Sample Category Title

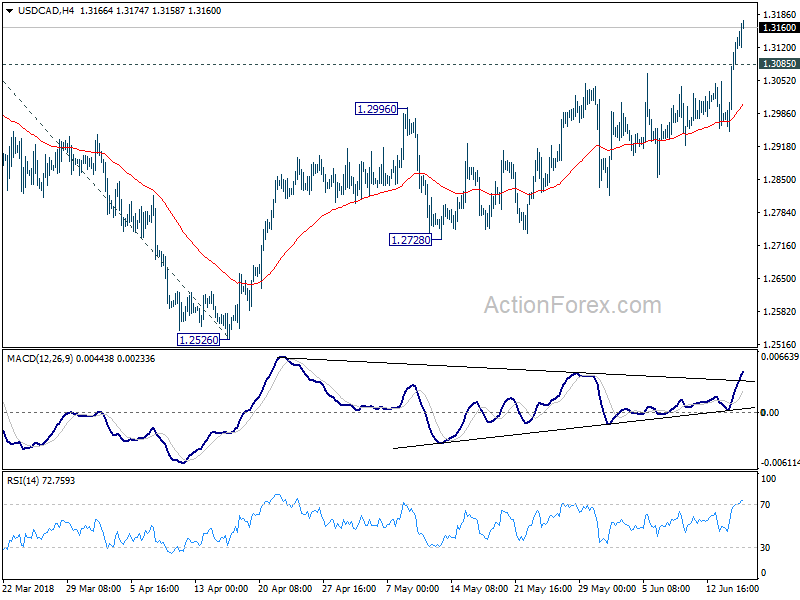

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2997; (P) 1.3054; (R1) 1.3163; More...

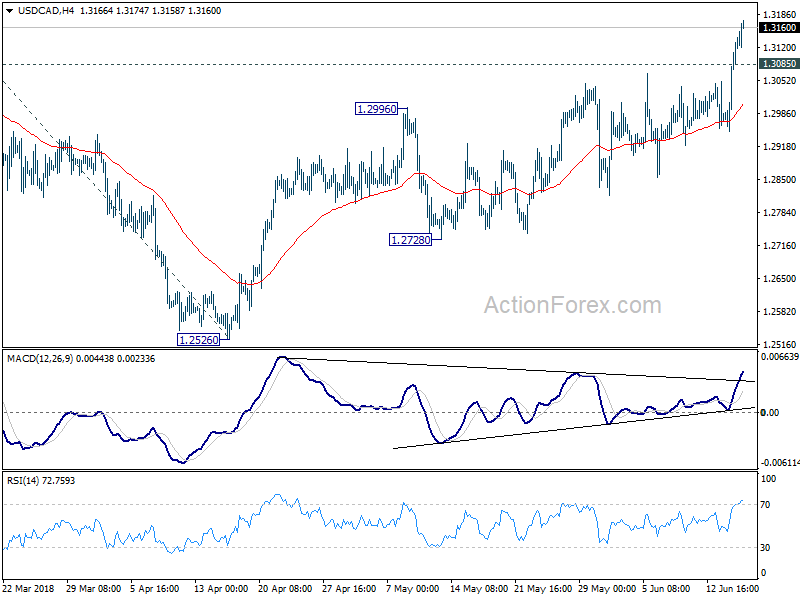

USD/CAD's rally continues today and reaches as high as 1.3174 so far. Intraday bias remains on the upside. Further rally should be seen to 100% projection of 1.2246 to 1.3124 from 1.2526 at 1.3404 next. On the downside, below 1.3085 minor support will turn intraday bias neutral and bring consolidation first, before staying another rally.

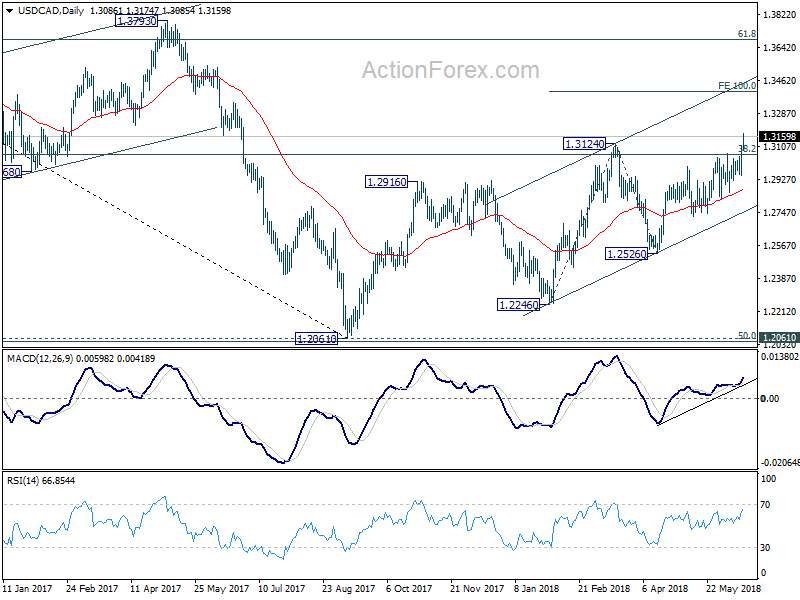

In the bigger picture, the current development affirms our bullish view. That is, firstly, rebound from 1.2061 is not finished yet. Secondly, the medium term decline from 1.4689 (2016 high) has completed and the trend is reversing. Sustained trading above 38.2% retracement of 1.4689 to 1.2061 at 1.3065 will confirm our view and target 61.8% retracement at 1.3685 and above. 1.3685. However, break of 1.2526 support will dampen this bullish view again. And, focus will be back on 1.2061 key support level, which is close to 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048.

