Sample Category Title

Markets Shrug Off Escalating Trade Tensions, Brexit Also In The Spotlight

Here are the latest developments in global markets:

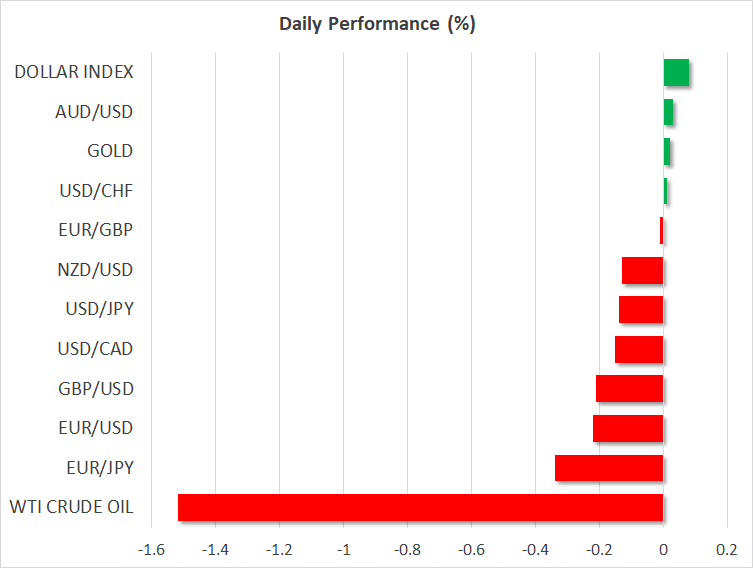

FOREX: The US dollar index was higher by nearly 0.1% on Monday, staying close to the seven-month high it posted last week. The Canadian dollar was 0.15% higher against its US counterpart, trying to recover some of the oil-induced losses it posted on Friday, when it reached a one-year low.

STOCKS: US markets closed lower on Friday in the aftermath of tariff announcements from both the US and China, though the magnitude of the downside moves was relatively small. The Dow Jones led the way lower, shedding 0.34%, while the Nasdaq Composite and S&P 500 fell by 0.19% and 0.10% respectively. Moreover, the slide looks set to extend today, as futures tracking the Dow, S&P, and Nasdaq 100 are all currently signaling a notably lower open for these indices. Indices in Asia were a sea of red on Monday as well. Japan’s Nikkei 225 and the Topix fell by 0.75% and 0.98% correspondingly. Europe was a similar story, with futures pointing to a negative open for all of the major benchmarks today.

COMMODITIES: Oil prices collapsed on Friday, following signals from China that crude oil will be included in the list of products it will impose tariffs on – something likely to curb demand for oil if enacted. Both WTI and Brent crude plunged by around $3 on Friday, to reach a two-week low and a six-week low respectively. The tumble occurred even despite reports that Venezuela, Iraq, and Iran, will seek to veto any production boosts proposed by Saudi Arabia and Russia at this week’s OPEC meeting, which would typically be a bullish signal for oil. In precious metals, gold is marginally higher on Monday, recovering some of the significant losses it posted in the previous session, when it dropped more than $20 to reach a new low for 2018. The metal exited to the downside the sideways range it was trading in even despite heightened risks around global trade, which has turned its technical outlook to negative.

Major movers: Markets mostly unfazed by escalating trade tensions

As widely expected, the US announced on Friday it will proceed with slapping 25% import tariffs on $50bn Chinese products, aimed predominantly at protecting US intellectual property. The US administration also noted that should China attempt to retaliate, then more measures would be forthcoming. Regardless, China quickly responded it will introduce 25% levies on $50bn US goods, ranging from food and vehicles to crude oil. Both sides said they would introduce tariffs on $34 billion goods starting July 6, which may be raised by another $16bn in the coming weeks.

The market reaction was mostly muted though, perhaps because both sides had signaled their intentions well in advance and thus their actions were hardly a surprise for investors. US stock indices closed lower, albeit only modestly so. Meanwhile, safe-havens like gold and the yen – which typically see inflows in times of turmoil – dropped instead of rising, indicating that trade concerns were not enough for investors to increase their exposure to such assets. Gold touched a fresh low for the year of $1,275, with its sizeable tumble also appearing like a delayed effect to the US dollar’s surge on Thursday.

