Sample Category Title

Trade War Uncertainty Continues, Focus On Central Bank Speeches From Portugal

The U.S. dollar managed to turn fairly stronger on the day on Tuesday. Economic data was limited. The U.S. building permits data showed an increase of 1.30 million. This was slower than the estimates of a 1.35 million increase. Housing starts fared better, rising 1.35 million and marked the highest increase on a month over month basis.

The market uncertainty continued with the U.S. President Trump announcing fresh tariffs on China which sent the equity markets closing lower on the day.

The lineup of speeches from various central bank chiefs takes precedence today. The speeches include that from the ECB President, Mario Draghi, BoJ's Kuroda, and the Fed's Powell. The central bankers are converging in Portugal for a banking conference.

It was only last year that the ECB President, Draghi talked up the euro currency which sent the currency pair rallying to fresh highs.

On the economic front, the U.S. existing home sales data will be coming out followed later in the evening by New Zealand's quarterly GDP report. The quarterly GDP is expected to rise at a pace of 0.5%, slightly slower than the 0.6% increase that was registered in the previous quarter.

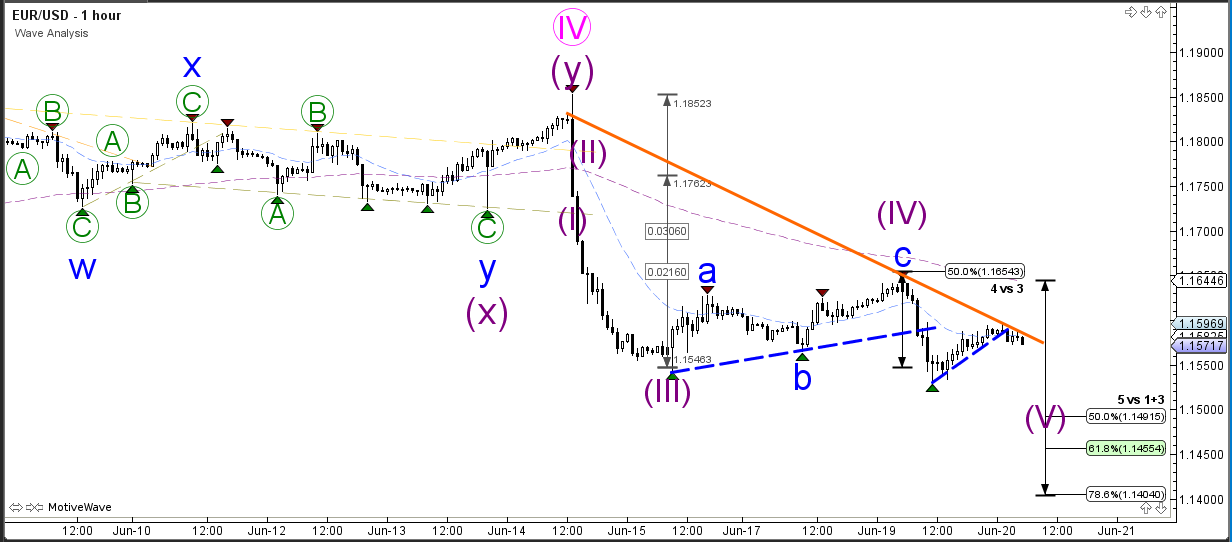

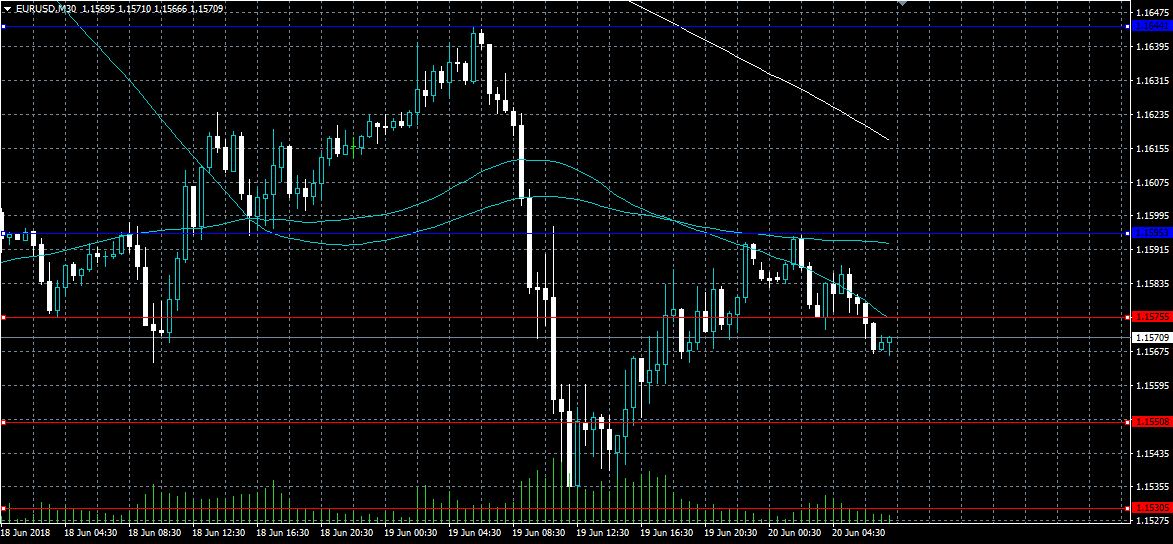

EURUSD Increasingly Bearish Below 1.1575

The euro continues to trade to the downside against the US dollar after ECB President Mario Draghi talked down a future ECB rate hike until late 2019 on Tuesday. The EURUSD pair currently trades around the 1.1570 level, after earlier find support from the 1.1530 level. Bearish selling pressure is increasing on the EURUSD pair after it was strongly rejected from the 1.1595 level.

