Sample Category Title

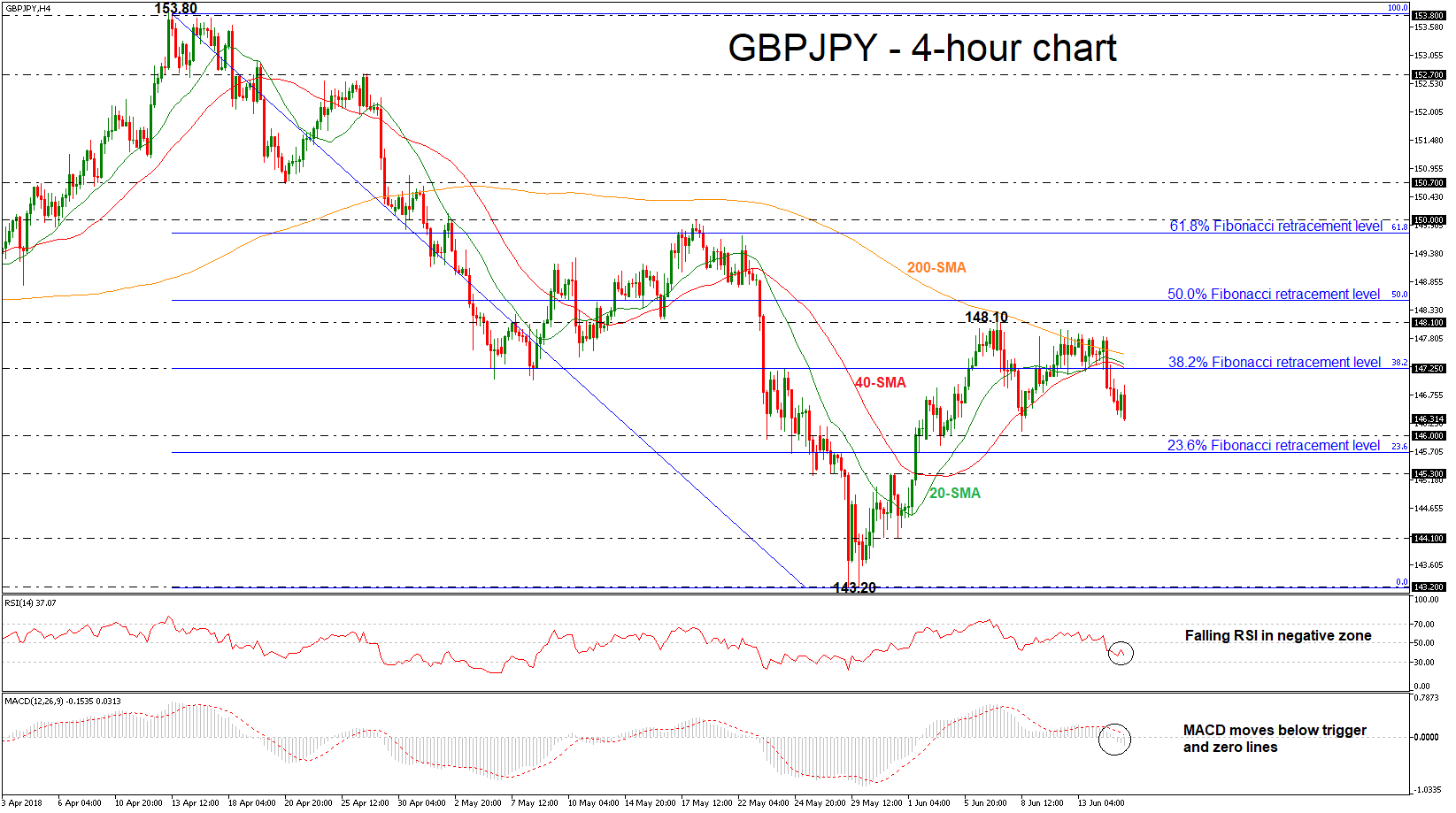

GBPJPY Retreats Sharply, Maintains Short-Term Bearish Bias

GBPJPY plunged below the 38.2% Fibonacci retracement level of the downleg from 153.80 to 143.20, around 147.25, which overlaps with the 40-simple moving average in the 4-hour chart. The aggressive bearish rally started during yesterday’s session and has shifted the near-term bias from positive to negative. Also, the momentum indicators are supportive of the bearish picture.

