Sample Category Title

Risk Off Moves Supported By Tit-For-Tat Trade Dispute

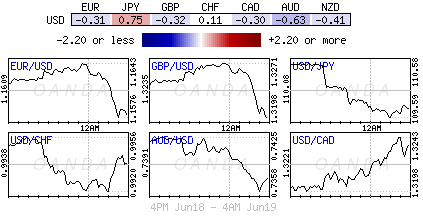

Tuesday June 19: Five things the markets are talking about

The trade dispute between the two economic superpowers, U.S and China, is getting ugly very quickly and has triggered a global sell-off of riskier assets and flight toward safe haven assets. The fallout is pressuring global equities and providing support for U.S treasuries, gold and yen.

Ongoing tough trade talk from President Trump has EUR and U.S stock futures seeing red for a third consecutive open, following losses across Asia as Chinese and Hong Kong shares plunged after reopening following a holiday.

The move towards protectionism has rattled commodities and commodity-linked currencies like the AUD, CAD and NOK. Even emerging markets are taking a hit on the real possibility that a global trade war becomes a reality and not just tough talk.

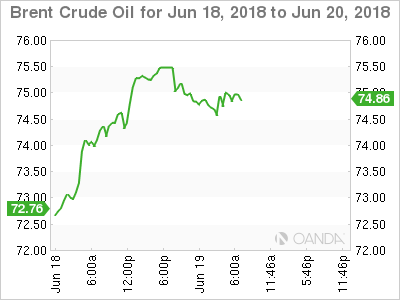

Crude oil prices are also taking a hit, paring yesterday’s gain as the market weigh OPEC’s discussions on a compromise over increasing output ahead of this week’s key meeting in Vienna (June 22/23).

On tap: U.S building permits & housing starts (June 19), NZD GDP (June 20), SNB & BoE monetary policy decision (June 21), OPEC (June 22/23)

1. Stocks see red

Asia equities fell to a new four-month low as President Trump raises the stakes in Sino-U.S trade war. Trump threatened yesterday to impose an additional +10% tariff on +$200B of Chinese goods, disobeying negotiation and consensus reached previously between the two countries. This has prompted a swift warning of retaliation from China.

In Japan, stocks plummeted to a three-week low overnight and posted the biggest daily percentage drop in three-months after Chinese equities were aggressively sold amidst escalating global trade struggles. The Nikkei share average ended -1.8% lower, while the broader Topix shred -1.6%.

Down-under, Aussie stocks bucked the trend and added +0.1%, helped by a depreciating AUD and an overnight bounce in commodity prices. In S. Korea, the Kospi depreciated -1.3%.

In Hong Kong, stocks closed at their lowest in more than four months, tracking other regional bourses dejected by escalating Sino-U.S trade frictions. The Hang Seng index closed down -2.8%, while the China Enterprises Index lost -3.2%.

In China, Shanghai equities plummeted nearly -4% to a two-year low overnight on Trump’s fresh tariff threats that could escalate into a full-blown trade war. The Shanghai Composite Index finished the session down -3.8%, while the blue chip CSI300 index fell -3.6%.

In Europe, regional bourses trade sharply lower across the board following on from Asia’s losses.

U.S stocks are set to open deep in the “red” (-1.2%).

Indices: Stoxx600 -0.9% at 32.6, FTSE -0.6% at 7587, DAX -1.5% at 12646, CAC-40 -1.2% at 5387, IBEX-35 -1.1% at 9658, FTSE MIB -0.8% at 21922, SMI -0.8% at 8452, S&P 500 Futures -1.2%

2. Oil prices dip on expectations of rising OPEC, gold higher

Oil prices are under pressure on expectations that OPEC and its key ally Russia will gradually increase output after withholding supplies since 2017.

Brent crude futures are at +$78.05 per barrel, down -29c, or -0.4%, from Monday’s close. U.S West Texas Intermediate (WTI) crude futures are at +$65.63 a barrel, down -22c, or -0.3%.