The EURUSD pair is strongly bearish while trading below the 1.1575 level, further downside towards 1.1530 and 1.1480 remains possible.

If the EURUSD pair moves above the 1.1595 level, the price may correct back towards the 1.1615 and 1.1644 levels.

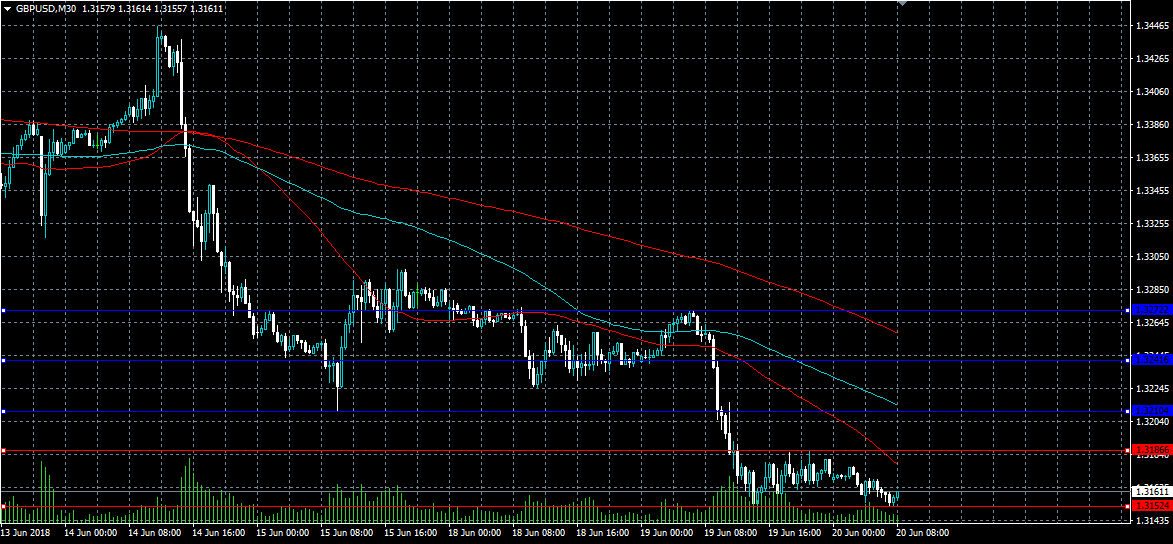

GBPUSD Strongly Bearish Below 1.3186 Level

The British pound continues to fall to fresh yearly trading-lows against the US dollar, with the GBPUSD pair earlier falling to 1.3152, marking its lowest trading level since November 2017. The GBPUSD pair came under heavy technical selling pressure after falling below the 1.3200 level yesterday, with price currently trades around the 1.3160 region. Further technical selling seems likely while sterling trades below the former swing-high, at 1.3186.

The GBPUSD pair is strongly bearish while trading below the 1.3186 level, key technical support is now located at the 1.3152 and 1.3110 levels.

If the GBPUSD pair moves above the 1.3186 level, key technical resistance can be found at the 1.3210 and 1.3241 levels.

Cryptocurrency Prices Drop After Another South Korean Exchange Hack

The price of several well-known cryptocurrencies dropped today after the second largest South Korean exchange announced that it had been hacked. In a tweet, Bithumb said that hackers had managed to steal currencies worth more than $30 million making this the second major cryptocurrency exchange hack this month. Two weeks ago, Coinrail, a South Korean exchange lost more than $37 million worth of digital tokens.

After the hack was reported, Bithumb revealed that it had halted all transactions and moved investor assets to a so-called cold wallet. Bithumb is the sixth largest exchange in the world with daily transaction volumes of more than $300 million.

The current hack confirms cryptocurrency concerns from critics. Their main criticism is that digital assets are an unsustainable means of exchange because of their risks. As a result, many businesses are not willing to accept the currencies because of how easy it is to lose them. With regards to fiat currencies, businesses are usually at ease because the funds are stored in safe banks that operate under tough regulations.

After the news, the price of Bitcoin dropped by 1.2% while Ethereum and Litecoin dropped by 0.8% and 1.0% respectively.

Litecoin is currently trading at $94.22. As the LTC/USD pair dropped today, it settled at the important support of $93.50. In recent weeks, the pair has formed an asymmetrical triangle pattern as shown below. Its current price is below the 14 and 28-day moving average. A drop further from the current support will see the pair test the support of $91.18

FED, ECB Speakers In The Spotlight

Monetary policy is back on the agenda Wednesday, as investors get to hear from top officials at the European Central Bank (ECB) and the US Federal Reserve. Both central banks issued their policy verdicts last week, helping to ignite a large decline in the euro and broad gains for the US dollar. Although Wednesday's speeches won't have the same impact, they could still provide clues about the future evolution of monetary policy on both sides of the Atlantic.

Kicking off the policy circuit is the ECB's Sabine Lautenschlager, who is scheduled to speak at 08:00 GMT. ECB Executive Board member Benoit Coeure will also deliver public remarks at the central bank's weeklong summit in Portugal. At 13:30 GMT, central bank president Mario Draghi will be in the headlines.

In the United States, Fed Chairman Jerome Powell is scheduled to deliver a speech at 13:30 GMT. Powell, who took over from Janet Yellen in February, has already hiked interest rates on two occasions as head of the all-powerful Fed.

