Sample Category Title

Gold Under Pressure After Sharp Drop From $1300

Gold is trading sideways in the Monday session. In North American trade, the spot price for one ounce of gold is $1278.63, down 0.09% on the day. It’s a quiet start to the week, with no major releases out of the U.S. On Tuesday, the focus is on construction numbers, with the release building permits and housing starts.

Are we heading for a global trade war? The markets are certainly concerned after U.S President Trump imposed further tariffs on some $50 billion of Chinese products on Friday. China has promised to retaliate against U.S imports, as trade ties between the world’s two largest economies continue to deteriorate. With the U.S recently slapping tariffs on the EU, Mexico and Canada, it is no wonder that investor anxiety has risen.

Tariffs aside, trade negotiations on the NAFTA agreement remain deadlocked. Canada is deadset against a U.S demand for a sunset clause after five years, which would require the parties to hammer out a new agreement. As well, Mexico and Canada are not happy with U.S demands to raise the American content of any vehicle produced in any of the three countries, which would significantly alter the NAFTA auto pact. Mexico is holding general elections on July 1, and a left-wing candidate, Andrés Manuel López Obrador, leads in the polls. If López Obrador becomes president, it could mean even more complications for the NAFTA talks.

Eco Data 6/19/18

[php_everywhere instance="1"]

Japanese yen edges lower on Weak Trade Balance

The Japanese yen has inched lower in the Monday session. In the North American trade, USD/JPY is trading at 110.45, down 0.19% on the day. On the release front, Japan surprised the markets by posting a trade deficit, the first in three months. The reading of -0.30 trillion yen was well off the forecast of a surplus of 0.14 trillion yen. There are no major U.S indicators on the schedule. On Tuesday, the focus is on construction numbers, as the U.S releases building permits and housing starts. Japan will release the minutes of the May policy meeting.

Investor risk appetite has waned after U.S President Trump imposed further tariffs on some $50 billion of Chinese products. China has promised to retaliate against U.S imports, as trade ties between the world’s two largest economies continue to deteriorate. With the U.S recently slapping tariffs on the E.U and the NAFTA talks in pause mode, it is no wonder that investor anxiety has risen. If the trade war between the U.S and its partners continues to escalate, the Japanese economy, which relies heavily on exports, could weaken and drag down the Japanese yen.

There were no surprises at Thursday’s Bank of Japan policy meeting. Policymakers maintained interest rates at -0.10%. The bank also downgraded its inflation forecast to a range of between 0.5% and 1.0%, underscoring that the massive stimulus program has failed to raise inflation anywhere near the bank’s target of around 2 percent. The Bank of Japan has stubbornly held onto its inflation target, even though there is little chance that the target will be met anytime soon. The recent improvement in the economy has stirred some debate about tapering stimulus, but the cautious BoJ is unlikely to make any such moves in 2018.

Potential U.S. Auto Tariffs: Canadian Scenario Analysis

Highlights

- U.S. President Donald Trump has initiated an investigation of American imports of motor vehicles and parts on national security grounds - the same basis that was used to justify tariffs on steel and aluminum.

- Assuming that the ultimate outcome of the investigation is the imposition of tariffs of a similar magnitude, the impact on Canada would be significant. 2019 growth would be reduced by half a percentage point as the economy stagnates for two quarters.

- Business investment is the most significantly impacted, creating permanent 'scarring' that reduces Canada's long-run economic capacity.

- Given the concentration of the auto sector, Ontario bears the brunt of the impact, with growth reduced by as much as two percentage points. Significant job losses also occur - up to 1 in 5 Ontario manufacturing jobs could be at risk.

- This analysis includes only direct impacts. Supply chain and income shocks could magnify the economic impacts.

Importantly, the scale of the impact will depend on the tariffs imposed (if any). More modest tariffs would moderate the outcomes presented. - TD Economics' baseline outlook remains that NAFTA disputes are ultimately resolved. The scenario presented here should only be taken as a 'what if' analysis, underscoring the importance of the ongoing negotiations.