The subdued reaction may reflect expectuld be that with July 6 still a few weeks away, markets are hoping a compromise may be reached before then. In any case, the next moves from either side could set the stage for what to expations that these moves are “hardball” US negotiating tactics aimed at generating leverage, and will not produce an actual trade war in the end. It may also be speculation the impact of a trade standoff will be only a “flesh wound” for the major economies, as the size of the announced tariffs is rather small. Or it coect. The US has threatened to hit China back if it retaliates, and media reports suggest the Commerce Department has already prepared another list of tariffs on $100bn worth of Chinese goods. While markets have been complacent so far, the same may not hold true if things heat up further from here.

Day ahead: Trade concerns and Brexit in the spotlight on quiet calendar day; ECB Forum kicks off

Trade deliberations and Brexit-related developments will be gathering attention on Monday in the absence of important releases out of major economies. In the meantime, the ECB Forum in Sintra, Portugal kicks off today and will feature remarks by influential central bank heads that have the capacity to move markets.

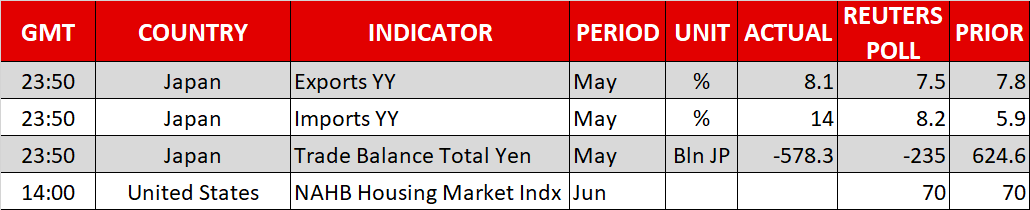

In terms of releases, the National Association of Home Builders (NAHB) housing market index is due out of the US at 1400 GMT and might attract some interest.

In the UK, after the votes in the House of Commons, the House of Lords will now debate the Brexit withdrawal bill that is fueling a rebellion against PM Theresa May by the pro-EU camp within the Tory party. Sterling pairs are expected to be sensitive to developments.

Politics are at play in Germany as well, where issues over migration are posing threats to Chancellor Merkel’s coalition.

On the trade front, the Trump administration’s decision on Friday to come one step closer to the imposition of tariffs on $50 billion in Chinese goods imported to the US, in conjunction with retaliatory actions of similar nature by China, are once again fueling the “trade war” narrative. Developments will be eyed, though it should be said that the market reaction as of late is such that indicates investors anticipate an eventual easing of tensions rather than a full-blown trade war.

Retiring New York Fed President William Dudley will be participating in a panel discussion at 1300 GMT. Starting today, up to now San Francisco Fed President John Williams, will replace him at the NY Fed; Williams will be giving a speech at the same venue as Dudley at 2000 GMT. The NY Fed President holds permanent voting rights within the FOMC. Of more importance in terms of policymakers’ appearances though is expected to be ECB President Mario Draghi’s comments at the ECB Forum on Central Banking in Sintra, Portugal (1900 GMT). In the coming days other important policymakers will be making public appearances at the forum, including Fed chief Jerome Powell and BoJ Governor Haruhiko Kuroda. Meanwhile, comments by Bank of Canada Deputy Governor Lynn Patterson are also on the agenda (1445 GMT).