Bank of Japan (BOJ) Governor Haruhiko Kuroda and Philip Lowe of the Reserve Bank of Australia (RBA) are also scheduled to speak publicly on Tuesday.

In terms of economic data, Germany will release the monthly producer price index (PPI) at 06:00 GMT.

Shifting gears to North America, the National Association of Realtors (NAR) will report on existing home sales at 14:00 GMT. The sale of previously-owned homes is forecast to rise 1.5% in May to a seasonally adjusted annual rate of 5.52 million units.

In other news, the Swiss National Bank (SNB) will issue its Quarterly Bulletin at 13:00 GMT. Since 1983, the Bulletin has provided insights on monetary policy, business cycle trends and the broader economy.

EUR/USD

Europe's common currency experienced yet another breakdown on Tuesday, as prices once again approached their year-to-date lows. EUR/USD bottomed at 1.1545, where it was down roughly 100 pips from the intraday high. The pair is now trading at 1.1577, where it was down slightly from the previous close. Immediate support is located at 1.1510.

GBP/USD

Cable resumed its downtrend Tuesday, as prices reached their lowest level in about seven months as the prospect of a Brexit deal began to fade. GBP/USD fell from a high above 1.3270 all the way back down to 1.3162. After falling below 1.3200, cable now faces immediate support at 1.3135. A breakdown below this level will likely expose 1.3100.

AUD/USD

The Australian dollar also headed for losses as the greenback continued to assert its dominance on the currency markets. AUD/USD bottomed near 0.7350 on Tuesday and has since recovered to around 0.7381. The pair faces immediate support at the 0.7333 handle, which reflects the swing low from May of last year.

Currencies: EUR/USD Holding Near Recent Lows Even As Global Tensions Ease

Rates: Gentle improvement in risk sentiment

Risk sentiment improved overnight with Asian stocks rebounding and the US note future and Japanese yen losing the past two days' momentum. Central bankers aren't expected to provide new insights in Sintra following last week's key decisions. The eco calendar is empty, suggesting risk sentiment will remain in the driver seat.

Currencies: EUR/USD holding near recent lows even as global tensions ease

Yesterday, FX markets were also affected by the trade-driven global risk-off trade. EUR/JPY, USD/JPY and EUR/USD all closed the session lower. This morning, it looks that trade tensions are easing. USD/JPY rebounds, but the upside in EUR/USD looks less easy. Sterling remains in the defensive ahead of a key Brexit vote in Parliament this afternoon.

The Sunrise Headlines

- The US equity markets continue to lose with the trade war still in play, with S&P500 losing all gains it made in 2018. The Asian markets opened rather positive, with only Chinese markets in red.

- Iran has indicated it will oppose Saudi Arabia and Russia, who want to leave the current deal of '16 to increase total output and thereby pleasing the US. Iran stated 'OPEC should not receive any instructions of the US'.

- In the UK, the House of Commons will vote today on the 'meaningful vote', after the House of Lords had rejected PM May's proposal on Monday. Today's vote can shape UK strategy for brexit and is expected to be a very close call.

- Russia has joined the trade debate and will impose import tariffs on certain goods from the US. The move follows a request from Russian businesses that were hit by US tariffs on steel and aluminium.

- Merkel and Macron have found common ground on the President's proposal to reform the Eurozone's budget. They left details open for discussion at the EU summit later this month. Both hailed 'a new chapter' for the currency union.

- A rare positive statement on international trade was made by President Trump yesterday saying progress was made in talks to update the NAFTA agreement. A deal between the US, Canada and Mexico, however, is not yet on the horizon.

- A skinny economic calendar for today, keeping the ECB's Forum in Sintra in the spotlight. Draghi will have discussions with his colleagues from the US (Fed gov. Powell), Japan (BOJ gov. Kuroda) and Australia (RBA gov. Lowe).

Currencies: EUR/USD Holding Near Recent Lows Even As Global Tensions Ease

EUR/USD holding near recent correction low

Contrary to what was the case of late, the trade war also affected global FX trading yesterday. Risk-off triggered broad yen-buying resulting in a decline of USD/JPY, EUR/JPY and via the crosses also of EUR/USD. Soft ECB comments at in Sintra reinforced the euro decline. Selling eased later but the three cross rates still finished in negative territory. EUR/USD closed at 1.1590 (from 1.1623). USD/JPY closed at 110.06 (from 110.55). The risk-off modus weighed on smaller, less liquid currencies like the CAD and the Aussie dollar and smaller currencies on boundaries of the euro zone (SEK, PLN, CZK and to a lesser extent NOK). This morning, Asian are rebounding off the recent lows, with China still underperfoming. The jury is still out, but the direct impact from the trade-war might be easing. USD/JPY tries to regain the 110 mark. EUR/USD trades off recent lows, but the picture stays unconvincing (1.1575). The decline in likes of the Aussie dollar, which suffered from the trade conflict looks like slowing down.

Today, US data, including existing homes sales are only of second tier significance for FX trading. Fed's Powell, BOJ's Kuroda, ECB's Draghi and other ECB members wil speak in Sintra. The question is whether markets will recover from yesterday's risk-off trade. If so, USD/JPY might profit and it might pressure on some smaller currencies. It doesn't feel that the euro is in pole-position to profit from easing tensions. Policy divergance between the Fed and the ECB as it appeared at last week's policy meetings, hampers a euro rebound, even if risk sentiment improves. Of late, we advocated that a retest of the 1.1510 correction low is possible. We maintain that view. The dollar can stay strong for longer. In a day-to-day perspective, the pressure on USD/JPY might ease, at least until the next flairing up of (geopolitical) uncerainty.

