Sample Category Title

EUR/USD Builds ABC Correction Back To 50% Fibonacci

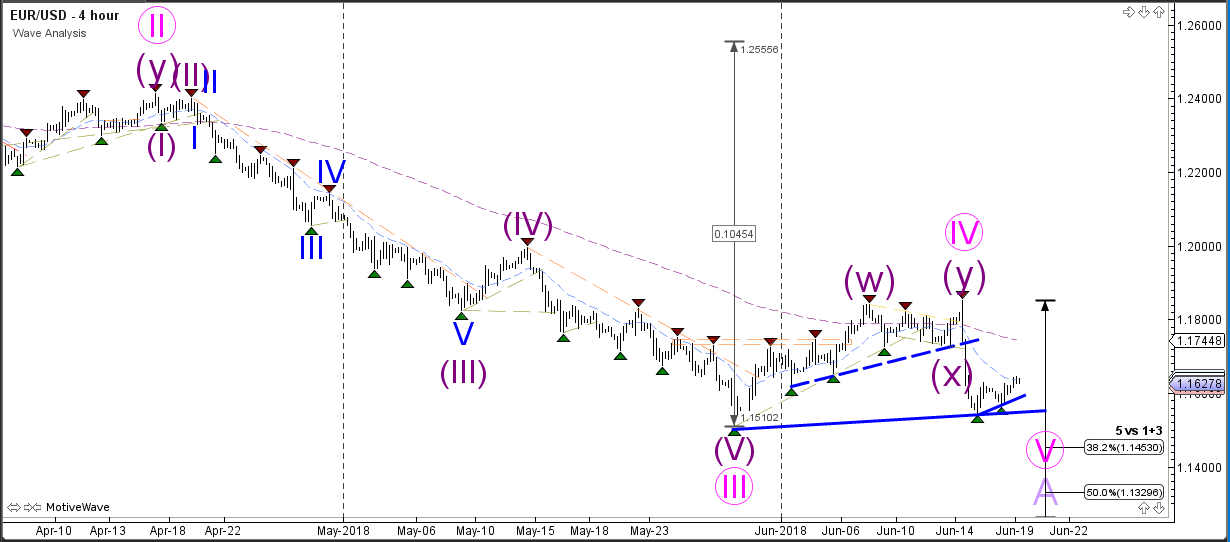

The EUR/USD seems to have completed a wave 4 (pink) correction after building a bearish turn at a 38.2% Fib resistance zone. Price is now building a potential 5th wave within wave A (purple) if price is able to break the support trend lines. The main target is 1.1450 due to the presence of a 50% Fibonacci retracement level on the weekly chart.

The EUR/USD seems to be building an ABC correction within wave 4 (purple) at the moment. The Fibonacci levels of wave 4 are potential resistance spots which could indicate a downtrend continuation but a breakout above the 50-61.8% Fib makes a wave 4 pattern less likely.

RBA unsure next move is a hike?

A major surprise from the RBA minutes released today is that it no longer predicts the next rate move as a increase. Back in the April and May meeting minutes, the central bank noted that "in the current circumstances, members agreed that it was more likely that the next move in the cash rate would be up, rather than down." But such reference is taken out from the June minutes. It could be a sign that RBA is less confidence that the next move is a rate hike.

While that's a notable change, it shouldn't be taken too seriously for the time being. The minutes were on the meeting held on June 5. On June 13, last Wednesday, RBA Governor Philip Lowe reiterated in a speech that "the national accounts provided confirmation that the Australian economy is moving in the right direction ... If this continues to be the case, it is likely that the next move in interest rates will be up, not down."

Otherwise, the minutes revealed nothing special. The main factor behind RBA's neutral stance is sluggish wage growth. It reiterated that the unemployment rate steadied at 5.5%. Ratio of job vacancies to the number of unemployed workers had remained well below levels seen a decade earlier. Both suggested that "spare capacity remained in the labour market." And, "wages had continued to grow at a low and stable rate".

(RBA) Minutes of the Monetary Policy Meeting of the Reserve Bank Board

Sydney – 5 June 2018

Members Present

Philip Lowe (Governor and Chair), Guy Debelle (Deputy Governor), Mark Barnaba AM, Wendy Craik AM, Ian Harper, Allan Moss AO, Catherine Tanna

Nigel Ray (Deputy Secretary, Macroeconomic Group, Treasury) attended in place of John Fraser (Secretary to the Treasury) in terms of section 22 of the Reserve Bank Act 1959.

Members granted leave of absence to Carol Schwartz AM in terms of section 18A of the Reserve Bank Act 1959.

