Sample Category Title

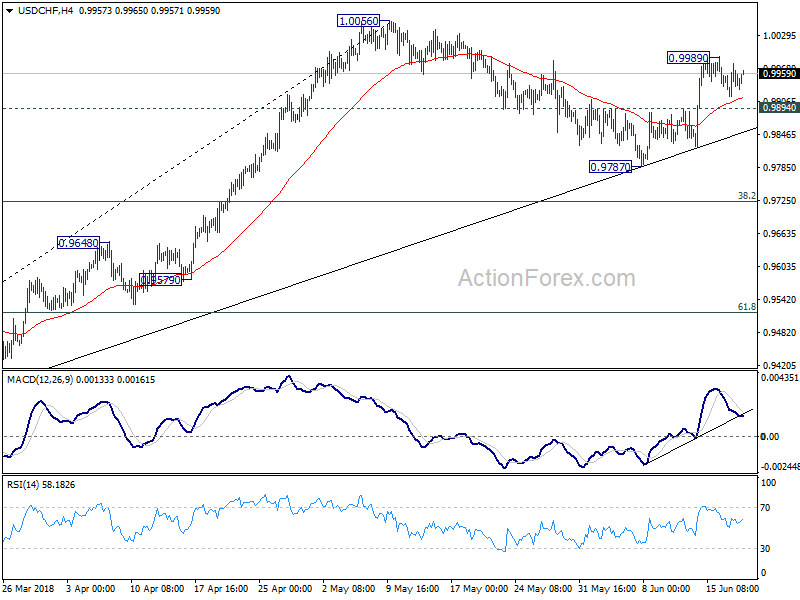

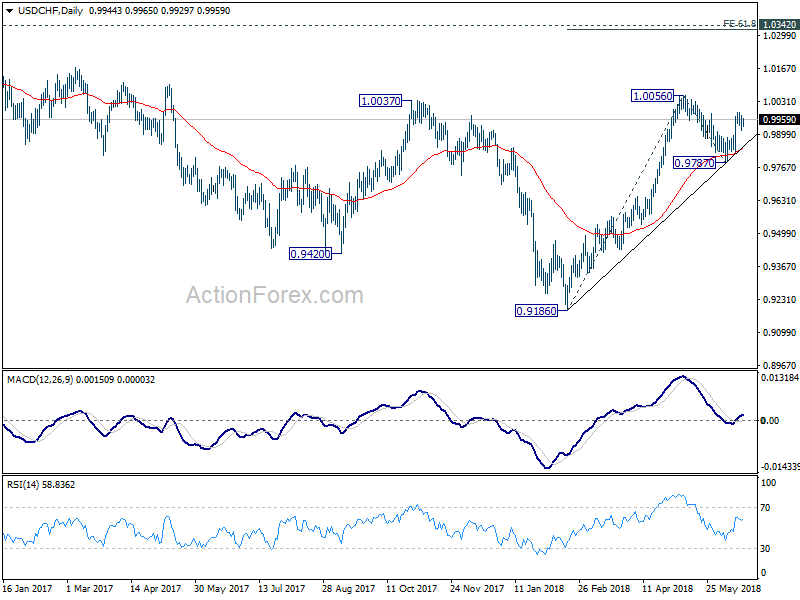

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9913; (P) 0.9945; (R1) 0.9974; More...

USD/CHF stays in tight range below 0.9989 and intraday bias remains neutral. Further rally is expected with 0.9894 minor support intact. As noted before, the corrective fall from 1.0056 should have completed at 0.9787. Above 0.9989 will bring retest of 1.0056 first. Break will resume the rise from 0.9186 and target 61.8% projection of 0.9186 to 1.0056 from 0.9787 at 1.0325, which is close to 1.0342 key resistance. However, break of 0.9894 will likely extend the correction, possibly through 0.9787 before completion.

In the bigger picture, medium term decline from 1.0342 has completed with three waves down to 0.9186. Rise from there is currently viewed as a leg inside the long term range pattern. Hence, while further rally would be seen, we'd be cautious on strong resistance from 1.0342 to limit upside. For now, further rise is expected as long as 38.2% retracement of 0.9186 to 1.0056 at 0.9724 holds. However, sustained break of 0.9724 will dampen this bullish view and would at least bring deeper fall to 61.8% retracement at 0.9518.