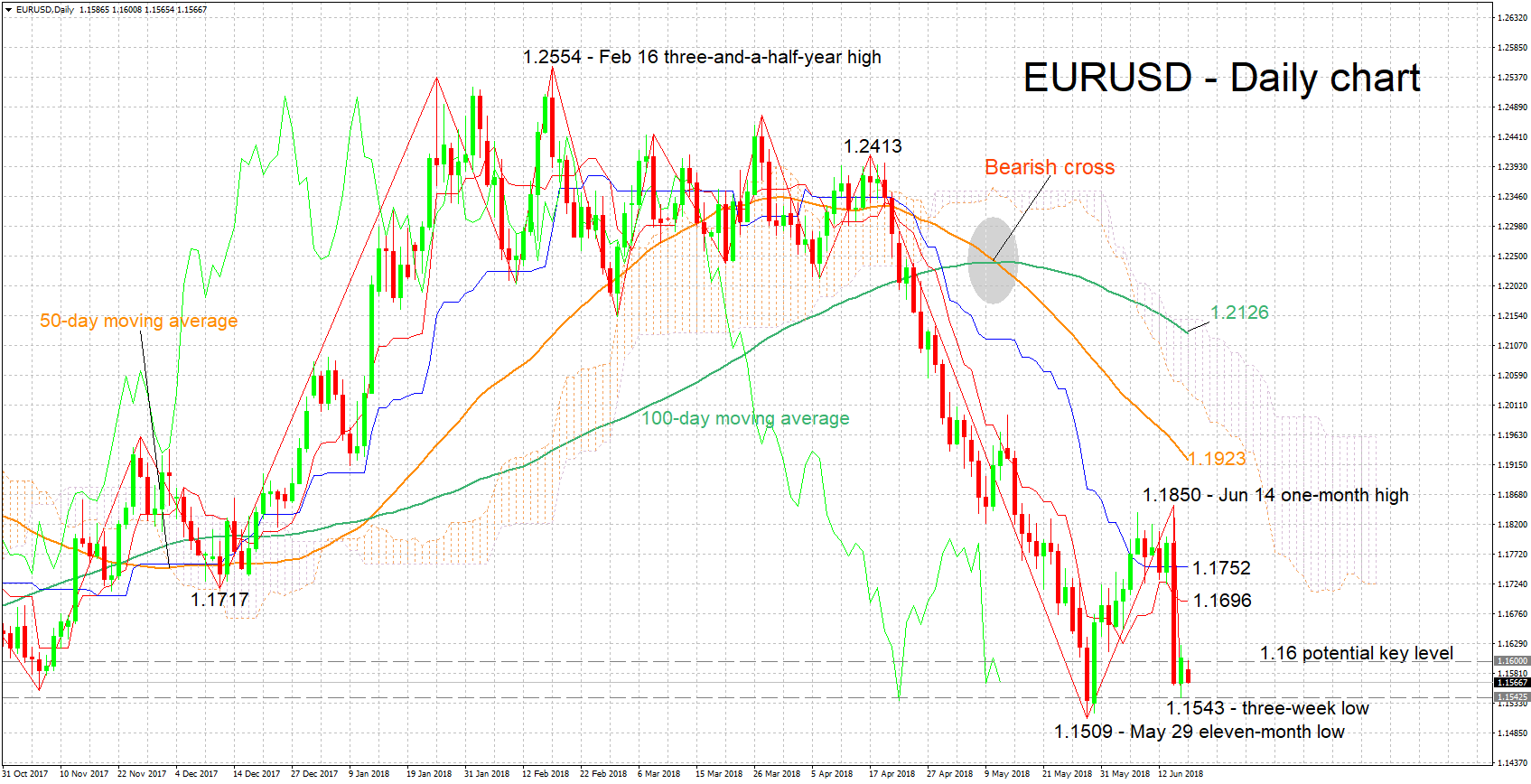

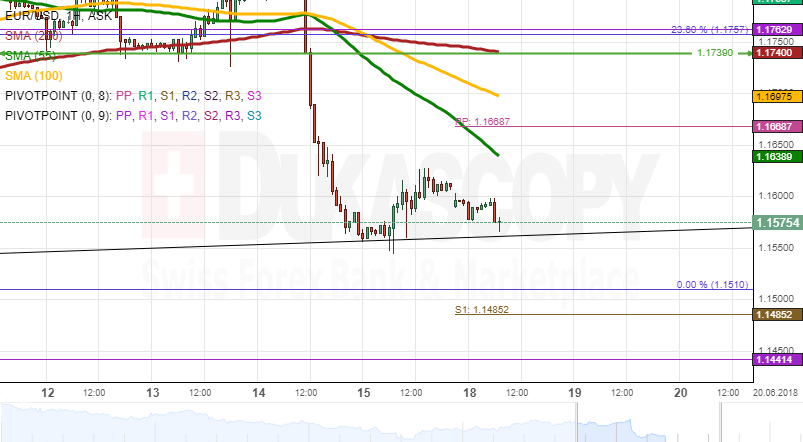

Technical Analysis: EURUSD bias remains to the downside, though negative momentum eases

EURUSD is trading not far above Friday’s three-week low of 1.1543. The negatively-aligned Tenkan- and Kijun-sen lines are pointing to the existence of a negative bias in the short-term. The flat Kijun-sen though is an indication that bearish momentum has eased.

Upbeat comments on the eurozone economy by ECB President Mario Draghi at the ECB Forum can lift the pair. Resistance could initially occur at the 1.16 round figure before the attention turns to the area around the current level of the Tenkan-sen at 1.1696.

A cautious tone though – as in last week’s ECB meeting – by the ECB chief is likely to push EURUSD further down. Support could come around last week’s three-week low of 1.1543, with a downside violation increasingly shifting the focus to the region around late May’s 11-month low of 1.1509.