Yesterday, Brexit uncertainty and a negative global risk sentiment weighed on the sterling. EUR/GBP trended higher in the 0.87 big figure. Cable set a new correction low below the 1.32 support. Today, the Lower House will to vote again on the ‘meaningful vote'. Even if May survives the vote, the domestic battle on Brexit won't be over. It is also not clear that markets will consider a victory of the government as sterling supportive, as it raises the chance on Britain to crash out of the EU. We don't preposition for a sustained sterling rebound yet. Tomorrow's BoE assessment might also remain cautious and provide little support for sterling

EUR/USD: easing global tenisons might not be a big help for the euro

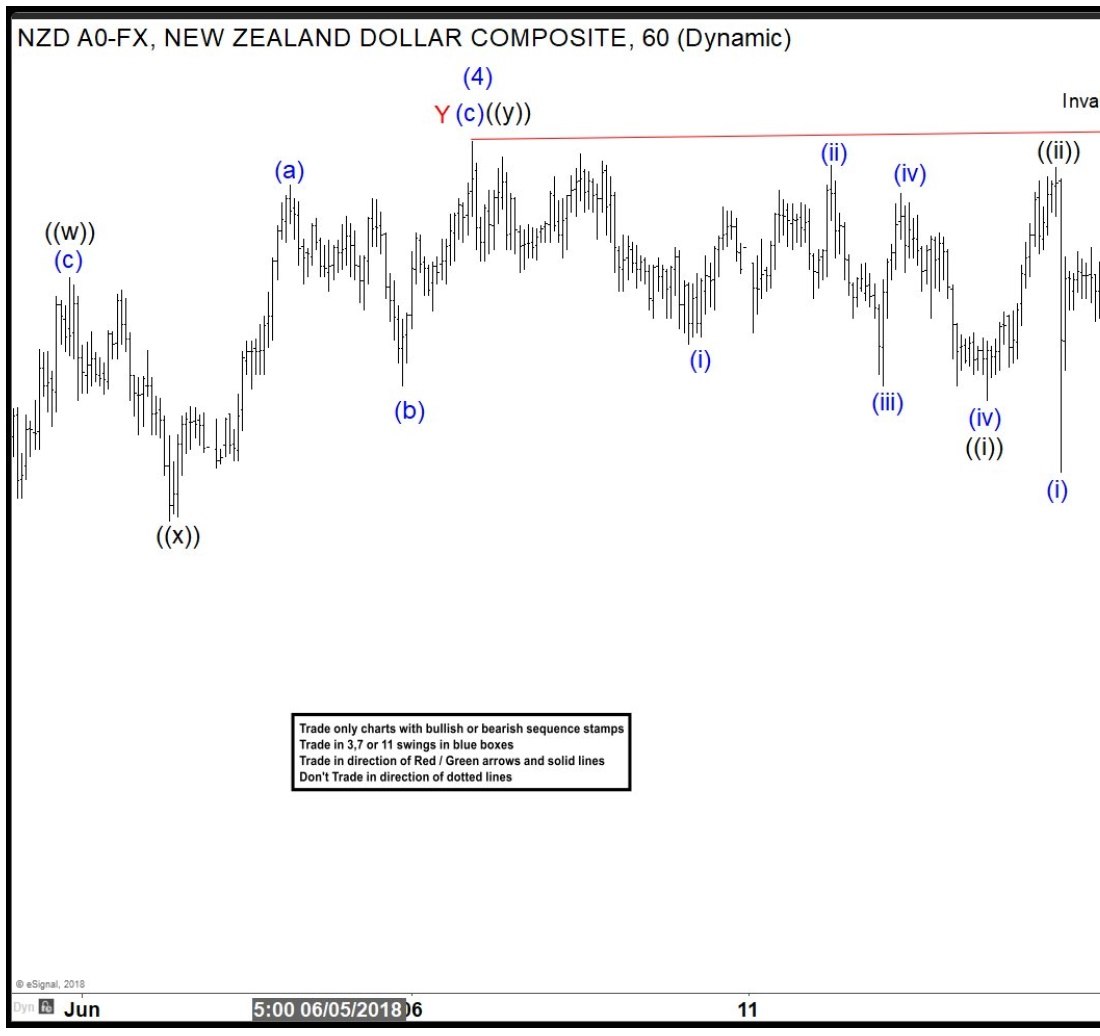

Elliott Wave Analysis: NZDUSD Ready For Recovery?

NZDUSD short-term Elliott Wave view suggests that the bounce to 0.7060 high ended intermediate wave (4). Down from there, the decline is unfolding as Impulse Elliott Wave structure where sub-division of Minute wave ((i)), ((iii)) & ((v)) are unfolding in 5 waves within a lesser degree cycle. On the other hand, the corrective Minute degree wave ((ii)) & ((iv)) should unfold in any 3 wave corrective sequence, such as zigzag, double three, flats.

Down from 0.7060 high, the pair ended the first leg lower in 5 waves at 0.6991 low in Minute wave ((i)). Minute wave ((ii)) ended at 0.7053, Minute wave ((iii)) ended at 0.6918 low in another 5 waves. Up from there, the bounce to 0.6955 high ended Minute wave ((iv)). Below from there, Minute wave ((v)) of 1 remains in progress in another 5 waves structure. Pair has already reached the minimum target in blue box, thus cycle from 0.7060 high is mature. Once Minor wave 1 is complete, pair should bounce in Minor wave 2 in 3, 7 or 11 swings before the decline resumes, provided pivot at 0.7060 high stays intact. We don’t like buying the pair in the proposed bounce.

