Sample Category Title

Gold Price Broke Key Support, Turned Bearish

Key Highlights

- Gold price failed to hold a major support near $1,285 and declined against the US Dollar.

- There was a break below a major bullish trend line with support at $1,296 on the 4-hours chart of XAU/USD.

- The US Housing Starts in May 2018 increased 5%, more than the forecast of +1.4%.

- Today, the US Existing Home Sales figure for May 2018 will be released, which is forecasted to grow by 1.5% (MoM).

Gold Price Technical Analysis

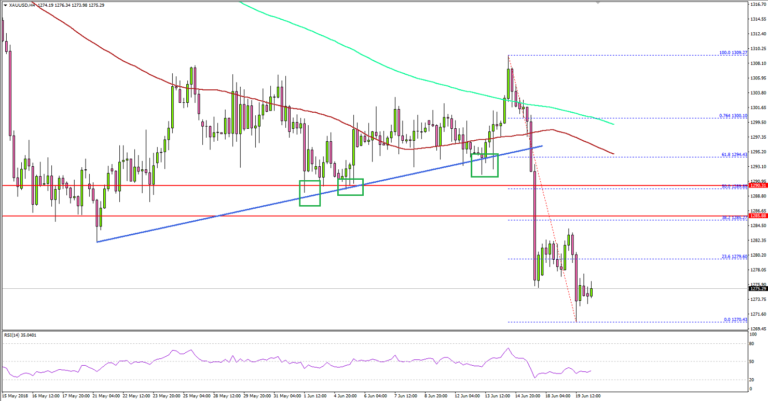

After trading above the $1,300 level, gold price failed to hold gains against the US Dollar. The price started a downside move and broke a few major supports including $1,295.

A high was formed at $1,309 before the price started a bearish wave. It declined below $1,300 and closed below the 100 simple moving average (red, 4-hour). During the decline, there was a break below a major bullish trend line with support at $1,296 on the 4-hours chart of XAU/USD.

More importantly, the price broke two key supports at $1,290 and $1,285, opening the doors for more losses. The price traded close to the $1,270 level and is currently consolidating losses.

On the upside, an initial resistance is near the 23.6% Fib retracement level of the last decline from the $1,309 high to $1,270 low. However, the most important hurdle is near $1,285, which was a support earlier and now coincides with the 50% Fib retracement level of the last decline from the $1,309 high to $1,270 low.

Therefore, if the price corrects higher, it is likely to face sellers near $1,285. On the downside, supports are seen near $1,270 and $1,266.

Recently, the US saw the release of the Housing Starts report for May 2018 by the US Census Bureau, at the Department of Commerce. The market was looking for a rise of 1.4% compared with the previous decline of 3.7%.

However, the result was positive as there was a rise of 5% in the Housing Starts. The last reading was also revised down to -3.1%. The report added:

Single-family housing starts in May were at a rate of 936,000; this is 3.9 percent (±10.6 percent)* above the revised April figure of 901,000. The May rate for units in buildings with five units or more was 404,000.

Overall, the US Dollar may continue to gain momentum. EUR/USD recently dipped and traded towards 1.1550, and GBP/USD also fell sharply below the 1.3200 support.

Economic Releases to Watch Today

- US Current Account Q1 2018 – Forecast $-129.0B, versus $-128.2B previous.

- US Existing Home Sales for May 2018 (MoM) – Forecast +1.5%, versus -2.5% previous.

The Winds Of A Trade War Are Howling

The winds of a trade war are howling

The winds of a trade war are howling as a tariff -induced polar vortex has frozen out investors dead in their tracks. It’s been an intense 24 hours of attrition which has seen many a savvy investor fold like a cheap deck of card, but for those that survived the carnage, the spoils of war may be there for the taking or more likely the fading.

Investors complacency has given way to sheer terror as there can be very little doubt that the US and China have locked horns in a legitimate trade war as battle lines get drawn, and investors hunker down with safe havens preparing to ride this one out.

Oil Market

Oil naturally was another major focal point as Saudi – Russia alliance continues to double down pushing for much more massive 1.5 mil production hike against a generally more OPEC pleasant hike of 300-500 K barrels. Of course, much of this could be little more than posturing designed to influence members to take a consensual step to 700 K barrels increase.