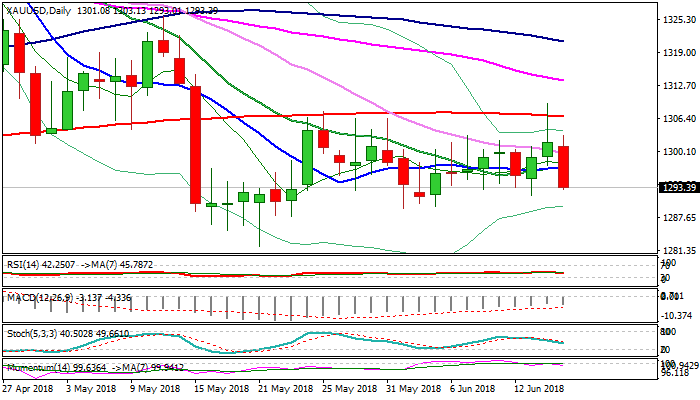

Spot Gold Outlook: Falls on Tariffs Announcement; Break Below $1292 Pivot to Spark Further Weakness

Spot Gold price fell after US tariff announcement, extending weakness from Thursday's high at $1309 where rally was rejected. The dollar benefited from dovish ECB on Thursday, sending the yellow metal price down, with additional pressure coming from new US tariffs on goods imported from China. Gold price reversed from $1309 high on Thursday, leaving daily candle with long upper shadow after false break above 200SMA, which was initial negative signal. Fresh extension lower on Friday pressures pivotal support at $1292 (Fibo 61.8% of $1282/$1309 ascend, break of which would generate strong bearish signal. Bearish daily techs maintain negative tone for extension towards $1289 higher base. Broken converged 10/20SMA's mark solid barrier at $1296, with extended upticks expected to hold below psychological $1300 barrier, reinforced by 30SMA.

Res: 1296; 1300; 1303; 1306

Sup: 1292; 1289; 1285; 1282

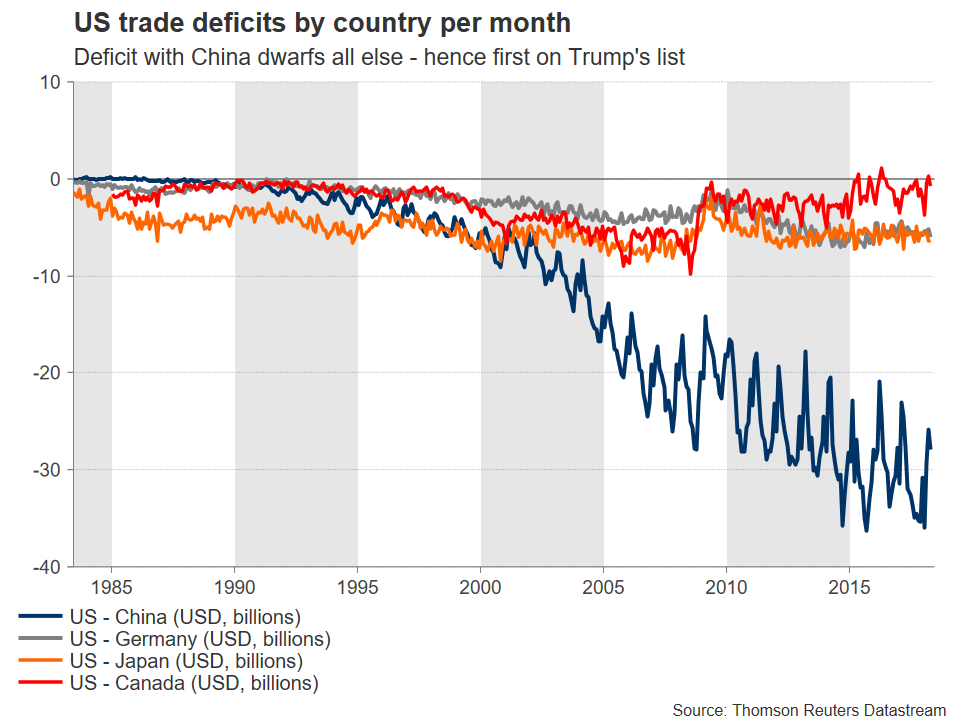

Stocks to Suffer, But Forex Steady as Trump Ignores Americans and Fires Another Shot in Trade War

US stocks futures are rocked by the announcement on formalizing the Section 301 tariffs against China. DOW futures point to triple digit loss at open and could threaten 25000 handle. The forex markets are relatively calm though. Euro is paring back some of yesterday's post ECB losses and takes Sterling higher. Yen is regaining some ground, likely on risk aversion. But the greenback remains firm against commodity currencies. In particular, Canadian Dollar is suffering fresh selling as Canada will likely be the biggest sufferer on all front due to US protectionism.

US announced Tariffs on USD 34B of Chinese imports, starting July 6. Added USD 16B products for public hearing

The US Trade Representative formally announced the section 301 tariffs on Chinese imports, targeting products related to the Made in China 2025 policy. USTR said these "strong defensive actions" are to " protect America's leadership in technology and innovation against the unprecedented threat posed by China's theft of our intellectual property, the forced transfer of American technology, and its cyber attacks on our computer networks." And it condemned that "China's government is aggressively working to undermine America's high-tech industries and our economic leadership through unfair trade practices and industrial policies like 'Made in China 2025.'"

There are two set of tariffs lines. The first set contains 818 lines of the original 1,333 lines announced in April. This set covers around USD 34B of Chinese imports. 25% tariffs will be imposed starting July 6, 2018. The second set contained 284 proposed tariff lines, covering around USD 16B in Chinese goods. This set will undergo further public view before finalizing.

Altogether they're valued around USD 50B. and focuses on products from industrial sectors that contribute to or benefit from the "Made in China 2025" industrial policy, which include industries such as aerospace, information and communications technology, robotics, industrial machinery, new materials, and automobiles. The list does not include goods commonly purchased by American consumers such as cellular telephones or televisions.

