Sample Category Title

ECB Mario Draghi’s introductory statement in press conference

One important point to note in the introductory statement is the revision in economic projections. ECB now projects annual GDP growth to be at 2.1% in 2018, that's notable downward revision from March projection of 2.4%. For 2019 and 2020, GDP projections were kept unchanged at 1.9% and 1.7% respectively. On the other hand, HICP inflation is projected to be 1.7% in 2018, 2019 and 2020. That's notably revised up from March projection of 1.4% in 2018, 1.4% in 2019 and 1.7% in 2020.

Below is the statement.

Mario Draghi, President of the ECB,

Luis de Guindos, Vice-President of the ECB,

Riga, 14 June 2018

INTRODUCTORY STATEMENT

Ladies and gentlemen, the Vice-President and I are very pleased to welcome you to our press conference. I would like to thank Deputy Governor Razmusa for her kind hospitality and express our special gratitude to her staff for the excellent organisation of today's meeting of the Governing Council. We will now report on the outcome of our meeting.

Since the start of our asset purchase programme (APP) in January 2015, the Governing Council has made net asset purchases under the APP conditional on the extent of progress towards a sustained adjustment in the path of inflation to levels below, but close to, 2% in the medium term. Today, the Governing Council undertook a careful review of the progress made, also taking into account the latest Eurosystem staff macroeconomic projections, measures of price and wage pressures, and uncertainties surrounding the inflation outlook.

As a result of this assessment, the Governing Council concluded that progress towards a sustained adjustment in inflation has been substantial so far. With longer-term inflation expectations well anchored, the underlying strength of the euro area economy and the continuing ample degree of monetary accommodation provide grounds to be confident that the sustained convergence of inflation towards our aim will continue in the period ahead, and will be maintained even after a gradual winding-down of our net asset purchases.

Accordingly, the Governing Council today made the following decisions:

First, as regards non-standard monetary policy measures, we will continue to make net purchases under the APP at the current monthly pace of €30 billion until the end of September 2018. We anticipate that, after September 2018, subject to incoming data confirming our medium-term inflation outlook, we will reduce the monthly pace of the net asset purchases to €15 billion until the end of December 2018 and then end net purchases.

Second, we intend to maintain our policy of reinvesting the principal payments from maturing securities purchased under the APP for an extended period of time after the end of our net asset purchases, and in any case for as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation.

Third, we decided to keep the key ECB interest rates unchanged and we expect them to remain at their present levels at least through the summer of 2019 and in any case for as long as necessary to ensure that the evolution of inflation remains aligned with our current expectations of a sustained adjustment path.

Today's monetary policy decisions maintain the current ample degree of monetary accommodation that will ensure the continued sustained convergence of inflation towards levels that are below, but close to, 2% over the medium term. Significant monetary policy stimulus is still needed to support the further build-up of domestic price pressures and headline inflation developments over the medium term. This support will continue to be provided by the net asset purchases until the end of the year, by the sizeable stock of acquired assets and the associated reinvestments, and by our enhanced forward guidance on the key ECB interest rates. In any event, the Governing Council stands ready to adjust all of its instruments as appropriate to ensure that inflation continues to move towards the Governing Council's inflation aim in a sustained manner.

Let me now explain our assessment in greater detail, starting with the economic analysis. Quarterly real GDP growth moderated to 0.4% in the first quarter of 2018, following growth of 0.7% in the previous quarters. This moderation reflects a pull-back from the very high levels of growth in 2017, compounded by an increase in uncertainty and some temporary and supply-side factors at both the domestic and the global level, as well as weaker impetus from external trade. The latest economic indicators and survey results are weaker, but remain consistent with ongoing solid and broad-based economic growth. Our monetary policy measures, which have facilitated the deleveraging process, continue to underpin domestic demand. Private consumption is supported by ongoing employment gains, which, in turn, partly reflect past labour market reforms, and by growing household wealth. Business investment is fostered by the favourable financing conditions, rising corporate profitability and solid demand. Housing investment remains robust. In addition, the broad-based expansion in global demand is expected to continue, thus providing impetus to euro area exports.

This assessment is broadly reflected in the June 2018 Eurosystem staff macroeconomic projections for the euro area. These projections foresee annual real GDP increasing by 2.1% in 2018, 1.9% in 2019 and 1.7% in 2020. Compared with the March 2018 ECB staff macroeconomic projections, the outlook for real GDP growth has been revised down for 2018 and remains unchanged for 2019 and 2020.

The risks surrounding the euro area growth outlook remain broadly balanced. Nevertheless, uncertainties related to global factors, including the threat of increased protectionism, have become more prominent. Moreover, the risk of persistent heightened financial market volatility warrants monitoring.

According to Eurostat's flash estimate, euro area annual HICP inflation increased to 1.9% in May 2018, from 1.2% in April. This reflected higher contributions from energy, food and services price inflation. On the basis of current futures prices for oil, annual rates of headline inflation are likely to hover around the current level for the remainder of the year. While measures of underlying inflation remain generally muted, they have been increasing from earlier lows. Domestic cost pressures are strengthening amid high levels of capacity utilisation, tightening labour markets and rising wages. Uncertainty around the inflation outlook is receding. Looking ahead, underlying inflation is expected to pick up towards the end of the year and thereafter to increase gradually over the medium term, supported by our monetary policy measures, the continuing economic expansion, the corresponding absorption of economic slack and rising wage growth.