NZDUSD 1 Hour Elliott Wave Chart

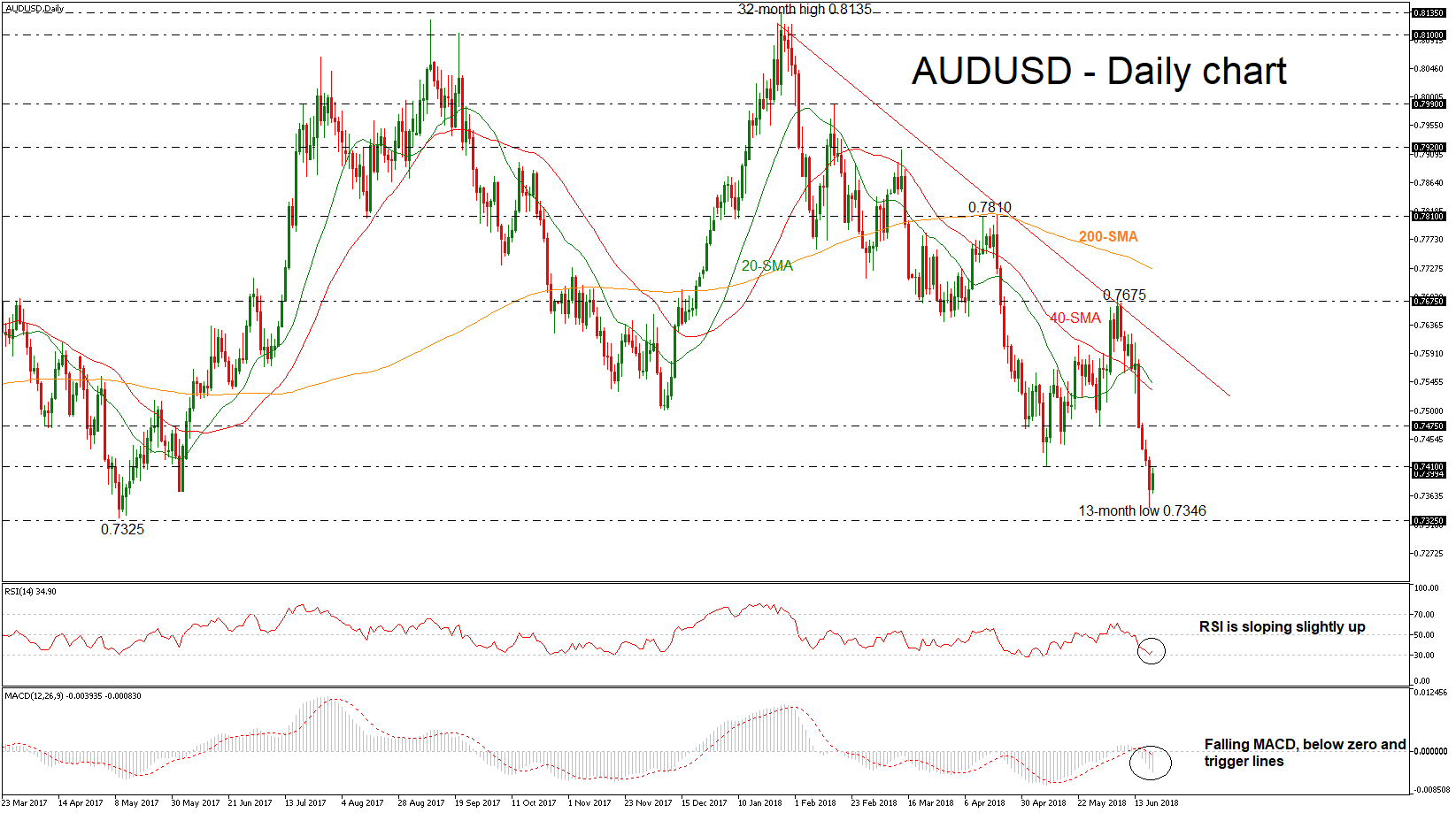

AUDUSD Jumps Above 13-Month Trough Of 0.7346, Still Looks Negative In Medium-Term

AUDUSD recorded an aggressive bearish rally over the past four days, reaching a fresh 13-month low of 0.7346 on Tuesday. Today, though, the pair is on the backfoot and the technical indicators seem to be mixed as the market could ease a little bit in the short-term.

In the daily timeframe, the RSI indicator is sloping slightly to the upside after the rebound on the oversold zone, while the MACD oscillator is currently increasing negative momentum below its red-trigger line and the zero line. Additionally, the simple moving averages (SMAs) are heading lower following the price action.

The medium-term picture is looking predominantly bearish at the moment and the next support level to have in mind is the 0.7325 barrier, taken from the low on May 2017. A drop below this area could open the way towards the 0.7160 hurdle, identified by the trough on December 2016.

A move to the upside may meet resistance near the intraday’s high around the 0.7410 resistance. In case of further gains, the price could touch the 0.7475 resistance, taken from the bottom on May 31. A jump above this level, the pair could meet the 40-SMA and then the 20-SMA at 0.7533 and 0.7541 respectively.

Overall, both the short- and medium-term outlooks are currently looking bearish, though caution is warranted in the near-term as there are signs of a possible small retracement to the upside.