Trump said in a separate statement that "the United States can no longer tolerate losing our technology and intellectual property through unfair economic practices." And, "these tariffs are essential to preventing further unfair transfers of American technology and intellectual property to China, which will protect American jobs." "In addition, they will serve as an initial step toward bringing balance to the trade relationship between the United States and China."

The formal response from China is awaited.

But Trump's action is drawing strong criticisms from Americans, which he refused to listen to. "Imposing tariffs places the cost of China's unfair trade practices squarely on the shoulders of American consumers, manufacturers, farmers, and ranchers. This is not the right approach," Thomas Donohue, president of the U.S. Chamber of Commerce, said in an swift email statement.

US agriculture associations cry #TradeNotTariffs

Agriculture Associations in the US turned to the Congress for help after their voices have fallen on Trump's deaf ears. The American Soybean Association (ASA), the National Corn Growers Association, National Association of Wheat Growers (NAWG), Association of Equipment Manufacturers (AEM) issued a joint appeal to the Congress with hashtag #TradeNotTariffs.

The urged the Congress to "convince the administration to halt tariffs and go back to the negotiating table." And, Under the hashtag #TradeNotTariffs, members of these organizations are also raising awareness on social media by sharing with the public what tariffs could mean for their livelihoods – and how severe that outlook could be.

This is an immediate response to the news that White House would announce the final list of tariffs on USD 50B in Chinese goods. Chinese has announced a retaliation list several months ago that include 25% tariffs on US soybeans. ASA described the Chinese retaliation as "devastating to growers of the number one US agricultural export." NAWG said "adding a 25 percent tariff on exports to China for US wheat is the last thing we need during some of the worst economic times in farm country."

NCGA warned farmers "cannot afford the immediate pain of retaliation nor the longer term erosion of long-standing market access and economic partnerships with some of our closest friends and allies." AEM also said "we strongly oppose a trade war with China because no one ever wins in these tit-for-tat dispute".

Here is the full release.

BoJ stands pat as widely expected

BoJ left monetary policy unchanged today as widely expected. Under the yield curve control framework, short term policy rate is held at -0.1%. BoJ will also continue target to keep 10 year JGB yield at around 0%. Annual pace of JGB purchase is kept at around JPY 80T. Goushi Kataoka dissented again in a 8-1 vote. Kataoka pushed to "further strengthen monetary easing" so that "yields on JGBs with maturities of 10 years and longer would broadly be lowered further."

The description on the economy is largely unchanged. One exception is that CPI is now "in the range of 0.5-1.0%", comparing to April's description of moving around 1 percent. On the outlook, BoJ noted that the economy is "likely to continue its moderate expansion." Domestic demand will follow an uptrend while exports will continue the moderate increasing trend. Risks to the outlook include the following: the U.S. economic policies and their impact on global financial markets; developments in emerging and commodity-exporting economies; negotiations on the United Kingdom's exit from the European Union (EU) and their effects; and geopolitical risks.

BoJ Kuroda: Deflationary mindset caps medium- and long-term inflation expectations

In the post meeting press conference, BoJ Governor Haruhiko Kuroda admitted that " year-on-year growth in consumer prices is slowing". Falling durable goods prices and temporary fluctuations in hotel costs were part of the reasons. However, "companies' price-setting behavior appears to be changing" as they're passing on rising costs to consumer. Hence, the economy is "sustaining momentum" to achieve the 2% inflation target. Kuroda also said there will be further debate on price moves at the next meeting in July, when the quarter long-term forecasts will also be published.

Kuroda added that "Japan's economy is seeing labor markets tighten and the output gap improving, but prices aren't rising much." There are external factors from US and Europe. At the same time, that's the deflationary mindset of households and companies, which became entrenched due to 15 years of deflation." That's the reason keeping medium- and long-term inflation expectations subdued.

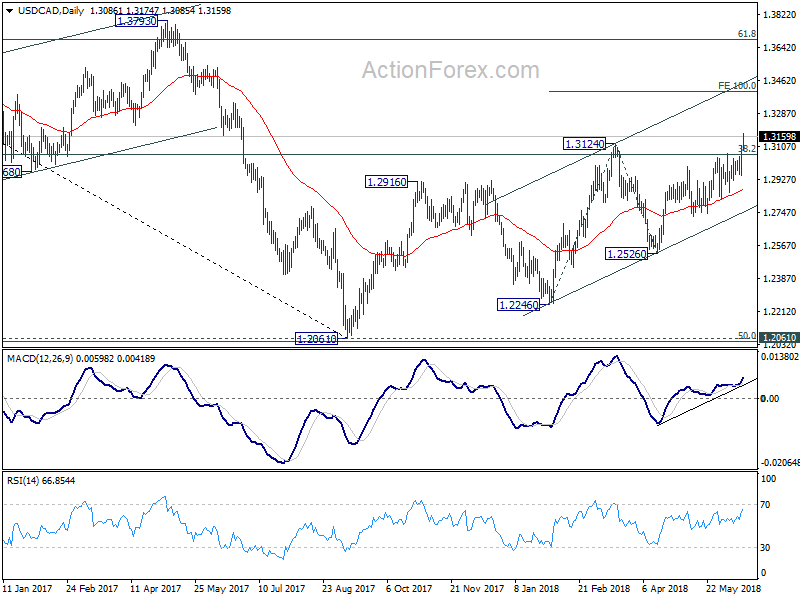

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2997; (P) 1.3054; (R1) 1.3163; More...

USD/CAD's rally continues today and reaches as high as 1.3174 so far. Intraday bias remains on the upside. Further rally should be seen to 100% projection of 1.2246 to 1.3124 from 1.2526 at 1.3404 next. On the downside, below 1.3085 minor support will turn intraday bias neutral and bring consolidation first, before staying another rally.