This assessment is also broadly reflected in the June 2018 Eurosystem staff macroeconomic projections for the euro area, which foresee annual HICP inflation at 1.7% in 2018, 2019 and 2020. Compared with the March 2018 ECB staff macroeconomic projections, the outlook for headline HICP inflation has been revised up notably for 2018 and 2019, mainly reflecting higher oil prices.

Turning to the monetary analysis, broad money (M3) growth stood at 3.9% in April 2018, after 3.7% in March and 4.3% in February. While the slower momentum in M3 dynamics over recent months mainly reflects the reduction in the monthly net asset purchases since the beginning of the year, M3 growth continues to be supported by the impact of the ECB's monetary policy measures and the low opportunity cost of holding the most liquid deposits. Accordingly, the narrow monetary aggregate M1 remained the main contributor to broad money growth, although its annual growth rate has receded in recent months from the high rates previously observed.

The recovery in the growth of loans to the private sector observed since the beginning of 2014 is proceeding. The annual growth rate of loans to non-financial corporations stood at 3.3% in April 2018, unchanged from the previous month, and the annual growth rate of loans to households also remained stable, at 2.9%.

The pass-through of the monetary policy measures put in place since June 2014 continues to significantly support borrowing conditions for firms and households and credit flows across the euro area. This is also reflected in the results of the latest Survey on the Access to Finance of Enterprises in the euro area, which indicates that small and medium-sized enterprises in particular benefited from improved access to financing.

To sum up, a cross-check of the outcome of the economic analysis with the signals coming from the monetary analysis confirmed that today's monetary policy decisions will ensure the ample degree of monetary accommodation necessary for the continued sustained convergence of inflation towards levels that are below, but close to, 2% over the medium term.

In order to reap the full benefits from our monetary policy measures, other policy areas must contribute more decisively to raising the longer-term growth potential and reducing vulnerabilities. The implementation of structural reforms in euro area countries needs to be substantially stepped up to increase resilience, reduce structural unemployment and boost euro area productivity and growth potential. Regarding fiscal policies, the ongoing broad-based expansion calls for rebuilding fiscal buffers. This is particularly important in countries where government debt remains high. All countries would benefit from intensifying efforts towards achieving a more growth-friendly composition of public finances. A full, transparent and consistent implementation of the Stability and Growth Pact and of the macroeconomic imbalance procedure over time and across countries remains essential to increase the resilience of the euro area economy. Improving the functioning of Economic and Monetary Union remains a priority. The Governing Council urges specific and decisive steps to complete the banking union and the capital markets union.

We are now at your disposal for questions.

US retail sales and jobless claims beat expectations

Initial jobless claims dropped -4k to 28k in the week ended June 9, slightly better than expectation of 223k. Four-week moving average of initial claims dropped -1.25k to 224.25k. Continuing claims dropped -49k to 1.697m in the week ended June 2, lowest since December 1, 1973. Four-week moving average of continuing claims dropped -3.75k to 1.726m, lowest since December 8, 1973.

Headline retail sales rose 0.8% in May versus expectation of 0.4% mom. Ex-auto sales rose 0.9% versus expectation of 0.3%. Import price rose 0.6% mom in May versus expectation of 0.5% mom.

Also released, new housing price index rose 0.0% mom in April versus expectation of 0.2% mom.

Canadian dollar steady ahead of U.S retail sales

The Canadian dollar is showing little movement in the Thursday session. Currently, USD/CAD is trading at 1.2978, down 0.04% on the day. On the release front, Canada releases the New Housing Price Index, which is expected to rise to 0.2%. In the U.S, consumer spending is expected to improve in May, with Retail Sales expected to rise to 0.4% and Core Retail Sales predicted to rise to 0.5%. Unemployment Claims is expected to tick up to 223 thousand. On Friday, the US publishes manufacturing and consumer confidence reports.

The markets had priced in a rate hike from the Federal Reserve on Wednesday, and the Fed didn’t disappoint. The central bank raised interest rates by a quarter-point, to a range between 1.75 percent and 2.00 percent. Fed Chair Jerome Powell sounded hawkish in his press conference, saying that the economy was performing well and that “overall outlook for growth remains favorable”. This message echoed the rate statement, in which policymakers said that “economic activity has been rising at a solid rate”, pointing to stronger consumer spending and business investment. What was may have been the most notable development was that the Fed rate projections were revised upwards, predicting two additional rate hikes in 2018, for a total of four hikes. Until now, the Fed had projected three rate hikes this year. This represents a nod to the strength of the U.S economy and could boost the dollar against its rivals.