Asian Stocks Gain Signaling Recovery Of Risk Sentiment, House Of Commons Votes On Brexit Amendments

Here are the latest developments in global markets:

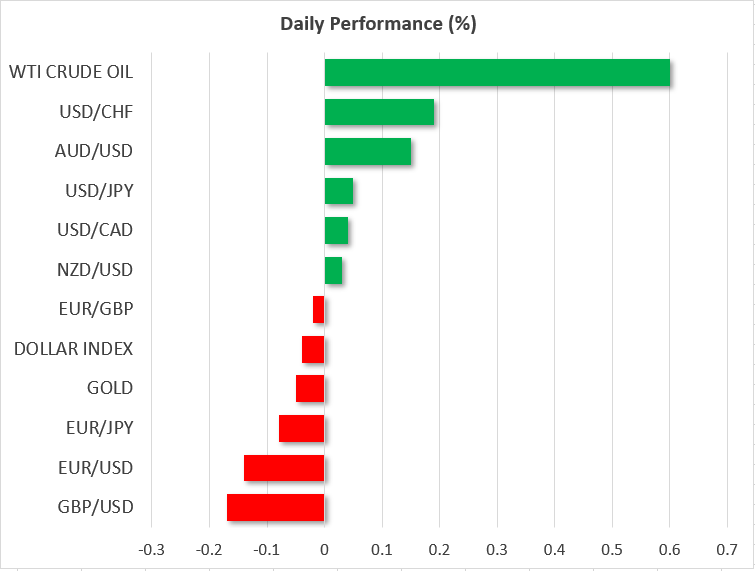

FOREX: The US dollar index is lower on Wednesday, though by less than 0.1%, giving back some of the gains it posted in the previous session as the currency with the most weight in the index – the euro – tumbled. The haven-perceived yen is also on the retreat, paring some of the gains it posted yesterday.

STOCKS: Wall Street closed lower on Tuesday, amid fears over an escalating US-China trade spat and its potential repercussions. The Dow Jones led the way lower, tumbling by 1.15%, while the S&P 500 and the Nasdaq Composite fell by 0.40% and 0.28% respectively, both paring a significant chunk of their earlier losses before the closing bell. Today may be different though, as futures tracking the Dow, S&P, and Nasdaq 100 are all signaling a higher open. The same was true in Asia, with some dovish comments from the PBOC supporting risk appetite. Japan's Nikkei 225 and Topix climbed by 1.24% and 0.51% correspondingly, while in Hong Kong, the Hang Seng rose 0.82%. In Europe, futures following all the major indices were a sea of green as well, pointing to a higher open today.

COMMODITIES: Oil prices are higher on Wednesday, buoyed by expectations that the OPEC meeting on Friday may not end up delivering a material increase in production. Iran reiterated yesterday that it will not support any increase in output, a position shared by Venezuela and Algeria, setting the stage for a showdown between those producers and OPEC's de-facto leader, Saudi Arabia. Any OPEC decision needs to be unanimous, and it increasingly appears this will not be the case this time. In precious metals, gold is marginally lower today, extending losses from Tuesday. The yellow metal has remained impervious to escalating trade tensions, a rather bizarre development considering the heightened uncertainty in markets. A reasonable explanation is that a stronger dollar is exerting downward pressure on prices, and that investors may be tactically selling gold to cover losses in riskier assets, such as equities.

Major movers: Risk sentiment recovers somewhat; euro softens after Draghi

The risk-off tone that characterized price action on Tuesday, amid an escalating trade spat between the US and China, seems to have eased on Wednesday. Haven assets such as the yen are trading a little lower, giving back some of the gains they posted in the previous session, while risk-sensitive currencies like the aussie and the kiwi are on the rebound. Meanwhile, although US stock markets closed lower yesterday, Asian indices are higher today, reflecting that the pessimism has been “put on hold for now” (to paraphrase the US Treasury Secretary).

Given the absence of any major news on the trade front, the trigger for the shift in sentiment appears to have been some market-friendly signals from the People's Bank of China (PBOC). The central bank said it is prepared for outside shocks and that China has room to face all sorts of trade frictions, fueling speculation for a loosening of policy should the trade outlook deteriorate. Ironically, any further easing from the PBOC could lead to a weaker yuan, thereby exacerbating the US-China trade deficit that the US administration is so desperately trying to reduce.

The euro came under renewed selling interest yesterday, following some remarks from ECB President Draghi, who reinforced expectations that a hike may only come after the summer of 2019. Looking at market pricing, investors seem to have digested the message. The Bank is currently expected to push the rate-hike button in Q4 2019, when it is anticipated to hike rates by a modest 10bps.

In the UK, Brexit remains front and center. The Government said yesterday it “cannot accept” a Lords amendment giving Parliament a meaningful vote on the final Brexit deal. The administration will reframe its rejected version of the bill and put it for another vote this week. Broadly speaking, anything that gives Parliament a greater say over Brexit is considered positive for sterling. Thus, the outcome of the vote could set the tone for the pound's direction over the remained of the week, especially given the absence of tier-one UK data.

Elsewhere, the Canadian dollar continued to lose ground on Tuesday, touching a fresh one-year low against its US counterpart. With little in the way of news or data out of Canada lately, the plunge appears to be owed more to fluctuations in oil prices, as well as the broader risk-aversion in markets seen yesterday clouding the outlook for commodity currencies like the loonie. Similarly, while aussie/dollar is in recovery-mode today, it touched a one-year low on Tuesday as well.

