Sample Category Title

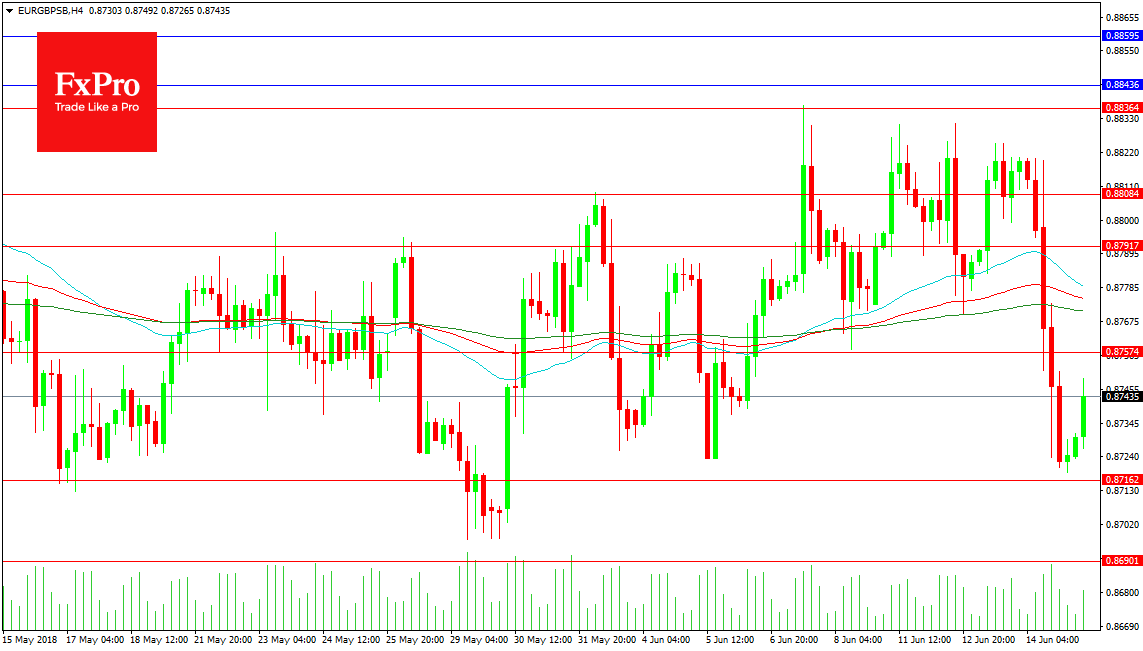

Forex Analysis: EURGBP

EURGBP pair was pushed lower yesterday after the ECB announcement. The pair has traded above 0.88000 and was using its 4 hour moving averages as support but the weakness in the Euro sent the price driving under this indicator at 0.87729 which was retested for good measure before the decent was halted at 0.87187. This market has been in a sideways range for many months so traders are watching for a breakout above 0.90000 with yesterday’s price action denting their hopes. The retracement this morning has gotten to 0.87492 so far with a full retrace of the move down pointing to 0.88500 being targeted.

Support can be seen on the chart at 0.87162 followed by the 0.87000 level. A move under the end of May lows can target 0.86900 followed by 0.86671 and the important swing low at 0.86200. From there buyers would look to enter the market as far down as 0.85700 but a loss of 0.85500 may result in a shakeout of positions and a drive to 0.84000 and beyond.

Dollar Is King, But Trade Tensions Cap Risk Appetite

Friday June 15: Five things the markets are talking about

This was always going to be a big week for capital markets and it has not disappointed.

Bond prices continue to rally and global equities trade under pressure as Sino-U.S trade tensions threaten to escalate, while capital markets weigh diverging monetary policies from the European Central Bank (ECB) and the Fed.

The ECB surprised investors Thursday, as its guidance that interest rates will remain at “low levels” for at least another year was more explicit than expected, and stands in stark contrast to the Fed’s determination to push rates higher.

Nevertheless, the most ‘dovish’ of central banks is the Bank of Japan (BoJ), who overnight stuck to its “ultra-easy” monetary policy, bucking the global tightening trend largely because inflation is not getting close to its +2% target.

On the trade front, dealers are bracing for the expected approval of U.S import tariffs on +$50B of Chinese goods – a move that China has said it will respond to in kind. A trade tiff will only be putting additional pressure on China’s economy, which is starting to show signs of cooling.

1. Stocks mixed on trade tension

The U.S dollar hitting a three-week high versus the yen (¥110.88) helped provide support to Japanese stocks overnight. The Nikkei closed Friday +0.5% higher, to finish the week with a gain of +0.7%. The broader Topix rallied +0.3%.

Note: The market had little reaction to the outcome of the BoJ meeting, which kept its short-term interest rate target at -0.1%, as expected, and a pledge to guide 10-year JGB’s yields around zero percent.

