Sample Category Title

Crude Oil: Oil Trading Lower, Ahead Of Baker Hughes Weekly Rig Count Data

For the 24 hours to 23:00 GMT, Crude Oil rose 0.44% against the USD and closed at USD66.94 per barrel.

In the Asian session, at GMT0300, the pair is trading at 66.94, with oil trading marginally lower against the USD from yesterday’s close.

The pair is expected to find support at 66.48, and a fall through could take it to the next support level of 66.02. The pair is expected to find its first resistance at 67.28, and a rise through could take it to the next resistance level of 67.62.

Crude oil is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

ECB: Rate Delay Outweighs End Of APP

ECB announces APP to be scaled down in Q4 and finished by end year…but… ….Markets react more to unexpected ‘lower for longer' signal for ECB rates ECB concerned not to lead markets to expect they would tighten too soon/much Dovish rate signal to dominate markets... but it may not be as conclusive as it seems Inflation at target by 2020, suggesting a case for a more restrictive policy path

Policy rates to remain lower for longer

By signaling its intention to scale back its monthly bond buying to €15bn from October and fully end its Asset Purchase Scheme (APP) by the end of this year, The European Central Bank took an important initial step towards moving towards more normal settings for its monetary policy. However, financial markets paid much more attention to the unexpected indication by the ECB that its official interest rates will ‘remain at their present levels at least through the summer of 2019 ...'. This unexpectedly dovish forward guidance prompted a significant and speedy market reaction.

Together with a generally cautious outlook for the EMU economy from Mr Draghi, the effective commitment not to raise policy rates until autumn of next year at the earliest served to underpin the view that the ECB will only move very slowly away from the exceptional scale and range of support it is now providing to interest rate markets.

As markets had come to view the early announcement of the ECB's intentions in regard to the ending of its APP as a possible pointer to an earlier and faster move on interest rates, yesterday's more explicit guidance on the timing of future rate moves came as something of a shock.

Markets quickly moved to re‐price expectations in regard to the timing of the initial ECB rate hike from mid to end 2019 (implying it would be possibly implemented by a successor rather than Mr Draghi whose term as president ends in October 2019). Not surprisingly, this re‐assessment prompted a softening in Euro area market rates as traders pushed back their expectations in regard to the timing and speed of the path of future ECB tightening moves.

In tandem with the release of strong US retail sales and a pull‐back in forward guidance on policy from a generally upbeat Federal Reserve Wednesday, the apparently significant contrast in economic performance and policy prospects on either side of the Atlantic highlighted by the ECB's pronouncements also led to a material drop in the exchange rate of the Euro against the Dollar.

While the immediate market reaction is entirely rational, there is some risk it may go too far. In the very near term, market sentiment may be slow to alter but there are several aspects to yesterday's outcome that argue markets should guard against excessive complacency in regard to the future path of ECB policy.

Was the ECB too careful?

In assessing the pronouncements, it should be recognized that there are good reasons why the ECB would have wanted to avoid an excessively hawkish signal. The major risk facing the ECB at present is that it would tighten too early or aggressively (as was the case in 2008 and 2011) and be quickly forced to reverse course. Allied to this was the possibility that unduly hawkish comments could cause market rates to move prematurely leading to an excessive tightening in financial conditions that would weaken an already somewhat hesitant EMU growth trajectory of late.

The opening statement nods in the direction of such concerns by adding to its risk assessment that ‘Moreover, the risk of persistent heightened financial market volatility warrants monitoring'. In these circumstances, the key requirement was to signal an eventual tightening of policy but avoid any notable rise in market interest rates or in the Euro. That has clearly been achieved‐ possibly by a message that was perhaps dovish to an unintended degree?

A second consideration is that heightened uncertainty in relation to the strength and durability of the upswing in the Euro area argues for buying a material amount of time before taking more decisive policy steps towards a less accommodative stance. While Mr Draghi downplayed the significance of recent Italian developments at the press conference, he repeatedly noted that a ‘soft patch' in Euro area growth seen in the first quarter could last somewhat longer than initially envisaged. He also added that the latest ECB projections do not take account of trade measures not yet implemented but acknowledged any escalation in this area could be significantly negative in its impact.