EUR/USD Analysis: Fails To Accelerate From 1.16

After the massive 2.28% plunge against the US Dollar on Thursday, the common European currency was expected to accelerate during the following trading session. The pair did manage to gain some momentum during the first part of the day, but nevertheless failed to reach the 55–hour SMA near 1.1650.

The rate has remained fluctuating near the 1.16 mark since late Thursday. Despite showing mixed signals today, technical indicators are starting to recover from their lows. This could indicate to further upside potential today. This advance is not expected to be significant, as the Euro's movement on Friday does show that it has remained weak.

The session high should be the 100-hour SMA at 1.17, while a fall below its one-year low and the weekly S1 at 1.15 is very unlikely this week.

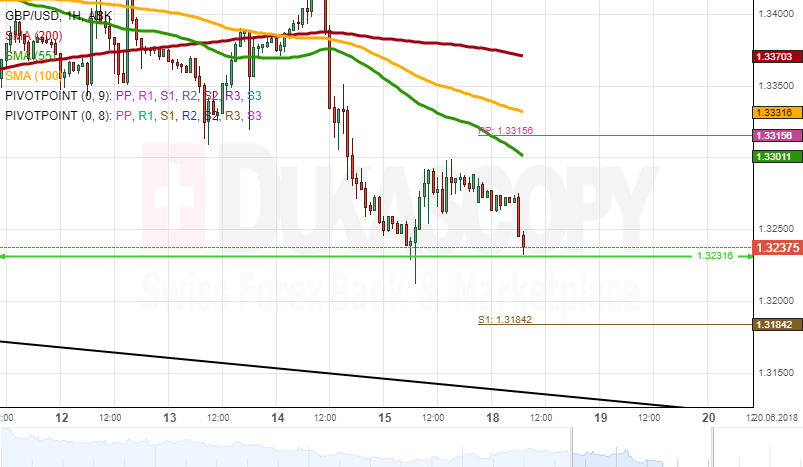

GBP/USD Analysis: Trades Below 1.33

The Pound continued to weaken against the US Dollar on Friday morning, thus re-testing its seven-month low of 1.3232. Bulls managed to move the rate slightly higher during the remaining part of the day, but a move above the psychological 1.33 level did not follow.

It is expected that the rate targets the upper channel line near 1.34 this week. In the meantime, this session might not result in significant advances due to several important resistance areas lying ahead. In addition, no fundamental data releases that could strengthen the bullish momentum are scheduled for this session.

Thus, today's highest point could be the 100– and 55-hour SMAs and the weekly PP at 1.3350. In case bears prevail, the 1.32 mark should remain intact.

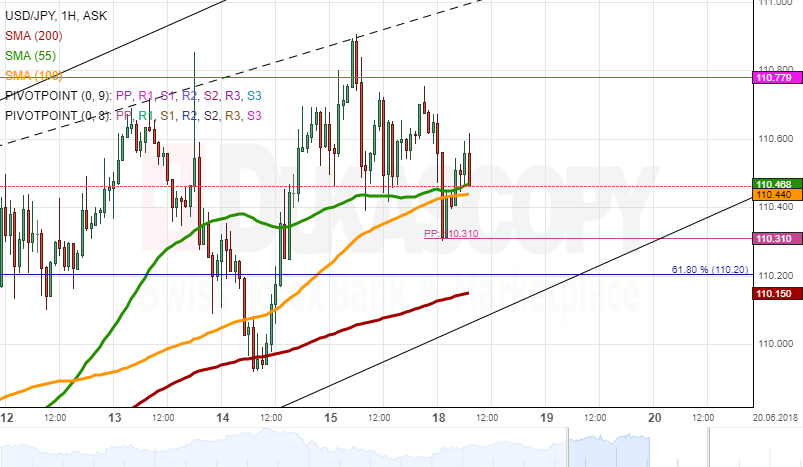

USD/JPY Analysis: Could Be Led By SMAs

USD/JPY was trading sideways on Friday, being restricted by the monthly R1 from above and the 55– and 100-hour SMAs—from below. The pair made a false breakout of the latter early today but nevertheless it had returned above this cluster by Monday morning.

The Greenback has diminished its trading range within a two-week ascending channel. This suggests that the pair might breach its lower boundary at 110.20, likewise reinforced by the 61.90% Fibonacci retracement and the 200-hour SMA, and move lower down to a more senior channel and the weekly S1 circa 109.70.

Meanwhile, technical indicators remain bullish for today. Under this scenario, the aforementioned SMAs should guide the pair higher towards the weekly R1 at 111.30.