Others Present

Luci Ellis (Assistant Governor, Economic), Christopher Kent (Assistant Governor, Financial Markets), Alexandra Heath (Head, Economic Analysis Department), Bradley Jones (Head, International Department) Merylin Coombs (Deputy Head, Economic Analysis Department)

Anthony Dickman (Secretary), Andrea Brischetto (Deputy Secretary)

Domestic Economic Conditions

Members commenced their discussion of the domestic economy by noting that the March quarter national accounts would be released the day after the meeting. Based on indicators for the quarter received to date, GDP growth was expected to have picked up to be at least 2¾ per cent over the year because export volumes were expected to have recovered after weakness in the December quarter. Growth was also expected to have been supported by consumption, public demand and business investment.

Early indicators for the June quarter suggested that surveyed business conditions had remained at their highest levels since the start of the global financial crisis a decade earlier, but consumption had been less buoyant. Growth in retail sales had been moderate in April; reports from the Bank's liaison program suggested that unseasonably warm weather had partly explained relatively subdued outcomes for sales of clothing in particular and at department stores more generally.

Preliminary data suggested that dwelling investment had picked up in the March quarter. Information from the Bank's liaison program suggested that demand for detached houses had remained strong, while off-the-plan apartment sales had slowed considerably as a result of weaker investor and foreign demand. Capacity constraints appeared to have limited the pace of work in higher-density construction, particularly in Sydney. The amount of building work in the pipeline remained high, and had increased recently in Victoria; the pipeline of work was expected to support a high level of dwelling investment for some time yet.

Conditions in the established housing market appeared to have eased further in Sydney and Melbourne. Housing prices had fallen a little in both cities, particularly for more expensive dwellings. Members observed that falls in housing prices in Melbourne had been concentrated in inner-city areas, whereas the declines in Sydney had been more widespread. Members noted that, nonetheless, housing prices were still 40 per cent higher in Sydney and Melbourne than at the beginning of 2014, while housing prices in Perth had fallen by around 10 per cent over the same period. Auction clearance rates in Sydney and Melbourne had fallen to their lowest levels in a number of years.

Public demand was expected to have grown significantly faster than expenditure in other parts of the economy in the March quarter. Both public consumption and public investment, which includes investment in infrastructure projects, were expected to have contributed. The Australian Government budget, tabled in May, had announced $25 billion in infrastructure spending, although some of this was conditional on state government funding and was expected to commence some years later; in general, both federal and state government budgets suggested that infrastructure investment was likely to continue to support growth for some time. Stronger economic conditions had resulted in the Australian Government's underlying cash deficit for 2018/19 being smaller than earlier projections.

The March quarter capital expenditure (Capex) survey suggested that non-mining business investment had continued to grow; investment in machinery & equipment had been stronger than expected in the March quarter, while non-residential construction activity had declined. Non-residential construction activity was expected to ease further in 2018/19, based on data from the Capex survey and the decline in non-residential building approvals in the first few months of 2018. Members observed that the Capex survey did not suggest a further pick-up in machinery & equipment investment, but they noted that the survey does not provide information on intangible investments or investment in some parts of the services sector, including education and health. Members also noted that profits in the non-mining sector as a share of output had been resilient, which was positive for future investment. Mining investment was still expected to fall over the subsequent few quarters, as construction of the remaining large liquefied natural gas (LNG) projects reached completion.

Members noted that labour market conditions had eased a little in recent months. Looking through the monthly volatility in the labour force data, members observed that employment growth had slowed from a very fast pace in 2017 to something closer to the rate of growth in the working-age population. However, forward-looking indicators of labour demand had continued to point to employment growth increasing to above-average rates in coming months. The unemployment rate had been broadly steady at around 5½ per cent since mid 2017, suggesting that spare capacity remained in the labour market. The ratio of job vacancies to the number of unemployed workers had remained well below levels seen a decade earlier, which also signalled spare capacity in the labour market.

Wages had continued to grow at a low and stable rate. The wage price index had increased by 2.1 per cent over the year to the March quarter. Wages growth had remained faster in the household services industries, particularly in healthcare and education (where a majority of employees are paid under collective wage agreements), than in other sectors. The Fair Work Commission had awarded a 3.5 per cent increase in the minimum wage and higher-classification award wages, which would boost wage outcomes in the September quarter. More broadly, members noted that there had been some evidence of increased wage pressures in some areas of the economy. An increased share of firms in the Bank's liaison program had reported that they expected wages growth to pick up and liaison contacts had continued to report pockets of wage pressures in construction and IT roles for which there had been skill shortages. In addition, a larger number of firms had reported greater difficulty in hiring workers with the requisite skills.

Members noted that export volumes were estimated to have increased strongly in the March quarter, partly unwinding the fall following supply disruptions in the December quarter. LNG production was expected to contribute to growth over the following year or so before levelling out at a high level. Exports of some other resources used extensively in renewable energy generation and battery storage, such as copper and lithium, were expected to contribute to growth over this period, but to a much smaller extent than had iron ore, coal and LNG in recent years.