Trade negotiators on both sides of the border could use a tip or two from soccer officials, as the joint bid from the U.S, Canada and Mexico won the right to host the 2026 World Cup. Such cooperation is only wishful thinking on the trade front, as the three countries remained deadlocked over the NAFTA agreement, notably over the U.S demand to increase the U.S content of cars produced in Canada or Mexico. A new headache for negotiators could be the Mexican national elections on August 1, with a leftist candidate, Andrés Manuel López Obrador, holding a comfortable lead at the polls. If Obrador wins the election, a new NAFTA deal could prove even more elusive, which could be bad news for the Canadian dollar.

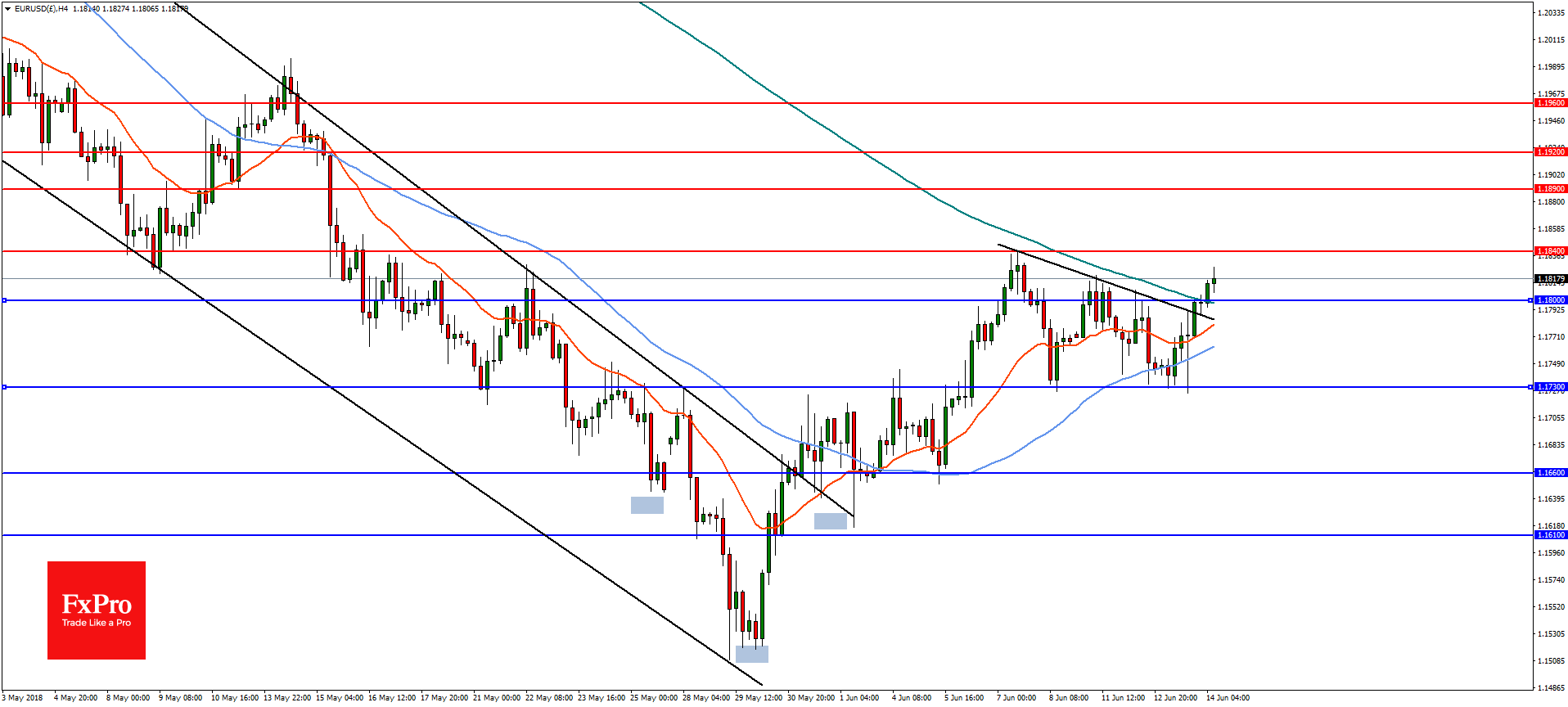

Euro dives after ECB as markets unhappy with rate path

Euro suffers steep selling after ECB's announcement. ECB did deliver an the decision on asset purchase program. That is, tapering it for three months after September and end it after December. But the markets seem to be rather unhappy with it. The decision to taper, instead of ending it right after September could be a factor.

The more important one could be this part of the statement. "The Governing Council expects the key ECB interest rates to remain at their present levels at least through the summer of 2019 and in any case for as long as necessary to ensure that the evolution of inflation remains aligned with the current expectations of a sustained adjustment path."

It suggests that for now, ECB is not even eyeing mid 2019 as the timing for the first rate hike.

Focus on EUR/USD is now back on 1.1713 minor support. Break will bring retest of 1.1509 low next. Euro now looks to Mario Draghi's press conference for rescue. Based on our experience on Draghi, he usually delivers something more cautious then the statements.