And indeed, trade war escalation has been a significant distraction while putting a more offered tone to the market on global growth concerns and adding another unwanted layer of uncertainty.

But the fine-tuning approach makes so much more sense not only from a producer perspective but would also reduce the chances of making a significant policy error during these unsettled times. Indeed, lots of moving parts.

Gold

Gold remains bearishly offered, and It’s all about the dollar strength as the greenback rockets higher on EM commodity and the China meltdown. And at least for the time being the markets have utterly forsaken the idea that the US trade war escalation could become ultimately detrimental for the dollar. But it’s the enormity of the EMFX meltdown that has investors chasing the dollar buck as capital outflows into the haven US treasuries is the flavour of the day.

Predictably with the move to 1275, retail buying interest has started to wane, but all eyes remained on currency markets and the Euro after Mario Draghi all but reaffirmed the ECB’s dovish stance as currency voles have switched into panic mode.

Gold will continue to be sold on rallies in this bullish USD environment.

Currency Markets

Very thematic !!!!

EUR: Under pressure from Draghi confirming ECB dovishness

AUD: Metals have been stricken by trade tensions, causing consternation on virtually every commodity desk. AS such the Aussie will remain under pressure as flow blow trade war looms

JPY: Market continues to buy dollar elsewhere given the overhang from political risk

Asia FX: the winds of a US-China trade war are howling and as storm clouds brew investors are running for the umbrella of haven assets.

The regional sentiment is an enormous risk- off, and local stock market toppled on global growth concerns. Look no further than USDCNH touching 4.48 as capital outflows intensify. And look no farther than the melt on the Shanghai composite to support that view.

MYR: only weakened slightly above 4.00. Despite uncertainty over the fiscal deficit. The MYR is better insulated from external trade shocks than regional peers due to oil But should continue to trade with a negative bias as regional sentiment continues to wane.

Keep in mind the MYR had weakened dramatically on the post-election outflows, so the Ringgit is not suffering from the unwinding of short dollar risk as some of the regional peers as positioning is much cleaner and slightly long biased.

I think this partially explains why the MYR has held up relatively well today, considering all the regional negatives.

Eco Data 6/20/18

[php_everywhere instance="1"]

US to announce withdrawal from UN human rights council

Reuters reported the U.S. Secretary of State Mike Pompeo and U.S. Ambassador to the United Nations Nikki Haley will announce to withdraw from United Nations Human Rights Council today. That would be another isolationist move by the US in rejection of multilateral engagements.

The US had history of boycotting the council for three years under George W. Bush, then rejoined under Barrack Obama in 2009.

Haley has been calling for reform and elimination of a "chronic anti-Israel bias" but the progress is seen as dissatisfactory.

Gold Drops to 2018 Low as Trade War Fears Boost Greenback

Gold is under pressure in the Tuesday session. In North American trade, the spot price for one ounce of gold is $1275.69, down 0.22% on the day. Earlier in the day, gold dropped to $1270, its lowest level since December. On the release front, construction indicators were a mix. Building Permits dropped to 1.30 million, shy of the estimate of 1.35 million. This marked a 3-month low. Housing Starts improved to 1.35 million, beating the estimate of 1.31 million. On Wednesday, Federal Reserve Chair Jerome Powell will participate in a panel at the European Forum in Sintra, Portugal. The U.S will release Existing Home Sales.

In times of crisis, nervous investors often turn to gold, a safe-haven asset. However, since the start of the new round of tit-for tat tariffs between China and the U.S began on Friday, gold has defied expectations and lost ground. The base metal has declined 1.9% since Friday. The U.S dollar has posted broad gains against other major currencies and has also moved higher against gold.

President Trump has raised the stakes in the escalating trade spat between the world’s two largest economies. After China said it would match the U.S move to slap tariffs on $50 billion in Chinese goods, Trump sent shock waves across global markets on Tuesday, threatening to impose 10 percent tariffs on some $200 billion in Chinese goods. Not surprisingly, China has threatened to retaliate against this latest move. Trump has vowed to take action on the $375 billion trade deficit that the U.S has with China, claiming that the latter is guilty of unfair trade practices. With the first of the U.S tariffs scheduled to take effect on July 6 and no signs that either side will blink first, there is a real danger of a global trade war, which could end up as lose-lose situation for both China and the United States.