Note: OPEC and non-OPEC producers, that include Russia, started withholding oil supplies in 2017 to end a global glut and prop up prices.

OPEC will meet later this week (June 22/23) in Vienna to discuss forward policy. Saudi Arabia and Russia are saying that production should be increased “gradually” if deemed necessary.

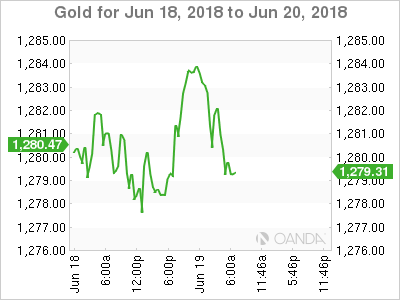

Ahead of the U.S open, gold prices are better bid, supported by a weaker U.S dollar and a dip in global bourses as a trade spat between the U.S and China intensifies. Spot gold is up +0.4% at +$1,282.54 an ounce, while U.S gold futures for August delivery are also +0.4% higher at +$1,285.70 per ounce.

3. Politics and ECB should remain the key drivers for Bunds and spreads

Eurozone government bond yields are trading lower with market participants looking at the ECB’s forum in Portugal as well as politics for further directional clues.

ECB President Draghi signalled earlier today that the bank could extend its QE program again and delay any interest-rate increases to counter possible shocks to the eurozone economy. These ‘easing’ comments have come only day’s after the ECB laid out plans to phase out its bond purchases (QE) – it would suggest that Euro policy makers remain very cautious about winding down its stimulus program just as the region’s economy appears to be slowing.

Germany’s 10-year Bund yield has declined -4 bps to +0.36%, hitting the lowest in almost three-weeks with its sixth straight decline. The yield on U.S 10-year Treasuries declined -6 bps to +2.86%, the lowest in almost three-weeks on the biggest decrease in three-weeks. In the U.K, the 10-year Gilt yield has dipped -5 bps to +1.324%, reaching the lowest in almost a month.

4. Dollar’s safe haven demand

Safe haven demand is lifting the U.S dollar as the possibility of a trade war escalates between the U.S and China.

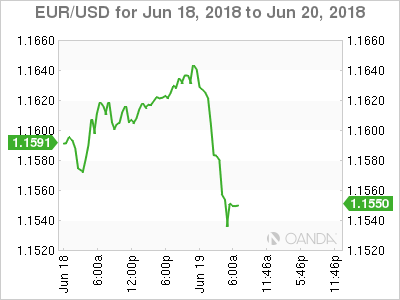

EUR/USD (€1.1543) is under pressure; matching last weeks intraday low outright (€1.1536) after downbeat comments from ECB’s Draghi earlier this morning. Speaking at the ECB forum in Portugal, he said, “uncertainty surrounding the eurozone growth outlook has recently increased.” He said the ECB would remain patient in determining the timing of the first rate rise. These comments come after last week’s ECB meeting, when the central bank set clear guidance that it wouldn’t raise interest rates at least until after the summer of 2019.

Sterling is off -0.4% at £1.3201 outright, as the USD benefits from its safe-haven status on the back of an escalating trade conflict with China. But there are domestic issues facing the pound as well. Brexit talks have not progressed much since March, while the June 28-29 summit is looming. Also, the Brexit withdrawal bill is still being debated in the U.K. parliament, while weaker U.K. economic data has lowered the chance of an interest rate increase this year.

Note: The fixed income market is pricing in a +8% chance of a BoE rate increase this Thursday.

5. Eurozone current-account surplus eases further

Data this morning from the ECB showed that the eurozone’s current-account surplus eased further in April, registering its third-consecutive monthly decline, but it remained elevated year-over-year.

The region’s current-account balance eased to +€28.4B from a revised surplus of +€32.8B in March.

Note: The surplus was +€22.9B billion in April 2017.

