Sample Category Title

Currencies: Euro Resists Trade Tensions, For Now. Yen Rallies

Rates: Risk aversion lifts core bonds

Rising oil prices and the de-escalation of the CDU/CSU rift drop from the equation which kept core bonds in balance yesterday, leaving the new tit-for-tat threats in the US/Chinese trade row as the only factor influencing trading. Core bonds profit from global risk aversion. Today's eco/event calendar probably won't put much counterweight.

Currencies: Euro resists trade tensions, for now. Yen rallies

The euro held up well yesterday and this morning, even as trade tensions between the US and China intensify. The yen strengthens with USD/JPY declining below the 110 handle. The US-Chinese trade conflict will continue to dominate trading today. A further decline of USD/JPY-EUR/JPY might finally also spill over to EUR/USD.

The Sunrise Headlines

- The US equity markets continues to lose with the trade war still in play. The Asian markets opened with losses and Chinese markets underperforming (Shanghai Comp -3%) after markets were closed yesterday.

- Ping pong between the US and China continues, with Trump announcing new tariffs on $200bn in Chinese goods. The trade conflict between the two world powers now seems to have escalated, with China announcing again to retaliate.

- In the UK, the House of Lords have rejected PM May's proposal on the ‘meaningful vote' that would give the Parliament only a symbolic vote on next steps in Brexit, if they don't approve the deal that May negotiated with the EU.

- Pedro Sanchez, Spain's new PM, stated he has no intentions of calling early elections and will go until the end of the term in 2020. Early elections were expected, since his party controls less than a quarter of the seats in parliament.

- FED's Bostic supports the rate hike of last week, but shifted his business optimism he had at the beginning of this year to a more balanced outlook: “risk-off behaviour appears to have become dominant due to the trade war”.

- Australia's central bank (RBA) expects the economy to pick-up growth with more than 3% this year. It warns, however, that high household debt and slow wage growth will keep interest rates at their all-time lows for some while longer.

- With few important eco data scheduled for release, the ECB's Forum in Sintra is the main topic on the eco agenda. At 10am Chairman Draghi gives a speech, followed by a panel chaired by its Chief Economist Peter Praet

Currencies: Euro Resists Trade Tensions, For Now. Yen Rallies

Euro resists trade tensions, for now

Yesterday, sentiment turned further risk-off with the US-China trade conflict the main driver. However, the impact on core bonds and FX was modest. After a dip early in the session, EUR/USD rebounded to close the day modestly stronger at 1.1623. USD/JPY also finished little changed (110.55). Overnight, the trade conflict escalated further. US President Trump instructed to identify another $200 bln of Chinese imports that could become subject to 10% import tariffs. China immediately said it will take ‘compressive quantitative and qualitative measures and retaliate forcefully'. This next step in the trade war weighs on Asian equities. US equity futures are losing up to 1%. The yen gains. USD/JPY declined from 110.60 to the 109.70 area. EUR/USD is little affected and even gained a few ticks (1.1630 area). Trade tensions also pushed AUD/USD to the 0.74 area. In the minutes of the June meeting the RBA stays positive on growth but it is in no hurry to raise rates.

Today, the data calendar is again thin. Markets will keep an eye at comments from the ECB conference in Sintra. However, Fed/ECB speakers will probably confirm indications from last week's meetings. The market focus will remain on the US-China trade conflict. The conflict is at risk to escalate further. (President Turmp already indicated a next step). For now, the euro stays out of focus, probably as current battle is mainly a US-China issue. Still, Europe/European growth might soon feel the fall-out from this conflict and also become a target. So we stay cautious on the euro as this conflict develops. As usual in a context of global risk-off, we keep a close eye on EUR/JPY. A further sell-off might also spill-over to EUR/USD. After the last week's ECB meeting, we turned cautious on the euro. Selling eased on Friday and yesterday, but policy divergence between the Fed and the ECB probably makes that the euro won't receive interest rate support soon. A retest of the 1.1510 correction low is possible. The dollar can stay strong against the euro for longer. The trade conflict also blocked the USD/JPY uptrend.