Pound Slips to 7-Month Low as Trade Tensions Boost US Dollar

The British pound has posted losses in the Tuesday session. In North American trade, GBP/USD is trading at 1.3173, down 0.55% on the day. On the release front, there are no British releases. In the US, construction data was mixed. Building Permits dropped to 1.30 million, shy of the estimate of 1.35 million. This marked a 3-month low. Housing Starts improved to 1.35 million, beating the estimate of 1.31 million. On Wednesday, Federal Reserve Chair Jerome Powell will participate in a panel at the European Forum in Sintra, Portugal. The U.S will release Existing Home Sales.

Are we heading for a global trade war? Investors are nervous, and this sentiment has boosted the U.S dollar on Tuesday. The British pound is having a rough week and is currently trading at its lowest level since early November. The most recent round of the trade spat between China and the U.S started on Friday, when the U.S announced a 25 percent tariff on $50 billion in Chinese goods. After China responded with an identical move on U.S. imports, President Trump has now threatened to impose 10 percent tariffs on some $200 billion in Chinese goods. Not surprisingly, China has threatened to retaliate against this latest move. Trump has vowed to take action on the $375 billion trade deficit that the U.S has with China, claiming that the latter is guilty of unfair trade practices. With the first of the U.S tariffs scheduled to take effect on July 6 and no signs that either side will blink first, the pound could continue to lose ground.

The Brexit talks remain stalled, as the European Union and the U.K remain far apart on a number of key issues. The Europeans are in no mood to play nice with the U.K and are exasperated by the lack of direction from the May government. Key issues remain the Irish border, the role of the European Court of Justice on EU citizens living in Britain, and the nature of trade relations between Britain and EU members in the post-Brexit era. Both sides are preparing for the possibility that a deal will not be reached by March 2019. The scenario of a ‘hard Brexit’ could sour investor sentiment towards the U.K and put pressure on the struggling British pound.

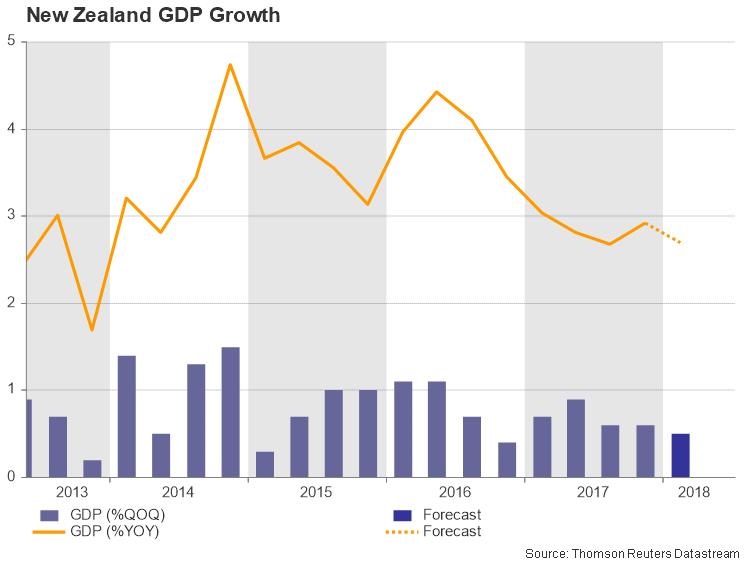

New Zealand GDP Predicted to Expand in Slower Pace While Kiwi Stalls Near $0.70

New Zealand will publish GDP figures on Thursday (Wednesday 2245 GMT) for the first quarter. Investors will be cautious for any clues as to whether the Reserve Bank of New Zealand (RBNZ) will raise or decrease interest rates. Economic growth is expected to have slowed down further in the first quarter of 2018.