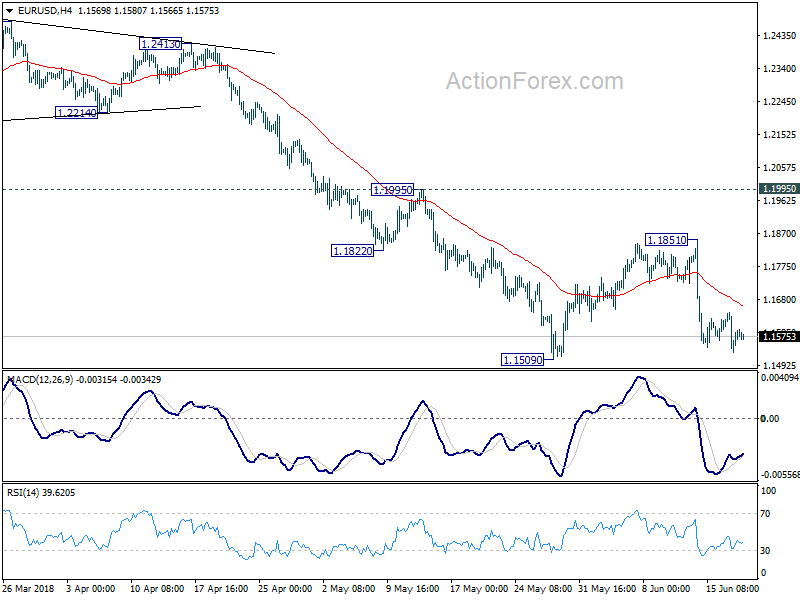

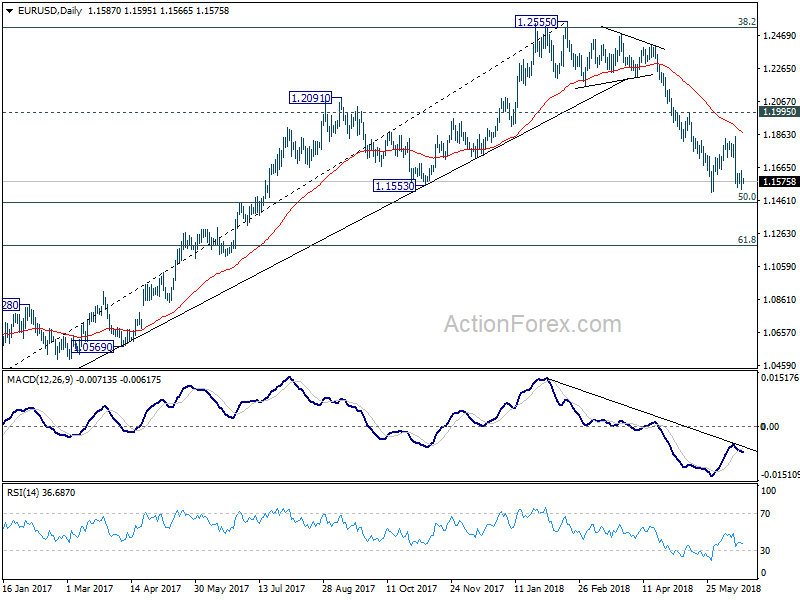

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1532; (P) 1.1589 (R1) 1.1646; More.....

Intraday bias in EUR/USD remains neutral as more consolidative could be seen. But in case of another recovery, upside should be limited below 1.1851 resistance to bring fall resumption. Firm break of 1.1509 will resume larger decline from 1.2555 through 50% retracement of 1.0339 to 1.2555 at 1.1447 to 61.8% retracement at 1.1186.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

