Sample Category Title

US-China Trade: Trade War Becomes A Reality As Trump Pushes Further

Key dates to watch

- 30 June: US announces investment restrictions and export controls on China.

- 6 July: tariffs by China and the US implemented on goods worth USD34bn. Trump said yesterday that Chinese tariffs would trigger tariffs of 10% on a further USD200bn of Chinese imports.

As we wrote yesterday in 'US-China trade - From 'Grand Bargain' towards trade war?', an escalation into a trade war had become increasingly likely. Yesterday evening, that trade war became a reality when Trump warned of a further 10% tariffs on Chinese imports worth USD200bn, with no signs of negotiations in sight.

The new escalation poses clear downside risks to global growth in the coming quarters as it raises uncertainty and is set to hurt global investment appetite.

Chicken game with a bad outcome

Trump pulled out the heavy ammunition yesterday when he announced that the US would increase the amount of Chinese imports by USD200bn with a tariff of 10% if China retaliates to the first US tariffs on Chinese imports worth USD50bn. He also said the US would increase it by a further USD200bn if China retaliated to that.

The move suggests that Trump believes he has the strongest hand and will continue to hit China with tariffs if it retaliates. China, on the other hand, has signalled clearly that it will not tolerate US tariffs and will respond in a tit-for-tat manner. Therefore, it looks as if we are facing a chicken game, which could have a bad outcome, as it is hard to see anyone backing down.

China's response came promptly yesterday with the Ministry of Commerce writing that China will respond 'forcefully' and 'take comprehensive quantitative and qualitative measures'. It also labelled the move by Trump 'extreme pressure and blackmail'.

How China could retaliate

As China does not have US imports worth more than USD130bn, it will not be able to follow suit on the exact amounts and tariffs. However, there are several other ways it could strike back. First, it could choose a higher tariff rate than 10%. Second, as it mentioned in the statement, it could take quantitative measures; for example, by buying Airbus airplanes instead of Boeing or buying more soybeans in Brazil and Argentina instead of the US. China could also place restrictions on US investments in China. It comes at a time when China is opening up more in general for investments in more sectors but US companies could be excluded from some sectors, putting them at a disadvantage in the fastest growing market in the world. Another way US companies could be hurt would be if a consumer boycott of some sort were to be initiated. GM sells more cars in China than in the US, and for most big US brands, China is a major market. We still do not expect China to use the selling of US treasuries, as this could backfire by causing financial instability.

Key dates to watch

The next key dates to watch will be 30 June – when Trump will announce restrictions on Chinese investments into the US, as well as export controls of US tech products to China – and 6 July – when the first Chinese tariffs on US goods are due to be implemented. As we stated, Trump has said that Chinese tariffs on US products would trigger the increase of the amount subject to tariffs by USD200bn

