Sample Category Title

GBP/USD Bearish Momentum Breaks 1.32 Support Zone

The GBP/USD broke below the support trend line (dotted green) after building a triangle chart pattern. Price also breached the critical round level of 1.32 for a continuation of the downtrend.

The GBP/USD is showing strong bearish price action and could be ready for a continuation towards the next round level at 1.30.

The GBP/USD is building a small consolidation after a bearish breakout, which could be part of a bearish wave 5.

USD/JPY Retraces Back To Critical Resistance Zone

The USD/JPY is building a bullish retracement back to the resistance trend lines and Fibonacci levels of wave B, which are key bounce or break zones.

The USD/JPY could make a bearish turn at the resistance zone if the wave patterns play out as expected via a potential wave ABC (blue) within wave Y (purple)

The USD/JPY is building a bullish channel. A break below the channel could indicate the end of the wave B whereas a break above the resistance could make it less likely. A break above the 100% Fib invalidates the ABC.

Market Focus Continues To Be On The US-China Trade Spat

Market movers today

We have published our Nordic Outlook with updated economic forecasts for the Nordic countries this morning. We expect Swedish growth to slow this year as it is no longer fuelled by housing, Norwegian growth to accelerate supported by oil investments, Danish growth to cruise along and Finland to slow down only a little after a very good run.

Market focus continues to be on the US-China trade spat. We have now entered what we would call a trade war as the t it -for-tat react ions are escalating, see US-China trade trade war becomes a reality as Trump pushes further, 19 June 2018. The next key dates to watch out for are 30 June (when Trump announces restrictions on Chinese investments into the US and export controls on US tech products to China) and 6 July (when Chinese tariffs on US begins, and Trump has said it will lead to further tariffs on Chinese products worth USD200bn).

It will be an interesting day at the ECB Sintra conference, with the key event being the panel at 15:30 CEST, which includes ECB President Mario Draghi, Fed Chairman Jerome Powell and Bank of Japan Governor Haruhiko Kuroda. See programme here.

Yesterday, we published an update on the political situation in Italy. See more here. Currently, no news on fiscal policy is good news for the Italian government bond market. However, we are st ill reluctant to go long BTPS and much prefer to be long Spain and Portugal.

Selected market news

There has been some stabilisation in the Asian equity markets despite the trade wars between US and China escalating. There were some small gains in the European government bond market yesterday on the back of the trade war between the US and China and more ECB comments from the conference in Sintra, Portugal.

There will be some more speeches from Sintra today, but we do not expect them to have much impact on markets. Furthermore, the focus on the inversion of the US yield curve continues to be strong. Next week, the US Treasury department is due to hold an auction in the 7Y segment , which could add to the pressure on the yield curve.

Renewed Talk That China Will Cut RRR

General Trend:

- Asian equity markets trade generally higher following declines on Tuesday; Shanghai continues to lag

- Chinese telecom ZTE rises over 10% (first gain in 5 sessions)

- Australia ASX 200 index outperforms and trades at highest level since early 2008; Financials and Utilities gain

- Australian telecom Telstra declines over 5%, announced job cuts and FY19 targets

- Philippines Central Bank expected to raise rates later today for the 2nd straight meeting; Thailand expected to leave rates unchanged

- New Zealand Q1 GDP figures due for release on Thursday, Debt agency to sell April 2037 bonds

Headlines/Economic Data

Japan

- Nikkei 225 opened +0.3%

- TOPIX Info & Communications index +0.4%, Securities +0.1%; Marine Transportation -1.9%, Iron & Steel -1.9%

- Japanese megabanks trade generally lower

- (JP) Japan FSA expected to take administrative action this week on some registered cryptocurrency exchange operators in Japan, including industry leader bitFlyer Inc - Japan press

- (JP) Bank of Japan (BoJ) April 26-27th Policy Meeting Minutes (2 meetings ago): Many agreed as there was still a long way to go to achieve the price stability target of 2%, it was necessary to maintain the current highly accommodative financial conditions

- (JP) Japan to extend current Diet session to July 22nd from today (as speculated)

Korea

- Kospi opened +0.4%

- SK Telecom, 017670.KR Separates 11Street from SK Planet in a move to catch up with Amazon - Korean press