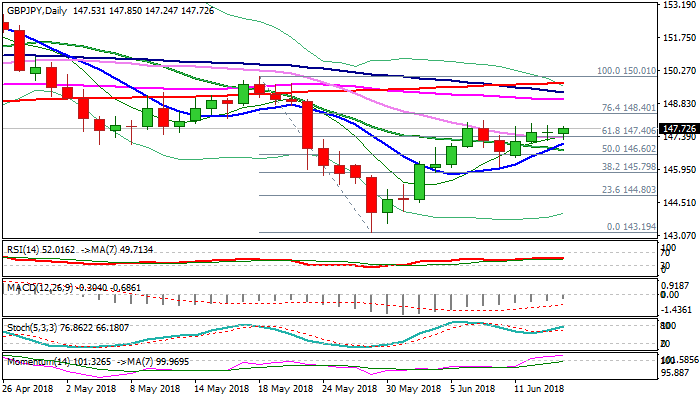

GBPJPY Outlook – Near-Term Outlook Improves Following Rally On Upbeat UK Data, But The Price Remains Within Three-Day Congestion

The cross moved higher around 60 pips as pound got boosted from stronger than expected UK retail sales (May 1.3% vs 0.5% f/c and Apr upward-revised figure at 1.8%).

Fresh strength pressures tops of 147.98/12 congestion which extends into third day and turns near-term focus higher after yesterday’s Doji signaled indecision.

Bullish bias is supported by 10/20SMA / daily Tenkan/Kijun-sen bull crosses and strengthening momentum, as daily cloud which lies above and twists next Tuesday, could attract fresh advance.

Bullish scenario requires close above 148.11 / 27 (07 June high / weekly cloud top) for confirmation and signal of bullish continuation towards the base of thinning daily cloud (149.41).

Conversely, fall below 147.12 (congestion low, reinforced by rising 10SMA) would generate initial negative signal, which requires confirmation on break below daily Kijun-sen (146.60).

Res: 147.98, 148.11, 148.27, 148.40

Sup: 147.25, 147.11, 146.60, 146.23

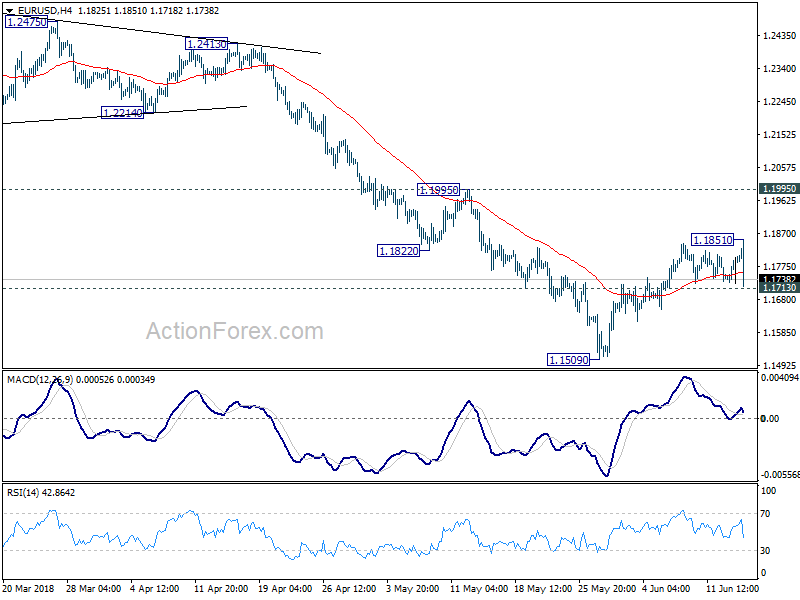

Forex Analysis: EURUSD And Gold Analysis

The focus for today will be the ECB monetary policy announcement where baseline interest rates are expected to be held steady but the market will look for any signal regarding the quantitative easing (QE) program. Recent comments Peter Praet, a member of the Executive Board of the ECB, gave a strong hint that the June meeting would see the ECB signal the end the QE. However, recent economic data has shown that Eurozone growth has slowed since the beginning of this year and there may be some reluctance to commit to ending QE. Without a clear signal to end QE, the monitory policy differential between the ECB and Fed could be bearish for the Euro and trigger another leg to the downside.

EURUSD

On the 4-hourly chart, EURUSD has formed an inverted head and shoulders pattern with a measured target of 1.1920. Provided the pair remains above support at 1.1800, upside continuation is likely with resistance near the 38.2% retracement of the April highs at 1.1840 and then 1.1890. A reversal below 1.1800 would negate the bullish outlook and the pair could continue to the downside with support at 1.1730.