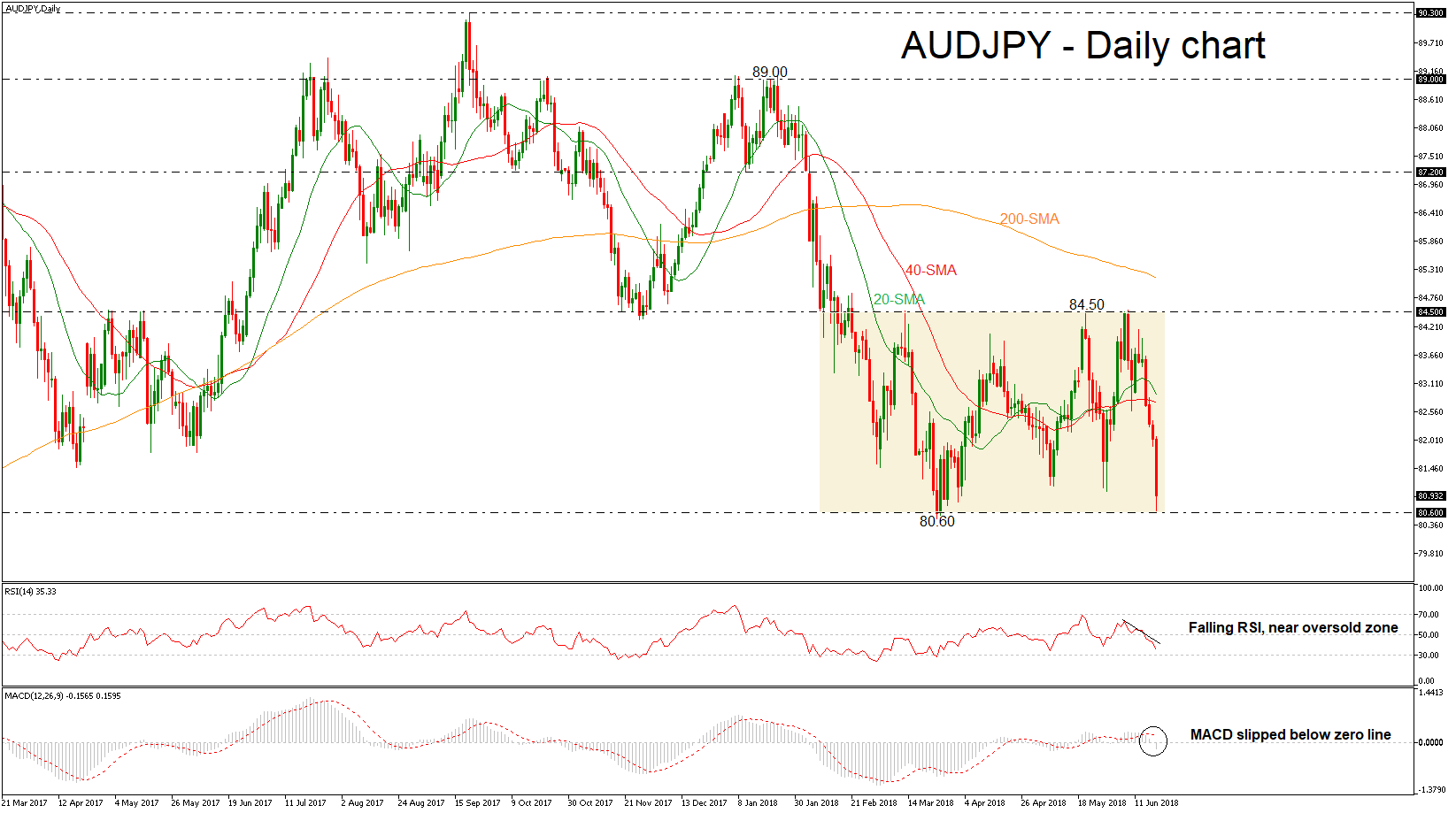

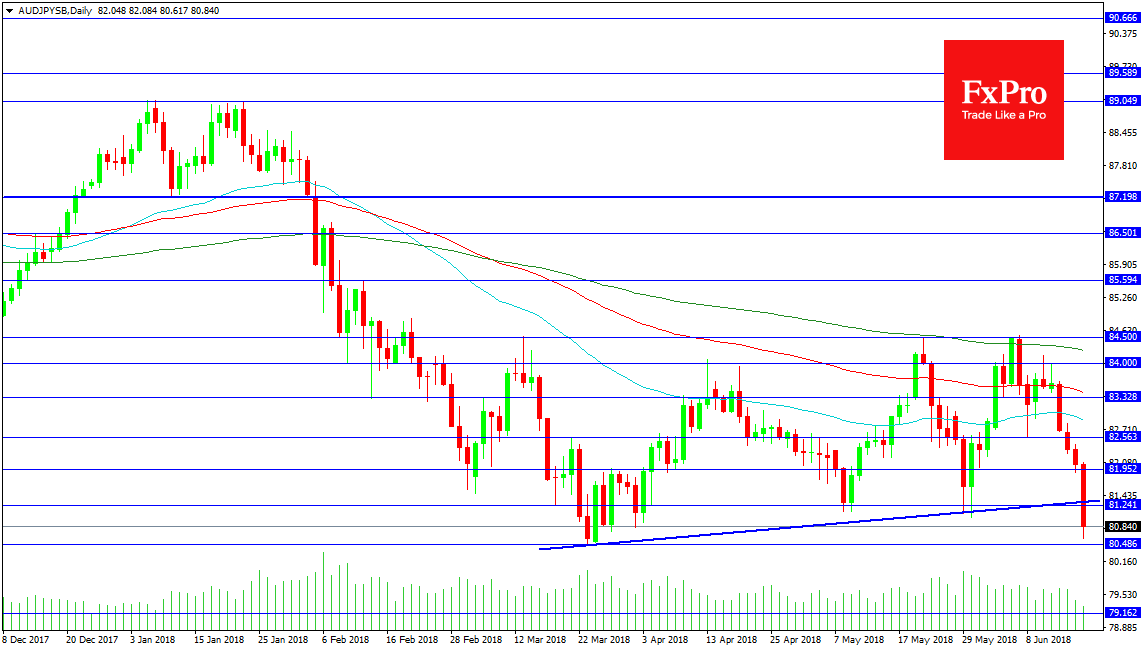

AUDJPY In Sharp Downside Pressure In Near Term, Stands In Consolidation Area

AUDJPY is set to record the fourth straight bearish day with strong momentum as it posted a fresh 12-week low near 80.61 on Tuesday. In the medium-term, the price has been developing within a trading range since mid-February with upper band the 84.50 resistance level and lower band the 80.60 support level.

The RSI is currently increasing negative momentum towards the threshold of 30, while the MACD is slowing down in negative territory, both hinting that the next move in prices could be on the downside rather than on the upside. Furthermore, the 20-simple moving average (SMA) is ready to touch the 40-SMA, creating a bearish cross.

Should the market extend losses and the price plummets below the consolidation area, this could drive the pair lower towards the 79.00 handle, identified by the high on September 2016.

Conversely, an upside correction could push the pair until the 40-SMA first at 82.72 and then at the 20-SMA at 82.89. Steeper advances, though, could move AUDJPY north towards the 84.50 upper band, fully reversing this and last week’s rally.

In the medium-term, the outlook remains negative since prices hold below all the moving average lines and the bearish cross between the 20- and the 40-day SMAs is near.

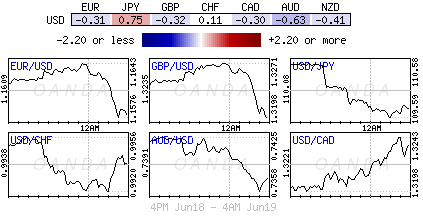

Demand For The Australian Dollar Fell Against The US dollar

Following the release of the meeting minutes of the Australian Monetary Policy Council and with the increasing divergence between Australian and US monetary policies, demand for the Australian dollar fell against the US dollar.

The price crossed the major support level, falling to 0.7412 and is expected to continue with a bearish trend mid-term.

In the short term, there is a possibility of a correction, and for the pull-back to break the support level.

Support levels: 0.7328, 0.7160

Resistance levels: 0.7412, 0.7676