Expect an elevated euro trade-surplus not to sit well with President Trump. Releases like this morning’s are very much susceptible to the odd drive by Trump Twitter rants just like his repeated ticking-off of Germanys bulging trade-surplus.

Digging deeper, in the 12-months through April, the eurozone recorded a current-account surplus of +€413.7B, which equals about +3.7% of its GDP.

Euro Slips As Trade War Worsens

EUR/USD has posted considerable losses in the Tuesday session. Currently, the pair is trading at 1.1552, down 0.60% on the day. On the release front, the ECB Forum kicks off with a speech from ECB President Mario Draghi. In the eurozone, the current account surplus narrowed for a third straight month, dropping to EUR 28.4 billion. This fell short of the estimate of EUR 30.3 billion. In the U.S, the focus is on construction data. Building Permits is expected to remain pegged at 1.35 million for a third straight month. We’ll also get a look at Housing Starts, which is forecast to rise to 1.31 million. On Wednesday, Mario Draghi and Fed Chair Jerome Powell will participate in a panel at the European Forum. Germany releases PPI and the US publishes Housing Starts.

The euro is under strong pressure, EUR/USD is struggling to stay above the 1.15 level. The pair has declined 1.3% in the month of June. Investors are reacting negatively to the escalating trade war between China and the U.S, and if the tit-for-tat tariffs continue, the euro could continue to head south. The U.S announced a 25 percent tariff on $50 billion in Chinese goods on Friday. After China responded with an identical move on U.S. imports, President Trump has now threatened to impose 10 percent tariffs on some $200 billion in Chinese goods. Not surprisingly, China has threatened to retaliate to this latest move. Trump has vowed to take action on the $375 billion trade deficit that the U.S has with China, claiming that the latter is guilty of unfair trade practices. With the first of the U.S tariffs scheduled to take effect on July 6 and no signs that any side will blink first, the markets should be preparing for stormy weather ahead.

Investors Concerns By Prospect Of More Trade Tariffs

- Additional tariffs trigger more risk aversion;

- Gold not benefiting from safe haven moves as dollar weighs;

- EUR and GBP continue slide ahead of central bank speeches.

US markets are on course for another day in the red as we await the open on Tuesday, with futures down more than one percent as US President Donald Trump threatens to intensify the trade spat with China.

Trump has requested that another $200 billion of Chinese goods be identified for a 10% tariff as he ramps up the pressure on China to address the trade imbalances between the world's two largest economies and stop other practices the President deems unfair. Trump has already pre-empted a response by China and claimed that any retaliation will be met with another $200 billion list being drawn up which suggests he has no intention of backing off, no matter what the consequences.

With China showing no desire to be bullied into submission, with its Commerce Ministry promising to retaliate to any new tariffs and its Foreign Ministry reaffirming that while it doesn't want a trade war, it's not afraid to engage in one, it's difficult to see how and when this ends. Moreover, it's difficult to fully grasp just how much damage will be done in the process, particularly with the European Union also drawing up counter-tariffs against the US.

The clear escalation that's occurred in recent days has shaken investors and appears to brought an end to the good run that US stock markets had been on since the start of May. While Chinese stocks are faring much worse at the moment, US companies are obviously not immune to a trade war and could come under more pressure unless both sides find a solution.

We're seeing plenty of risk aversion in the markets in response to the tariffs although interestingly Gold is not seeing the usual safe haven gains as a stronger dollar is weighing on demand for the yellow metal. The dollar appears to be benefiting from a combination of safe haven Treasury demand which has driven the 10-year yield back below 2.9% and weakness in the euro and the pound.

The euro is still suffering from the ECBs successful attempts to wrap a hawkish policy move in dovish rhetoric last Thursday which has pushed the single currency back towards 1.15 which has been a notable support level over the last 10 months. Sterling on the other hand appears to be suffering ahead of the Bank of England meeting on Thursday, with Brexit-related uncertainty hanging over Prime Minister Theresa May ahead of some crucial talks with the EU this month.