In the short-term, the Relative Strength Index indicator dropped below the 50 threshold after it bounced off the positive area, while the MACD oscillator lies below the trigger and zero lines.

To the downside, immediate support is being provided by the 146.00 psychological level. Moreover, should prices dip lower again, the next support would likely come from the 23.6% Fibonacci retracement around 145.70. A drop below this level would signal the start of a deeper bearish phase until the 145.30 barrier.

Should the market surpass the 38.2% Fibonacci, resistance could be met at the 148.10 hurdle, taken from the peak on June 7. If there is a jump above this region, the next major resistance would come from the 50.0% Fibonacci of 148.50. A successful close above this level could see a retest of the 61.8% Fibonacci of 149.75.

Overall, in the medium-term, the pair is continuing the negative outlook after the pullback from the 153.80 resistance level on April 13.

ECB Announces QE End, But Dovish On Hikes, Trade Developments Eyed

Here are the latest developments in global markets:

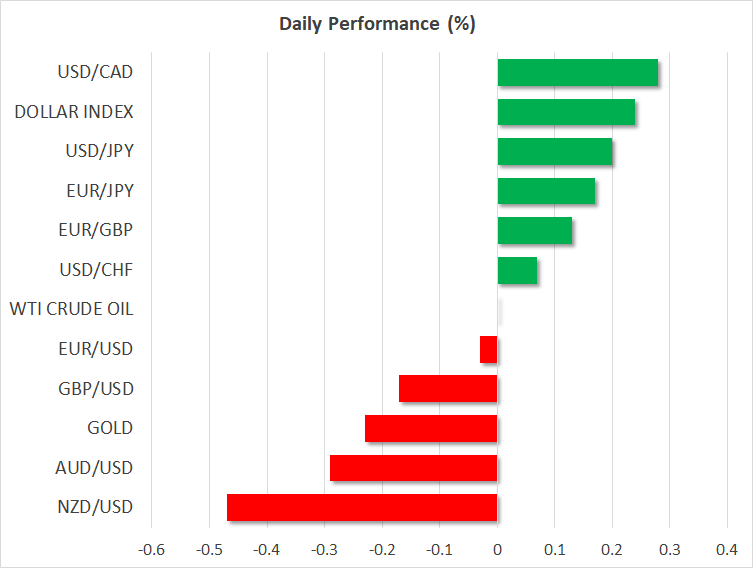

FOREX: The US dollar index is up by almost 0.25% on Friday, touching a fresh 7-month high and extending the spectacular gains it posted yesterday as the currency with the heaviest weight in the index – the euro – collapsed after the ECB policy decision (see below). The yen was on the back foot as well, falling by 0.2% versus the dollar, after the BoJ downgraded its inflation view at its own policy gathering overnight.

STOCKS: US markets closed mixed on Thursday. The Nasdaq Composite outperformed to rise by 0.85%, bringing the tech-heavy index to a fresh all-time high. The S&P 500 gained 0.25%, but the Dow Jones pulled back by 0.10%. Futures tracking the Dow, S&P, and Nasdaq 100 are currently pointing to a lower open today, though note the direction of these indices today will probably depend on whether the US unveils its list of tariffs against China. Asian markets were mostly lower on Friday, perhaps as the threat of US tariffs cast a shadow. In Hong Kong, the Hang Seng fell 0.13%, while South Korea's Kospi 200 was down by 0.79%. In Japan though, the Nikkei 225 and Topix climbed by 0.50% and 0.29% respectively, buoyed by a weaker yen brightening the outlook for exporting firms. In Europe, futures tracking all major indices suggest a slightly higher open, with the only exception being the British FTSE 100.

COMMODITIES: In energy markets, oil prices were practically flat on Friday, after posting some modest gains in the previous session. The liquid looks set to close the week in positive territory, with reports on Thursday that major Libyan oil ports were closed after attacks counterbalancing concerns of an imminent production increase by OPEC and associated producers. The instability in Libya is expected to lead to a supply loss of 240,000 barrels per day. In precious metals, gold is down by nearly 0.25% today, currently trading just above the $1,298 per ounce level. The metal tried to break above its crucial 200-day moving average at $1,307 yesterday, but was rejected as the dollar gained ground after the ECB decision. It could attempt another test of that territory today should the US announce tariffs against China, triggering another bout of risk aversion.