In the bigger picture, the current development affirms our bullish view. That is, firstly, rebound from 1.2061 is not finished yet. Secondly, the medium term decline from 1.4689 (2016 high) has completed and the trend is reversing. Sustained trading above 38.2% retracement of 1.4689 to 1.2061 at 1.3065 will confirm our view and target 61.8% retracement at 1.3685 and above. 1.3685. However, break of 1.2526 support will dampen this bullish view again. And, focus will be back on 1.2061 key support level, which is close to 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | BusinessNZ Manufacturing PMI May | 54.5 | 58.9 | 59.1 | |

| 02:41 | JPY | BoJ Rate Decision | -0.10% | -0.10% | -0.10% | |

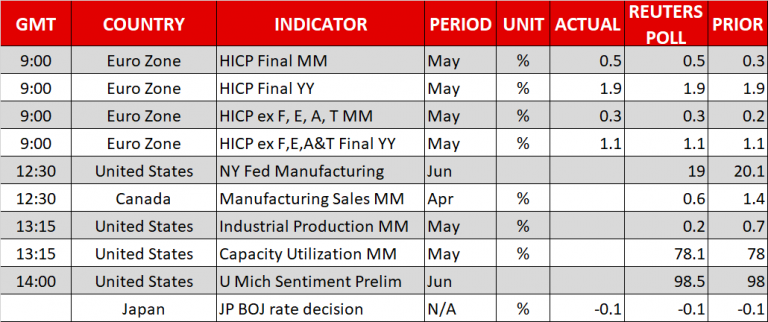

| 09:00 | EUR | Eurozone Trade Balance (EUR)Apr | 18.1B | 20.2B | 21.2B | |

| 09:00 | EUR | Eurozone CPI M/M May | 0.50% | 0.30% | 0.30% | |

| 09:00 | EUR | Eurozone CPI Y/Y May F | 1.90% | 1.20% | 1.20% | |

| 09:00 | EUR | Eurozone CPI Core Y/Y May F | 1.10% | 1.10% | 1.10% | |

| 09:00 | EUR | Eurozone Labour Costs Y/Y Q1 | 2.00% | 1.90% | 1.50% | 1.40% |

| 12:30 | CAD | International Securities Transactions (CAD) Apr | 9.13B | 5.49B | 6.15B | 6.40B |

| 12:30 | CAD | Manufacturing Sales M/M Apr | -1.30% | 0.20% | 1.40% | |

| 12:30 | USD | Empire State Manufacturing Jun | 25 | 19.75 | 20.1 | |

| 13:15 | USD | Industrial Production M/M May | 0.30% | 0.70% | ||

| 13:15 | USD | Capacity Utilization May | 78.10% | 78.00% | ||

| 14:00 | USD | U. of Mich. Sentiment Jun P | 98.5 | 98 |

US announced Tariffs on USD 34B of Chinese imports, starting July 6. Added USD 16B products for public...

The US Trade Representative formally announced the section 301 tariffs on Chinese imports, targeting products related to the Made in China 2025 policy. USTR said these "strong defensive actions" are to " protect America's leadership in technology and innovation against the unprecedented threat posed by China's theft of our intellectual property, the forced transfer of American technology, and its cyber attacks on our computer networks." And it condemned that "China's government is aggressively working to undermine America's high-tech industries and our economic leadership through unfair trade practices and industrial policies like 'Made in China 2025.'"

There are two set of tariffs lines. The first set contains 818 lines of the original 1,333 lines announced in April. This set covers around USD 34B of Chinese imports. 25% tariffs will be imposed starting July 6, 2018. The second set contained 284 proposed tariff lines, covering around USD 16B in Chinese goods. This set will undergo further public view before finalizing.

Altogether they're valued around USD 50B. and focuses on products from industrial sectors that contribute to or benefit from the "Made in China 2025" industrial policy, which include industries such as aerospace, information and communications technology, robotics, industrial machinery, new materials, and automobiles. The list does not include goods commonly purchased by American consumers such as cellular telephones or televisions.

US announced tariffs on USD 50B of Chinese imports, full statement

USTR Issues Tariffs on Chinese Products in Response to Unfair Trade Practices

Washington, DC – The Office of the United States Trade Representative (USTR) today released a list of products imported from China that will be subject to additional tariffs as part of the U.S. response to China’s unfair trade practices related to the forced transfer of American technology and intellectual property.

On May 29, 2018, President Trump stated that USTR shall announce by June 15 the imposition of an additional duty of 25 percent on approximately $50 billion worth of Chinese imports containing industrially significant technologies, including those related to China’s “Made in China 2025” industrial policy. Today’s action comes after an exhaustive Section 301 investigation in which USTR found that China’s acts, policies and practices related to technology transfer, intellectual property, and innovation are unreasonable and discriminatory, and burden U.S. commerce.

“We must take strong defensive actions to protect America’s leadership in technology and innovation against the unprecedented threat posed by China’s theft of our intellectual property, the forced transfer of American technology, and its cyber attacks on our computer networks,” said Ambassador Robert Lighthizer. “China’s government is aggressively working to undermine America’s high-tech industries and our economic leadership through unfair trade practices and industrial policies like ‘Made in China 2025.’ Technology and innovation are America’s greatest economic assets and President Trump rightfully recognizes that if we want our country to have a prosperous future, we must take a stand now to uphold fair trade and protect American competitiveness.”

The list of products issued today covers 1,102 separate U.S. tariff lines valued at approximately $50 billion in 2018 trade values. This list was compiled based on extensive interagency analysis and a thorough examination of comments and testimony from interested parties. It generally focuses on products from industrial sectors that contribute to or benefit from the “Made in China 2025” industrial policy, which include industries such as aerospace, information and communications technology, robotics, industrial machinery, new materials, and automobiles. The list does not include goods commonly purchased by American consumers such as cellular telephones or televisions.