The fact that the ECB has at least begun to set out the initial steps it will take to end its APP at a time when trade tensions and Italian difficulties have created significant uncertainty suggests there is an important element within the ECB'S Governing council that is pushing for a less accommodative policy stance. In current circumstances, it would have been relatively easy for the ECB to postpone its announcement on the ending of the APP possibly for several months. However, there is clearly a view that some signaling of a move towards the exit from easy policy is now needed.

However, it should also be emphasised that, as has been the case for some time, opinions around the ECB Governing council table likely differ materially on when and how fast policy should change. Mr Draghi noted on several occasions that today's decisions were ‘unanimous'. To achieve agreement, some element of compromise was clearly needed.

Interestingly, Mr Draghi also noted that various options for winding down the APP hadn't been discussed as significant work at committee level within the ECB had produced a widely shared view at the Governing council level. While it has little relevance for the near term policy outlook, the likelihood is that similar committee work is already underway at least in a preliminary fashion on various possible paths for policy rates through 2019 and beyond

How binding is the ECB's commitment?

A notable clarification from Mr Draghi was that the ECB's commitments in terms of future policy are ‘both ‘state and date dependent'. This was most clearly signaled in the opening press statement in relation to the ending of the APP which makes that action conditional on ‘incoming data confirming our medium‐term inflation outlook'.

The market reaction to the ECB pronouncements was heavily influenced by the apparent double bind of state and date commitments in relation to the forward guidance provided on key policy interest rates that ‘we (the ECB) expect them to remain at their present levels at least through the summer of 2019 and in any case for as long as necessary to ensure that the evolution of inflation remains aligned with our current expectations of a sustained adjustment path'.

The intention of this phrasing is clear. However, the commitment implied by the word ‘expect' may not be quite as watertight as the market assumes. Draghi added that there was a ‘desire to retain optionality' in relation to the ECB's guidance on future policy changes. He further noted when asked if the chosen wording ruled out an initial rate move in September 2019 that ‘the guidance was intended to give a time dimension but not a precise one'.

So, it would appear that the ECB wants to ensure that markets do not discount a rapid sequence of tightening moves. However, this later starting point should provide the Euro area with additional stimulus which, in turn, could argue for a faster eventual pace of rate increases than would otherwise be the case.

Projections suggest restrictive policy path

In the context of a generally dovish presentation by Mr Draghi, it is not surprising that new ECB projections received little attention. Significantly, a downgrade to the growth forecast for 2018 (largely reflecting the poorer Q1 outturn) did not spill over into downward revisions to 2019 or 2020 (in fact the upper end of the range for 2020 GDP was revised up marginally). Employment growth through each of the three years of the projections was also unchanged, underlining official expectations of a sustained and solid upswing in activity.

The most interesting aspect of the new projections was an upward revision to inflation forecasts. While the ECB press statement suggests this is ‘mainly reflecting higher oil prices', the detailed projections also show ‘core' inflation moving up to 1.6% in 2019 from 1.5% previously and, more importantly, to 1.9% in 2020 from 1.8%. With headline inflation at 1.7% through the projection period and core inflation at 1.9% in 2020 (while GDP growth remains above potential), this outlook would, in isolation, seem to point towards the requirement for a somewhat more restrictive policy path than the ECB signaled yesterday.

The sense of an environment in which price pressure are gradually building (albeit from a low base) is also evident in a notably more upbeat assessment in the opening press statement; ‘Domestic cost pressures are strengthening amid high levels of capacity utilization, tightening labour markets and rising wages. Uncertainty around the inflation outlook is receding. Looking ahead, underlying inflation is expected to pick up towards the end of the year and thereafter to increase gradually over the medium term'.

Dovish sentiment to prevail in near term

These conditions would seem to argue for a clearer path to a less accommodative policy than markets inferred from yesterday's pronouncements by Mr Draghi. If they materialize, they would suggest that the ECB might need to move somewhat earlier than implied or in larger steps later. Indeed, the additional stimulus likely to come from the markets re‐pricing of ECB expectations should boost activity and inflation further. In such circumstances the date and state dependency of yesterday's guidance could be tested.