On May 23, the U.S. Department of Commerce began a 'Section 232' investigation of automotive imports, including parts. This is the same section of legislation that was used to justify recently imposed tariffs on steel and aluminum on national security grounds (see commentary). This report considers a scenario in which the results of this investigation are used to justify U.S. tariffs on autos and parts of a similar magnitude to those imposed on steel and aluminum. Given the importance of the auto sector to Canada (nearly a fifth of total 2017 bilateral trade in goods), and in particular to Ontario (roughly 40% of exports), this scenario is unequivocally negative. Annual growth in 2019 is reduced by half a percentage point at the national level. Ontario fares even worse, bearing the brunt of the impact. What's more, a 'scarring' of business investment occurs, meaning the level of investment is permanently lower as a result, reducing Canada's long term economic capacity. The magnitude of this scenario underscores the high stakes facing Canadian trade negotiators.

Current state of play

U.S. President Trump has on numerous occasions expressed distaste for auto imports. Words became actions on May 23, as the U.S. Department of Commerce began an investigation of auto and parts imports on national security grounds. The Department is required to report its findings and recommendations by February of 2019, although it may do so earlier. The President then has 90 days to make a decision, with no requirement that the President implement the recommendations in any specific way.1

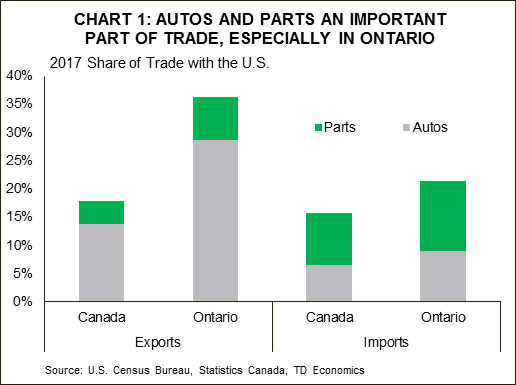

Auto sector a significant part of Canada's economy

The auto sector is a significant part of the Canadian economy, and Ontario's in particular. Autos and parts exports made up nearly a fifth of the 2017 total (Chart 1), with this share roughly double for Ontario. The sector has become integrated across North America, particularly with significant bilateral trade in both finished vehicles and parts with the United States. All told, roughly C$74 billion dollars of exports stand to be impacted by potential tariff imposition (nearly 4% of Canadian GDP), with spillover effects likely to hit the roughly C$45 billion of auto and auto part imports as well. The appendix contains a listing of specific products assumed to be targeted based on the U.S. Commerce Department's investigation announcement.2

Key assumptions

A tariff of 10% on motor vehicle parts, engines, etc. is assumed, and a 25% tariff on motor vehicles. This is meant to follow the rough 'logic' of applying a greater tariff to the greater value-added trade category, and minimize, to an extent, U.S. supply chain disruptions. This results in a weighted tariff rate of 21% on autos and parts exported to the U.S. from Canada, equivalent to a 2.9% tariff on overall exports.3 Taking the aluminum and steel tariffs as precedent, Canada is assumed to retaliate, applying equivalent tariffs on an equal value of imported U.S. goods. The result is an effective 5.4% weighted tariff on imports.4 Tariffs are assumed to become effective on July 1, 2019 - similar to the steel and aluminum tariffs, a response to the Commerce Department findings from the President is expected in March 2019 with an initial exemption that ultimately expires.

Scenario analysis suggests a modest economic pull-back, concentrated in Ontario

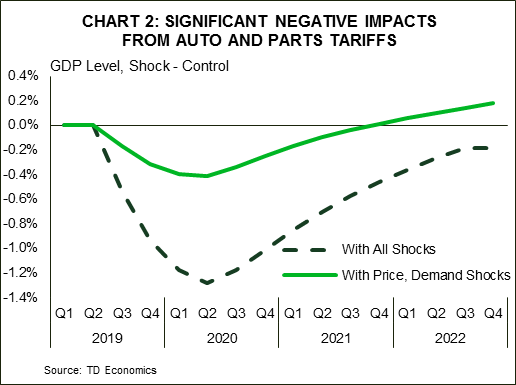

The scenario analysis consists of two key shocks that occur simultaneously. The first is the direct tariffs impacts, applied as shocks to export and import prices. This generates a permanent shift in these price levels. U.S. spending is assumed to respond in line with historic elasticities, creating a negative demand shock for Canadian goods. The second element consists of confidence impacts, which negatively affect equity markets, consumer sentiment, and most importantly, business confidence and investment intentions.