Down-under, bank stocks led Aussie shares to a higher finish overnight, supported by G7 rate differentials and the U.S dollar’s resulting strength. The S&P/ASX 200 index gained +1.3% on the day and +0.8% for the week. In S. Korea, stock indexes lagged again with the Kospi setting session lows into the close and finished down -0.8%.

In Hong Kong, stocks posted their biggest weekly drop in three-months as Washington looks set to unveil a tariff list targeting +$50B of Chinese goods, and with Beijing vowing to retaliate, has put investors on edge. The Hang Seng index fell -0.4%, while the China Enterprises Index lost -0.7%. For the week, Hang Seng fell -2.1%, while HSCE dropped -2.4%.

In China, stocks plummeted to a 20-month low overnight on trade tension. The blue-chip CSI300 index fell -0.5%, while the Shanghai Composite Index ended down -0.7% – both indexes were down for the third session in a row.

In Europe, regional bourses opened mixed and have since slipped to the downside waiting on Trump’s China tariff confirmation.

U.S stocks are set to open in the ‘red’ (-0.4%).

Indices: Stoxx50 -0.1% at 3,530, FTSE -0.5% at 7,723, DAX flat at 13,113, CAC-40 +0.2% at 5,540; IBEX-35 -0.4% at 9,916, FTSE MIB -0.3% at 22,412, SMI +0.2% at 8,671, S&P 500 Futures -0.4%

2. Oil mixed as dollar gains, gold prices lower

Oil prices are a tad lower heading into the U.S session, as a stronger dollar weighed and a key supply-setting meeting of OPEC looms (June 22).

Brent crude fell -0.3% to +$75.73 a barrel, the lowest in more than a week, while West Texas Intermediate (WTI) crude dipped -0.2% to +$66.78 a barrel, the first retreat in a week.

Both Brent and WTI hit three-year highs last month, but have since drifted lower, indicating investors expect the market to soon become better supplied as U.S crude production rises and as OPEC and its allies look poised to increase output.

Note: With global crude inventories falling, Venezuelan production plummeting and imminent sanctions against Iran, OPEC may soon end their supply cuts as early as next weeks meeting in Vienna (June 22).

Don’t be surprised to see oil prices being pushed about on rhetoric mostly over the next week.

Ahead of the U.S open, gold prices have slipped from a one-month high hit yesterday (+$1,309.30 an ounce) as investors booked profits and the dollar strengthened, while worries over U.S/China trade dispute is capping losses for the moment. Spot gold fell -0.3% to +$1,298.25 per ounce, while U.S gold futures for August delivery is down -0.5% at +$1,301.50 per ounce.

3. Yields under pressure

Eurozone government bond yields trade slightly lower; extending yesterday’s rally induced by the ECB’s announcement that rate increases will not come any time soon.

Germany’s 10-year Bund yield is trading -1 bps lower at +0.42%, while Italy’s 10-year BTP yield, which led yield falls in the eurozone yesterday, trades -3 bps lower at +2.73%.

Note: There is no sovereign supply today, but Spain and France are set to announce details of their respective auctions next week.

Elsewhere, the yield on 10-year Treasuries has dipped -2 bps to +2.91%, the lowest in two-weeks, while in the U.K, the 10-year Gilt yield has dipped -4 bps to +1.334%, the lowest in more than a week.

4. Dollar is King, but trade tensions cap risk appetite

Rate divergence has dominated currency price action over the past 48-hours. A ‘hawkish’ Fed and a ‘dovish’ ECB has provided the dollar bull the fortitude to push the ‘big’ dollar prices to multi-week and month highs across the board. However, traded tensions on multiple fronts are beginning to provide a cap for risk appetite.

The EUR/USD (€1.1600) is rallying into the U.S open after being beaten up from a ‘dovish’ ECB stance yesterday.

Note: ECB policy makers expect the key interest rates to remain at their present levels at least through the summer of 2019 and that QE would still be “subject to incoming data.”

JPY (¥110.53) is reversing some its overnight losses on safe-haven flows that’s being supported by trade tension fears. USD/JPY was approaching the psychological ¥111 handle on rate differentials.

5. E.U wages rise and trade surplus narrows

Eurozone data this morning showed wages rose at a faster pace during the three-months through March. Eurostat said pay per hour worked was +1.8% higher than a year earlier, a faster increase than the +1.6% recorded in Q4 of 2017.

Note: Data like this provides further proof that the ECB remains on track to keep inflation at the target.

However, other data also released by Eurostat indicated there has been no strong rebound from a Q1 slowdown in economic growth, as Eurozone’s surplus in its trade in goods with the rest of the world narrowed in April (€18.1B vs. €19.8B).