However, these are issues for another day. For now, the apparent commitment not to raise rates until the end of the third quarter of 2019 at the earliest will act as significant restraints on euro area market interest rates and on the exchange rate of the Euro.

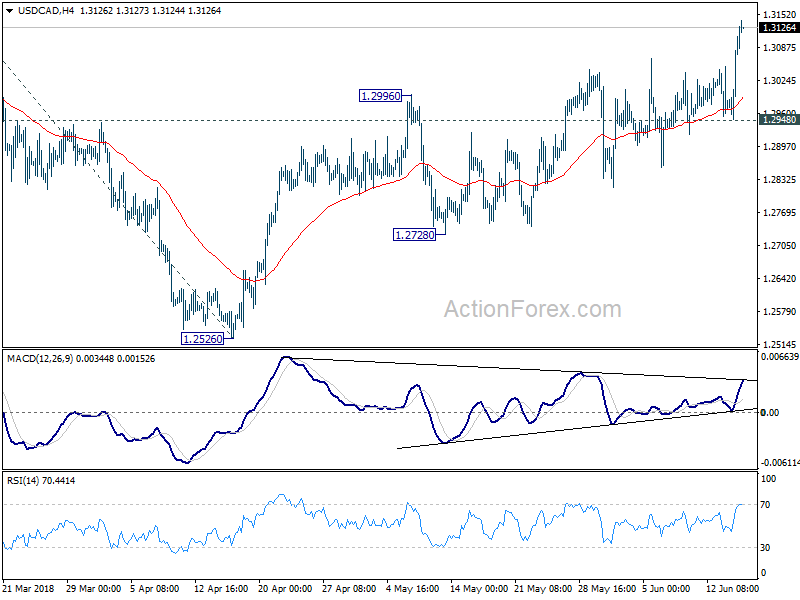

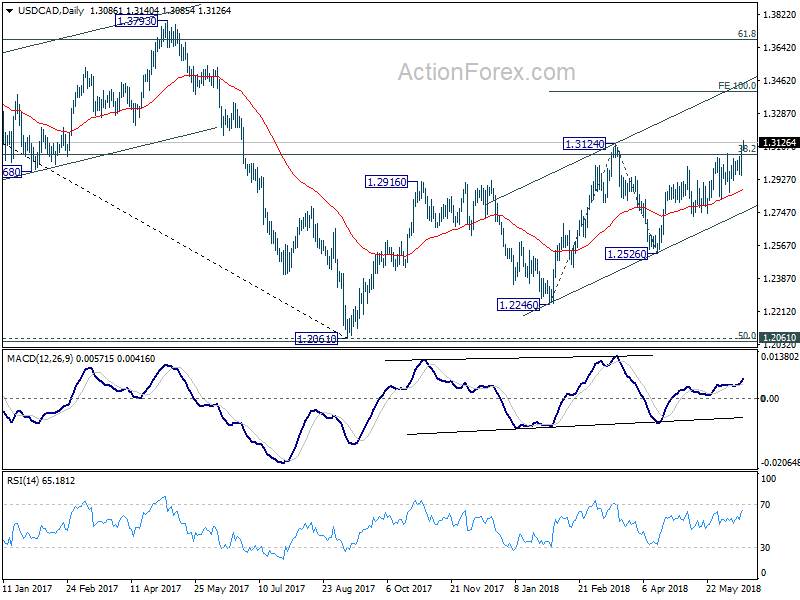

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2997; (P) 1.3054; (R1) 1.3163; More.....

USD/CAD surges to as high as 1.3140 so far today and breaches 1.3124 key resistance. The development suggests resumption of whole rebound from 1.2061. Intraday bias is now on the upside for 100% projection of 1.2246 to 1.3124 from 1.2526 at 1.3404 next. On the downside, break of 1.2948 support is needed to indicate short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, the current development affirms our bullish view. That is, firstly, rebound from 1.2061 is not finished yet. Secondly, the medium term decline from 1.4689 (2016 high) has completed and the trend is reversing. Sustained trading above 38.2% retracement of 1.4689 to 1.2061 at 1.3065 will confirm our view and target 61.8% retracement at 1.3685 and above. 1.3685. However, break of 1.2526 support will dampen this bullish view again. And, focus will be back on 1.2061 key support level, which is close to 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048.