Major movers: ECB announces end to QE, but euro collapses on dovish rate signals

The European Central Bank (ECB) kept interest rates unchanged yesterday, and announced an end to its asset purchase (QE) program. The Bank will continue buying assets at a pace of EUR 30bn per month until the end of September, at which point it will halve its monthly purchases to EUR 15bn until the year ends, and then stop them altogether. While that would have been a hawkish signal by itself, the Bank also stressed interest rates will remain unchanged at least through the summer of 2019, which was somewhat later than markets expected. Moreover, it included language to tie the QE tapering with the quality of incoming data, meaning it could decide to extend the program again if the outlook becomes less favorable.

These signals sent the euro sharply lower on the decision, and the currency continued to collapse throughout President Draghi's press conference. Euro/dollar fell by roughly 280 pips on the day to hit a two-week low of 1.1560, as the ECB chief maintained a cautious tone on practically every issue. He mentioned trade risks, suggested the economy's soft patch may extend for longer than expected, and emphasized the high degree of uncertainty policymakers are operating under, making the case for keeping policy optionality at every step. Overall, he sent the message that any rate increase is still far, far away, and conditional on economic forecasts materializing, which apparently dwarfed everything else in the eyes of investors.

Strikingly, sterling/dollar plunged in the aftermath of the ECB decision as well, which implies the pound could not gain as much as the dollar from a bleeding euro – a testament to the fragile sentiment currently surrounding the British currency.

Overnight, the Bank of Japan (BoJ) kept its ultra-loose policy framework unchanged via an 8-1 vote, providing little-to-no fresh guidance. It downgraded its view of consumer inflation, now seeing it “in a range of 0.5 to 1 percent” from “around 1 percent” previously. The yen moved lower on the decision, though the move was relatively minor. BoJ still seems unlikely to even consider altering its stimulus program anytime soon, which in isolation, is a factor arguing for a weaker yen from a relative rates perspective, especially against currencies of nations who are normalizing policy, like the dollar.

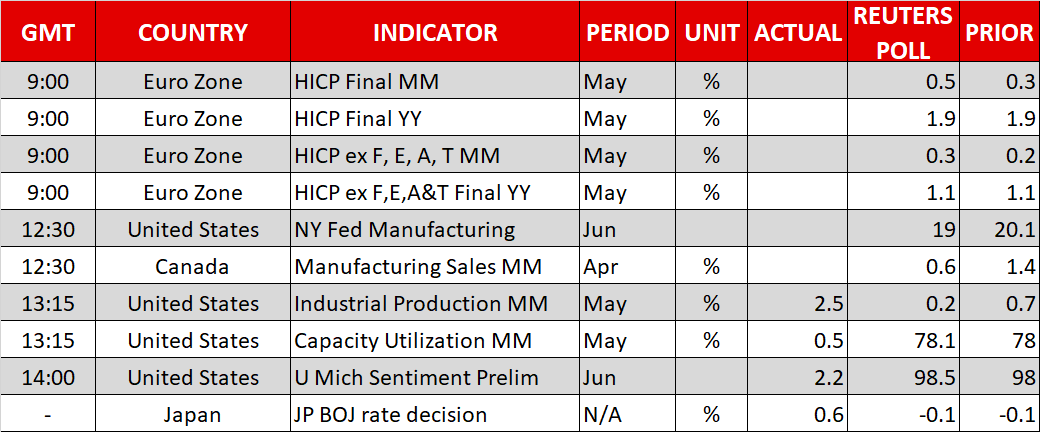

Day ahead: Eurozone inflation, US industrial production and University of Michigan survey due; trade developments eyed

Revised eurozone inflation figures, US industrial production data and the University of Michigan's survey on consumer sentiment are some of the releases attracting attention out of Friday's calendar. Trade developments though, that have the capacity to escalate tensions between the US and China, could well end up dominating attention during today's trading.

The eurozone's final inflation numbers for the month of May are scheduled for release at 0900 GMT. Annual growth in the headline Harmonised Index of Consumer Prices (HICP) that uses a common methodology across EU countries is expected to be confirmed at 1.9% y/y. The core measure that excludes volatile food, energy, alcohol and tobacco items is anticipated at 1.1%, again the same as in the preliminary release.

At 1230 GMT, the New York Fed manufacturing index will be made public out of the US; a decline is projected in the index during June relative to May. Canadian manufacturing sales pertaining to the month of April will be released at the same time.