Yesterday the House of Lords rejected the government's proposal on the ‘meaningful vote'. The law returns to the Lower House. UK PM May risks another defeat with potentially big political consequences. EUR/GBP rebounded both on Brexit uncertainty and intraday euro strength. There are no UK data today. The focus will remain on the political bickering within the conservative party. Global uncertainty is also no positive for sterling. We expect EUR/GBP to stay in the 0.8725/0.8843 range.

EUR/USD: no fall-out from rising trade conflict yet, but picture remains fragile

China Responds To Report US Is Looking To Implement Additional $200B In Tariffs

General Trend:

- Asian equity markets trade mostly lower after US President Trump threatened additional tariffs on $200B worth of Chinese goods; China threatens more countermeasures

- MSCI Asia-Pacific (ex-Japan) index trades at 4-month low

- Shanghai Composite declines over 2% after Monday’s holiday, index breaches 3,000 for the first time since 2016

- Shares of Chinese telecom ZTE remain under pressure, company’s A-shares trade limit down (-10%)

- Australian equities outperform on gains in the energy and financial sectors

- Japan IPO, Mercari opens strong, 67% above IPO pricing in its first day of trade, rising 76% from pricing

- AUD/JPY declines over 0.5%, trade concerns overshadow RBA minutes; USD/JPY breaches ¥110

- China PBoC conducts second medium-term lending facility (MLF) this month at unchanged rate; Press speculation continues to mount regarding RRR cut

- US 10-yr Treasury yields decline by over 3bps amid the equity weakness

- N. Korea's Kim arrives in China for a 2 day visit

Headlines/Economic Data

Japan

- Nikkei 225 opened -0.5%

- TOPIX Retail trade index -1.6%, Marine Transportation -1.6%, Real Estate -1.6%, Securities -1.5%

- (JP) Yesterday's earthquake in western Japan hit aging infrastructure hard, exposing weaknesses - Nikkei

- XRX Fujifilm files $1B breach of contract suit against Xerox over terminated merger (as expected)

- Kubota Pharma, [+22%], 4589.JP EMIXUSTAT trial showed better results v placebo

- (JP) Japan MoF sells ¥698.9B v ¥700B indicated in 0.8% (0.8% prior) 30-yr bonds; Avg yield: 0.707% v 0.746% prior; Bid to cover: 4.22x v 4.41x prior

Korea

- Kospi opened -0.1%

- (KR) South Korea mobile carriers have secured frequency spectrums for the upcoming fifth-generation network in an auction at a total of KRW3.6T - Korean press

- Woori Bank, 000030.KR Seeking approval for holding company structure - Korean press

- (KR) South Korea Deputy Fin Min Kim: Govt to continue its efforts to realign budget spending in a way to tackle the country's chronic low birth rate, boost job creation and facilitate innovative growth

- (KR) US and South Korea agree to suspend joint military drill scheduled for August - press citing SK military

- (KR) North Korea Kim planning a visit to China as soon as today - Nikkei

China/Hong Kong

- Hang Seng opened -1.0%, Shanghai Composite -1.3%

- Hang Seng Industrial Goods index -3.7%, Materials -3.6%, Services -3%, Energy -3%, Info Tech -2.8%, Consumer Goods -2.7%, Financials -2.4%, Property/Construction -2.3%

- 763.HK , [-13%],(US) US Senate has enough votes to pass defense bill which includes penalties for China telecom firm ZTE

- (US) US President Trump: Has asked USTR to identify $200B in China goods for additional tariffs at a rate of 10% - financial press

- (CN) China PBoC expected to increase 'targeted' monetary support - Chinese Press

- (CN) China Commerce Ministry (MOFCOM): US threats on $200B tariffs list disobeys negotiation and consensus reached previously between the two countries: to take qualitative and quantitative measures if US publishes additional tariffs list