European Stock Markets Soar As ECB Dampens Hopes Of Rate Hike

The DAX index has steadied on Friday, after posting sharp gains on Thursday. Currently, the DAX is at 13,104, down 0.04% on the day. On the release front, German WPI posted a strong gain of 0.8%, well above the estimate of 0.3%. In the eurozone, Final CPI rose to 1.9% and Final Flash CPI climbed to 1.1.%, as both readings matched their estimates. As well, the eurozone trade surplus narrowed to EUR 18.1 billion, shy of the estimate of EUR 21.2 billion.

It has been a week of contrasts from the Federal Reserve and the ECB. The Fed raised rates by a quarter-point, and the rate statement was hawkish, reflecting a booming US economy, with a tight labor market and strong spending by consumers and businesses. Just a day later, the ECB announced that it was winding up its stimulus program this year. However, the ECB added that that interest rates would remain steady “at least through the summer of 2019”, giving policymakers plenty of wiggle-room to delay any rate hikes. This sent German and French markets sharply higher on Thursday – the DAX jumped 1.9% and the CAC climbed 2.3%, while the euro dropped sharply. The ECB pledged to taper its bond-purchase program to EUR 15 billion/mth, in October, down from the current pace of EUR 30 billion/mth. The program will wind up at the end of the year. Draghi sounded dovish in his press conference, saying that the eurozone economy was facing “increasing uncertainty”. Draghi was likely referring to the G-7 meeting which ended in disarray as well as the election of a euro-sceptic government in Italy. The ECB also lowered its growth forecast for the eurozone to 2.1%, down from 2.4% earlier this year.

As widely expected, the Federal Reserve raised interest rates by a quarter-point, to a range between 1.75 percent and 2.00 percent. Fed Chair Jerome Powell sounded hawkish in his press conference, saying that the economy was performing well and that “overall outlook for growth remains favorable”. This message echoed the rate statement, in which policymakers said that “economic activity has been rising at a solid rate”, pointing to stronger consumer spending and business investment. What was may have been the most notable development was that the Fed rate projections were revised upwards, predicting two additional rate hikes in 2018, for a total of four hikes. Until now, the Fed had projected three rate hikes this year. This represents a nod to the strength of the U.S economy and could boost the dollar against its rivals.

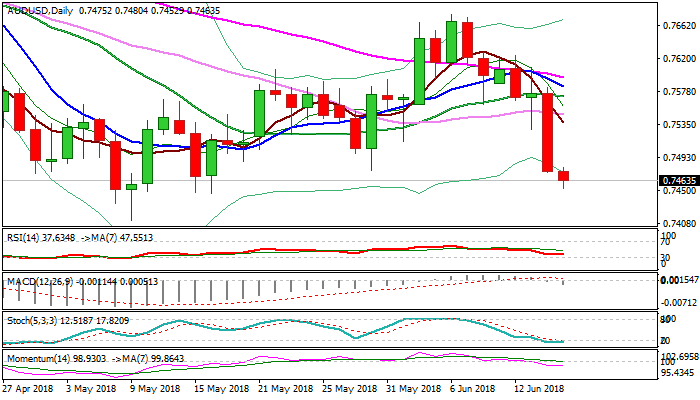

AUDUSD Outlook: Bears Eye Key Support At 0.7412, In Extension Of Thursday’s 1.3% Fall

The Aussie dollar holds in red on Friday following previous day's strong fall when the Australian currency was down 1.3% against its US counterpart.

Weak Australian jobs data and China's data did not make stronger impact on Aussie, but it couldn't survive ECB shock.

Thursday's fall marked the biggest one-day loss since 02 Feb, with scope seen for further weakness.

Loss of psychological 0.75 handle opened way for test of key support at 0.7412 (2018 low, posted on 09 May), loss of which would signal continuation of downtrend from 2018 high at 0.8135 and expose next significant support at 0.7325 (Fibo 61.8% of 0.6825/0.8135 2016/2018 rally).

Daily techs turned into full bearish setup after Thursday's rally and support further weakness, but hesitation on approach to key 0.7412 support could be anticipated. Upticks on profit-taking and oversold studies would be positioning for fresh attempts lower and should be capped below daily cloud base (0.7551).

The pair is also on track for strong bearish weekly close which adds on negative outlook, with weekly close below 0.7412 pivot to generate strong bearish signal.

Res: 0.7480, 0.7513, 0.7551, 0.7571

Sup: 0.7450, 0.7412, 0.7349, 0.7325

Markets Under Pressure Ahead Of Tariff Announcement

- More Trump Tariffs Causing a Wobble in Markets;

- Trump Has Leeway to Put Economy Second After Recent Successes;

- EURUSD Under Pressure After This Week's Central Bank Meetings.

It's been a relatively mixed start to trading in Europe on Friday and the US is on course to post small losses at the open, as the focus shifts from central banks back to trade.

US President Donald Trump is expected to announce tariffs on $50 billion of Chinese imports today that will once again stoke fears of a trade war and protectionist policies and likely trigger a response from the world's second largest economy. Trump has been picking fights with a number of countries on trade in an attempt to address the large deficit the US runs and China is clearly his primary target.