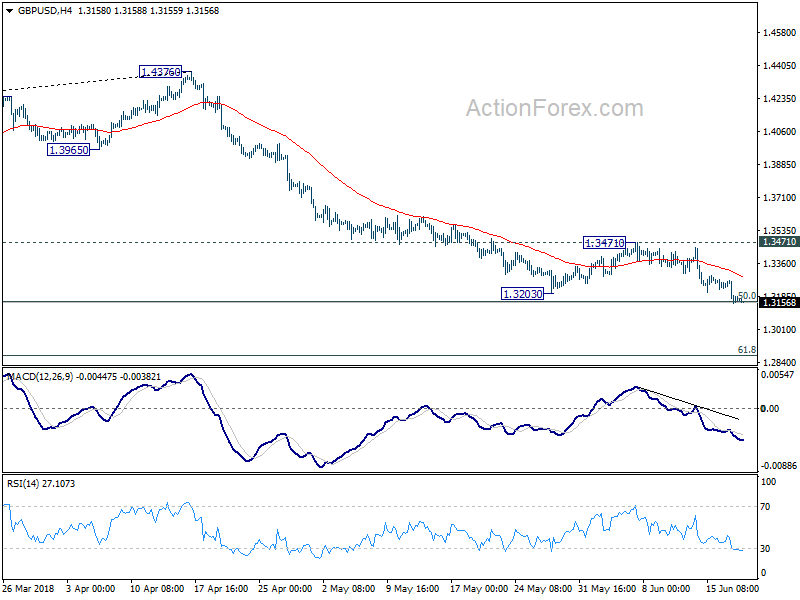

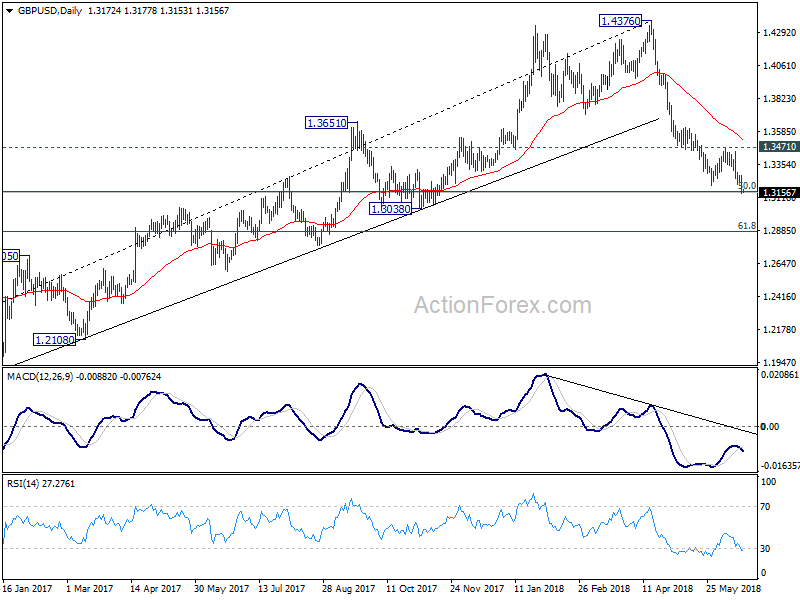

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3125; (P) 1.3199; (R1) 1.3249; More...

Intraday bias in GBP/USD remains on the downside for the moment. Decline from 1.4376 is in progress. Sustained break of 50% retracement of 1.1946 to 1.4376 at 1.3161 will pave the way to 61.8% retracement at 1.2875 next. On the upside, break of 1.3471 resistance is now needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4177). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 55 day EMA (now at 1.3527) holds, even in case of strong rebound.

Yen Retreats Mildly as Sentiments Stabilized, Sterling Weak ahead of BoE

Sentiments somewhat stabilized slightly in Asia as markets digest trade war triggered losses. China's Shanghai composite is losing -0.59% at the time of writing. But Nikkei and Hong Kong HSI are up 0.36% and 0.41% respectively. DOW lost -287.26 or -1.15% to close at 24700.21, but it has already pared much losses after hitting as low as 24567.75 overnight. S&P 500 closed down -11.16 pts or -0.40% at 2762.59. NASDAQ lost -21.44 pts or -0.28% to 7725.59, still the better performing one. In the currency markets, Australia, Canadian and New Zealand Dollar recover mildly today while Yen retreats. But for the week, Yen remains the strongest one, followed by Swiss Franc. Sterling is the weakest one ahead of BoE rate decision, followed by Aussie and then Canadian.

The economic calendar remains light today. Australia Westpac leading index dropped -0.2% in May. Germany will release PPI and UK will release CBI trends total orders in European session. US will release current account and existing home sales. Nonetheless, there are some big guns due to speak at the ECB forum, including panel discussion with ECB President Mario Draghi, BoJ Governor Haruhiko Kuroda, RBA Governor Philip Lowe and Fed Chair Jerome Powell.

Asian business sentiments deteriorated on trade war risks

Sentiments of Asian Business deteriorated in Q2 according to a survey by Thomson Reuters and INSEAD, over June 1-15. The sentiment index, representing six-month outlook from 61 firms, dropped -5pts to 74 in Q2. It hit a seven-year high of 79 in Q1. That's also the first decline since September 2017 even though reading above 50 still indicates a positive outlook.