This list of products consists of two sets of U.S tariff lines. The first set contains 818 lines of the original 1,333 lines that were included on the proposed list published on April 6. These lines cover approximately $34 billion worth of imports from China. USTR has determined to impose an additional duty of 25 percent on these 818 product lines after having sought and received views from the public and advice from the appropriate trade advisory committees. Customs and Border Protection will begin to collect the additional duties on July 6, 2018.

The second set contains 284 proposed tariff lines identified by the interagency Section 301 Committee as benefiting from Chinese industrial policies, including the “Made in China 2025” industrial policy. These 284 lines, which cover approximately $16 billion worth of imports from China, will undergo further review in a public notice and comment process, including a public hearing. After completion of this process, USTR will issue a final determination on the products from this list that would be subject to the additional duties.

USTR recognizes that some U.S. companies may have an interest in importing items from China that are covered by the additional duties. Accordingly, USTR will soon provide an opportunity for the public to request the exclusion of particular products from the additional duties subject to this action. USTR will issue a notice in the Federal Register with details regarding this process within the next few weeks.

Background

President Trump announced on March 22, 2018, that USTR shall publish a proposed list of products and any intended tariff increases in order to address the acts, policies, and practices of China that are unreasonable or discriminatory and that burden or restrict U.S. commerce.

These acts, policies and practices of China include those that coerce American companies into transferring their technology and intellectual property to domestic Chinese enterprises. They bolster China’s stated intention of seizing economic dominance of certain advanced technology sectors as set forth in its industrial plans, such as “Made in China 2025.” (See USTR Section 301 Report here.)

On April 3, USTR announced a proposed list of 1,333 products that may be subject to an additional duty of 25 percent, and sought comments from interested persons and the appropriate trade advisory committees.

Interested persons filed approximately 3,200 written submissions. In addition, USTR and the Section 301 Committee convened a three-day public hearing from May 15-17, 2018, during which 121 witnesses provided testimony and responded to questions. The public submissions and a transcript of the hearing are available on www.regulations.gov in docket number USTR-2018-0005.

Click here to view a fact sheet on the Section 301 product list.

Click here to view a fact sheet on the Section 301 investigation.

Dollar Closing in on 111 Yen as Trade War Escalates

The Japanese yen has inched lower in the Friday session. In the North American trade, USD/JPY is trading at 110.73, up 0.09% on the day. On the release front, the Bank of Japan held the course on monetary policy. In the U.S, the Empire State Manufacturing Index is forecast to drop to 19.1 points. We’ll also get a look at UoM Consumer Confidence, which is forecast to soften to 98.5 points.

There were no surprises from the Bank of Japan policy meeting. Policymakers maintained interest rates at -0.10%. The bank also downgraded its inflation forecast to a range of between 0.5% and 1.0%, underscoring that the massive stimulus program has failed to raise inflation anywhere near the bank’s target of around 2 percent. Japanese officials are nervously watching as the Trump administration slapped further tariffs on $50 billion of Chinese products. Although Japan appears to be in Trump’s good graces for now, an escalation in tariffs could trigger a global trade war, which would be disastrous for Japan’s export-reliant economy.

As widely expected, the Federal Reserve raised interest rates by a quarter-point, to a range between 1.75 percent and 2.00 percent. Fed Chair Jerome Powell sounded hawkish in his press conference, saying that the economy was performing well and that “overall outlook for growth remains favorable”. This message echoed the rate statement, in which policymakers said that “economic activity has been rising at a solid rate”, pointing to stronger consumer spending and business investment. What was may have been the most notable development was that the Fed rate projections were revised upwards, predicting two additional rate hikes in 2018, for a total of four hikes. Until now, the Fed had projected three rate hikes this year. This represents a nod to the strength of the U.S economy and could boost the dollar against its rivals.

Canadian Dollar Slides to 1-Year Low as Trump Prepares China Tariffs

The Canadian dollar continues to lose ground in the Friday session, after strong gains on Thursday. Currently, USD/CAD is trading at 1.3129, up 0.18% on the day. Earlier in the day, the Canadian currency dropped to its lowest level since June 2017. On the release front, Canadian Manufacturing Sales is expected to fall to 0.6%. In the U.S, the Empire State Manufacturing Index is forecast to drop to 19.1 points. We’ll also get a look at UoM Consumer Confidence, which is forecast to soften to 98.5 points.

As widely expected, the Federal Reserve raised interest rates by a quarter-point, to a range between 1.75 percent and 2.00 percent. Fed Chair Jerome Powell sounded hawkish in his press conference, saying that the economy was performing well and that “overall outlook for growth remains favorable”. This message echoed the rate statement, in which policymakers said that “economic activity has been rising at a solid rate”, pointing to stronger consumer spending and business investment. What was may have been the most notable development was that the Fed rate projections were revised upwards, predicting two additional rate hikes in 2018, for a total of four hikes. Until now, the Fed had projected three rate hikes this year. This represents a nod to the strength of the U.S economy and could boost the dollar against its rivals.

Prime Minister Justin Trudeau is still smarting from the disastrous G7 summit which he hosted. Canada, along with other members of the G7, vociferously complained about the tariffs which Trump imposed on Canada and the European Union. The summit ended in disarray, with Trump labeling Trudeau “weak” and “dishonest”. The meeting exposed fault lines between Trump and the other leaders over trade, and Trump’s protectionist stance could spell trouble for the Canadian economy and send the wobbly Canadian dollar even lower. Trump is expected to impose further tariffs on China as early as Friday, which has lowered risk appetite and weighed on the Canadian currency. Meanwhile, negotiations to update the NAFTA agreement are deadlocked, with Canada unhappy about a U.S demand for a sunset clause after five years, which would require the parties to hammer out a new agreement. Mexico is holding general elections on July 1, and a left-wing candidate, Andrés Manuel López Obrador, leads in the polls. If López Obrador becomes president, it could mean more complications for the NAFTA talks.

