Sample Category Title

US-China Trade: From ‘Grand Bargain’ Towards Trade War?

- The US-China trade frictions escalated further over the weekend and we are unfortunately moving away from the ‘Grand Bargain' scenario towards the ‘trade war' scenario.

- While there are no winners in a trade war, the US is focused on protecting US technology and sees the tariffs on Chinese tech products as a legitimate action. China clearly disagrees, which is why we believe we are heading into a tit-for-tat scenario, in which we believe the US will soon raise the amount subject to tariffs to USD150bn.

- The Chinese retaliation pattern shows that China intends to follow Donald Trump with ‘equal scale and equal strength' on every move he takes against China.

- Even if the amount subject to tariffs is raised to USD150bn, our rough calculations suggest it would not reduce global GDP by more than 0.2%. The calculations are very uncertain though and it is likely the effects would be front-loaded. This suggests downside risk to growth in the second half of 2018 and early 2019 but not a complete derailing of the global recovery.

- Although not part of the US-China trade spat, Europe is looking fragile as growth has already slowed and the fiscal policy is less of a support compared with the US.

Tit-for-tat just started again

While we have been arguing for a ‘Grand Bargain' scenario since the US-China trade spat started, the recent development suggests we are moving more towards the ‘trade war' scenario. US President Donald Trump on Friday announced 25% tariffs on Chinese goods worth USD50bn within tech products and warned that the US would impose additional tariffs should China take retaliatory measures.

However, this did not stop China from saying immediately that it would retaliate with ‘equal scale and equal strength'. On Friday evening, China announced tariffs on US products of an equal amount and implemented them on the same date (6 July) as the US intends to implement tariffs on China. At the same time, China pulled back from the deal made with the US on 21 May, which, among other things, involved buying more US products worth USD70bn. The US products subject to tariffs in China will be mainly within agriculture, seafood and autos.

With the move China sends a clear signal that it will follow Trump one-to-one on whatever move he takes against China. Although China has a total of only USD130bn to put tariffs on (versus the USD500bn of Chinese imports into the US), China has other tools to use in the trade conflict. The strongest is probably a consumer boycott of US consumer goods but it can also use restrictions on investments in China by US companies as there are far more US companies in China than the other way around.

Is China’s threat of retaliation credible?

We believe so. China has clearly stated it does not want a trade war and knows it will cause pain in the short term. However, at the same time, it has tools domestically to weather the negative effects. Monetary policy can be eased quite significantly and there is also some room to ease fiscal policy, for example by compensating sectors hurt by the tariffs and thus also dampening the inflationary effect. China is also likely to beef up even more investment in technology and innovation, as it is becoming clearer that it will be more difficult to import high-technology products from the US in the future.

In addition, China believes a trade war will be as painful for the US – not least in the longer term, as US companies will be disadvantaged in the fastest growing market in the world. China gets confidence in this from the many protests by US corporates that are against the tariffs and favour a negotiated deal. China thus sees its hand as equally strong as that of the US.

Finally, China wants to send a clear signal to the US that it will not be ‘bullied’ or accept the bypassing of the multilateral trade system through the WTO. Even if China has to pay a price in the short term, what matters for growth in the long term is China’s productivity catching up. China aims to increase productivity by investing heavily in technology and education and any negative effects of the trade war would be likely to hold back growth for a while but not stop China’s continued rise in productivity if it sticks to reforms and investment in technology and education. This is exactly why China has a strong focus on the ‘reform and opening’ policy continuing and has put focus on technology and education.

As a trade war would damage both countries, our baseline scenario has all along been that a ‘Grand Bargain’ would be the outcome. However, if Trump believes he has the strongest hand and thus will win the chicken game or the US wants to protect US technology even if it comes at a cost, then a trade war could be the outcome

What’s next? Escalation increasingly likely

So what should we look for next? There are several things that will determine whether we are heading for a real trade war.

- Will Trump increase the amount of Chinese imports subject to tariffs to USD150bn? This is probably the most important thing to watch. If so, there will be a 60-day hearing period before it can be implemented but the announcement itself would be an escalation. China would signal immediately that it would strike back with ‘equal scale and equal strength’.