Concerns about the durability of Chinese steel demand had eased and demand for Australia's bulk commodities was expected to remain strong in the near term. This had contributed to a recovery in coking coal prices; by contrast, iron ore prices had been little changed over the prior month. Overall, bulk commodity prices had increased a little since the previous meeting. Sustained strength in bulk commodity prices had contributed to a rise in the growth of mining sector profits and the terms of trade in the March quarter. Oil prices had increased earlier in May to their highest level since 2014, but had fallen back in the period leading up to the meeting.

Members discussed a range of longer-term demographic developments. They noted that Australia had experienced strong population growth over the preceding decade or so, in large part driven by net overseas migration of younger people. The composition of net overseas migration had affected the age structure of the population. As a result, Australia's median age and old-age dependency ratios were projected to increase by less than those of other advanced economies, despite a relatively high life expectancy. This would make Australia one of the youngest populations within this group of countries. Demographic trends varied by state. For much of the preceding decade, population growth had been particularly strong in Victoria and less so, though still relatively high, in New South Wales, and the median age had declined in these states. The mining investment boom had had a noticeable influence on demographic patterns in Western Australia and Queensland over the 2000s.

Members observed that the increase in Australia's population and the changes to its demographic characteristics had led to significant changes in labour supply and demand for housing. Over the prior decade, females in most age groups and males aged over 55 years had increased their participation in the labour force by enough to offset the effects of the ageing of the population. Members noted that changes in policy settings and societal attitudes were likely to have played an important role in these participation decisions. Differences in demographic developments helped to explain some of the differences in housing investment cycles across states. Members observed that continuing investment in infrastructure was required to service Australia's larger population.

International Economic Conditions

Members noted that global economic conditions had remained solid. While growth appeared to have eased a little in the major advanced economies early in the year, more recently growth had strengthened in China and global activity indicators, such as growth in industrial production and survey measures, had remained consistent with an ongoing expansion. In the advanced economies, there had been further evidence of tightening capacity constraints, which were expected to translate into higher inflation over time. Inflation in the emerging economies had remained relatively low. The prospect of additional tariff measures being introduced, either by the US administration or in response to its actions, continued to present a downside risk to the global economic outlook. Increased political uncertainty in Italy and concerns about the economic prospects of some emerging markets, notably Argentina, Brazil and Turkey, had led to increased volatility in some financial market prices.

In China, recent indicators suggested economic conditions had strengthened modestly in April. Growth in industrial production had picked up and steel production had increased, supported by high margins as well as ongoing demand for steel from the construction sector. Activity in the housing sector had been resilient, partly because growth in housing demand had remained strong in cities where tightening measures were not in place. However, growth in infrastructure investment had slowed, which partly reflected tighter funding conditions for local governments. Growth in bank lending had remained steady, while the provision of alternative sources of financing had continued to contract in the face of tighter regulation and stronger enforcement.

Growth in India had picked up to be close to 8 per cent in year-ended terms. Members noted that government efforts to support investment had contributed to this strength. India's ability to boost its business service exports over recent years was also viewed as an indicator of brighter prospects for future growth. GDP growth in Korea had picked up in the March quarter as a result of stronger domestic demand. Members observed that many economies in east Asia, including Taiwan and Korea, had benefited from the pick-up in demand for electronics in recent years and the resulting increase in trade through global supply chains.

Inflation had generally remained low in the Asia-Pacific region. It had picked up in India to be above the Reserve Bank of India's 4 per cent target, but had eased further in New Zealand, partly reflecting low imported inflation and subdued wage pressures.

In the major advanced economies, GDP growth had eased in the March quarter, after strengthening over recent years, but had still been strong enough to continue to absorb spare capacity. Unemployment rates in the United States, Japan and Germany had fallen to their lowest levels in several decades and the ratio of job vacancies to the number of unemployed people had continued to rise in many advanced economies. Although wages growth had picked up in all the major advanced economies, it had increased by less than historical experience would imply, given the extent of labour market tightness. Core inflation had remained low in Japan and the euro area, but had increased to be close to target in the United States.

Some slowing in US economic growth had been expected because the boost to consumption and investment in the December quarter from the post-hurricane recovery had passed. Surveys and labour market indicators nonetheless had confirmed that the underlying momentum in the US economy had remained strong ahead of the sizeable fiscal stimulus that was scheduled for 2018 and 2019. The US labour market had continued to tighten and reports that it was difficult to find people to hire had become widespread. Members noted that evidence of wage pressures building in the United States had become clearer over recent months.