While the data calendar looks a little bare today, with US building permits and housing starts the only notable releases, we are preparing for remarks from a number of prominent central bankers over the next couple of days that could have a significant market impact. We heard from Mario Draghi earlier in the European session but the ECB President offered little more than a rehash of earlier statements.

SNB To Stand Idle

SNB Up Next

On Thursday, the SNB will meet to broadcast their monetary policy strategy. In the light of higher domestic inflation, ECB “normalization” signal and mounting political risk in Europe, this generally sleepy meeting should get additional attention. At the March meeting the SNB held sight deposit rates at -0.75% while reiterating the bank would remain active if necessary in the foreign exchange market. We anticipate a broadly dovish communication, particularly in the light of recent ECB forward guidance. Since the last statement, the CHF has generally appreciated ensuring that the “highly valued” term will remain. In addition, uncertainty in Europe, specifically in Italy will keep the SNB vigilant. We suspect that the near term inflation forecast and growth assessment will remain unchanged despite clear improvements.

Firstly, the SNB will avoid sparking any speculation that might cause CHF to appreciate. Secondly, global growth and macro backdrop are a cause for concerns for the small alpine economy, which will provide plenty of coverage for the SNB. Interestingly, the SNB has expressed concerned over overheating of the housing markets. Even suggesting a need for a price correction. We are uncertain how the SNB will handle this issue.

However, Swiss general economy continues to surprise to the upside. PMI are running above average, while GDP growth is coming off a strong 1Q. We continued to see the SNB as one of the last G10 movers towards normalization. Our call is for the first interest rate hike, is September 2019. This forecasts is based less on the trajectory of Swiss inflation and more the ECB policy path. We anticipate ECB asset purchase will end in 2018 and first rate hike March 2019. This give the SNB six month to judge the markets reaction on Euro before preceding. The significant lag between G10 central banks and the SNB and excellent candidate for global funding currency, suggests that risk rewards trade-off for the EURCHF remains to the upside.

Italy's trade balance drops in April as further uncertainty looms

Under strong uncertainties with regard to recently formed coalition of both the League and the 5 Star movement at that time, Italy's April trade balance strongly decreased, given at EUR 2'938 million (prior: EUR 4'531 million), due to a strong increase in imports (+0.70%) while exports remained flat (+0.10%). On equity side however, the outlook is rather different, as Italy's FTSE MIB surged by 7% (year-to-date: -0.28%) during the single month of April, an impressive rise compared to Europe's leading blue-chip index Euro Stoxx 50 which rose by +5.21% (year-to-date: -2.28%) during the same period.

One could think that the situation improved since the Italian government was officially built, however the truth is very different. Indeed, investors' concerns with regard to budget extension are confirmed, as recent rumours confirm that Finance Minister Giovanni Tria will be willing to renegotiate a balanced-budget target extension by 2021 from 2020 expected during EU summit in Luxemburg on Thursday. Italy's government priorities will also be discussed on this occasion.

Accordingly, as continued fears among EU countries continues (e.g. Germany/EU immigration disagreement, Brexit-EU divorce), we would expect further weakness with regard to the EUR/USD for the ongoing week. Currently trading at 1.1586, the pair is expected to decrease along the 1.1565 range in the short-term.

Risk Aversion Flows Dominate Price Action

Notes/Observations

- Trade war rhetoric heats up aiding risk aversion flows

- ECB officials reiterate it could be patient in any 1st potential rate hike

Asia:

- China Commerce Ministry (MOFCOM): US threats on $200B tariffs list disobeys negotiation and consensus reached previously between the two countries: to take qualitative and quantitative measures if US publishes additional tariffs list. If US published additional imports tariff list, China will have to adopt comprehensive measures to fight back firmly

Europe:

- UK PM May defeated in House of Lords over plans to give lawmakers "meaningful vote" over final Brexit agreement (as expected). Vote was 354-235. Bill moves back to House of Commons for vote on Wed, Jun 20th

- European Commission reportedly won't agree to any back channel UK-EU talks to avert aviation crisis in the event of no deal Brexit. Diplomats from the EU’s 27 other countries are now seriously considering whether a statement following a summit next week should say that “no deal” is a real proposition

Americas:

- US President Trump: Has asked USTR to identify $200B in China goods for additional tariffs at a rate of 10%. Stated that if China increases tariffs yet again, US would respond with tariffs on another $200B in Chinese goods.