- XIAOMI.IPO China Securities Regulator (CSRC): Xiaomi applied to have review of CDR IPO postponed; co. is seeking to issue H-shares first and then CDRs

- (CN) China PBoC Open Market Operation (OMO): Injects CNY100B in 7, 14 and 28-day reverse repos v CNY100B injected in 7, 14 and 28-day reverse repos prior: Net: CNY50B injection v CNY90B injected prior

- (CN) CHINA PBOC CONDUCTS CNY200B IN 1-YEAR MEDIUM-TERM LENDING FACILITY (MLF) V CNY463B PRIOR AT 3.30% V 3.30% PRIOR

- (CN) China PBoC sets yuan reference rate at 6.4235 v 6.4306 prior

- (CN) There is renewed speculation that the PBoC could ‘soon’ cut the reserve ratio requirement (RRR) – financial press

- (CN) China State Planner (NDRC) Chief: Need to closely monitor new problems in the economy; would like to see targeted policy for boosting investment

Australia/New Zealand

- ASX 200 opened +0.1%

- ASX 200 Energy index +1.2%, Financials +0.6%, Telecom +0.5%

- AGO.AU Board assessed offer from Hancock and determined that it could be expected to lead to a superior proposal vs Mineral Resources offer

- IAG.AU [+3%],Confirms to sell operations in Thailand, Indonesia and Vietnam to Tokio Marine for A$525M

- (AU) Reserve Bank of Australia (RBA) June Meeting Minutes: Pricing in money markets implied that the cash rate was expected to remain unchanged for a considerable period, with a 25 basis point increase not expected before the second half of 2019

- (AU) AUSTRALIA Q1 HOUSE PRICE INDEX Q/Q: -0.7% V -1.0%E; Y/Y: 2.0% V 1.7%E

Other Asia

- (ID) Indonesia Central Bank Gov Warjiyo: Ready to be preemptive regarding Fed and ECB policy

North America

- US equity markets ended mixed: Dow -0.4%, S&P500 -0.2%, Nasdaq flat, Russell 2000 +0.5%

- S&P500 Energy +1%; Consumer Staples -1.4%

- JD Reports 618 mid-year shopping festival sales CNY127.5B v CNY119.9B y/y - Chinese press

- AAPL Trump said to have told CEO Cook that iPhones will be excluded from China tariffs - NYT

Europe

- (UK) Chancellor Hammond has reportedly warned cabinet about any new spending after being forced to find £25B for the NHS - UK press

- (UK) PM May defeated in House of Lords over plans to give lawmakers meaningful vote over final Brexit agreement - press (as expected)

- Ministerial meeting of the 33 member Global Forum on Excess Steel Capacity scheduled for Wednesday in Paris has been cancelled due to trade tensions - Nikkei

- (ES) Spain PM Sanchez: plan to call elections in 2020 - TV interview

- (EU) ECB's Draghi: Economies have undergone profound structural changes

Levels as of 01:30ET

- Hang Seng -2.5%; Shanghai Composite -3.0%; Kospi -0.9%; Nikkei225 -1.4%; ASX 200 +0.2%

- Equity Futures: S&P500 -0.9%; Nasdaq100 -1.0%, Dax -1.1%; FTSE100 -0.8%

- EUR 1.1619-1.1644; JPY 109.66-110.57; AUD 0.7388-0.7427;NZD 0.6924-0.6944

- Aug Gold +0.3% at $1,285/oz; Aug Crude Oil -0.6% at $65.28/brl; Jul Copper -0.7% at $3.10/lb