The results are striking. The impact of phase one is relatively modest, sending economic output roughly 0.4% lower than would otherwise have been the case, reaching peak impact after roughly four quarters. This lost ground is made up within about two years. Inclusion of confidence effects creates a significantly worse outcome. The peak impact on the level of output is roughly 1.2%, again after about four quarters. This is an output loss of about $25 billion in 2007 constant dollars (i.e. real terms). What's more, significant disinvestment also occurs, meaning that part of this lost output is never recovered. This 'scarring' (or negative supply shock) leaves the level of output permanently 0.2 percentage points below the 'business as usual' or baseline scenario (Chart 2).

To put it in more concrete terms, GDP growth stagnates, effectively flat for half a year with growth of -0.7% and -0.1% q/q annualized in 2019Q3 and 2019Q4 respectively. This shaves roughly half a percentage point off of 2019 growth. Significant job losses also result, with roughly 160k net positions shed, relative to status quo. Almost all of these losses would occur in Ontario.

For perspective, 1.7 million Canadians worked in manufacturing in 2017, of which 771k were in Ontario. This shock thus means there is the potential of losing nearly 1 in 10 of the jobs in this sector, or 1 in 5 in Ontario. This would be effectively a repeat of the job losses recorded between 2008 and 2010 - losses that have yet to be recovered.5 Such a shock would be enough to erase all of the gains (across all industries) in employment that Ontario experienced over the last two years.

Although Canada as a whole may experience a brief pause in growth, for Ontario the impacts are more severe. GDP growth would be reduced by as much as 2 percentage points, similar to the 2007/2008 experience. Some offset to these impacts would be expected via monetary policy, as the Bank of Canada would likely cut its policy interest rate in response to such significant tariffs. The loonie would also depreciate by 8% to 15%, with significant volatility coming alongside. That the negative impacts summarized in Table 1 occur despite these offsets speaks to the size of the risks around current trade negotiations.

Importantly, this analysis does not include potential government support programs. As has been shown by Quebec's reaction to aluminum tariffs, there is likely to be a government response. Given the importance of the sector, both provincial and federal support is likely. This may ease some of the impact, but given the significant trade exposure and substitutability of a number of major products, it is difficult to envision a support package able to mitigate the bulk of the negative impacts.

Even those Canadians fortunate enough not to be in the direct line of fire are likely to feel the pinch in their pocketbooks. Tariffs generate what economists call a 'deadweight loss' - the impacts on prices and consumption that result are usually larger than the revenue generated by the tariffs. This means that even were the government to redistribute these revenues to those affected, it would not be enough to make them whole again. This well established result is one of the key reasons that free trade is an area in which economists almost universally support.6

Indeed, although the focus of this report is Canada, the U.S. would also be negatively impacted. Roughly half of new vehicles sold in the U.S. in 2017 were imported, meaning U.S. consumers will feel the hit, even before supply chain disruptions and other negative impacts are considered.

This scenario may paint a fairly negative picture, but if anything, the risks are tilted further to the downside. The economic models employed in this analysis are typically used for macroeconomic forecasting and policy analysis, and don't include full industry linkages. Thus, while the confidence shocks should account for most of them, the spill-over effects may be even larger. It is not hard to envision negative impacts hitting housing markets, retail sales, and other key indicators, particularly in the Greater Golden Horseshoe area of Ontario, where a significant portion of the auto sector is located.

Bottom line

From the auto pact through to CUSFTA and NAFTA, the Canadian auto sector has enjoyed a long history of access to the U.S. market, and is an important element of the Canadian economy. This importance means that a potential U.S. imposition of tariffs, and corresponding retaliatory tariffs by Canada, would have a deleterious effect on economic output, leaving the economy effectively at a standstill for half a year. The impact on Ontario would be markedly worse given the sectoral concentration. Fortunately, this analysis stands as simply a 'what if'. Our baseline view remains an eventual resolution of NAFTA negotiations, despite recent developments that increase the tail risk of a dissolution or outright trade war. Given U.S. capacity utilization rates, recommended tariffs may be lower than those assumed in this analysis, reducing their impact. Plus, the high visibility of potential tariffs and resulting price increases are unlikely to prove popular with voters. Nevertheless, the importance of the auto sector and of trade more generally to the Canadian economy underscores the magnitude of the challenges facing Canada's trade negotiators.