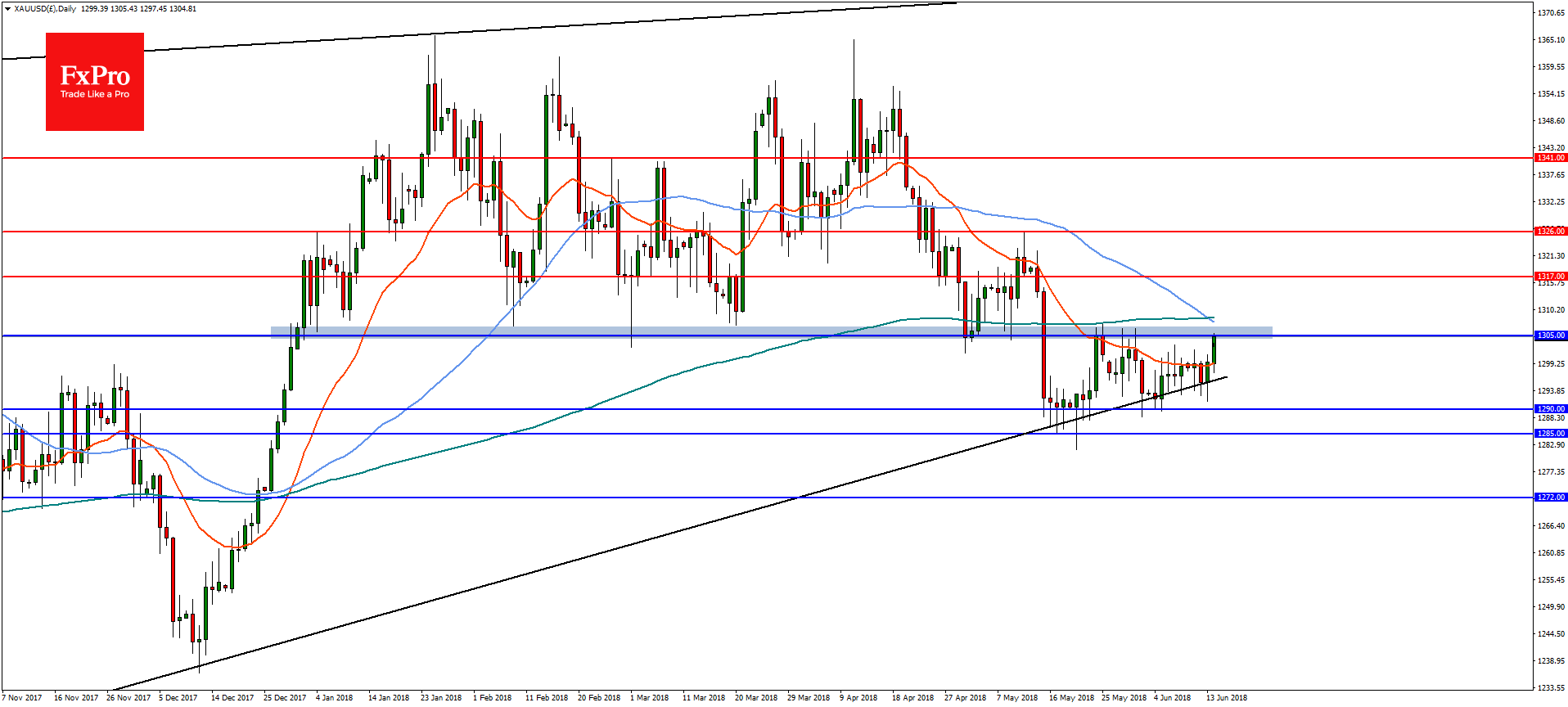

GOLD

After the FOMC announcement yesterday, Gold has been strengthening and is now trading at a critical level ahead of the ECB. In the daily timeframe, Gold is trading the major horizontal resistance near 1305. A decisive break of 1305 is needed to open the way to a move towards resistance at 1317 and then 1326. On the flip side, a bearish reversal and break of trend line at 1290 would see a downside continuation to supports at 1285 and then the 38% retracement from the Oct 2016 lows at 1272.

Euro Bulls Run Higher Ahead Of ECB Rate Decision, BoJ Policy Meeting Eyed Too

Here are the latest developments in global markets:

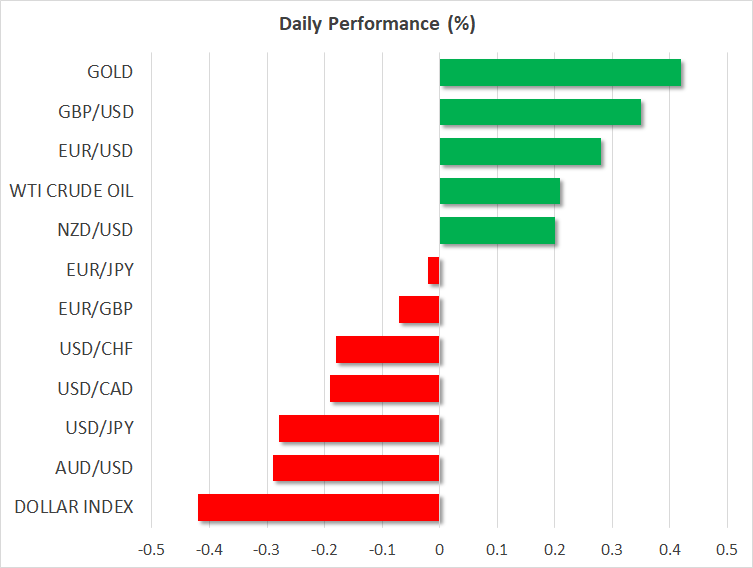

FOREX: The focus turns to the European Central Bank (ECB) interest rate decision and press conference a bit later on Thursday, with euro/dollar picking up by 0.31% before the meeting. The US dollar dived back from 3-week highs against the Japanese yen on Wednesday, erasing previous gains made after the Fed signaled two more rate hikes this year, bringing the total number of rises to four from the three previously thought. The FOMC raised the Fed funds rate by 25 bps to a range of 1.75%-2.00% as was widely expected. The pair, however, lost ground immediately after the FOMC announcement, with the sell-off continuing today to 109.96 (-0.33%) on the back of a stronger euro and pound as well as rising trade risks. Also, the US dollar index dipped by 0.44% to 93.30. Pound/dollar jumped considerably by 0.40% to a 5-day high of 1.3445 after UK retail sales climbed for a second consecutive month, on a monthly basis. The retail sales industry increased by 1.3% m/m in May versus 1.6% m/m in the preceding month, beating expectations, while year-on-year the index advanced by 3.9% from 1.4% before. Turning to the antipodean currencies, aussie/dollar slipped after job creation in Australia and industrial production in China fell short of expectations during the Asian session. The Australian unemployment rate, though, ticked surprisingly lower. The pair fell by 0.25% to 0.7556, while kiwi/dollar rose by 0.16% to 0.7034. Dollar/loonie slid by 0.19% to 1.2955.

STOCKS: Stocks retreated in global markets on Thursday. European equities were in a sea of red at 1030 GMT with the pan-European STOXX 600 and the blue-chip Euro STOXX 50 being down by 0.49% and 0.32% respectively. The German DAX 30 fell by 0.30%, the British FTSE 100 decreased by 0.57% to the lowest in more than two weeks, while the French CAC 40 dived by 0.24%. The Italian FTSE MIB declined by 0.40%. In the US, futures tracking stock indices were on the back foot as well, pointing to a negative open.

COMMODITIES: Oil prices were mixed today as investors waited for the OPEC policy meeting next week. West Texas Intermediate (WTI) crude gained 0.18% to $66.76 per barrel, while London-based Brent declined by 0.20% to $76.59 per barrel. In precious metals, gold was up by 0.45%, trading close to $1,305 per ounce level, printing the largest increase in more than a week. Sources so far support that OPEC members will increase oil output, a proposal made by Saudi Arabia and Russia. However, the meeting could take an interesting turn since Iran, Iraq, and Venezuela oppose the idea.

Day ahead: European Central Bank and Bank of Japan next to decide on interest rates

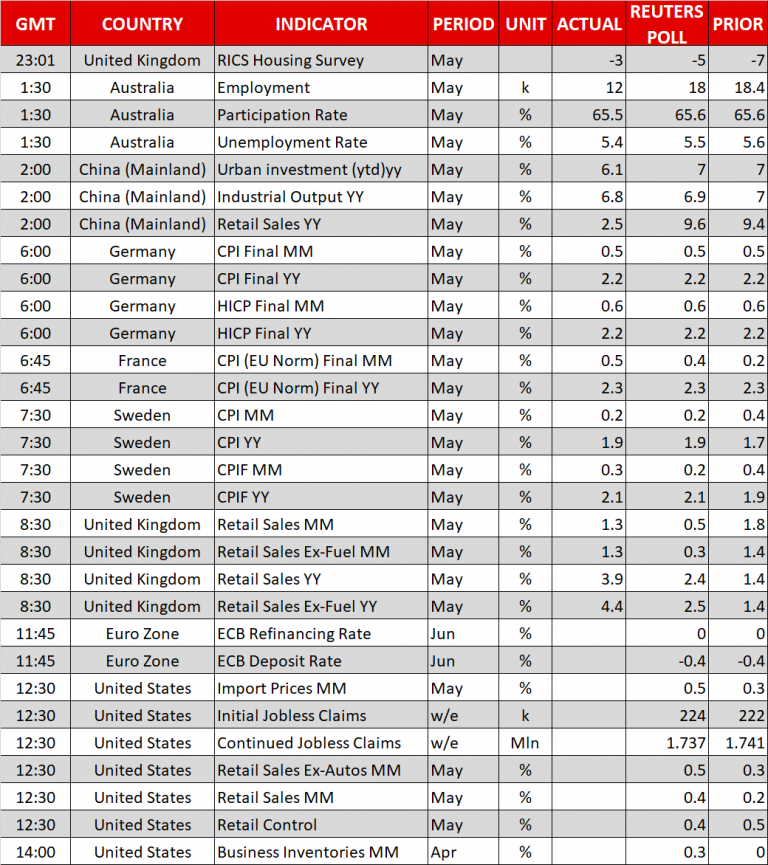

A policy meeting by the European Central Bank will take the center stage later on Thursday before a stream of data come out of the US, while trade and geopolitical headlines will remain in focus.