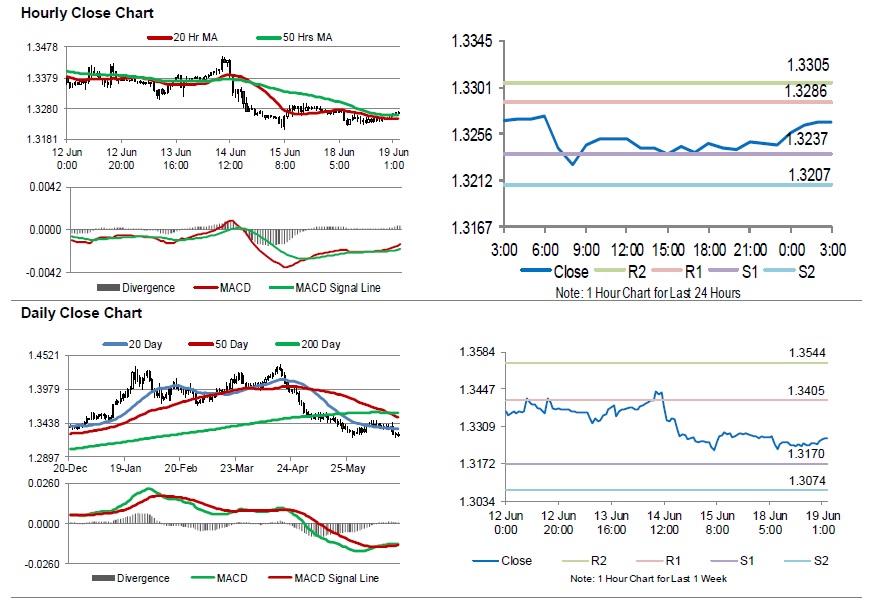

Euro Trading Higher In The Morning Session

For the 24 hours to 23:00 GMT, the EUR rose 0.29% against the USD and closed at 1.1621.

Data showed that, in Italy, Europe’s third largest economy, trade surplus narrowed to €2.9 billion in April, compared to a revised surplus of €4.5 billion reported in the previous month. Markets were expecting trade surplus to narrow to €3.2 billion.

Macroeconomic data released in the US indicated that the NAHB housing market index unexpectedly fell to a level of 68.0 in June, compared to a reading of 70.0 in the prior month. Markets were expecting the housing market index to record a steady reading.

In the Asian session, at GMT0300, the pair is trading at 1.1633, with the EUR trading 0.10% higher against the USD from yesterday’s close.

The pair is expected to find support at 1.1585, and a fall through could take it to the next support level of 1.1537. The pair is expected to find its first resistance at 1.1661, and a rise through could take it to the next resistance level of 1.1689.

Looking ahead, traders would keep a close watch on the Euro-zone’s current account balance and construction output data, both for April, slated to release in a few hours. Moreover, the US housing starts and building permits data, both for May, scheduled to release later in the day, will keep investors on their toes.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

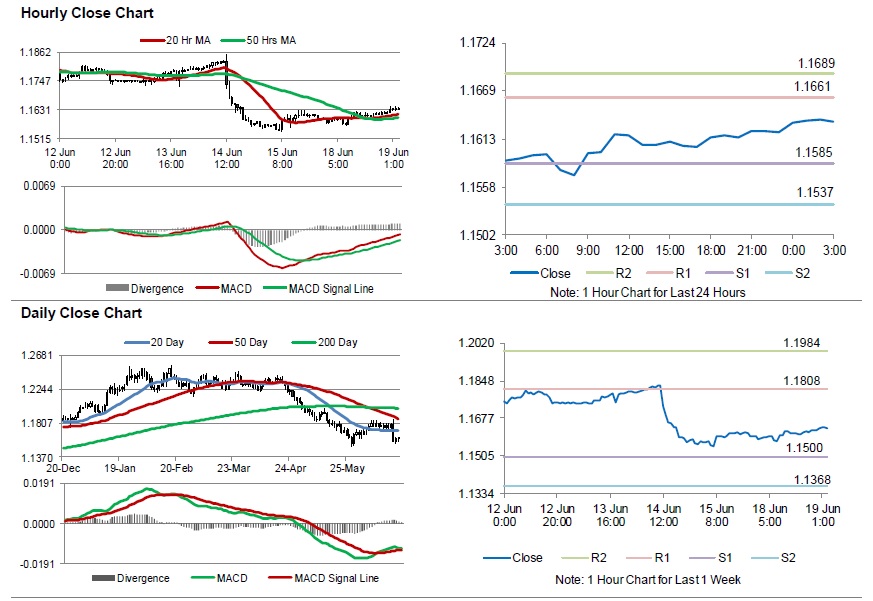

Sterling Trading Higher In The Morning Session

For the 24 hours to 23:00 GMT, the GBP declined 0.20% against the USD and closed at 1.3246.

