rose 0.05% against the JPY and closed at 109.98 on Friday.

In the Asian session, at GMT0300, the pair is trading at 109.51, with the USD trading 0.43% lower against the JPY from Friday’s close, on renewed trade tensions.

Separately, the Bank of Japan’s (BoJ) summary of opinions report showed that officials stressed the need to “patiently continue” its powerful monetary easing and enhance its commitment to reach the 2.0% inflation goal.

The pair is expected to find support at 109.23, and a fall through could take it to the next support level of 108.96. The pair is expected to find its first resistance at 110, and a rise through could take it to the next resistance level of 110.5.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

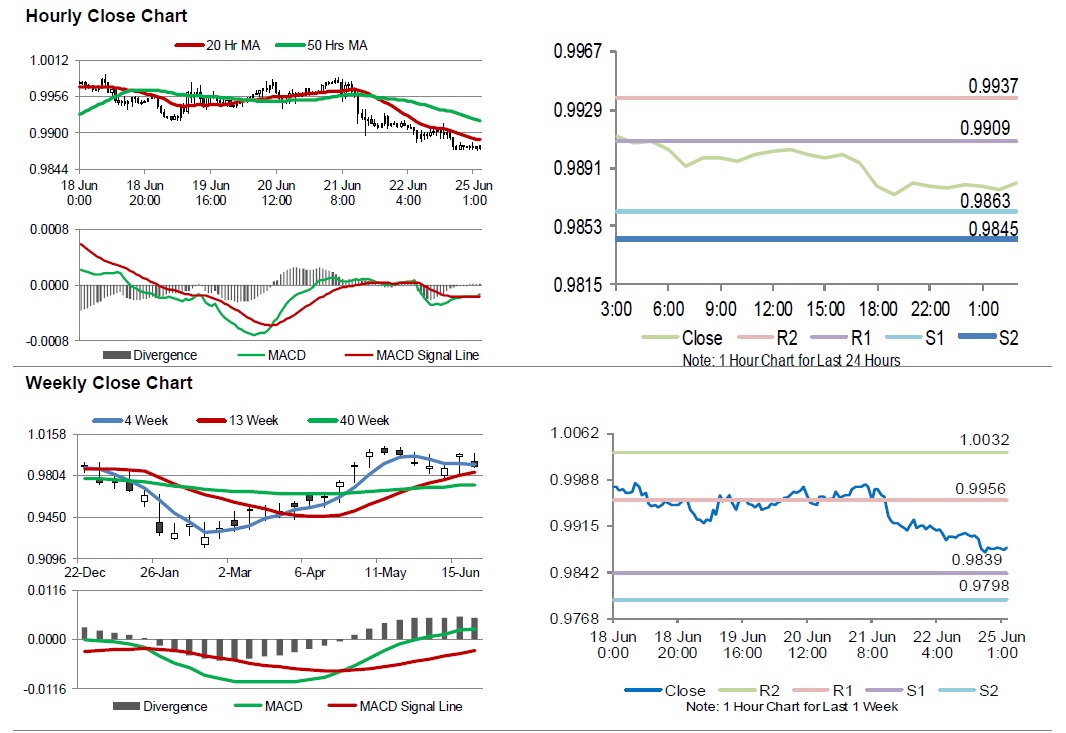

Swiss Franc Trading Flat In The Asian Session

For the 24 hours to 23:00 GMT, the USD declined 0.34% against the CHF and closed at 0.9881 on Friday.

In the Asian session, at GMT0300, the pair is trading at 0.9881, with the USD trading flat against the CHF from Friday’s close.

The pair is expected to find support at 0.9863, and a fall through could take it to the next support level of 0.9845. The pair is expected to find its first resistance at 0.9909, and a rise through could take it to the next resistance level of 0.9937.

Amid no macroeconomic releases in Switzerland today, investor sentiment would be governed by global macroeconomic factors.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