Markets will always be vulnerable to trade spats between countries and while the response to the G7 meeting may have been quite muted, that more likely a sign of such an outcome being in line with expectations than markets becoming less sensitive to it.

The biggest concern here is naturally that this will continue to escalate and more and more counter-tariffs will be imposed, something that will harm all economies and weigh on investor sentiment. Perhaps Trump feels that the strength of the US economy and recent success in Singapore gives him the breathing room to make a sacrifice on the economy and jobs in an attempt put additional pressure on other countries.

There are a number of economic data releases to look out for today, although they may be a little overshadowed by the US tariff announcement. The UoM consumer sentiment survey, empire state manufacturing index, capacity utilization rate and industrial production figures are all notable releases for the US and will be released around the open on Wall Street so should be of interest.

The week's central bank events may be behind us but they're continuing to have an influence on the markets today. The euro is paring some gains early in the day after coming under substantial pressure as the ECB laid out plans for the end of quantitative easing and the first interest rate hike.

As ever, a hawkish shift in policy was accompanied by some very dovish language from President Draghi which sent the single currency tumbling. Combine this with a more hawkish result from the Federal Reserve meeting on Wednesday and it's no surprise the EURUSD pair is under pressure again despite a brief recovery over the last couple of weeks. The pair found some support around 1.15 last time but may not be so lucky this time around, while 1.13 could be an interesting level.

Talk Of A 2nd Tariff List From US Against China Being Composed

Notes/Observations

- Talk of a 2nd US tariff list of $100B against China dampens risk outlook

Asia:

- BOJ left policy steady (as expected). Kept Interest Rate on Excess Reserves (IOER) Unchanged at -0.10%. Downgraded assessment of CPI (as speculated) and now saw CPI in range of 0.5% to 1.0%

Europe:

- ECB policymakers reportedly at odds over policy statement wording on end of QE and rate hike; some wanted to signal possible rate hike in mid 2019 and others want to keep option open for extension of bond buys

- Bank of France raised its 2018 inflation outlook from 1.6% to 2.0% and cut its 2018 GDP growth outlook from 1.9% to 1.8%

- Leading pro-EU Tory lawmaker Grieve stated that the govt compromise on Brexit meaningful vote was 'unacceptable' (Note: Sets the scene for another showdown when the bill returns to parliament during the week of Jun 18th)

- ESM Board approved disbursement of remaining €1.0B for Greece with payment was linked to arrears clearance

- UK PM is expected to announce on Monday, Jun 18th a 3% annual boost to NHS funding as part of multiyear settlement to mark its 70th birthday

Americas:

- Trump administration official stated that President Trump would direct 'pretty significant action' on tariffs against China; expected to affect $50B in Chinese products (Note: Treasury Sec Mnuchin argued in meeting against imposing tariffs)

Economic Data:

- (SE) Sweden May Maklarstatistik Housing Prices Y/Y: 1.0% v 0.0% prior

- (NL) Netherlands Apr Retail Sales Y/Y: No est v 3.6% prior

- (PE) Peru Apr Economic Activity Index (monthly GDP) Y/Y: 6.2%e v 3.9% prior

- (PE) Peru May Unemployment Rate: 7.1%e v 7.3% prior

- (EU) EU27 New Car Registrations: 0.8% v 9.6% prior

- (DK) Denmark May PPI M/M: 1.2% v 1.5% prior; Y/Y: 3.9% v 2.8% prior

- (NO) Norway May Trade Balance (NOK): 16.3B v 18.7B prior

- (FI) Finland Apr Current Account: -€0.1B v -€0.1B prior

- (FI) Finland Apr GDP Indicator WDA Y/Y: 1.8% v 4.0% prior

- (AT) Austria May CPI M/M: 0.2% v 0.2% prior; Y/Y: 1.9% v 1.8% prior

- (ES) Spain Q1 Labour Costs Y/Y: 0.7% v 0.7% prior

- (CN) Weekly Shanghai copper inventories (SHFE): 253.0K v 256.2K tons prior

- (RU) Russia Narrow Money Supply w/e Jun 8th: 10.06T v 9.92T prior

- (IT) Italy Apr Industrial Sales M/M: 0.3% v 0.6% prior; Y/Y: 4.0% v 3.3% prior

- (IT) Italy Apr Industrial Orders M/M: -1.3% v +0.3% prior; Y/Y: 6.4 v 2.3% prior

- (IN) India May Trade Balance: -$14.6B v -$14.3Be

- (IT) Italy Apr General Government Debt: €2.312T (record high) v €2.302T prior

- (EU) Euro Zone Apr Trade Balance (Seasonally Adj): €18.1B v €20.0Be; Trade Balance NSA (unadj): €16.7B v €26.9B prior