In the Asian session, at GMT0300, the pair is trading at 1.3267, with the GBP trading 0.16% higher against the USD from yesterday’s close.

The pair is expected to find support at 1.3237, and a fall through could take it to the next support level of 1.3207. The pair is expected to find its first resistance at 1.3286, and a rise through could take it to the next resistance level of 1.3305.

In absence of key economic releases in the UK today, traders would keep an eye on global macroeconomic releases for further indication.

The currency pair is trading above with its 20 Hr moving average and 50 Hr moving averages.

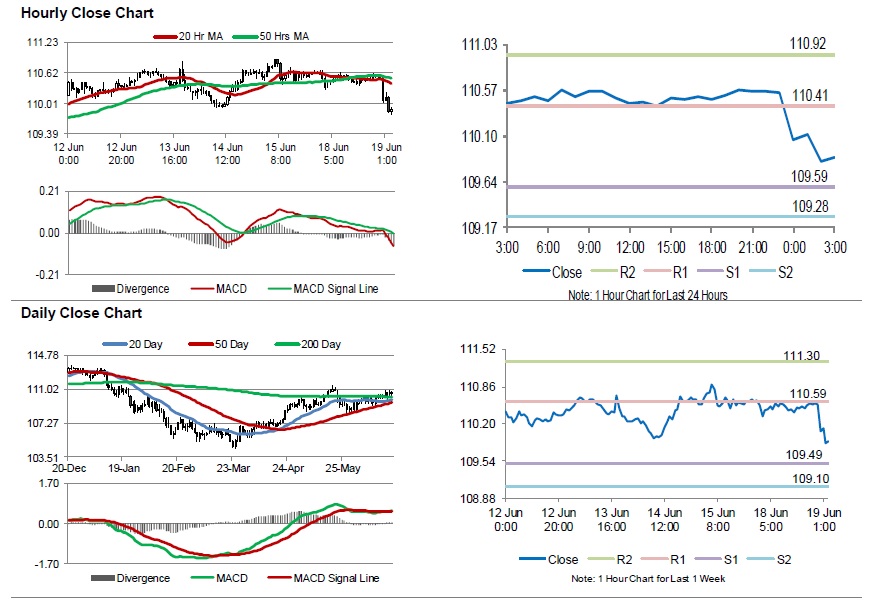

Japanese Yen Trading Higher, Ahead Of BoJ’s Policy Meeting Minutes

For the 24 hours to 23:00 GMT, the USD rose 0.18% against the JPY and closed at 110.54.

In the Asian session, at GMT0300, the pair is trading at 109.89, with the USD trading 0.59% lower against the JPY from yesterday's close.

The pair is expected to find support at 109.59, and a fall through could take it to the next support level of 109.28. The pair is expected to find its first resistance at 110.41, and a rise through could take it to the next resistance level of 110.92.

Moving ahead, investors would keep an eye on the Bank of Japan's (BoJ) June monetary policy meeting minutes, due to be released overnight.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