USDJPY – Trade War Leads To Risk Aversion

The Chinese government began imposing tariffs on certain US imports yesterday. The US government and President Trump threatened to impose new tariffs on $200 billion in Chinese imports.

This Trade War between the two major economic super powers, are increasing international tensions and leading to risk aversion in the financial markets, which causes the demand for the Japanese yen to rise.

At present, the price crossed support levels and the mid-range moving average in the 4-hour timeframe and has reacted to the lowest level of the Ichimoku Como cloud.

A downward trend is expected mid-term following a correction wave in the short-term.

Support levels: 109.20, 108.10, 107.77

Resistance levels: 110.90, 111.40, 112.03

Trump Hits Back Again

President Trump anchored the tensions further between the US and China (as if there was not already enough friction between them) on the topic of the trade war. Donald Trump is in full Tit for tat mod, he ordered his department to look for $200 billion worth of Chinese goods for further tariffs at a rate of 10 percent. Investors are nervous because it would surely have another reaction from Beijing. The world’s largest two countries cannot afford to have this kind of attitude as it would have serious impact on the global growth. One of the side should eat their ego and only then this entire conflict can steer itself to some direction for a more suitable solution.

US futures and European markets are trading sharply lower as a result of the trade war. One could say that the trade war is not here yet but one should also think that the moment the word “trade war” came into the play, we started to sail towards uncertainty.

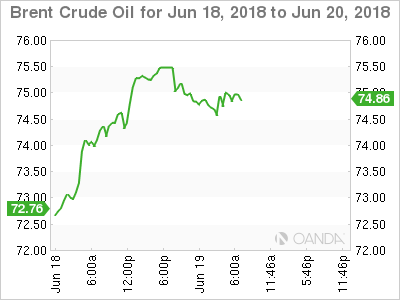

The black gold is out of luck amidst traders as they are pricing in that the OPEC and Russia would increase production. The meeting is due in Vienna on the 22nd June, 2018. The upcoming meeting would be highly interesting and it has a potential to bring higher volatility in the market.

