Sample Category Title

China Makes Changes To Composition Of PBoC

General Trend:

- Shanghai Composite trades at over 1-year low

- South Korean equities and Won (KRW) decline

- Australia ASX 200 outperforms on gains in the telecom, energy, utilities and financial sectors

- BoJ affirms moderate expansion for the economy, despite Q1 GDP contraction; cuts inflation assessment (as speculated)

- China PBoC’s reluctance to raise OMO rates after recent Fed hike has led to concerns about the domestic economy (Chinese press)

- China makes changes to composition of PBoC

- Argentina shakes up central bank following recent IMF agreement

- BoJ Gov Kuroda’s post-rate decision press conference expected at 0630 GMT

Headlines/Economic Data

Australia/New Zealand

- ASX 200 opened +0.3%

- ASX 200 Telecom index +1.9%, Utilities +1.6%, Financials +1.5%, Energy +1.5%, Resources +1.1%

- (AU) Reserve Bank of Australia (RBA) Assist Gov Ellis: Infrastructure can have significant spillover benefits

- (NZ) New Zealand May Business NZ PMI: 54.5 v 58.9 prior

- (NZ) New Zealand May Non Resident Bond Holdings: 58.9% v 59.8% prior

China/Hong Kong

- Shanghai Composite opened -0.2%, Hang Seng -0.1%

- Hang Seng Materials index -1.2%, Telecom -0.9%, Energy -0.6%, Utilities -0.5%,Consumer Goods -0.4% Financials -0.2%

- Shanghai Composite property sub-index rises by over 1%

- Brokers in Hong Kong said to offer HK$155B in margin loans related to IPO for Xiaomi - HK Press

- (US) Trump administration official: Trump will direct 'pretty significant action' on tariffs against China; expected to affect $50B in Chinese products

- (CN) White House said to put tariffs on a smaller list of 800 to 900 products from China tomorrow (trimmed from original list of 1,300 products) – CNBC

- (CN) CHINA MAY NEW HOME PRICE M/M: 0.7% V 0.6% PRIOR: Y/Y: 4.7% V 4.7% PRIOR

- (CN) PBoC conducts CNY60.5B Pledged Supplemental Lending (PSL) operation

- (CN) PBoC names Vice Finance Minister Liu Wei as member of Monetary Policy Committee; PBoC Chief Economist Ma Jun named as PBoC Adviser; Names PBoC Gov Yi Gang as Committee Chief.

- (CN) China PBoC Open Market Operation (OMO): Injects CNY100B in 7, 14 and 28-day reverse repos v CNY150B injected in 7, 14 and 28-day reverse repos prior: Net: CNY90B injection v CNY70B injected prior

- (CN) For the week, PBoC injected net of CNY240B in open market operations v CNY300B net drain w/w

- (CN) China Finance Ministry (MOF): Cut subsidies for certain renewable energy project including waste-to-energy and biomass

- (CN) China NDRC said to consider investment management rules for the auto industry – Chinese Press

- (CN) China Finance Ministry sells 30-year bonds: yield 4.1082% v 4.10%e, bid to cover 1.75x v 1.91x prior

Japan

- Nikkei 225 opened +0.6%

- TOPIX Electric Appliances index +0.5%, Information & Communication +0.5%, Real Estate +0.3%

- Megabanks lag the overall market

- (JP) BoJ leaves policy unchanged (as expected); Sees CPI in range of 0.5% to 1.0%

Korea

- Kospi opened +0.4%

- (KR) South Korea May Unemployment Rate: 4.0% v 3.8% prior

- (KR) South Korea Finance Min: May job market report was ‘shocking’ in that job growth remained weak; Labor difficulties in certain industries are worsening

- (KR) South Korea Finance Min Kim: Impact of ECB is ‘limited”

Other

- (PH) Water rates in the Philippines are expected to rise due to FX impact - Local Press

North America

- US equity markets ended mixed: Dow -0.1%, S&P500 +0.3%, Nasdaq +0.9%, Russell 2000 +0.5%

- S&P500 Utilities +1.2%, Consumer Discretionary +1%; Financials -0.9%

- NXP Semiconductors [NXPI]: China said to approve sale to Qualcomm, says HK report; The transaction is still awaiting Chinese approval, according to separate financial press report

- (CA) Bank of Canada (BOC) Wilkins: To evaluate effect of US tariffs on consumer prices