- How great will the restrictions be that Trump will put on Chinese investments into the US? This will be announced on 30 June and may trigger a response from China.

- How significant will the export controls on technology products to China be? These are also set to be announced on 30 June.

- Will the US and China resume the negotiations that began in May when a Chinese delegation was in the US and two US delegations went to Beijing?

While Trump has not yet responded to China’s retaliation, we see a high probability he will announce an increase in Chinese imports subject to tariffs to USD150bn soon. We also believe he will announce quite severe restrictions on Chinese investments in the US as well as further export controls on US tech exports to China on 30 June. With China retaliating, it would lead to a further escalation and using the term ‘trade war’ would then be justified

What could stop Trump from increasing the tariff amounts? The pressure from US corporates for him to back down from a tariff war is increasing (see ‘US business leaders warn on impact of Trump tariffs’, Financial Times, 18 June). There is a possibility this could persuade Trump to back down despite his signal that he would retaliate on Chinese counter-measures.

How it will affect the global economy

As we do not know where this will end ultimately, it is hard to put any clear numbers on it. However, we can make some quick back-of-the-envelope calculations on the short-term effects. Let us start with China.

The direct effect: USD50bn corresponds to 0.4% of Chinese GDP. Assuming the import contents of exports amounts to 50% and that we see a reduction in exports of the specific goods of 25%, it would subtract 0.05 percentage points from Chinese GDP, all else being equal. However, there are likely to be multiplier effects, as lower exports mean less investments and fewer jobs and thus less consumption. Consumption would also be hurt by higher inflation as the tariffs raise consumer prices. Including this, we end up with a negative effect of 0.1% of GDP.

The indirect effect: On top of this, there is also a sentiment effect as uncertainty increases during a trade war, which would hamper investments and consumer spending in sectors other than those hit directly by the tariffs. This is very hard to gauge but we assume it would be of a similar magnitude, so shaving off 0.1% of GDP.

The reallocation effect: There could also be a positive effect on investment. If US companies see a risk the tariff wall on US products will be permanent, it will give them greater incentive to move more production to China to avoid having to pay the tariff (and vice versa). This effect would probably take time though, so we discard it here as we are focusing on the short-term effects over the next year. The above effects so far amount to around 0.2% of GDP. However, there is another mitigating effect.

The policy response: With weaker growth, the People’s Bank of China can compensate by increasing liquidity and pushing down bond yields. China could also ease fiscal policy to fill the demand gap. These measures could, in theory, compensate fully but we assume they reduce the above effects by only half.

This leaves us with a net effect of 0.1% of GDP – hardly a big deal. If the amount subject to tariffs is USD150bn instead, the effect would be three times bigger and thus close to 0.3% of Chinese GDP. It would be felt but would still not be a disaster.

For the US, it is even harder to gauge the effects (how do you calculate the effect of a potential Chinese consumer boycott?) but they will probably be smaller as a percent of GDP, simply because GDP at USD18trn is 50% higher in the US than in China, where GDP is USD12trn. Going through the same effects as with China takes us to 0.2% of GDP in the scenario of tariffs on goods worth USD150bn on US imports.

The weighted effect is thus around 0.25% of GDP and as the two countries are around 40% of global GDP, it takes us to 0.12% of global GDP. On top of this, there are likely to be negative sentiment effects in the rest of the world, which we put at 0.1% of GDP. In sum, we end up at around 0.2% of global GDP that could be shaved off in this scenario.

It is hardly a disaster but it is still likely to be felt over the next six months, as the effects will probably be front-loaded, as the impact of companies postponing investments could come quite quickly.

Europe would be hit by the sentiment effect as well as by lower growth on export markets and, given the soft data seen recently and higher uncertainty already from Italy and US tariffs, we see Europe as quite fragile in the current environment. The US is probably more resilient as the fiscal boost is currently creating some support to growth.

In the medium to longer term, a world with higher tariffs would reduce global productivity and increase inflation. It would disrupt the global supply chain that has been built up over the past few decades and while it could lead to more investment as production might move within a tariff wall, it would also imply that previous investments would have to be written off. This would hurt corporate profits and thus equities.

Why is Trump leaving the negotiation track?

Why is Trump leaving the negotiation track already, when there seemed to be agreement to stop tariff threats while negotiations were ongoing and Trump got more concessions from China than any other president has achieved?

