Sample Category Title

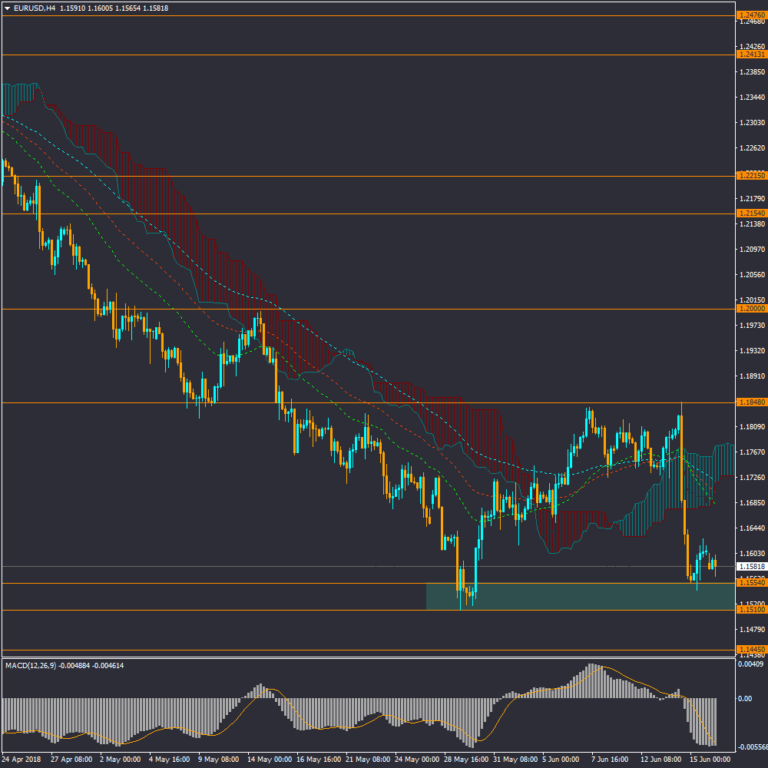

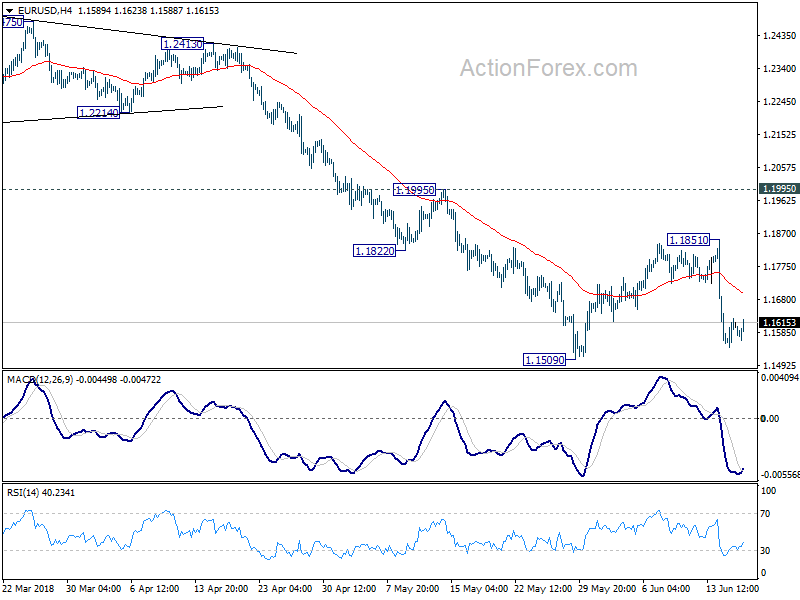

EURUSD, ECB Chairman Mario Draghi Will Be Speaking Today In Portugal And Is Expected To Affect Overall Market Volatility

Last week, the Council of the ECB Monetary policies announced a timetable for declining quantitative easing (QE). The announcement predicted an increase in interest rates starting second half of 2019 which led to a decline in demand for the euro in the market. The Eurozone inflation rate (CPI) was also announced to remain unchanged at 1.9%. In addition, ECB Chairman Mario Draghi will be speaking today in Portugal and is expected to affect overall market volatility.