End Notes

- For example, the steel investigation recommended tariffs of 24% on all steel imports, and 7.7% for aluminum. In both cases, higher targeted tariffs were recommended as an alternative. Ultimately, tariffs of 25% and 10% were implemented respectively, with some countries exempted based on voluntary export restrictions (quotas).

- Of note, the statement makes no reference to other transportation products such as motor coaches, buses, or aircraft.

- It should be noted that in the case of the steel and aluminum tariffs, the levels recommended by the Commerce Department were chosen with the goal of bringing capacity utilization in these sectors to the 80% mark. This is considered the "minimum rate needed for the long-term viability of the industry". By way of comparison, in April of 2018, U.S. motor vehicle and parts manufacturers were operating at 80.5% capacity. Capacity utilization for 2017 as a whole averaged 77.7%

- Despite the relatively high industry tariff assumed, the effective rate used in this analysis may be slightly conservative as the highly integrated nature of the North American auto industry means that parts can cross the border multiple times during the production process, potentially compounding tariff impacts.

- Manufacturing employment in Ontario peaked at around 1.1 million in 2004, but has remained around the 750k mark from 2010 onwards.

- See for instance the results of the IGM forum survey of a wide sample of economists from across the political spectrum. It is of course worth also acknowledging that the benefits come with distributional income and employment impacts that should be recognized.

Appendix: Specific product categories and tariffs assumed

The following product categories (and HS codes) and tariffs form the basis of the analysis:

CAC Slips as Trump Tariffs Spook Investors

The CAC index has started the week with sharp losses. In the Monday session, the CAC is at 5436, down 1.2% on the day. On the release front, there are no eurozone or French indicators. The highlight of the day is the opening of the ECB Forum, which kicks off with a speech from ECB President Mario Draghi. On Tuesday, Draghi will participate in a panel discussion. As well, the eurozone releases current account, with the surplus expected to drop to EUR 30.3 billion.

The markets are watching nervously, as trade relations between the United States and China continue to deteriorate. Investor risk appetite has softened after U.S President Trump imposed further tariffs on some $50 billion of Chinese products. China has promised to retaliate against U.S imports, as trade ties between the world’s two largest economies continue to deteriorate. With the U.S recently slapping tariffs on the E.U and the NAFTA talks in pause mode, it is no wonder that investor anxiety has risen. If the trade war between the U.S and its partners continues to escalate, traders can expect global equities to continue to lose ground.

The CAC jumped on Thursday, posting gains of 2.0%. The markets jumped after the ECB policy meeting, when the ECB said that it had no intention of raising interest rates prior to the second half of 2019. The ECB pledged to taper its bond-purchase program to EUR 15 billion/mth, in October, down from the current pace of EUR 30 billion/mth. The program will wind up at the end of the year. However, investors detected a ‘dovish flavor’ to the announcement, as the ECB added that interest rates would remain steady “at least through the summer of 2019”, giving policymakers plenty of wiggle-room to delay any rate hikes. The markets were anticipating a rate hike shortly after the end of the bond-purchase program, so this announcement surprised the markets and sent the euro sharply lower. ECB head Mario Draghi sounded dovish in his press conference, saying that the eurozone economy was facing “increasing uncertainty”. Draghi was likely referring to the G-7 meeting which ended in disarray as well as the election of a euro-sceptic government in Italy. The ECB also lowered its growth forecast for the eurozone to 2.1%, down from 2.4% earlier this year.