Perhaps of more importance out of the US are industrial production numbers for May due at 1315 GMT. Industrial output is projected to slow compared to April, while manufacturing production – a subset of industrial output – will also be closely watched. Data on May's capacity utilization are also due at the same time.

Lastly in terms of important releases, the University of Michigan's preliminary survey gauging consumer morale in June is slated for release at 1400 GMT and is forecast to show a slight improvement in sentiment relative to May. Meanwhile, the surveys sub-indexes on inflation expectations will also be attracting attention.

An expected announcement on the Trump administration's list of $50 billion of Chinese goods imported into the US and targeted for higher tariffs is on the horizon on Friday. China's response will be awaited; the trade war saga might receive a new chapter, diverting funds into perceived safe-haven assets to the detriment of riskier ones. The world's second-largest economy said it will walk away from commitments made in bilateral talks with the US if the Trump administration eventually pushes forward with the imposition tariffs.

In the meantime, politics might be at play in the UK with PM Theresa May potentially on the receiving end of a Tory rebellion, as some members within her party favoring a softer Brexit were left unsatisfied – to say the least – in relation to efforts for a compromise with the government on key Brexit legislation.

In energy markets, the US Baker Hughes will be hitting the markets at 1700 GMT.

In terms of policymakers' appearances, ECB executive board member Benoit Coeure and Dallas Fed President Robert Kaplan (non-voting FOMC member in 2018) will be giving speeches at 0845 GMT and 1730 GMT respectively.