Economic Data:

- (SE) Sweden May Unemployment Rate: 6.5% v 6.6%e; Unemployment Rate (Seasonally Adj): 6.1% v 6.3%e

- (EU) Euro Zone Apr Current Account (Seasonally adj): €28.4B v €32.8B prior; Current Account NSA (unadj): €26.2B v €41.36B prior

- (PL) Poland May Sold Industrial Output M/M: 1.6% v 0.0%e; Y/Y: 5.4% v 3.6%e, Construction Output Y/Y: 20.8% v 17.8%e

- (PL) Poland May PPI M/M: 1.1% v 1.0%e; Y/Y: 2.8% v 2.7%e

- (IT) Italy Apr Current Account: €B v €3.4B prior

- (HK) Hong Kong May Unemployment Rate: 2.8% v 2.8%e (matches lowest level since 1998)

- 05:00 (EU) Euro Zone Apr Construction Output M/M: % v -0.3% prior; Y/Y: % v +0.8% prior

Fixed Income Issuance:

- (ES) Spain Debt Agency (Tesoro) sold total €2.42B vs. €2.0-3.0B indicated range in 3-month and 9-month bills

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 -0.9% at 32.6, FTSE -0.6% at 7587, DAX -1.5% at 12646, CAC-40 -1.2% at 5387, IBEX-35 -1.1% at 9658, FTSE MIB -0.8% at 21922, SMI -0.8% at 8452, S&P 500 Futures -1.2%]

- Market Focal Points/Key Themes: European Indices trade sharply lower across the board following on from steep losses in Asia overnight and weaker US futures on continuing trade concerns as the Shanghai composite declined almost 4% for its lowest close since 2016. On the corporate front, a third profit warning from UK retailer Debenhams, and a profit warning from McCarthy and Stone sees shares sharply lower. Ashtead Group, Telecom plus also trade lower following results, with Ferguson outperfoming after strong earnings. Inmarsat trades higher on a potential higher bid, while Roche trades slightly higher after acquiring Foundation Medicine for $137/shr. In other news PSA group trades lower after its CFO stepped down to join Sanofi.

Movers

- Consumer Discretionary McCarthy and Stone [MCS.UK] -15% (Proift warning), Debenhams [DEB.UK] -7% (Profit warning), Ferguson [FERG.UK] +2.2% (Earnings), Ashtead Group [AHT.UK] -5% (Earnings)

- Industrials DS Smith [SMDS.UK] -3% (Rights issue), Volkswagen [VOW3.DE] -2.6% (Momentum), PSA Group [UG.FR] -1.6% (CFO leaves) -Materials K+S [SDF.DE]-2.4% (Canada production halts to weigh on Q2)

- Telecoms Inmarsat [ISAT.UK] 2.4% (Potential higher bid), Telecom Plus [TEP.UK] -4% (Earnings)

Speakers

- ECB President Draghi reiterated Council view that inflation was gradually returning toward target and that significant monetary accommodation was still needed. ECB to be patient in determining the timing of the 1st potential rate hike and than would take a gradual approach after the 1st rate hike. Economy developing underlying strength; growing evidence that broad-based growth was beginning to generate positive pricing dynamics

- ECB's Lane (Ireland): Central bank has a wide range of tools; interest rates was only one aspect. Inflation was low around the world. Global economy prospects were currently balanced but trade dimensions a risk factor. Trade issues were relatively contained but need to keep a close eye on issues

- ECB's Liikanen stated that the General Council could hold rates steady even longer than summer 2019 if necessary