Dollar Extending Post ECB Gains, Section 301 Tariffs Against China to be Formalized

Dollar is trading as the strongest one as partly helped by the post ECB selloff in Euro. In part, there were delayed reactions to the hawkish Fed announcement too, which indicates it will hike two more times this year. The greenback in extending it's strong, broad based gains in Asian session today, in particular, against commodity currencies. But whether Dollar could end the week as the strongest would depend on market reactions to announcement of Section 301 tariffs against China.

Technically, USD/CAD has breached a key resistance level at 1.3124 which affirms medium term bullishness. Development in other Dollar pairs are also suggesting up trend resumption. But more is needed to confirm. 1.1509 support in EUR/USD, 1.3203 support in GBP/USD, 1.0056 resistance in USD/CHF are the key levels to watch today.

Trump approved Section 301 tariffs on USD 50B of Chinese imports

It's reported that Trump has approved the Section 301 tariffs on USD 50B in Chinese imports and the formal announcement would be made today. That came after a 90-minute meeting with the core team of senior White House officials, national-security officials and senior representatives of the Treasury, Commerce Department, Trade Representative's Office. The initial proposal include around 1,300 lines of products targeting the "Made in China 2025" plan. But it's uncertain what changes would be made to the list after public hearing. Also, it's uncertain when the tariffs will come into effect.

China has pledged retaliation yesterday if the tariffs are enforced. Foreign Minister Wang Yi warned yesterday that China and the US faced a choice between cooperation and confrontation. Wand said "China chooses the first". But "of course, we have also made preparations to respond to the second kind of choice."

US agriculture associations cry #TradeNotTariffs

Agriculture Associations in the US turned to the Congress for help after their voices have fallen on Trump's deaf ears. The American Soybean Association (ASA), the National Corn Growers Association, National Association of Wheat Growers (NAWG), Association of Equipment Manufacturers (AEM) issued a joint appeal to the Congress with hashtag #TradeNotTariffs.

The urged the Congress to "convince the administration to halt tariffs and go back to the negotiating table." And, Under the hashtag #TradeNotTariffs, members of these organizations are also raising awareness on social media by sharing with the public what tariffs could mean for their livelihoods – and how severe that outlook could be.

This is an immediate response to the news that White House would announce the final list of tariffs on USD 50B in Chinese goods. Chinese has announced a retaliation list several months ago that include 25% tariffs on US soybeans. ASA described the Chinese retaliation as "devastating to growers of the number one US agricultural export." NAWG said "adding a 25 percent tariff on exports to China for US wheat is the last thing we need during some of the worst economic times in farm country."

NCGA warned farmers "cannot afford the immediate pain of retaliation nor the longer term erosion of long-standing market access and economic partnerships with some of our closest friends and allies." AEM also said "we strongly oppose a trade war with China because no one ever wins in these tit-for-tat dispute".

Here is the full release.

IMF warned of US fiscal and trade policies

IMF saw a positive picture of the US economy in a report released yesterday, but warned of fiscal and trade policy. IMF said that near-term outlook for the U.S. economy is one of strong growth and job creation. And, a slow but steady rise in wage and price inflation is expected as labor and product markets tighten. It projects US economy to grow 2.9% In 2018 and 2.7% in 2019 but slow sharply to 1.9% in 2020. Core PCE is projected to hit 2.0% in 2018 and accelerate to 2.3% in 2019 before slowing back to 2.2% in 2020.