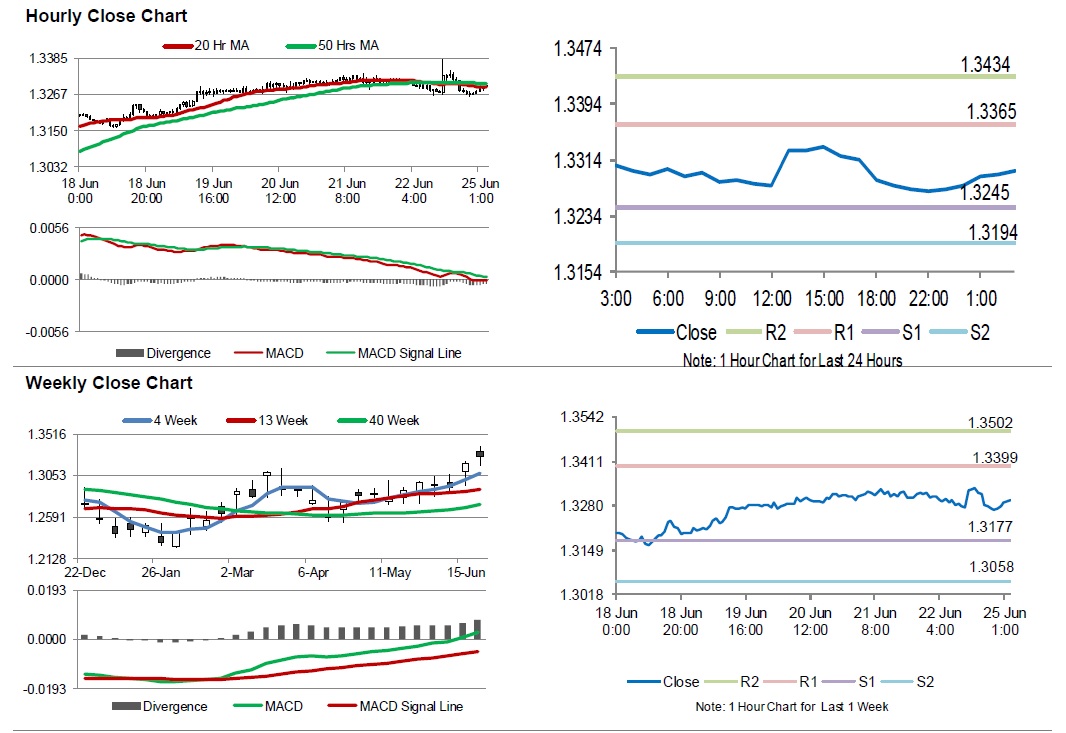

Canadian May CPI Misses Market Expectations, Retail Sales Unexpectedly Falls In April

For the 24 hours to 23:00 GMT, the USD declined 0.34% against the CAD and closed at 1.3271 on Friday.

Data indicated that Canada’s consumer price index (CPI) rose by 2.2% on an annual basis in May, less than market expectations for a gain of 2.6%. The CPI had recorded a similar reading in the prior month.

On the other hand, the nation’s retail sales unexpectedly declined by 1.2% on a monthly basis in April, suggesting weakness in the Canadian economy. Retail sales had registered a revised advance of 0.8% in the previous month, while investors had envisaged for a flat reading.

In the Asian session, at GMT0300, the pair is trading at 1.3297, with the USD trading 0.20% higher against the USD from Friday’s close.

The pair is expected to find support at 1.3245, and a fall through could take it to the next support level of 1.3194. The pair is expected to find its first resistance at 1.3365, and a rise through could take it to the next resistance level of 1.3434.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