Analysts are estimating New Zealand’s economy grew by just 0.5% in the three months to the end of March, easing slightly from the previous two quarters of 0.6%. On an annual basis, GDP is expected to have expanded by 2.7% versus 2.9% in the preceding period. The data are unlikely to change the RBNZ’s view and a more disappointing release would endorse the scenario for another cut in rates rather than an increase for the near future.

Turning to monetary policy, the central bank kept its official cash rate unchanged at a record low of 1.75% on May 10, as widely expected. The last change in key rate was in November 2016. Policymakers highlighted that inflation remains below the 2% mid-point of the target due to recent low food and import price inflation, as well as subdued wage pressures. Meanwhile, inflation advanced by 1.1% y/y in the first three months of this year versus a 1.6% y/y increase in the previous quarter, matching market expectations. This figure was the slowest since the third quarter of 2016. It is worth mentioning that the unemployment rate ticked lower to 4.4% in Q1 from 4.5% before. This was the fifth consecutive quarter the unemployment rate has fallen and was the lowest number since the last quarter of 2008.

On the political front, US President Donald Trump’s trade war could have a negative effect on New Zealand and its currency. Trump has put a hefty tariff on Chinese imports and China has retaliated by imposing tariffs of their own. The country is already seeing impacts from the steel and aluminum exports, where tariffs were brought in earlier in 2018. The New Zealand dollar is moving sharply lower and could fall even more in case of worse-than-expected data.

From the technical point of view, kiwi/dollar has slipped more than 2% since last week, recording a fresh three-week low of 0.6883. The strong sell-off rally started after the pullback on the 0.7050 resistance level, while the moving averages are following the bearish structure in the short-term.

If GDP numbers surpass the consensus then the expectation is a run until the 20-SMA near 0.6940 at the time of writing. A break above the aforementioned obstacle could open the door towards the next barrier of 0.6955 taken from the significant top on June 18.

A worse-than-expected figure could continue the downward pressure for the pair and would retest the latest low of 0.6881. Further losses could drive kiwi/dollar until the 0.6870 support before being able to re-challenge the 0.6850 region. In case of steeper decreases, the next support to have in mind is the 0.6820 barrier, taken from December 8 low.

The Aussie is Falling: Investors are Getting Away From Risks

The Australian Dollar is under pressure against the USD due to the market situation. On Tuesday afternoon, the Aussie is getting weaker mostly because investors are choosing “safe haven” assets, such as the USD and the Yen, in order to avoid risks.

At the time when everybody is running away from Chinese-American “trade wars” risks, it can be quite clearly seen that the demand for “safe haven” assets in significantly increasing. In this light, one may expect the Australian Dollar to continue trading downwards, at least until the balance of power on the market changes.

The Monetary Policy Meeting Minutes report published by Australia today says that the expensive national currency prevents the country’s economy and the Consumer Price Index from growing. Now, when the Australian Dollar is under pressure, the Australian GDP may boost a little bit. The report also says that the areas that require greater attention are still the labor market and the inflation. Expectations for the GDP growth are 3% while the inflation target remains at 2%.

A special focus in the RBA Minutes is put of “trade wars” risks. The regulator believes that the current tariff adjustment in world commerce implies many risks and may force the global economy to slow down. In the present context, such comments may be very essential, because the USA and China don’t seem to stop fighting without outside interference.

In general, the Australian Dollar would feel more stable and confident, if there weren’t so many emotions on the market right now.

Since the “market crowd” is usually driven by emotions instead of the common sense, one can see that the technical picture of AUDUSD is still showing the downtrend. If one takes a look at the previous correction to the upside, it can be seen that after breaking the support line, the pair has formed a new descending impulse and reached the projected support line. While forming the impulse to the downside, the instrument is moving towards the long-term fractal low at 0.7328. After breaking it, the price may test the support line of the long-term channel at 0.7275. This is exactly the area, which the price may rebound from.