Antonio Fatas, a Singapore-based economics professor at global business school INSEAD, said in the released that "Trade war is not a risk but a reality." He added that "U.S. tariffs are going up against China but also against some of its traditional allies, such as Canada and the European Union. They are all about to retaliate and today we do not see an easy way out." Fatas also said "companies can try to go around tariffs by moving production to other countries, this is costly and inefficient. It is a short-term solution but not optimal."

Among responses, worries of global trade war, higher interest rates, rising oil/commodity prices and foreign exchange fluctuation are see as the biggest perceived risks to business outlook.

China vows to fight as concessions will not appease Trump's blood lust

China stepped up its rhetoric against US threat of tariffs through an English editorial in the official China Daily. There it warned that "faced with this heightened intimidation from the US, China has no choice but to fight back with targeted and direct measures aimed at persuading the US to back off, since it appears that any concessions it makes will not appease the Trump administration, which wants to suck the lifeblood from the Chinese economy."

And, "Beijing will have to ensure that Washington is aware that there will be heavy price to pay every action it strikes against China if it is to avoid being a victim of the Trump administration's growing blood lust." "Those US companies and workers that feel the brunt of China's retaliation should pass the word to Washington, that despite the pronounced aim of the Trump administration being to protect domestic industries and workers, the injuries that will be done them will be because of its actions."

On other hand, White House trade adviser Peter Navarro warned China "may have underestimated the strong resolve of President Donald J. Trump." And, "if they thought that they could buy us off cheap with a few extra products sold and allow them to continue to steal our intellectual property and crown jewels, that was a miscalculation."

Suggested readings on trade war:

- US Companies Doomed to Suffer from Trump's Protectionist Policy

- US-China Trade: Trade War Becomes A Reality As Trump Pushes Further

- Potential U.S. Auto Tariffs: Canadian Scenario Analysis

- US-China Trade: From 'Grand Bargain' Towards Trade War?

- Who Would Feel the Pain from American Auto Tariffs?

- Weighing the Impact of U.S. Steel and Aluminum Tariffs on Canada

BoJ minutes: Timing of reaching inflation target was merely a projection

BoJ released minutes of the April 26-27 meeting today. The only surprise out of that meeting was that BoJ dropped the time frame it set for achieving the 2% inflation target. The minutes provided more details on the discussions. Many members believed that the timing of reaching the 2% inflation was "merely a projection". At the some time, "some market participants perceived this projection as a deadline for achieving 2 percent inflation, linking changes in said timing to policy adjustments, and this view was deeply entrenched among them."

Some members expressed that "attracting excessive attention merely to forecast figures would not be appropriate from the perspective of communication with the markets". And, most members expressed that " it was appropriate to cease providing a description on the projected timing of achieving the price stability target". And that was with the aim to clarify that the timing was "not a specific deadline" for meeting inflation target. Nonetheless, one member expressed the concern that dropping the time frame could "weaken the effects of the commitment" of BoJ to hit target.

BoE to stand pat tomorrow, August hike uncertain

BoE will most likely keep the Bank Rate unchanged at 0.50% tomorrow. Known hawks Ian McCafferty and Michael Saunders are expected to vote for rate hike while others would vote for standing pat. There will be no inflation report but just the meeting minutes. And attention will on whether the minutes give any hint on an August hike.

According to the latest Bloomberg survey, only 55% of respondents forecast a hike in August. That's even down from 60% in a similar survey in May. The economists projected UK economy to growth 1.4% in 2018, better than May projection of 1.3%, after some positive economic data. Inflation forecast was unchanged at 2.5% yoy in 2018 and 2.1% yoy in 2019.

One side note to mention is that McCafferty will end his term on August 31. He will be replaced by Jonathan Haskel, an professor of economics at Imperial College Business School. At this point, it's unsure how the replace with reshape the MPC.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3125; (P) 1.3199; (R1) 1.3249; More...