Trade Tensions Set to Escalate, Will Markets Take Notice?

The trade narrative has been somewhat overshadowed by geopolitics and central bank meetings lately, but that may change as soon as today. The US is set to announce a revised list of Chinese products it will impose tariffs on, which could provoke a proportional response from China and reignite fears of a trade war. While the situation may escalate in the near-term, potentially unleashing another bout of risk aversion, the end result still appears more likely to be a trade deal, and not a “war”.

To say that the global trade outlook appears bleak would be somewhat of an understatement. Even former Fed Chair Alan Greenspan lately suggested we are “on the edge of a trade war”, as recent hopes that negotiations could bear fruit quickly faded, replaced with signals that further intensification in frictions is looming. The next few weeks will probably be very interesting.

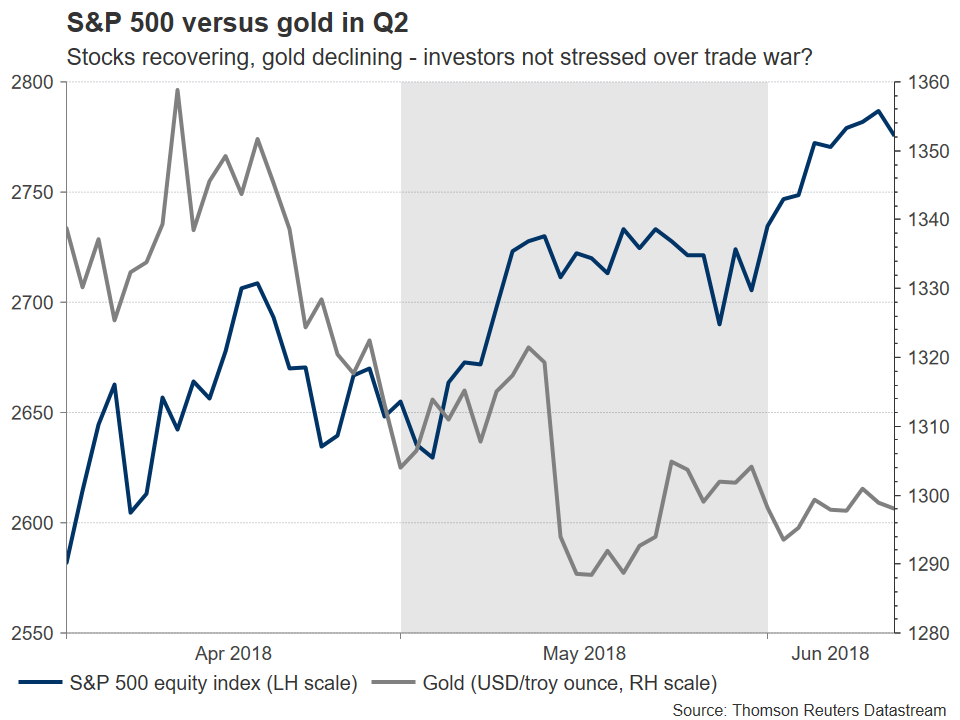

Much ado about nothing?

While developments around protectionism have dominated media headlines in recent months, investors have remained surprisingly unfazed. Yes, markets have moved on major announcements, but those moves often did not have a lasting impact and retraced quickly. Haven assets such as gold – which typically see increased demand in times of turmoil – have moved lower in Q2, while major stock indices like the S&P 500 have slowly managed to recover most of their losses from earlier this year.

Merging price action with actual developments, one can reach two conclusions. Investors still perceive the US moves as “hardball” negotiating tactics that will not produce an actual trade war, and/or believe the impact of a trade standoff will be rather small and thus not a reason to adjust their portfolios. Both arguments have merit. The Trump administration’s moves indeed appear to be aimed at ramping up pressure to draw concessions from other nations once negotiations begin, and not the opening salvo in a trade war. Meanwhile, the consensus among the economics community is that if only the so-far announced tariffs are implemented, the effects on the major economies would be negligible – at worse shaving off one to two tenths of a percent from GDP growth.

Crucially though, it’s a thin line between threatening tariffs as part of a high-stakes negotiating tactic to gain leverage, and “over-posturing” with such measures, risking the other party walking away from talks or worse still, replying in kind. As for whether the impact will be just a “flesh wound” for the broader economy, that may well be true in a model, but it’s debatable whether such models accurately capture the knock-on effects trade barriers could have on sentiment, business investment, and even hiring. Moreover, it may be unfair to judge the impact of tariffs on the whole economy, as some sectors would be severely impacted, while others not affected at all. Not to mention that the prospect of future tariffs – in case frictions heat up further – is not included in such calculations.

US set to escalate, and China may “play ball”

Even though things were looking rosy a few weeks ago, with the US and China citing progress in talks, that narrative quickly got turned on its head after the White House announced it will impose 25% tariffs on $50bn of Chinese goods. The US is due to announce today the specific list of goods, something likely to provoke a symmetrical response from China, potentially unleashing another wave of risk aversion as concerns for a tit-for-tat escalation are reignited. That could divert funds out of riskier assets like equities, and into safe-havens such as gold and the yen.