Europe

- (EU) ECB policymakers reportedly at odds over policy statement wording on end of QE and rate hike; some wanted to signal possible rate hike in mid 2019 and others want to keep option open for extension of bond buys - press

Levels as of 01:30ET

- Nikkei 225 +0.5%, ASX 200 +1.3%, Hang Seng -0.1%; Shanghai Composite -0.8%; Kospi -0.5%

- Equity Futures: S&P500 flat; Nasdaq100 flat, Dax flat; FTSE100 +0.1%

- EUR 1.1555-1.1585 ; JPY 110.45-110.81 ; AUD 0.7452-0.7480 ;NZD 0.6946-0.6977

- Aug Gold -0.3% at $1,304/oz; Jul Crude Oil +0.1% at $66.97/brl; Jul Copper +0.3% at $3.212 /lb

ECB Stepped Up Its Forward Guidance On Rates

Market movers today

It has been an ext remely busy week but it is not over yet ! The most important event today is whether Trump is going to publish the full list of the Chinese tech products (USD50bn) being hit by 25% tariffs or not. And perhaps more importantly, how will China then react over the weekend? Risk of an escalation has increased.

In the US, we will keep an eye on the Empire manufacturing index and the preliminary consumer confidence index from University of Michigan. Especially the former will be interest ing, as we have mixed signals from the manufacturing sector at the moment .

We expect the Russian central bank to cut its policy rate from 7.25% to 7.00% today.

Selected market news

The ECB announced its formal end to QE at its monetary policy meeting yesterday, saying that it will buy bonds unt il the end of the year with a purchase rate of EUR15bn per month in Q4. At the same time, the ECB stepped up its forward guidance on rates and said interest rates will remain at their present levels at least through the summer of 2019. This means that we expect the first ‘live' meeting t o be in Sept ember 2019. While timing of the announcement was somewhat of a surprise as we expected the ECB to change its communicat ion in July and not in June, the announcement was as we expected and we maintain our call on the first ECB rate hike being by 20bp in December 2019.

Overall, Mario Draghi struck a dovish tone throughout the ECB press conference and markets took the introductory statement and Q&A as dovish: the euro weakened and European fixed income markets rallied significantly. There remain a lot of ‘ifs' in the statement (i.e. ‘st ate dependency'), making the further reduct ion of QE in Q4 and first hike timing still dependent on incoming data on economic/inflation developments. We still think the ECB will continue to be dovish, at least in the near term. See ECB Review: End of APP - but stronger on rate guidance.

The Bank of Japan (BoJ) kept i ts monetary policy unchanged with an 8-1 vote as widely expected. The BoJ downgraded its assessment of inflation and now sees the CPI inflation in a range of 0.5-1% which indicates that the BoJ might revise down its inflation out look when it releases its quarterly forecast update in July. Hence, the BoJ is not in the normalisation camp with central banks like the Fed and ECB. We expect the BoJ to keep its current yield curve control unchanged for the next 12 months. USD/JPY trades slightly higher after the announcement and has generally been supported by a const ruct ive risk sent iment overnight .

Political uncertainty remains high in the UK, as the Conservat ive Party remains ext remely divided on how to proceed with the Brexit negot iat ions and not least what a "meaningful vote" in the UK parliament means in practice. A couple of days ago, it seemed likely that PM Theresa May would pass her EU withdrawal bill, but the development yesterday suggests that she might lose the vote when the bill returns to the House of Commons next week (House of Lords vote on Monday). May thinks she has the numbers to avoid a defeat to the Conservative anti - Brexiteers and soft Brexiteers. Overall, do not expect much to be agreed upon at the EU summit on 28-29 June, making the EU summit in October even more important.

Currencies: EUR/USD Nears 1.1510 Correction Low As ECB Cements Low Rates

- Rates: Lower for longer trumps end of APP

The ECB's change to forward guidance on rates, lower for longer, trumped the announcement to end APP this year and caused investors to push back early rate hike bets. German yields dropped up to 7 bps. The German and US 10-yr yields' test of respectively 0.5% and 3% resistance failed this week, suggesting consolidation ahead. - Currencies: EUR/USD nears 1.1510 correction low as ECB cements low rates

Yesterday, EUR/USD nosedived as the ECB committed to keep policy rates unchanged at least through the summer of next year. The dollar remains supported by strong US data. Today, markets might further adapt positions in the wake of yesterday's ECB meeting. EUR/USD nears the 1.1510 correction low. Rising trade tension probably won't help the euro as well.