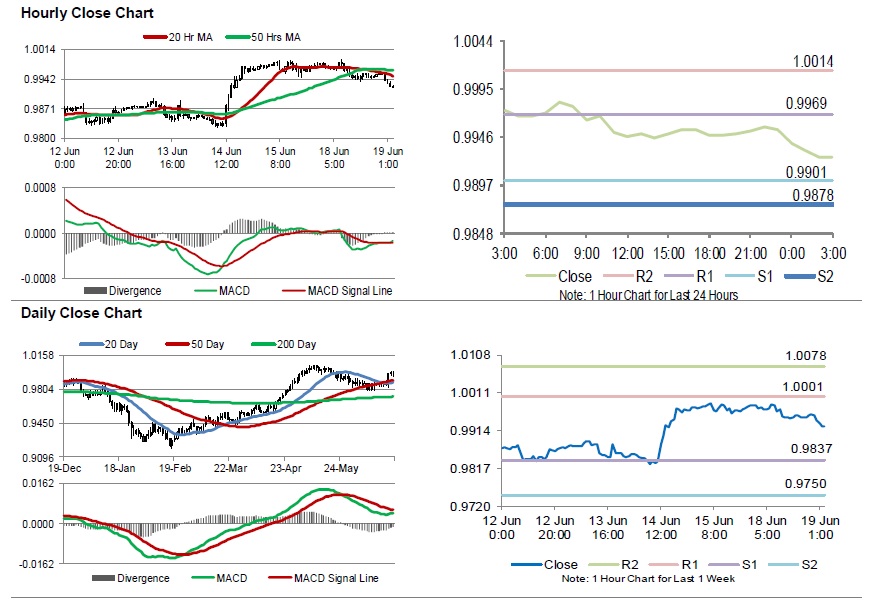

Swiss Franc On A Stronger Footing This Morning

For the 24 hours to 23:00 GMT, the USD declined 0.17% against the CHF and closed at 0.9954.

In economic news, Switzerland’s total sight deposits rose to a level of CHF576.5 billion in the week ended 15 June, from CHF576.3 billion in the previous week.

In the Asian session, at GMT0300, the pair is trading at 0.9925, with the USD trading 0.29% lower against the CHF from yesterday’s close.

The pair is expected to find support at 0.9901, and a fall through could take it to the next support level of 0.9878. The pair is expected to find its first resistance at 0.9969, and a rise through could take it to the next resistance level of 1.0014.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

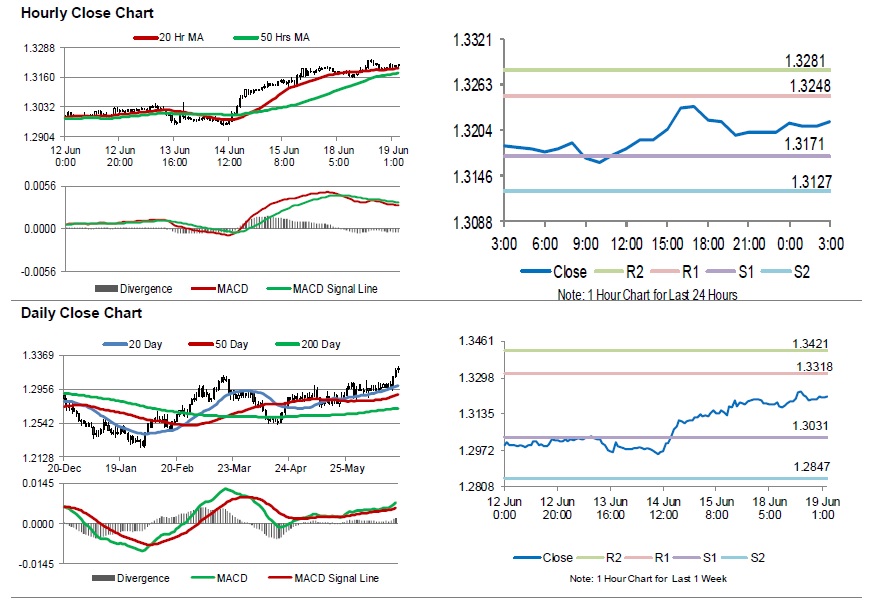

Loonie Trading On A Weaker Footing This Morning

For the 24 hours to 23:00 GMT, the USD rose marginally against the CAD and closed at 1.3202.

In the Asian session, at GMT0300, the pair is trading at 1.3215, with the USD trading 0.10% higher against the CAD from yesterday’s close.

The pair is expected to find support at 1.3171, and a fall through could take it to the next support level of 1.3127. The pair is expected to find its first resistance at 1.3248, and a rise through could take it to the next resistance level of 1.3281.