- (KR) North Korea KCNA: Leader Kim Jong Un and China's Xi exchanged opinions; had understanding on issues including denuclearization of the Korean peninsula

- (US) Commerce Dept imposes trade duties on polyester staple fiber from South Korea and Taiwan

- (KR) South Korea crypto currency exchange Bitthumb has been hacked; KRW35B in crypto currency said to have been stolen - South Korean Press

- (KR) South Korea Foreign Min Kang: Sanctions on North Korea to remain until completely denuclearized

- (KR) South Korea Fin Min Kim: To review ruling party request for expansionary fiscal policy - Korean press

China/Hong Kong

- Hang Seng opened 0.0%, Shanghai Composite -0.6%

- Hang Seng Consumer Goods index +1%, Services +0.9%, Info Tech +0.8%, Energy +0.7%; Materials -1.3%

- (CN) China PBOC Gov Yi Gang: Investors should stay calm; confident of capital market development; financial liquidity reasonable, stable (after the close)

- (CN) China Securities Journal: No basis for continuous plunge in A-shares

- (CN) China PBoC Open Market Operation (OMO): Injects CNY100B in 7 and 14 day reverse repos v CNY100B injected in 7, 14 and 28-day reverse repos prior: Net: CNY40B injection v CNY50B injected prior

- (CN) China PBoC sets yuan reference rate at 6.4586 v 6.4235 prior

- (CN) China Banking and Insurance Regulatory Commission (CBIRC): banking and insurance sectors have been performing on solid footing, with risks under control - Xinhua

- 763.HK ZTE: US Commerce Dept official: still working out escrow agreement necessary to lift ZTE ban; it's part of a normal process

Australia/New Zealand

- ASX 200 opened +0.3%

- ASX 200 Financials index +1.8%, REIT +0.9%, Utilities +0.9%, Energy +0.9%; Telecom -4.2%

- Telstra,[-5%], TLS.AU Announces restructuring: To layoff 8.0K employees and contractors; Guides FY19 EBITDA A$8.7-9.6B ex ~A$600M in restructuring costs

- (NZ) New Zealand Q2 Westpac Consumer Confidence: 108.6 v 111.2 prior

- (NZ) New Zealand Q1 BoP Current Account Balance (NZ$): 180M v 50Me; Current Account to GDP Ratio: -2.8% v -2.8%e

- (AU) Australia sells A$700M v A$700M indicated in 2.25% Nov 2022 bonds, avg yield 2.2716% v 2.4172% prior, bid to cover 4.03x v 7.11x prior

- (AU) Australia May Westpac Leading Index m/m: -0.2% v +0.2% prior

- (AU) Australia govt crackdown on foreign property sales seen as a failure; only finding 4.3K not in compliance since 2015 - AFR

Other Asia

- Noble Group, [+50%], NOBL.SG Issues update on financial restructuring plan: Shareholder Goldilocks agreed to discontinue all claims and proceedings on a no-fault basis

- (MY) Malaysia May CPI Y/Y: 1.8% v 1.8%e (3rd straight month of annual pace below target)

North America

- US equity markets ended mostly lower: Dow -1.2%, S&P500 -0.4%, Nasdaq -0.3%, Russell 2000 +0.1%

- S&P500 Industrials -2.1%, Materials -1.8%

- WBA To replace GE in Dow Jones Industrial Average, effective June 26th

- SBUX Cuts FY18 adj EPS $2.39-2.43 v $2.49e (prior $2.48-2.53); Raises Quarterly dividend 20% to $0.36 from $0.30 (indicated yield 2.51%) - Oppenheimer conf comments

- BTC/USD Coinbase CEO: Price dip in bitcoin can be attributed to people being irrationally pessimistic; sees downturns as the perfect time to make progress as a company "while everyone else gets distracted." - press citing talk to new employees

- (US) Weekly API Oil Inventories: Crude: -3M v +0.8M prior

- (US) SEMI: May North America Billings $2.70B (3-month avg basis), +0.6% m/m and +19.2% y/y

Europe

- (EU) ECB's Lane (Ireland): need to see sizable inflation shock to reverse decision to end QE

- (IR) Iran Oil Min Zanganeh: does not think there will be agreement at this OPEC meeting; Iran will not accept even a modest increase in output - comments in Vienna