The Sunrise Headlines

- The US equity markets reacted positively to the ECB news, with only the DOW JONES closing with losses (-0.1%). Nasdaq wins 0.85%. Asian markets opened mixed this morning, with Japan recording gains and China in red.

- The Bank of Japan (BOJ) kept its short-term interest rate target at -0.1%, continuing its loose monetary policy. It states that the economy is expanding only moderately and inflation tempered in May, moving around 0,5-1%.

- Today, President Trump will approve to impose tariffs on $50bn on Chinese imports. Tariffs will focus on Chinese exports linked to Beijing's' “Made in China 2025” plan to lead the world in 10 key sectors, including robotics.

- UK PM May's counter proposal for the 'meaningful vote' has furiously been rejected. Tory rebels accuse her of going back on an earlier deal. PM May now faces defeat when the EU withdrawal bill returns to the Commons next week.

- Italy's new government threatened not to ratify the EU-Canada trade (CETA), which could endanger the entire agreement. Italy's agriculture minister used “weakening of citizens' rights” and “unfair competition” as arguments.

- The European Stability Mechanism (ESM), the euro zone bailout fund, has approved a new key payment. This approval was seen as a precondition to open new debate on new debt relief measures held in Athens next week.

- The US will release its numbers on Empire Manufacturing for June and the Industrial Production (MoM) for May. In the EU, ECB's Nowotny and Smets present the Austrian and Belgian Economic Outlook.

Currencies: EUR/USD Nears 1.1510 Correction Low As ECB Cements Low Rates

Euro hammered as ECB cemented rates

Yesterday, markets anticipated the ECB to make a step toward policy normalisation. The ECB indeed signalled to stop APP end of 2018, but also committed to keep rates unchanged through the summer of 2019. This soft guidance on rates hammered EMU yields and the euro. EUR/USD touched an intraday top in the mid 1.18 area before the ECB decision, but finished the day at 1.1568. USD/JPY wasn't affected much by the decline in core yields and closed at 110.63 (from 110.34).

This morning, Asian equities are trading mixed. China underperforms. The US preparing a new batch tariffs on Chinese imports and a stronger dollar are potential negatives for Chinese markets. The BOJ left is policy unchanged but downgrades its assessment on inflation after soft data of late. USD/JPY gained a few more ticks and is trading in 110.75 area. EUR/USD (1.1565 area) hovers within reach of the post ECB low.

Today, the final May EMU CPI will be published, expected unchanged at 1.9% Y/Y (headline). The impact from a revision will probably be limited as the ECB cemented expectations on policy rates. In the US, the Empire manufacturing survey, production and Michigan consumer sentiment will be published. US data recently mostly surprised on the upside. Will good data support further USD gains? Markets will also look out for new US import tariffs on Chinese goods. Of late, the dollar and other US assets were quite resilient to the fall-out from trade dispute. Over the previous days, we assumed EUR/USD to stay north of the 1.1510 support as tensions on Italy eased and as we expected the ECB to make a next step to policy normalisation. However, yesterday's ECB decision signalled that the euro won't get additional interest rate support anytime soon. We turn more cautious on the single currency and look out how a retest of the EUR/USD 1.1510 support turns out. A rise in the trade tension or a less positive risk sentiment probably also won't help the euro. The dollar can stay strong for longer.

Yesterday, EUR/GBP nosedived in line with the global post-ECB decline of the euro. Good UK retail sales were only of second tier importance. A further rift within the UK Conservative party on the role of Parliament in the Brexit process also had only limited impact. Brexit might stay on focus today as there are no important UK data. Even after yesterday's move, we assume that the downside in EUR/GBP remains much better protected than in EUR/USD. First support is seen near 0.87 ahead of the 0.8621 correction low.