Regarding fiscal policy, IMF warned that the combined effect of the administration's tax and spending policies will cause the federal government deficit to exceed 4.5% of GDP by 2019. And, such a procyclical fiscal policy will elevate the risks to the U.S. and global economy. The risks include higher public debt, a inflation surprise, international spillover, future recession and increased global imbalances. IMF said Fed will need to raise policy rates at a faster pace to achieve its dual mandate. And policymakers should be ready to accept some modest, temporary overshooting of its medium-term inflation goal

On trade, IMF warned that the measures to impose new tariffs or otherwise restrict import "are likely to move the globe further away from an open, fair and rules-based trade system, with adverse effects for both the U.S. economy and for trading partners". Risks include:

- Catalyzing a cycle of retaliatory responses from others, creating important uncertainties that are likely to discourage investment at home and abroad.

- Expanding the circumstances where countries choose to cite national security motivations to justify broad-based import restrictions. As such, this has the potential to undermine the rules-based global trading system.

- Interrupting global and regional supply chains in ways that are likely to be damaging to a range of countries, and to U.S. multinational companies, that are reliant on these supply chains.

- Impacting a range of countries, particularly some of the more vulnerable emerging and developing economies, through increased financial market or commodity price volatility associated with these trade actions.

Full report here.

Euro stays weak after ECB triggered selloff

Euro recovers mildly after yesterday's post ECB selloff. But for now, it's trading down against all other major currencies except Australian Dollar. ECB announced yesterday that the current EUR 30B per month asset purchase program will continue to run as planned till the end of September. Then, the monthly size will be tapered to EUR 15B, subject to incoming data. The program will then run till the end of December 2018 and end there. Market responded negatively to the forward guidance that interest rates will remain at their present levels at least through the summer of 2019

More in

- ECB to End QE in December, No Rate Hike At Least Until Summer 2019

- ECB: Making Plans to Dial Back Policy Accommodation

- ECB Review: End of APP But Stronger on Rate Guidance

- ECB Mario Draghi's introductory statement in press conference

BoJ stands pat as widely expected

BoJ left monetary policy unchanged today as widely expected. Under the yield curve control framework, short term policy rate is held at -0.1%. BoJ will also continue target to keep 10 year JGB yield at around 0%. Annual pace of JGB purchase is kept at around JPY 80T. Goushi Kataoka dissented again in a 8-1 vote. Kataoka pushed to "further strengthen monetary easing" so that "yields on JGBs with maturities of 10 years and longer would broadly be lowered further."

The description on the economy is largely unchanged. One exception is that CPI is now "in the range of 0.5-1.0%", comparing to April's description of moving around 1 percent. On the outlook, BoJ noted that the economy is "likely to continue its moderate expansion." Domestic demand will follow an uptrend while exports will continue the moderate increasing trend. Risks to the outlook include the following: the U.S. economic policies and their impact on global financial markets; developments in emerging and commodity-exporting economies; negotiations on the United Kingdom's exit from the European Union (EU) and their effects; and geopolitical risks.

Elsewhere

New Zealand Business NZ manufacturing PMI dropped to 54.5 in May, down from 59.1. Eurozone will release trade balance, labor costs and CPI final in European session. Later in the day, Canada will release international securities transactions and manufacturing sales. US will release Empire State manufacturing index, industrial production and U of Michigan sentiment.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2997; (P) 1.3054; (R1) 1.3163; More.....

USD/CAD surges to as high as 1.3140 so far today and breaches 1.3124 key resistance. The development suggests resumption of whole rebound from 1.2061. Intraday bias is now on the upside for 100% projection of 1.2246 to 1.3124 from 1.2526 at 1.3404 next. On the downside, break of 1.2948 support is needed to indicate short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, the current development affirms our bullish view. That is, firstly, rebound from 1.2061 is not finished yet. Secondly, the medium term decline from 1.4689 (2016 high) has completed and the trend is reversing. Sustained trading above 38.2% retracement of 1.4689 to 1.2061 at 1.3065 will confirm our view and target 61.8% retracement at 1.3685 and above. 1.3685. However, break of 1.2526 support will dampen this bullish view again. And, focus will be back on 1.2061 key support level, which is close to 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | BusinessNZ Manufacturing PMI May | 54.5 | 58.9 | 59.1 | |