Pundits suggest the US could shy away from imposing tariffs as a gesture of good faith to restart negotiations. Others argue a reversal would draw fierce criticism from both Democrats and Republicans, causing the President to lose popularity with his voting base. Indeed, it appears Trump may need a “victory” on trade, especially ahead of the midterm elections in November, where his Republican party is polling behind Democrats. This means drawing out more Chinese concessions, which may not be forthcoming considering all the compromises the Asian nation has already agreed to, including lowering import tariffs on products like cars and opening its economy further to foreign investment. Besides, Chinese politicians may want to preserve face themselves by not appearing intimidated by US threats.

EU and Japan on Trump’s radar too

While most attention has fallen on US-China frictions, the next target on President Trump’s “hit list” is most likely the EU, and specifically Germany. He has frequently thrown jabs at European economies for running surpluses with the US, setting the stage for an eventual action. The US is currently considering tariffs on imported cars, which would disproportionately single out Japan and Germany – two of the largest vehicle exporters to the US. Similar to how the steel and aluminum tariffs were rolled out, the US Commerce Department is currently investigating whether to impose such levies. The study will likely conclude later this year, at which point the US-German standoff could become a dominant theme.

The same may not be true for Japan though, as there are caveats Prime Minister Abe can use in negotiating. For instance, 75% of all Japanese-brand vehicles sold in the US are actually produced in North America, with those plants employing hundreds of thousands of Americans. More importantly, considering the delicate situation with North Korea and Japan’s position, Abe may well choose a less-confrontational route towards reducing the US-Japan trade deficit, such as agreeing to buy more US military equipment. That could also appease domestic calls to raise defense spending amid growing security risks.

Blame Canada

Let’s not forget NAFTA. Despite frequent reports the three sides (US, Canada, Mexico) are making “real progress”, the negotiations have not produced any tangible results. The trilateral push to reach a deal before Mexico’s presidential elections on July 1 appears to have failed, implying the talks are likely to drag on as Mexico’s leadership change and US midterm elections complicate matters.

Meanwhile, the relationship between Trump and Canadian PM Trudeau appears to have hit new lows. The US President was apparently infuriated by Trudeau’s remarks at the latest G7 summit, saying “that’s going to cost a lot of money for the people of Canada” – dashing hopes for a swift resolution to NAFTA. The uncertainty has likely been among the factors keeping the loonie and peso on the back foot, and in the case of Canada is also disrupting the central bank’s job, which is raising rates amid heightened trade risks. While a potential NAFTA agreement would probably lead to a remarkable rally in both the loonie and peso, the situation currently looks unlikely to resolve itself anytime soon, suggesting trade risks may remain a drag on the two currencies for a while more.

Things may escalate, but ultimate deal still more likely than “war”

As America attempts to renegotiate its trading relationship with the rest of the world, it is playing a very delicate negotiating game, and recent signals suggest things could heat up further. The US seems ready to unveil fresh tariffs against China, at which point China will probably strike back with its own levies. The question is, what does the US do after that? Seek fresh negotiations, or start looking for new ways to hit back, unleashing another bout of trade-war fears? While markets have been complacent so far, the same may not hold true if the situation truly escalates.

In the bigger picture though, looking past the posturing and politics, every side wants to avoid a real trade war. The impact of one could be devastating for all involved, with prices for goods and services likely jumping, causing discontent among consumers (who also vote) and disrupting economic growth. This suggests that even if things escalate, the most likely longer-term outcome remains striking a deal that helps everyone go home with a “victory”. Perhaps this is why investors have not overreacted yet. Let’s hope they are right.

Euro Posts Modest Gains But Set For Weekly Loss; Trump to Finalize List of Targeted Chinese Goods

Here are the latest developments in global markets:

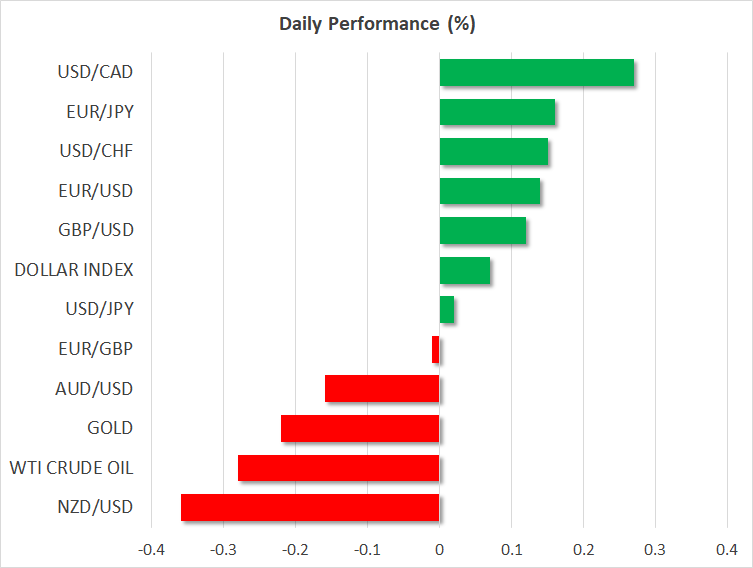

FOREX: The euro edged higher by 0.26% versus the US dollar on Friday but was set to post its biggest weekly loss in 19 months after the European Central Bank (ECB) signaled it will keep rates at record lows until late 2019, pushing euro/dollar down by more than 250 pips at one point on Thursday. Meanwhile, Eurozone’s final CPI readings for May were in lie with preliminary estimates, with ECB member, Ewald Nowotny, saying that the central bank’s inflation target of just below 2.0% is close to be achieved. Sterling started the day in negative territory amid rising Brexit tensions, challenging $1.3210 but managed to move higher later, gaining 0.11% against the greenback. Dollar/yen was flat at 110.65, below the almost one-month high of 110.89 reached earlier after the Bank of Japan (BOJ) kept its policy unchanged but downgraded its assessment on inflation earlier on Friday. Meanwhile, the US dollar index reached a 7-month high of 95.13 before it slid to 94.87 (+0.11%). Trade uncertainties continued to weigh on the greenback as the EU backed a retaliatory plan against US import tariffs on Thursday, while India also joined later on, announcing potential countermeasures on US goods. In the antipodean sphere, aussie/dollar touched a 1-month low of 0.7450 today, falling by 0.20%, while kiwi/dollar dived by 0.43% to 0.6952. Dollar/loonie rose by 0.34% towards a new 1-year high of 1.3153.