On the other side of the Atlantic, the announcement of more contraction policies by the Federal Reserve led to an increase in demand for the US Dollar.

The Potential Reversal Zone (PRZ) is defined by the two support levels of 1.1554 and 1.1510, with the price reacting to this range significantly, on a mid-term trend basis. The price is expected to decline with a bearish trend in the short term. The support levels are 1.1554, 1.1510 and 1.1445, and the resistance levels are 1.1848, 1.2 and 1.2154 against the price increase.

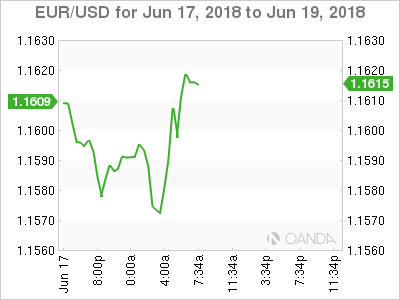

Into US session: Euro recovering post ECB losses

Entering into US session, Euro receives a wave of buying in the current 4H. It's probably already past the first post-ECB selling climax.

Still, upside momentum is not too convincing as seen in EUR Action Bias table.

We've mentioned here out hesitation on selling EUR/USD right after ECB as D action bias didn't turn downside red. And it happened that D action bias is still staying in neutral green.

Though, the overall outlook stays bearish in EUR/USD and it's just a matter of time for downside breakout. Hence, we'll stick with a safer strategy to sell EUR/USD at 1.1700, slightly above 4 hour 55 EMA, with stop above 1.1851 resistance.

Dollar Rises On Falling Risk Appetite

Monday June 18: Five things the markets are talking about

Global trade is again top of capital markets agenda, as dealers and investors are now officially worried about the intensifying confrontation between the U.S and China.

Global equities are trading under pressure over the escalating protectionist standoff between the two largest economies, along with crude oil prices ahead of this week significant OPEC meeting (June 22). The U.S dollar remains supported while U.S Treasuries are steady.

President Trump approved tariffs of +25% on about +$50B of Chinese goods on Friday, prompting Chinese officials to hit back by announcing the country would levy penalties of the same rate on U.S goods of the same value. Coupled with the concerns about the fate of the Nafta and tariffs imposed on European allies are also adding to investor anxiety.

Again this week, the market is also looking to central bankers for further guidance on monetary policy after the Fed and the ECB both held meetings last week. The Bank of England (BoE) and Swiss National Bank (SNB) are meeting on Thursday (June 21). No rate hikes are expected.

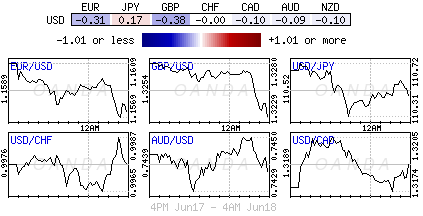

In currencies, the EUR (€1.1587) remains under pressure as a migration policy crisis threatens German Chancellor Merkel's coalition, while the pound (£1.3235) has ticked lower ahead of a parliament debate on the Brexit withdrawal bill.

On tap: AUD monetary policy minutes (June 18), NZD GDP (June 20), SNB & BoE monetary policy decision (June 21), OPEC (June 22/23)

1. Stocks see red

In Japan, market worries over how the trade spat between the U.S and China will play out supported the yen (¥110.53) and helped pressure domestic stocks. The Nikkei fell -0.75%, helped by the energy/coal segment sinking another -3.7%, while the broader Topix index fell the most in almost three-weeks after a strong earthquake hit Osaka, one of Japan's industrial heartlands.

Down-under, Aussie shares finished slightly higher overnight as gains in financials and real estate stocks outweighed a fall in materials stocks on lower commodities prices. The S&P/ASX 200 index close up at +0.2%. The benchmark rose +1.3% on Friday. In S. Korea, the Kospi fell amid fears of an escalating Sino-U.S trade spat, the index was down -1.15%.

Note: Markets were closed for the holidays in China and Hong Kong.