Intraday bias in GBP/USD remains on the downside for the moment. Decline from 1.4376 is in progress. Sustained break of 50% retracement of 1.1946 to 1.4376 at 1.3161 will pave the way to 61.8% retracement at 1.2875 next. On the upside, break of 1.3471 resistance is now needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4177). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 55 day EMA (now at 1.3527) holds, even in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BOJ Minutes | ||||

| 00:30 | AUD | Westpac Leading Index M/M May | -0.20% | 0.20% | ||

| 06:00 | EUR | German PPI Y/Y May | 0.30% | 2.00% | ||

| 06:00 | EUR | German PPI M/M May | 2.50% | 0.50% | ||

| 10:00 | GBP | CBI Trends Total Orders Jun | 1 | -3 | ||

| 12:30 | USD | Current Account Balance Q1 | -129B | -128B | ||

| 14:00 | USD | Existing Home Sales May | 5.55M | 5.46M | ||

| 14:30 | USD | Crude Oil Inventories | -4.1M |

Asian business sentiments deteriorated on trade war risks

Sentiments of Asian Business deteriorated in Q2 according to a survey by Thomson Reuters and INSEAD, over June 1-15. The sentiment index, representing six-month outlook from 61 firms, dropped -5pts to 74 in Q2. It hit a seven-year high of 79 in Q1. That's also the first decline since September 2017 even though reading above 50 still indicates a positive outlook.

Antonio Fatas, a Singapore-based economics professor at global business school INSEAD, said in the released that "Trade war is not a risk but a reality." He added that "U.S. tariffs are going up against China but also against some of its traditional allies, such as Canada and the European Union. They are all about to retaliate and today we do not see an easy way out." Fatas also said "companies can try to go around tariffs by moving production to other countries, this is costly and inefficient. It is a short-term solution but not optimal."

Among responses, worries of global trade war, higher interest rates, rising oil/commodity prices and foreign exchange fluctuation are see as the biggest perceived risks to business outlook.

China vows to fight as concessions will not appease Trump’s blood lust

China stepped up its rhetoric against US threat of tariffs through an English editorial in the official China Daily. There it warned that "faced with this heightened intimidation from the US, China has no choice but to fight back with targeted and direct measures aimed at persuading the US to back off, since it appears that any concessions it makes will not appease the Trump administration, which wants to suck the lifeblood from the Chinese economy."

And, "Beijing will have to ensure that Washington is aware that there will be heavy price to pay every action it strikes against China if it is to avoid being a victim of the Trump administration's growing blood lust." "Those US companies and workers that feel the brunt of China's retaliation should pass the word to Washington, that despite the pronounced aim of the Trump administration being to protect domestic industries and workers, the injuries that will be done them will be because of its actions."

On other hand, White House trade adviser Peter Navarro warned China "may have underestimated the strong resolve of President Donald J. Trump." And, "if they thought that they could buy us off cheap with a few extra products sold and allow them to continue to steal our intellectual property and crown jewels, that was a miscalculation."

US Companies Doomed to Suffer from Trump’s Protectionist Policy

US-China trade tensions intensified shortly after Trump-Kim Summit. Last Friday (Jun 15), the White House announced that it would impose 25% tariffs on a list of Chinese exports worth of US$34B, effective on 6 July, with another list of goods, covering US$ 16B under further review. In response, China indicated that it would impose 25% tariffs on US$34B worth of US goods, including agricultural products and autos, also effective on July 6, while the second set of US$ 16B will be implemented later (depending on US’ timetable). China’s move is obviously retaliatory and comes in accordance to its “equal scale, equal intensity” approach. Things aggravated as Trump announced yesterday that he would go further to impose 10% tariff on US$ 200B worth of Chinese exports to the US, adding that an additional US$ 200B would be taxed if China retaliates again. In response, China’s Ministry of Commerce pledged that it would “retaliate with "comprehensive quantitative and qualitative measures" if the US imposes more tariffs. Recent developments suggest that the chance of deeper trade conflict between the two biggest world economies has increased. While the US’ assertiveness reveals its belief that China would be the one who suffers more, this assessment appears superficial and reveals the lack of considerations on services trade and non-tariff measures that China could take to retaliate.

Let’s take a look at the details of US’ two sets of tariffs. According to the statement released in the USTR office, the tariff announced on June 15 covers over 1000 types of products, targeting “industrially significant technologies, including those related to China’s “Made in China 2025” industrial policy”. USTR indicated that the moves are “strong defensive actions to protect America’s leadership in technology and innovation against the unprecedented threat posed by China’s theft of our intellectual property, the forced transfer of American technology, and its cyber attacks on our computer networks. The tariff announced earlier this week is a follow up to China’s retaliation. As Trump suggested, China’s “reciprocal” tariff reflects the “determination to keep the US at a permanent and unfair disadvantage”. He believes that “further action must be taken to encourage China to change its unfair practices, open its market to US goods, and accept a more balanced trade relationship with the US”.