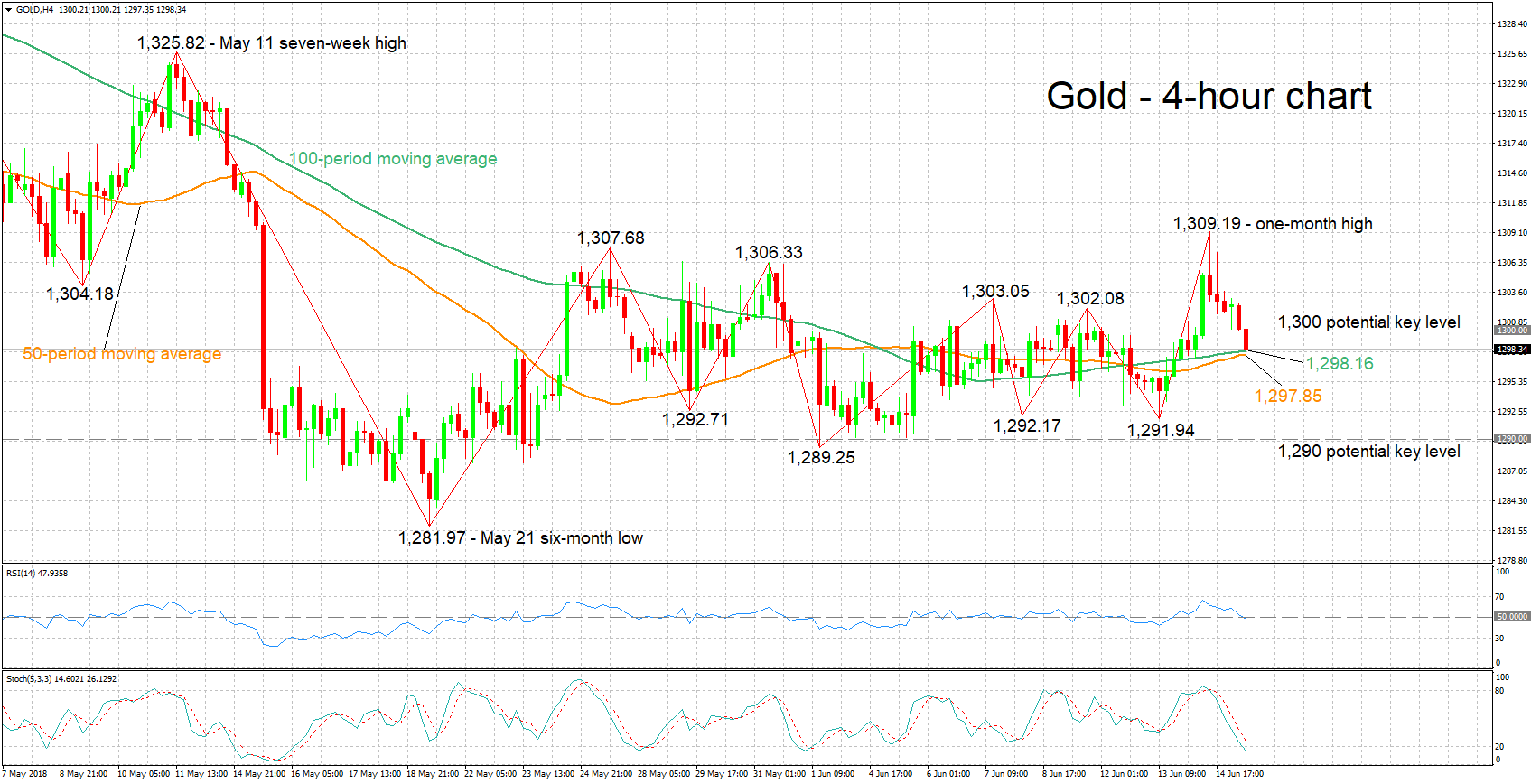

Technical Analysis: Gold looking bearish in short- and very short-term

Gold has lost ground after touching a one-month high of 1,309.19 during Thursday's trading. The RSI is declining in support of a negative short-term picture, while the stochastics are also giving a bearish signal in the very short-term; the %K line is below the slow %D one and both lines are heading lower.

Rising trade uncertainties may divert funds into the perceived safe-haven asset. Resistance to advances may come around the 1,300 round figure that may carry psychological significance (the area around this encapsulates numerous peaks from the recent past as well – see chart), with yesterday's one-month high of 1,309.19 being eyed in case of stronger gains.

Receding trade risks on the other hand are likely to weaken gold, benefitting riskier assets. Support to declines could come around the current levels of 100- and 50-period moving average lines, at 1,298.16 and 1,297.85 respectively. Attention would next turn to the region around 1,290 which captures a number of bottoms from previous days and weeks.

The greenback's direction can also affect gold; given that the yellow metal is denominated in dollars, a stronger US currency renders it less attractive to non-dollar holders.

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

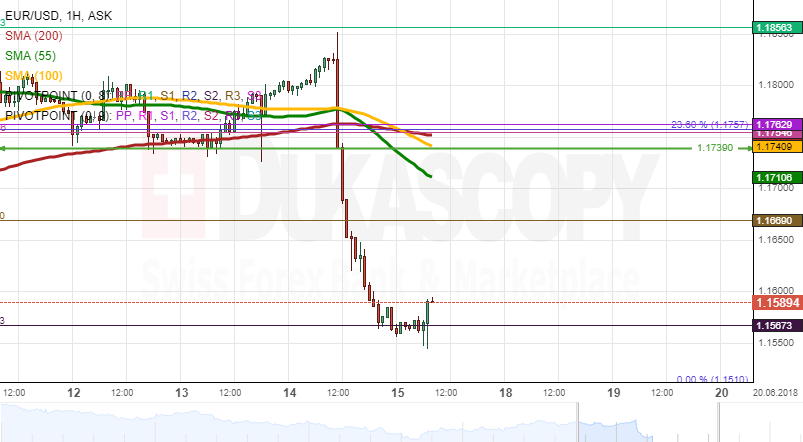

EUR/USD

Current level - 1.1569

The spike to 1.1850 was followed by a massive sell-off and currently the pair is approaching 1.1510 lows. The slide is running out of steam, so I favor a corrective rebound towards 1.1650 and even probably to the major 1.1720. Minor intraday resistance lies at 1.1616.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.1650 | 1.1830 | 1.1510 | 1.1480 |