In Europe, regional bourses trade broadly lower as trade concerns keep risk appetite muted. German stocks continue to be impacted by political concerns over immigration disagreement in CDU/CSU coalition.

U.S stocks are set to open deep in the 'red' (-0.4%).

Indices: Stoxx50 -0.7% at3,486 , FTSE -0.1% at 7,628, DAX -0.8% at 12,912, CAC-40 -0.6% at 5,470; IBEX-35 -0.4% at 9,810, FTSE MIB -0.3% at 22,142, SMI -0.9% at 8,570, S&P 500 Futures -0.4%

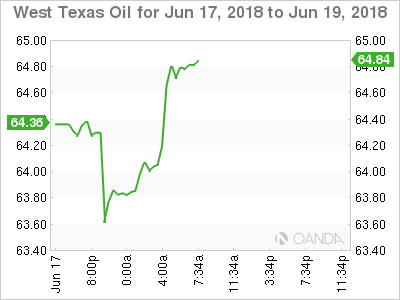

2. Oil down on China tariffs, expected OPEC supply rise

Oil has extended its decline as Saudi Arabia and Russia prepare for a clash with other OPEC members and allies over whether to raise production. Not helping the cause is China threating to impose duties on U.S crude imports in their trade dispute.

Note: U.S oil exports have rocketed in the past 24-months as shale oil production has surged, with China becoming one of the biggest customers of American crude.

North Sea Brent is down -36c at +$73.08 a barrel, while U.S light crude oil has printed a two-month low of +$63.59 a barrel before edging back to +$64.00, down -$1.06.

OPEC meets June 22 and 23 in Vienna where they will debate output policy. Saudi Arabia and Russia are saying that production should be increased “gradually” if deemed necessary.

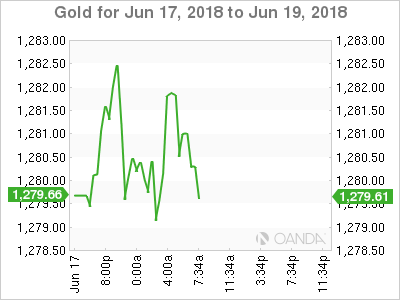

Ahead of the U.S open, gold prices have inched higher overnight after falling to a six-month low on Friday, as a Sino-U.S trade dispute triggered safe-haven buying, but a strong U.S dollar has put a cap on the upside for the time being. Spot gold has edged up +0.1% to +$1,279.70 per ounce. U.S gold futures for August delivery are up +0.3% at +$1,282.10 per ounce.

3. Eurozone bond yields trade little changed

Eurozone government bond yields are little changed overnight, with yields atop of their low levels after the ECB's commitment last week to keep interest rates at present levels through summer 2019.

Note: A three-day ECB forum kicks off in Portugal today and gives the ECB the opportunity to give markets further guidance on their plans to wind down QE later this year. ECB chief Mario Draghi speaks later in the day.

The 10-year German Bund yield is trading +0.05 bps higher at +0.40%. However, the dealers are expecting Bund yields to come under further pressure this week, as eurozone bond supply will be significant this week.

Note: Both Slovakia and Belgium to auction bonds later today.

Elsewhere, the yield on 10-year Treasuries decreased -1 bps to +2.92%, the lowest in more than two-weeks. In the U.K, the 10-year Gilt yield dipped -1 bps to +1.328%, reaching the lowest in almost two weeks on its fifth straight decline.

4. Dollar rises on falling risk appetite

The 'mighty' dollar remains better bid on safe-haven demand as the market become more risk averse due to escalating global trade war fears after the U.S imposed tariffs on China. China has retaliated, pushing U.S President Trump to up 'his' ante with perhaps even more tariffs.

Which two of these economies has a greater staying power in a drawn out trade war?

EUR/USD (€1.1596) trades just below the psychological €1.1600 handle as the dollar approaches a seven-month high as continued trade tensions weigh. For the 'bears,' the appetite for “carry” trades is likely to go up after the ECB said last week it would not raise interest rates at least until after the summer of 2019.