Sunset Market Commentary

Markets:

Global core bonds eked out some gains today, but they remain relatively small given losses on stock markets (-1% and more). Risk sentiment is negatively influenced by this weekend’s escalation in the trade conflict with China retaliating Friday’s US measures. The automotive sector takes an additional hit after Audi CEO Stadler was taken into custody in the diesel-cheating scandal. Higher oil prices probably helped tilting the balance in the Bund with Brent crude rebounding from $72.5/barrel to $74.5/barrel. Rumours indicate that OPEC+ won’t increase production as much as proposed by Russia and Saudi Arabia. The bloc meets in Vienna on Friday. German Chancellor Merkel took the sting out the migration quarrel between her and CSU Interior Minister Seehofer by accepting a 2-week deadline to win European agreement on a tougher policy. This time buying removed another positive short term factor for the safe haven Bund. The eco and event calendar was empty, but heats up later this week with the ECB’s Sintra conference and EMU PMI’s. US yields decline by 0.6 bps (2-yr) to 1.5 bps (10-yr) at the time of writing. The German yield curve shift up to 1.3 bps (5-yr) lower. Peripheral yield spreads vs Germany narrow by 2 to 5 bps.

EUR/USD: The escalating trade conflict between the US and China and political uncertainty in the UK and Germany left investors in a risk-off mood at the start of the new trading week. European equities joined the decline from Asia. However, the risk-off sentiment hardly supported core US and European yields. A similar indecisiveness was also visible in EUR/USD. The pair dropped to the 1.1565 area early in European dealings, but soon returned back to the 1.16 area. For now, the political topics dominating the market talk didn’t cause any additional euro selling. The risk-off trade hardly affected USD/JPY trading. The pair is holding in the mid 110 area. For now, the dollar fails to profit from rising overall uncertainty even as recent CB action suggests that USD will maintain a big interest rate differential over the euro and the yen. Eco data were second tier and largely ignored as a driver for FX trading.

GBP: the never-ending Brexit battle within the Conservative Party continued to dominate market headlines. The House of Lords is expected to approve a proposal on the ‘meaningful vote’ issue that is unacceptable for the UK government and for the pro-Brexit MP’s of May’s Conservative party. If so, the law will return to the House of Commons on Wednesday. A harsh positioning of both sides could cause a defeat for PM May with big political consequences. The direct impact from the Brexit noise on sterling remains modest. At the same time, it doesn’t help sterling. EUR/GBP trended higher, above 0.8750. The ongoing political uncertainty and mixed UK eco data will probably make to BoE cautious to revive market expectations on an August rate hike at Thursday’s policy meeting.

News Headlines:

CSU interior minister Horst Seehofer has lifted his ultimatum on his proposed changes to Germany’s asylum policy (refusing refugees at the border who are already registered as asylum seeker in another EU country). Merkel has now a chance to find an agreement at the EU summit later this month that would make Seehofer’s proposal unnecessary.

The German Bundesbank has projected that the German economy should rebound in the second quarter after disappointing results in Q1. However, the 2.0% growth estimate for this year is well below the 2.5% projection of December last year.2019 growth is estimated at 1.9% (from 1.7%).

The Belgian debt agency tapped 4 OLO’s today: OLO 79 (€0.58bn 0.2% Oct2023), OLO 85 (€1.52bn 0.8% Jun2028), OLO 75 (€0.93bn 1% Jun2031) and OLO 78 (€0.57bn 1.6% Jun2047). The combined amount sold was the maximum of the targeted €3.1bn-€3.6bn. Total OLO issuance stands at €22.04bn so far this year, which is already 71% of the stated €31bn OLO funding target.

ECB Vasiliauskas: Rate hike goes towards autumn

ECB Governing Council member, Lithuania's central bank governor Vitas Vasiliauskas said today that the foreward guidance suggested rate hike could come around autumn of 2019.

He noted, "we said 'through the summer', but as traditionally there is no meeting in August, it is obvious that we could talk about September-October."

So, "I'd say it goes towards autumn."

John Williams takes over New York Fed, pledges openness and transparency

Ex-San Francisco Fed President John Williams takes over the job of New York Fed President today. In a statement, he pledged openness and transparency, objectivity and independence of thought, and commitment to the diverse needs of familis and business across the District.

Below is the full statement.

Statement from President Williams

I am pleased to be starting my tenure today as president and CEO of the Federal Reserve Bank of New York. As someone who has dedicated his career to public service, I can think of no better place from where to continue to support the nation's economic well-being.