- Italy Govt might push back balanced budget target by one year until 2021. Govt foresaw renegotiation of budget flexibility with EU

- EU Chief Brexit Negotiator Barnier stated that it must have effective information exchange with UK. EU needed more realism about what was possible. Reiterated view that much work needed to be done ahead of the Jun EU Leader Summit. Hoped that Brexit talks concluded in October

- Sweden Debt Office updated its Borrowing Forecasts and mage no change to its issuance plans. To sell SEK32B in nominal bonds and SEK9B in I/L bonds in 2018 and to sell SEK30 in nominal bonds and SEK9B in I/L bonds in 2019. Reducing issuance would hurt liquidity but was open to discuss liquidity measures

- German IFO institute cut its 2018 and 2019 GDP growth forecasts. Cut itss 2018 German growth from 2.6% to 1.8% and 2019 German growth from 2.1% to 1.8%

- Turkey Econ Min Zeybekci: Emergency rule should not be renewed again. Reiterated view that TRY currency (Lira) weakness is due to speculation ahead of the Jun elections

- Japan Cabinet Office (Gov’t) Monthly Economic Report for June: Maintained its overall assessment that economy was recovering at a moderate pace

- China FX Regulator SAFE reiterated view that cross-border flows remained basically stable. Domestic Economy stabilized in May

- China Foreign Ministry reiterated view to take effective measures to safeguard globalization and urged the US to come back to rationality

- China PBOC Working paper: Necessary conditions for monetary policy transformation have been satisfied. Should vigorously promote price-based monetary policy with deepening of supply-side reform. Maintaining relatively high RRR was necessary as a developing nation for the long-term. China should appropriately lower the RRR (ease RRR burdens on financial institutions)

- Iran’s OPEC Rep Kazempour Ardebili: OPEC output increase would swell oil stockpiles again

Currencies

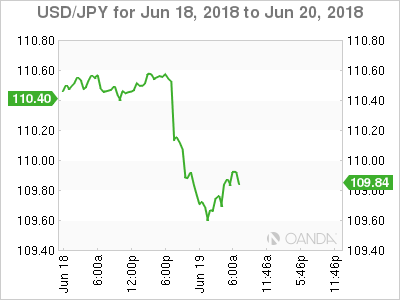

- Trade war rhetoric heats up aiding risk aversion flows with the usual safe-haven flows of USD, JPY and CHF all benefitting.

- EUR/USD hit a 3-week low below 1.1550 as the session progressed from safe-haven flows and reiteration from ECB officials that it could be patient in any 1st potential rate hike

- USD/JPY approached the 109.50 area

- EUR/CHF cross moved below the 1.15 level.

- The AUD and other commodity-related pairs were lower as China demand-driven commodity futures including iron ore, copper, zinc and aluminum registered sharp declines, as the US considered imposing tariffs on an additional US$200B of Chinese exports. AUD/USD at 0.7365 just ahead of the NY morning.

Fixed Income

- Bund Futures trade 65 ticks higher at 161.76 as Bund yields fall back below 0.40%. Upside targets 162.25 followed by 162.75, while a return lower targets the 158.75 level.

- Gilt futures trade at 123.09 higher by 54 ticks as US Treasuries rally. Support continues stands at 121.75 then 120.25, with upside resistance at 123.85 then 124.25.

- Tuesday's liquidity report showed Monday's excess liquidity fell from €1.862T to €1.849T. Use of the marginal lending facility rose from €95M to €116M.