EUR/USD: nears 1.1510 correction low as ECB cemented rates

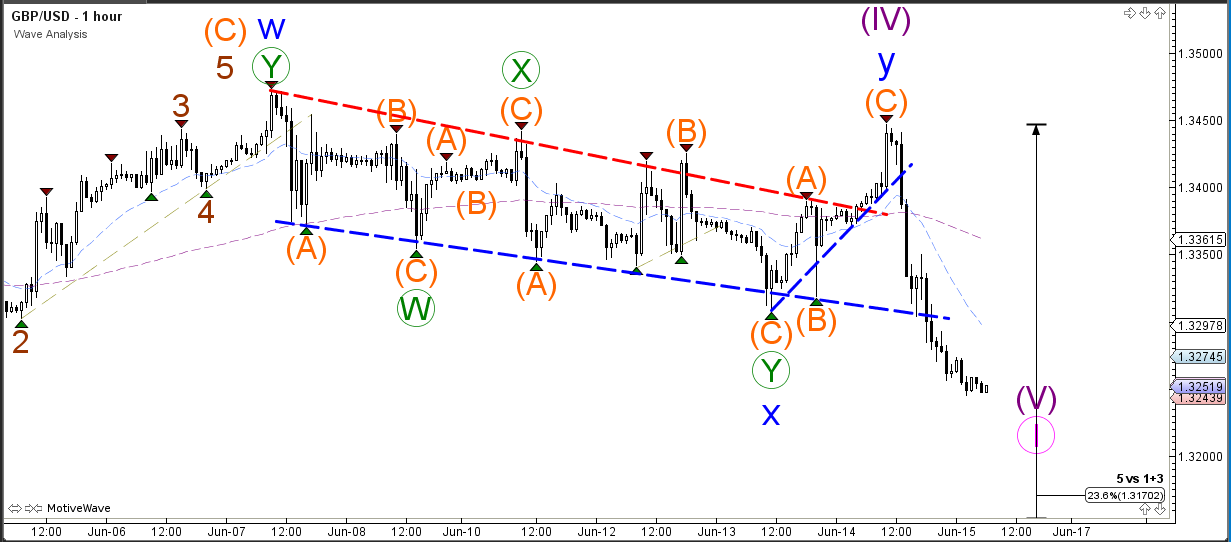

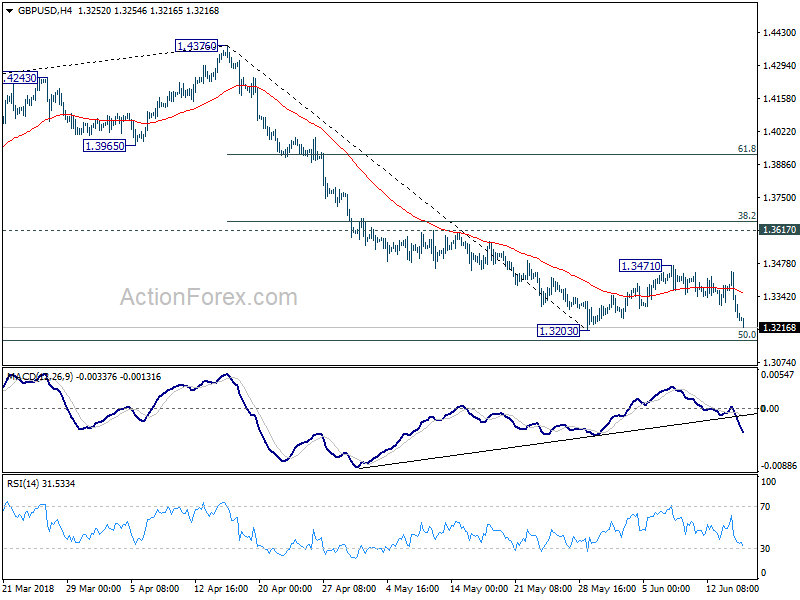

GBP/USD Breaks Support Trend Line And Challenges 1.3250

The GBP/USD failed to break above the resistance trend line (orange) and made a bearish reversal at this decision zone. Price broke below key support levels and is now challenging the 1.3250 round level and the previous bottom. A bearish break below 1.32 could see price fall towards the Fibonacci targets.

The GBP/USD broke the resistance trend line (dotted red) but price action was unable to break above the previous top. The quick bearish reversal saw price break below two support trend lines (dotted blue), one steeper and one shallower. Any bullish retracement could move up to the moving averages, which could act a resistance point.