First, Trump faced significant criticism from fellow Republicans and Democrats for the deal he made with China on 21 May. Being a long-term critic of China and heading into mid-term elections, Trump may have had second thoughts about the negotiations. Second, the US tariffs are not just about a big trade deficit with China. They are as much about a long-term rivalry between the US and China, which has intensified under the Trump administration and is set to continue as China grows bigger and in the coming decades surpasses the US as the biggest economy in the world. China is seen as a strategic rival and consensus is growing that the US needs to take action to protect US technology and respond to theft of intellectual property.

The rivalry was very clear in the US National Security Strategy from December 2017, in which Trump described China (and Russia) as a ‘revisionist power’ seeking to ‘shape a world antithetical to US values and interests’. It also said ‘We will protect our national security innovation base from those who steal our intellectual property and unfairly exploit the innovation of free societies’.

For the same reasons, the US is set to put restrictions on Chinese investments in the US, when Trump announces the result of an investigation into this area on 30 June. On the same day, the US is also scheduled to release export controls within technology. When it comes to technology, Trump will insist on protectionism versus China and the tariffs imposed now do not seem likely to be removed in a negotiation. Trump sees this protection as fully legitimate. For the same reason, he sees Chinese retaliation as illegitimate, which is why we expect him to step up tariffs further soon.

Oil recovers as OPEC might raise output by only 300k to 500k barrels a day

According to a Bloomberg report, OPEC members could finally compromise of raising production by 300k - 600k barrels a day over the next few months. Such increase will likely be taken up mainly by those with spare capacity, like Saudi Arabia, Russia and the United Arab Emirates. But it's unsure whether this can be the consensus in the upcoming OPEC+ meeting in Vienna this week.

Russia is proposing an increase of of 1.5m barrels a day. And the increase would be shared proportionally among all members. But some countries like Venezuela would be unable to raise the output.

Oil price responded positively to the news. WTI crude oil dipped to as low as 63.59 earlier today but is now back at 64.69.

Forex Forecast and Cryptocurrencies Forecast for June 18-22, 2018

First, a review of last week’s forecast:

EUR/USD. Billionaire George Soros is confident that further strengthening of the dollar will lead to a new financial crisis. At the same time, 10 out of 60 analysts interviewed by Reuters believe that the growth of the US currency will be completed within a month, 35 are confident that the strengthening of the dollar will last at least until the fall, and another 15 give the USD growth until the end of the year. Experts from ABN Amro are among the latter, they believe that the euro should fall to the level of 1.1000, and only then, in 2019, it will be able to restore some of the lost ground.

Interestingly, the decision of the US Federal Reserve to raise the interest rate to 2%, which was announced last week, did not surprise anyone. The information that this year should expect two more similar increases, and three in the future did not cause a stir either. The euro quickly recovered and, moreover, demonstrated growth against the background of these events to the level of 1.1850.

But the ECB's decision to extend the quantitative easing (QE) regime instantly dropped the euro against the dollar by more than 300 points. Our experts had named the level 1.1570 as the main support zone, to which the EUR/USD did rush. Due to the unusually powerful bearish impulse, by inertia, it even dropped 30 points lower, however, after coming to its senses, it soon turned around and completed the trading session at 1.1610;

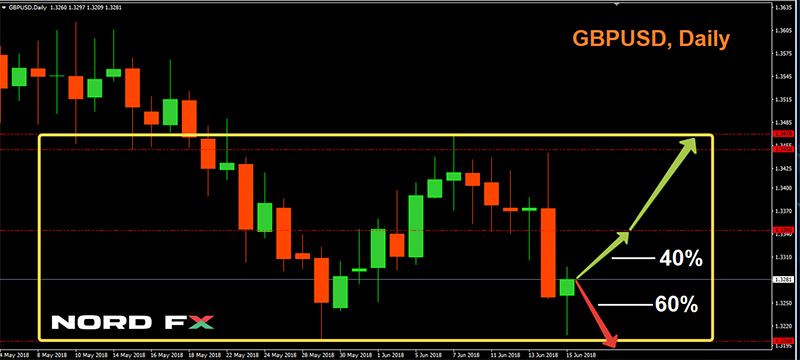

65% of analysts expected further correction of the GBP/USD to the level of 1.3615, after which it had to resume its movement to the south. However, the pair could not rise even above the level of 1.3445 and rushed down again, trying, as on May 29, to break through support in the zone of 1.3200. And, just like in May, the attempt failed, after which the pair returned to zone 1.3280;