GBP/USD (£1.3255) is also weaker on dollar strength ahead of this weeks BoE's rate decision. Dealers expect the pound's price action to be rather muted until Thursday.

5. Italian trade surplus

Data this morning showed that Italy's trade surplus totalled +€2.938B in April.

Digging deeper, the surplus with non-E.U. countries was at +€1.861B and the surplus with E.U countries at +€1.077B.

In the first four months of the year, the trade deficit totalled -€10.470B. However, ex-energy products, the trade surplus reached +€22.975B.

Trade Concerns Key Focus As European Indices Decline

Notes/Observations

- Oil prices rise on reports of OPEC lifting output by 300-600Kbpd

- Overall weakness in European Indices with trade tensions weighing

Asia:

- China Commerce Ministry: to impose additional 25% tariff on chemicals, medical equipment, energy products, commodities from U.S. in response to tariffs set by the US, threatens to levy tariffs on US crude oil, nat gas and other energy products

- (CN) China PBOC reiterates view that monetary policy to be prudent and neutral; to stabilize market expectations

- Market participation limited by holidays in China, Hong Kong and Taiwan

- Earthquake rocks Osaka Japan region, more than 200 reported injured, so far no reports of issues with nuclear plants or major damage; several companies closing production plants to assess damages

- Google to invest $500M into JD.com for 21.1M class A shares At $20.29/shr or $40.58/ADS in a strategic partnership

Europe:

- The CSU party is said to have denied a German press report which suggested that the party would give Merkel 2 weeks (until the EU summit) before making a decision on the immigration plan.

- UK PM May outlines plans to increase spending on healthcare, which will rise by £20B by 2023, through money saved from being out the EU and increased contribution from voters.

Energy:

- Iran’s OPEC Rep Kazempour Ardebili: Iran will block OPEC output raise (Note Saudi Arabia can bypass veto)

- OPEC reportedly considering an output hike of 300-600K bpd

Economic Data:

- (IT) Italy Apr Trade Balance: €2.9B v €4.5B prior; Trade Balance EU: €1.1B v €0.7B prior

- (CZ) Czech May PPI Industrial M/M: 1.0% v 0.5%e; Y/Y: 1.5% v 1.0%e

- (TR) Turkey Mar Unemployment Rate: 10.1% v 10.6% prior

- (PL) Poland May Employment M/M: 0.0% v 0.0%e; Y/Y: 3.7% v 3.8%e

- (CH) SNB Total Sight Deposits for Week Ended Jun 15th

- (CHF): 576.5B v 576.3B prior

Fixed Income Issuance:

- Non seen

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx50 -0.7% at 3,486, FTSE -0.1% at 7,628, DAX -0.8% at 12,912, CAC-40 -0.6% at 5,470; IBEX-35 -0.4% at 9,810, FTSE MIB -0.3% at 22,142, SMI -0.9% at 8,570, S&P 500 Futures -0.4%]

- Market Focal Points/Key Themes: European markets open broadly lower continued in that direction as the session progressed; FTSE 100 only exchange to open higher, but later moved to the downside; trade concerns keep risk appetite muted; German equities impacted by political concerns over immigration disagreement in CDU/CSU alliance; technology stocks and utilities underperformers; financial sector performing marginally positive;Trukey closed for holiday; CYBG confirms takeover of Virgin Money; Nexans cuts outlook impacting telecom sector in Italy

Equities

- Consumer discretionary: Koovs KOOV.UK +16.3% (results), Norwegian Air NAS.NO +10.4% (Lufthansa contact)

- Energy: Engie ENGI.FR -2.1% (cuts outlook)

- Financials: CYBG CYBG.UK -1.0% (confirms deal with Virgin Money), Virgin Money CM.UK -2.7% (takeover deal)

- Industrials: Enav ENAV.IT +1.2% (analyst action)

- Technology: Nexans NEX.FR -16.2% (outlook)

- Telecom: Prysmian PRY.IT -1.8% (sympathy with Nexans)

Speakers

- (DE) German CSU's Soeder (Prime Minister of Bavaria): Want to support provision in immigration masterplan to turn away migrants at border; Will make decision on migration policy today, then the federal interior minister will decide how he implements it

- (UK) UK Foreign Sec Johnson: NHS funding boost will come from vibrant economy as well as discontinuing payments to Brussels

Currencies

- EUR/USD trades slightly lower hovering below 1.16 as the dollar approaches a 7 month high as continued trade tensions weigh. GBP/USD is also weaker on dollar strength ahead of this week's Bank of England rate decision.