| 2:41 | JPY | BoJ Rate Decision | -0.10% | -0.10% | -0.10% | |

| 9:00 | EUR | Eurozone Trade Balance (EUR)Apr | 20.2B | 21.2B | ||

| 9:00 | EUR | Eurozone CPI M/M May | 0.30% | 0.30% | ||

| 9:00 | EUR | Eurozone CPI Y/Y May F | 1.20% | 1.20% | ||

| 9:00 | EUR | Eurozone CPI Core Y/Y May F | 1.10% | 1.10% | ||

| 9:00 | EUR | Eurozone Labour Costs Y/Y Q1 | 1.90% | 1.50% | ||

| 12:30 | CAD | International Securities Transactions (CAD) Apr | 6.15B | |||

| 12:30 | CAD | Manufacturing Sales M/M Apr | 0.20% | 1.40% | ||

| 12:30 | USD | Empire State Manufacturing Jun | 19.75 | 20.1 | ||

| 13:15 | USD | Industrial Production M/M May | 0.30% | 0.70% | ||

| 13:15 | USD | Capacity Utilization May | 78.10% | 78.00% | ||

| 14:00 | USD | U. of Mich. Sentiment Jun P | 98.5 | 98 |

BoJ stands pat as widely expected

BoJ left monetary policy unchanged today as widely expected. Under the yield curve control framework, short term policy rate is held at -0.1%. BoJ will also continue target to keep 10 year JGB yield at around 0%. Annual pace of JGB purchase is kept at around JPY 80T. Goushi Kataoka dissented again in a 8-1 vote. Kataoka pushed to "further strengthen monetary easing" so that "yields on JGBs with maturities of 10 years and longer would broadly be lowered further."

The description on the economy is largely unchanged. One exception is that CPI is now "in the range of 0.5-1.0%", comparing to April's description of moving around 1 percent. On the outlook, BoJ noted that the economy is "likely to continue its moderate expansion." Domestic demand will follow an uptrend while exports will continue the moderate increasing trend. Risks to the outlook include the following: the U.S. economic policies and their impact on global financial markets; developments in emerging and commodity-exporting economies; negotiations on the United Kingdom's exit from the European Union (EU) and their effects; and geopolitical risks.

Full statement here.

IMF warned of US fiscal and trade policies

IMF saw a positive picture of the US economy in a report released yesterday, but warned of fiscal and trade policy. IMF said that near-term outlook for the U.S. economy is one of strong growth and job creation. And, a slow but steady rise in wage and price inflation is expected as labor and product markets tighten. It projects US economy to grow 2.9% In 2018 and 2.7% in 2019 but slow sharply to 1.9% in 2020. Core PCE is projected to hit 2.0% in 2018 and accelerate to 2.3% in 2019 before slowing back to 2.2% in 2020.

Regarding fiscal policy, IMF warned that the combined effect of the administration's tax and spending policies will cause the federal government deficit to exceed 4.5% of GDP by 2019. And, such a procyclical fiscal policy will elevate the risks to the U.S. and global economy. The risks include higher public debt, a inflation surprise, international spillover, future recession and increased global imbalances. IMF said Fed will need to raise policy rates at a faster pace to achieve its dual mandate. And policymakers should be ready to accept some modest, temporary overshooting of its medium-term inflation goal

On trade, IMF warned that the measures to impose new tariffs or otherwise restrict import "are likely to move the globe further away from an open, fair and rules-based trade system, with adverse effects for both the U.S. economy and for trading partners". Risks include:

- Catalyzing a cycle of retaliatory responses from others, creating important uncertainties that are likely to discourage investment at home and abroad.

- Expanding the circumstances where countries choose to cite national security motivations to justify broad-based import restrictions. As such, this has the potential to undermine the rules-based global trading system.

- Interrupting global and regional supply chains in ways that are likely to be damaging to a range of countries, and to U.S. multinational companies, that are reliant on these supply chains.

- Impacting a range of countries, particularly some of the more vulnerable emerging and developing economies, through increased financial market or commodity price volatility associated with these trade actions.

Full report here.

US agriculture associations cry #TradeNotTariffs

Agriculture associations in the US turned to the Congress for help after their voices have fallen on Trump's deaf ears. The American Soybean Association (ASA), the National Corn Growers Association, National Association of Wheat Growers (NAWG), Association of Equipment Manufacturers (AEM) issued a joint appeal to the Congress with hashtag #TradeNotTariffs.