USD/JPY. 50% of analysts supported the growth of this pair, referring to the horizons as 110.25 and 111.40 as resistance, between which, at 110.60, it completed the five-day period;

Cryptocurrencies. In recent days, following their leader bitcoin, almost all of them have broken through important support levels and moved further south, testing new horizons. Thus, BTC managed to break through supports of $7,125 and $7,000 and reached a weekly low of $6,110 on June 14, then it managed to win back about 7% and rise to $6,575. Similar dynamics were demonstrated by the remaining virtual currencies included in the TOP-10 market capitalization.

Since the beginning of the year, the crypto market capitalization has decreased by 44.3% (from $611 billion to $340 billion). Just over the night of 10 to 11 June, the market shrank by another $25 billion. Many traders and analysts tried to explain this collapse by the Coinrail exchange in South Korea being hacked, but in reality, it lost only $40 million, so the theft was most likely just an excuse for another lowering the price of crypto-coins.

As for the forecast for the coming week, summarizing the opinions of a number of analysts, as well as forecasts made on the basis of a variety of methods of technical and graphical analysis, we can say the following:

In addition to the extension of the QE program mentioned above, the ECB's decision to leave the benchmark interest rate at a record low of 0%, and the deposit rate at -0.4%, also exerts strong pressure on the euro. It was also stated that these rates will not be raised "at least until the summer of 2019". At the same time, Mario Draghi admitted that the economy of the Eurozone in 2018 will not return to the forecasted level of growth.

All this, coupled with the success of President Donald Trump's economic policy, creates significant prerequisites for the further strengthening of the dollar. That's why 65% of experts expect that in the coming week the EUR/USD will test the level of 1.1500 and, if successful, could drop another 100 points lower. 90% of the oscillators on H4 and D1 also agree with this development.

As for the remaining 35% of experts, in their opinion, the pair still has chances to return to zone 1.1825, but the likelihood of such a development will depend on what the ECB Head Mario Draghi and the Fed, J. Powell, will say in their statements earlier this week;

it is clearly visible on the GBP /USD chart that the pair moves in the lateral channel 1.3200-1.3470.for the fourth week in a row. At the same time, 60% of analysts believe that, following the euro, the British pound will also continue its decline. In their view, the pair GBP/USD may as well break through the lower boundary of this channel and move to the level of 1.3050-1.3200. This scenario is supported by graphical analysis on D1 and the absolute majority of indicators.

An alternative point of view, represented by 40% of experts, suggests the movement of the pair in the side corridor 1.3200-1.3345. The next resistance is in the zone is 1.3400.

On Thursday, June 21, the next meeting of the Bank of England should take place. However, with a high probability, it will not present any surprises, so it is not worth it to expect serious exchange rate jumps at this moment;

A day earlier than their British counterparts, the Committee on Monetary Policy of the Bank of Japan will hold a meeting. As for the experts, two-thirds of them cautiously support the small growth of the pair USD JPY to the area of 111.00-111.50. The next resistance is 112.00.

This time, a third of analysts, graphic analysis on H4 and D1, as well as 20% of oscillators, side with the bears, signalling the pair is overbought. In case their scenario turns out to be correct, the pair is expected to decline first to support 109.40, and then, possibly, further - to levels 109.00 and 108.50;

Most of the forecasts for basic cryptocurrencies can be reduced to just two sentences: 1) in the near future they will continue to fall, and 2) they should grow in the long term. For example, according to the forecast of Fundstrat Global Advisors analysts, the bitcoin can fall to the level of $ 3,250. However, even this, in their opinion, "will not break the long-term ascending trend of the first cryptocurrency".