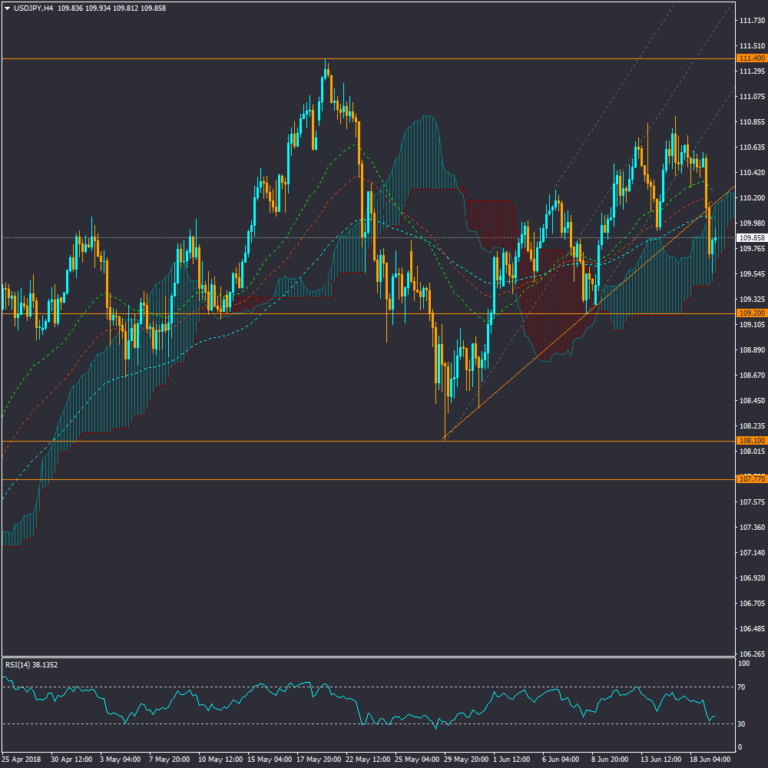

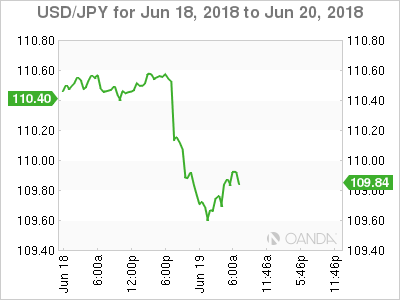

USDJPY Strongly Bearish Below 109.54

The US dollar remains under heavy selling pressure against the Japanese yen, as risk-off trading sentiment spreads through broader financial markets. The USDJPY pair continues to fall lower and risks suffering deeper intraday losses below the 109.54 level. Traders remain focused on trade wars between the US and China, and will look to a key speech from FED Chair Jerome Powell later today.

The USDJPY pair is strongly bearish while trading below the 109.54 level, key technical support is found at the 109.19 and 108.63 levels.

If the USDJPY pair moves above the 110.00 level, key intraday resistance is found at the 110.28 and 110.48 levels.