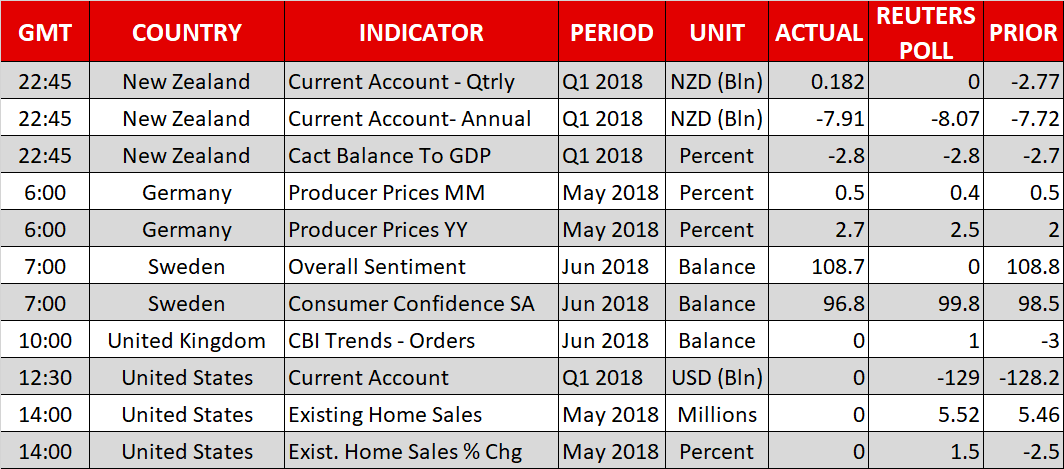

Day ahead: House of Commons vote, global trade developments and ECB Forum panel discussion in focus; US existing home sales and current account data due

Existing home sales and current account data out of the US are the releases generating most interest out of Wednesday's calendar. A House of Commons vote on Brexit amendments that has the potential to put PM Theresa May's position in jeopardy, as well as the ongoing trade spat between the US and China will be taking priority over today's releases though. Meanwhile, a panel discussion featuring the heads of the ECB and the Federal Reserve will also be in focus.

At 1000 GMT, the Confederation of British Industry's gauge of order books pertaining to factory output is expected to return to positive territory at +1, after falling to -3 in May, its lowest level since November 2016.

In the US, current account data for Q1 due at 1230 GMT are anticipated to show the deficit widening to $129.0 billion from $128.2bn in Q4. Later (1400 GMT), the country's existing home sales for May are projected to have risen by 1.5% m/m, after declining by 2.5% in April.

Sterling is expected to be sensitive to a House of Commons vote that may cast fresh doubts on PM May's leadership, adding a layer of uncertainty over the UK; a clash between Theresa May and pro-EU “fellow” Conservatives over her Brexit plans might play out today.

Escalating US-China trade tensions that have weighed on global equity markets on Tuesday will also be closely monitored during today's trading.

The EIA's weekly report on crude oil inventories due at 1430 GMT might offer some short-term direction to oil prices ahead of the upcoming two-day OPEC meeting in Vienna commencing on June 22. Crude stocks are projected to have declined by around 1.9 million barrels during the week ending June 15, after falling by around 4.1m in the previously tracked week.

Among policymakers making appearances are ECB President Mario Draghi, Fed Chairman Jerome Powell, Bank of Japan Governor Haruhiko Kuroda and Reserve Bank of Australia Governor Philip Lowe. They will all be participating in an eagerly-awaited panel discussion on central bank policy at the ECB Forum in Sintra, Portugal at 1330 GMT. In the meantime, a report on the eurozone economy presented by the governor of the Bank of France at 0730 GMT might attract interest.

In the meantime, North Korea's Kim Jong Un will be completing his two-day visit to Beijing.