- Corporate issuance saw Bayer announce a $15B debt offering in eight parts for the Monsanto acquisition

Looking Ahead

- (CO) Colombia May Consumer Confidence: 3.8e v 1.5 prior

- (UR) Ukraine Q1 Final GDP Q/Q: No est v 0.9% prelim; Y/Y: 3.1%e v 3.1% prelim

- 05.30 (UK) Weekly John Lewis LFL sales data - 05:30 (HU) Hungary Debt Agency (AKK) to sell in 3-month Bills

- 05:30 (EU) ECB 7-day Main Financing Tender (MRO) allotment

- 05:30 (DE) Germany to sell €4.0B in 0% Jun 2020 Schatz

- 05:30 (ZA) South Africa announces to sell combined ZAR2.4B in 2030, 2031 and 2044 bonds

- 06:00 (PT) Portugal May PPI M/M: No est v 0.1% prior; Y/Y: No est v 1.2% prior

- 06:00 (TR) Turkey to sell 2019, 2024 and 2028 bonds

- 06:30 (EU) ESM to sell €2.0B in 6-month Bills

- 06:45 (US) Daily Libor Fixing

- 07:00 (BR) Brazil Jun IGP-M Inflation (2nd Preview): 1.7%e v 1.2% prior

- 07:00 (IE) ECB's Lane (Ireland) and Fed Bullard (dove, non-voter) speak in Sintra, Portugal

- 07:45 (US) Weekly Goldman Economist Chain Store Sales

- 08:00 (HU) Hungary Central Bank (MNB) Interest Rate Decision: Expected to leave Base Rate unchanged at 0.90%

- 08:00 (RU) Russia announces weekly OFZ bond auction (held on Wed)

- 08:05 (UK) Baltic Dry Bulk Index

- 08:30 (US) May Housing Starts: 1.311Me v 1.287M prior; Building Permits: 1.350Me v 1.352M prior

- 08:55 (US) Weekly Redbook Sales

- 09:00 (BE) Belgium Apr Trade Balance: No est v €0.3B prior

- 09:00 (EU) Weekly ECB Forex Reserves (RU) Russia May PPI M/M: 1.3%e v 1.2% prior; Y/Y: 9.6%e

- 09:00 (EU) ECB’s Nouy (SSM chief) in EU Parliament in Brussels

- 09:00 (HU) Hungary Central Bank (MNB) Gov Matolcsy post rate decision statement

- 11:30 (US) Treasury to sell 4-Week and 52-Week Bills

- 15:00 (AR) Argentina Q1 GDP Q/Q: No est v 1.0% prior; Y/Y: 3.5%e v 3.9% prior

- 16:30 (US) Weekly API Oil Inventories

Crude Oil Rebound In Sight

Pivot (invalidation): 64.90

Our preference Long positions above 64.90 with targets at 66.35 & 66.70 in extension.

Alternative scenario Below 64.90 look for further downside with 64.15 & 63.60 as targets.

Comment The RSI is mixed to bullish.

Silver Spot Key Resistance At 16.6400

Pivot (invalidation): 16.6400

Our preference Short positions below 16.6400 with targets at 16.3900 & 16.2900 in extension.

Alternative scenario Above 16.6400 look for further upside with 16.7800 & 16.9300 as targets.

Comment Even though a continuation of the technical rebound cannot be ruled out, its extent should be limited.

Gold Spot Turning Up

Pivot (invalidation): 1277.00

Our preference Long positions above 1277.00 with targets at 1286.00 & 1290.00 in extension.

Alternative scenario Below 1277.00 look for further downside with 1273.00 & 1269.00 as targets.

Comment The RSI advocates for further upside.

EUR/GBP The Bias Remains Bullish

Pivot (invalidation): 0.8755

Our preference Long positions above 0.8755 with targets at 0.8780 & 0.8800 in extension.

Alternative scenario Below 0.8755 look for further downside with 0.8740 & 0.8725 as targets.

Comment Even though a continuation of the consolidation cannot be ruled out, its extent should be limited.

AUD/USD The Downside Prevails

Pivot (invalidation): 0.7435

Our preference Short positions below 0.7435 with targets at 0.7385 & 0.7365 in extension.

Alternative scenario Above 0.7435 look for further upside with 0.7455 & 0.7480 as targets.

Comment As Long as 0.7435 is resistance, look for choppy price action with a bearish bias.