At 1145 GMT, ECB policymakers will conclude their two-day gathering, but no rate hikes are expected to be announced, with investors turning attention to the forward guidance in the rate statement and the press conference scheduled to start at 1230 GMT. Particularly investors will be eager to hear whether the ECB is ready to end its bond-buying program in December or whether it thinks is necessary to expand QE beyond the anticipated deadline. If the ECB chairman, Mario Draghi, flags the termination of the program by year-end then the euro could drift higher to fresh highs, though probably by not much as the news is almost priced into the markets. Otherwise, a more cautious tone, expressing the need to increase the duration of the QE, could pressure the common currency.

No change in interest rates is also widely expected in Japan early on Friday at a tentative time, where the Bank of Japan is anticipated to stand pat on its monetary strategy. In this case traders will take a look at the rate statement and the BoJ’s chief, Haruhiko Kuroda’s press conference to identify whether policymakers have changed their views on the country’s economic status after inflation, which is not even halfway of the BoJ’s target, continued its downtrend in May and GDP growth remained in negative territory in Q1 (second estimates). Specifically, it would be interesting to see what Kuroda has to say about the path of inflation after he decided to remove from the quarterly projections report the sentence referring to the timeline inflation could reach the BoJ’s target of 2.0%. Note that the central bank will not renew its economic forecasts at Friday’s meeting.

Meanwhile in the US, a number of economic releases are expected to keep investors busy at 1230 GMT. The Census Bureau is expected to show that US retail sales have marginally improved in May, posting a growth of 0.4% month-on-month compared to a rise of 0.2% in April. The expansion, however, is projected to be larger in the absence of the volatile automobiles, seen at 0.5% m/m versus 0.3% in the preceding month. Initial jobless claims for the week ending June 8 are forecasted to inch up as well, while May’s import prices are projected to support stronger inflationary pressures on a monthly basis.

In Beijing, the trade battle with the US is still open as Chinese officials wait for Washington to announce on Friday its final list of Chinese products subject to a 25% import tariff on $50 billion of goods.

The North Korean story will be under the spotlight as well. After the symbolic summit between the US President Donald Trump and the North Korean leader, Kim Jong Un spread hopes of peace between the two countries and the complete denuclearization of the North Korean peninsula, negotiating teams from both sides will continue talks to achieve these goals. Yesterday, the US Secretary of State, Mike Pompeo who met its South Korean and Japanese counterparts in Seoul said that the US will not abandon its sanctions against North Korea until it sees a complete denuclearization of the isolated region.

ECB to taper APP to EUR 15B/M after Sep, end it after Dec. Full statement

ECB left main refinancing rate unchanged at 0.00% as widely expected. Regarding the asset purchase program, ECB decided to taper it from EUR 30B per month to EUR 15B per month after the end of September. And, the program will end after December 2018.

Press conference to start at 12:30GMT

https://www.youtube.com/watch?v=hBJw3y2i1-s

Full statement below.

Monetary Policy Decisions

At today's meeting, which was held in Riga, the Governing Council of the ECB undertook a careful review of the progress towards a sustained adjustment in the path of inflation, also taking into account the latest Eurosystem staff macroeconomic projections, measures of price and wage pressures, and uncertainties surrounding the inflation outlook.

Based on this review the Governing Council made the following decisions:

First, as regards non-standard monetary policy measures, the Governing Council will continue to make net purchases under the asset purchase programme (APP) at the current monthly pace of €30 billion until the end of September 2018. The Governing Council anticipates that, after September 2018, subject to incoming data confirming the Governing Council's medium-term inflation outlook, the monthly pace of the net asset purchases will be reduced to €15 billion until the end of December 2018 and that net purchases will then end.

Second, the Governing Council intends to maintain its policy of reinvesting the principal payments from maturing securities purchased under the APP for an extended period of time after the end of the net asset purchases, and in any case for as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation.

Third, the Governing Council decided that the interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility will remain unchanged at 0.00%, 0.25% and -0.40% respectively. The Governing Council expects the key ECB interest rates to remain at their present levels at least through the summer of 2019 and in any case for as long as necessary to ensure that the evolution of inflation remains aligned with the current expectations of a sustained adjustment path.

Today's monetary policy decisions maintain the current ample degree of monetary accommodation that will ensure the continued sustained convergence of inflation towards levels that are below, but close to, 2% over the medium term.

The President of the ECB will comment on the considerations underlying these decisions at a press conference starting at 14:30 CET today.

(ECB) Monetary Policy Decisions

At today's meeting, which was held in Riga, the Governing Council of the ECB undertook a careful review of the progress towards a sustained adjustment in the path of inflation, also taking into account the latest Eurosystem staff macroeconomic projections, measures of price and wage pressures, and uncertainties surrounding the inflation outlook.

Based on this review the Governing Council made the following decisions:

First, as regards non-standard monetary policy measures, the Governing Council will continue to make net purchases under the asset purchase programme (APP) at the current monthly pace of €30 billion until the end of September 2018. The Governing Council anticipates that, after September 2018, subject to incoming data confirming the Governing Council's medium-term inflation outlook, the monthly pace of the net asset purchases will be reduced to €15 billion until the end of December 2018 and that net purchases will then end.