STOCKS: European equities were heading downwards on Friday at 1120 GMT, with the French CAC 40 which was up by 0.17% underpinned by gains in the healthcare sector being the exception. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were down by 0.41% and 0.44% respectively, with financials losing the most. The German DAX 30 dropped by 0.31% and the Italian FTSE MIB declined by 1.14%. The British FTSE 100 was in negative territory as well, losing 0.77%, while the Spanish IBEX 35 dived by 1.16%. Futures tracking US stock indices were flashing red, pointing to a negative open.

COMMODITIES: Oil prices retreated on Friday before the OPEC meeting in Vienna on June 22 on rising prospects of increased supply in the market. West Texas Intermediate (WTI) crude oil dipped by 0.27% to $66.71 per barrel, while London-based Brent plummeted by 1.04% to $75.15 per barrel. In precious metals, gold pulled back from a 1-month high of $1,309.30 reached yesterday to $1,299.05/ounce (-0.27%).

Day ahead: Trump to reveal list of Chinese goods that may face tariffs; US industrial production pending

Later on Friday, all eyes will turn to the US, where the White House is expected to announce the final list of Chinese products that could be subject to a 25% tariff, a move that could further deteriorate the trade relations between the world’s two largest economies. Today a Chinese foreign ministry spokesman warned that Beijing will void all US-China trade talks if the US pushes forward with tariffs. Meanwhile on Thursday, the IMF director Christine Laggard expressed her opposition to the US actions on trade as well, saying that the measures “are likely to move the globe further away from an open, fair and rules-based trade system, with adverse effects for both the US economy and for trading partners”.

Besides trade headlines, investors will also pay attention to US industrial production trends due at 1315 GMT. The numbers are expected to show a weaker growth of 0.2% m/m in industrial output in April compared to a 0.7% expansion in the previous month; manufacturing output data are also of significance. Earlier at 1230 GMT, the New York Fed is anticipated to indicate a slowdown in its Empire State Manufacturing Index, whereas, at 1400 GMT, June’s preliminary reading for the University of Michigan Consumer Sentiment Index is forecasted to improve by 0.5 points to 98.5.

Elsewhere, manufacturing sales in Canada are projected to post a slower increase for the third consecutive month, with the gauge expected to ease from 1.4% m/m to 0.6%.

In energy markets, the Baker Hughes company will report on US oil drilling activity at 1700 GMT, possibly bringing another wave of volatility to oil prices. Note that the number of active oil drills has been rising since March 29 and another tick to the upside could potentially put the market under pressure once again.

Brexit news will be of greater importance in the UK ahead of the Bank of England’s policy meeting next week. Despite Theresa May’s withdrawal bill getting a winning vote on amendments at the House of Commons on Tuesday, a few days later the chancellor, Philip Hammond, claimed that the amendment published on Thursday was not consistent with what had been promised by May.

As for today’s public appearances, Dallas Fed President Robert Kaplan (non-voting FOMC member in 2018) will be speaking before a business leaders luncheon hosted by the Fort Worth Chamber of Commerce at 1730 GMT.

On Monday, Japanese trade figures will gather some interest during the Asian trading session. Analysts expect Japan’s trade balance has turned negative in May, declining from a surplus of 626 billion yen in April to a deficit of 235bn.

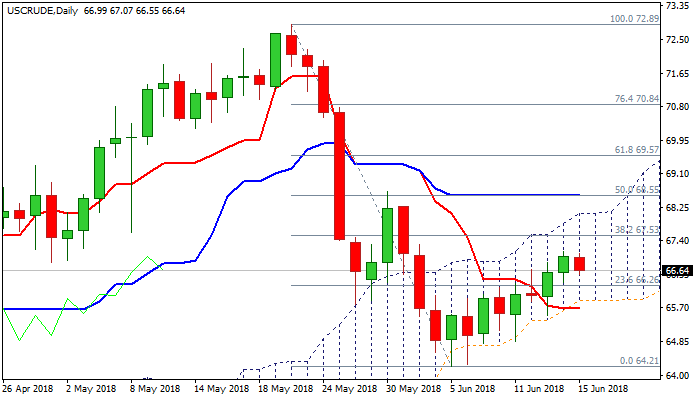

WTI OIL Outlook: Stands At The Back Foot On Concerns About Production Increase

WTI oil holds in red on Friday as on rising concerns among market participants that OPEC could vote to increase output at its meeting next week.

Shortage in supplies from Iran and Venezuela pressures main world oil producers to think of increasing production.

Initial idea of Saudi Arabia for output increase by 500,000 to 1 million barrels, gradually or at once, will be very likely on agenda on OPEC's 22 June meeting in Vienna.

Oil price could fall if OPEC start increasing the output, which would be the first time since main oil producers agreed to reduce oil production by 1.8 million barrels in 2017, with the deal expiring at the end of 2018, if not extended.

Today's easing so far looks like consolidation as oil price is in uptrend from $64.21 (05 May low) and maintaining strong momentum.

The bull-leg remains supported by the base of rising daily cloud and lays at $65.90 today, marking key support.

Corrective dips are expected to find footstep at cloud base to keep bullish structure intact.

At the upside, cloud top at $68.09, marks the upper pivot, break above which is needed to generate strong signal for bullish continuation.

Res: 67.14, 67.53, 68.09, 68.55

Sup: 66.55, 65.90, 65.51, 64.84