The New York Fed plays a unique role in the Federal Reserve System, with responsibilities for implementing monetary policy, managing a critical payments system, overseeing a large number of complex financial institutions and managing international relationships. I take each of these responsibilities with the utmost seriousness and am committed to executing my role as president of the New York Fed and on the Federal Open Market Committee (FOMC) to the absolute best of my ability.

So what can you, the public, expect of me?

- Openness and transparency. I am dedicated to learning from a wide range of perspectives and experiences from across the District. Openness flows both ways, and we have a duty to explain the reasoning behind our actions. I am committed to acting in as transparent a manner as possible.

- Objectivity and independence of thought. I will continue to make monetary policy recommendations based on what I believe is in the best interest of our economy. Throughout, I will strive to explain my reasoning, particularly when my views may differ from those of others.

- Commitment to the diverse needs of families and businesses across our District. Understanding the varied financial and economic needs of families, businesses, and communities, and advocating for them at the policy table is a critical component of my role. I am equally committed to building a diverse and inclusive workforce and workplace at the New York Fed, which will help us better serve our communities.

I start my first day with a deep commitment to securing the stability of our financial system and prosperity for our economy. I look forward to engaging with and learning from members of our communities and stakeholders throughout the District and beyond.

John C. Williams became the 11th president and chief executive officer of the New York Fed on June 18, 2018.