Fixed Income

- Bund Futures trade 22 ticks higher at 161.22 as Merkel’s position as German leader is under threat over immigration split. Upside targets 161.75 followed by 162.50, while a return lower targets the 158.75 level.

- Gilt futures trade at 122.66 higher by 6 ticks near the midpoint for the month of June. Support continues stands at 120.75 then 119.25, with upside resistance at 122.85 then 123.35.

- Monday's liquidity report showed Fridays's excess liquidity fell from €1.887T to €1.862T. Use of the marginal lending facility rose from €65M to €95M.

- Corporate issuance as the primary market saw $23.9B issued last week

Looking Ahead

- 10:00 (US) Jun NAHB Housing Market Index: No est v 70 prior

- 16:00 (US) Weekly Crop Progress Report

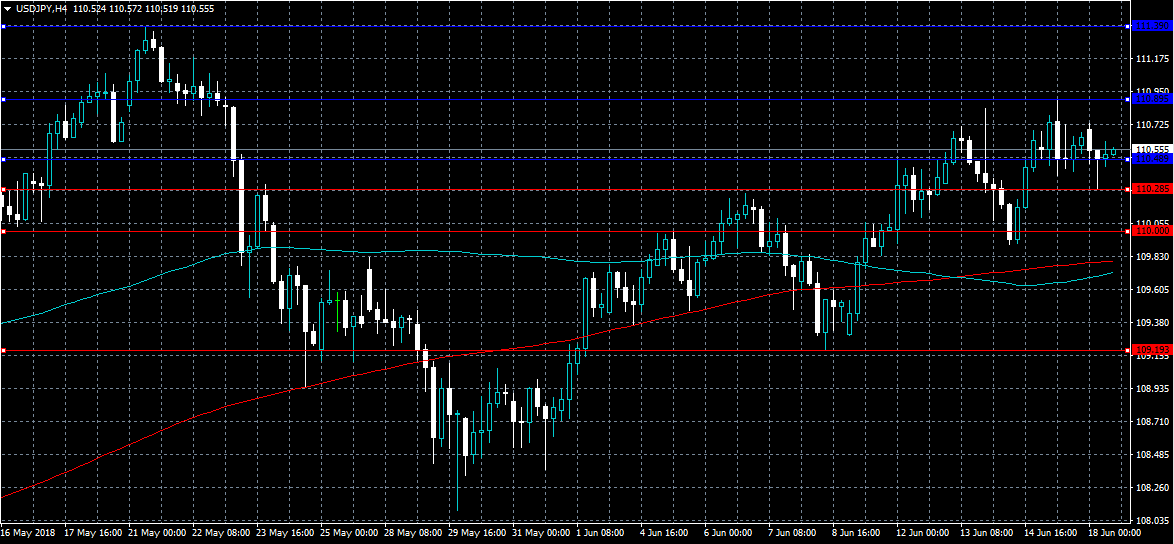

USDJPY Dip Buyers In Control

The US dollar continues to remain well bid against the Japanese yen currency, with dip buyers earlier moving in from the 110.28 support level. Price action currently trades around the 110.55 region, with the USDJPY pair retaining its intraday bullish bias while price holds above the 110.48 level. Traders now look to scheduled speeches from Federal Reserve members Bostic and Williams.

The USDJPY pair is intraday bullish while trading above the 110.48 level, key technical resistance remains at the 110.89 and 111.39 levels.

If the USDJPY pair moves below the 110.48 level, key intraday support is found at the 110.28 and 110.00 levels.