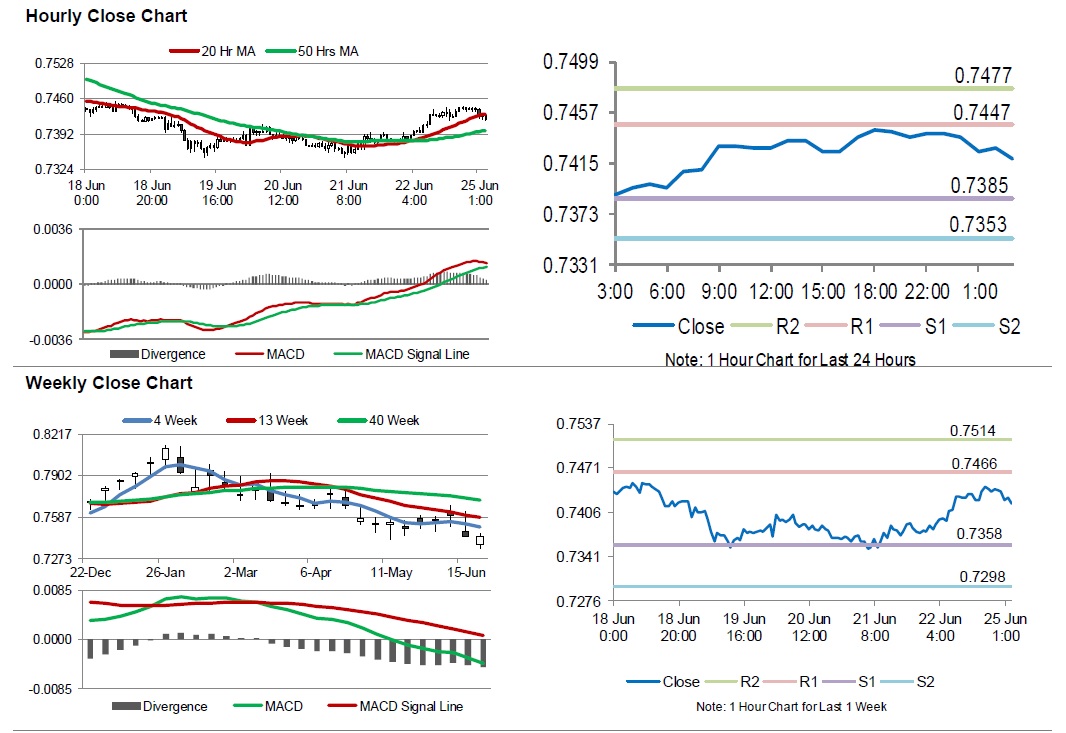

Aussie Reverses Its Gains In The Asian Session

For the 24 hours to 23:00 GMT, the AUD rose 0.79% against the USD and closed at 0.7437 on Friday.

LME Copper prices declined 0.1% or $1.0/MT to $ 2166.0/MT. Aluminium prices rose 0.2% or $10.0/MT to $6811.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7418, with the AUD trading 0.26% lower from Friday’s close.

The pair is expected to find support at 0.7385, and a fall through could take it to the next support level of 0.7353. The pair is expected to find its first resistance at 0.7447, and a rise through could take it to the next resistance level of 0.7477.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

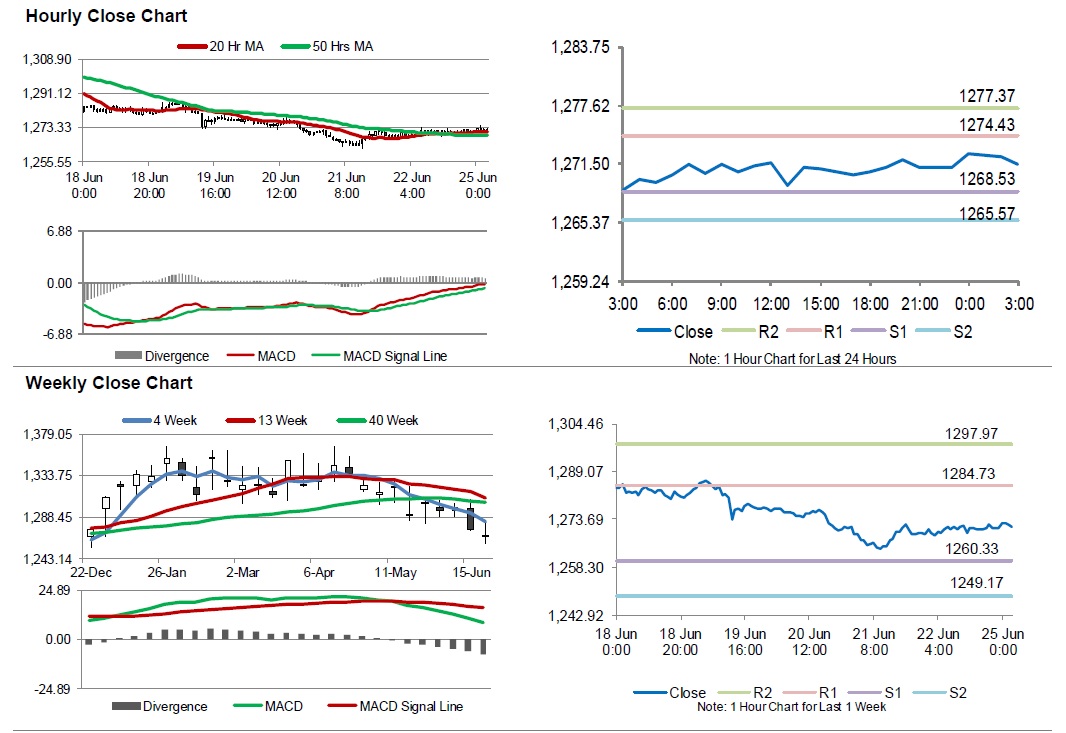

Gold: Yellow Metal Trading A Tad Higher In The Morning Session

For the 24 hours to 23:00 GMT, Gold rose 0.13% against the USD and closed at USD1271.10 per ounce on Friday, amid weakness in the greenback.

In the Asian session, at GMT0300, the pair is trading at 1271.50, with gold trading slightly higher against the USD from Friday’s close.

The pair is expected to find support at 1268.53, and a fall through could take it to the next support level of 1265.57. The pair is expected to find its first resistance at 1274.43, and a rise through could take it to the next resistance level of 1277.37.

The yellow metal is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.