The easing of growth in the March quarter in Japan and the euro area had partly reflected bad weather and other temporary factors. In Japan, consumption and investment growth were expected to be supported by strong business conditions, the tight labour market, accommodative monetary policy and the global economic upswing. In the euro area, however, surveys suggested that business conditions had eased somewhat, and that this had continued into the June quarter. Members noted that political uncertainty in Italy could also weigh on confidence in the euro area. Members observed that real GDP per capita in Italy was lower than before the global financial crisis and that the Italian unemployment rate had declined only marginally after nearly doubling following the onset of the crisis.

Financial Markets

Members commenced their discussion of developments in financial markets by noting that, while global financial conditions had remained expansionary, political risk in the euro area and instability in some emerging markets had come into greater focus. International trade policy developments in the United States had also remained a concern for market participants.

Political uncertainty in Italy had been accompanied by a significant increase in Italian bond yields and a decline in the price of Italian bank stocks. Members noted that the bulk of Italian government debt is held domestically and that Italian banks hold a substantial amount of Italian government debt relative to their assets. The longer-term fiscal and economic challenges facing Italy were discussed. Members noted that measures of sovereign risk, as reflected in the yield spread of Italian over German bonds, had remained well below levels recorded in the 2011–12 episode of instability in the euro area. There had been limited signs of spillovers to other euro area sovereign markets. It was also noted that a change of government in Spain had not generated disruptive effects in financial markets there.

Members observed that long-term government bond yields for a number of major sovereign issuers, including Australia, had declined in May. In the euro area, the fall in German yields had reflected, in part, the effect of safe-haven flows and an easing in growth momentum in the euro area. In the United States, 10-year bond yields had traded in a wide range before finishing slightly lower for the month, reflecting a modest reduction in expectations for policy tightening by the Federal Reserve.

Members noted that central bank policy settings in the major advanced economies had been unchanged since the previous meeting. The US Federal Reserve had continued gradually to reduce the size of its balance sheet, in accordance with its earlier announced plans, while the European Central Bank and Bank of Japan had maintained asset purchases consistent with their highly accommodative policy settings.

Members noted that conditions in US dollar short-term money markets had eased since early April, although they remained tighter than in 2017. A similar profile had been evident in Australian money markets, although interest rate spreads had begun to pick up again in recent days. It was also noted that corporate bond spreads in the advanced economies had remained low. Movements in global equity markets had been mixed over the preceding month. While US equity prices had been supported by strong corporate earnings, Chinese markets had been little changed and European markets had been weighed down by declines in equity prices of financial institutions. Australian equity prices had been largely unchanged over May; increases in resource stocks had been underpinned by higher commodity prices, while the equity prices of Australian financial institutions had declined.

Members also discussed developments in emerging markets, noting that problems in a few countries had largely reflected idiosyncratic weaknesses and that spillovers to Asia had been limited to date. In particular, large current account and budget deficits, high inflation and political uncertainty in Argentina and Turkey had contributed to substantial exchange rate depreciations and widening bond spreads over US Treasuries in those countries. Central banks had intervened in foreign exchange markets in an effort to stem further depreciation and they had raised their policy interest rates. Argentina had also sought financial support from the International Monetary Fund. In Brazil, authorities had intervened to slow the depreciation of the real in the context of heightened political and fiscal uncertainty and high levels of debt. The Mexican peso had depreciated in response to developments in Argentina and Brazil, as well as uncertainty over the future of Mexico's trading relationship with the United States and the upcoming presidential election.

By contrast, financial markets in the Asian region had been generally resilient. Bank Indonesia had raised policy rates twice in the second half of May and intervened in the foreign exchange and bond markets in order to dampen volatility; the rupiah had depreciated only modestly over the course of 2018. Despite considerable uncertainty over international trade developments, Chinese financial asset prices, including the renminbi exchange rate, had been relatively stable, and authorities had continued to take measures to reduce risks in the financial system.

The Australian dollar had been little changed over the prior month and thus had remained in the range seen over the preceding two years.

Members noted that housing loan approvals had eased in recent months, driven by approvals to investors, although approvals for owner-occupiers had also declined. This was consistent with an easing in the demand for credit as well as lenders tightening their lending standards. Members noted that banks had recently started to collect more information from loan applicants on living expenses to assess a borrower's capacity to service a loan based on actual living expenses, rather than relying on a proxy measure of minimum expenses based on survey benchmarks. Members noted that, while there may be some further tightening of lending standards affecting housing credit growth in the period ahead, any such tightening was expected to be modest. At the same time, lenders had been competing for high-quality borrowers, which had led to a decline of around 15 basis points in the average mortgage interest rate on outstanding loans since August 2017. Slightly higher funding costs for banks appeared to have had little effect on mortgage rates.

Pricing in money markets implied that the cash rate was expected to remain unchanged for a considerable period, with a 25 basis point increase not expected before the second half of 2019.