| 1.1720 | 1.2060 | 1.1480 | 1.1300 |

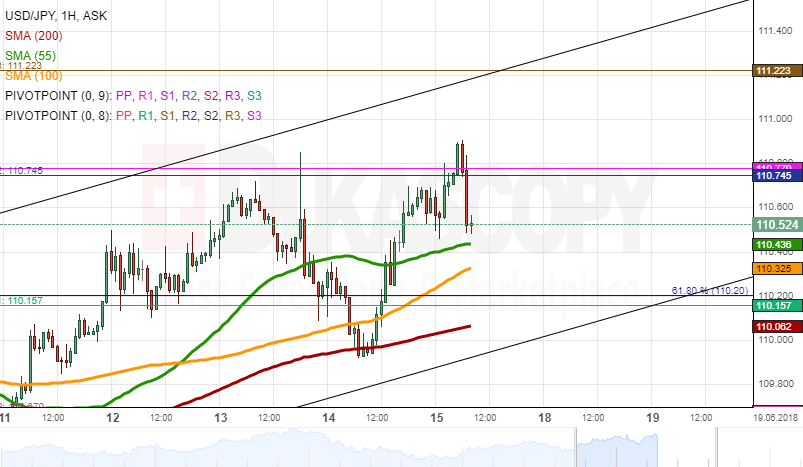

USD/JPY

USD/JPY

Current level - 110.70

My outlook here is counter-trend below 111.40, for a dip to 109.20.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 111.40 | 111.40 | 109.90 | 107.80 |

| 111.40 | 114.40 | 109.20 | 106.70 |

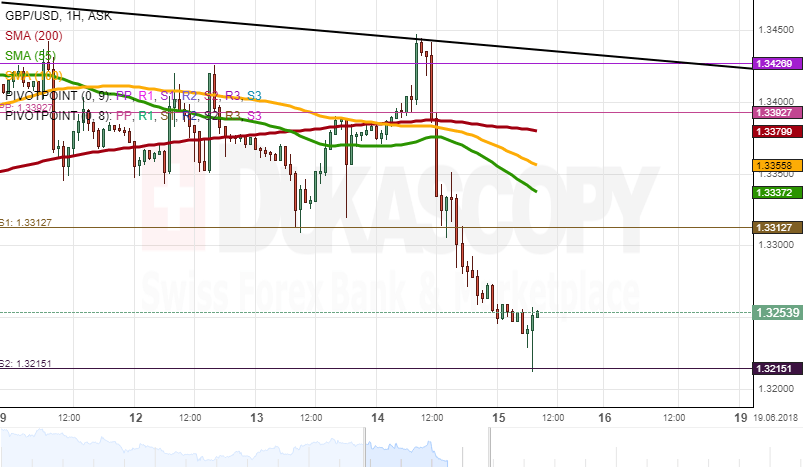

GBP/USD

Current level - 1.3234

Yesterday's failure at 1.3460 provoked a reversal and a sharp sell-off to 1.3203 lows. Intraday I favor a corrective rebound towards 1.3300 resistance and an eventual break through 1.3200 will challenge the next support around 1.3040.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3300 | 1.3618 | 1.3203 | 1.3210 |

| 1.3460 | 1.3990 | 1.3110 | 1.3040 |

Euro Plunges On Dovish ECB, Eurozone CPI Matches Forecast

EUR/USD has steadied in the Friday session, after sharp losses on Thursday. Currently, the pair is trading at 1.1603, up 0.30% on the day. On the release front, German WPI posted a strong gain of 0.8%, well above the estimate of 0.3%. In the eurozone, Final CPI rose to 1.9% and Final Flash CPI climbed to 1.1.%, as both readings matched their estimates. As well, the eurozone trade surplus narrowed to EUR 18.1 billion, shy of the estimate of EUR 21.2 billion. In the U.S, the Empire State Manufacturing Index is expected to drop to 19.1 points. We’ll also get a look at UoM Consumer Confidence, which is forecast to soften to 98.5 points.

The euro plunged to a 2-week low on Thursday, in response to a dovish rate statement from the EC and remarks from ECB President Draghi. The ECB pledged to taper its bond-purchase program to EUR 15 billion/mth, in October, down from the current pace of EUR 30 billion/mth. The program will wind up at the end of the year. However, investors detected a ‘dovish flavor’ to the announcement, as the ECB added that interest rates would remain steady “at least through the summer of 2019”, giving policymakers plenty of wiggle-room to delay any rate hikes. The markets were anticipating a rate hike shortly after the end of the bond-purchase program, so this announcement was a disappointment. Draghi sounded dovish in his press conference, saying that the eurozone economy was facing “increasing uncertainty”. Draghi was likely referring to the G-7 meeting which ended in disarray as well as the election of a euro-sceptic government in Italy. The ECB also lowered its growth forecast for the eurozone to 2.1%, down from 2.4% earlier this year.