Levels as of 01:30ET

- Hang Seng +1.3%; Shanghai Composite +0.2%; Kospi +1.3%; Nikkei 225 +1.1%; ASX 200 +1.0%

- Equity Futures: S&P500 +0.3%; Nasdaq100 -0.1%, Dax +0.2%; FTSE100 +0.4%

- EUR 1.1567-1.1596; JPY 109.55-110.57; AUD 0.7369-0.7405;NZD 0.6890-0.6917

- Aug Gold -0.2% at $1,276/oz; Aug Crude Oil -0.7% at $65.25/brl; Jul Copper +0.5% at $3.05/lb

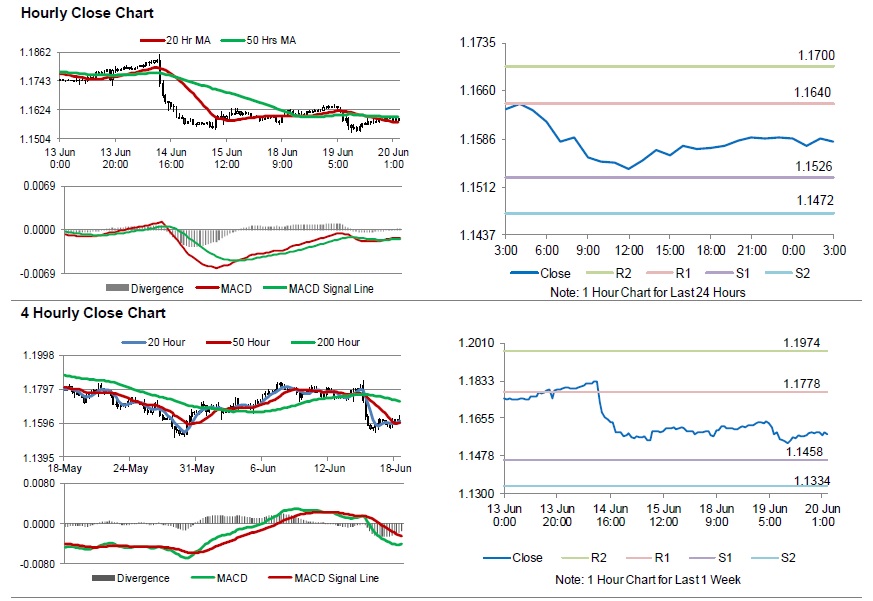

Euro Trading On A Negative Footing This Morning

For the 24 hours to 23:00 GMT, the EUR declined 0.28% against the USD and closed at 1.1589.

On the economic front, Euro-zone's seasonally adjusted current account surplus narrowed more than expected to €28.4 billion in April, compared to a surplus of €32.0 billion in the prior month and marking its lowest level since June 2017. Markets were expecting trade surplus to narrow to £30.3 billion. Meanwhile, the region's seasonally adjusted construction output unexpectedly rose 1.8% on a monthly basis in April, after recording a revised fall of 0.2% in the previous month.

Macroeconomic data released in the US indicated that housing starts jumped 5.0% on a monthly basis, to an annual rate of 1350.0K in May, hitting a 11-year high level and more than market consensus for a rise to a level of 1311.0K. Housing starts had recorded a revised reading of 1286.0K in the previous month. Also, the nation's building permits fell by 4.6% on a monthly basis, to an annual rate of 1301.0K in May, compared to a revised reading of 1364.0 K in the prior month and marking its lowest level since September 2017. Market anticipation was for building permits to fall to a level of 1350.0 K.

In the Asian session, at GMT0300, the pair is trading at 1.1581, with the EUR trading 0.07% lower against the USD from yesterday's close.

The pair is expected to find support at 1.1526, and a fall through could take it to the next support level of 1.1472. The pair is expected to find its first resistance at 1.1640, and a rise through could take it to the next resistance level of 1.1700.

Moving ahead, investors would look forward to Germany's producer price index for May scheduled to release in a few hours. Moreover, the US MBA mortgage applications followed by existing homes sales data for May, set to release later in the day, will be on investors' radar. The currency pair is trading above its 20 Hr and showing convergence with its 50 Hr moving average.