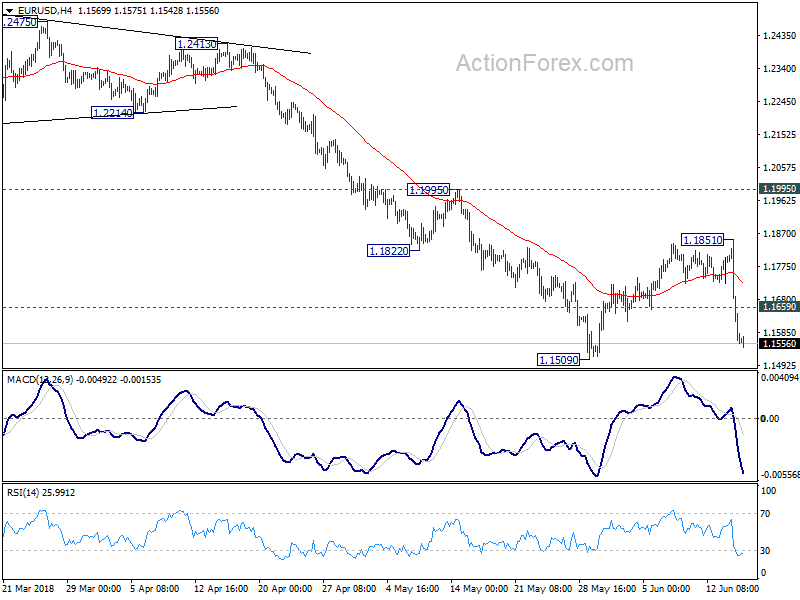

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1468; (P) 1.1659 (R1) 1.1756; More.....

Intraday bias in EUR/USD remains on the downside for 1.1509 low first. Break there will confirm resumption of larger decline from 1.2555. EUR/USD should take out 50% retracement of 1.0339 to 1.2555 at 1.1447 with ease to 61.8% retracement at 1.1186. On the upside, above 1.1659 minor resistance will delay the bearish case and bring more consolidation first.

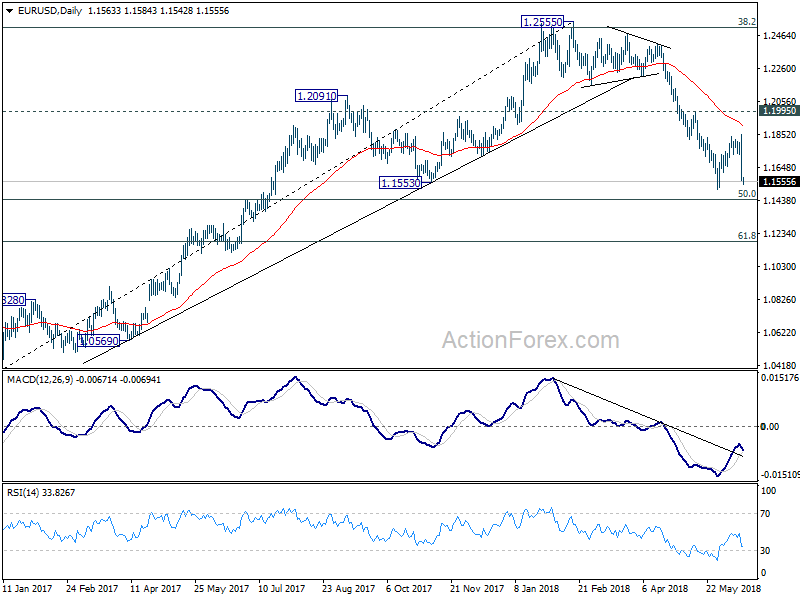

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

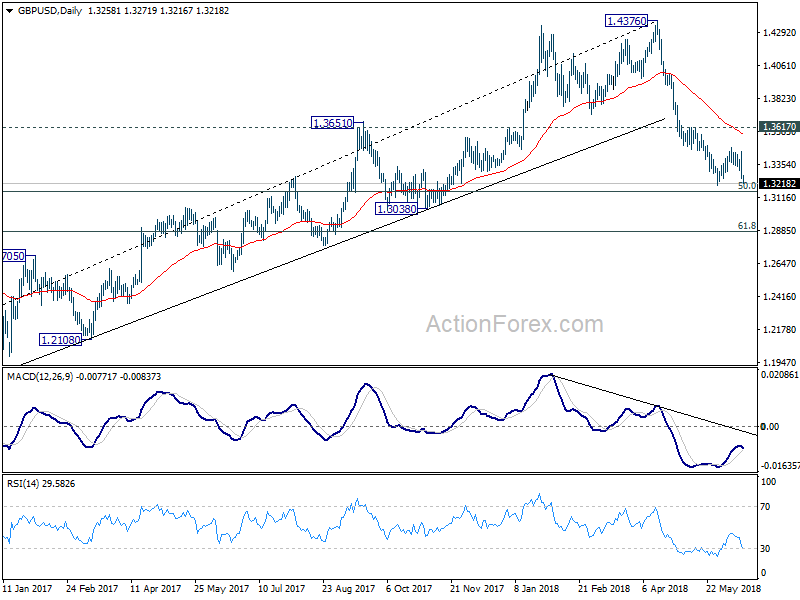

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3196; (P) 1.3321; (R1) 1.3384; More...