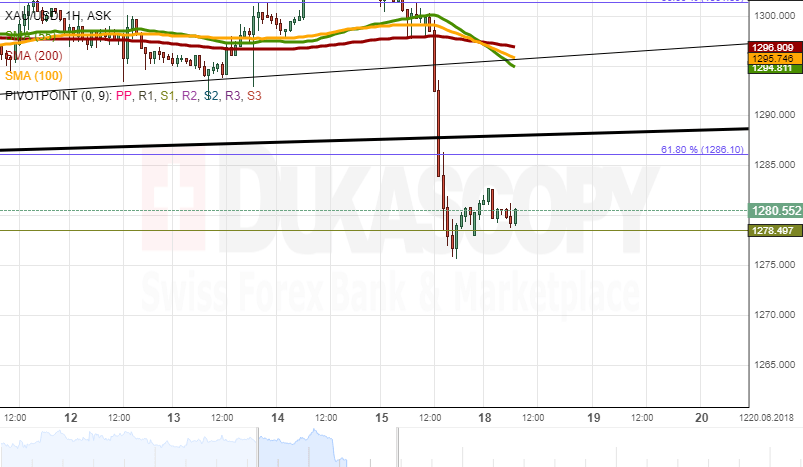

Gold Analysis: Plunges 1.81% On Friday

Gold lost value against the US Dollar significantly on Friday, thus closing the day with a 1.81% plunge. As a result, the commodity dashed through several important support levels, including the senior channel which was formed in November, 2016. This strong fall was stopped solely by the monthly S1 at 1,2878.50.

It is more likely that the bearish sentiment eases in this session, thus allowing bulls to gain some advantage in the market. The nearest significant resistance is the 55-, 100– and 200-hour SMAs near 1,300.00, while, in case of a weaker bullish momentum, Gold might likewise retrace from the breached channel line at 1,290.00 and subsequently move back lower.

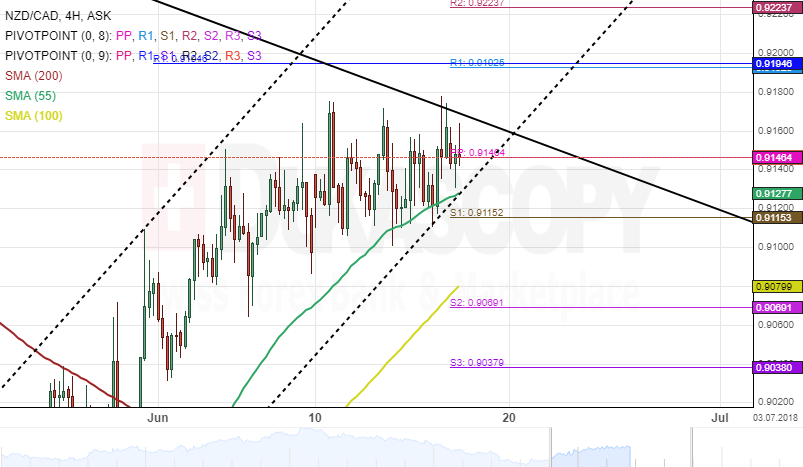

NZD/CAD 4H Chart: Sets For A Breakout

The NZD/CAD exchange rate has been trading in a narrow ascending channel since mid-May. The currency pair bounced off the lower boundary of the narrow pattern on May 15 and has since gained 390 base points.

The New Zealand Dollar has reached the upper boundary of a medium-term descending channel and could be prepared for a breakout within the next trading sessions.

If and when the aforementioned breakout occurs, the currency exchange rate could begin a new wave to the upside within the following week. However, the price movement first needs to surpass strong resistance cluster at 0.91 set by the weekly and monthly PPs.

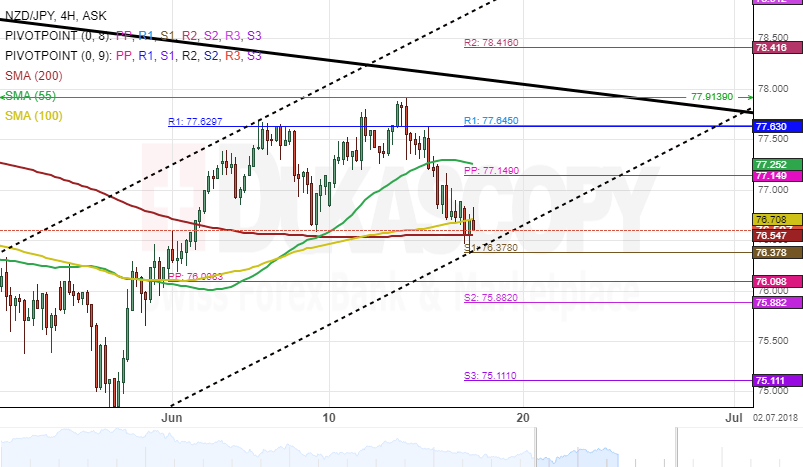

NZD/JPY 4H Chart: Finds Support

The price movement of the NZD/JPY exchange rate has been constrained by a junior ascending pattern. The currency pair re-tested the lower boundary of the ascending channel during the early hours of Monday's trading session.