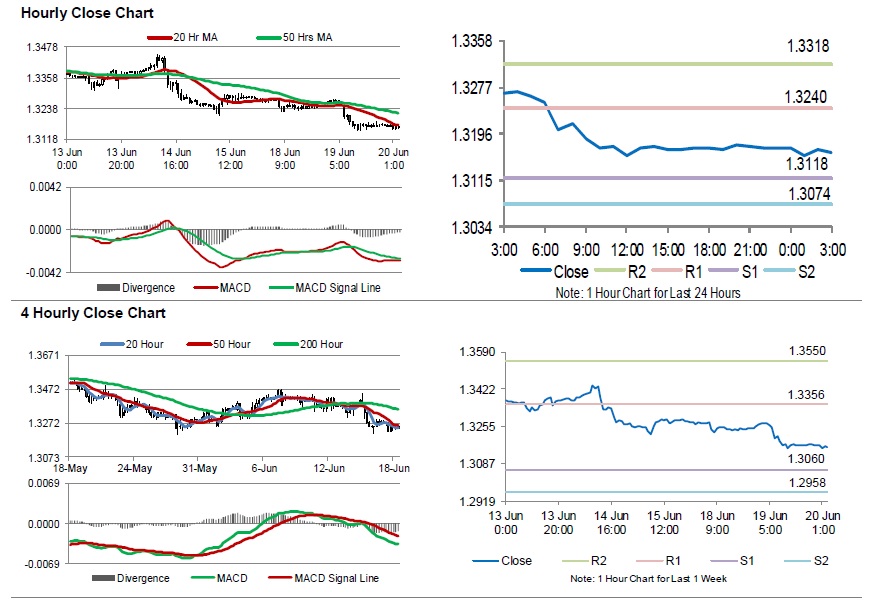

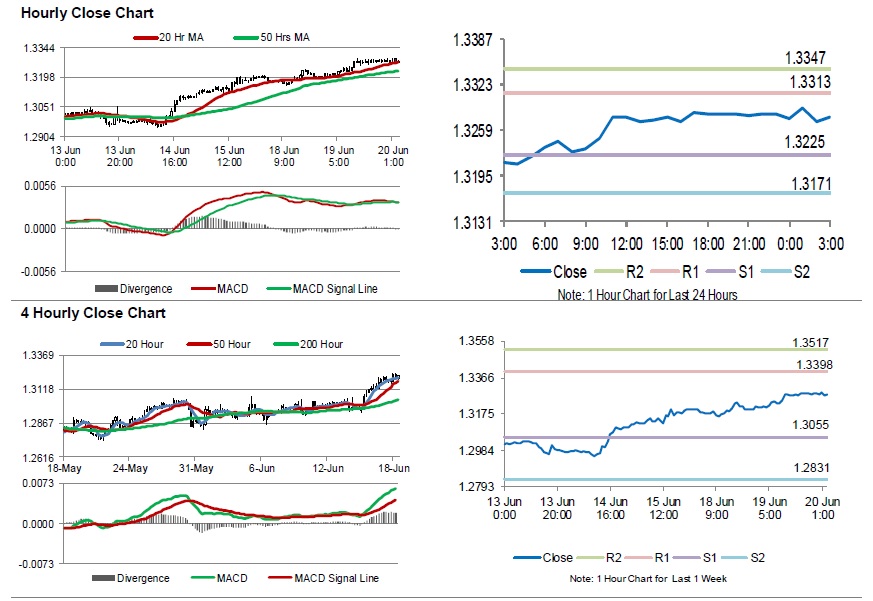

Sterling Extends Its Losses In The Morning Session

For the 24 hours to 23:00 GMT, the GBP declined 0.56% against the USD and closed at 1.3172.

In the Asian session, at GMT0300, the pair is trading at 1.3163, with the GBP trading 0.07% lower against the USD from yesterday’s close.

The pair is expected to find support at 1.3118, and a fall through could take it to the next support level of 1.3074. The pair is expected to find its first resistance at 1.3240, and a rise through could take it to the next resistance level of 1.3318.