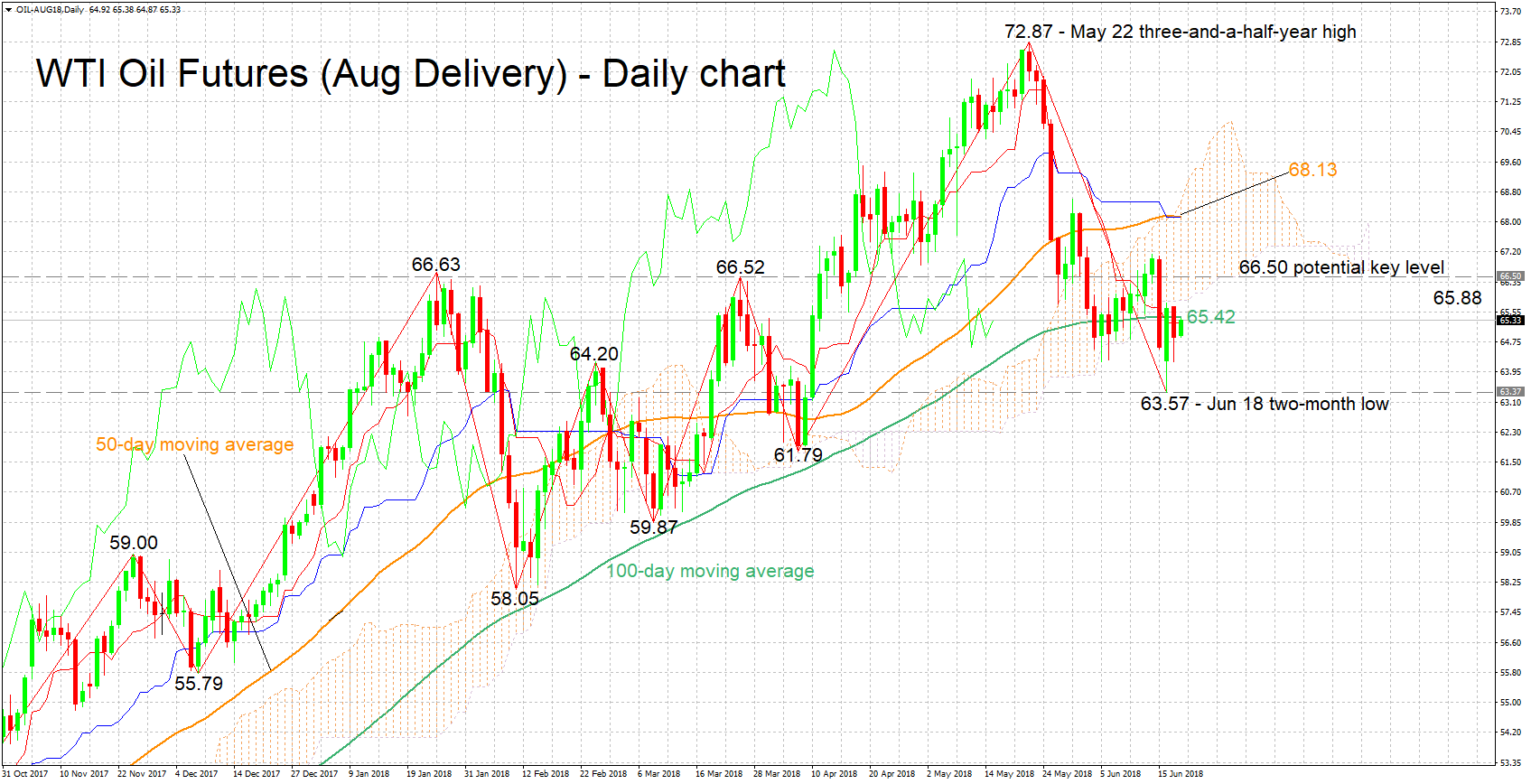

Technical Analysis: WTI oil futures bearish bias eases

WTI oil futures (August delivery) have managed to recover from Monday's two-month low of 63.57. Still, the short-term bias remains to the downside as evidenced by the Tenkan-sen which is below the Kijun-sen line and following a notable decline from a three-and-a-half-year high of 72.87 in late May. The bearish momentum has eased though, with the flat Kijun-sen also attesting to this.

If today's EIA report shows a larger-than-anticipated drawdown in crude inventories, then prices could move higher. The area around the current level of the 100-day moving average at 65.42 seems to be providing immediate resistance to advances. The Tenkan-sen (65.25) which was violated earlier in the day and the Ichimoku cloud bottom (65.88) are also part of the region around the 100-day MA. Further above, the range around 66.50, which encapsulates a couple of peaks from previous months, may be of significance.

On the downside and in case of a smaller-than-expected drawdown in crude stocks (or a buildup) that pushes prices down, support could be provided around 64.20, this being a previous top. Steeper losses would shift the focus to Monday's two-month low of 63.57 for additional support.

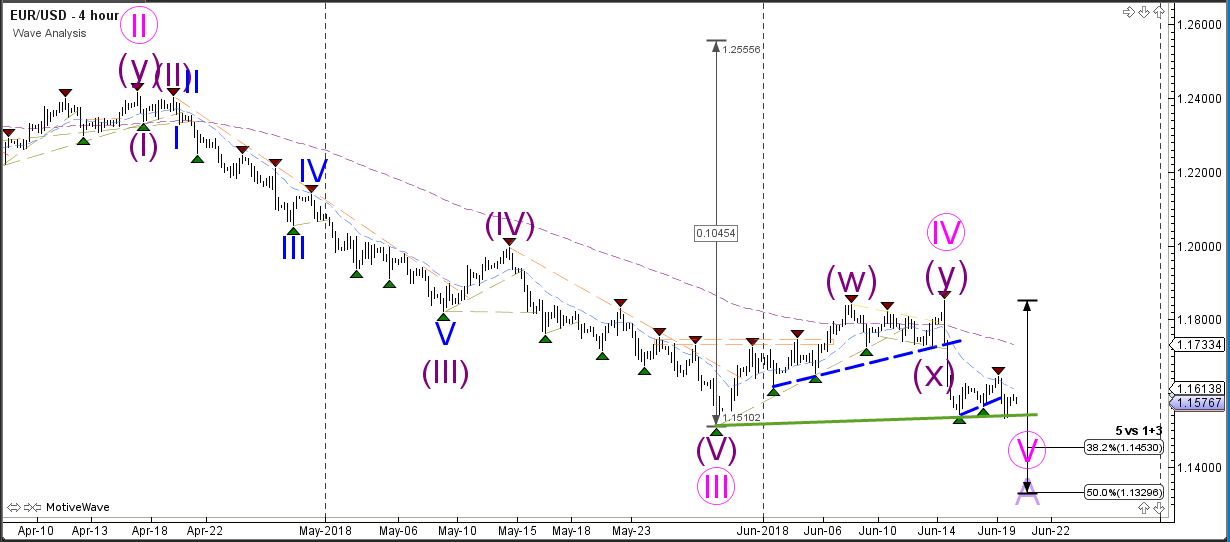

EUR/USD Downtrend Continues After Bearish Breakout

The EUR/USD downtrend continues after another bearish break of a smaller consolidation zone. The next key support zone (green) is the previous bottom. Price seems to be building a potential 5th wave within wave A (purple) but price needs to break below support. The main target is 1.1450 due to the presence of a 50% Fibonacci retracement level on the weekly chart.

The EUR/USD seems to building a potential break, pullback and continuation within the bearish wave 5 (purple).