- (EU) Euro Zone May Final CPI Y/Y: 1.9% v 1.9%e; CPI Core Y/Y: 1.1% v 1.1%e, CPI M/M: 0.5% v 0.5%e

- (EU) Euro Zone Q1 Labour Costs Y/Y: 2.0% v 1.4% prior

- (IT) Italy May Final CPI (includes tobacco) M/M: 0.3% v 0.4% prelim; Y/Y: 1.0% v 1.1% prelim; CPI Index (ex-tobacco): 102.0 v 101.9e

- (IT) Italy May Final CPI EU Harmonized M/M: 0.3% v 0.4% prelim; Y/Y: 1.0% v 1.1%e

Fixed Income Issuance:

- None seen

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx50 -0.1% at 3,530, FTSE -0.5% at 7,723, DAX flat at 13,113, CAC-40 +0.2% at 5,540; IBEX-35 -0.4% at 9,916, FTSE MIB -0.3% at 22,412, SMI +0.2% at 8,671 , S&P 500 Futures -0.4%]

- Market Focal Points/Key Themes: European markets opened mixed and slipped to the downside as the session progressed, following press reports of second China tariff list being considered by White House; personal consumption and autos best performers; financials and energy stocks underperforming; many indices across Asia closed for holiday; upcoming earnings releases expected in the US session include Canadian Goose and PermRock

Equities

- Consumer discretionary: Hennes & Mauritz HMB.SE -4.0% (results), Tesco TSCO.UK +2.2% (results)

- Healthcare: Roche ROG.CH +0.5% (study results), Indivior INDV.UK -16.1% (FDA approval of generic Suboxone)

- Industrials: PostNL PNL.NL +7.6% (government to scale down participation in market), Rolls Royce RR.UK +11.2% (outlook)

- Materials: Umicore UMI.BE +1.5% (analyst action)

Speakers

- ECB's Nowotny (Austria): Inflation was in-line with ECB target. ECB inflation goal of close to 2% is achieved but added that full policy normalization would take significant time. Policy to remain significantly expansive. The central bank was beginning the normalization process but without setting off taper tantrum in the markets

- ECB's Coeure (France): Growth in Europe was strong and that inflation was expected to durably converge closer to target. Italy's economic challenge was not linked to the Euro currency

- German Bundesbank updated its outlook: Domestic economic boom was continuing. Cut its 2018 GDP growth forecast from 2.5% to 2.0% while raising the 2019 GDP growth forecast from 1.7% to 1.9%. Raised the 2018 inflation forecast from 1.6% to 1.8% and maintained 2019 inflation forecast at 1.7%

- BOJ Gov Kuroda post rate decision press conference reiterated view that the domestic economy was expanding moderately while still some distance from the 2% inflation target. Too early to talk about specifics of any policy exit at this time; needed to make best effort to achieve the price target Affirmed its new CPI forecast that inflation was seen rising between 0.5-1% y/y (**Note: prior view was around 1%). Reiterated to adjust policy as needed, taking into account economy, prices, financial conditions to maintain momentum towards 2% price target.

- US said to be nearing completion of a 2nd tariff list comprising of $100B in Chinese goods, subject to same hearing conditions of approx 60 days

- China Foreign Ministry reiterated view that will take appropriate measures if US enacts tariffs. All trade agreements would be called off

Currencies

- Central bank divergence theme evolved in price action over the past two sessions with the combination of a hawkish Fed on Wednesday and a dovish ECB on Thursday. However, talk of a 2nd list of tariffs against China circulated in the session and provided a headwind on risk appetite. The USD pared back earlier gains.

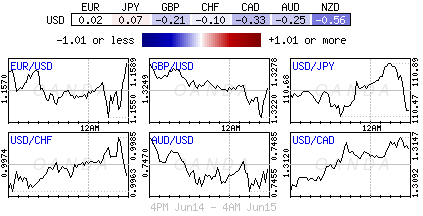

- The EUR/USD opened the EU session lower as dealers continued to assess the ECB statement. The inclusion of calendar based guidance on rates is the first time the ECB had done such a thing and viewed as a material evolution to the policy framework. ECB expected the key ECB interest rates to remain at their present levels at least through the summer of 2019. Also dovish the conditional taper with analysts noting a caveat was QE would still be "subject to incoming data confirming the Governing Council's medium-term inflation outlook. Global trade jitters help the Euro try to regain the 1.16 handle just ahead of the US morning.

- The JPY reversed its earlier losses on some safe-haven flows on trade jitters with USD/JPY hovering in the mid-110.50 area. The pair was approaching the 111 area before trade concerns prompted some safe-haven buying of the yen currency.

Fixed Income

- Bund Futures trade at 161.24, up 53 ticks ahead as markets digest the ECB actions yesterday. Further upside targets 161.66, while a pullback would target 160.36 then 159.94.