Second, the Governing Council intends to maintain its policy of reinvesting the principal payments from maturing securities purchased under the APP for an extended period of time after the end of the net asset purchases, and in any case for as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation.

Third, the Governing Council decided that the interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility will remain unchanged at 0.00%, 0.25% and -0.40% respectively. The Governing Council expects the key ECB interest rates to remain at their present levels at least through the summer of 2019 and in any case for as long as necessary to ensure that the evolution of inflation remains aligned with the current expectations of a sustained adjustment path.

Today's monetary policy decisions maintain the current ample degree of monetary accommodation that will ensure the continued sustained convergence of inflation towards levels that are below, but close to, 2% over the medium term.

The President of the ECB will comment on the considerations underlying these decisions at a press conference starting at 14:30 CET today.

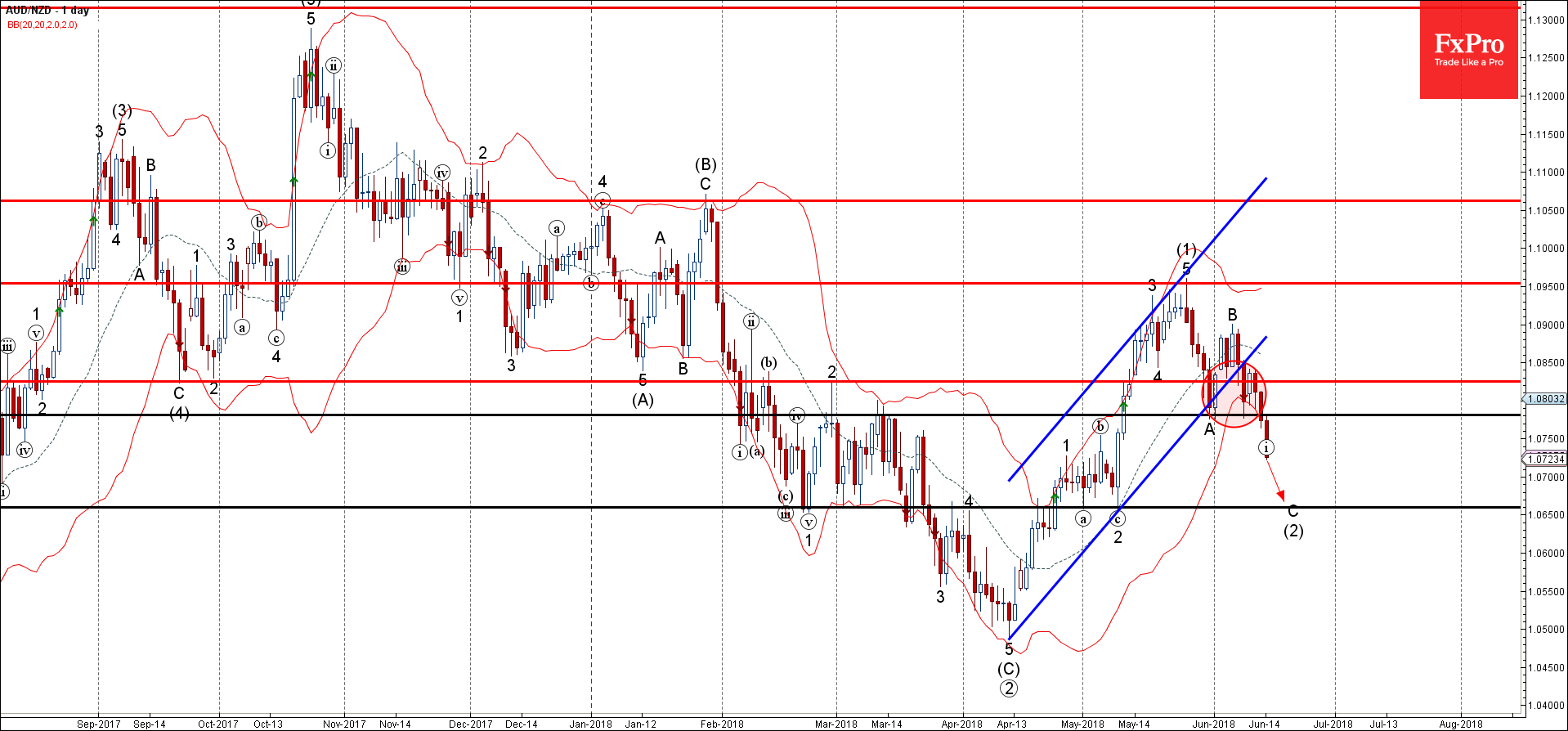

Forex Analysis: AUDNZD Wave Analysis

AUDNZD broke support area

Likely to fall further

AUDNZD recently broke through the support area lying between key support level 1.0780 (which stopped the A-wave of the active ABC correction (2) from May) and the support trendline of the daily up channel from April (which has enclosed the previous medium-term impulse wave (1)).

The breakout of this support area accelerated the active short-term impulse wave C – which belongs to the medium-term ABC correction (2) from last month.

AUDNZD is likely to fall further and re-test the next support level 1.0660 (low of previous waves (a) and 2 and the target for the completion of wave (2)).