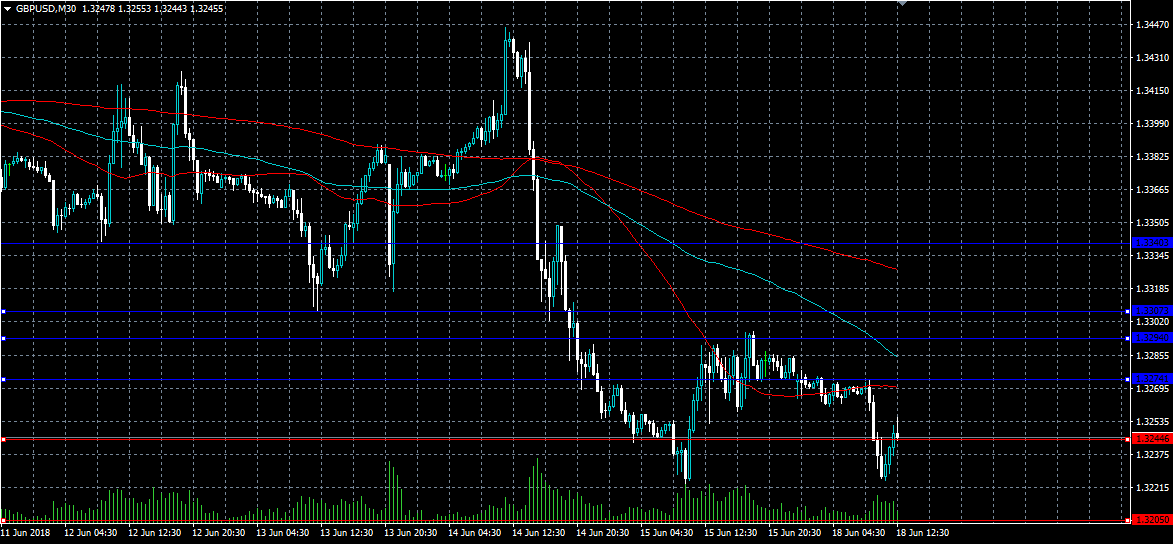

GBPUSD Further Bearish Below 1.3244

The British pound earlier staged a weak recovery against the US dollar, hitting 1.3274, with sellers now using any moves higher in sterling as a selling opportunity. The GBPUSD pair currently trades around the key 1.3244 level, after finding interim weekly support at the 1.3224 level. Sellers will now try to break the 1.3200 level, while buyers will try to hold price above the 1.3244 level.

The GBPUSD pair is strongly bearish while trading below the 1.3244 level, key technical support is now located at the 1.3224 and 1.3200 levels.

If the GBPUSD pair holds above the 1.3244 level, further upside towards the 1.3274 and 1.3294 levels remains possible.

Forex Analysis: S&P 500 And Nasdaq 100

Asian equities were hit overnight on fears of a trade war between the world’s top two economies with US equities set to open lower today. On Friday, the US unveiled a list of $50bn in Chinese goods which will attract 25% tariffs and threatened more duties if China retaliated. Within a few hours China released its own list of retaliatory tariffs on US imports. The tit-for-tat tariffs have brought the two powers a step closer to a full-blown trade war and this will likely be the immediate focus for markets. This week looks relatively light on economic events compared to last week, which saw both the North Korea summit and a Federal Reserve rate hike. However, the Organization of the Petroleum Exporting Countries (OPEC) will meet in Vienna on Friday which will be watched for news of changes to output.

S&P 500

On the daily chart, the S&P500 (SPX) turned lower from the zone of resistance between 2785-2800. On Friday, the index fell significantly during the trading session but did find enough support to turn things around and form a hammer. However a break of 2800 will be needed for a continuation towards 2820 and then new all time highs. Any retracement will find support 2760 and then 2740.

Nasdaq 100

On the daily chart, the Nasdaq 100 (NDX) again broke to new all time highs last week. The index is trading in a potential ascending wedge and if broken could lead to a correction. A break of 7190 could open the way for a move lower to support at 7130 followed by the 23.6% retracement of the lows in April at 7050. However, as long as 7190 holds, another test of the high at 7290 is possible and a break should see the index push towards 7340.