- Gilt futures trade at 122.67 up 22 ticks tracking Bunds and Treasuries higher with resistance seen 122.95 then 123.17. A move back lower sees 121.33.

- Friday's liquidity report showed Thursday's excess liquidity fell from €1.903T to €1.887T. Use of the marginal lending facility fell from €99M to €65M.

- Corporate issuance saw a pick up in acitivity with 9 issuers raising $11.9B. For the week ending June 13th High Yield funds saw inflows of $324M compared to $2.42B outflows last week.

Looking Ahead

- 05:30 (PL) Poland to sell Bonds (switch auction)

- 06:00 (IE) Ireland Apr Trade Balance: No est v €4.0B prior

- 06:00 (UK) DMO to sell combined £4.0B in 1-month, 6-month and 12-month Bills (£1.0B, £1.0B and £2.0B respectively)

- 06:30 (RU) Russia Central Bank (CBR) Interest Rate Decision: Analysts split between keeping Key 1-Week Auction Rate unchanged at 7.25% or cut by 25bps to 7.00%

- 06:45 (US) Daily Libor Fixing - 07:00 (IL) Israel May CPI M/M: 0.5%e v 0.4% prior; Y/Y: 0.5%e v 0.4% prior

- 07:00 (BR) Brazil Jun FGV Inflation IGP-10 M/M: 1.7%e v 1.1% prior

- 07:30 (BR) Brazil Apr Economic Activity Index (monthly GDP) M/M: +0.6%e v -0.7% prior; Y/Y: +3.9%e v -0.7% prior

- 07:30 (IN) India Weekly Forex Reserves

- 08:00 (PL) Poland May CPI Core M/M: 0.0%e v 0.5% prior; Y/Y: 0.6%e v 0.6% prior

- 08:00 (RU) Russia Central Bank (CBR) Govr Nabiullina post rate decision press conference

- 08:00 (IN) India announces upcoming bill issuance (held on Wed)

- 08:00 (ES) Spain Debt Agency (Tesoro) announces upcoming issuance

- 08:15 (UK) Baltic Dry Bulk Index

- 08:30 (US) Jun Empire Manufacturing: 18.8e v 20.1 prior

- 08:30 (CA) Canada Apr Int'l Securities Transactions (CAD): No est v 6.2B prior

- 08:30 (CA) Canada Apr Manufacturing Sales M/M: 0.6%e v 1.4% prior

- 09:00 (BE) Belgium Apr Trade Balance: No est v €0.3B prior

- 09:00 (CA) Canada May Existing Home Sales M/M:

- 1.4%e v -2.9% prior

- 09:15 (US) May Industrial Production M/M: 0.2%e v 0.7% prior; Capacity Utilization: 78.1%e v 78.0% prior, Manufacturing Production: 0.0%e v 0.5% prior

- 10:00 (US) Jun Preliminary University of Michigan Confidence: 98.5e v 98.0 prior

- 11:00 (CO) Colombia Apr Industrial Production Y/Y: 5.6%e v -1.4% prior

- 11:00 (CO) Colombia Apr Retail Sales Y/Y: 6.7%e v 5.5% prior

- 11:00 (EU) Potential sovereign ratings after the European close (United Kingdom Sovereign Debt to be rated by Moody's; Ireland Sovereign Debt to be rated by Fitch)

- 13:00 (US) Weekly Baker Hughes Rig Count data

- 16:00 (US) Apr Total Net TIC Flows: No est v -$38.5B prior; Net Long-term TIC Flows: No est v $61.8B prior

Strategy: The US Is Leaving The Euro Area Behind

Today's key points

- Global growth has slowed but is set to stay above the potential growth rate.

- Volatility has increased but fundamentals support equities in 3-12M.

- Gradual monetary policy tightening amid muted inflation pressures.

- EUR/USD lower for longer but not forever.

From boom to cruising speed

Yesterday, we published our biannual The Big Picture, containing our updated macro forecasts for the global economy (see The Big Picture – From boom to cruising speed, 7 June). Following a strong end to 2017, we see clear signs that the business cycle is losing momentum. While global growth might be decelerating, we do not expect it to turn into a marked downturn over the next few years – rather, we believe growth in the world economy should go from boom to cruising speed in line with its potential. We expect global growth to come in at 3.8% this year, declining to 3.7% in 2019 and 3.6% in 2020.

The risks to our forecasts are skewed on the downside, from an escalation of trade tension into a full-blown trade war and a renewed Italian debt crisis. Unfortunately, the positive developments in the US-China trade conflict did not last long and the risk of renewed escalation over coming weeks has increased, as US President Trump has announced he will impose tariffs on USD50bn imports from China despite China having agreed to buy more US goods to bring down the trade balance (see US-China Trade Talks – Why things are getting tricky, 4 June. In Italy, markets are still waiting for indications of whether or not the new Five Star-League government will back down on some of its promises.