Going ahead, investors would await the UK’s CBI total trends orders for June, scheduled to release in a few hours.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

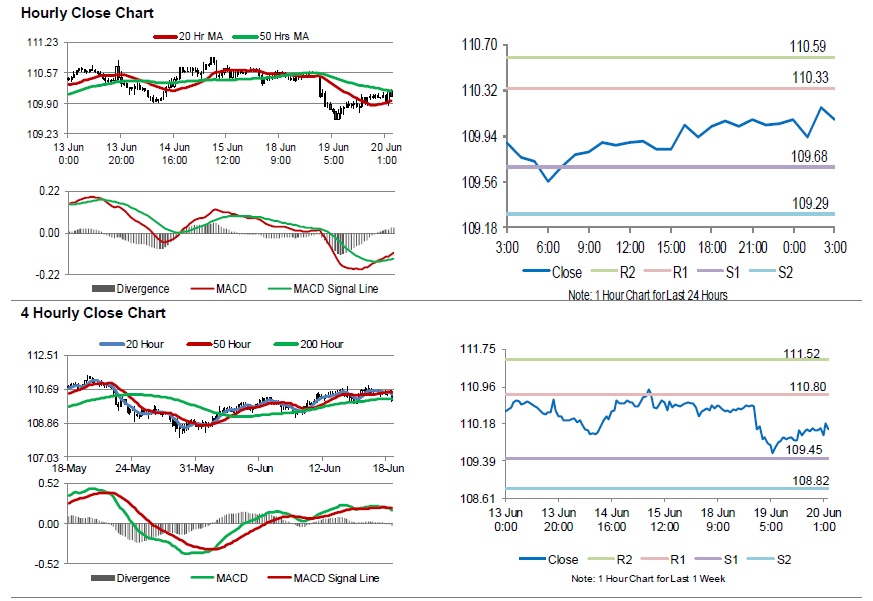

BoJ Erases Set Timeline For Inflation Target

For the 24 hours to 23:00 GMT, the USD declined 0.45% against the JPY and closed at 110.04.

In the Asian session, at GMT0300, the pair is trading at 110.07, with the USD trading slightly higher against the JPY from yesterday’s close.

The minutes of the Bank of Japan (BoJ) April monetary policy showed that the BoJ’s reflationist Goushi Katoka was against the view of other policymakers to keep monetary policy unchanged and suggested that further easing was required to accelerate inflation. Moreover, members indicated that it was appropriate to drop the timeframe the bank had set for achieving its 2.0% inflation target. Further, most of the officials shared the view that the country’s economic expansion was progressing as expected and is likely to continue.

The pair is expected to find support at 109.68, and a fall through could take it to the next support level of 109.29. The pair is expected to find its first resistance at 110.33, and a rise through could take it to the next resistance level of 110.59.

In absence of key economic releases in Japan today, investor sentiment would be determined by global macroeconomic events.

The currency pair is trading above its 20 Hr moving average and showing convergence with its 50 Hr moving average.

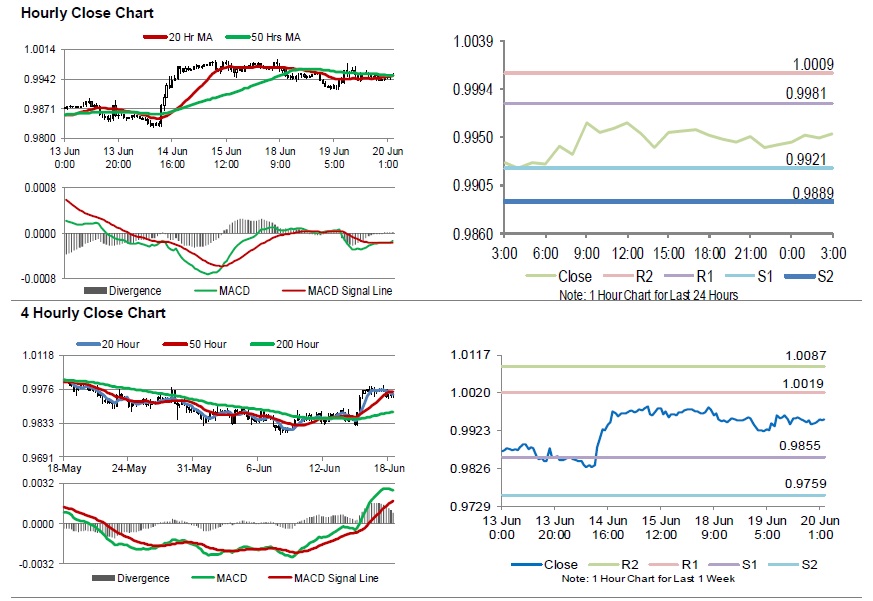

Swizz Franc Trading On A Weaker Footing This Morning

For the 24 hours to 23:00 GMT, the USD declined 0.12% against the CHF and closed at 0.9942.