The break of 1.3307 reaffirmed the case that correction from 1.3203 has completed. Intraday bias is back on the downside for 1.3203 first. Break there will resume the decline from 1.4376 and through 50% retracement of 1.1946 to 1.4376 at 1.3161 first, and 61.8% retracement at 1.2875 next. For now, outlook remains bearish as long as 1.3471 resistance holds, in case of recovery.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4223). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 1.3617 resistance holds, even in case of strong rebound.

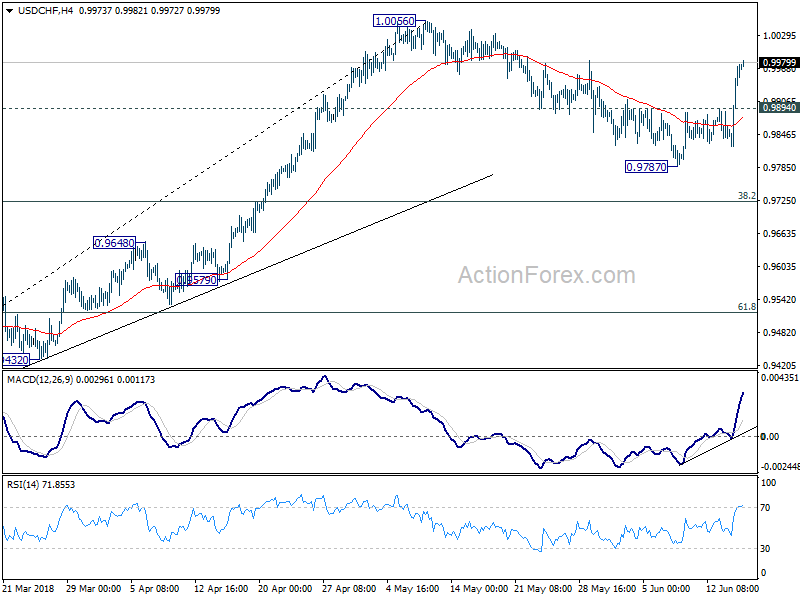

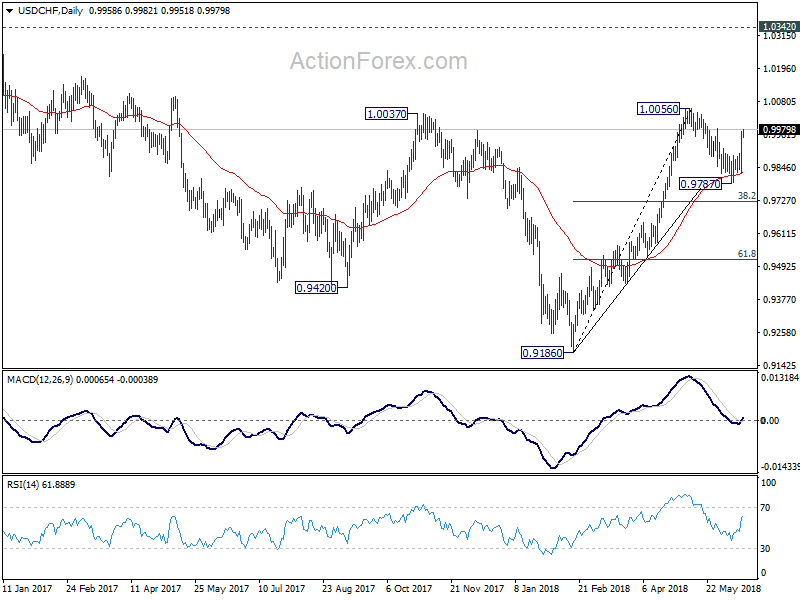

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9874; (P) 0.9923; (R1) 1.0022; More...

Intraday bias in USD/CHF remains on the upside for 1.0056 high. Decisive break there will resume larger rise fro 0.9186 and target 1.0342 key resistance next. On the downside, below 0.9894 minor support will turn bias neutral and could extend the correction from 1.0056 for a while.