Previously, we had anticipated that trade tariffs proposed by both sides are bargaining chips for negotiations. However, failure to proceed to a concrete deal despite China’s promise to increase purchases of US agricultural and energy products (June 2-3) and Trump’s abrupt hardening of stance shortly after the Trump-Kim summit signal that it is increasingly possible that both the US and China could implement the protectionist measures in full. Both sides would suffer in such scenario. It is estimated that both sets of US tariffs (25% on US$ 50B of Chinese goods+10% on US$ 200B of Chinese goods), if fully implemented, would result in 0.2- 0.3 percentage point reduction in China’s GDP growth.

US’ assertive stance is based on the belief that China would suffer more on trade tariffs and this can pressure China to make concessions. However, this belief reveals that the US only focuses on “exports of goods”, while neglecting “exports of services” and non-tariff policies. According to Citigroup’s estimates, about 37% of Chinese goods exports to the US are consumer goods. While Chinese goods exports to the US is over three times bigger than US goods exports to China, this gap narrows by about 60% after taking into account US’ services exports the domestic value added of US exports to China. It is also estimated that about 3.8% of the value-added in China’s manufactured goods exports to the US comes from the US itself. That is, the negative impacts on the US resulting from the tariff imposed by itself could be much higher than initially anticipated.

Meanwhile, besides tariffs, China could impose non-tariff and regulatory measures, such as targeting US companies through regulatory policies, if US continues to escalate. The outcome could be significant since, according to 2016 data, US’ foreign direct investment (FDI) in China is more than two times that China’s FDI in the US.

| Date | US action | China action |

| 22-Mar | Announced intention to impose tariffs on US$ 50-60B of Chinese exports | |

| 4-Apr | Released a list of about US$ 50B of Chinese goods targeted for 25% tariffs | Announced it would impose 25% tariffs on US$ 50B of US exports to China, including soybean, aircraft, and autos |

| 6-Apr | President Trump ordered USTR to consider tariffs on an additional of USD100bn worth of Chinese imports | |

| 10-Apr | Xi pledged further open-up, and called for peace and cooperation through dialogue | |

| 3-4 May | 7-member US delegation visited Beijing | |

| 15-19 May | Chinese delegation (led by Liu He) visited the US: joint statement released, agreeing to “substantially reduce US trade deficit with China” with tariffs are on hold | |

| 29-May | Announced that a final list of US$ 50B of Chinese exports subject to tariffs would be published by June 15 | |

| 2-3 Jun | US Commerce Secretary Wilbur Ross went to China: China agreed to buy more US agricultural and energy products, no deal reached | |

| 15-Jun | Announced 25% additional tariffs on a list of Chinese goods, worth of of US$ 34B (effective on 6 July), another list covering US$ 16B would follow | Announced tariffs to match with the US |

BoE to stand pat tomorrow, August hike uncertain

BoE will most likely keep the Bank Rate unchanged at 0.50% tomorrow. Known hawks Ian McCafferty and Michael Saunders are expected to vote for rate hike while others would vote for standing pat. There will be no inflation report but just the meeting minutes. And attention will on whether the minutes give any hint on an August hike.

According to the latest Bloomberg survey, only 55% of respondents forecast a hike in August. That's even down from 60% in a similar survey in May. The economists projected UK economy to growth 1.4% in 2018, better than May projection of 1.3%, after some positive economic data. Inflation forecast was unchanged at 2.5% yoy in 2018 and 2.1% yoy in 2019.

One side note to mention is that McCafferty will end his term on August 31. He will be replaced by Jonathan Haskel, an professor of economics at Imperial College Business School. At this point, it's unsure how the replace with reshape the MPC.

Market Morning Briefing: Dollar Yen Saw A Low Near 109.55

STOCKS

Dow (24700.21, -1.15%) has broken below the daily trendline support near 24750 and has opened up scope of falling further towards 24000-23600 levels in the coming sessions. Unless we see an immediate bounce back above 24750, view for the medium term remains bearish.

Dax (12677.97, -1.22%) tested 12600 on the downside as expected. If 12700 acts as an earlier support turned resistance, the Dax could fall further towards 12400. Else we could see a bounce from current levels back towards 12800-12900 levels.

Nikkei (22287.42, +0.040%) has fallen as expected and looks further bearish towards 21800.