The urged the Congress to "convince the administration to halt tariffs and go back to the negotiating table." And, Under the hashtag #TradeNotTariffs, members of these organizations are also raising awareness on social media by sharing with the public what tariffs could mean for their livelihoods – and how severe that outlook could be.

This is an immediate response to the news that White House would announce the final list of tariffs on USD 50B in Chinese goods. Chinese has announced a retaliation list several months ago that include 25% tariffs on US soybeans. ASA described the Chinese retaliation as "devastating to growers of the number one US agricultural export." NAWG said "adding a 25 percent tariff on exports to China for US wheat is the last thing we need during some of the worst economic times in farm country."

NCGA warned farmers "cannot afford the immediate pain of retaliation nor the longer term erosion of long-standing market access and economic partnerships with some of our closest friends and allies." AEM also said "we strongly oppose a trade war with China because no one ever wins in these tit-for-tat dispute".

Here is the full release.

Market Morning Briefing: Gold Has Moved Up Above 1300

STOCKS

Dow (25175.31, -0.10%) has not been able to break above 25500 and instead has been coming off from there gradually to test 25000 in the next few sessions. This is contrary to our expectation of arise towards 25750 and higher. Now daily candle support near 25000 is important and a bounce from there is preferred which could again take the index back towards 25500. Near term is bearish towards 25000.

Dax (13107.10, +1.68%) has moved up sharply after the ECB meeting yesterday and broken above our mentioned resistance near 13100. It is important to watch price action here. A break above 13100 if sustains could take it higher towards 13400 and higher in the coming sessions next week. Else a fall back to levels below 13100 would be indicative of some bearishness next week.

Nikkei (22827.77, +0.39%) has neither seen a sharp rise above 22800 nor is it falling off to levels below 22800. There seems to be some sideways range-trade in the 23000-22800 region for now with small movements. Overall a dip in Dollar Yen could restrict further upside for Nikkei in the near term.

Shanghai (3023.79, -0.67%) is coming off towards 3000 and looks weak just now. It would be important to see if the index breaks below 3000 eventually. Near to medium term looks bearish while below 3050.

Nifty (10808.05, -0.45%) came down for the second session yesterday after testing resistance at 10900. While 10900 holds, the index looks bearish towards 10700-10650 in the medium term.

COMMODITIES

Brent (75.84) and WTI (66.94) have dipped a bit and could remain stable for now. Brent came off from 77 yesterday and may test lower levels of 75 in the next 1-2 sessions. WTI on the other hand has some scope of bullishness towards 68.

Gold (1302.10) has moved up above 1300. While the rise continues, Gold is likely to move up towards 1320-1325 in the near term.

Copper (3.2094) has bounced from 3.20 in line with our expectation and could move back towards 3.2250 and higher in the coming sessions.

FOREX

Euro (1.1564): The ECB's policy stance turned out to be a mix of hawkishness (quantitative easing ending by Dec '18) and dovishness (rates remaining constant till 2019 summers). The hawkish part seemed already factored in by the markets, while the dovishness came as a surprise, thereby leading to a drastic weakening of the Euro (against our expectation). The Euro saw its biggest intra-day fall since Dec '16, as it fell from 1.185 towards a low near 1.156.

On technical charts, it is testing crucial support on 3 day and weekly candle charts near 1.155. However there is lower support near 1.145 (on daily line chart) which could still be tested. While above 1.145, we can expect Euro to rise back towards 1.160-1.165 next week. A break below 1.145-1.140 might open up levels near 1.12.

Dollar index (94.95): Along with the ECB's weakening effect on Euro, the Dollar Index rose also due to the positive US Retail Sales data for May '18 (beating expectations). It is now testing crucial resistance on weekly candles near 95 and has higher resistance near 96 on the 3 day line chart. A breach of 96 could make Dollar Index bullish towards 97.5.