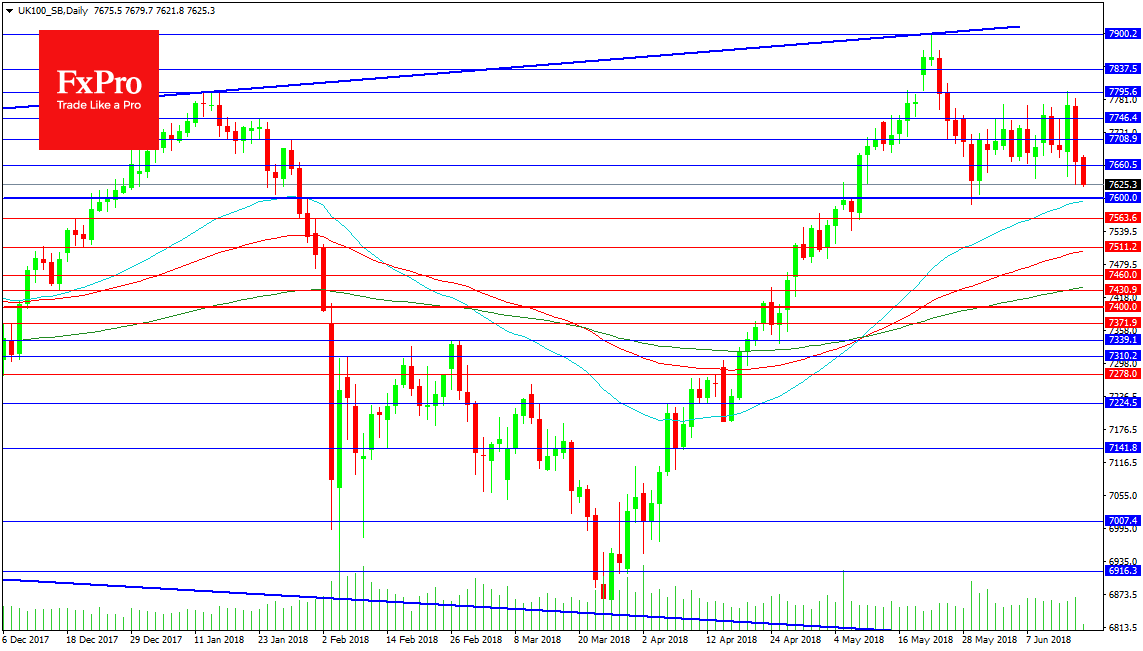

Forex Analysis: FTSE100

The UK 100 Index is moving lower again today after a horrid selloff on Friday. The retracement from the high at 7900.00 on the 22 of May merged into a sideways consolidation pattern if not an outright bear flag over the last month and we are on the verge of accelerating the move down with a break of support at 7600.00. This level is quite significant as it contains the 50 DMA and is just above the recent swing low at 7589.5. The next support below on the daily chart is the 100 DMA at 7503.6 with the 200 DMA at 7436.6. These levels represent quite achievable targets with 7300.00 being the ultimate target if a bear flag is triggered. Beyond that 7000.00 comes into focus.

The bulls are down but not yet out with the potential for significant supply in the 7600.00 area. A move higher needs to erase Friday’s candle which is a tall order but spread over a number of sessions, it can be achieved. The 7700.00 level represents a minor hurdle while 7800.00 would swing the balance with bearish stops above the level. Building on this success would be a retest of 7900.00 followed by a test of 8000.00. Bulls may wish to take profit if this milestone is reached with higher level becoming targets for later in the year.