The closest target for BTCUSD, according to the founder of Onchain Capital Ran Neuner, is the level of $5,900. The optimistic part of his forecast is that "if the price of the bitcoin reaches 20, 40 or 80 thousand dollars within a few years, then no one will be worried about whether it was bought for $6,000 or $6,500. Only traders working on a scale of less than a year should be concerned about the current drop in the market price. "The only thing that the expert didn't specify is when this long-awaited take-off to 80,000 takes place.

Markets In Risk Averse Mode After Tariffs Announcement

- US and China trade spat heats up;

- Stocks in the red but FTSE outperforms on weaker GBP;

- OPEC meeting and central bank speeches eyed this week.

We're seeing a slightly risk averse tone in financial markets at the start of the week after the trade spat between the US and China ramped up over the weekend. Both countries have laid out plans to impose tariffs on one another on 6 July which is making investors a little uncomfortable, more so due to the potential for the situation to escalate further than the tariffs themselves. The question now is how much pain both sides will be willing to inflict on the other – and themselves in the process – before coming to an agreement that removes tariffs and eases investor concerns.

It's possible that with the US economy doing so well and President Donald Trump last week securing a significant victory following his meeting with North Korean leader Kim Jong Un, he may be willing to use some of this political credit he's earned and make the necessary economic sacrifice in order to force China into concessions. That's certainly the impression he's giving.

While we're only seeing moderate risk aversion in the markets at the moment, it is enough to drag European stocks markets down with French and German indices off between 0.5% and 1%. The FTSE is holding up ok although this is being aided by the weaker pound which supports the large number of external looking companies in the index.

Traditional safe havens are naturally doing well this morning with Gold up a couple of dollars and the yen in the green against the dollar euro and pound.

Oil remains well of its highs as traders look ahead to the OPEC meeting later in the week with the cartel likely to discuss reducing or even ending its coordinated output cut which was imposed in an attempt to bring inventories back in line with the five-year average which has been successful. An increase in production from the OPEC nations and others including Russia involved in the deal will be welcomed by Trump who has recently been berating them for pushing prices higher, despite the fact that part of this has been driven by US sanctions on Iran.

It's going to be a quiet day on the data side but we will hear from a number of prominent central bankers which is very much going to be the theme of this week. Incoming Bank of New York Fed President John Williams will be speaking later on in the day, as will his colleague Raphael Bostic. We'll also hear from ECB President Mario Draghi who's due to appear on a number of occasions this week.

Bundesbank: Projection paints a picture of an ongoing economic boom

In the Bundesbank's June Monthly Report published today, it noted "all in all, the projection paints a picture of an ongoing economic boom, in which increasing supply-side bottlenecks are reflected in strong wage growth and in higher domestic inflation." It projected German GDP growth to slow to 2.0% in 2018, 1.9% in 2019 and then 1.6% in 2020. HICP inflation is projected to be rather steady, at 1.8% in 2018, 1.7% in 2019 and 1.8% in 2018.

But Bundesbank also warned that "risks outweigh opportunities". President Jens Weidmann noted that "uncertainties regarding the prospects for the German economy are considerably greater than they were." And, downside risks relating to the external environment outweigh the effects resulting from the probably more expansionary fiscal policy in Germany.

In particular, exports and commercial investment are likely to see weaker growth. employment growth is dampened by growing lack of skilled workers. And that tens to "brake" the rise in household disposable incomes.

Here is the link to the monthly report.

Here is the Outlook for the German economy – macroeconomic projections for 2018 and 2019 and an outlook for 2020

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 1.1569

The consolidation pattern above 1.1540 is still on the run, so a I favor a rise towards 1.1650.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.1650 | 1.1830 | 1.1510 | 1.1480 |

| 1.1720 | 1.2060 | 1.1480 | 1.1300 |

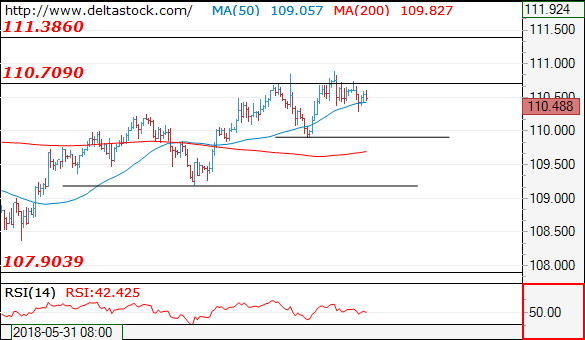

USD/JPY

Current level - 110.48

Intraday allow a dip to 110.10, which should be followed by a break through the trigger at 110.70, towards 111.40.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 111.40 | 111.40 | 109.90 | 107.80 |