The Swiss Franc rose after the government maintained its growth outlook for the country.

According to the State Secretariat for Economic Affairs, the economy will grow 2.4% in 2018, in line with expectations. Meanwhile, the projection for 2019 was retained at 2.0%. Nevertheless, inflation outlook for this year was raised to 1.0% from 0.6%.

In the Asian session, at GMT0300, the pair is trading at 0.9952, with the USD trading 0.10% higher against the CHF from yesterday’s close.

The pair is expected to find support at 0.9921, and a fall through could take it to the next support level of 0.9889. The pair is expected to find its first resistance at 0.9981, and a rise through could take it to the next resistance level of 1.0009.

With no macroeconomic releases in Switzerland today, investors would look forward to global macroeconomic events for further direction

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

Loonie Trading Slightly Higher In The Morning Session

For the 24 hours to 23:00 GMT, the USD rose 0.61% against the CAD and closed at 1.3282.

In the Asian session, at GMT0300, the pair is trading at 1.3279, with the USD trading a tad lower against the CAD from yesterday’s close.

The pair is expected to find support at 1.3225, and a fall through could take it to the next support level of 1.3171. The pair is expected to find its first resistance at 1.3313, and a rise through could take it to the next resistance level of 1.3347.

In absence of any macroeconomic releases in Canada today, investor sentiment would be governed by global macroeconomic factors.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

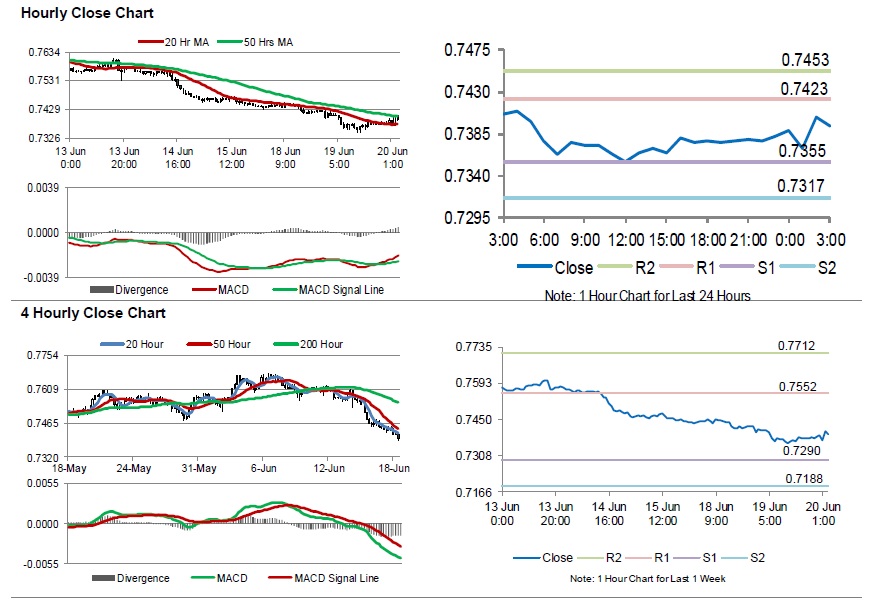

Aussie Reverses Its Losses In The Asian Session

For the 24 hours to 23:00 GMT, the AUD declined 0.53% against the USD and closed at 0.7383.

LME Copper prices declined 10.12% or $707.0/MT to $6280.0/MT. Aluminium prices declined 1.87% or $41.5/MT to $2179.0 /MT.

In the Asian session, at GMT0300, the pair is trading at 0.7393, with the AUD trading 0.14% higher against the USD from yesterday’s close.

Overnight data indicated that Australia’s Westpac leading index retreated by 0.22% on a monthly basis in May. The index had climbed by a revised 0.23% in the prior month.

The pair is expected to find support at 0.7355, and a fall through could take it to the next support level of 0.7317. The pair is expected to find its first resistance at 0.7423, and a rise through could take it to the next resistance level of 0.7453.

The currency pair is trading above its 20 Hr moving average and showing convergence with its 50 Hr moving average.