Dollar Yen (110.74): Dollar has strengthened against the Yen as well and is currently testing resistance on the daily line chart near current levels. There is higher resistance between 111 and 112 on 3 day and weekly line chart. We have been preferring for this resistance to hold. The Bank of Japan has maintained status quo in its policy announcement but has also offered a bleaker view on inflation. This could be negative for Yen strength. We will have to wait and watch if this weakens the Yen above 111-112.

Euro Yen (128.06): Given the Euro's fall, Euro Yen dropped to lows near 128 (against our expectation). It is still near horizontal support on weekly line chart and might rise from here if Euro respects support near 1.155 and Dollar Yen rises closer to 111-112.

Pound (1.3252): As expected, Pound has moved lower towards 1.32 (having seen a low near 1.325 already). Support near 1.315 on daily candles could be a possible downside target for next week.

Dollar Rupee (67.625): Dollar Rupee could keep ranging between 67.5-67.8 today. Euro's drastic weakening could have a negative impact on Rupee strength.

INTEREST RATES

After the US Fed's hawkishness day before yesterday, the ECB came out with a mixed policy. On the hawkish side, it indicated that net asset purchases woud be halved to 15 billion Euros from Oct '18 to Dec '18 and after Dec '18, they would be completely stopped. However the dovish bit of the policy statement overpowered the hawkish bit – key interest rates are to remain constant till atleast the summers of 2019. This has led to a fall in bond yields across Europe and US yields have dipped a bit. The German 10 Year yield has dipped to 0.43% from levels near 0.51% and could fall further towards support near 0.3% on medium term chart.

Moreover US Retail Sales data also came out positive. The expectation of a 0.4% m-o-m increase was comfortably surpassed as Retail Sales grew by 0.8% in May '18.

Earlier, the US Fed had hiked rates by 25 bps. The language in the policy statement was clearly more hawkish than previous statements - reflected in the fact that the phrase about keeping rates low to boost the economy was dropped. The likelihood of 2 more rate hikes this year has increased beyond 50% for the first time this year. However the impact of this hawkishness hasn't yet translated into a rise past 3% for the 10 Year yield.

Current US yields: US 10 year (2.93%), 30 Year (3.05%), 5 Year (2.80%), 2 Year (2.56%)

The Bank of Japan has maintained status quo in its policy statement few minutes back but has given a bleaker view on inflation. This could lead to a fall in Japanese bond yields.

Trump approved Section 301 tariffs on USD 50B of Chinese imports

It's reported that Trump has approved the Section 301 tariffs on USD 50B in Chinese imports and the formal announcement would be made today. That came after a 90-minute meeting with the core team of senior White House officials, national-security officials and senior representatives of the Treasury, Commerce Department, Trade Representative's Office. The initial proposal include around 1,300 lines of products targeting the "Made in China 2025" plan. But it's uncertain what changes would be made to the list after public hearing. Also, it's uncertain when the tariffs will come into effect.

China has pledged retaliation yesterday if the tariffs are enforced. Foreign Minister Wang Yi warned yesterday that China and the US faced a choice between cooperation and confrontation. Wand said "China chooses the first". But "of course, we have also made preparations to respond to the second kind of choice."

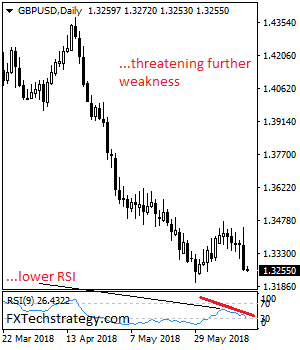

GBPUSD – Closes Lower On Price Sell Off

GBPUSD - The pair faces further weakness as it closed lower on sell off on Thursday. Support lies at the 1.3200 level where a break will turn attention to the 1.3150 level. Further down, support lies at the 1.3100 level. Below here will set the stage for more weakness towards the 1.3050 level. Its daily RSI remains biased to the downside suggesting more declines. Conversely, resistance stands at the 1.3300 levels with a turn above here allowing more strength to build up towards the 1.3350 level. Further out, resistance resides at the 1.3400 level followed by the 1.3450 level. On the whole, GBPUSD remains biased to downside pressure on trend resumption.