| 111.40 | 114.40 | 109.20 | 106.70 |

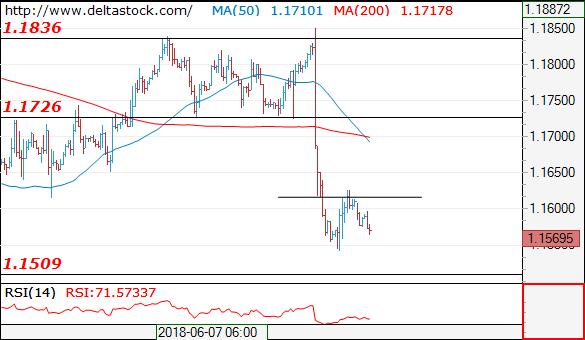

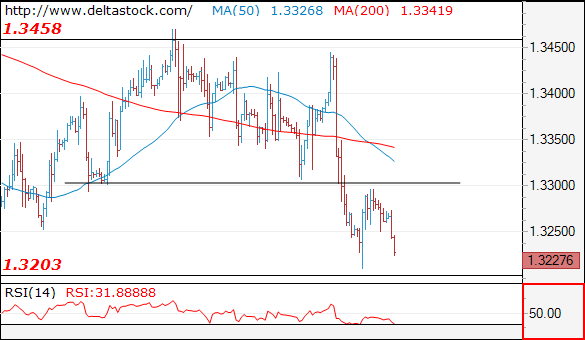

GBP/USD

Current level - 1.3227

My outlook is positive above 1.3200, for a second leg towards 1.3300 hurdle.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3300 | 1.3618 | 1.3203 | 1.3210 |

| 1.3460 | 1.3990 | 1.3110 | 1.3040 |

Euro Trading Sideways, ECB Forum Next

EUR/USD has ticked lower in the Monday session. Currently, the pair is trading at 1.1597, down 0.10 on the day. In economic news, it’s a quiet start to the week, with no major releases. The highlight of the day is the opening of the ECB Forum, which kicks off with a speech from ECB President Mario Draghi. On Tuesday, Draghi will participate in a panel discussion. Over in the US, the focus will be on construction numbers, with the release of Building Permits and Housing Starts.

All eyes are on the ECB Forum, where central bankers will converge to rub shoulders and discuss policy. In addition to host Mario Draghi, we’ll also hear from Fed Chair Jerome Powell and Bank of Japan Governor Haruhiko Kuroda. At last year’s meeting, the euro posted strong gains after hawkish remarks from Draghi, so traders will be listening carefully in case Draghi again shakes up the currency markets. Draghi will likely make mention of last week’s ECB meeting, in which he spoke of possible headwinds for the eurozone economy.

The euro has steadied, after posting sharp losses late last week. EUR/USD slipped 1.9% on Thursday, as investors gave a thumbs-down to a dovish rate statement from the ECB and remarks from ECB President Draghi. The ECB pledged to taper its bond-purchase program to EUR 15 billion/mth, in October, down from the current pace of EUR 30 billion/mth. The program will wind up at the end of the year. However, investors detected a ‘dovish flavor’ to the announcement, as the ECB added that interest rates would remain steady “at least through the summer of 2019”, giving policymakers plenty of wiggle-room to delay any rate hikes. The markets were anticipating a rate hike shortly after the end of the bond-purchase program, so this announcement was a disappointment. Draghi sounded dovish in his press conference, saying that the eurozone economy was facing “increasing uncertainty”. Draghi was likely referring to the G-7 meeting which ended in disarray as well as the election of a euro-sceptic government in Italy. The ECB also lowered its growth forecast for the eurozone to 2.1%, down from 2.4% earlier this year.

Trade Tensions Take Centre Stage

Risk sentiment deteriorates amid escalating trade tensions

With the ECB and Fed meetings in the rear mirror, investors switch attention to the trade war between the US and China. On Monday morning, safe havens assets, such as the Japanese yen and Swiss franc, were better bid, while the greenback extended gains against most its peers. The single currencies currency continued to suffer from the ECB’s decision to hold rate until the end of summer 2019, at least. After falling more than 2% last week, the single currency stabilised around 1.1580.