In the bigger picture, medium term decline from 1.0342 has completed with three waves down to 0.9186. Rise from there is currently viewed as a leg inside the long term range pattern. Hence, while further rally would be seen, we'd be cautious on strong resistance from 1.0342 to limit upside. For now, further rise is expected as long as 38.2% retracement of 0.9186 to 1.0056 at 0.9724 holds. However, sustained break of 0.9724 will dampen this bullish view and would at least bring deeper fall to 61.8% retracement at 0.9518.

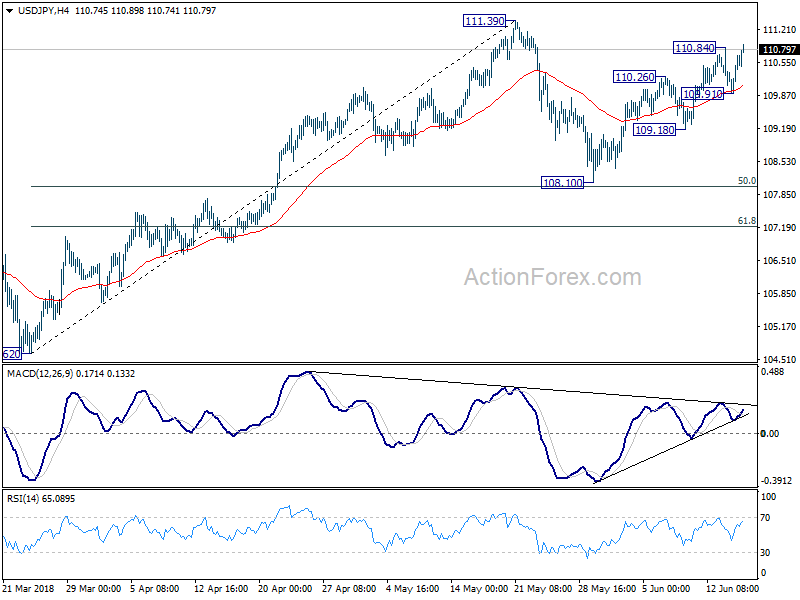

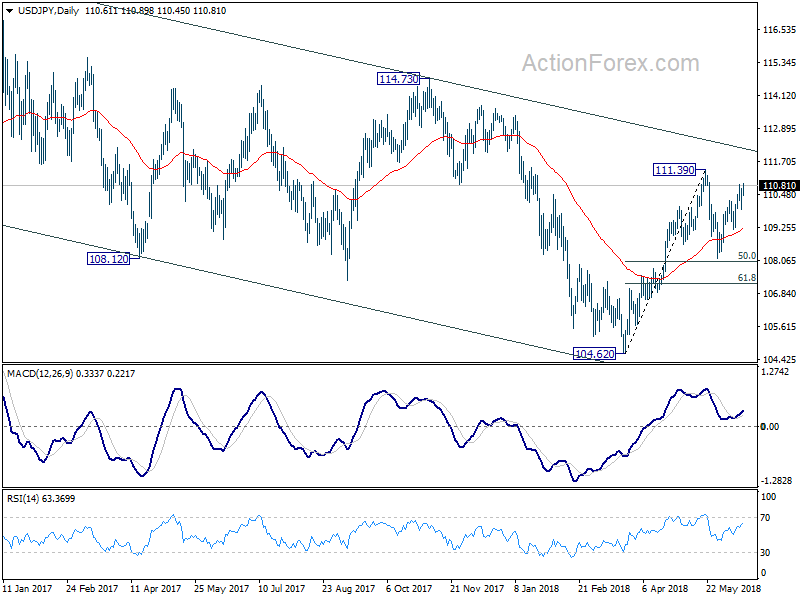

USD/JPY Daily Outlook

Daily Pivots: (S1) 110.13; (P) 110.41; (R1) 110.91; More...

Break of 110.84 suggests resumption of rebound from 108.10. Intraday bias is turned back to the upside for 111.39 high first. Break there will resume larger rebound from 104.62 and target 114.73 resistance. On the downside, though, break of 109.91 will turn bias to the downside and bring another fall towards 108.10 to extend the corrective pattern from 111.39.

In the bigger picture, at this point, we're slightly favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 will affirm this view and target 114.73 for confirmation. However, it should be noted that USD/JPY is bounded in medium term falling channel from 118.65 (2016 high). Sustained break of 61.8% retracement of 104.62 to 111.39 at 107.20 will likely resume the fall from 118.65 through 104.62 low.