As widely expected, the Federal Reserve raised interest rates by a quarter-point, to a range between 1.75 percent and 2.00 percent. Fed Chair Jerome Powell sounded hawkish in his press conference, saying that the economy was performing well and that “overall outlook for growth remains favorable”. This message echoed the rate statement, in which policymakers said that “economic activity has been rising at a solid rate”, pointing to stronger consumer spending and business investment. What was may have been the most notable development was that the Fed rate projections were revised upwards, predicting two additional rate hikes in 2018, for a total of four hikes. Until now, the Fed had projected three rate hikes this year. This represents a nod to the strength of the U.S economy and could boost the dollar against its rivals.

EURUSD Analysis: Plunges 2.28% After ECB Decision

Any bullish signals shown by technical indicators early on Thursday were swiped away mid-session following the ECB monetary policy decision. Even though the main benchmark rate was in line with expectations, comments by the ECB President Draghi of continuous low-interest-rate environment and end of the Bank's asset purchase program weighted heavily on the Euro.

As a result, the rate lost 2.28% during the previous session and consequently fell down to the weekly S2 at 1.5073. Given that the pair has been lingering near this area for several hours and technical indicators are located in the strongly oversold territory, it is likely that bulls try to regain some lost positions today.

A possible target is the 1.17 area which is limited by the 100-period (4H) SMA. Hourly moving averages are likewise located nearby.

GBPUSD Analysis: Weakens 1.60% Since Mid-Thursday

The Pound surpassing the 55-, 100– and 200-hour SMAs on Thursday morning signaled to a possible surge during the given session. This assumption, however, was abandoned when the rate reached the 200-period (4H) SMA at he 1.2450. This was followed by a massive 1.60% plunge down to the weekly S2 at 1.3215 at the time of this analysis.

It is likely that bears still push the Sterling lower within the following hours until the psychological 1.32 level is reached. Technical indicators are located at historic lows; therefore, some upside potential is apparent today.

The most probable daily high should be all the three SMAs and the weekly PP circa 1.3360. The 55– and 100-period moving averages are likewise located in this territory.

Chinese foreign ministry warns on immediate action against US unilateralism and protectionism

Below is the transcript of Chinese foreign ministry spokesman Geng Shuang's reply to question regarding US tariffs during a regular press briefing.

Q: It is reported that US officials said President Trump has decided to approve the value of 50 billion US dollars of Chinese exports to the US goods to levy a 25% tariff, the decision will be formally announced Friday US time. Did the U.S. inform the Chinese side? The Chinese side has repeatedly stated that if the U.S. side introduces trade sanctions including the increase of tariffs, all trade and economic achievements negotiated by the two parties will not take effect. Yesterday, State Councilor and Foreign Minister Wang Yi stated that if the United States chooses the idea of confrontation and double lose, China is ready. Do you have any further response to this? What kind of countermeasures will China take?

A: Yesterday, U.S. Secretary of State Pompeo visited China during the visit and exchanged views with China on Sino-U.S. relations and important international and regional issues, including China-US economic and trade issues. Please read carefully the relevant news released by the Chinese side. China’s position on China-U.S. economic and trade issues is very clear in the press release. Here I want to emphasize a few more points:

First, the nature of Sino-U.S. economic and trade relations is mutually beneficial and win-win. We have always advocated that, on the basis of mutual respect, equality, and mutual benefit, we should handle economic and trade issues in a constructive manner through dialogue and consultation, and constantly narrow differences and expand cooperation for the benefit of both. People of the country.

Second, China and the United States maintained communication on economic and trade issues, including China-US economic and trade frictions, and also conducted consultations. In fact, they have made some progress. If you remember, after the Sino-U.S. economic and trade consultations earlier this month, China issued a statement. In the statement, we clearly pointed out that if the U.S. side introduces trade sanctions including the increase of tariffs, all the economic and trade achievements negotiated by the two parties will not take effect.

Thirdly, at the beginning of April this year, spokespersons of the Ministry of Commerce and spokesmen of the Ministry of Foreign Affairs had all made formal responses to some U.S. unilateralist words and deeds. The Chinese position is consistent. Here I would like to reiterate that if the U.S. side adopts unilateralism and protectionism and damages China’s interests, we will respond in the first instance and take necessary measures to firmly safeguard our legitimate rights and interests.

USDJPY Analysis: Gains Momentum

The Greenback gained momentum against the Japanese Yen mid-Thursday. This appreciation of the US Dollar was likewise apparent for other major pairs trading against it.