A support level set by the weekly pivot point at 76.37 was providing support for the rate at the time of this analysis.

Everything being equal, it is likely that the currency exchange rate could bounce off the bottom border of the aforementioned ascending pattern and strengthen within the following trading sessions. Furthermore, bulls might target a strong resistance cluster at the 77.62 mark.

BOE Preview – Focus on June Meeting Minutes

Last month, BOE left the policy rate at 0.5% and the asset purchase program at 435B pound. It acknowledged the growth slowdown in the first quarter but noted that more information is needed to confirm whether it was driven by temporary factors. Although deputy governor Dave Ramsden suggested earlier this month that the intermeeting data has “confirmed” that the first quarter slowdown was driven by temporary factor, i.e., adverse weather condition, we believe moderation in inflation and lukewarm wage growth would likely keep the central bank on the sideline. Six weeks’ data since the last meeting would not be sufficient for the central bank to change its stance. Equally, the incoming data since then cannot justify the central bank's “temporary factor” rhetoric.

Inflation has been softening after BOE’s rate hike last November. In May, both headline and core CPI stayed unchanged at 2.4% y/y and +2.1%, respectively. These are compared with recent peaks of +3.1% and +2.7% in November last week. Meanwhile, RPI eased -0.1 percentage point to +3.3% y/y in May from a month ago. The key contributor to the moderation was housing price, of which the ONS index dropped to a weak 3.9% y/y. Overall, the inflation report suggests that the worry about inflation overshooting is behind us and BOE is far less obliged to raise the policy rate to ease the price level when compared with 2H17. On the job market, claimant count dropped -7.7K in May, better than expectation of 11.3K rise. Unemployment rate stayed unchanged at 4.2% in the 3 months through April, the lowest rate since 1975. However, wage growth remained lukewarm. Average weekly earnings, including bonus, slowed to +2.5% y/y during the period, worse than both consensus and March’s reading of +2.6%.

Concerning different sector activities, the Markit report shows that manufacturing PMI recovered in May, climbing higher to 54.4 from April’s 17-month low of 53.9. While staying in the expansionary territory, both April and May readings are still lower that the average 54.9 in 1Q18. The services PMI improved to 52.8 in April and then to 54 in May, from 51.7 in March. The average reading for April and May, at 53.4, is only mildly higher than first quarter’s average of 53.07. We find it difficult to confirm from these indicators that the disappointment in 1Q18 is over.

Deputy governor Dave Ramsden is convinced that "the data we have had so far suggests our interpretation of the slowdown in Q1 as temporary looks to be being borne out”. He noted that “consumer confidence and consumer credit both picked up in the latest data, as did retail sales and several business surveys. That included the latest services [Purchasing Managers’ Index] output balance, representing 80% of the economy. So far at least our May judgement looks on track”. This view is not shared by the statistics department. With the second estimate of the GDP staying unrevised at +0.1%, ONS’s head of GDP Rob Kent-Smith suggested that, “the economy performed poorly in the first quarter” overall. While admitting that “poor weather” hit “construction and high street shopping”, he noted that “this was offset to an extent by increased energy supply and online sales”. The ONS believes that there was evidence of an underlying growth slowdown in the first quarter.

The June meeting does not include updated economic projection or a press conference. As such the meeting minutes would be in focus, serving as an indicator for the likelihood of an August rate hike. If hopes of an August rate hike falter, the chance of a November hike would be more remote. Hawkish Ian McCafferty is leaving the Committee and would be replaced by Jonathan Haskel, an Imperial College Business School professor.