USD/CHF treaded water around 0.9975, while USD/JPY fell 0.13% to 110.53. AUD/USD is approaching the key $0.7412 support (low from May 9th 2018). A break of the later support would open the road towards the next one that lies at $0.7329 (low from May 9th 2017). Over the past two weeks, the Australian dollar has suffered greatly from escalading trade tensions between China and the US as could dampen significantly Australia’s economic outlook. Indeed, as an open economy that relies heavily on exports, a global trade war could have dramatic consequences; especially should the situation between the US and China - Australia’s biggest trade partner - spirals further.

Japan exports rise despite trade tensions

Regardless of the current trade tension situation, the Japanese economy manages to maintain steady exports growth for four consecutive months. Estimated at 8.10% y/y in May, Japan exports moderate growth does not show clear signs of trade tensions so far, with Food (+25.70%), Raw Materials (+13.50%), Minerals (+33.60%) and Chemicals (+12.50%) being the largest contributors. In spite of intensifying retaliatory threat measures between its key partners, Japan’s exports towards China and the US rose by +8.60% and +16.80% respectively, a rather good news for Prime Minister Shinzo Abe who’s been striving for tighter relationships with both nations.

Due to increasing domestic demand in the country, we would consider to treat May adjusted trade balance data with sensitivity. Indeed, given at JPY -296.8 billion (USD -2.73 billion), a major decrease after JPY +453.94 billion (USD +4.16 billion) in prior month, May trade balance is essentially explained by recent unusual import numbers, strongly boosted by oil, aircraft and pharmaceutical product imports.

Accordingly, recent trade data are suggesting a rather decent growth trend for the world largest economies, supported by strong domestic consumption. On Japanese side, we expect a rapid bilateral trade resolution with the US and continued healthy trade relation with China.

Currently trading at 110.54, the USD/JPY is gaining strength, approaching the 110.80 range and expected to progress further since recent bounce from 109.92 (14/06/2018 low).

Bitcoin / Dollar The Downside Prevails As Long As 6581 Is Resistance

Our pivot (invalidation) point is at 6581.

Our preference The downside prevails as Long as 6581 is resistance.

Alternative scenario Above 6581, look for 6794 and 6921.

Comment The RSI is below its neutrality area at 50. The MACD is below its signal line and negative. The configuration is negative. Moreover, the pair is trading under both its 20 and 50 MAs (respectively at 6450 and 6507).

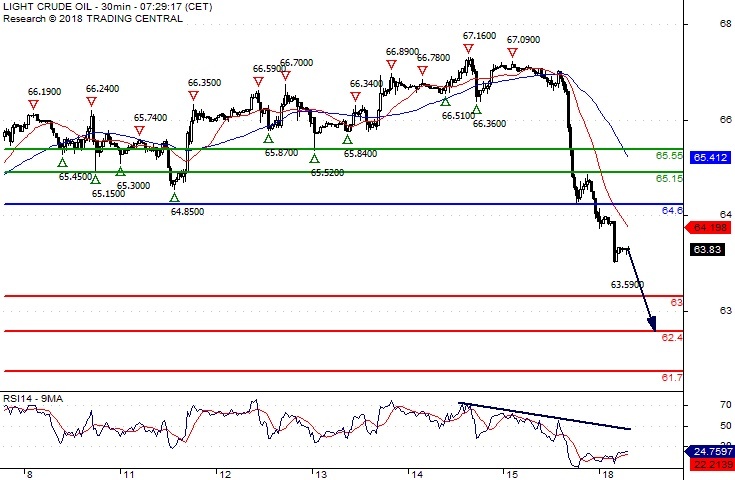

Crude Oil The Downside Prevails

Pivot (invalidation): 64.60

Our preference Short positions below 64.60 with targets at 63.00 & 62.40 in extension.

Alternative scenario Above 64.60 look for further upside with 65.15 & 65.55 as targets.

Comment The RSI has broken down its 30 level. The prices are trading below both 20-period and 50-period moving averages.