The slight fall apparent on Thursday morning was reversed to the upside when the rate reached the strong support of the 55–period (4H), 200-hour and 200-day SMAs circa 110.00. This resulted in a surge up to its two-week high and even further early today, as the rate passed the weekly R2 and the monthly R1 at 110.75.

Technical indicators remain bullish for this session, especially if the above resistance was breached. The nearest resistance now is the weekly R3 and the upper channel line at 111.22.

By and large, the pair should move towards the senior channel and the monthly R2 at 133.25 within the following trading sessions.

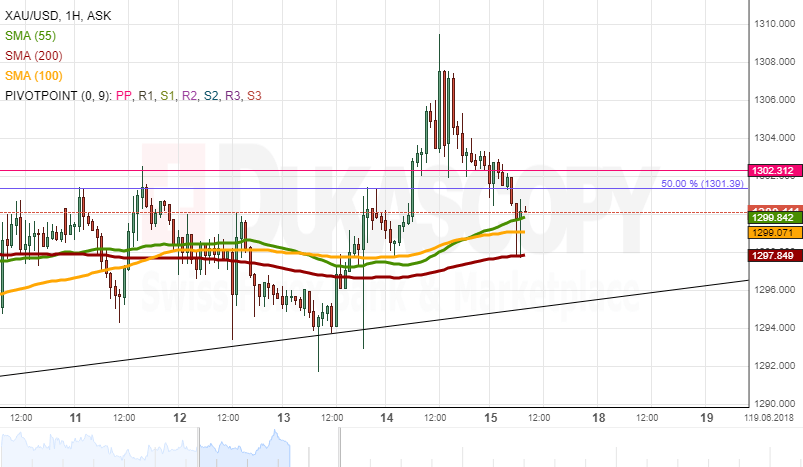

Gold Analysis: Returns Below 1,300.00

Gold finally managed to overcome the strong one-week resistance of the 50.00% Fibonacci retracement and the monthly PP at 1,302.00 on Thursday. A further surge, however, did not follow, as the yellow metal was once again pushed below the psychological 1,300.00 level.

Downside pressure was provided by the 200-day SMA which is located at this reversal point. By Friday morning, the pair had breached several important support levels and was testing the 55– and 100-period (4H) and 200-hour SMAs at 1,297.00.

In case this barrier is breached, Gold should approach the senior channel and the 61.80% Fibo. Conversely, a failure to do so is most likely to cause ranging movement between the 200-day SMA and these smaller-scale lines.

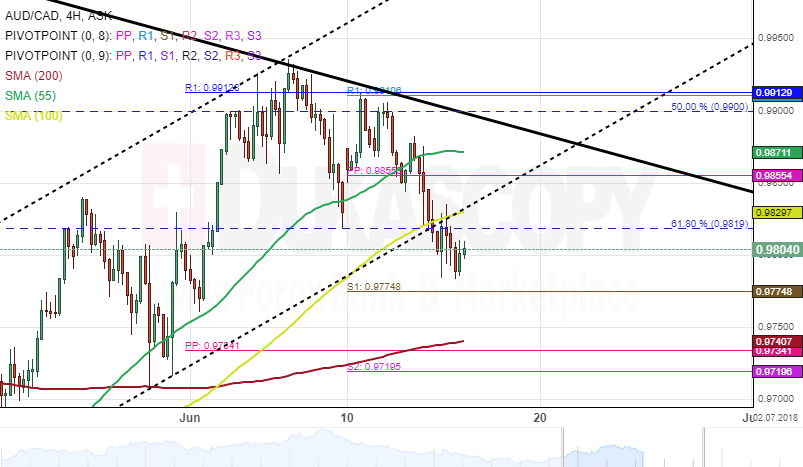

AUD/CAD 4H Chart: Moved Past 61.80% Fibo

Following up on last week Friday analysis for the AUD/CAD exchange rate. Bears took control of the currency pair as expected and as a result, the rate breached the 55-and 100-hour SMAs.

Given that a breakout had occurred through the lower boundary of an ascending channel and price action has moved past the 61.80% Fibonacci retracement level, the pair could target a strong support cluster set by the 200– hour simple moving average and the combination of the weekly and the monthly PPs located near the 0.97 mark.

Technical indicators are in favour of bears to continue their dominance in the market during the following trading sessions.