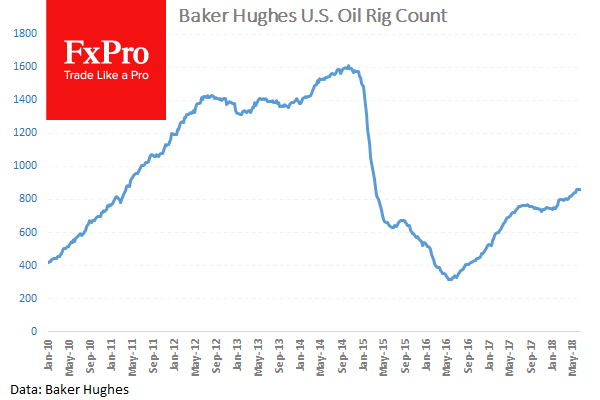

Oil Down Over 4% From Friday’s Open As OPEC Plans To Discuss Production Output In Vienna This Week

OPEC and non- OPEC members are meeting in Vienna on Thursday for the start of a 3 day summit where production cuts are on the agenda. US Rig counts on Friday showed an increase of 1 to 863 as more US production comes online. The market expects production cuts to be eased adding more supply to the market and putting downward pressure on prices. The meeting is set to be contentious as Saudi Arabia and Russia are said to back the proposal to increase production by 1.5 million barrels per day, in order to maintain their market share, while Iran, Iraq and Venezuela are set to block the proposal fearing lower prices and market instability. USDCAD traded higher to the 1.32000 level as Oil fell.

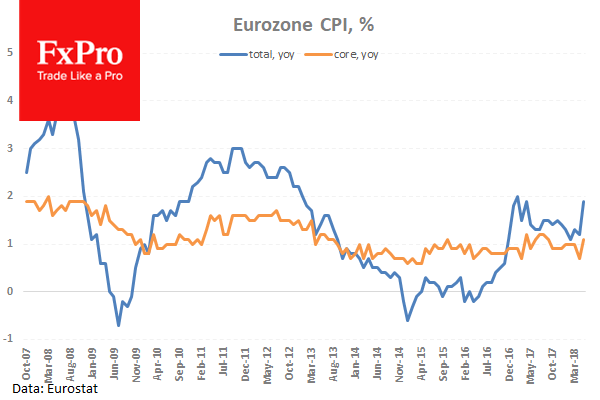

Eurozone Consumer Price Index (Apr) was released and came in at 0.5% (MoM) and 1.9% (YoY) with a consensus for 0.5% (MoM) and 1.9% (YoY) from 0.3% (MoM) and 1.9% (YoY) previously. Consumer Price Index – Core (Apr) was 0.3% (MoM) and 1.1% (YoY) against an expected at 0.3% (MoM) and 1.1% (YoY) from 0.2% (MoM) and 1.1% (YoY) prior. Labour Cost (Q1) was 2.0% against an expected 1.9% from 1.5% previously which was revised down to 1.4%. CPI data showed an increase on the monthly figures from the previous but was in line with consensus, while yearly figures came in as expected and remained in line with the previous reading. EURUSD rose from 1.15862 to 1.16149 due to this data.

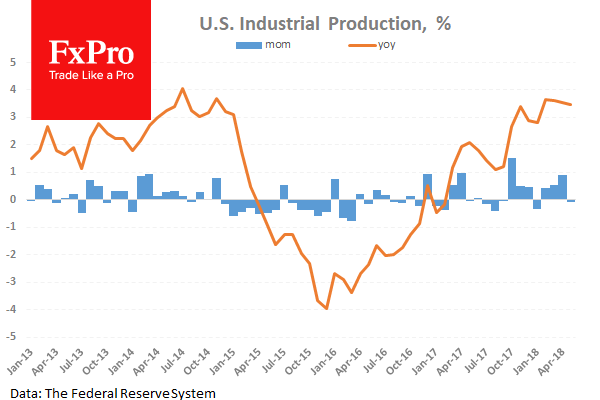

US Industrial Production (MoM) (May) was released and came in at -0.1% against the consensus of 0.2% from 0.7% previously which was revised up to 0.9%. This measure slipped below the zero line against to the level of the February low at -0.1%. Capacity Utilization (May) was also released at this time coming in at 77.9% against an expectation for 78.1% from 78.0% previously which was revised up marginally to 78.1%. The number remains close to the two year high from December and the 80.0% mark. USDJPY moved from a low of 110.408 to 110.648 following the data release.