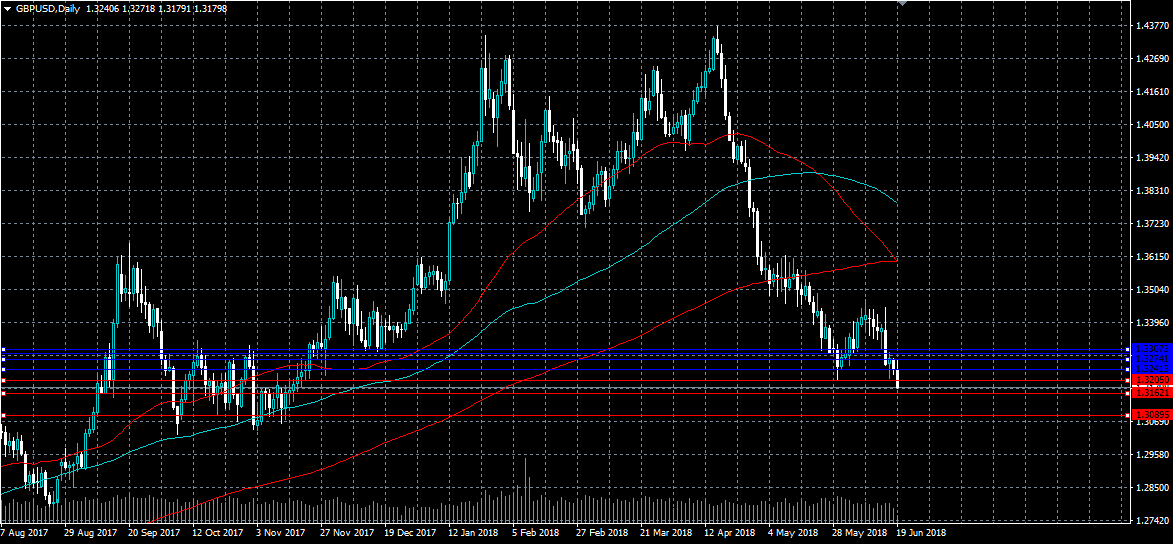

GBPUSD Bearish Below 1.3200

The British pound has fallen to a fresh 2018 trading-low against the US dollar, as the greenback moves higher amidst trade war concerns with China. The GBPUSD pair has tumbled below the 1.3200 level, and now risks deeper protracted losses below the 1.3100 level. Key daily technical indicators are also turning lower, adding further intraday bearish selling pressure to the GBPUSD pair.

The GBPUSD pair is strongly bearish while trading below the 1.3200 level, key technical support is now located at the 1.3162 and 1.3089 levels.

If the GBPUSD pair moves above the 1.3200 level, key technical resistance can be found at the 1.3205 and 1.3241 levels.

Forex Analysis: AUDJPY

The AUDJPY pair was hammered overnight as US President Trump announced his wish to impose a further $200 Billion worth of tariffs on trade with China. The Australian economy is largely dependent on exports of raw materials to China and the AUD reacted accordingly. The price broke under trend line support at 81.314 but remains above the March low at 80.480. This is a critical level for the pair with a fall under this support extending losses towards 80.000 and 79.162. It is possible that the trend line is retested and this will determine the next move after this decline.

Resistance can be seen at 81.240 and the trend line followed by 81.952 and the 82.000 level. Of more importance is the resistance at 82.563 with the 50 DMA turning lower now at 82.893. Above the 83.000 level is horizontal resistance at 83.328 with the 100 DMA turning lower at 83.442. Again horizontal resistance can be seen at 84.000 which is the start of a band that extends up to the next highly significant level at 84.500 and also contains the 84.242. This band contains considerable strength and held price down since late February. Therefore a break above this area could result in a target of 87.000 or even 89.000.