With no macroeconomic releases in Canada today, investors would look forward to global macroeconomic events for further direction.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

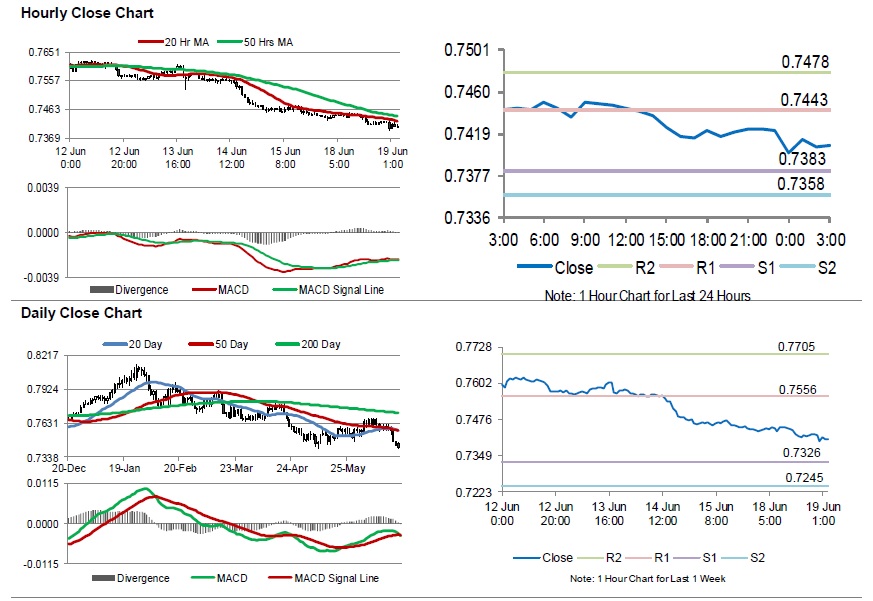

Officials Upbeat On Economy, But Warn Over The Rise In Aussie: RBA

For the 24 hours to 23:00 GMT, the AUD declined 0.20% against the USD and closed at 0.7422.

LME Copper prices declined 2.13% or $152.0/MT to $6987.0/MT. Aluminium prices declined 0.85% or $19.0/MT to $2220.5/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7407, with the AUD trading 0.20% lower against the USD from yesterday’s close.

Early morning data indicated that Australia’s house price index slid 0.7% on a quarterly basis in first three months of 2018, falling short of market expectations for a fall of 1.0%. In the previous quarter, the index had advanced 1.0%.

According to the minutes of the Reserve Bank of Australia’s (RBA) June monetary policy meeting, policymakers expect a rise in economic activity. Further, interest rates are expected to remain at the current low levels, in the wake of high household debt and weak wage growth. Also, officials expect gradual improvement in unemployment and inflation. Meanwhile, the RBA warned that rise in the local currency could lead to slowdown in economic growth and inflation.

The pair is expected to find support at 0.7383, and a fall through could take it to the next support level of 0.7358. The pair is expected to find its first resistance at 0.7443, and a rise through could take it to the next resistance level of 0.7478.

Looking forward, traders would await Australia’s Westpac leading index for May, set to release overnight.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