Higher volatility but fundamentals support equities

Last year was quite extraordinary, as growth rose across regions and risks diminished. Increasing economic growth, very high optimism among businesses and consumers and record-low volatility (as measured by the VIX index) were a good cocktail for equities, which rose steadily over the year. This year, with slower economic growth and more risks stemming from the political situation in Italy and the US-China trade conflict, it is not a big surprise that volatility has increased. However, as economic growth remains above potential and earnings growth is solid, we still expect equities to move higher but the ride is going to be bumpier than in 2017. Then again, it was 2017 that was extraordinary and we have just returned to a more ‘normal' situation.

Gradual monetary policy tightening amid muted inflation pressure

Despite the expansion, especially in the US, having lasted for some time and the labour markets having tightened substantially, inflation and wage growth pressures remain modest. We believe some of the explanation is in the relatively muted inflation expectations and globalisation pressures. We believe the biggest upside risk to inflation is in the US, given its sizeable fiscal expansion and limited slack in the economy, and we think US PCE core inflation is set to move slightly above 2%, although it is likely to be a gradual process given that inflation is quite persistent in nature. The Federal Reserve is unlikely to panic by hiking aggressively on the back of this, as it has said it can accept core inflation moving slightly above 2% temporarily, as core inflation has run under the 2% target for a long time. While we think the Fed will raise the target range by 25bp to 1.75-2.00% next week, we do not think it will make big changes to its current policy strategy and still believe it is on track to deliver a total of three to four hikes this year

The expansion is a bit younger in Europe and the ECB is still fighting a tough battle against too low inflation relative to its 2% target. The ECB is still on track to end its QE programme this year but we think it is too early for Mario Draghi and the ECB to change their forward guidance at next week's meeting, although the probability has increased since Chief Economist Peter Praet's hawkish comments a couple of days ago. We expect the ECB to wait until July. In any case, the first ECB rate hike is still unlikely before the end of 2019, so in Europe we still expect to have a negative key policy rate over the next few years.

EUR/USD lower for longer but not forever

EUR/USD has been on a rollercoaster ride this year. It went above 1.25 in early February and reached its low at the end of May, slightly above 1.15. It has rebounded slightly since then and is currently trading a bit above 1.18. We have revised our EUR/USD forecast profile, as a hesitant ECB and USD carry is set to keep the cross lower for longer and EUR/USD does not seem to be heading back to the mid-.20s near term. We now see the cross at 1.17 in 1M, 1.17 in 3M (previously 1.19) and 1.20 (1.23) in 6M. We still believe the next big move remains higher though and think it will move to 1.25 in 12M (1.28). On a 6-12M horizon, we expect the ECB to end QE and believe forward guidance on rates will take centre stage. Although the first hike is distant, this should allow EUR/USD gravity to kick in, as the eurozone capital tide turns

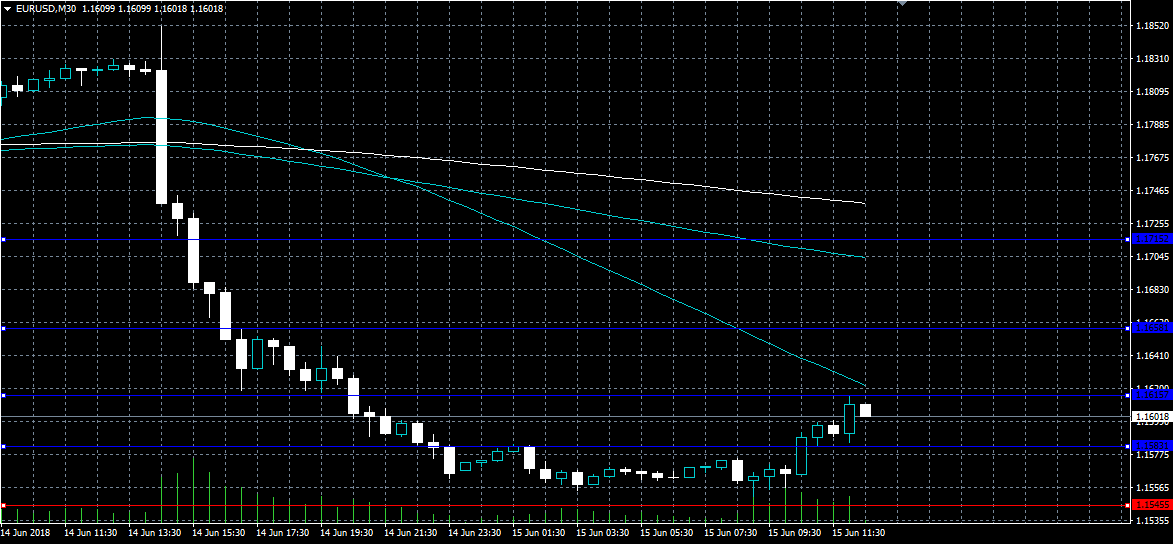

EURO Only Intraday Bullish Above 1.1615 Level

The euro has corrected higher against the US dollar during the European trading session, as the US dollar index moves lower after briefly moving above the key 95.00 level. The EUR/USD pair has so far found resistance from the 1.1615 level, after earlier finding strong support from the 1.1545 level. Further technical selling in the EURUSD remains likely as the pair is still bearish while trading below the 1.1615 level.