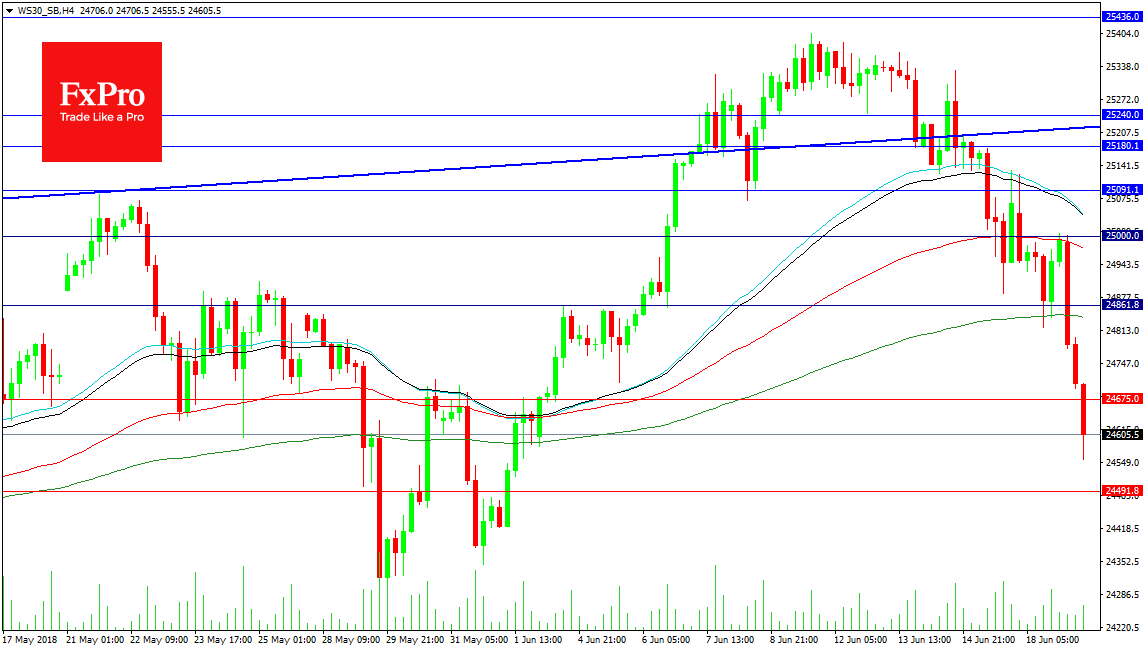

Forex Analysis: US 30 Index

This Index has weakened after an impressive rally earlier this month, peaking at 25400.00. Trade war worries shift sentiment to a more defensive stance and Investors rotated into Tech early last week leaving industrials searching for liquidity. The trend line was loss as price tried to stabilize at the 50 and 55 period MAs but selling on Friday sent price under 25100.00 and we are now 500 points lower. Support today comes in at 24500.00 followed by 24345.00 and 24245.00. A loss of 24200.00 would target 24000.00 on the initial drop.

Resistance comes in around 24700.00 with the 200 period MA at 24839.00 and the nearby level of 24862.00. The 100 MA is found just under 25000.00 at 24976.5 and this level is important from a psychological perspective as seen by the jump higher on the 6th of June. The 50 and 55 period MAs are declining at 25050.00 and were retested as resistance after they were broken last week. A break above 25240.00 would encourage bullish traders that this market can create new highs.

Risk Off Moves Supported By Tit-For-Tat Trade Dispute

Tuesday June 19: Five things the markets are talking about

The trade dispute between the two economic superpowers, U.S and China, is getting ugly very quickly and has triggered a global sell-off of riskier assets and flight toward safe haven assets. The fallout is pressuring global equities and providing support for U.S treasuries, gold and yen.

Ongoing tough trade talk from President Trump has EUR and U.S stock futures seeing red for a third consecutive open, following losses across Asia as Chinese and Hong Kong shares plunged after reopening following a holiday.

The move towards protectionism has rattled commodities and commodity-linked currencies like the AUD, CAD and NOK. Even emerging markets are taking a hit on the real possibility that a global trade war becomes a reality and not just tough talk.

Crude oil prices are also taking a hit, paring yesterday’s gain as the market weigh OPEC’s discussions on a compromise over increasing output ahead of this week’s key meeting in Vienna (June 22/23).

On tap: U.S building permits & housing starts (June 19), NZD GDP (June 20), SNB & BoE monetary policy decision (June 21), OPEC (June 22/23)

1. Stocks see red

Asia equities fell to a new four-month low as President Trump raises the stakes in Sino-U.S trade war. Trump threatened yesterday to impose an additional +10% tariff on +$200B of Chinese goods, disobeying negotiation and consensus reached previously between the two countries. This has prompted a swift warning of retaliation from China.

In Japan, stocks plummeted to a three-week low overnight and posted the biggest daily percentage drop in three-months after Chinese equities were aggressively sold amidst escalating global trade struggles. The Nikkei share average ended -1.8% lower, while the broader Topix shred -1.6%.

Down-under, Aussie stocks bucked the trend and added +0.1%, helped by a depreciating AUD and an overnight bounce in commodity prices. In S. Korea, the Kospi depreciated -1.3%.

In Hong Kong, stocks closed at their lowest in more than four months, tracking other regional bourses dejected by escalating Sino-U.S trade frictions. The Hang Seng index closed down -2.8%, while the China Enterprises Index lost -3.2%.

In China, Shanghai equities plummeted nearly -4% to a two-year low overnight on Trump’s fresh tariff threats that could escalate into a full-blown trade war. The Shanghai Composite Index finished the session down -3.8%, while the blue chip CSI300 index fell -3.6%.

In Europe, regional bourses trade sharply lower across the board following on from Asia’s losses.

U.S stocks are set to open deep in the “red” (-1.2%).

Indices: Stoxx600 -0.9% at 32.6, FTSE -0.6% at 7587, DAX -1.5% at 12646, CAC-40 -1.2% at 5387, IBEX-35 -1.1% at 9658, FTSE MIB -0.8% at 21922, SMI -0.8% at 8452, S&P 500 Futures -1.2%

2. Oil prices dip on expectations of rising OPEC, gold higher

Oil prices are under pressure on expectations that OPEC and its key ally Russia will gradually increase output after withholding supplies since 2017.