Considerations for Monetary Policy

In considering the stance of monetary policy, members noted that conditions in the global economy had strengthened over the prior year. Output in China had grown solidly, which had supported demand for Australia's resource exports and commodity prices. At the same time, Chinese authorities had continued to implement policies to manage risks in the financial sector and ensure the sustainability of future growth. Growth in the major advanced economies had eased a little in the first quarter of 2018, but underlying momentum in these economies had still been consistent with above-trend growth. Wage pressures were increasing, particularly in the United States and Japan, where labour market conditions were very tight by historical standards.

Growth in global output was expected to continue to absorb spare capacity, leading to a lift in inflation. As a result, a number of central banks had withdrawn some monetary stimulus and further steps in this direction were expected. Conditions in US dollar short-term money markets were tighter than they had been a year earlier. Although these higher rates had flowed through to higher short-term interest rates in a few other economies, including Australia, overall financial conditions globally remained expansionary. Members noted that the direction of trade policy in the United States continued to be uncertain. In addition, concerns about political developments in Italy and developments in some emerging market economies had affected some financial prices. The Australian dollar had been relatively unaffected by these developments and had remained within the range it had been in for the preceding two years.

Members noted that recent data had been consistent with the Bank's central forecast for GDP growth to pick up to be above 3 per cent by the end of 2018. Business conditions were positive and non-mining business investment was expected to increase. Public spending, including on infrastructure, and exports were also expected to support growth. While consumption was expected to grow at a broadly stable rate in the near term, the outlook for consumption growth continued to be a source of uncertainty, given that household income growth had been slow and debt levels remained high.

Employment had grown strongly over the previous year, but the unemployment rate had been little changed because strong labour demand had been met by people entering the labour force or delaying retirement. Although employment growth had slowed over recent months, forward-looking indicators suggested employment would continue to grow faster than the working-age population over the period ahead and that, as a result, there would be a gradual decline in the unemployment rate. Although wages growth had remained low, members noted that there had been more evidence that employers were having difficulty hiring workers with the requisite skills and that wage pressures were building in some parts of the economy.

Inflation remained low and was likely to remain so for some time, reflecting slow growth in labour costs and strong competition in the retail sector. However, a gradual pick-up in inflation to be above 2 per cent was still expected as the economy strengthens and wages growth increases. An appreciation of the exchange rate would be expected to result in a slower pick-up in economic activity and inflation than currently forecast.

Conditions had continued to ease in established housing markets in Sydney and Melbourne and had remained subdued in most other capital cities. Growth in housing credit had slowed over the preceding year, especially to investors. An easing in the demand for credit as well the Australian Prudential Regulation Authority's supervisory measures and tighter credit standards had been helpful in containing the build-up of risk on household balance sheets, although the level of household debt remained high. While there might be some further tightening of lending standards in the period ahead, the average mortgage interest rate on outstanding loans had declined over the previous year.

The low level of interest rates was continuing to support the Australian economy. Further progress in the period ahead in reducing unemployment and returning inflation to the target was therefore expected, although this progress was likely to be gradual. In the current circumstances and taking account of the available information, the Board judged that holding the stance of monetary policy unchanged would be consistent with sustainable growth in the economy and achieving the inflation target over time.

The Decision

The Board decided to leave the cash rate unchanged at 1.5 per cent.

China condemns US blackmailing after Trump threatens with extra tariffs on USD 200B Chinese products

Trump ordered US Trade Representative to identify USD 200B worth of Chinese products for additional 10% tariffs. It noted in the statement that "the initial tariffs that the President asked us to put in place were proportionate and responsive to forced technology transfer and intellectual property theft by the Chinese. It is very unfortunate that instead of eliminating these unfair trading practices China said that it intends to impose unjustified tariffs targeting U.S. workers, farmers, ranchers, and businesses. At the President's direction, USTR is preparing the proposed tariffs to offset China's action."

The Chinese Ministry of Commerce vowed to fight back with "qualitative" and "quantitative" for any additional tariffs. The MOFCOM condemned to initiative of imposing extra tariffs on USD 200B of Chinese goods. It said in a statement today that "Such a practice of extreme pressure and blackmailing deviates from the consensus reached by both sides on multiple occasions, and is a disappointment for the international community." And, "the United States has initiated a trade war and violated market regulations, and is harming the interests of not just the people of China and the U.S., but of the world."

US farmer group to launch TV ads against trade war

Trump's protectionist trade policy are causing a lot of concerns from US farmers. The steel and aluminum tariffs on Mexico have already triggered retaliation on US agriculture products. The trade war with China is even a bigger concern. Brian Kuehl, executive director of Farmers for Free Trade, said "the reason you are seeing people increase the pressure now is because the pressure is increasing on them. Now the impact is really starting to hit. It is not something you can just take lightly."