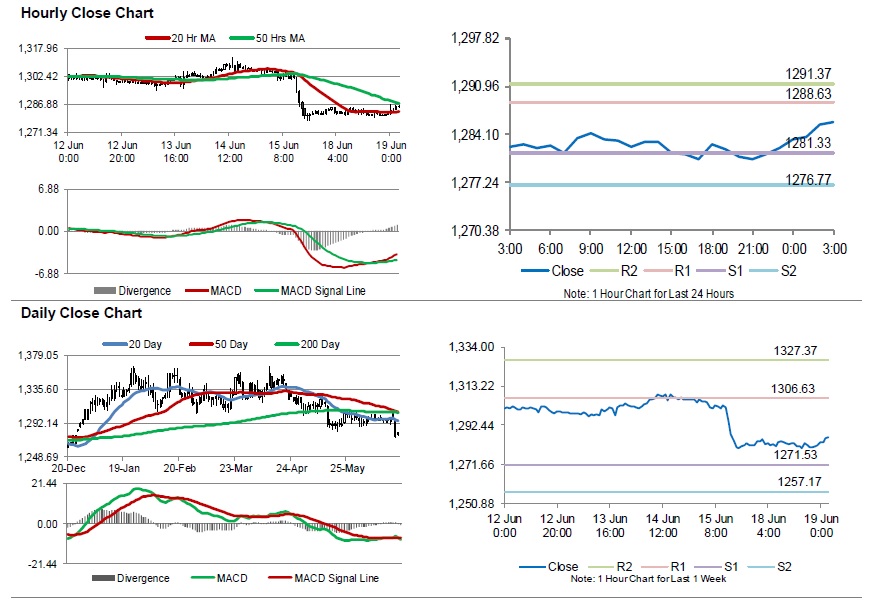

Gold: Yellow Metal Trading Between Its MA’s

For the 24 hours to 23:00 GMT, Gold declined 0.27% against the USD and closed at USD1281.30 per ounce.

In the Asian session, at GMT0300, the pair is trading at 1285.90, with gold trading 0.36% higher against the USD from yesterday's close, as US-China trade tensions escalate.

The pair is expected to find support at 1281.33, and a fall through could take it to the next support level of 1276.77. The pair is expected to find its first resistance at 1288.63, and a rise through could take it to the next resistance level of 1291.37.

The yellow metal is trading between its 20 Hr and 50 Hr moving averages.

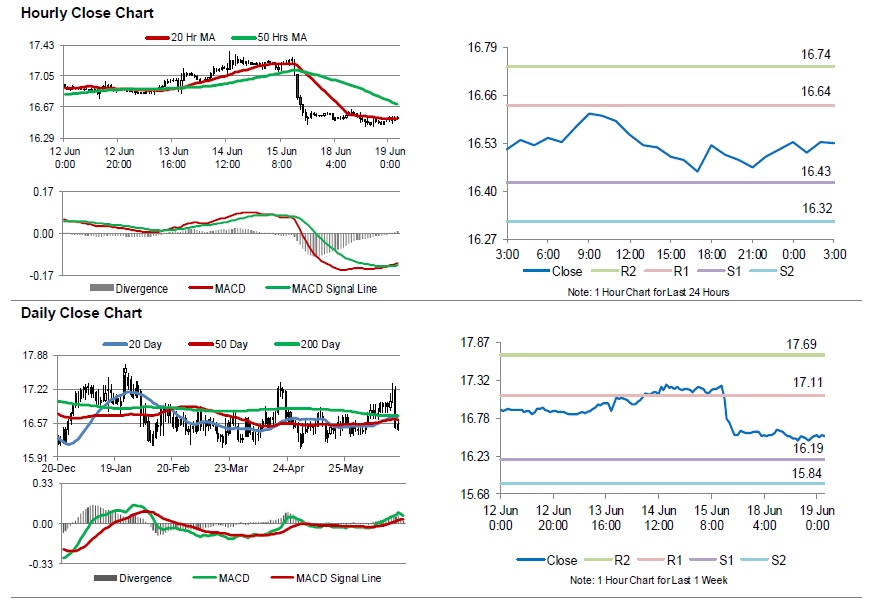

Silver: White Metal Reverses Its Losses In The Asian Session

For the 24 hours to 23:00 GMT, Silver declined 0.45% against the USD and closed at USD16.52 per pounce.

In the Asian session, at GMT0300, the pair is trading at 16.53, with silver trading 0.09% higher against the USD from yesterday’s close.

The pair is expected to find support at 16.42, and a fall through could take it to the next support level of 16.32. The pair is expected to find its first resistance at 16.63, and a rise through could take it to the next resistance level of 16.74.

The white metal is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.