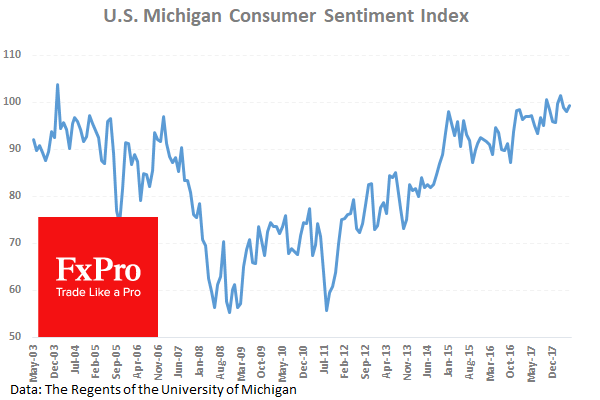

US Michigan Consumer Sentiment Index (June) was 99.3 against an expected 98.5 from a previous 98.0. The March reading was a record high for the index at 102.0 and the data is showing the number holding under the 100.0 level since. The data came in above expectations for the second month in a row showing consumers are financially confident. GBPUSD moved higher from 1.32599 to 1.32976 after the data release.

EURUSD is down -0.10% overnight, trading around 1.15941.

USDJPY is down -0.13% in the early session, trading at around 110.500

GBPUSD is down -0.03% this morning trading around 1.32708

Gold is down -0.10% in early morning trading at around $1,279.68

WTI is down -0.62% this morning, trading around $63.76

Central Bank Representatives Dominate Today’s Calendar

At 12:45 GMT, US Fed's William Dudley is scheduled to give a speech today. Comments made can move prices in USD crosses.

At 17:00 GMT, FOMC Member Bostic is due to speak about the economic outlook and monetary policy at the Rotary Club of Savannah. Audience questions are expected to follow. USD crosses can be impacted from this event.

At 17:30 GMT, ECB President Mario Draghi is due to deliver opening remarks at the ECB Forum on Central Banking, in Portugal. EUR crosses can be impacted by any comments made.

At 20:00 GMT, US FOMC Member Williams is due to deliver closing remarks at a conference on banking culture, hosted by the Federal Reserve Bank of New York. USD pairs can react to this event.

Major data releases for the week ahead:

On Tuesday at 01:30 GMT, Reserve Bank of Australia's meeting minutes will be released.

At 08:00 GMT, ECB President Mario Draghi will be speaking.

On Wednesday at 00:00 GMT, Bank of Japan Monetary Policy Meeting Minutes will be published.

At 13:30 GMT, US FED's Powell, ECB's Draghi, BOJ's Kuroda and RBA's Lowe are due to participate in a panel discussion at the ECB Forum on Central Banking, in Portugal

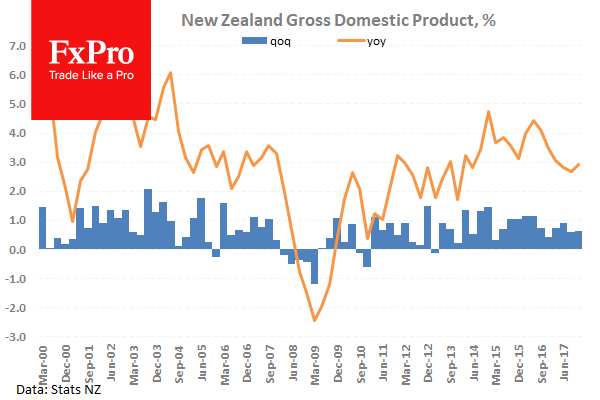

At 21:45 GMT, New Zealand GDP data will be released.

On Thursday at 07:30 GMT, SNB Interest Rates Decision will be released with a Press Conference to follow at 09:00 GMT.

At 11:00 GMT, BOE Interest Rate Decision will be announced along with the Meeting Minutes and Monetary Policy Summary.

Tentative – OPEC are meeting for a 3 day summit in Vienna.

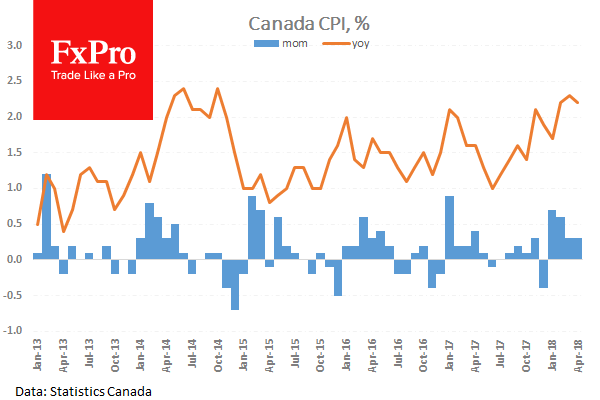

On Friday at 12:30 GMT, Canadian Retail Sales and CPI data will be released.