Sunset Market Commentary

Markets:

Rising oil prices and the de-escalation of the CDU/CSU rift dropped from the equation which kept core bonds in balance yesterday, leaving the new tit-for-tat threats in the US/Chinese trade row as the only factor influencing trading. Core bonds profited from global risk aversion. The main move occurred overnight (US Note future) or in the European opening (Bund). Both entered a more sideways pattern afterward. The ECB Sintra conference featured plenty ECB governors, including chairman Draghi. They all kept last week’s dovish line on policy rates. Draghi explicitly mentioned that current market expectations about a first rate hike, which is towards the end of Q4 2019, broadly reflect the ECB’s principles. Today’s eco calendar only contained second tier data with mixed US housing figures. The German yield curve bull flattens with yields 0.8 bps (2-yr) to 4.9 bps (30-yr) lower. Changes on the US yield curve vary between -1.7 bps (2-yr) and -2.6 bps (10-yr). 10-yr yield spread changes vs Germany widen up to 2 bps with Italy (+7 bps) underperforming.

EUR/USD. Global trade tensions were the main driver for global FX. Over the previous days, the impact of the enfolding trade war was mostly limited to a risk-off sentiment on equity markets. However, this time global FX was also affected. Global yen buying triggered a ‘classic’ risk off repositioning. USD/JPY selling in Asia was followed by a substantial decline in EUR/JPY and EUR/USD during the European trading session. EUR/JPY dropped (temporary?) below the 127 mark and EUR/USD fell to the 1.1530/35 area. Euro selling was reinforced by soft ECB speak from the ECB conference in Sintra. ECB’s Draghi said the Bank will be patient in the timing of the first rate hike. Other governors even indicated that the first rate hike could be later than September 2019. So, the euro indeed won’t receive interest rate support anytime soon. Risk sentiment eased slightly after US equity market opening. EUR/USD is trading off the intraday lows (1.1560 area) and so is USD/JPY (110 area). Even so, the trade-weighted dollar set a new 2018 top north of 95 today. The risk-off modus also infected the likes of the CAD and the Aussie dollar. Smaller currencies on boundaries of euro zone (SEK, PLN, CZK, to a lesser extent NOK) all lost ground, not only against the dollar, but also against the single currency. Lower liquidity often weighs on those currencies in a risk-off context. Maybe markets also delay rate hike expectations for most of those central banks in the wake of recent ECB guidance.

GBP. Sterling trading was still driven both by global uncertainty on trade factors and by the ongoing debate on the ‘Meaningful vote amendment’ that will be return to the House of Commons for a new vote tomorrow. The rift between the UK government and the pro-Bexit members of the Conservative Party persists. Both factors were a tentative sterling negative. Sterling struggled not to lose further ground against the euro even as EUR/USD was also under pressure. Cable dropped below the 1.32 level, reaching the lowest level since November last year. The low 1.30 support area is coming within reach.

News Headlines:

Hungary's central bank kept its policy rate unchanged at 0.90%, but dropped a reference to maintaining the base rate and loose monetary conditions "for an extended period" as the current easy conditions were not sustainable through its policy horizon. "In the Monetary Council's view, the current loose monetary conditions can no longer prevail up to the end of the 5 to 8-quarter horizon of monetary policy. In the Council's assessment, the international environment is changing. We are nearing the end of a period of ample liquidity and persistently low interest rates, seen in previous years.". The forint strengthened away from historically low levels with EUR/HUF dropping from 325 to 321.50.

EU to pursh for WTO reforms at upcoming summit

According to a draft statement prepared for the June 28-29 EU summit, European leaders are ready for retaliation against US steel and aluminum tariffs. There is also an initiative to push for reforms in the WTO to preserve and deepen rules-based multilateral global trade system.

The draft reiterated EU's stance that US steel and aluminum tariffs "cannot be justified on the grounds of national security." And, the European Council "fully supports the re-balancing measures, potential safeguard measures to protect our own markets, and the legal proceedings at the WTO." Initial retaliation include 25% duty on EUR 2.8B US imports including motor cycles, jeans and whiskies.

Regarding WTO, the draft said "in a context of growing trade tensions, the European Council underlines the importance of preserving and deepening the rules-based multilateral system." And, "it invites the commission to propose a comprehensive approach to improving, together with like-minded partners, the functioning of the WTO in crucial areas such as more flexible negotiations, new rules that address current gaps, including in the field of subsidies, reduction of trade costs, a new approach to development and effective and transparent enforcement, with a view to ensuring a level playing field."