The group issued a statement last week in response to the section 301 tariffs on China. There it noted imposing tariffs on China is "no longer a negotiating tactic" and it's a "tax" on farmers livelihoods. It's "downright scary". And the group criticized that the tariffs is a "win for our competitors", including South Maerica and Australia. The group called for elected officials to stop this trade war.

Here is the statement:

Farmers for Free Trade Executive Director, Brian Kuehl released the following statement following reports that the Administration will move forward with $50 billion in tariffs on China which are expected to result in heavy retaliatory tariffs on U.S. agricultural exports.

"For American farmers this isn't theoretical anymore, it's downright scary. It's no longer a negotiating tactic, it's a tax on their livelihoods. Within days, soybean, corn, wheat and other American farmers are likely to be hit with retaliatory tariff of up to 25% on exports that keep their operations afloat. When they do, they're not going to remain silent.

"The imposition of these tariffs is not only a blow to our farmers, it's a win for our competitors. When American soybeans and corn become more expensive, South America wins. When beef becomes more expensive, Australia wins. As this trade war drags on, farmers will rightly question why our competitors are winning while we're losing.

"Farmers for Free Trade will continue to hold town hall meetings across the country this summer to ensure farmer's voices are being heard. The message will be loud and clear: American farmers demand that elected officials support them by ending this trade war."

The group will also launch a TV ads on Tuesday in Pennsylvania and Michigan urging Trump to stop trade war.

https://www.youtube.com/watch?v=qTLHdwyMn8A

US halts wargames with South Korea, continues with Japan

The joint military exercises of the US and South Korea are formally halted. The South Korean defense ministry said in a statement that "South Korea and the United States have agreed to suspend all planning activities regarding the Freedom Guardian military drill scheduled for August." Pentagon spokeswoman Dana White said separately that "we are still coordinating additional actions. No decisions on subsequent wargames have been made."

On the other hand, the join military exercises of US and Japan will continue as usual. Japan's Chief Cabinet Secretary Yoshihide Suga said there is no change to the planned drills. And, Suga added "the United States is in a position to keep its commitment to its allied nations' defense and our understanding is there is no change to the U.S. commitment to the Japan-U.S. alliance and the structure of American troops stationed in Japan."

At the same time, North Korean leader Kim Jong-un arrives in Beijing today for a two-day visit. It's believed that Kim will brief Chinese President Xi Jinping on last week's summit with Trump in Singapore.

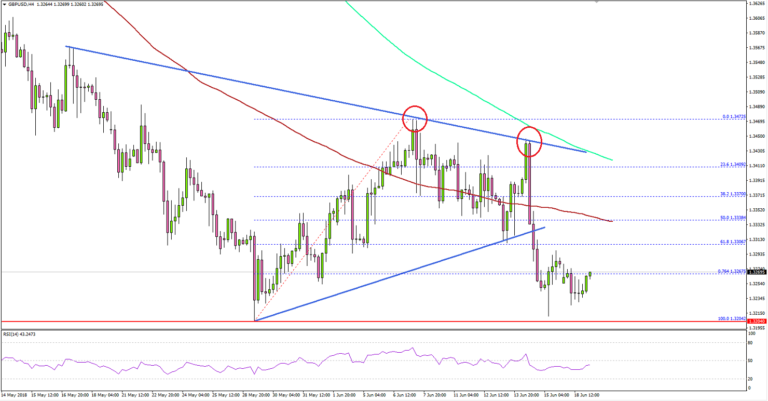

GBP/USD Likely To Revisit 1.3200 In Near Term

Key Highlights

- The British Pound declined sharply from well above 1.3400 and broke 1.3300 against the US Dollar.

- There was a downside break below 1.3330 on the 4-hours chart of GBP/USD.

- The pair is now in a bearish zone and it could decline back towards the 1.3200 level in the near term.

- Today in the US, the Building Permits for May 2018 will be released, which is forecasted to decline by 1.4%.

GBPUSD Technical Analysis

The British Pound formed a topping pattern near 1.3440 against the US Dollar. The GBP/USD pair started a major downside move and broke the 1.3350, 1.3300 and 1.3280 support levels.

Looking at the 4-hours chart, there was a clear downside break below a contracting triangle with support at 1.3330. The pair settled below 1.3330 and the 100 (red) and 200 (green) simple moving average (4-hour).

The pair is now trading well below the 76.4% fib retracement level of the last wave from the 1.3204 low to 1.3472 high. Therefore, there are high chances of more declines back towards the last swing low of 1.3204.

Below the low, the pair could test the 1.236 Fib extension level of the last wave from the 1.3204 low to 1.3472 high. Should there be an upside correction, the pair is likely to face sellers near the 1.3280 and 1.3300 resistance levels.

However, the most important resistance for buyers is near the 1.3330 level and the 100 SMA. A close back above the mentioned resistance is needed for further gains towards the 1.3400 level in the near term.