Brent crude futures are at +$78.05 per barrel, down -29c, or -0.4%, from Monday’s close. U.S West Texas Intermediate (WTI) crude futures are at +$65.63 a barrel, down -22c, or -0.3%.

Note: OPEC and non-OPEC producers, that include Russia, started withholding oil supplies in 2017 to end a global glut and prop up prices.

OPEC will meet later this week (June 22/23) in Vienna to discuss forward policy. Saudi Arabia and Russia are saying that production should be increased “gradually” if deemed necessary.

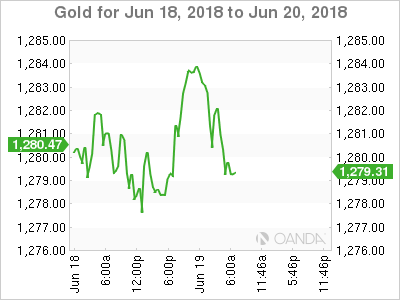

Ahead of the U.S open, gold prices are better bid, supported by a weaker U.S dollar and a dip in global bourses as a trade spat between the U.S and China intensifies. Spot gold is up +0.4% at +$1,282.54 an ounce, while U.S gold futures for August delivery are also +0.4% higher at +$1,285.70 per ounce.

3. Politics and ECB should remain the key drivers for Bunds and spreads

Eurozone government bond yields are trading lower with market participants looking at the ECB’s forum in Portugal as well as politics for further directional clues.

ECB President Draghi signalled earlier today that the bank could extend its QE program again and delay any interest-rate increases to counter possible shocks to the eurozone economy. These ‘easing’ comments have come only day’s after the ECB laid out plans to phase out its bond purchases (QE) – it would suggest that Euro policy makers remain very cautious about winding down its stimulus program just as the region’s economy appears to be slowing.

Germany’s 10-year Bund yield has declined -4 bps to +0.36%, hitting the lowest in almost three-weeks with its sixth straight decline. The yield on U.S 10-year Treasuries declined -6 bps to +2.86%, the lowest in almost three-weeks on the biggest decrease in three-weeks. In the U.K, the 10-year Gilt yield has dipped -5 bps to +1.324%, reaching the lowest in almost a month.

4. Dollar’s safe haven demand

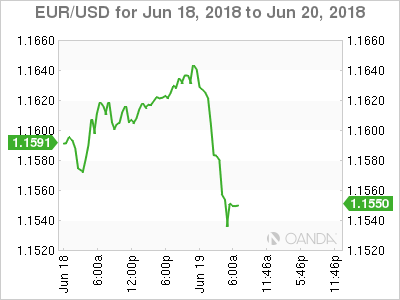

Safe haven demand is lifting the U.S dollar as the possibility of a trade war escalates between the U.S and China.

EUR/USD (€1.1543) is under pressure; matching last weeks intraday low outright (€1.1536) after downbeat comments from ECB’s Draghi earlier this morning. Speaking at the ECB forum in Portugal, he said, “uncertainty surrounding the eurozone growth outlook has recently increased.” He said the ECB would remain patient in determining the timing of the first rate rise. These comments come after last week’s ECB meeting, when the central bank set clear guidance that it wouldn’t raise interest rates at least until after the summer of 2019.

Sterling is off -0.4% at £1.3201 outright, as the USD benefits from its safe-haven status on the back of an escalating trade conflict with China. But there are domestic issues facing the pound as well. Brexit talks have not progressed much since March, while the June 28-29 summit is looming. Also, the Brexit withdrawal bill is still being debated in the U.K. parliament, while weaker U.K. economic data has lowered the chance of an interest rate increase this year.

Note: The fixed income market is pricing in a +8% chance of a BoE rate increase this Thursday.

5. Eurozone current-account surplus eases further

Data this morning from the ECB showed that the eurozone’s current-account surplus eased further in April, registering its third-consecutive monthly decline, but it remained elevated year-over-year.

The region’s current-account balance eased to +€28.4B from a revised surplus of +€32.8B in March.

Note: The surplus was +€22.9B billion in April 2017.

Expect an elevated euro trade-surplus not to sit well with President Trump. Releases like this morning’s are very much susceptible to the odd drive by Trump Twitter rants just like his repeated ticking-off of Germanys bulging trade-surplus.

Digging deeper, in the 12-months through April, the eurozone recorded a current-account surplus of +€413.7B, which equals about +3.7% of its GDP.