Shanghai (2881.21, -0.92%) is down sharply on tensions over US-China Trade relations and the index could test levels near 2800-2750 which could provide some near term support.

Nifty (10710.45, -0.83%) is likely to get some support from 10700-10650 levels. Near term looks bearish just now but the downside could be capped at 10650.

COMMODITIES

Brent (75.30) and WTI (65.09) are stable just now. WTI could be stable in the 67-64 region for now while Brent is likely to trade below resistance at 76. The next couple of sessions could see some range-trade.

Gold (1276.30) has immediate support on the 3-day charts. If this holds, we may see a bounce towards 1300 else indication of medium term bearishness may be triggered on a fall below 1270 opening up chances of testing 1250-1240 levels soon.

Copper (3.0455) has also come off as expected losing all the gains seen last week. 3.02-3.00 could be an immediate support where a pause is likely just now. Keep an eye on the falling Shanghai and Aussie as that could keep Copper weak for the coming sessions.

FOREX

Euro (1.1584): Against our expectation, Euro fell yesterday and for the first time, dipped below crucial support on weekly candles near 1.156 to see a low near 1.153. Euro could now break decisively below this support in this week. In that case, its next downside target would be 1.145 (89 weeks MA).

Dollar Index (95.02): Dollar strengthened against most global currencies yesterday (except the Yen) and the Dollar Index saw an 11 month high near 95.30. It could now move further up towards resistance near 95.5-95.6 on the 3 day line chart and even breach that to target 96 in this week.

Dollar Yen (110.14): Dollar Yen saw a low near 109.55 yesterday but has again moved up from there. As mentioned yesterday, it could continue to see oscillation between 111.0-109.5 in this week and then break below support on daily candles (near 109.5-110.0) ultimately, which could make it bearish towards 107 in the medium term.

Euro Yen (127.58): With chances of bearishness in both Euro and Dollar Yen, Euro Yen is likely to break horizontal support on weekly line chart near 127.0 in this week / by next week. Its target in the next 2-3 weeks could well be support on weekly candles near 124.

Pound (1.3166): As per expectation, Pound moved lower towards 1.31 yesterday, seeing a low near 1.3151. A test of support on 3 day candles near 1.31 in this week and then a further downmove towards 1.30 in the next 1-2 weeks seems likely.

Dollar Rupee (68.385): Crucial resistance level near 68.50 could be tested in the coming sessions. A break beyond that could translate into an upmove towards upside target of 69.

INTEREST RATES

US-China trade war prospects are rising after Trump signalled that tariffs might be imposed on $200 billion worth of Chinese imports. Risk aversion seems to be setting in, channeling funds into debt and taking yields lower.

German 10 year yield (0.373%) has broken support near 0.4% on short term chart and could now move lower towards support near 0.3% on the medium term chart.

US 10 year (2.89%), 30 Year (3.0244%), 5 Year (2.77%), 2 Year (2.545%): US 10 Year yield dropped to levels near 2.87%-2.88% yesterday and has risen slightly from there. However it still continues to stay below support near 2.9% on medium term chart. As mentioned before, if this break sustains, it could lead to a further downmove towards 2.60% in the medium term.

US Yield curve inversion fears are gripping the bond markets. The less talked about US 10-7 Year spread is near 0.04% and could possibly invert ie go negative soon. In the past, it has been a precursor to more important spreads ie (10-5 and 10-2) inverting. The 10-2 Year spread had broken long term support near 0.4% in the last few days and is currently near 0.345%

BoJ minutes: Timing of reaching inflation target was merely a projection

BoJ released minutes of the April 26-27 meeting today. The only surprise out of that meeting was that BoJ dropped the time frame it set for achieving the 2% inflation target. The minutes provided more details on the discussions. Many members believed that the timing of reaching the 2% inflation was "merely a projection". At the some time, "some market participants perceived this projection as a deadline for achieving 2 percent inflation, linking changes in said timing to policy adjustments, and this view was deeply entrenched among them."

Some members expressed that "attracting excessive attention merely to forecast figures would not be appropriate from the perspective of communication with the markets". And, most members expressed that " it was appropriate to cease providing a description on the projected timing of achieving the price stability target". And that was with the aim to clarify that the timing was "not a specific deadline" for meeting inflation target. Nonetheless, one member expressed the concern that dropping the time frame could "weaken the effects of the commitment" of BoJ to hit target.