Economic Releases to Watch Today

- US Housing Starts May 2018 (MoM) – Forecast 1.317M, versus 1.287M previous.

- US Building Permits May 2018 (MoM) – Forecast 1.350M, versus 1.352M previous.

Market Morning Briefing: Aussie Has Been Falling Sharply

STOCKS

Shanghai has fallen breaking crucial 3000 support indicating further bearishness. Nikkei, Nifty and other Asian equity indices could follow soon. Dax and Dow are also trading lower and could also be dragged down in the near to medium term.

Dow (24987.47, -0.41%) and Dax (12834.11, -1.36%) are trading lower. Dow has immediate support near 24750 and while that holds, there is a slight chance of a bounce back to higher levels. A break below 24750 would turn strongly bearish for the medium term. Similar support on the Dax is seen near 12700, which on a downside break would trigger bearishness.

Asian equities have been falling for the last few sessions and are indicative of bearishness for the near term. Nikkei (22482.89, -0.87%) is heading towards our mentioned 22400-22200 target. A break below 22200 would take it to much lower levels in the near term.

Shanghai (2961.78, -1.98%) has led the Asian equities being the first to break immediate support at 3000 and to indicate upcoming bearishness in the overall indices across major currencies. Shanghai is likely to test 2900 in the coming sessions.

Nifty (10799.85, -0.17%) continues to remain stable near 10800. A sharp down move is required to take it lower towards 10600.

COMMODITIES

Brent (74.99) and WTI (65.99) have recovered a bit from the recent fall. WTI may head towards 67 while Brent could test 77 resistance in this week.

Gold (1283.51), if falls below 1275-1270 could open up chances of testing 1250/40 on the downside. For now there could be some stable movement near current levels.

Copper (3.1170) has dipped some more from 3.13 seen yesterday. Looking at the bearishness in Shanghai and Aussie, Copper could also move down in the near to medium term. A break below 3.10 could take it down towards 3.07-3.05 in the coming sessions.

FOREX

Euro (1.1634): As per expectation, Euro has risen towards 1.165 and could test levels near 1.167 in today’s session before dipping towards 1.162 again. Last week the ECB’s decision to keep key rates constant till 2019 summers was perceived to be dovish and led to a fall in the Euro from 1.185 to 1.154.

Dollar Index (94.596): Dollar Index could see a further dip towards 94.5-94.4, followed by a rise back towards 94.6-94.7. This week could see a gradual downmove towards 94.3-94.2, while it stays below resistance near 95.5. Last week, the Euro’s weakness and a strong US Retails Sales data release had led to a rise in the Dollar Index from 93.2 to a high near 95.1.

Dollar Yen (109.87): Dollar Yen has dipped after testing resistance near 110.9 on daily candles. It could see oscillation between 111.0-109.5 in this week and then break below support on daily candles (near 109.5-110.0) ultimately, which could make it bearish towards 107 in the medium term.

Euro Yen (127.84): Euro Yen has been testing crucial horizontal support on weekly line chart near current levels. A week close below this support (near 127) would be crucial for Euro Yen turning bearish towards 124 in the medium term.

Aussie (0.7407) has been falling sharply for quite a few sessions now and has immediate supports near 0.7370 and further down near 0.7325. These are likely to hold in the medium term with some hope of an upward correction in Aussie back towards 0.75. Near term looks bearish but downside could be limited to 0.7325.

Pound (1.3267): As mentioned yesterday, Pound could be bearish towards 1.30 in the medium term. In this week, it could target support near 1.31 on 3 day candles.

Dollar Rupee (67.99) : Dollar Rupee may test 67.75 on the downside while below 68.

INTEREST RATES

US 10 Year (2.88%), 30 Year (3.0173%), 5 Year (2.76%), 2 Year (2.52%):

The US 10 Year yield (2.88%) seems to be sustaining its break of support on medium term chart. Elevated US-China trade tensions might be a reason for a rise in risk-averseness amongst investors. As mentioned yesterday, this downmove might just extend till 2.60%-2.55% in the medium term.

Last week, US Fed had hiked rates by 25 bps. Although the rate hike was expected, the language in the policy statement turned out to bemore hawkish than expected. The likelihood of 2 more rate hikes this year has increased beyond 50% for the first time this year.

US 10 - 2 Year yield Spread (0.36%) continues to stay below long term support near 0.4%. The persistence of this break would suggest an impending slowdown for the US economy.

Last week, the ECB came out with a mixed policy. The end of quantitative easing was expected by the markets – however that was overpowered by its dovish stance on interest rates, which led to a fall in the German 10 Year yield towards 0.4%. On medium term chart, the German 10 Year yield looks bearish towards 0.3%; but for that, it would have to break support on short term chart near 0.4%.