If the EURUSD pair moves above the 1.1615 level, buyers may test towards the 1.1658 and 1.1715 resistance levels.

If the EURUSD pair continues to trade below the 1.1615 level, further losses towards the 1.1583 and 1.1545 levels seem likely.

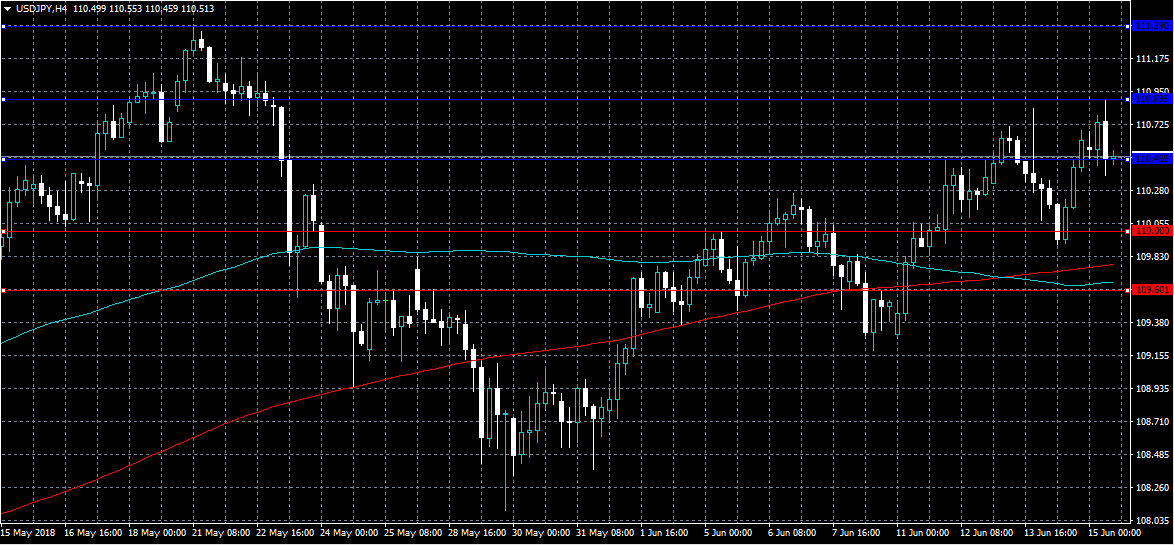

USDJPY Bullish Above 110.48 Level

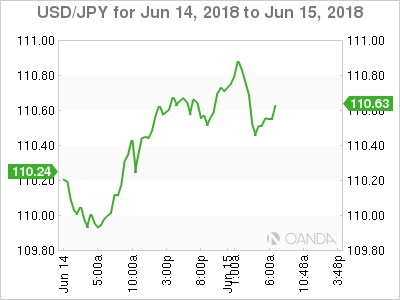

The US dollar is currently testing key technical support against the Japanese yen, as the pair starts to drift lower after earlier hitting a fresh monthly trading-high, of 110.89. The Bank of Japan Monetary Policy Decision was largely a non-event for the USDJPY pair, with the US dollar remaining the key driver of the pair. Price is currently testing the 110.48 level, with the USDJPY pair still retaining its intraday bullish bias while trading above this key level.

The USDJPY pair is intraday bullish while trading above the 110.48 level, key technical resistance is now found at the 110.89 and 111.39 levels.

If the USDJPY pair moves below the 110.48 level, key intraday support is found at the 110.26 and 110.00 levels.

Forex Analysis: German 30

The German 30 Index was propelled higher yesterday as the Euro weakened in response to the ECB decision to taper its QE purchases. The index broke above resistance at 12950.00 and 13000.00 before falling short of the 13200.00 level. It has come off the highs this morning and found support at 13100.00. It remains to be seen if this rally can be sustained as US equity markets were mixed yesterday and remain depressed this morning. Traders will be watching for a break of the 13200.00 area which points to a moved back to the highs at 13600.00.

Support below 13100.00 comes in at 13060.00 followed by 13000.00. A drop under this level would signal a reversal of the move yesterday and a swing towards a more bearish outlook. Supports under 12900.00 take the form of the moving averages with the 200 period MA at 12814.40. The 12750.00 level represents the median of the recent range extending down to 12607.00 and 12544.00. A move down out of this range can point to further declines as the summer progresses.