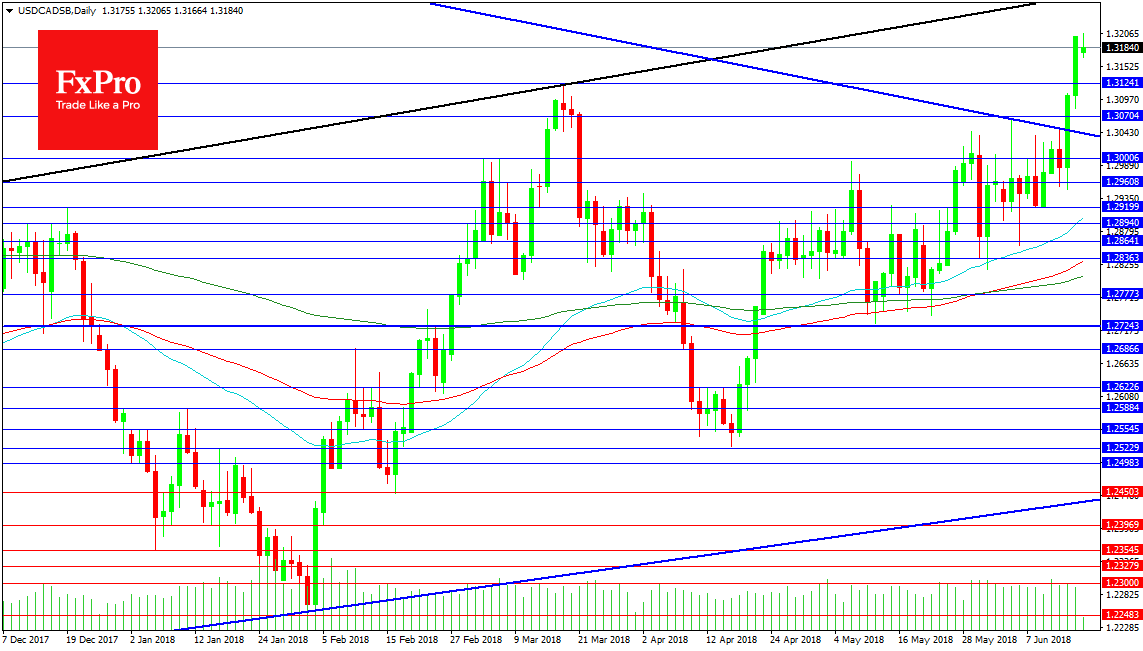

Forex Analysis: USDCAD

The Oil market is on the back foot at present after a large decline on Friday from the highs at $67.00. The selloff came in advance of the OPEC meetings this week where production cuts are to be discussed. Trade negotiations with the US are also affecting the price of the pair along with Economic data from both countries and the Fed’s path of rate hikes. The market broke higher from the falling blue trend line on Thursday around 1.30450 with a strong move that continued into Friday’s trading session. The high reached this morning was 1.32063 with prices currently just off the highs. Resistance is found at the black rising trend line at 1.32630 with the 1.33000 level beyond.

Support for the pair comes in at 1.31240 followed by 1.31000 and the 1.30700 level. The falling blue trend line that was broken on Thursday is currently positioned at 1.30428 and a retest of this line should be supported particularly by the 1.30000 level. The 50 DMA is found at 1.29000 and a loss of this level puts the uptrend under a little pressure. The 100 DMA and 200 DMA should add strength to the 1.28000 level on any decline. There is strong support in the 1.27243 area and a drop under this line can see 1.26000 or 1.25000 tested.

Abe’s advisor Kawai: Alliance with US changed to a transactional one under Trump

Katsuyuki Kawai, a ruling Liberal Democratic Party (LDP) lawmaker who advises Prime Minister Shinzo Abe on foreign affairs, raised his "personal" concern over the change in US foreign policy under Trump. He said in a Reuters interview that the alliance between Japan and the US has "changed from one based on shared values to a transactional alliance." And, "this is the reality now". He also pointed to the Kim-Trump submit and said it "will serve as a trigger for the Japanese people to begin to realize that it is risky to leave Japan's destiny to another country."

An unnamed Japanese government source also said "trade is more worrisome," and "it's getting worse ... There is no reliable (U.S.) cabinet level person who can say 'No' to unreasonable proposals."

The Nikkei business newspaper also criticized in a weekend analysis that "Mr. Trump mixes up economics and security with the mind-set of a real estate deal is a big cause for concern".