Fed Bostic: Business optimism replaced trade policy and tariffs concerns

Atlanta Fed President Raphael Bostic delivered a speech titled "The Path to Economic Resilience" to the Rotary Club os Savannah yesterday. There he expressed his support further further rate hike as the economy "appears to be in a pretty good place".

His growth outlook "hasn't changed materially" since the start of the year and output is expected to growth at a "moderately above-trend pace this year and next", then slow to slightly less than 2%.

Regarding inflation, Bostic said he hasn't seen a "dramatic shift" in inflation expectation or measured retail price inflation yet. And aggregate wage growth "appears to have flattened out" over the past year to a level that's inline with fundamentals.

Bostic is comfortable to "move policy toward a more neutral stance", where it's "neither accommodative nor restrictive". While neutral rate is "something we know with precision", he believed Fed is getting close to the "lower part of most plausible estimates of the neutral rate". And he noted the key question is the number of hikes are required to reach neutral.

He also warned of trade policy of the US. Bostic said "I began the year with a decided upside tilt to my risk profile for growth, reflecting business optimism following the passage of tax reform. However, that optimism has almost completely faded among my contacts, replaced by concerns about trade policy and tariffs. Perceived uncertainty has risen markedly. Projects already under way are continuing, but I get the sense that the bar for new investment is currently quite high. 'Risk off' behavior appears to be the dominant sentiment among my contacts. In response, I've shifted the risks to my growth outlook to balanced."

World Cup Effect Weighing On Volumes

Trade War Escalation

That was quick and sudden and reminding us just how quickly things can get right out of hand.

On the back of Secretary of State Mike Pompeo mincing few words by branding China's openness and globalisation as a joke, President Trump has asked the USTR to identify $200B in China goods for other tariffs at a rate of 10% and will up the stakes to $400B if China retaliates.

Indeed, this is moving beyond 'tit for tat 'levels, and predictably, investors are running for cover under the haven umbrellas as global equity indices are crumbling under the weight of an escalating trade war.

What was a mild risk-off tone at the end of the NY session is threatening to morph into a full-blown rout in global equity markets?

It's amazing how quickly the tides can shift as only hours ago the market seemed to be backing off the worst of trade war concerns, and to shift into a full panic mode.

All bets are off on this one!!! Buckle up as this could get messy

World Cup effect weighing on volumes

Volumes are running low confirming the World Cup effect, but the lack of any substantial data has also contributed to the downturn in volume.

Equity Market

Risk off sentiment continues to dog equity markets as heightened trade tension between China and the US have investors yet again bracing for the worst as a full-blown trade war were to materialise it would have negative impacts on the US economy. But with US market trading off session lows, the start of the week would be better characterised as a case of investor jitters rather than a full-blown risk-off move

Oil Market

Elsewhere in oil, with the OPEC meeting looming on Friday the headline procession marches on. Despite a likely veto from Iran to block the Vienna group production rises, most OPEC members are optimistic the group can agree on a production hike. The oil complex has bounced back from Friday weakness as overnight headlines are now pointing to 300,000 and 600,000 barrels a day production hike. While much less than feared and closer to my desk consensus, the figure excludes non-OPEC producer Russia, so the effective increase in supply could be 0.2-0.3 mmbpd more.T his supports our long-held view that we will likely see a compromise which should set the stage for gradual barrels added over time, which is likely to be endorsed by most. This approach makes logical sense as a fine-tuning approach will ultimately keep both end users and producer happy.

Gold market

Despite bouncing slightly overnight the precious complex is again giving in to the dollar strength. Despite tentatively recouping some of Friday loses, gold remains under pressure from the prospects of a strengthening dollar. Also, Friday's stinging 2% + sell-off, the gold complex remains extremely vulnerable to more long liquidation, from a technical perspective,

Currency Market

Not everyone is as bearish as me on the Euro but, it remains a complete mystery why the ECB decided to kick the rate hike can down the road for another 15 months, even more so as ECB's Vasiliauskas (Member of the governing council) said t that he sees ‘no clouds' for euro area in the medium term. Thus, the market will be focusing on Mario Draghi conference in Sintra for a convincingly dovish follow up before sticking the fork in the Euro

While lower remains apparent near-term path of least resistance for the euro, over the medium term however the vast interest rate differential will like narrow while the uncertainty around trade wars and the demise of the US influence on global trade as China continues to assert its position, should ultimately prove detrimental for the dollar in the long run

Asia FX

Asia FX continues to struggle and look to be extremely vulnerable as outflows continue to pick up momentum as investor angst over trade war, and policy divergence remains front and centre as investors remain extremely cautious about re-engaging risk.

MYR: The Ringgit tested the critical USDMYR level. And while trading a negative correlation to local risk, the moves have been less harmful perhaps reflecting that despite the political noise, the MYR remain less vulnerable to external trade shocks and a stronger USD than its regional peers.