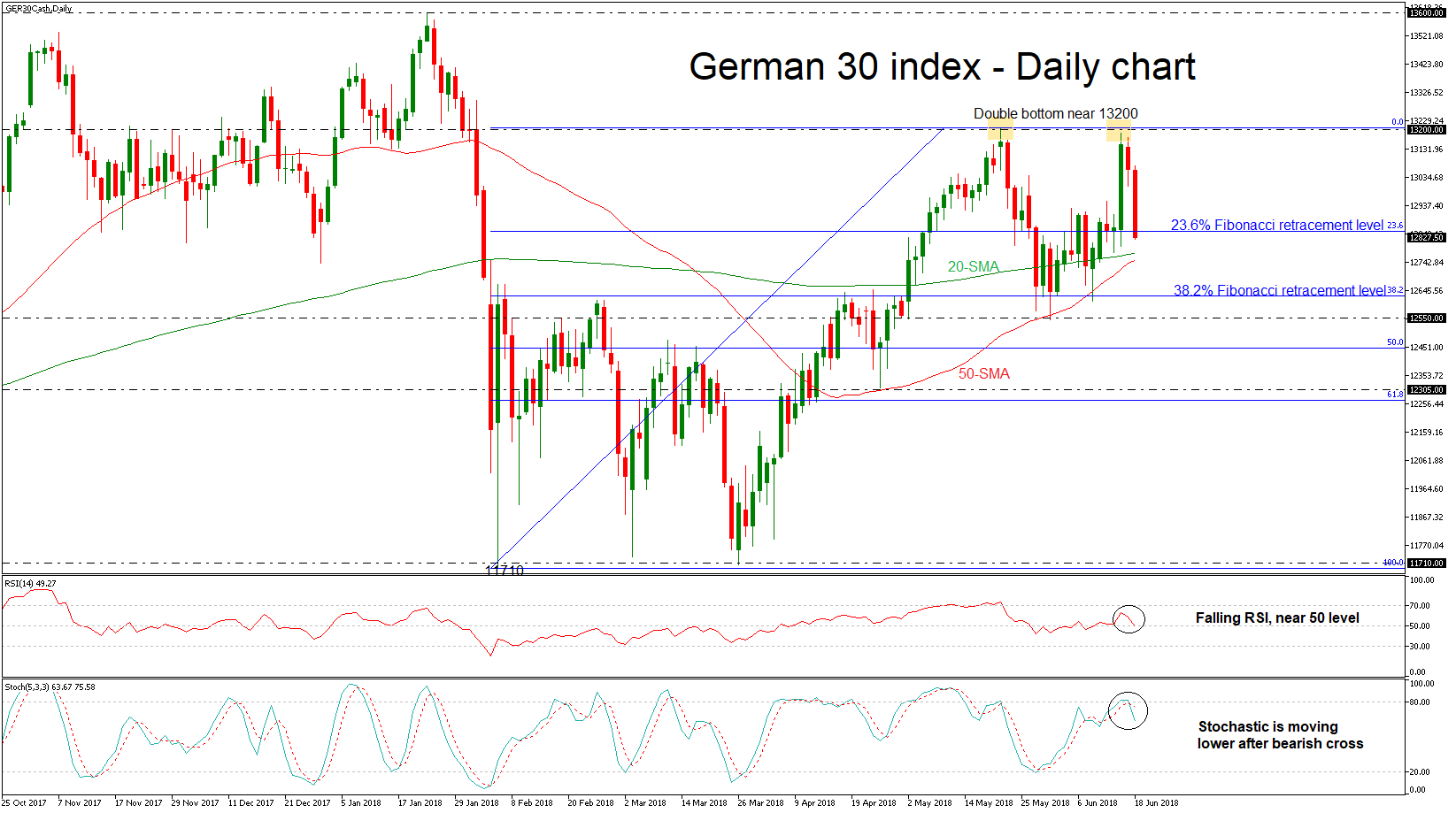

German 30 Stock Index Loses Momentum after Creating Double Top

The Germany 30 stock index has plunged today after the significant bounce on the double top level near the 13200 barrier. The sharp sell-off has driven the price towards the 50- and 200-simple moving average (SMA) in the medium-term, which are expected to post a bullish crossover in the next few sessions if the price recoups the losses.

Looking at the daily timeframe, the RSI indicator holds near the 50 level and is sloping down; some caution may be warranted given that the indicator is trying to enter the negative territory. Moreover, the stochastic oscillator posted a downward crossover – the %K line moved below the %D.

As the price is developing below the 23.6% Fibonacci the next level to have in mind is the 38.2% Fibonacci retracement level of the upleg from 11710 to 13200, around 12627.26. It is worth mentioning that the price would first need to drop below the 50 and 200 SMAs. If there is a break below this level, it would challenge the 12550 support. However, there is also the chance of a pullback at moving averages that could lead to some gains.

In case of an upward attempt, the index should see the 13200 resistance level, taken from the peak on May 22. If there is an upside break, the index would likely meet resistance at 13600, this being its all-time high.

In the medium term, the neutral outlook remains intact, as the index failed to endorse the previous bullish structure over the last five weeks.

Canadian Dollar Slips to 1.32 on Trade Tensions

The Canadian dollar is trading sideways in the Monday session. Currently, USD/CAD is trading at 1.3183, up 0.05% on the day. On Friday, the pair broke above the 1.32 line for the first time since June 2017. On the release front, there are no major events on the schedule. On Tuesday, the U.S releases building permits and housing starts.

The Canadian currency continues to look vulnerable after U.S President Trump imposed further tariffs on some $50 billion of Chinese products on Friday. China has promised to retaliate against U.S imports, as trade ties between the world’s two largest economies continue to deteriorate. With the U.S recently slapping tariffs on Canadian steel and the NAFTA talks in pause mode, it is no wonder that investor anxiety has risen. If the trade war between the U.S and its partners continues to escalate, the big losers could be export-reliant economies, such as Canada. With some 80% of Canadian imports heading to the U.S, Canada can ill-afford a trade spat with its giant neighbor. With President Trump showing no hesitation about slapping tariffs on Canadian steel and threatening further tariffs against Canada, the wobbly Canadian dollar could continue to head lower.

Prime Minister Justin Trudeau is still smarting from the disastrous G7 summit, which he hosted. Canada, along with other members of the G7, vociferously complained about the tariffs which Trump imposed on Canada and the European Union. The summit ended in disarray, with Trump labeling Trudeau “weak” and “dishonest”. The meeting exposed fault lines between Trump and the other leaders over trade, a. Trump is expected to impose further tariffs on China as early as Friday, which has lowered risk appetite and weighed on the Canadian currency. Meanwhile, negotiations to update the NAFTA agreement remain deadlocked, with Canada unhappy about a U.S demand for a sunset clause after five years, which would require the parties to hammer out a new agreement. Mexico is holding general elections on July 1, and a left-wing candidate, Andrés Manuel López Obrador, leads in the polls. If López Obrador becomes president, it could mean more complications for the NAFTA talks.