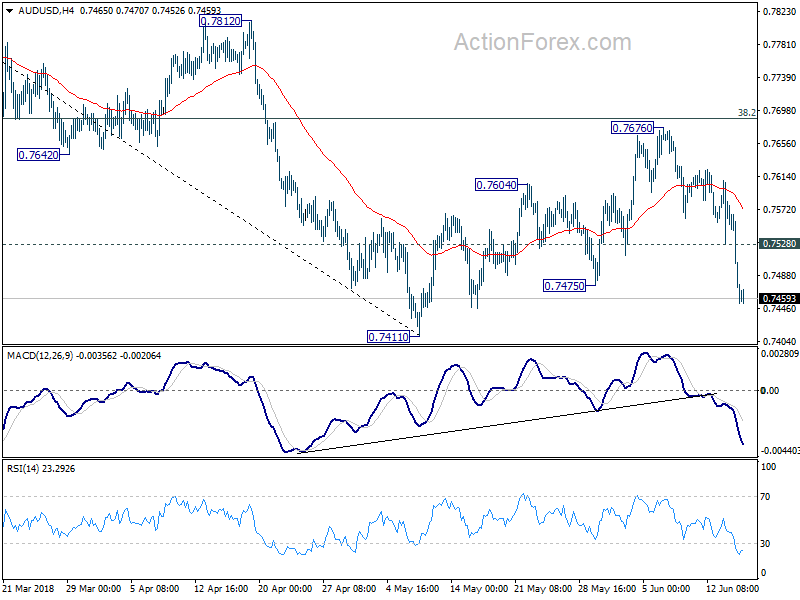

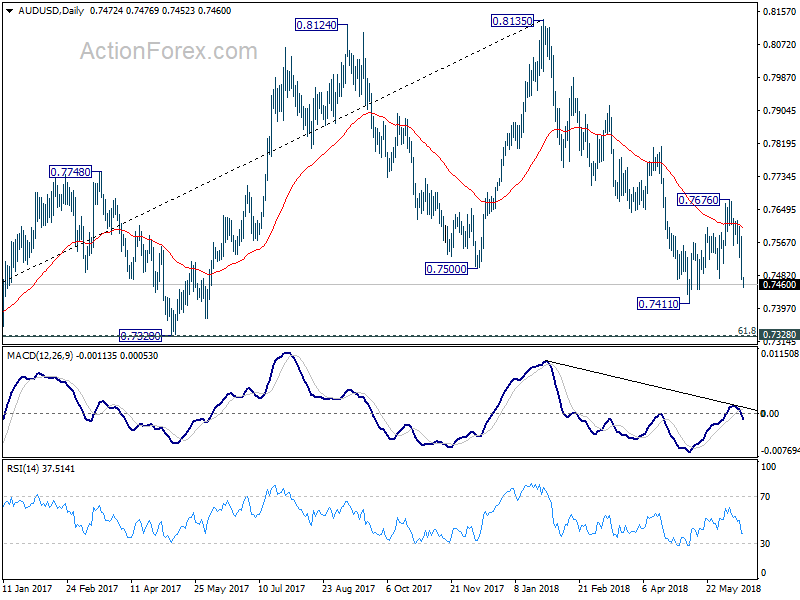

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7440; (P) 0.7512; (R1) 0.7549; More...

AUD/USD drops sharply to as low as 0.7452 so far and intraday bias remains on the downside. Corrective rise from 0.7411 should have completed at 0.7676 and larger decline from 0.8135 is resuming. Break of 0.7411 will confirm and target 0.7328 cluster support (61.8% retracement of 0.6826 to 0.8135 at 0.7326). On the upside, above 0.7528 minor resistance will delay the bearish case and bring more consolidations first.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. Prior break of 0.7500 key support suggests that such correction is completed at 0.8135. Deeper decline would be seen back to retest 0.6826 low. In case of another rise, we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption eventually.

USD/JPY Bounces at 61.8% Fib and Breaks Resistance Line

The USD/JPY bounced and reversed at the bottom of the uptrend channel as expected. Price is now ready to challenge and test the previous top.

The USD/JPY seems to be building a bullish channel within a wave C. A break above the previous top could see price move higher towards the -27.2% Fibonacci target.

The USD/JPY broke above the resistance trend line (dotted red) after bouncing at the Fibonacci levels of wave 4. Price could now be moving higher as part of a wave 5, which could become extended if price manages to break above the resistance trend line (orange) of the uptrend channel.